World Bank Document€¦ · World Bank team including Dung Thi Ngoc Tran on editing, Chi Kim Tran...

182

47023 Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of World Bank Document€¦ · World Bank team including Dung Thi Ngoc Tran on editing, Chi Kim Tran...

47023P

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

ed

Vietnam Development Report 2009

Capital Matters

World Bank Report to the Vietnam Consultative Group MeetingHanoi, December 4-5, 2008

47023

CURRENCY EQUIVALENTS

CURRENCY UNIT = DONGUS$ = 16,500

GOVERNMENT FISCAL YEARJanuary 1 to December 31

ACRONYMS AND ABBREVIATIONS

ACB Asia Commercial BankADB Asian Development BankAFTA ASEAN Free Trade AreaBIDV Bank for Investment and Development of VietnamBOT Build-Operate-TransferBTO Build-Transfer-OperateCDS Credit Default SwapDAD Development Assistance DatabaseDFID Department for International Development of the United KingdomDRG Diagnostic Related GroupDRS Debtor Reporting SystemEC European CommissionEximbank Vietnam Import Export BankEIT Enterprise Income TaxEVN Electricity of VietnamFDI Foreign Direct InvestmentGAC Governance and Anti-corruptionGDP Gross Domestic Product GDT General Department of TaxationGNI Gross National IncomeGSO General Statistics OfficeHaSTC Hanoi Stock Trading CenterHCMC Ho Chi Minh CityHIFU Ho Chi Minh City Investment Fund for Urban DevelopmentHOSE Ho Chi Minh City Stock ExchangeHSBC Hong Kong and Shanghai Banking CorporationIBRD International Bank for Reconstruction and DevelopmentICOR Incremental Capital-Output RatioIDA International Development AgencyIFC International Finance CorporationIMF International Monetary FundIPO Initial Public OfferingIT Information TechnologyJICA Japan International Cooperation AgencyJSB Joint Stock BankJSC Joint Stock CompanyLDIF Local Development Investment Fund

MHB Mekong Housing BankMOF Ministry of Finance MPI Ministry of Planning and InvestmentMTEF Medium-Term Expenditure FrameworkNDF Non-Deliverable ForwardNGO Non-Governmental OrganizationNPL Non-Performing LoanNPV Net Present ValueOCBC Overseas Chinese Banking CorporationOECD Organization for Economic Co-operation and DevelopmentOTC Over-the-Counter P/E Price-to-Earnings PIT Personal Income TaxPPP Purchasing Power ParityPPP Public Private PartnershipsPRSC Poverty Reduction Support CreditSacombank Sai Gon Thuong Tin Commercial Joint Stock BankSAE Small-Area EstimatesSASAC State-owned Assets Supervision and Administration CommissionSBV State Bank of VietnamSCIC State Capital Investment CorporationSEDP Socio-Economic Development PlanSMBC Sumitomo Mitsui Banking CorporationSOCB State-Owned Commercial BankSOE State-Owned EnterpriseSRO Self-Regulatory OrganizationSSC State Securities CommissionSSI Saigon Securities Inc.Techcombank Vietnam Technology and Commercial Joint Stock BankUNCTAD United Nations Conference on Trade and DevelopmentUSBTA US-Vietnam Bilateral Trade AgreementVAT Value Added TaxVBARD Vietnam Bank for Agriculture and Rural DevelopmentVBSP Vietnam Bank for Social PoliciesVDB Vietnam Development BankVietcombank Vietnam Foreign Commercial Joint Stock BankVietinbank Vietnam Bank for Industry and TradeVMBA Vietnam Bond Market AssociationVSD Vietnam Securities DepositoryVSS Vietnam Social InsuranceVPBank Vietnam Commercial Bank for Private EnterprisesVPSSC Vietnam Postal Savings Service CompanyWTO World Trade Organization

ACKNOWLEDGMENTS

This report was prepared by the World Bank for the Consultative Group meeting ofDecember 4-5, 2008. The outline and content of the report were discussed with donors, bothvirtually and at a workshop held in Hanoi on March 28. Comments and suggestions by LaurieBarnier (European Commission, EC), Bridget Crumpton (Department for InternationalDevelopment of the United Kingdom, DFID), Elke Foerster (on behalf of the Like-MindedDonor Group), Bahodir Ganiev (Asian Development Bank), Daniel Lenggenhager (SwissDevelopment Cooperation), Yasuhisa Ojima (Japan International Cooperation Agency, JICA)and Huong Thuy Vu (Embassy of Ireland) are gratefully acknowledged. The report alsobuilds on various studies conducted or funded by donors in areas related to the content of thereport over the months and years preceding its writing. Such studies, listed in thebibliography section, were prepared as part of each donor’s own country program.

The preparation of the report involved consultations with Vietnamese researchers andpractitioners who participated on a personal capacity. Their inputs and feedback werecoordinated through a Reviewing Committee comprising Mr. Ha Bui (Ministry of Planningand Investment), Dr. Doanh Dang Le (Institute of Development Studies), Mr. Nghia Xuan Le(State Bank of Vietnam), Mme. Tam Thi Bang Le (advisor), Mme. Cuc Thi Nguyen (GeneralDepartment of Taxation), Mr. Do Thanh Nguyen (Ministry of Finance), Mr. Huy QuangNguyen (State Bank of Vietnam), Mme. Yen Thi Hoang Nguyen (Ministry of Finance), Mme.Lan Chi Pham (Institute of Development Studies), Dr. Thanh Tri Vo (Central Institute forEconomic Management), and Mr. Bang Vu (State Securities Commission).

The team in charge of formally writing the report was led by Martin Rama. Viet Tuan Dinhand Keiko Kubota contributed to the entire report. Noritaka Akamatsu, James Anderson,Quang Hong Doan, Tuan Minh Le, Lasse Melgaard, Dzung The Nguyen, Nga NguyetNguyen, Duc Minh Pham, Kalpana Seethepalli, Susan Shen, Viet Quoc Trieu and QuyenHoang Vu contributed inputs for specific chapters. The writing team built on a range ofstudies prepared by colleagues in the World Bank. It also benefited from substantivecontributions by partners outside the World Bank. Special thanks go to Daniel Alvarez (DukeUniversity), Michael Engelschalk (consultant), Cuong Viet Nguyen (National EconomicsUniversity), GP Shukla (Duke University), and Roy Van Der Weide (consultant).

Nha Thi Vu (Vietnam Development Information Center - VDIC) was in charge ofbibliographical research and referencing. The processing of the document was done by aWorld Bank team including Dung Thi Ngoc Tran on editing, Chi Kim Tran on publishing, andPhuong Minh Le on administrative Supoort.

Overall guidance was provided by Vikram Nehru, from the World Bank. Homi Kharas(Brookings Institution) and Luiz Pereira Da Silva (World Bank) served as peer reviewers.The report was discussed with the International Monetary Fund (IMF). Comments andsuggestions by numerous colleagues are gratefully acknowledged.

g

TABLE OF CONTENTS

AcknowledgementsExecutive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .i

PART I: NEEDS AND IMPACTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11. Financing Growth . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .32. Transformation and Turbulence . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .16

PART II: SOURCES AND USES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .273. Tax Revenue . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .294. Debt and Liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .415. State Capital . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .526. Policy Lending . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .647. Banking Credit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .718. Equity Investment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .849. Private Partnerships . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9310. Donor Support . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .102

PART III: A POLICY AGENDA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11411. Ensuring Stability . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11712. Sustaining Growth . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .128

Bibliography . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .136Statistical Appendix . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .139

Boxes

Box 1.1: What Does an ICOR Tell about Efficiency? ......................................................7Box 2.1: How many Years to Catch Up? ........................................................................23Box 3.1: The Tax Reform Program ................................................................................32Box 3.2: Land Administration Reform and Property Tax................................................36Box 4.1: Defining Government Debt ..............................................................................42Box 5.1: Equitization Methods: Competition versus Direct Sale ....................................60Box 5.2: China’s Approach to the Management of State Ownership Rights ..................63Box 6.1: Microcredit in Cambodia and Vietnam ............................................................70

