World Bank Document production began in September 1981 in the Erawan field at a ... thereby reducing...

77

Document of The World Bank . c?f> FOR OFFICIAL USE ONLY Report NO. 4201-TH STAFF APPRAISAL REPORT THAI LAND PROVINICIAL POWER DISTRIBBUTION PROJECT May i7, 1983 Proj ects Department East Asia and Pacifi c Regional Office This document hasa restricted distribution and may be used by recipients only ill the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of World Bank Document production began in September 1981 in the Erawan field at a ... thereby reducing...

Document of

The World Bank . c?f>

FOR OFFICIAL USE ONLY

Report NO. 4201-TH

STAFF APPRAISAL REPORT

THAI LAND

PROVINICIAL POWER DISTRIBBUTION PROJECT

May i7, 1983

Proj ects DepartmentEast Asia and Pacifi c Regional Office

This document has a restricted distribution and may be used by recipients only ill the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

Currency Unit - Thai Baht (B)

US$1.00 B 23.0B 1.00 = US$0.0435

(as of April 1983)

FISCAL YEAR

October 1 to September 30

WEIGHTS AND MEASURES

km - kilometer (0.62 miles)

sq km - square kilometer (0.386 square mile)m ton - metric ton (2,204.6 pounds)kV - kilovolt (1,000 volts)

kVA - kilovolt-ampere (1,000 volt-amperes)MVA - megavolt-ampere (1,000 kilovolt-amperes)kW - kilowatt (1,000 watts)

MW - megawatt (1,000 kilowatt)k,h - kilowatt-hour (1,000 watt-hours)GWh - gigawatt-hour (1 million kilowatt-hours)cu ft - cubic foot (0.0283 cubic meter)tcf - one trillion cubic feet

MMSCFD - one million standard cuiTLc feet per dayMMBTU - one million British thermal units

ABBREVIATIONS

ADB - Asian Development Bank

ADAB - Australian Development Assistance BureauCIDA - Canadiarn International Development AgencyCPPD - Committee for Power Policy and DevelopmentEDL - Electricite du LaosEGAT - Electricity Generating Authority of ThailandKFAED - Kuwait Fund for Arab Economic DevelopmentKFW - Kreditanstalt fuir Wiederaufbau (Germany)'fEA - Metropolitan Electricity AuthorityMOF - Ministry of FinanceNREP - Normal Rural Electrification ProgramNEA - National Energy AdministrationNESDB - National Economic and Social Development BoardNEB - National Electricity Board of MalaysiaOECF - Overseas Economic Cooperation Fund (Japan)OPEC - Organization of Petroleum Exporting CountriesPEA - Provincial Electricity AuthorityPTT - Petroleum Authority of Thailand

RTG - Royal Thai Government

FOR OFFICIAL USE ONLY

THAILAND

PROVINCIAL ELECTRICITY AUTHORITY

PROVINCIAL POWER DISTRIBUTION PROJECT

Table of Contents

Page No.

I. THE ENERGY SECTOR . . . . . . . . . . . . . . . . . . . . 1

A. Energy Consumption .1... . . . . . . . . . . . . . . . IB. Energy Resources . . . . . . . . . . . . . . . . . . . . 1

Natural Gas. . . . . . . . . . . . . . . . . . . . . . 1Oil. . . . . . . . . . . . . . . . . . . . . . . . . . 1Lignite Reserves .... . . . . . . . . . . . . . . . 2Hydro Potential .... . . . . . . . . . . . . . . . 2Other Energy Resources .... . . . . . . . . . . . . 2Energy Supply Alternative ... . . . . . . . . . . . 2

C. Energy Investment Program . . . . . . . . . . . . . . . 3D. Role of the Power Sector in the Economy . . . . . . . . 3E. The Power Sector Organization . . . . . . . . . . . . . 4

General ..... . . . . . . . . . . . . . . . . . . 4The Electricity Generating Authority of Thailand

(EGAT) ...................... . 4The Metropolitan Electricity Authority (MEA). 4The Provincial Electricity Authority (PEA) . . . . . . 4Private Franchises .... . . . . . . . . . . . . . . 5Government Agencies . . . . . . . . . . . . . . . . . 5

F. Power Sector Coordination . . . . . . . . . . . . . . . 5G. Tariff Levels .... . . . . . . . . . . . . . . . . . 6H. Bank Participation in the Sector . . . . . . . . . . . . 7I. Power Market and Supply .... . . . . . . . . . . . . 7J. Degree of Electrification . . . . . . . . . . . . . . . 8K. Rural Electrification . . . . . . . . . . . . . . . . . 9L. Project Performance Audits . . . . . . . . . . . . . . . 10

II. THE BORROWER . . . . . . . . . . . . . . . . . . . . . . . . 10

A. Organization and Management . . . . . . . . . . . . . . 10B. Manpower and Training . . . . . . . . . . . . . . . . . 11C. Billing and Collections . . . . . . . . . . . . . . . . 12D. Accounting and Audit . . . . . . . . . . . . . . . . . . 12E. Taxes .13F. Insurance . . . . . . . . . . . . . . . . . . . . . . . 13G. Existing Facilities . . . . . . . . . . . . . . . . . . 13

This report was prepared by Messrs. A. Mejia and W. Cao on the basis of anappraisal conducted in July 1982.

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

- ii -

Page No.

III. PEA'S POWER MARKET . . . . . . . . . . . . . . . 3. . . . . . 13

A. Background . . . . . . . . . . . . . . . . . . . . . . 13B. PEA's Load Forecast . . . . . . . . . . . . . . . . . 15C. Project's Load Forecast . . . . . . . . . . .. . . . . . 16

IV. THE PROGRAM AND THE PROJECT . .. . . . . . . . .. . . . . . 17

A. PEA's Development Strategy . . . . . . . . . .. . . . . . 17B. PEA's Development Program . . . . . . . . . .. . . . . . 18C. The Project . . . . . . . . . . . . . . . . 9. . . . . . 19

Background . . . . . . . . . . . . . . . . 9. . . . . . 19Description . . . . . . . . . . . . 0. . . . . . . . . 20

Part A - Village Electrification . . . . . . . . . . . 20

Subproject Selection Criteria . . . . . . . . . . . . 21

Part B - strengthening of PEA's Operations . . . . . . 22

Cost Estimate . . . . . . . . . . . . . . . . . . . . 23Financing Plan . . . . . . . . . . . . . . . . . . . . 25Implementation ... . . . . . . . . . . . . . . . . . 25Procurement . . . . . . . . . . . . . . . . . . . . . 26Disbursement . . . . . . . . . . . . . . . . . . . . . 26Monitoring . . . . . . . . . . . . . . . . . . . . . . 26Risks .27Environmental Effects. 27

V. FINANCIAL ANALYSIS . . . . . . . . . . . . . . . . . . . . . 27

A. PEA's Financial Performance FY77 through FY81 . . . . . 27B. Future Profitability . . . . . . . . . . . . . . . . . . 29C. Tariffs .. . . . . . . . . . . . . . . . . . . . . . 30D. Financing of PEA's Development Program . . . . . . . . . 32E. Debt Control ... . . . . . . . . . . . . . . . . . . . 33F. Liquidity Position . . . . . . . . . . . . . . . . . . . 33

VI. ECONOMIC ANALYSIS . . . . . . . . . . . . . . . . . . . . . 33

Economic Rate of Return . . . . . . . . . . . . . . . . 33

VII. AGREEMENTS REACHED AND RECOMMENDATIONS . . . . . . . . . . . 35

A. Agreements . . . . . . . . . . . . . . . . . . . . . . . 35B. Recommendations .................... . 36

- iii -

ANNEXES

1. Highlights of EGAT, MEA and PEA Operations2. PEA's Organization Chart3. PEA's Market:

Table 1: Historical Evolution of PEA's MarketTable 2: PEA's Forecast of Energy Sales and Power Demands

4. PEA's Investment Program, FY82-915. Scope of Works of the NRE Program and Phases I and II6. Backlog of Applications for Electrification Under NREP as of May 19827. Cost Estimates NREP Phases I and II8. Procurement and Implementation Schedule9. Estimated Disbursement Schedule10. Description of PEA monitoring system11. PEA's Historical Financial Statements, FY77-81

Table 1: Income StatementsTable 2: Funds Flow StatementsTable 3: Balance Sheets

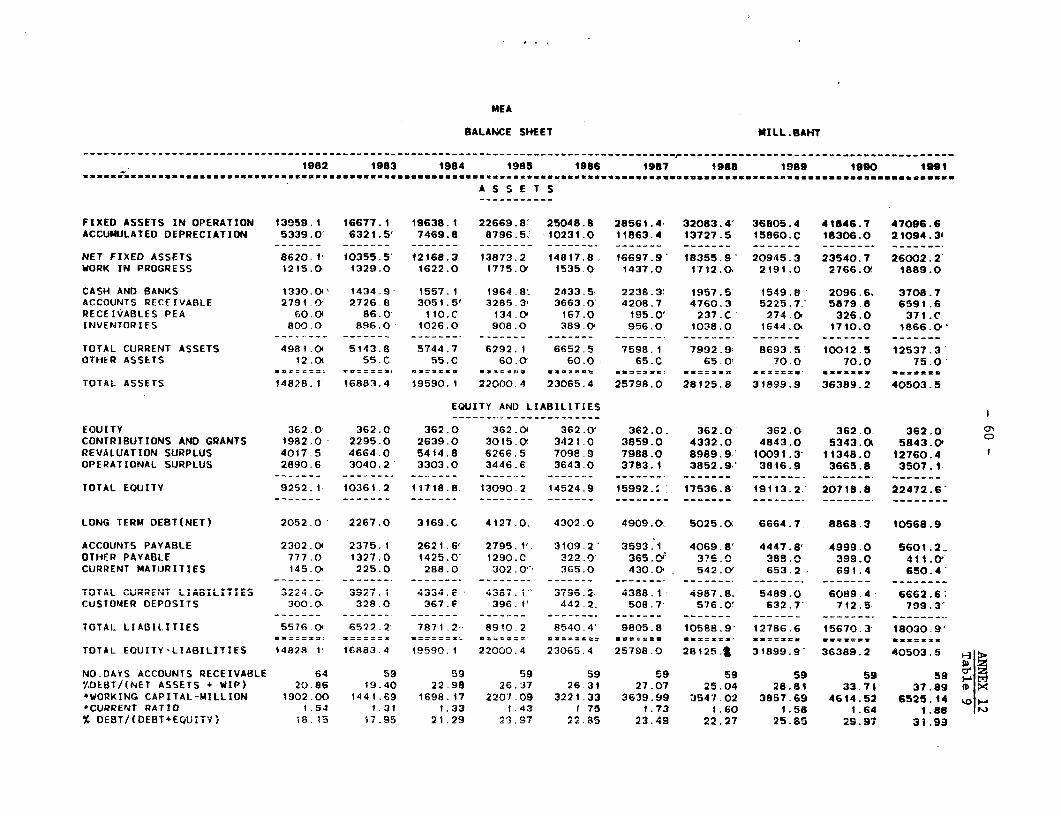

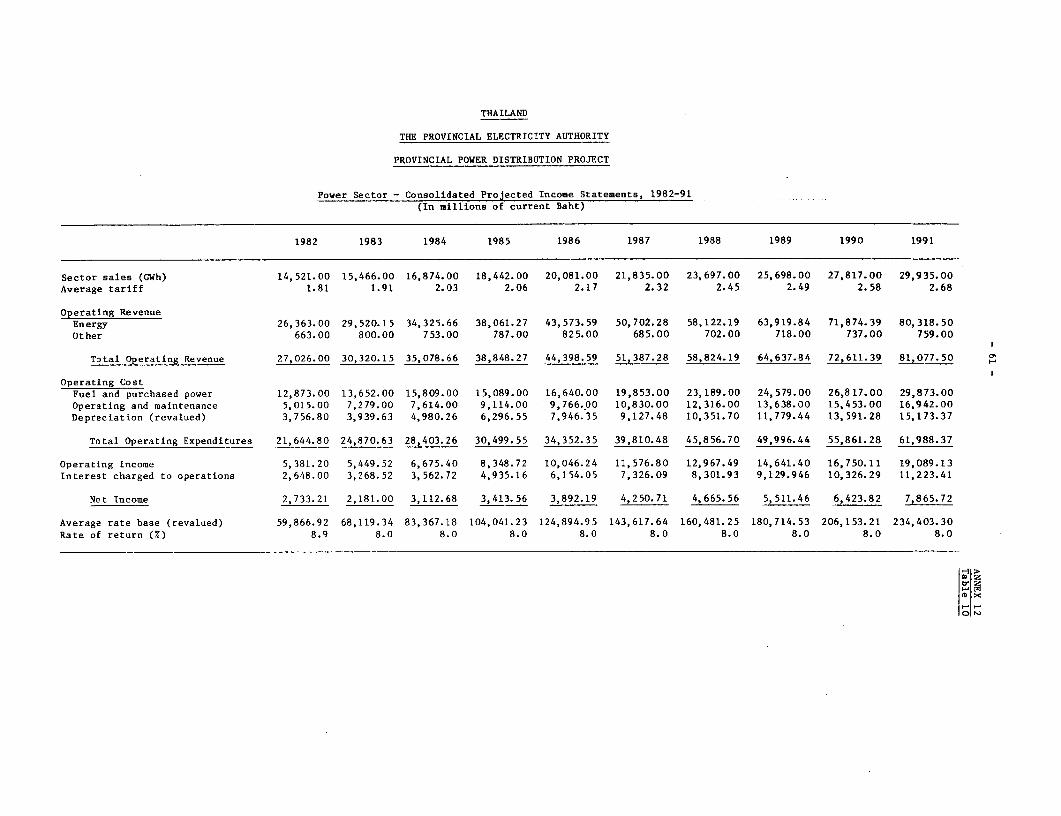

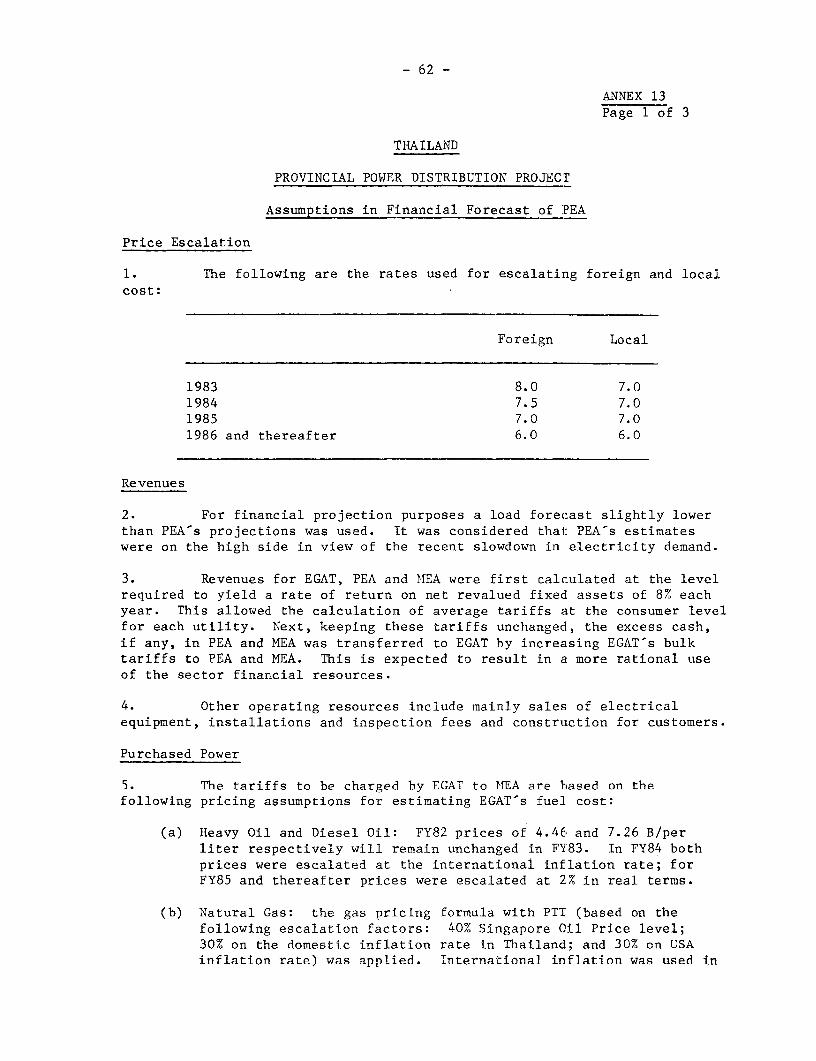

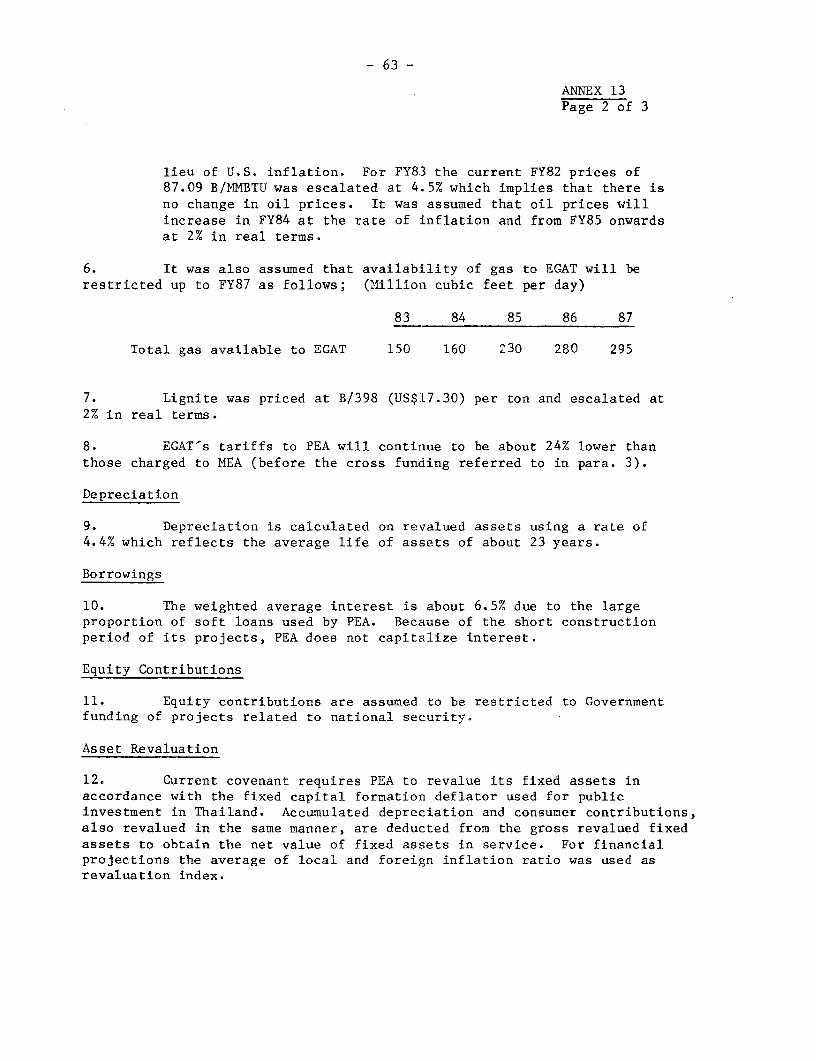

12. Projected Income Statements, Funds Flow, Balance Sheets, 1982-1991Tables 1 through 3: PEATables 4 through 6: EGATTables 7 thrQugh 9: MEATable 10: Power Sector - Consolidated Income Statements

13. Assumptions in Financial Forecast of PEA14. Rate of Return Calculation15. Related Documents and Data Available in Project File

MAP

IBRD 16683

THAILAND

PROVINCIAL ELECTRICITY AUTHORITY

PROVINCIAL POWER DISTRIBUTION PROJECT

I. THE ENERGY SECTOR

A. Energy Consumption

1.01 Total commercial energy consumption in Thailand has increased from5.9 million tons of oil equivalent in 1970 to over 16.2 million tons of oilequivalent in 1981, an average annual growth rate of 8.8%. In 1981, petrol-eum products accounted for 71% of total energy. Indigenous resources haveaccounted for the rest of total energy consumption, with fuelwood/charcoal,bagasse, hydro, and lignite forming 13%, 7%, 5% and 4% shares, respectively.The price of crude oil has increased almost twelvefold since 1972 and hasbecome a heavy burden on the Thai economy. After the second oil shock, theshare of Thailand's energy imports in total imports increased to 31%, and 45%of the economy's export earnings were required to finance energy imports alonein 1980.

B. Energy Resources

Natural Gas

1.02 Natural gas reserves in the Gulf of Thailand are currently esti-mated to amount to about 20 trillion cubic feet (tcf) of which about 4 tcfare proven. Gas production began in September 1981 in the Erawan field at arate of 70-80 million standard cubic feet per day (MMSCFD). During 1982production gradually increased to about 130 MMSCFD, but remained short of the200 MMSCFD which had originally been expected. The shortfall is attributableto technical difficulties and to the fact that the gas reserves aredistributed over smaller than expected reservoirs. Proven reserves arecurrently being reassessed. With the addition of further production capacityin other fields, production would increase to 600 MMSCFD by 1987. The Bankmade a loan of $107 million (Loan 1773-TH) in FY80 for the development of thefirst phase of the natural gas pipeline, and a Bank loan of $90 million (Loan2184-TH) to help finance a gas separation plant and marketing facilities wassigned on August 17, 1982. It is expected that by 1990, about 40% of EGAT-sprojected total generation of 32,950 GWh would be from thermal stations usingnatural gas, thereby reducing substantially the demand for fuel oil.

Oil

1.03 The exploration for oil in Thailand has recently led to improvedexpectations of domestic oil production beyond what was thought possibleduring the preparation of the Fifth Plan. Current finds are all in NorthernThailand. Three small oil fields in the Fang area currently yield about400 bpd, while production at Sirikit is expected to begin in 1983 at a rate of5,000 bpd, increasing to 8,000 bpd by the! end of 1983, and to 17,000 bpd by1986. Subject to positive results elsewhere in the concession productionmay reach 50,000 bpd by late 1990s. Finally, oil shae deposits have been

2-

found in Tak province near the Burmese border, which could yield anestimated 10 million tons of oil. The Department of Mineral Resources, withthe assistance of the German Government, has initiated studies to determinethe technical feasibility and economic viability of developing these oilshale resources. At present prices, however, oil shale development isunlikely to be economically viable.

Lignite Reserves

1.04 Substantial increases in Thailand-s lignite deposits have beenindicated by recent drillings. Lignite is relatively uneconomical to trans-port because of its high moisture and ash content, while :Lts tendency todecompose and self-ignite in open air makes it unsafe to store. Hence, inThailand as elsewhere, lignite is used almost exclusively for large-scalepower generation at the mine site. The present lignite reserves totalling770 million metric tons (mt) are located at Mae Moh (650 million mt), Krabi(100 million mt), and Li (20 million mt). Of the reserves at Mae Moh, 350million mt are proven and probable reserves, sufficient to sustain a totalgenerating capacity of about 1,725 MW for about 25 years. It is estimatedthat by 1990, about 25% of EGAT's total generation would be from lignitefired thermal stations.

Hydro Potential

1.05 The total hydropotential of Thailand's rivers is estimated at about9,300 MW, not including the international rivers (Mekong aLnd Salween), whosedevelopment of 25,000 MW is currently beyond reach due to major politicaland social obstacles. About 1,380 MW of hydropower are now in operation,2,100 MW are under construction, and about 2,500 MW in 25 projects are at astage of identification or feasibility study. Mini-hydro potential isestimated at about 3,290 MW at over one hundred sites. According to currentplans, hydropower production will increase at an average annual rate ofabout 13% between 1981 and 1995.