h

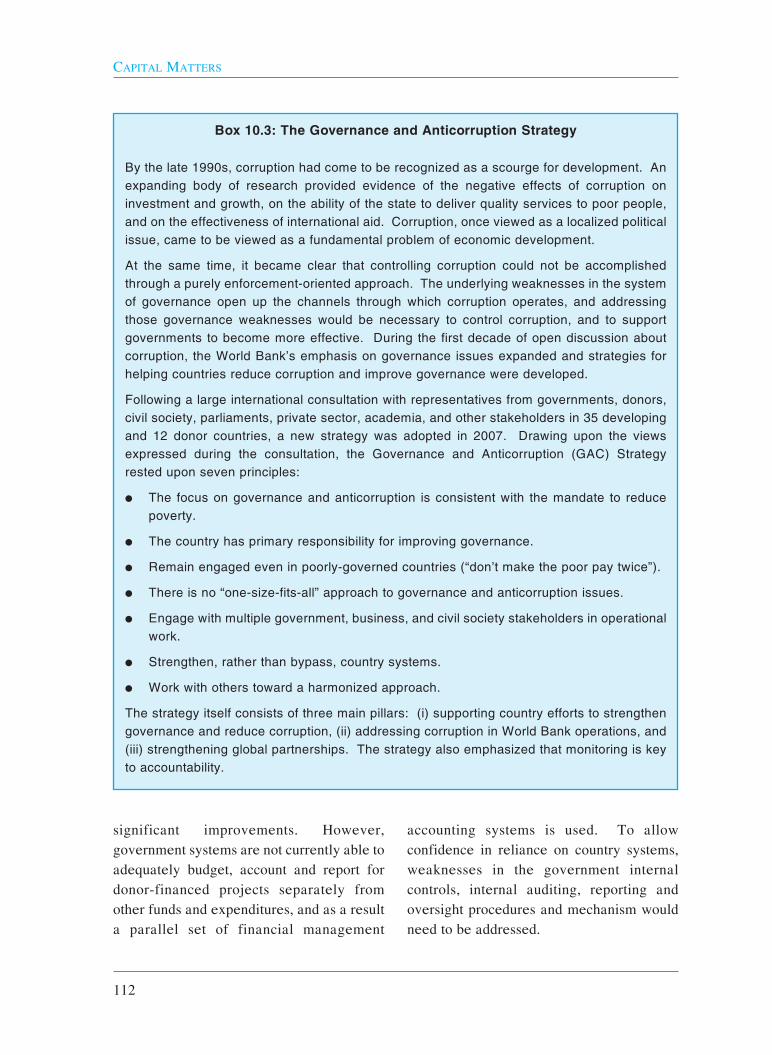

Box 7.1: Strategic Investments in the Banking Sector ....................................................75Box 7.2: Assessing the Quality of Bank Lending............................................................82Box 8.1: A Combination of Temasek and Treuhand ......................................................89Box 8.2: Does Listing Improve Performance? ................................................................91Box 9.1. PPP Schemes and Modalities ............................................................................94Box 9.2: Successes and Failures in the Granting of Guarantees ....................................98Box 9.3: Local Development Investment Funds............................................................100Box 10.1: Aid Fungibility in the Transport and Health Sectors ......................................106Box 10.2: China’s Graduation from Concessional Lending ............................................110Box 10.3: The Governance and Anticorruption Strategy ................................................112Box 11.1: Systemic Risk in East Asian Economic Crises ..............................................120Box 11.2: Identifying Poor and Vulnerable Households ................................................127

Tables

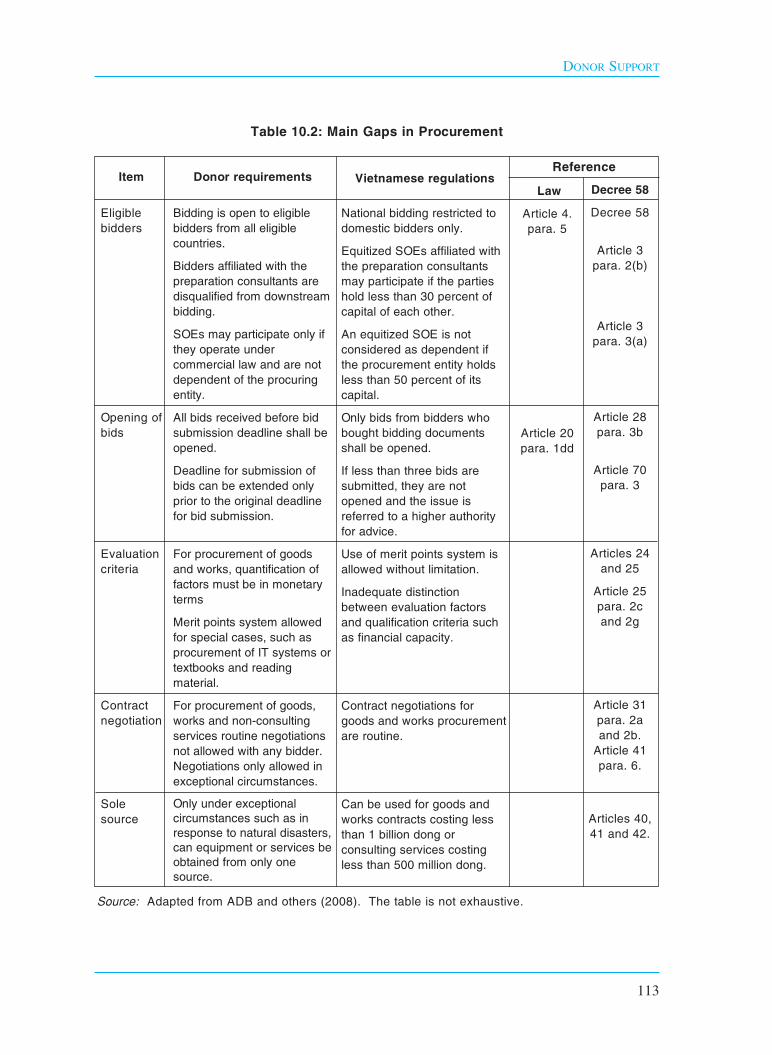

Table 1.1: Total Investment at Current Prices ....................................................................4Table 1.2: The Engineering Approach to Investment ..........................................................9Table 1.3: The Financial Approach to Investment ............................................................12Table 3.1: Composition of Government Revenue..............................................................30Table 3.2: The Revenue Gap on EIT ................................................................................33Table 3.3: Partial Tax Filing Compliance ..........................................................................39Table 4.1: Debt Issuance by SOCBs and Large SOEs ......................................................50Table 5.1: Public Investments by Sector of Activity ..........................................................55Table 6.1: Beneficiaries from Social Policy Lending ........................................................66Table 7.1: Financial Investments by Large SOEs ..............................................................76Table 7.2: Key Financial Ratios for SOCBs ......................................................................78Table 7.3: Key Financial Ratios for JSBs ..........................................................................79Table 8.1: Joint Stock Companies: Public versus Listed....................................................87Table 10.1: What are the Main Priorities? ........................................................................109Table 10.2: Main Gaps in Procurement..............................................................................113

Figures

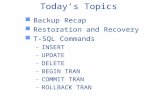

Figure 1.1: Key Investment Ratios ........................................................................................5Figure 1.2: The Incremental Capital-Output Ratio................................................................8Figure 1.3: The Economic Approach to Investment ............................................................10Figure 1.4: A Robust External Debt Position ......................................................................15Figure 2.1: Richer Countries Are more Expensive ............................................................18Figure 2.2: Richer Provinces Are more Expensive ............................................................20

i

Figure 2.3: A Changing Balance of Payments ....................................................................21Figure 2.4: The Rise and Fall of Real Estate Prices ..........................................................22Figure 2.5: The Real Exchange Rate and Export Performance ..........................................24Figure 3.1: A Progressive Tax Burden ................................................................................33Figure 3.2: Gaps in Operational Processes..........................................................................40Figure 4.1: A Multiplicity of Small Bond Series ................................................................44Figure 4.3: Will Future Pensions Be Affordable? ..............................................................48Figure 5.1: Funding Sources for Public Investments ..........................................................54Figure 5.2: Rate of Return on Assets by Enterprise Ownership..........................................58Figure 6.1: Is Social Policy Lending Well Targeted?..........................................................67Figure 6.2: One among Several Sources of Finance ..........................................................69Figure 7.1: Financial Deepening or Monetary Turbulence? ..............................................73Figure 7.2: How Much Borrowing by SOEs? ......................................................................80Figure 8.1: Stock Market Trends and Fundamentals ..........................................................85Figure 9.1: The Gap between Investment Plans and Available Financing ........................95Figure 10.1: Donor Support Looking Backward..................................................................103Figure 10.2: Donor Support Looking Forward ....................................................................108Figure 11.1: Dramatic Fluctuations in Commodity Prices ..................................................118Figure 11.2: Good policies are not enough..........................................................................124

Now, more than ever, it matters howVietnam raises and uses capital.

In 2007 the world experienced unprecedentedeconomic growth. There was abundantcapital seeking profitable investments inemerging countries, and country riskpremiums were low. Vietnam’s accession tothe World Trade Organization (WTO) wasinterpreted as a sign that its government wasserious about economic reform. Given itshardworking population and excellentlocation, market sentiment was strong. Manysaw Vietnam as a new economic tiger in themaking, the “+1” country in a “China+1”investment strategy. Resources flowed inunder many forms, from remittances toforeign direct investment (FDI) to portfolioinvestments. Capital inflows were four timeshigher relative to GDP than anything Chinahad experienced since the beginning of itsown reform process.

In 2008 the world economy went into a tailspin. What started as financial difficulties ina risky segment of the mortgage market inthe United States grew into a global financialcrisis of unprecedented proportions. Fearparalyzed economic activity, bringing creditto a halt and pushing many who had investedin emerging countries to sell their assets toraise liquidity.

What the next few years will bring isuncertain. What is certain, however, is that

2009 will be a difficult year. The downturnin industrial countries will lead to a declinein developing country exports. FDI projectsunder implementation may be delayed, orcancelled altogether. New FDI will decline,perhaps dramatically. Portfolio investmentwill become rare and even remittances couldsuffer, as those who send money home maysee their jobs disappear and their earningsdwindle. In the year 2009, mobilizingcapital for development will be very difficultindeed. Using it efficiently will beimperative.