Other Energy Resources

1.06 Thailand's other energy resources include fuelwood and possiblygeothermal energy. Fuelwood resources, once plentiful, are rapidlydepleting and deforestation is becoming a serious problem. Geothermalexploration is being carried out by EGAT in the northern part of Thailandnear Chiangmai.

Energy Supply Alternatives

1.07 Prospects for reducing Thailand's dependence on imported energy inthe 1980s are good, at least for its electricty sector. The Government'spolicy is to reduce Thailand-s dependence on imported energy by (a) develop-ing indigenous energy resources such as natural gas, lignite and hydro potenr-tial; (b) pursuing a rational pricing policy; and (c) conservation programs.

-3-

Based on the development of natural gas and lignite resources proven to dateand on the continued expansion of its hydro potential, Thailand should beable to reduce its share of imported energy for the electricity sector fromabout 71% in FY81 to less than 20% in FY90. However, without a substantialincrease in the natural gas and lignite reserves or the development ofinternational hydro potential, Thailand will re-emerge in the 1990s as amajor importer of energy for its power sector. In the other large energyconsuming sectors, i.e., transportation and industry, the prospects forconverting to other forms of energy are rather limited in the near term.Thus, there is a need to focus on curtailing energy demands and encouraginggreater energy conservation.

C. Energy Investment Program.

1.08 The Thai Government reacted in recent years to the growing energydemands of the Thai economy, the increased cost of foreign supplies, and thediscovery of domestic energy resources by rapidly expanding its expenditure,especially capital spending, in the energy sector. This expansion has beenparticularly rapid since 1980, with the result that energy is now thesingle most important sector for public spending, having increased its shareof total public expenditure from 12.5% in 1977 to 22.1% in 1981. For theFifth Plan period, NESDB projects that the energy sector will contributeabout 26% to total governmental spending, up from the average of 18% duringthe Fourth Plan period. Energy sector spending weighs even more heavilyin total public investment, reaching a share of 31.9% in 1981, up from 13.5%in 1970 and 13.7% in 1977. As a percent of state enterprise investment,the energy sector enterprises have in recent years accounted for more than50% and are expected to do so during the Fifth Plan period. Four agenciesin particular have contributed the bulk of these investments: EGAT accountedfor 55-75% of total public investment in the energy sector, MEA for 5-15%,and PEA for 10-25%. PTT-s investments were minor as recently as 1979, butwere very sizable in 1980 and 1981, when they accounted for almost a quarterof total public investments in the energy sector in connection with theconstruction of the gas pipeline. For the Fifth Plan period, EGAT isexpected to retain its large share in energy spending, with PTT continuingto grow in importance as it is involved in further gas and oil developmentand utilization projects.

D. Role of the Power Sector in the Economy

1.09 Electricity revenue accounts for only about 1.9% of GDP. However,electricity provides motive power to the manufacturing and mining industrieswhich account for 20.8% and 1.7% of GDP respectively.

1.10 The growth of the power sector has kept pace with Thailand'seconomic development. Between FY76 and 81, when GDP grew at an average rateof about 7.3% in real terms, total electricity consumption grew at an averagerate of about 9.9%.

-4-

E. The Power Sector Organization

General

1.11 The power sector consists of eight government agencies (para.1.18), three state utilities, the ministries to which they report, and foursmall private franchises (para. 1.17). The three state utLilities supplynearly all of the electricity consumed in the country, the privatefranchises and self-generating industries represented 12.9% of the installedcapacity in FY81 (Table 1.1).

1.12 The state-owned utilities are EGAT, the Metropo:Litan ElectricityAuthority (MEA), and the Provincial Electricity Authority (PEA). Highlightsof the EGAT, MEA and PEA operations are shown in Annex 1.

The Electricity Generating Authority of Thailand (EGAT)

1.13 EGAT was established in 1968 as a wholly-owned Government corpora-tion for the purpose of increasing the efficiency of electricity supplythroughout the country and coordinating the generation and transmissionsystems and is responsible to the Prime Minister's Office. EGAT generated94.6% of all electric energy in Thailand in FY81; the balance was generatedby PEA, NEA, private franchises and self-generating industries and a smallamount was purchased from Laos and Malaysia.

The Metropolitan Electricity Authority (MEA)

1.14 MEA was established in 1958 as a wholly-owned Government corpora-tion under the Ministry of Interior with responsibility for supplying elec-tricity to the Bangkok Metropolitan Area covering the provinces of Bangkok,Thon Buri, Nonthaburi and Samut Prakon. In FY81, 8,182 GW'h were sold to793,000 consumers. Compared with FY80, energy sales and number of consumersincreased by 4.0% and 7.4% respectively. Distribution losses were about3.7% in FY81. All of MEA's power is purchased from EGAT. The Bank hasnever been asked to assist MEA, as foreign funds requirements were providedby the Asian Development Bank (ADB) and commercial banks, in the past.

The Provincial Electricity Authority (PEA)

1.15 PEA was established in September 1960 as a wholly-owned Governmentcorporation under the Ministry of Interior with responsibility for providingand distributing electricity in all provinces of the country except in theareas served by MEA. PEA purchases most of its energy in bulk from EGAT butalso generates small quantities in areas not yet connected to the grid. InFY81, PEA purchased 5,761 GWh and generated 45 GWh; 5,210 GWh were sold to2.3 million consumers. Compared with FY80, GWh sold and the number of con-sumers connected increased by 11.0% and 20.4%, respectively. System losseswere about 10.2% in FY81. This is acceptable considering the size and loaddensity of its service areas.

- 5 -

1.16 PEA is the Government agency responsible for implementing theaccelerated rural electrification program (para. 1.29). The program onlysubstantially began with Loan 1527-TH made by the Bank to PEA in 1978 for thefirst major phase which will provide electricity to about 4,560 villages bythe end of 1983. Another loan (1871-TH) was made in 1980 to assist in theelectrification of about 7,800 villages by 1986.

Private Franchises

1.17 Following the fuel crisis and the Goverrment's policy of restrict-ing tariff increases, most of the franchises asked to be taken over by PEA.Since FY76, 52 franchises have been purchased leaving four in private handsat the end of FY81; two of them purchase their power needs in bulk from PEAand one directly from EGAT. The remaining franchise had an installedcapacity of only 18 KW and generated 11.5 MWh in FY81.

Government Agencies

1.18 Eight Government agencies which have a direct interest in thepower sector: Committee for Power Policy and Development (CPPD); BudgetBureau; Tariff Rate Committee (TRC); National Economic and Social DevelopmentBoard (NESDB); Ministry of Finance (MOF); National Energy Administration(NEA); Foreign Loan Committee (FLC); and Petroleum Authority of Thailand(PTT). These agencies review: tariff recommendations; capital projectproposals and budgets for submission to the Council of Ministers; annualfinancial performance; and requests for Government equity and loans. Noneof them has overall policy responsibility; decisions on the sector arearrived at after all the agencies including the state utilities reach aconsensus. The system is designed to ensure that sector capital expendituresare rigidly controlled. The interest of PTT in the sector arises from thefact that EGAT, as the utility responsible for generation, will be for sometime to come, the predominant customer for natural gas and is the largestcustomer for fuel oil.

F. Power Sector Coordination

1.19 Coordination among the different government agencies concernedwith the electricity subsector is achieved through close working relation-ships promoted by two separate arrangements. The first is the Load ForecastWorking Group, made up of representatives from the NESDB, the NEA, EGAT, PEAand MEA. The working group ensures that the subsector market developmentand the utilities' investment program requried to support it are consistentiP size, technical characteristics and timing. The second arrangement ismanifested by the current procedure for setting electricity rates wherebyattention is given to the cross-funding necessary to ensure that eachutility generates an adequate proportion of its capital investment and toprevent cash imbalances among EGAT, PEA and MEA.

-6-

1.20 The Government has been promoting further subsector coordinationin other ways. In 1977, the CPPD was formed to oversee the functioning anddevelopment of the subsector and to provide overall coordination. Inrecognition of the importance of energy issues, the Ministry'of Science,Energy and Technology was established in 1979. Coordination in the powersubsector is satisfactory while possibilities for further strengthening ofpolicy coordination of the energy sector as a whole are being pursuedthrough continuing dialogue with the Government and under the StructuralAdjustment loans to Thailand.

G. Tariff Levels

1.21 Tariff levels were adequate throughout the late 1960s and the early1970s, and the financial position of the sector remained strong. Duringthat period, the electricity sector enjoyed substantial economies of scalethrough shifts to hydroelectric and large steam generation coupled withrapid increases in the demand and number of consumers. Tariffs were reducedfrom time to time during these years. However, the fuel crisis and economicslowdown of 1973/74 necessitated large increases in tariffs, but only par-tial adjustments were politically feasible.

1.22 Severe droughts in 1977 and 1978 adversely affected the thermal/hydro generation mix, while in 1979 fuel oil prices increased some 115%.In an attempt to prevent higher energy costs from accelerating inflation,the Government chose to delay passing the rising costs of electricity toconsumers. By mid-1979, the Government, faced with mounting criticism ofits handling of the economy, introduced direct budgetary subsidies on elec-tricity tariffs, costing an estimated $9.0 million a month. In 1980, how-ever, the government agreed to a Plan of Action to remove subsidies andrestore the sector's financial viability, in connection with EGAT-s Mae MohLignite Project (Loan 1852-TH). This plan was implemented through asurcharge for heavy consumers established in August 1980 and tariffincreases in October 1980, January 1981 and April 1981. Thus, despite adifficult political climate and rapid inflation, the Government implementedoverall increases in EGAT's electricity tariff of 158% between February 1980and April 1981, and eliminated oil subsidies.

1.23 The present tariff structure contains a substantial subsidy fromlarge consumers in favor of small consumers. Although in general this isdesirable, tariffs for lower brackets group of residential consumers areunnecessarily low. As mentioned in para. 5.02, this is affecting PEA'searning power. Both PEA and the Government are aware of this situation.A Subcommittee on Tariff Structure was formed recently to look into thismatter. It is expected that adjustments will be gradually introduced asthe political and social realities of the country allow thLem.

-7-

H. Bank Participation in the Sector

1.24 The Bank has made two loans totalling US$100 million to PEA tofinance its Accelerated Rural Electrification Projects, and eleven loans toEGAT and its predecessor totalling US$542 million to help finance powerplants and transmission facilities. Another loan of US$72 million (Loan1852-TH, Mae Moh Lignite Project) was made to EGAT in June 1980 for ligniteproduction. The first eight projects made to EGAT have been completed andare operating satisfactorily. The Ninth Power Project (Loan 1690-TH, 550 MWBang Pakong Thermal Power Project) is about 46% complete. The Tenth PowerProject (Loan 1770-TH, Khao Laem Hydroelectric Project) is about 43%complete. The last loan (US$100 million) to EGAT was the Power SubsectorProject (Loan 2000-TH) which was approved by the Bank on May 21, 1981 andbecame effective on October 26, 1981. PEA's first Accelerated RuralElectrification Project (Loan 1527-TH) of $25.0 million became effective inJune 7, 1978. Of a total of 4,560 villages, 2,970 have been electrified andin another 1,060 villages construction and installation work has started. Aloan of US$75 million for PEA's Second Accelerated Rural ElectrificationProject (Loan 1871-TH) was made in FY80 but did not become effective untilAugust 20, 1981 due to delays in complying with cross-effectivenessrequirements with co-lenders. The project will cover about 7,800 villages;construction has started in the first 480 villages. Continuation of Bankfinancial assistance to PEA's development program is considered necessary topursue the support to improvements in PEA's operation.

I. Power Market and Supply

1.25 Annex 1 presents the highlights of EGAT, PEA and MEA operations.As shown in Table 1.1, at the end of FY81 EGAT represented about 83% of thecountry-s generating capacity.