* * *

Vietnam’s balance of payments offers boththe prospect of faster growth and the risk ofgreater turbulence. In late 2007, theabundance of capital inflows created strongpressure for the dong to appreciate,affecting export competitiveness. Resistingthat pressure meant injecting massiveamounts of liquidity into the economy. Theresult was a boom in banking credit, risinginflation, and an asset price bubble. In late2008 and early 2009, export growth is boundto slow, capital inflows will decline, and theinvestment rate will fall. As economicactivity slows and jobs are lost, real incomegrowth will weaken, and the poor are likelyto suffer the most.

The shifts in market sentiment that driveexternal capital flows are one of the main

i

EXECUTIVE SUMMARY

risks faced by the Vietnamese economy. Butthe package of macroeconomic policies atpresent available to the government may beinsufficient to mitigate the impact of thoseshifts. Another risk stems the possibility forenterprises and banks, both state-owned andprivate, to contract more debt than theyshould, running up implicit claims on thegovernment. This risk has not materializedyet, and current circumstances make itunlikely in the short term. But in afinancially open economy, this is more thanjust a theoretical possibility.

Disengagement from world markets is notthe answer, however. Global integration hasbeen the country’s ticket to prosperity.Linking domestic prices to internationalmarkets allowed farmers to get better returnsfor their products and emerge from poverty.FDI inflows resulted in the creation of wageemployment, making it possible for Vietnamto absorb millions of entrants into its labormarket. Exports have been the main driverof economic growth, as domestic enterprisesconnected increasingly to internationalmarkets. Opening the services sector to newentry brought competition into activitiespreviously dominated by large state-ownedenterprises (SOEs) and state-ownedcommercial banks (SOCBs), resulting insubstantial efficiency gains.

As Vietnam reaches middle-income status itwill need to engage more deeply withprivate capital markets, including the globalfinancial market. Without this, Vietnam’sinvestment rate will be constrained by itsdomestic savings rate, which hovers around30 percent of GDP. That may be high byinternational standards, but it is not highenough to support Vietnam’s ambition tobecome an industrial country in one

generation. To bridge the difference andrealize this ambition, Vietnam will have toembrace international capital, but with anadequate policy and institutional framework.

Global integration may hold the key toprosperity, but it also confronts the countrywith new challenges, especially in the areaof economic management. Financial crisesare a hazard of life in middle-incomecountries. Such crises can be costly,economically and socially, and set backeconomic growth. When capital marketconditions change and lenders stop providingfinance, long-gestation projects can be leftincomplete, new ones are not constructed,real wages and asset prices fall, and the realexchange rate depreciates, spreadingturmoil through the rest of the economy.

Managing risk requires decisive policyaction. Limited reliance on short-term debtand a safe level of international reserves arecritical, but may not be sufficient. Alsoneeded are appropriate monetary policy, asound banking system with the capacity toassess credit risks well, and solid financialsector supervision.

* * *

To ensure stability, Vietnam will need toreconcile its financing needs with a prudentreliance on foreign capital. A sudden surgein inflows as occurred in 2007 can lead toexchange rate appreciation, makingborrowing in foreign currency moreattractive and encouraging further short-term inflows. A flexible exchange rate canhelp deal with such a situation, andVietnam’s move in this direction iswelcome. But excessive exchange ratevariability can also hurt export

CAPITAL MATTERS

ii

competitiveness and the business climateand affect balance sheets in enterprises andbanks. Exchange rate flexibility may alsoaccentuate instability in the presence oflarge short-term capital inflows or outflows.

Given these constraints, exchange ratepolicy alone will not be sufficient.Reconciling financing needs withmacroeconomic stability will require a morecomprehenive policy framework across allthe major policy instruments: exchange ratepolicy, monetary policy, and fiscal policy.But for this framework to be effective, allthree instruments will need to be brought upto speed, and the coordination between themwill have to be improved.

Monetary policy can be effective in theabsence of short-term capital movements, ashad been the case until 2006. But monetarypolicy became less independent in thepresence of large capital movements, as inlate 2007 and early 2008, when theauthorities basically lost control of creditgrowth and could not prevent significantdemand pressures in the economy, resultingin rising inflation, a current account deficit,and asset price bubbles.

Effective fiscal policy requires goodinformation on government revenue andexpenditures, and strong control over publicinvestments. Vietnam faces shortcomings inall three fronts. Its measure of the budgetbalance differs from standard internationalpractice. The treatment of amortization, off-budget accounts, and revenue carry-overssubstantially distort the budget position of thegovernment. Information is particularlyweak for budget-funded investment projects,which account for 30 percent of total capitalaccumulation in Vietnam. Just as it did in late

2007 and early 2008 in responding tooverheating, the government should moresystematically stop or delay projects withweak justification, insufficient funding orpoor performance.

* * *

Investing efficiently should be a top priorityof the government, regardless of the level ofcapital inflows. Capital efficiency isprobably low, and may have deteriorated inlate 2007 and 2008. During this period,state-owned Economic Groups and largeState corporations relied on their deeppockets to diversify into sectors far removedfrom their core business, such as real estate,financial investments and the establishmentof new banks. Real estate investments mighthave looked highly profitable as long as theasset price bubble was growing, but theiractual returns were punctured when thebubble burst.

Economic Groups and large corporationsinvesting in finance pose a potential threat tomacroeconomic stability. Efforts to reformthe state sector in Vietnam have relied onincreased competition and harder budgetconstraints. If Economic Groups and largeState corporations can raise funds directlyfrom the public through deposit takinginstitutions, scrutiny over the bankability oftheir investment projects will inevitablydeteriorate. Poor investment decisions couldbe pursued for longer than they should.Fortunately, in Vietnam the asset pricebubble was short-lived, so that many of theseinvestments did not have time to materialize.But looking forward this is an area wherecaution is warranted.

The usual evidence provided to claim thatinvestment efficiency is low in Vietnam is its

EXECUTIVE SUMMARY

iii

growing Incremental Capital-Output Ratio(ICOR). But this can be misleading. In 2007,for example, the most dramatic increase hasbeen for the foreign-invested sector, notbecause it is the most inefficient, butbecause it has grown the fastest.

Since ICORs are not necessarily helpful inassessing Vietnam’s investment efficiency,this report analyzes in some depth howfinancial resources are raised, allocated andchanneled to specific projects. The approachexamines the sources and uses of funds,quantifies the gaps between investment andsavings for each of the main economicagents, and highlights the mechanismsthrough which the agents that save channelresources to those that invest. The reportthen explores in more detail the efficiency ofeach of these mechanisms, including theraising of tax revenues by government, theissuance of debt, the allocation of resourcesthrough the budget, the targeting of socialpolicy lending, the mobilization of bankingcredit, the raising of equity finance, theparticipation of the private sector ininfrastructure projects, and the mobilizationof donor support.

* * *

The main challenges revealed by thisanalysis are the shortage of long-termfinance and the institutional constraints todevelop private-public partnerships ininfrastructure. Investment projects withpotentially high returns may never beimplemented due to the lack of funding. Thebond market is still thin, and will probablyremain that way unless there is moreprogress in consolidating the large numberof outstanding series of government bondsand bills, thus supporting the emergence of a

reliable yield curve. The main obstacle toprivate-public partnerships is the absence ofa specialized agency with the capacity tofoster competition and with the ability toidentify the financial support needed wherethere is a perceived funding gap.

Other sources of investment finance arefunctioning better, but improvements arepossible in their case too. For example,much progress has been made in relation tothe tax system. But the lack of a genuineproperty tax and the variability of theeffective tax burden across enterprises withdifferent ownership suggest that more couldbe done to improve efficiency and equity. Inthe banking system, there is need forstronger credit risk rating to rapidly identifyborrowers under stress and weak loanportfolios. In the stock market severalimprovements can be made at the level ofthe trading platforms. In the medium term,its dynamism would be boosted by a faster(but still transparent) equitization of largeSOEs and SOCBs.

The selection of public investment projectsand their implementation are two areaswhere large improvements can be made inthe use of public resources. Decentralizationhas brought key decisions closer tobeneficiaries, and this should in principleimprove project selection. But it has also ledto weaker project appraisal andimplementation processes. Cost-benefitanalyses are not always undertaken, and themonitoring of project execution is not strongenough to avoid substantial delays and costoverruns. A Law on Public Investment isneeded to identify the steps that lineministries and local governments need totake to prepare, appraise and implementprojects. The Ministry of Planning and

CAPITAL MATTERS

iv

Investment (MPI) also needs the capacity toreview feasibility studies and monitorimplementation. The Law should alsoprovide clarity on the powers of the centralgovernment to suspend or stop investmentprojects, especially because the ability toadjust investment volumes rapidly may holdthe key to macroeconomic stability in anincreasingly uncertain world.

* * *

Vietnam has made important progress inestablishing well-functioning capital markets

as the infrastructure to ensure itsindustrialization and modernization. But ithas not fully succeeded yet. Investmentrates have been high. But domestic savingshave not always being mobilized efficiently,and foreign savings cannot always be reliedupon. Meanwhile, investment decisions donot always channel resources to the rightsectors and activities. And some of themcould increase the vulnerability of theVietnamese economy to shifts in marketsentiment. In this context, the system formobilizing and using capital matters.