Table 1.1: THAILAND - INSTALLED CAPACITY BY OWNERSHIP AT END OF FY81

Ownership Irnstalled capacity (MW) %

EGAT 3,808.4 82.8PEA & NEA 199.1 4.3Private franchises - /a -Self-generating industries 594.1 12.9

Total 4,601.6 100.0

/a With an installed capacity of 18 KW only.

-8-

1.26 From the viewpoint of sources of electricity (Table 1.2), in FY81thermal plants represented more than half of Thailand's installed capacityand generated three fourths of the total electricity available. About 71%of the electricity generated during FY81 came from imported sources ofenergy.

Table 1.2: THAILAND - DISTRIBUTION BY SOURCES OF GEIERATING CAPACITYAT THE END OF FY81 AND ENERGY AVAILABLE IN FY81

Generating capacity Energy availableSource MW % Gah %

Steam plants 2,280.8 49.6 12,574.3 74.5Hydro plants 1,361.1 29.6 2,974.4 17.6Gas turbines 610.0 13.2 383.5 2.3Diesel 349.7 7.6 200.1 1.2Purchased /a - - 739.9 4.4

Total 4,601.6 100.0 16,872.2 100.0

/a From Electricite du Laos (EDL) (Laos) and National ElectricityBoard (NEB) (Malaysia).

1.27 Total electricity consumption was 13,845 GWh in FY81 or 289 kWh percapita; 3,192.6 GWh (23.0%) were used by residential consumers; 1,564.4 GWh(11.3%) by commercial consumers; 8,968.1 Gwh (64.8%) by industrial consumersand 119.9 GWh (0.9%) by street lighting and others. Total losses were about17.9% including station services.

J. Degree of Electrification

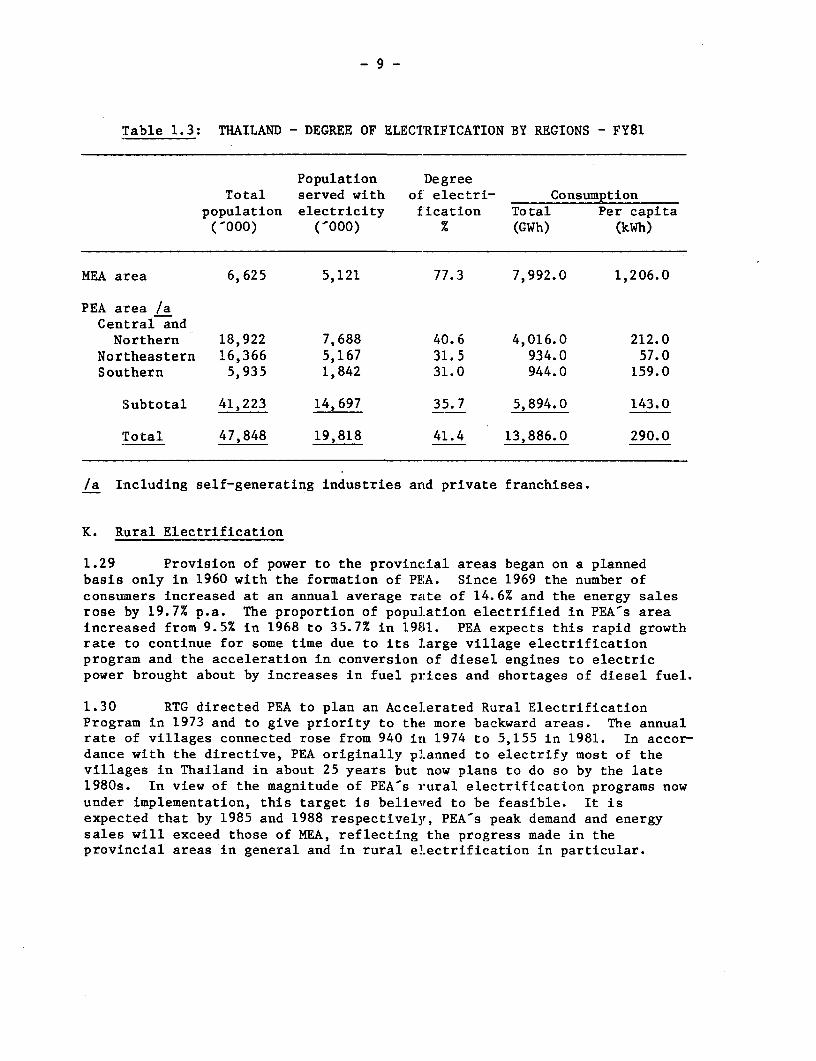

1.28 Regional imbalances exist in the degree of electrification as wellas in per capita consumption as presented in Table 1.3.

- 9 -

Table 1.3: THAILAND - DEGREE OF ELECTRIFICATION BY REGIONS - FY81

Population DegreeTotal served with of' electri- Consumption

population electricity f'ication Total Per capita('000) ('000) % (GWh) (kWh)

MEA area 6,625 5,121 77.3 7,992.0 1,206.0

PEA area /aCentral andNorthern 18,922 7,688 40.6 4,016.0 212.0

Northeastern 16,366 5,167 31.5 934.0 57.0Southern 5,935 1,842 31.0 944.0 159.0

Subtotal 41,223 14,697 35.7 5,894.0 143.0

Total 47,848 19,818 41.4 13,886.0 290.0

/a Including self-generating industries and private franchises.

K. Rural Electrification

1.29 Provision of power to the provincial areas began on a plannedbasis only in 1960 with the formation of PEA. Since 1969 the number ofconsumers increased at an annual average rate of 14.6% and the energy salesrose by 19.7% p.a. The proportion of population electrified in PEA's areaincreased from 9.5% in 1968 to 35.7% in 1981. PEA expects this rapid growthrate to continue for some time due to its large village electrificationprogram and the acceleration in conversion of diesel engines to electricpower brought about by increases in fuel prices and shortages of diesel fuel.

1.30 RTG directed PEA to plan an Accelerated Rural ElectrificationProgram in 1973 and to give priority to the more backward areas. The annualrate of villages connected rose from 940 in 1974 to 5,155 in 1981. In accor-dance with the directive, PEA originally planned to electrify most of thevillages in Thailand in about 25 years but now plans to do so by the late1980s. In view of the magnitude of PEA-s rural electrification programs nowunder implementation, this target is believed to be feasible. It isexpected that by 1985 and 1988 respectively, PEA's peak demand and energysales will exceed those of MEA, reflecting the progress made in theprovincial areas in general and in rural electrification in particular.

- 10 -

L. Project Performance Audits

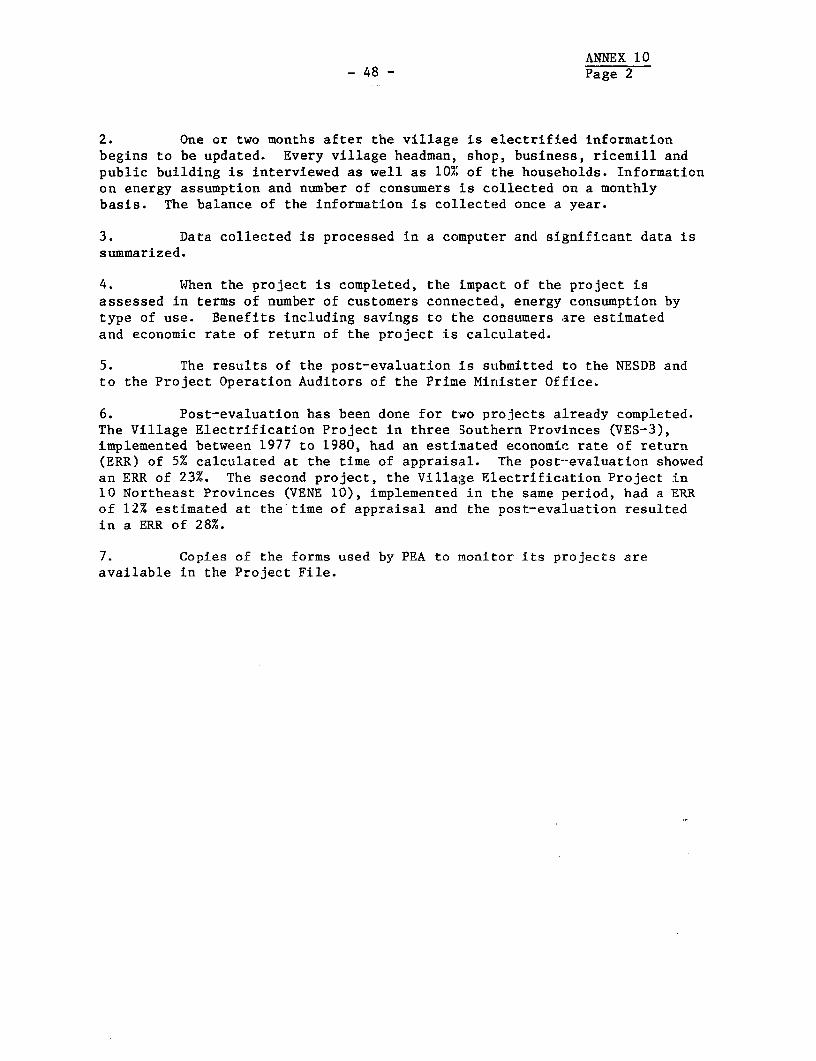

1.31 To date no project performance audit reports (PPAR) have been pre-pared in respect to PEA's operations. PPARs have been prepared on three ofthe early loans to EGAT, the First Power Project (Loan 65i5-TH), the SouthBangkok Thermal Unit No. 4 Project (Loan 790-TH) and the Ban Chao Nen(Srinagarind) Hydroelectric Project (Loan 977-TH). The PPARs concluded thatthe major objectives of the project had been met. EGAT complied with allthe covenants, and its financial performance was satisfactory.

1.32 PEA has conducted its own post-evaluation of two projects alreadycompleted (not financed by the Bank). Both projects met or exceeded theirobjective and had Economic Rates of Return in excess of 23%.

II. THE BORROWER

2.01 The Borrower would be PEA, established in September 1960 underthe Provincial Electricity Act (BE2503) as a state enterprise reporting tothe Ministry of Interior. PEA is responsible for the distribution ofelectricity throughout the country except in the Metropolitan Bangkok areawhich is served by MEA. At the end of FY81, PEA had 965 offices grouped intwelve regional areas. In FY81 96% of PEA energy requirements werepurchased from EGAT, about 3% from MEA and NEA and the balance generatedfrom diesel plants.

A. Organization and Management

2.02 PEA's Board of Directors is appointed by the Council of Ministersand consists of up to nine members. For its operations, PEA is organizedinto three functional areas: Administration, Operations and Techniques,each headed by a Deputy General Manager. In addition, there is a smallstaff of senior officials who act as assistants to the General Manager.Annex 2 presents PEA's organization chart.

2.03 During the past five years PEA has experienced a rapid growth.The number of customers has more than doubled, the annual investment programhas increased threefold and revenues from sales in FY81 were about fourtimes those of FY77. It is expected that this pace will continue in thecoming four or five years in order to meet the RTG rural electrificationtargets.

2.04 Early in 1982 PEA retained a group of professors from a localuniversity to prepare a diagnosis of its operations and to indicate theadjustments required to improve PEA's efficiency in handling its growingvolume of activity. The diagnosis, in summary, shows that PEA needs totake actions to:

- 11 -

(a) strengthen the corporate planning system;

(b) modernize procedures for planning, purchasing and controllingconstruction materials;

(c) improve coordination in project planning and implementation;

(d) modernize the billing and collection procedures and improvecash management;

(e) strengthen and expand PEA's internal controls;

(f) improve budgeting and planning procedures; and

(g) modernize the electronic data processing equipment and expandits applications.

2.05 As part of the project, PEA is taking action to introduce adjust-ments in its operations to improve its efficiency (para. 4.14).

B. Manpower and Training

2.06 PEA personnel is experienced and well qualified. Table 2.1 showsthe growth of staff and the break-down by academic qualifications during thelast five years. Although the number of employees has grown at about thesame rate as the number of customers, the sales per employee has decreasedslightly reflecting the characteristics of PEA's expansion program.

2.07 PEA operates a modest training center which in FY81 trained about1,100 lower level staff. In addition, staff is trained in local and foreignuniversities. PEA is aware that, as the butlk of its rural electrificationis completed in 1986-87, its main activity will shift from construction tooperation and maintenance. This change will be reflected in the require-ments of PEA's work force. The Bank has provided guidance to PEA on thepreparation of a training program which is expected to be part of PEA'sinstitutional development program (para. 4.14).

- 12 -

Table 2.1: PEA-S STAFF BY CATEGORIES 1977-81

Averageannualgrowth

Category 1977 1978 1979 1980 1981 (%)

University graduates 677 775 869 990 1,098 12.8Technical diploma 1,057 1,313 1,636 2,00'5 2,326 21.8Vocational certificate 2,792 3,436 4,169 4,800 6,029 21.2Others 4,357 5,070 5,600 6,515 6,809 11.8

Total 8,883 10,594 12,274 14,310 16,262 16.3

Customers per employee 129 127 128 131 139Mwh sales per employee 357 344 346 332 320

C. Billing and Collections

2.08 Billing is made in the 12 regional offices usirLg electricaccounting machines which, although efficiently operated, lack the requiredmemory to properly record accounts receivable and are slow for the presentvolume of operations. A mini-computer is planned to be installed in ChiangMai as a pilot project to develop procedures to modernize PEA's billingsystem. PEA-s collections are efficient. Accounts receivable at the end ofFY81 represented 42 days of billings in spite of the slow collection fromGovernment entities. During negotiations, the Government agreed to makearrangements for the prompt payment of electricity bills rendered by PEA toits departments and agencies.

D. Accounting and Audit

2.09 The accounting system is adequate and the staff are competent.Accounting is carried out centrally in Bangkok, supported by 12 regionalaccounting centers.

2.10 PEA'a accounts are audited by the National Audit Council (NAC),the government entity responsible for auditing all state enterprises inThailand. In 1979 the Bank reviewed the auditing standards of the NAC asapplied to PEA. Most of the recommendations made at that time have beenimplemented. Nevertheless, there are translation difficulties which haveresulted in delays in the presentation of the auditors reports to the Bankand lack of clarity in some portions of the same. This situation will befollowed closely in the future to determine if alternative arrangements areneeded.

- 13 -

2.11 The head of the internal audit office reports directly to thegeneral manager. It is expected that as part of the activities mentioned inpara. 4.14, PEA will review its internal control procedures in order tobring them in line with the present complexity of its operations.

E. Taxes

2.12 PEA pays custom duties (from 8% t:o 40%) on imported material andequipment. Its Act also provides that any surplus funds be remitted toGovernment in lieu of corporate tax. Due to the size of PEA's investmentprogram and its needs for funds, PEA has not made any remittances and is notexpected to do so in the future.

F. Insurance

2.13 PEA carries adequate insurance protection against fire forbuildings and their contents. No third party liability insurance iscarried. This is the generalized practice in most public enterprises inThailand and given the characteristics of the risk for PEA it isacceptable. Insurance policies are reviewed and updated once a year.

G. Existinig Facilities

2.14 The energy sold to PEA from EGAT's 81 substations is distributedby PEA in 69 provinces by a radial type of distribution system of 11, 22 and33 kV design. PEA steps the high tension voltage down to low tension at400/230 volt, 3-phase, 4-wire; 230 volt, 1-phase, 2 wire or 460/230, 1phase, 3-wire (including one neutral) for supplying the energy tocustomers. Medium sized business and industrial loads are supplied at thevoltage level of 11, 22 or 33 kV.

2.15 At the end of FY81, the electric distribution systems in PEAservice areas totaled 50,650 circuit-km of primary distribution lines and3,538 MVA of transformer capacity.

III. PEA's POWER MARKET

A. Background

3.01 PEA-s market covers all of Thailand except the Metropolitan Bangkokarea which is served by MEA.

- 14 -

Table 3.1: PEA - SALES BY CATEGORY OF CUSTOMEE'S - FY81

Number of Salesconsumers GWh %

Residential 2,230,216 1,582.1 30.4Small business 28,060 528.6 10.2Large business 1, 586 537.7 10.3Small industrial 1,897 935.0 18.0Large industrial 196 1,517.6 29.0Irrigation 256 18.4 0.3Street lighting 2,569 19.8 0.4Others 5,589 70.5 1.4

Total 2,270,369 5,209.7 100.0

3.02 PEA's power market has had a long history of rapid growth, theaverage annual increase in peak demand and energy sales being 16% and 19.7%,respectively, over the period FY70-81. Growth was stimulated by an expandingeconomy and Government's emphasis on improving the standard of living inthe rural areas. A breakdown of PEA's sales is shown in Table 3.1 and PEA'sgrowth rates in energy sales and peak demand are presented in Table 3.2.Annex 3 presents the historical evolution of PEA's market by type ofconsumption as well as the growth of different groups of customers.

- 15 -

Table 3.2: PEA - HISTORICAL SALES 1969-1981

Energy sales Peak demand

Fiscal year GWh increase MW increase

1969 601.8 - 199.5 -1970 769.4 27.8 222.4 11.41971 924.3 20.1 269.4 21.11972 1,211.4 31.L 327.6 21.61973 1,557.4 28.6 375.1 14.51974 1,779.2 14.2 433.2 15.51975 2,120.0 19.2 516.9 19.31976 2,616.7 23.4 640.1 23.81977 3,174.4 21.3 740.8 15.71978 3,649.6 14.9 851.7 15.01979 4,253.7 16.5 949.1 11.41980 4,695.8 10.4 1,040.1 9.61981 5,209.7 10.9 1,180.7 13.5

Average FY70-81 19.7 16.0

B. PEA's Load Forecast

3.03 PEA's load -orecast is normally reviewed at least once a year. Itis derived from a study of trend analysis of sales to different categoriesof consumers, market surveys of new industries and the rural electrificationprogram. The review is carried out by the Load Forecast Working Group(LFWG) which is chaired by NESDB and consist of Representatives of NEA andthe three utilities.

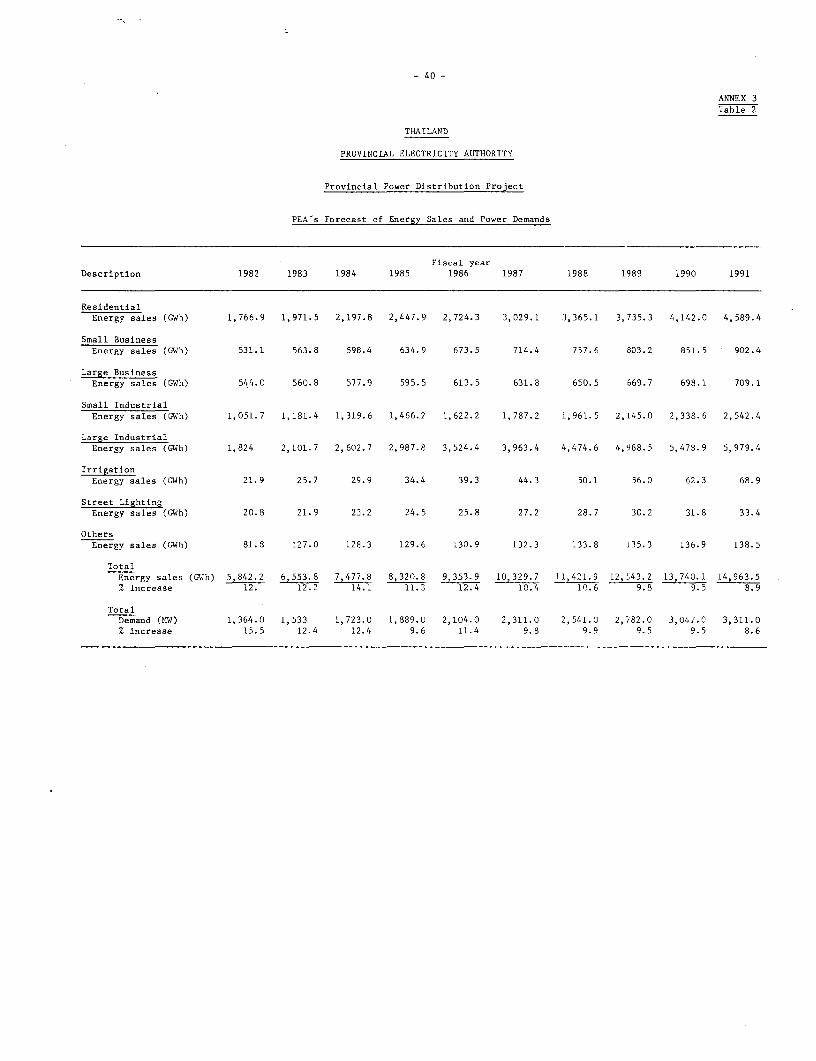

3.04 The Bank considered that the June 1982 forecast prepared bythe LFWG did not fully take into account the recent demand slowdown.Accordingly, it was revised slightly downwards. The revised forecast issummarized in Table 3.3 and presented in detail in Annex 3.

- 16 -

Table 3.3: PEA - LOAD FORECAST 1982-1991

Energy sales Peak demand

Fiscal year GWh increase MW increase

1982 5,842 12.1 1,364 15.51983 6,553 12.2 1,533 12.41984 7,478 14.1 1,723 12.41985 8,321 11.3 1,889 9.61986 9,354 12.4 2,L04 11.41987 10,330 10.4 2,311 9.81988 10,422 10.6 2,541 9.91989 12,543 9.8 2,782 9.51990 13,740 9.5 3,047 9.51991 14,963 8.9 3,311 8.6

Average FY82-91 11.0 10.3

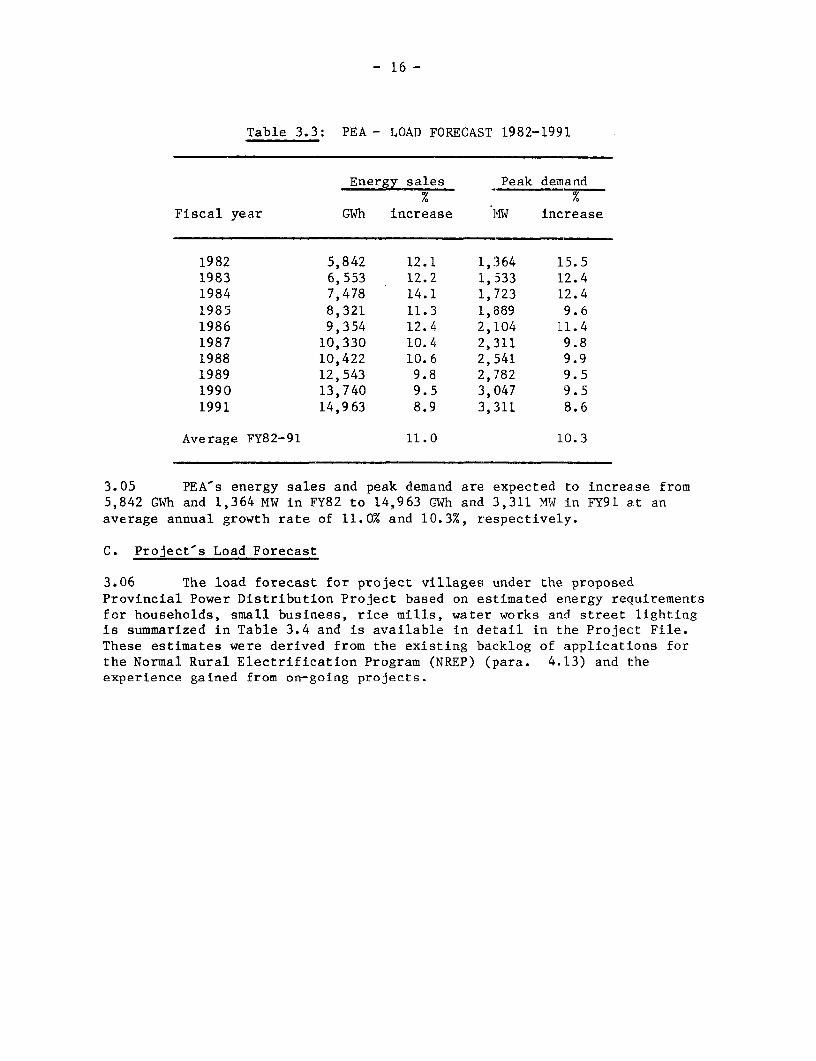

3.05 PEA's energy sales and peak demand are expected to increase from5,842 GWh and 1,364 MW in FY82 to 14,963 GWh and 3,311 MW in FY91 at anaverage annual growth rate of 11.0% and 10.3%, respectively.