EXECUTIVE SUMMARY

v

PART I: NEEDS AND

IMPACTS

1

Vietnam has been one of the fastest growingcountries in the world, with rapid outputgains being sustained (among others) onmassive capital accumulation. Reassuringly,the share of investments undertaken by theprivate sector, and especially by thedomestic private sector, has grown steadily.By now, the state sector accounts for roughly40 percent of the total, compared to 60percent at the beginning of the decade. Butwith the investment rate exceeding 45percent of the Gross Domestic Product(GDP) in 2007, questions remain regardingthe efficiency and the affordability of thismassive accumulation effort. Attempts toassess the efficiency of investment have sofar relied on macroeconomic data, which isquestionable on methodological grounds andleads to non-conclusive results anyway. Onthe other hand, some macroeconomicanalyses are well suited to assess theaffordability of the accumulation effort. Theengineering approach to investment “needs”does not fall in this category, as it tends tofocus on a few (mainly infrastructure)sectors, assuming that all master plans haveto be implemented and all governmenttargets attained. Moreover, the engineeringapproach remains silent on who (of theprivate sector of the state) should undertakethe investments. But the economic approachgives a sense of magnitude of the investmenteffort needed to attain different growth

targets, and shows how large the currentaccount deficit of the balance of paymentscan be when those targets are ambitious.And the financial approach highlights howthe main stakeholders raise and channelresources for investments of various sorts.An assessment of debt sustainabilitysuggests that Vietnam can afford a relativelyhigh level of capital accumulation. But arigorous analysis of the efficiency of capitalaccumulation in Vietnam needs to dig intoeach of the main sources and uses of fundsidentified by the financial approach.

Massive accumulation

Over the present decade, and especiallyafter the acceleration of economic reformsthat followed the 9th Party Congress, in2001, Vietnam has experienced high ratesof economic growth. Its GDP per person,measured at constant prices, increased onaverage by 6.5 percent per year.Admittedly, China has grown faster, ashave also done a few other countries(many of them small, relying on naturalresource booms or emerging fromconflict). But when the period 2001-2007as a whole is considered, Vietnam ranks24 among 139 countries in terms of thegrowth of its GDP per person measured atconstant prices (the ranking excludescountries and territories with a GDP of lessthan 2 billion dollars in 2007).

3

1. FINANCING GROWTH

Another common way to measure progress isin current dollar terms. From thisperspective, Vietnam climbed from a GDPper person of 413 dollars in 2001 to 836 in2007, and will most likely surpass the 1000milestone in 2008, a couple of years ahead ofthe target set by the Socio-EconomicDevelopment Plan (SEDP) 2006-2010. At12.5 percent, the annual growth rate of GDPper person over the period 2001-2007 ismuch higher than when measured at constantprices. This is not surprising, given thegradual loss in the value of the dollar.Figures measured in current dollars are alsomore subject to fluctuations due to short-termmovements in exchange rates.

However, there is more than inflation andshort-term turbulence in the gap betweenmeasures at constant prices and in currentdollar terms, and the implications will bediscussed recurrently in this report. Beyondwhich GDP measure is used, it is clear thatVietnam has grown fast. Such rapid growthhas been one of the main drivers of povertyreduction, another area where Vietnam hasdone remarkably well, regardless of themeasure used.

Rapid economic growth has been partlysustained on massive capital accumulation

(Table 1.1). By 2007, Vietnam wasinvesting 521.7 trillion dong per year, almostexactly three times as much as in 2001, wheneconomic reforms accelerated. Only afraction of this increase can be attributed tocapital goods being more expensive.

The growth in investment has been faster inthe private sector than in the state sector,with the strongest performance (both inabsolute and in relative terms)corresponding to the domestic private sector.As a result, the fraction of total investmentcontributed by different stakeholders haschanged dramatically since the accelerationof economic reforms. In 2001, the statesector accounted for almost 60 percent oftotal capital accumulation in Vietnam, withthe rest divided roughly equally betweenforeign invested companies and thedomestic private sector. By 2007, it was theprivate sector which accounted for 60percent, with more than half of the amountcontributed by domestic enterprises (Figure1.1, left panel).

Investment has grown much faster thanGDP. The share of total output dedicated togross capital accumulation has increasedfrom 35.4 percent in 2001 to an astounding45.6 percent in 2007 (Figure 1.1, right

CAPITAL MATTERS

4

Table 1.1: Total Investment at Current Prices

2001 2002 2003 2004 2005 2006 2007e 2008p

State 102.0 114.7 126.6 139.8 161.6 185.1 208.1 236.0

Private domestic 38.5 50.6 74.4 109.8 130.4 154.6 184.3 190.0

Foreign 30.0 34.8 38.3 41.3 51.1 65.6 129.3 153.0

Total 170.5 200.1 239.2 290.9 343.1 404.7 521.7 579.0

Source: General Statistics Office (GSO). Figures are in trillion dong. The state sector includesSOEs.

panel). Not all of this effort translates intonet capital accumulation, as some of theinvestment simply compensates thedepreciation of existing capital. Based onnational accounts, over the period 2001-2007, capital depreciation has accounted forroughly 4.5 percent of GDP, measured atcurrent prices. But regardless of whichmeasure of capital accumulation isconsidered, it is clear that Vietnam currentlyhas one of the highest investment ratios inthe world. For instance, on the grossaccumulation measure only 12 out of the 139countries considered had a higher ratio thanVietnam in 2007.

Efficient accumulation?

When a country is devoting such a massiveamount of resources to capital accumulation,an obvious question is whether thoseresources are being invested efficiently.There is evidence, from studies usingindividual records from the enterprise surveyof GSO that total factor productivity at theenterprise level is increasing rapidly. This

means that not all economic growth inVietnam comes from increases in the volumeof capital or the size of labor force. Butregardless of the magnitude of total factorproductivity gains, the question is whetherthe additional capital is being allocated to the“right” sectors, activities, and projects.

Because market mechanisms are still beingdeveloped in Vietnam, and publicinvestment processes are only partiallymodernized, this is not just a hypotheticalconcern. Much of the economic policydebate in recent years, and especiallyaround the 10th Party Congress, in 2006, wason the distinction between “quantity” and“quality” of growth. By now there is nodoubt that Vietnam is delivering on the“quantity” dimension. Whether it does so onthe “quality” dimension is much less clear.

However, providing an answer to thisquestion is less straightforward than manycommentators suggest. The usualcommentary uses the ICOR as proof. On thesurface, this is a sensible approach. The

FINANCING GROWTH

5

0

10

20

30

40

50

60

70

2001

2002

2003

2004

2005

2006

2007

e

Perc

ento

ftot

alin

vestm

ent

State Non-state Foreign

0

10

20

30

40

50

2001

2002

2003

2004

2005

2006

2007

e

Perc

ento

fGD

P

Total investment

Figure 1.1: Key Investment Ratios

Source: Based on data from GSO.

ICOR measures how many units of capitalare associated with every additional unit ofoutput. So, in principle at least, the higherthe ICOR the less efficient investment is(because more units of capital are needed togenerate one additional unit of output).

A cursory look at the date suggests that theICOR has indeed increased substantially inVietnam in recent years. Using the standardmeasure, at constant prices, it went from 4.5in 2001 to 6.6 in 2007. Some increase in theICOR can be expected as the capital stock ofthe economy expands and the most urgentgaps are addressed. The first, criticallyimportant investments in basic infrastructureshould do more to expand GDP thansubsequent projects with lower priority. Buta 48 percent increase in just six years seemstoo high to be due to the mere effect of arelative abundance of capital; especiallybecause infrastructure gaps remain severe inVietnam.

An important assumption underlying theinterpretation of the ICOR as an efficiencyindicator is that capital accumulation willresult in a higher GDP within one year.While this might be plausible in the case ofsmall commercial investments, it may beonly partially true in the case of majorindustrial undertakings and it is mostcertainly wrong in the case of largeinfrastructure projects. It follows that theICOR should increase when growthaccelerates due to surge in investment, anddecrease when investment decelerates.

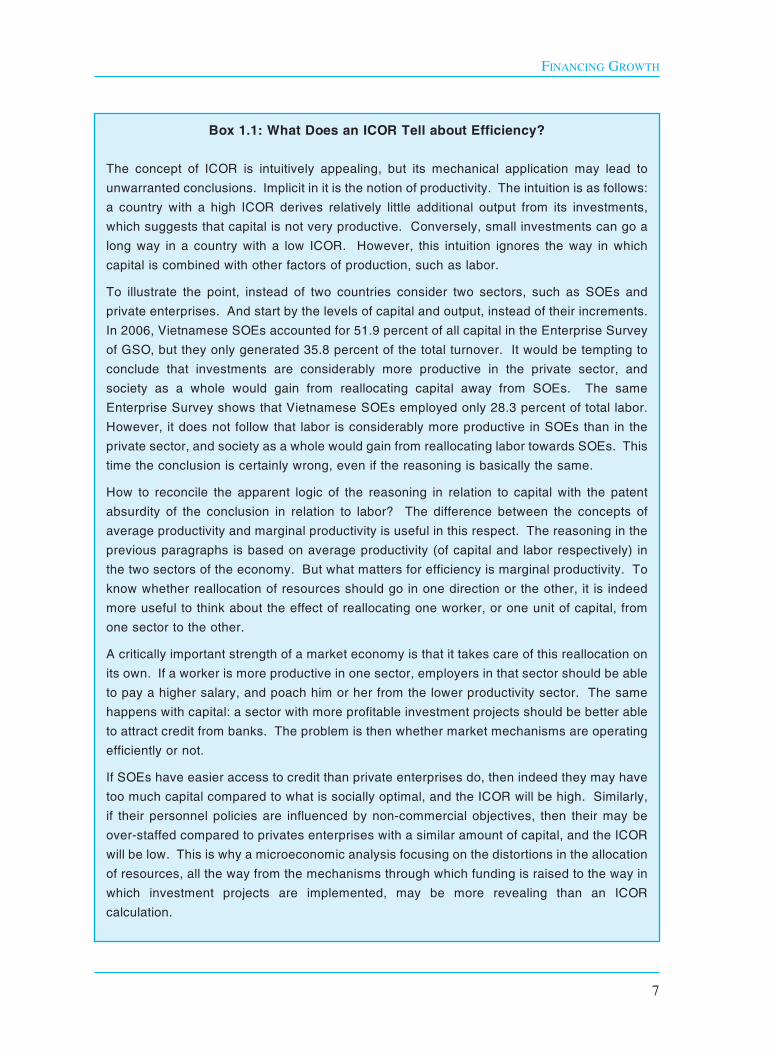

Some would even question that the ICORshould be at all used to assess the efficiencyof investment (Box 1.1). But even if thestandard measure of the ICOR at constantprices was retained, most of the surge