C. Project's Load Forecast

3.06 The load forecast for project villages under the proposedProvincial Power Distribution Project based on estimated energy requirementsfor households, small business, rice mills, water works and street lightingis summarized in Table 3.4 and is available in detail in the Project File.These estimates were derived from the existing backlog of applications forthe Normal Rural Electrification Program (NREP) (para. 4.13) and theexperience gained from on-going projects.

- 17 -

Table 3.4: PEA - NORMAL RURAL ELECTRIFICATION - LOAD FORECAST

Energy Peakrequirement demand Load

Year (GWh/year) (MW) factor

1 18.8 19.5 11.02 64.9 46.8 15.83 118.1 77.6 17.44 176.4 115.8 17.45 232.2 143.9 18.4

10 445.6 242.8 21.015 655.4 317.9 23.520 907.5 409.0 25.325 1,189.4 499.7 27.230 1,497.9 581.3 29.4

3.07 Energy requirements in the project villages are expected toincrease from about 19 GWh in FY 1983 to 1,498 GWh in FY 2012, an averageannual growth rate of 16%; and peak demand from about 20 MW in FY 1983 toabout 580 MW in FY 2012, an average annual growth rate of 12.4%. Growth isexpected to be rapid in the early years and would then taper off as connec-tion of the majority of the premises (about 80% of households) is achievedby FY 1993.

IV. THE PROGRAM AND THE PROJECT

A. PEA's Development Strategy

4.01 PEA's electrification strategy envisages development of the sectorin four consecutive stages: L.ist to electrify provincial centers and majorcities; second district centers; third, TAMBON /1 centers and fourth ruralvillages. The first two stages are completed and an effort is now beingdirected towards the last two. At the end of FY81 about 24,000 (46%) out ofa total of 52,000 villages had electricity.

/1 Thailand's lowest administrative unit consisting of a group ofvillages.

- 18 -

4.02 In developing its system PEA undertakes two groups of activities:

(a) the Power Distribution System Reinforcement program, toimprove the capacity and reliability of the backbone distributionsystem; and

(b) the Village Electrification Programs, to extend the electricservices to the population in rural areas.

4.03 There are three types of village electrification programs currentlybeing carried out by PEA: (a) Projects prepared to address the need forelectrification on a regional basis, PEA selects the villages to be electri-fied under each particular project. This group includes the First and SecondAccelerated Rural Electrification Projects (ARE I, ARE II) and the VillageElectrification Project (VEP); (b) the TAMIBON project (TEP) is intended togive power to all TAMBON headquarters and surrounding villages that can beconnected at a reasonable cost; and (c) the Normal Rural ElectrificationProgram (NREP), carried out by the regional offices connecting villageswhich are not included in other programs and request to be electrified. Inaddition, the NREP extends the electric services to groups of households invillages partially electrified under other projects.

4.04 In the past, the extension of PEA-s system has been carried outon a piecemeal basis under different projects. As part of a program forinstitutional development, PEA is planning to start a process of modernizingits Distribution System Planning in order to improve reliability, safety andeconomy (para 4.14).

B. PEA's Development Program

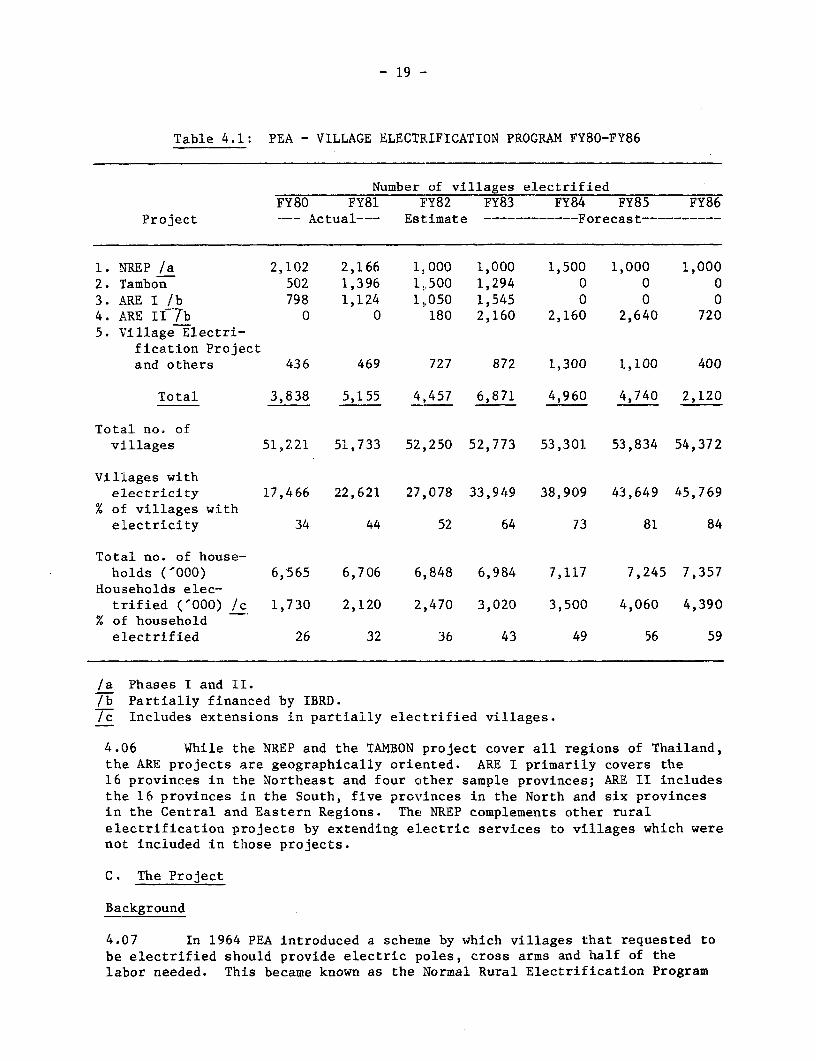

4.05 Under the National Plan for Total Electrification of Thailand,approved by the Council of Ministers on August 28, 1973 PEA orginally plannedto electrify all villages in Thailand in about 25 years. Later PEA embarkedon a greatly accelerated program which plans to reach most villages by thelate 1980s. A summary of the projects undertaken by PEA is presented inAnnex 4 and PEA's Village Electrification Program is shown in Table 4.1, andMap IBRD 16683 shows the regional distribution of PEA's rural electrificationprojects.

- 19 -

Table 4.1: PEA - VILLAGE ELECTRIFICATION PROGRAM FY80-FY86

Number of villages electrifiedFY80 FY81 FY82 FY83 FY84 FY85 FY86

Project --- Actual--- Estimate ------------Forecast----------

1. NREP /a 2,102 2,166 1,000 1,000 1,500 1,000 1,0002. Tambon 502 1,396 1,500 1,294 0 0 03. ARE I /b 798 1,124 1,050 1,545 0 0 04. ARE II7 b 0 0 180 2,160 2,160 2,640 7205. Village Electri-

fication Projectand others 436 469 727 872 1,300 1,100 400

Total 3,838 5,155 4,457 6,871 4,960 4,740 2,120

Total no. ofvillages 51,221 51,733 52,250 52,773 53,301 53,834 54,372

Villages withelectricity 17,466 22,621 27,078 33,949 38,909 43,649 45,769

% of villages withelectricity 34 44 52 64 73 81 84

Total no. of house-holds ('000) 6,565 6,706 6,848 6,984 7,117 7,245 7,357

Households elec-trified ('000) /c 1,730 2,120 2,470 3,020 3,500 4,060 4,390

% of householdelectrified 26 32 36 43 49 56 59

/a Phases I and II./b Partially financed by IBRD./c Includes extensions in partially electrified villages.

4.06 While the NREP and the TAMBON project cover all regions of Thailand,the ARF projects are geographically oriented. ARE I primarily covers the16 provinces in the Northeast and four other sample provinces; ARE II includesthe 16 provinces in the South, five provinces in the North and six provincesin the Central and Eastern Regions. The NREP complements other ruralelectrification projects by extending electric services to villages which werenot included in those projects.

C. The Project

Background

4.07 In 1964 PEA introduced a scheme by which villages that requested tobe electrified should provide electric poles, cross arms and half of thelabor needed. This became known as the Normal Rural Electrification Program

- 20 -

(NREP) (para. 4.03). Tn recent years the practice has been for the villagesto make a monetary contribution equivalent to those materials and labor,which facilitates compliance with technical specifications. Thiscontribution represents about 25% to 30% of the project cost. The balancewas originally financed from government budget contributions. Later it wasdecided that subsidized domestic loans from the Krung Thai Bank and theMinistry of Finance to PEA should replace such grants.

4.08 The NREP is open-ended since it depends on applications fromvillages from all over the country. It complements other rural electrifica-tion projects. Typically villages under the NREP were not originally includedin other on-going programs because, at that time, they were too distant fromthe grid. However, since the transmission lines have been extended throughdifferent schemes, the electrification of these villages has become feasible.

4.09 During the last 4 years the NREP has electrified close to 9,000villages and extended electric service in another 2,000 partially electrifiedvillages.

4.10 In recent years, the demand for electrification under the NREP hasincreased but the availability to PEA of local loans, the major traditionalsource of financing for the NREP, has become scarce. In view of this, PEAstructured a five-year programr (1983 to 1987) which would facilitate accessto foreign sources of financing. Following the advise of the Nationaleconomic and Social Development Board (NESDB), the programa was divided in twophases. The first phase, to be implemented from 1983 to 1986 is expected tocover about 3,000 unelectrified villages and the extension of electricservice in another 3,000 partially electrified villages. The second phasewould electrify about 2,000 villages, expand the electric service in 2,000other villages and would be implemented from 1985 to 1987. To reduce itsfinancial cost, PEA decided to divide the First Phase into two identicalprojects to be implemented in parallel and to request the Bank to finance oneof them and the OECF of Japan to finance the other. (OECF interest rate is3.0% p.a. with a repayment period of 30 years including 10 years graceperiod).

Description

4.11 The proposed project has two parts. Part A, as explained above,constitutes the electrification of about 1,500 new villages and theextension of electricity to another 1,500 partially electrified villages.Part B, described in para. 4.14, includes the implementatlon of a group ofactions for strengthening PEA-s operations.

PART A - Village Electrification

4.12 The number of villages, extensions and households under IBRD andOECF projects and by phases are shown in Table 4.2. The estimatedquantities of the main components of the proposed Provincial Power

- 21 -

Distribution Project proposed to be financed by the Bank are presented inTable 4.3. Annex 5 shows the whole program..

Table 4.2 PEA - NORMAL RURAL ELECTRIFICATION PROGRAM (NREP) FY83-87

Number Number Number ofof of initial

villages households customers

Phase I (FY83-86)(a) IBRD

1. Unelectrified villages 1,500 175,000 94,0002. Extensions 1,500 45,000 33,000

(b) OECF Japan

1. Unelectrified villages 1,'500 175,000 94,0002. Extensions 1,500 45,000 33,000

Total Phase I 6,000 440,000 254,000

Phase II (FY85-87)

1. Unelectrified villages 2,000 234,000 126,0002. Extensions 2,000 60,000 44,000

Total Phase II 4,000 294,000 170,000

Total NREP 10,000 735,000 425,000

Subproject Selection Criteria

4.13 The following criteria was agreed during negotiations for selectingthe villages to be financed under the proposed loan. Subprojects with aninvestment cost per connection equal to or less than the average investmentcost of all the different rural electrification projects now being undertakenby PEA would be eligible for financing under the project. This averageinvestment cost is about B/.8,000 ($348) per connection at 1982 prices andwould be adjusted yearly for inflation. Subprojects exceeding that averagecost could be accepted provided they have an Economic Rate of Return (ERR) ofnot less than 10%. (PEA has developed a computer program to calculate the ERRusing the information routinely collected at the time of processing theapplications from the villages.) A preliminary review indicates that of thepresent backlog of 7,640 applications, (see Annex 6), about 5,400 villageshave a cost per connection lower than B/.8,000).

- 22 -

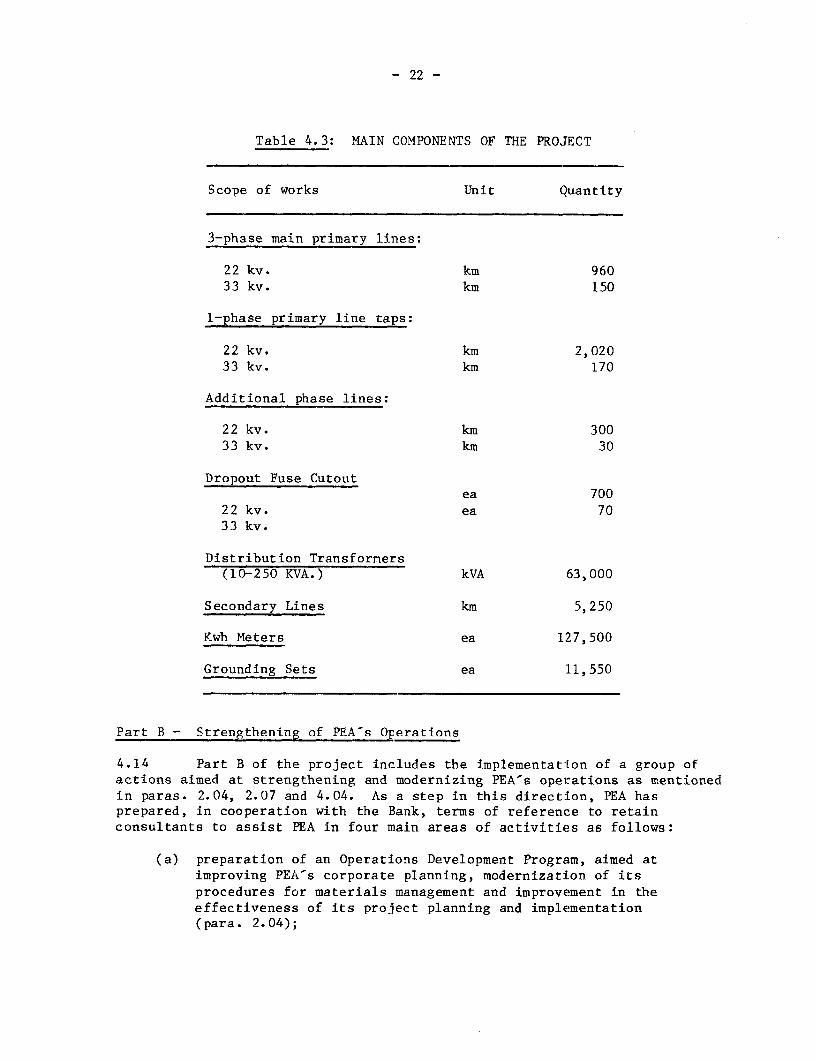

Table 4.3: MAIN COMPONENTS OF THE PROJECT

Scope of works Unit Quantity

3-phase main primary lines:

22 kv. km 96033 kv. km 150

1-phase primary line taps:

22 kv. km 2,02033 kv. km 170

Additional phase lines:

22 kv. km 30033 kv. km 30

Dropout Fuse Cutoutea 700

22 kv. ea 7033 kv.

Distribution Transformers(10-250 KVA.) kVA 63,000

Secondary Lines km 5,250

Kwh Meters ea 127,500

Grounding Sets ea 11,550

Part B - Strengthening of PEA's Operations

4.14 Part B of the project includes the implementation of a group ofactions aimed at strengthening and modernizing PEA's operations as mentionedin paras. 2.04, 2.07 and 4.04. As a step in this direction, PEA hasprepared, in cooperation with the Bank, terms of reference to retainconsultants to assist PEA in four main areas of activities as follows:

(a) preparation of an Operations Development Program, aimed atimproving PEA's corporate planning, modernization of itsprocedures for materials management and improvement in theeffectiveness of its project planning and implementation(para. 2.04);

- 23 -

(b) review of PEA's electronic data processing activities in orderto modernize them and to expand its applications;

(c) preparation of a Training Program to help develop PEA's staff andto make the necessary adjustments in PEA's manpower in responseto the changing role of the organization (para. 2.07); and

(d) preparation of a Distribution System Planning Program to improvethe reliability, safety and economy of PEA's distribution network(para. 4.04);

4.15 It is envisaged that the consultants will work closely with PEA'sstaff. Also, during the implementation process a good amount of training onthe job is expected.

4.16 The consultants cost is estimated at US$1.0 million. It providesfor 108 man-months of consulting services. The average man-months cost,including salary, costs, fees, international travel and subsistence isUS$9,200. PEA has requested a grant equivalent to US$1.0 million from theAustralian Development Assistance Bureau (ADAB). The Australian Governmenthas approved in principle this cofinancing.

4.17 During negotiations PEA agreed that in the unlikely event that bySeptember 30, 1983, the grant from ADAB has not materialized, PEA willfurnish to the Bank, by December 31, 1983, for Bank comments, a Plan ofAction. Such Plan would contain the alternate arrangements for introducingthe necessary adjustments in PEA-s operations to improve its overallefficiency. PEA also agreed that in such event, the Plan of Action would becarried out in a timely manner, taking into account the Bank's comments.

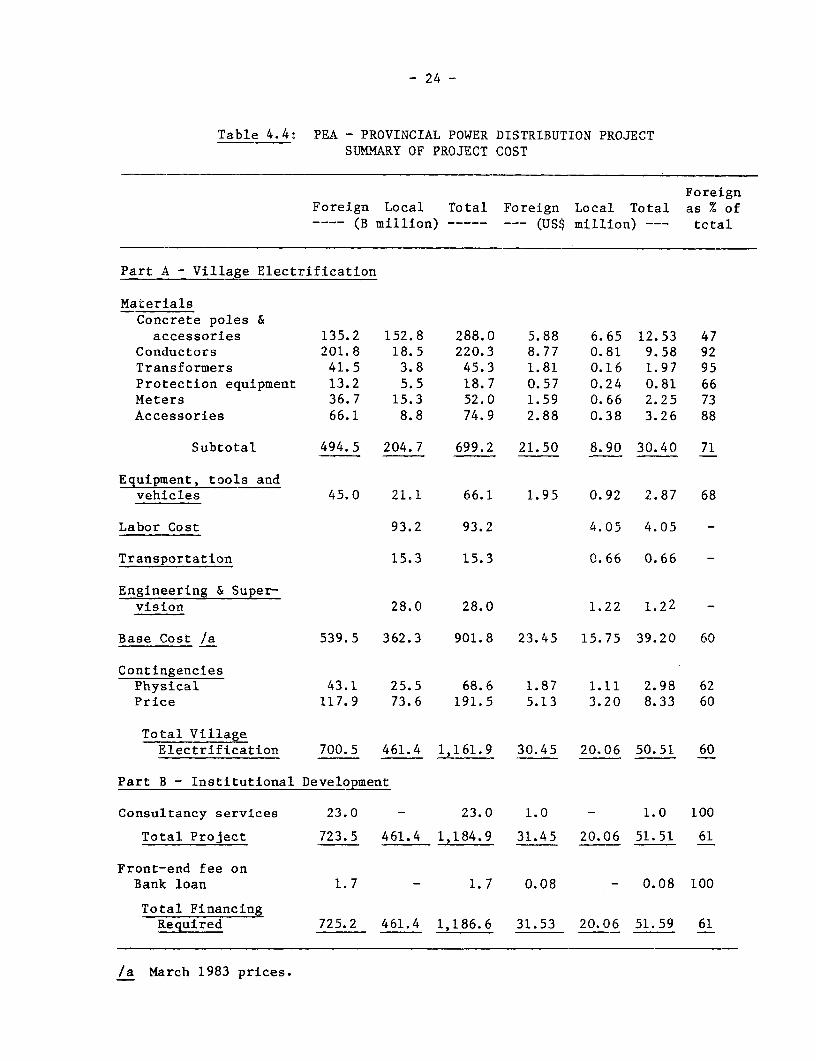

Cost Estimate

4.18 The cost estimate for the NRE Program was derived from the analysisof the existing backlog of applications for which surveys and cost estimateshave been prepared. Table 4.4 presents the total financing required for theproject, including the front-end fee on Bank loan. Annex 7 presents totalestimated costs for both Phase I and II.

- 24 -

Table 4.4: PEA - PROVINCIAL POWER DISTRIBUTION PROJECTSUMMARY OF PROJECT COST

ForeignForeign Local Total Foreign Local Total as % of

(B million) ----- --- (US'> million) --- total

Part A - Village Electrification

MaterialsConcrete poles &

accessories 135.2 152.8 288.0 5.88 6.65 12.53 47Conductors 201.8 18.5 220.3 8.77 0.81 9.58 92Transformers 41.5 3.8 45.3 1.81 0.16 1.97 95Protection equipment 13.2 5.5 18.7 0.57 0.24 0.81 66Meters 36.7 15.3 52.0 1.59 0.66 2.25 73Accessories 66.1 8.8 74.9 2.88 0.38 3.26 88

Subtotal 494.5 204.7 699.2 21.50 8.90 30.40 71

Equipment, tools andvehicles 45.0 21.1 66.1 1.95 0.92 2.87 68

Labor Cost 93.2 93.2 4.05 4.05 -

Transportation 15.3 15.3 0.66 0.66 -

Engineering & Super-vision 28.0 28.0 1.22 1.22 -

Base Cost /a 539.5 362.3 901.8 23.45 15.75 39.20 60

ContingenciesPhysical 43.1 25.5 68.6 1.87 1.11 2.98 62Price 117.9 73.6 191.5 5.13 3.20 8.33 60

Total VillageElectrification 700.5 461.4 1,161.9 30.45 20.06 50.51 60

Part B - Institutional Development

Consultancy services 23.0 - 23.0 1.0 - 1.0 100

Total Project 723.5 461.4 1,184.9 31.45 20.06 51.51 61

Front-end fee onBank loan 1.7 - 1.7 0.08 - 0.08 100

Total FinancingRequired 725.2 461.4 1,186.6 31.53 20.06 51.59 61

/a March 1983 prices.

- 25 -

4.19 Physical contingencies were assumed to be about 8% based on PEA'spast experiences in distribution projects. Price contingencies for foreigncosts were derived by applying the following annual rates of escalation: 8%for 1983, 7.5% for 1984, 7% for 1985, and 6% for 1986 and thereafter. Theprice contingencies for local costs were assumed to be 7% for 1983, 1984, and1985, and 6% for 1986 and thereafter. Price contingencies represent about 20%of basic cost, including physical contingencies. It is PEA's policy not tocapitalize interest during construction due to the usually short constructionperiod of its projects. The total cost, excluding taxes and duties, estimatedat B 77.5 million (US$3.3 million), is B 1,109.1 million (US$48.3 million).