observed in 2007 would be driven byforeign-invested companies (Figure 1.2).Admittedly, some relatively heroicassumptions are needed to disaggregate totaloutput by institutional sector. It is also clearthat an upward trend is noticeable in the caseof the state sector and the domestic privatesector, perhaps reflecting decreasing returnsto capital as the most urgent investment gapsare addressed. But something radicallydifferent happened in relation to foreigninvestment in 2007, something that helpsexplain the macroeconomic turbulence ofthat year, and understand the unprecedentedchallenges faced by policy makers in theirquest for stability.

Investment “needs”

While macroeconomic data is not adequateto evaluate the efficiency of investment, it iswell-suited to assess its affordability. Thecapacity of Vietnam to sustain an investmentratio as high as in 2007 is questionable.Over time, various analyses have beenproposed to determine the investment levelVietnam should aim for.

The simplest and intuitively most appealingapproach focuses on investment “needs”.One popular variant of this approach,favored by those dealing with infrastructure,uses sectoral targets and master plans as itsstarting point. Through its developmentstrategies and socio-economic plans,Vietnam has set ambitious objectives andtargets across a range of areas. Some ofthose objectives and targets are related tooutcome indicators, such as the proportion ofthe population having access to specificservices. Others are spelled out in outputterms, such as kilometers of highways orpassenger airport capacity. Meeting these

CAPITAL MATTERS

6

FINANCING GROWTH

7

Box 1.1: What Does an ICOR Tell about Efficiency?

The concept of ICOR is intuitively appealing, but its mechanical application may lead tounwarranted conclusions. Implicit in it is the notion of productivity. The intuition is as follows:a country with a high ICOR derives relatively little additional output from its investments,which suggests that capital is not very productive. Conversely, small investments can go along way in a country with a low ICOR. However, this intuition ignores the way in whichcapital is combined with other factors of production, such as labor.

To illustrate the point, instead of two countries consider two sectors, such as SOEs andprivate enterprises. And start by the levels of capital and output, instead of their increments.In 2006, Vietnamese SOEs accounted for 51.9 percent of all capital in the Enterprise Surveyof GSO, but they only generated 35.8 percent of the total turnover. It would be tempting toconclude that investments are considerably more productive in the private sector, andsociety as a whole would gain from reallocating capital away from SOEs. The sameEnterprise Survey shows that Vietnamese SOEs employed only 28.3 percent of total labor.However, it does not follow that labor is considerably more productive in SOEs than in theprivate sector, and society as a whole would gain from reallocating labor towards SOEs. Thistime the conclusion is certainly wrong, even if the reasoning is basically the same.

How to reconcile the apparent logic of the reasoning in relation to capital with the patentabsurdity of the conclusion in relation to labor? The difference between the concepts ofaverage productivity and marginal productivity is useful in this respect. The reasoning in theprevious paragraphs is based on average productivity (of capital and labor respectively) inthe two sectors of the economy. But what matters for efficiency is marginal productivity. Toknow whether reallocation of resources should go in one direction or the other, it is indeedmore useful to think about the effect of reallocating one worker, or one unit of capital, fromone sector to the other.

A critically important strength of a market economy is that it takes care of this reallocation onits own. If a worker is more productive in one sector, employers in that sector should be ableto pay a higher salary, and poach him or her from the lower productivity sector. The samehappens with capital: a sector with more profitable investment projects should be better ableto attract credit from banks. The problem is then whether market mechanisms are operatingefficiently or not.

If SOEs have easier access to credit than private enterprises do, then indeed they may havetoo much capital compared to what is socially optimal, and the ICOR will be high. Similarly,if their personnel policies are influenced by non-commercial objectives, then their may beover-staffed compared to privates enterprises with a similar amount of capital, and the ICORwill be low. This is why a microeconomic analysis focusing on the distortions in the allocationof resources, all the way from the mechanisms through which funding is raised to the way inwhich investment projects are implemented, may be more revealing than an ICORcalculation.

objectives and targets, in turn, requiresimplementing a range of investmentprojects.

Going from these diverse objectives andpotential projects to concrete investmentfigures per sector is not straightforward. Forinstance, no readily-available estimatescould be found in the case of irrigation. Andfor other sectors, compiling the variousavailable estimates in a coherent way is adaunting task. However, the picture thatemerges from this exercise is one wherecapital accumulation needs remain massiveover the next few years (Table 1.2). Basedon this “engineering” approach, thegovernment would need to invest around11.5 billion dollars per year. This is theequivalent of more than 16 percent ofVietnam’s GDP in 2007.

However, no matter how impressive thetotal figure, this approach to assessinginvestment needs has important limitations

that reduce its usefulness. First, as the caseof irrigation shows, there is always a risk ofomitting important sectors, activities orprojects. Second, the engineering approachdoes not say much about who shouldundertake which investments. Most of theeffort goes into quantifying the cost ofpublicly funded infrastructuredevelopment. But it is clear that some ofthe effort could be undertaken by theprivate sector (electricity, oil and gas, andtelecommunications are obvious examples).Third, and related to the previous point, theengineering approach remains silent oninvestment needs in commercially-orientedsectors, such as manufacturing, real estateor tourism. Last but not least, it assumesthat all development objectives are attainedand all master plans implemented, whilethis may not be feasible (or may not be thebest choice) under all circumstances.

Another frequently used approach to assessinvestment “needs”, more economic in

CAPITAL MATTERS

8

0

2

4

6

8

10

12

14

2001 2002 2003 2004 2005 2006 2007

ICO

R(in

cons

tant

pric

es)

State sectorDomestic private sectorForeign-owned companies

Figure 1.2: The Incremental Capital-Output Ratio

Source: Based on data from GSO.

nature, relies on the ICOR. As discussedabove, the ICOR captures the relationshipbetween incremental capital on the one handand additional output on the other. Dividingboth terms by GDP, the relationshipbecomes one between the net investmentrate (incremental capital over GDP) and thegrowth rate of the economy (additionaloutput over GDP). Adding the depreciationrate to the investment rate, one obtains thegross investment rate.

The economic approach has the merit of itssimplicity, although the question remainswhether the standard ICOR is the relevantindicator for this calculation. To illustratehow the economic approach works, assumethat the ICOR is equal to 5, which is a roughaverage of the last few years in Vietnam.Assume also a depreciation rate equivalentto 4.5 percent of GDP, which is again the

average for Vietnam in recent years, basedon national accounts. Under theseassumptions, a GDP growth rate of 8.4percent per year is associated withinvestment “needs” amounting to 46.5percent of GDP (= 8.4 x 5 + 4.5). If thegrowth rate fell to 6 percent instead,investment needs would drop to 34.5 percentof GDP (= 6 x 5 + 4.5).

The economic approach also provides astraightforward assessment of the wayinvestment needs can be funded. This isusually done by assuming a constantdomestic savings rate. The differencebetween investment needs and the savingsrate needs to be financed by the rest of theworld. By definition, this difference is thedeficit of the current account of the balanceof payments. Put differently, if the countryinvests more than it saves someone else has

FINANCING GROWTH

9

Table 1.2: The Engineering Approach to Investment

Sector Billion dollars Forecast periodper year

I. Economic developmentTransport 2.8 n.a. Electricity 4.0 Until 2010Oil and gas 0.9 Imputed from 2008Telecommunications 0.7 Until 2010Urban development 0.7 Until 2010Water and sanitation (rural) 0.1 Until 2020Environmental protection 0.3 Until 2011Agriculture n.a.

II. Social developmentEducation 1.2 Imputed from 2008

Health 0.7 Imputed from 2008Total investment needs (I + II) 11.5

Source: Based on estimates by the World Bank, the International Monetary Fund (IMF), the Ministryof Finance (MOF), and various line ministries.

to fill the gap. In countries with low savingsrates, the current account deficit is mainlydue to large imports of consumer goods, inexcess of total exports. In countries withhigh investment rates, like Vietnam, largeimports of capital goods tend to drive thedeficit.

Again, to illustrate how this approach works,assume a domestic savings rate equal to 30percent of GDP, close to the Vietnameseaverage in recent years. With a growth rateof 8.4 percent per year, the current accountdeficit amounts to 16.5 percent of GDP (=46.5 – 30). This is a remarkably large figure,one that would raise concerns among creditrating agencies. But the current accountdeficit would drop by more than two thirds,to a much more palatable 4.5 percent of GDP(= 34.5 – 30), if the growth rate fell to 6percent (Figure 1.3). Modulating the growthrate of the economy is thus a way to controlthe magnitude of the current account deficit.Much of the recent macroeconomic debate

in Vietnam has implicitly relied on this typeof analysis.

Investment funding

A less mechanical way to analyze theprovenance and use of resources is the flow-of-funds analysis (Table 1.3). The mostrecent year for which this snapshot analysiscan be conducted is 2007. Ideally, theexercise should be conducted annually, tointroduce a time-series dimension, inaddition to the snapshot. Moreover, themacroeconomic situation is changing quitedramatically as a result of the globalfinancial crisis, so that the analysis for 2008could be quite different. And the quality ofavailable data leaves something to bedesired, so the results should be interpretedwith caution. Nevertheless, this snapshotgives interesting insights.

Following a standard practice, the economyis divided into government, the privatesector, government, the banking sector, andthe rest of the world. The government sector

CAPITAL MATTERS

10

0

10

20

30

40

50

60

0 2 4 6 8

GDP growth rate (in percent)

Perc

ento

fGD

P

Net investment Gross investment Savings

Figure 1.3: The Economic Approach to Investment

Source: Own estimates.

includes on-budget capital expenditure and“off-budget” investment expenditure(mainly infrastructure bonds). A moredifficult decision concerns the classificationof on-lending of ODA and other resources.Much of the on-lending goes to lower levelsof government, but large SOEs such asElectricity of Vietnam have benefitted fromit as well. The balance is probably tilted inthe opposite direction in the case of lendingby the Vietnam Development Bank (VDB),which has a strong customer base amongSOEs. Short of classifying on a loan-by-loanbasis, the most defensible rule is to classifyVDB loans as finance for SOEs and the restof on-lending as budgetary resources forlower levels of government. Followingstandard practice, SOEs are counted as partof the private sector. An effort to treat themseparately required too many assumptions tobe credible.

The main sources of information to conductthe flow-of-funds analysis are the budget inthe case of the government, the monetarysurvey in the case of the banking sector, andthe balance of payments in the case of therest of the world. Private sector data iscompiled from the other sources, using thedouble entry principle, and balancing theaccount through the estimate of value addedfrom domestic sales (a variable that can onlybe measured with a considerable margin oferror). In principle, the accounts for theother three sectors should balance, in thesense that financing should match thedifference between expenditures andincome, if there is any. Unfortunately,budget sector data in Vietnam do not meetthis requirement. The budget deficit is muchhigher when it is measured as the differencebetween expenditures and income (thestandard definition) than when it is

calculated as the sum of all financialresources mobilized (such as domestic debtand foreign debt). The difference betweenthe two measures is due to revenuecarryovers, which are treated here as othergovernment income.

This snapshot analysis reveals some clearpatterns. A few of them are clearly visible inmore standard presentations of the samedata; others less so. Among the relativelyobvious patterns is the breakdown ofinvestment by sector. The governmentaccounts for roughly 30 percent of totalcapital accumulation, whereas the privatesector and SOEs contribute 70 percent of it,with roughly 10 percentage points investedby SOEs. This pattern was already clear inthe gross investment data discussed earlier.

Both government and the business sectorinvested more than they saved, implyingthat they both needed to resort to finance.On the surface, they did it to similarextents. The financing gap for the privatesector and SOEs was 58.7 trillion dong,equivalent to 3.6 percent of their totalincome and 18.0 percent of total capitalaccumulation. In the case of government,the gap amounted to 26.2 trillion dong, andthe corresponding ratios were 7.6 and 18.6percent respectively. However, this isbecause carryovers are being treated asrevenue. If they were classified asfinance, then the ratios for governmentwould climb to 17.1 and 38.4 percentrespectively. It follows that in 2007 thegovernment was less thrifty than theprivate sector and SOEs. The mainprovider of financial resources was the restof the world, with the current accountdeficit representing roughly 18.2 percent oftotal capital accumulation in Vietnam.

FINANCING GROWTH

11

CAPITAL MATTERS

12

Table 1.3: The Financial Approach to Investment

Government

Source Use Items included

1. ReceiptsExportsTransfers 4.3 ODA grantsTaxes 265.9 Taxes and oil-related revenueOther income 73.4 Non-tax revenue + carryovers

2. Current ExpenditureConsumption 157.3 Non-salary expenditureImports 4.7 Gasoline subsidy

Transfers 67.3 SalariesTaxesOther

3. Investment expenditure 140.5 Includes off budget but no VDB4. Saving (=1- 2) 114.35. Net financing (=6+7+8+9) 26.26. To/from government7. To/from private sector 15.8 Bonds and VDB borrowing8. To/from financial sector 7.4 Change in deposits - loans9. To/from rest of the world 17.8 Change in foreign public debt

Private sector and SOEs

Source Use Items included

1. ReceiptsExports 878.5 Exports of goods and servicesTransfers 108.2 Remittances + gasoline subsidyTaxesOther income 660.2 Domestic value added (residual)

2. Current ExpenditureConsumptionImports 1032.2 Imports of goods and services

TransfersTaxes 265.9 Taxes and oil-related revenueOther 80.5 FDI profits + non-tax revenue

3. Investment expenditure 327.0 Total - government investment4. Saving (=1- 2) 268.35. Net financing (=6+7+8+9) 58.76. To/from government 15.8 Bonds and VDB borrowing7. To/from private sector8. To/from financial sector 115.1 Change in deposits + liquidity9. To/from rest of the world 189.6 FDI + portfolio + loans

(continued)

FINANCING GROWTH

13

Table 1.3: The Financial Approach to Investment (Continued)

Financial sector

Source Use Items included

1. ReceiptsExportsTransfersTaxesOther income

2. Current ExpenditureConsumptionImports

TransfersTaxesOther

3. Investment expenditure4. Saving (=1- 2)5. Net financing (=6+7+8+9)6. To/from government 7.4 Change in deposits - loans7. To/from private sector 115.1 Change in deposits + liquidity8. To/from financial sector 9. To/from rest of the world 122.5 Change in bank's foreign assets

Rest of the world

Source Use Items included1. Receipts

Exports 1032.2 Imports of goods and servicesTransfers 34.7 FDI profitsTaxesOther income

2. Current ExpenditureConsumptionImports 878.5 Exports of goods and services

Transfers 103.5 RemittancesTaxesOther

3. Investment expenditure4. Saving (=1- 2)5. Net financing (=6+7+8+9) 84.96. To/from government 17.8 Change in foreign public debt7. To/from private sector 189.6 FDI + portfolio + loans8. To/from financial sector 122.5 Change in bank's foreign assets9. To/from rest of the world

Source: Own calculations based on data from CSO, IMF and SBV. Figures are in trillion dong.

(Flow-of-fund analyses are built on theassumption that the financial sector is apure intermediary, neither saving norinvesting).

A closer look at the government accountshows the importance of taxes as the mainsource of revenue, and the relatively evensplit of finance between domestic borrowingand external borrowing. It also appears thatthe government used some of theseresources to increase its financial assets,under the form of an additional 7.4 trilliondong in deposits in commercial banks. Thismay not be a good choice from an economicpoint of view, and may simply reflectweaknesses in cash management.

In the case of the business sector, exportsaccount for 53.3 percent of total income,which shows how open the Vietnameseeconomy is by now. And an additional 6.3percent of income is under the form ofremittances from abroad. The role of globalintegration is even more striking whenlooking at the financing side of the equation.An astounding 189.6 trillion dong, theequivalent of 58 percent of total capitalaccumulation by the private sector andSOEs, was received under the form of FDI,portfolio investment or lending from abroad.It is also striking to see the large fraction ofbusiness resources devoted to financialinvestments in 2007. Changes in bankingdeposits (net of loans) and governmentbonds (directly or through social securitycontributions) were equivalent to roughly 40percent of capital accumulation. This is anindication of financial deepening, but such arapid pace is a matter for concern.

Sustainable accumulation?

With Vietnam investing considerably more

than it saves, the question is whether thismassive accumulation effort is sustainableover time. For the country as a whole, thefinancing gap is the same as the currentaccount deficit of the balance of payments.In 2007, this deficit almost reached 10percent of GDP, which is usually considereda warning threshold. However, comparingthe current account deficit to the country’sGDP is a rudimentary approach to assesswhether it is too large or of adequate size.

Vietnam’s external debt position hashistorically been robust. Most of its debt isconcessional, enjoying a low average, fixedinterest rate, long maturities, and nobunching of repayments. With support froma variety of multilateral and bilateralcreditors, it also has a fairly diversifiedcurrency composition. It has access to strongprivate remittances, which help finance itstrade deficit, and strong FDI inflows whichprovide significant non-debt creatingfinancing. Moreover, the government hasbeen prudent in external borrowing. Thesovereign external market was onlyaccessed once, for a ten-year maturity 750million dollar bond. External debt isestimated to total 29.7 percent of GDP, and21.6 percent in the case of the public sector.

In terms of liquidity, in 2007 the service ofexternal debt amounted to 6.2 percent ofexports whereas the service of publicexternal debt represented 11.9 percent ofgovernment revenues. These ratios remainmanageable, well within the thresholdsjointly established by the World Bank andthe IMF. And they are expected to declinefurther in 2008, to 3.2 and 4.2 percentrespectively. Although the current accountdeficit increased markedly in 2007,

CAPITAL MATTERS

14

financing from FDI and portfolio inflowsalso rose considerably. The rapid growth ofexports and FDI inflows, buoyantgovernment revenue and the appreciation ofthe dong underlie the expected reduction inthese ratios in 2008.

Vietnam’s debt situation has remainedrelatively favorable despite the significantmacroeconomic imbalances that emerged in2007. The much larger current account deficitwas partly financed by much higher FDI andportfolio inflows. The latter declined in 2008,

but the former increased. Looking forward,under plausible macroeconomic assumptions,the present value of external debt is projectedto decline consistently in relation to GDP,exports, and revenue (Figure 1.4). Stress testsindicate that the present value of debt to GDPratio is most sensitive to an increase in otherdebt creating flows, and to a lower primaryfiscal balance. A one-time 30 percentdepreciation would have less impact on thepresent value of debt. But even the mostextreme negative shock would not destabilizekey ratios over the longer term.

FINANCING GROWTH

15

0

10

20

30

40

2007 2008 2009 2010 2011 2012 2013 2014

Perc

ento

fGD

P

All nominal Public sector nominal

All present value Public sector present value

Figure 1.4: A Robust External Debt Position

Source: Joint IMF-World Bank debt sustainability assessment (IMF, 2008).

16

The analysis of economic growth is usuallydissociated from that of macroeconomicstabilization. This is because the time spansinvolved are different, and also becausegrowth is perceived as dealing withquantities, whereas stabilization has to dowith prices. However, in an economyaccumulating resources as massively asVietnam, the connection between growthand stability cannot be ignored. There aretwo mechanisms connecting largeinvestments with prices. One of them isrelatively benign, the other more worrisome.On the benign side, some goods and servicesbecome more expensive as countries growricher. These are basically goods andservices that cannot be easily traded with therest of the world. Housing and personalservices are obvious examples. The result isthat richer countries tend to be moreexpensive, and the same pattern can beobserved across provinces within Vietnam.The implication is that rapid growth isassociated with real exchange rateappreciation. In a country growing rapidly,appreciation happens at a non-trivial speed.The more worrisome mechanism is relatedto the balance of payments. Unless thedomestic savings rate increasessubstantially, accumulating capital in thescale Vietnam did in recent years is bound torequire large foreign savings. However,capital inflows tend to be volatile, as they

are affected by market sentiment. Investors’perceptions can switch from exuberance tofear in no time, for reasons that may havelittle to do with Vietnam’s actualperformance. Sudden capital outflows areobviously dangerous for economic stability,but surges in capital inflows are dangeroustoo, as they can result in asset price bubbles.These more dramatic swings in relativeprices typically result in inefficiencies in theallocation of capital and may eventually leadto costly financial crises. Massive capitalaccumulation may thus hold the key to rapideconomic growth, but it also confronts policymakers with unusual challenges.

Prices and quantities

Massive capital accumulation is associatedwith a greater availability of goods andservices, but also with changes in therelative prices of those goods and services.The first dimension (quantities) isemphasized in most analyses abouteconomic growth, but the second one(prices) is quite often ignored. Or, moreaccurately, variation in relative prices isanalyzed from a cross-country perspective,for instance in the context of purchasingpower parity analyses, but not from a timeperspective.

Dissociating quantities from prices isunderstandable when long-term growth of

2. TRANSFORMATION AND TURBULENCE

GDP per person is in the order of 1 or 2percent per year, as was the case for most ofthe Western countries which are developedby now. At that pace, changes in relativeprices are bound to take place over longperiods of time. So long that they becomeirrelevant from the point of view ofmacroeconomic policy. But several EastAsian countries have experienced muchfaster growth, crossing in one or twogenerations the income range that industrialcountries spanned over one or two centuries.As Vietnam stands a chance to do the same,it is useful to understand how rapid growthmay affect relative prices in the short term.

Purchasing power parity analyses provide auseful starting point. These analysescompare the price, in dollar terms, of acommon set of goods and services acrosscountries. The simplest version focuses onjust one homogeneous product which issupposed to be made to the samespecifications and delivered in the samemanner all around the world, namelyMcDonald’s Big Mac hamburger. In spite ofthe homogeneity of the product, the price ofa Big Mac varies from 1.8 dollars in China to3.6 dollars in the United States to 7.9 dollarsin Norway. More refined analyses considera broader basket of goods and services, withthe assessment becoming increasinglycomplicated when items such as health careor education are considered.

Whatever the definition of the basket andthe methodological choices made formeasurement, the ratio between the cost ofthe basket in a specific country and the samebasked in the United States indicates howmany cents of a dollar are needed in thatcountry to enjoy the same purchasing powerone dollar has in the United States.

As an illustration, PPP correction factorshave played an important role in themeasurement of world poverty, whichusually involves counting which fraction ofthe population lives on less than “one dollara day”. In this context, “one dollar” meansone dollar with United States purchasingpower. In developing countries, that isactually much less than one dollar. Forinstance, in the case of Vietnam the mostrecent PPP correction factor is 0.322, whichmeans that 32.2 cents buy the same inVietnam as one dollar does in the UnitedStates.

As a general rule, adjustments forpurchasing power parity are larger in poorercountries, which is another way to say thatthose countries are cheaper (Figure 2.1).While there is considerable dispersionacross countries, the overall pattern is clear.A regression analysis involving the 169countries for which data are available showsthat an increase of 1 percent in GDP perperson (measured in dollar terms) isassociated with a 0.2 percent increase inprices (measured in dollar terms too). If thesame relationship applied to individualcountries over time, a growth rate of GDPper capita of 12.5 percent (the rough figurefor Vietnam in 2001-2007) would beassociated with an annual appreciation in theorder of 2.5 percent.

Exchange rate appreciation

There are reasons to suspect that the pace ofappreciation could be even faster in the caseof Vietnam. To begin with, Vietnam remainsconsiderably cheaper than other countries ata similar development level. While its PPPconversion factor is 0.322, the predictedvalue (given by the estimated line in Figure

TRANSFORMATION AND TURBULENCE

17

2.1) is 0.441. Just catching up to thepredicted value would require a 37 percentincrease in domestic prices, in dollar terms.Admittedly, the development level is not theonly good predictor of PPP conversionfactors. But increased internationalintegration, especially after the WTOaccession, can be expected to lead to a moreaccelerated convergence of Vietnam toglobal norms and patterns across a range ofdimensions. Similarity of prices could beone of them.

Price disparities across provinces also hint atthe possibility of rapid appreciation. Thestandard analyses of PPP correction factorsacross countries can indeed be reproducedusing Vietnamese provinces as the unit ofobservation (Figure 2.2). In this case, ratherthan a given basket, a set of individual goodsand services such as rice, labor and housingcan be considered. In terms of the scope totrade these goods and services across

provinces, they range from the fully mobile(rice) to the partially mobile (labor) to thefully immobile (housing).

In line with the pattern uncovered by cross-country analyses, goods and services aremore expensive in richer provinces. And notsurprisingly, the relationship is steeper theless mobile the good or service is. Anincrease of one percent in expenditure perperson is associated with a 0.11 percentincrease in the average price of rice (perkilo), a 0.83 percent increase in the averagewage level (per hour), and a 1.63 percentincrease in the average housing price (persquare meter). Admittedly, housing andworkers are less homogeneous acrossprovinces than rice, which implies that someof the estimated gap in prices may simplyreflect differences in quality. But thepotential for appreciation implied by theestimated relationships seems considerable.

To illustrate the point, consider the

CAPITAL MATTERS

18

0.0

0.2

0.4

0.6

0.8

1.0

0 2,000 4,000 6,000 8,000

GDP per person (current dollars)

Loc

alpr

ices

rela

tive

toU

Spr

ices

Actual Vietnam

Figure 2.1: Richer Countries Are more Expensive

Source: Own calculations using data from the World Bank.

average growth rate of Vietnam’s GDP perperson during the period 2001-2007,measured in dollars. This rate was about12.5 percent, so that the growth rate ofexpenditures per person must have beensimilar. If quality effects are ignored, a12.5 percent increase in averageexpenditures per person, measured indollars, would be associated with a 1.4percent increase in the price of rice, a 10.4percent increase in labor earnings and a20.4 percent increase in the cost ofhousing. These increases are measured indollar terms too. And while they sufferfrom measurement problems, related to thedifferent quality of labor and housingacross provinces, they are plausible. Forinstance, based on household survey data,labor earnings grew by a cumulative 12.5percent per year between 1998 and 2006,at a time when the exchange rate wasstable. A weighted average of thesefigures reflecting the relative importanceof mobile, partially mobile and less mobileitems in a hypothetical basket of goods andservices is bound to yield a large priceincrease associated with growth, possiblymuch larger than cross-country analysessuggest.

Last but not least, time trends in theadjustment for purchasing power parity alsopoint in the direction of rapid appreciation.Between 2001 and 2007, the ratio ofdomestic prices to United States prices grewby 3 percent per year in the case of Vietnam,half a percentage point faster than the cross-country comparison would suggest, and halfa percentage point faster than China too.This does not appear to be a statisticalartifact, given that the trend is almost thesame when a longer period is considered.

For instance, between 1991 and 2007, theratio of domestic prices to United Statesprices increased by 2.9 percent per year,compared to 1.5 percent in the case of China.

Capital inflows and prices

The acceleration of capital accumulationexperienced by Vietnam in recent years wasaccompanied by a dramatic change in thecomposition of the balance of payments.Between 2005 and 2007 the investment ratioincreased from 40.9 to 45.6 of GDP. Overthe same period, the current account deficitincreased from 0.9 to 9.8 percent of GDP.The capital account surplus increased evenfaster, from 4.8 to 24.6 percent of GDP.

This trend is now being reversed, due to theturbulence in international financial markets,and the reversal could be dramatic.However, beyond the shifts in marketsentiment, it is clear that attempts to growrapidly are bound to lead to current accountdeficits if they are not accompanied by anincrease in the domestic savings rate. Largecurrent account deficits need to be matchedby similarly large capital inflows. And this,in turn, may create considerable pressure ondomestic demand and prices.

In 2007 alone, 17.5 billion dollars in FDI,portfolio investments, banking credit andOfficial Development Assistance (ODA)entered the country. If remittances areadded (they are usually counted as part ofthe current account) total inflows reached 24billion dollars (Figure 2.3). This is theequivalent of 33.7 percent of GDP. To givea sense of perspective, in none of the yearsfor which data are available did the capitalaccount balance of China exceed 5 percentof GDP. Out of 129 countries for which data

TRANSFORMATION AND TURBULENCE

19

are available in 2007, only 13 had largercapital account balances than Vietnam.

Absorbing such large capital inflows would bedifficult for an industrial country with maturefinancial institutions. It is enormouslychallenging for a country that is still in theprocess of establishing a modern central bank.To be clear, a large capital account balance isthe flip side of massive capital accumulation.As shown by the economic approach tofinancing needs, an investment ratio in excessof the domestic savings rate is bound to leadto a current account deficit. But in the case ofVietnam, the hype associated with WTOaccession resulted in capital inflows farexceeding the current account deficit.

This confronted the government with the“impossible trinity” of having capitalmobility a fixed exchange rate and anindependent monetary policy.

Massive capital inflows needed to beconverted into dong to support the purchaseof goods, services and financial instrumentsin Vietnam. In the absence of governmentintervention, this would have resulted in amore expensive dong or, equivalently, acheaper dollar. Most mature economieswould have allowed this nominal exchangerate appreciation as a way to absorb theshock. But the government preferred toprevent this appreciation, mainly to avoid aloss of competitiveness. There was a fearthat nominal exchange rate appreciationwould punish exporters and eventuallyundermine the appetite of foreign investorsto bring capital to Vietnam.

In practice, there is an additional reason whya prudent approach to exchange rateflexibility might have been warranted, andthat is the risk of affecting the liquidity, or

CAPITAL MATTERS

20

0

20

40

60

80

100

120

140

0 2000 4000 6000 8000 10000 12000

Expenditure per person (thousand dong)

Pric

eof

rice

(ave

rage

=10

0)

Actual Predicted

0

50

100

150

200

250

0 2000 4000 6000 8000 10000 12000

Expenditure per person (thousand dong)

Ear

ning

spe

rho

ur(a

vera

ge=

100)

Actual Predicted

0

200

400

600

800

0 2000 4000 6000 8000 10000 12000

Exoenditure per person (thousand dong)

Pric

eof

hous

ing

(ave

rage

=10

0)

Actual Predicted

Figure 2.2: Richer Provinces Are more Expensive

Source: Own calculations using data from GSO.

even the solvency, of commercialenterprises and financial institutions.Balance sheet effects of this sort were one ofthe main reasons why the East Asian crisis of1997 was so severe.

Currency mismatches are still common inVietnam, and hedging against exchange riskis not developed. Accounting standards donot reveal which fraction of assets andliabilities is denominated in dong and whichfraction in foreign currency, making itdifficult to tell who is exposed and who isnot. Moreover, after many years with thedong unofficially pegged to the dollar, thevery notion of exchange rate risk soundedhypothetical to many.

Regardless of whether the decision tostabilize the exchange rate market wasjustified or not, it certainly led to asubstantial increase in the liquidity of theeconomy. When SBV purchases the capitalinflow to prevent the currency fromappreciating, it injects dong in the economy.This additional liquidity can in turn be

“mopped up” by selling bonds, but in 2007the SBV almost run out of governmentsecurities to sell. Money supply can also betightened by selling SBV bills, but theinterest rate offered was not attractiveenough. As a result, banking credit wasgrowing by more than 63 percent by March2008, fueling consumer prices, imports, anda real estate bubble.

Asset price bubbles

There is an inherent instability in the“impossible trinity”. Once themacroeconomic situation runs out of control,it can rapidly drift in the direction offinancial instability. Towards the end of2007, the government started facing failureafter failure in its attempts to sell securitiesin order to mop up liquidity. The interestrate needed to make bonds and securitiesattractive appeared to be too high, hence tocostly to either the budget or SBV.Sterilization did not catch up with capitalinflows, liquidity expanded and the bankingsystem recycled it into loans. This in turn

TRANSFORMATION AND TURBULENCE

21

0

5

10

15

20

25

2005 2006 2007

Billio

nU

Sdo

llars

Portfolio, short-term and errorsMedium and long-term loansRemittancesFDI net of profit repatriation

0

5

10

15

20

25

2005

Billio

nU

Sdo

llars

Trade deficit (goods and services)

Figure 2.3: A Changing Balance of Payments

Source: Own estimates based on data from State Bank of Vietnam (SBV) and GSO.

resulted in additional demand for mostlyeverything. In the case of mobile goods andservices, such as cars or cosmetics,additional demand translated into a surge inimports. In the case of less mobile goods andservices, such as land, housing or officespace, it led to a surge in prices.

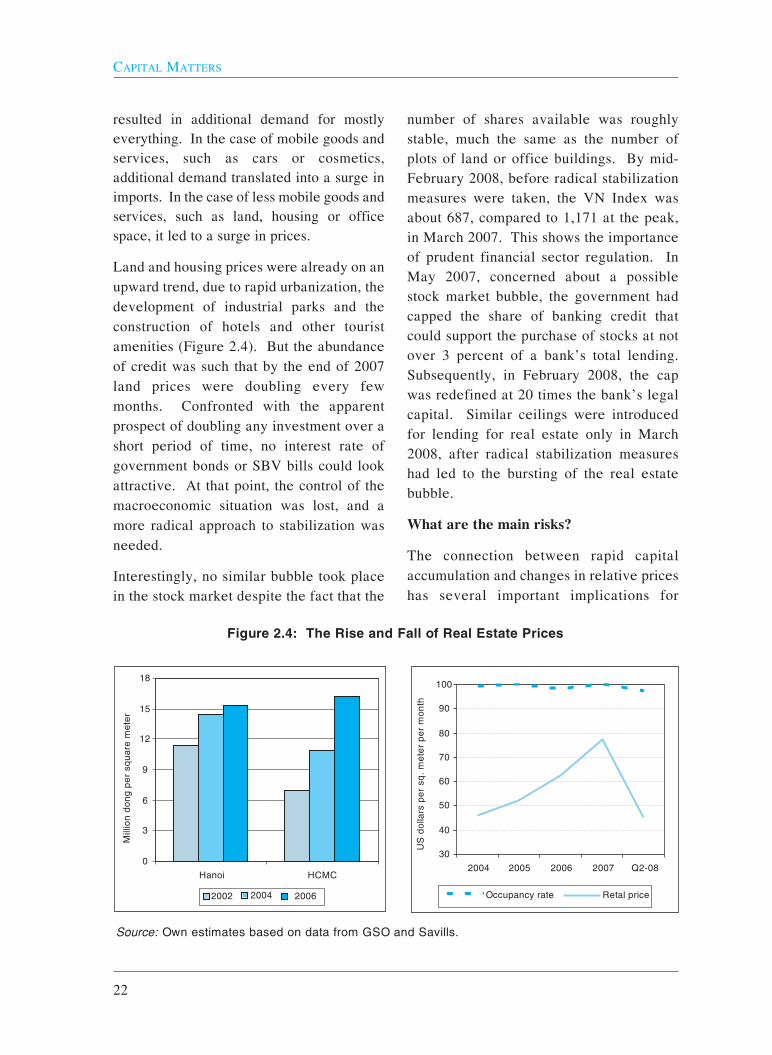

Land and housing prices were already on anupward trend, due to rapid urbanization, thedevelopment of industrial parks and theconstruction of hotels and other touristamenities (Figure 2.4). But the abundanceof credit was such that by the end of 2007land prices were doubling every fewmonths. Confronted with the apparentprospect of doubling any investment over ashort period of time, no interest rate ofgovernment bonds or SBV bills could lookattractive. At that point, the control of themacroeconomic situation was lost, and amore radical approach to stabilization wasneeded.

Interestingly, no similar bubble took placein the stock market despite the fact that the

number of shares available was roughlystable, much the same as the number ofplots of land or office buildings. By mid-February 2008, before radical stabilizationmeasures were taken, the VN Index wasabout 687, compared to 1,171 at the peak,in March 2007. This shows the importanceof prudent financial sector regulation. InMay 2007, concerned about a possiblestock market bubble, the government hadcapped the share of banking credit thatcould support the purchase of stocks at notover 3 percent of a bank’s total lending.Subsequently, in February 2008, the capwas redefined at 20 times the bank’s legalcapital. Similar ceilings were introducedfor lending for real estate only in March2008, after radical stabilization measureshad led to the bursting of the real estatebubble.

What are the main risks?