Financing Plan

4.20 The proposed Bank loan of US$30.6 million would finance the foreigncost of Part A of the project and the front-end fee. The cost of consultancyservices for Part B of the Project, estimated at US$1.0 million, will befinanced by the ADAB (para. 4.16). The local cost of US$20 million would befinanced from consumers' contributions in an amount estimated to be US$12.6million and the balance from PEA's internally generated funds.

4.21 The proposed Bank loan is equivalent to 59% of the total financingrequirements. During negotiations it was agreed that front--end fee will becapitalized. Villages customarily pay their contribution to PEA at the timetheir applications are approved. These conl:ributions are normally collectedby the village headman from the potential initial customers, historicallyabout 60% of the total number of households.

Implementation

4.22 As mentioned in para. 4.10, the new villages to be electrified underthe First Phase of the NREP as well as the extensions to households invillages already partially electrified, are intended to be distributed in twoprojects by equal parts for financing by the Bank and OECF. Under thisarrangement each party would help finance the electrification of about 1,500unelectrified villages and extensions in another 1,500 partially electrifiedvillages (see Table 4.2).

4.23 The planning, engineering and construction of the project will becoordinated by PEA's Project and Planning Division and the subprojects willbe implemented by the regional offices. To avoid initial delays in thestarting of t-he project construction PEA is preparing the necessary actionsto ensure the availability of human resources and equipment in the provinceswhere the project will be implemented. Procurement is expected to startin June 1983 and construction will begin in January 1984, using materialsfrom PEA-s inventories if necessary. The total implementation period will befrom mid-1983 through December 1986 (see Annex 8 for implementation schedule).

- 26 -

4.24 Most of the distribution lines would follow main or village roads.For lines which cross private land no compensation is pa:Ld although suchcompensation is provided for in PEA's Act, as the experience has been thatvillagers welcome the provision of electric services. PEA has experiencedlittle difficulty in obtaining easements over farmland.

Procurement

4.25 Except for concrete poles and minor items, all equipment andmaterials to be financed under the proposed Bank loan would be procured onthe basis of international competitive bidding in accordance with the BankGuidelines. A preference of 15% of the c.i.f. price of iimported goods, orthe prevailing custom duty, whichever is lower, would be extended to quali-fied local manufacturers. Local competitive bidding procedures acceptable tothe Bank would be applied to: (a) concrete poles (as shipping charges wouldnot warrant concrete poles being procured internationally); and (b) otherminor items costing less than $100,000 each and up to an aggregate amount of$2.5 million. Bidding packages for equipment and materiaLls over $500,000will be reviewed and commented on in advance by the Bank.

Disbursement

4.26 Disbursement from the proposed loan would be made against:

(a) 100% of the foreign exchange cost of directly imported equipmentand materials;

(b) 100% of ex-factory cost for equipment and material manufacturedlocally;

(c) 65% of total expenditures for imported equipment and materialsprocured locally; and

(d) 47% of total expenditures ex-factory for concrete poles.

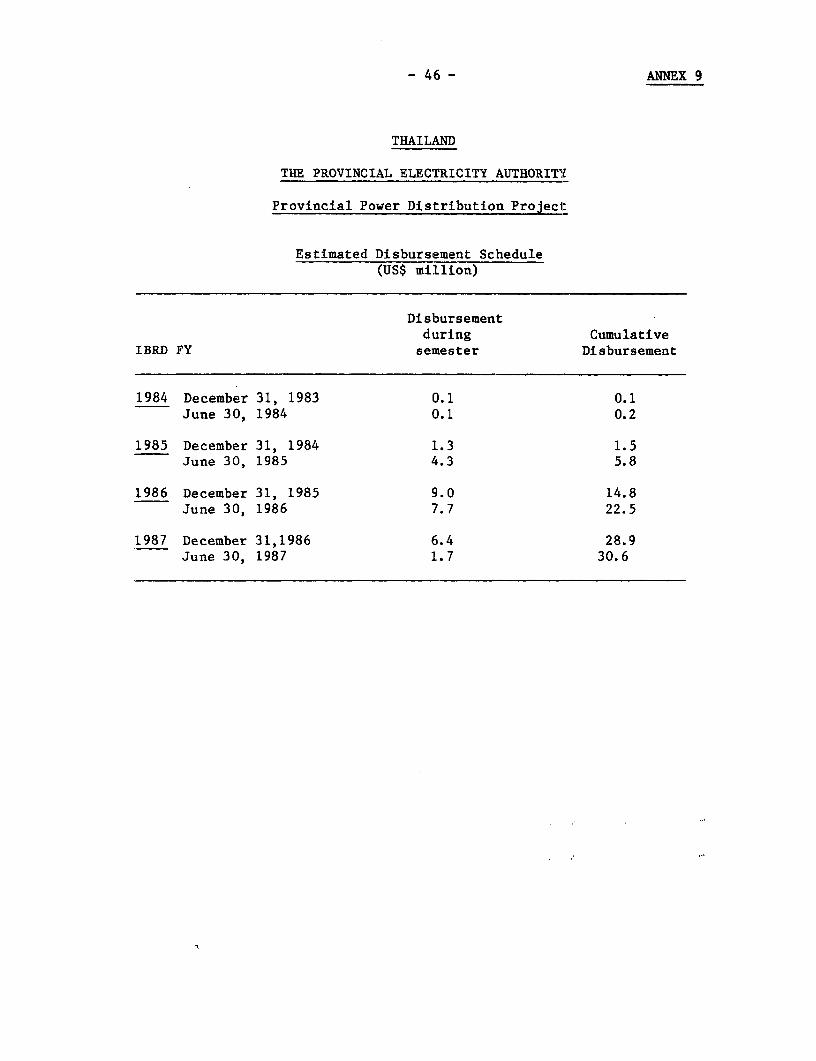

Since the proposed loan will finance a time-slice of an on-going program,there are no disbursement profiles available that could be compared with theone prepared for the proposed loan. The disbursement schedule presented inAnnex 9 was derived on the basis of the Implementation Schedule (Annex 8)and PEA-s experience with on-going projects. The closing date of the loanwould be June 30, 1987.

Monitoring

4.27 PEA has established an effective system to moniltor its investmentin the two Accelerated Rural Electrification projects and to assess theimpact of such projects in the electrified villages. A similar system willbe used to monitor the proposed project. Details on PEA's monitoring systemare presented in Annex 10.

- 27 -

Risks

4.28 The project risks are acceptable. The two accelerated RuralElectrification projects financed by the Bank faced start-up delays.Nevertheless, since the NREP is an on-going program, such delays are lesslikely to occur. The sensitivity analysis shows that if project _ostsincrease by 20% the Economic Rate of Return (ERR) would be reduced from 14%to 12%. On the other hand, if benefits are reduced by 20% (due to less thanexpected connection rate, load or savings) the ERR would be 11%.

Environmental Effects

4.29 The project is not expected to cause any significant environmentalproblem.

V. FINANCIAL ANALYSIS

A. PEA's Financial Performance FY77 through FY81

5.01 As shown in Table 5.1, during the past five years PEA's revenuesincreased rapidly at an annual average rate of 38% reflecting the expansionof PEA's market and the large tariff adjustments implemented in FY80 andFY81. This increase in revenues was largely offset by a substantialincrease in the cost of power purchased from EGAT which grew at an annualaverage rate of 50%. This and the fact that PEA's yearly investment trebledduring the period, explains the downward trend of PEA's rate of return(Table 5.1) and self-financing ratio (Table 5.2).

Table 5.1: SUMMARY HISTORICAL INCOME STATEMENTS, FY77-FY81(In millions of current Baht)

Averageannual

FY77 FY78 FY79 FY80 FY81 growth

Energy sales (Gwh) 3,174 3,650 4,254 4,696 5,210 13.2Revenues 2,394 3,168 3,697 5,080 8,742 38.2Average tariff B/kWh 0.75 0.87 0.87 1.08 1.62 22.3Operating expenditures 2,140 2,811 3,348 4,843 8,428 40.9Operating income 254 357 349 237 314 5.4Net income 173 354 342 146 151 -3.3Rate of return (revalued) (%) 10.3 12.0 9.3 5.0 4.8Number of connections ('000) 1,144 1,350 1,574 1,886 2,270 18.7Energy Revenue per connection (B) 1,909 2,282 2,283 2,618 3,718 18.1Operating expendituresper connection (B) 1,870 2,082 2,127 2,568 3,713 18.7

- 28 -

5.02 It is also worth noting that PEA's operating cost per connectionincreased to match the revenue from electricity sales per connection byFY81, as shown at the bottom of Table 5.1. This is the result of PEA'sexpansion into the rural market where customers are main:Ly in the lowertariff brackets. In other words, during the past few years, in order toproduce a positive net income, PEA has relied mainly on revenues fromsources other than its electricity sales such as installation and inspectionfees, construction for customers, interest, etc.

5.03 To complement its internally generated funds, (luring the periodunder consideration PEA made extensive use of its borrowing capacity andrelied on some contributions from consumers. Equity contributions from theGovernment were limited as shown in Table 5.2.

5.04 PEA has customarily relied largely on soft foreign loans from theOverseas Economic Cooperation Fund (OECF) of Japan, the Kreditanstalt FurWiederaufbau (KFW) of West Germany, the Kuwait Fund for Arab EconomicDevelopment (KFAED), the Canadian International Development Agency (CIDA)and the Organization of Petroleum Exporting Countries (OEEC) Fund forInternational Development. In addition, the Government h,as subsidized theinterest rate paid by PEA on domestic loans, mainly from the Ministry ofFinance and the Krung Thai Bank.

Table 5.2: SUMMARY HISTORICAL SOURCES AND APPLICATIONS OF FUNDS, FY77-FY81(In millions of current Baht)

Averageannual

FY77 FY78 FY79 FY80 FY81 growth

Internal sources 461 708 789 703 1,023 22.0Borrowings 673 413 740 1,344 2,516 39.0Equity investments 10 77 49 63 205 118.3Other 262 247 303 357 681 39.1

Total Sources 1,406 1,445 1,881 2,467 4,425 33.2

Capital expenditures 902 1,051 1,320 1,527 2,452 28.4Debt service 108 186 276 367 637 55.8Working capital increase 320 161 141 153 1,185 38.7Other 76 47 144 420 151 18.7

Total Applications 1,406 1,445 1,881 2,467 4,425 33.2

Debt service coverage 4.2 3.8 2.8 1.9 1.6Contribution to construc-tion (%) 39.1 49.6 38.8 22.0 15.7

- 29 -

5.05 This conservative financing policy is reflected in a debt servicecoverage ratio which, although declining, has remained above 1.6. During theperiod PEA's long-term debt as a percentage of its capital structure wasalways below 41%. (See Table 5.3.)

Table 5.3: SUMMARY HISTORICAL BALANCE SHEETS, FY77-FY81(In million of current Baht)

FY77 FY78 FY79 FY80 FY81

Net working capital 1,090 1,127 1,131 1,218 2,399Net fixed assets 4,241 5,265 6,874 9,054 11,889Other assets 125 40 152 542 492

Total Assets 5,456 6,432 8,157 10,814 14,780

Debt equity 2,372 2,528 3,029 4,302 6,563Equity 3,084 3,904 5,128 6,512 8,217

Total Liability & Equity 5,456 6,432 8,157 10,814 14,780

Debt as % of capital structure 37.3 34.4 32.7 35.3 41.0Current ratio 1.7 1.6 1.3 1.3 1.7Quick ratio 0.8 0.8 0.4 0.3 0.5

5.06 During the past five years PEA's current ratio exceeded 1.3 at alltimes. However, the quick ratio (current ratio excluding inventories) hasbeen declining reflecting the large accumulation of inventories. At the endof FY81 PEA's inventory was equivalent to 17 months of investment. This isconsidered on the high side. In addition,, the inventory is not properlybalanced presenting shortages of some key materials. PEA expects tomodernize its materials management systems as part of the program forstrengthening its operations (para. 4.14).

5.07 Detailed historical financial sltatements are presented in Annex11.

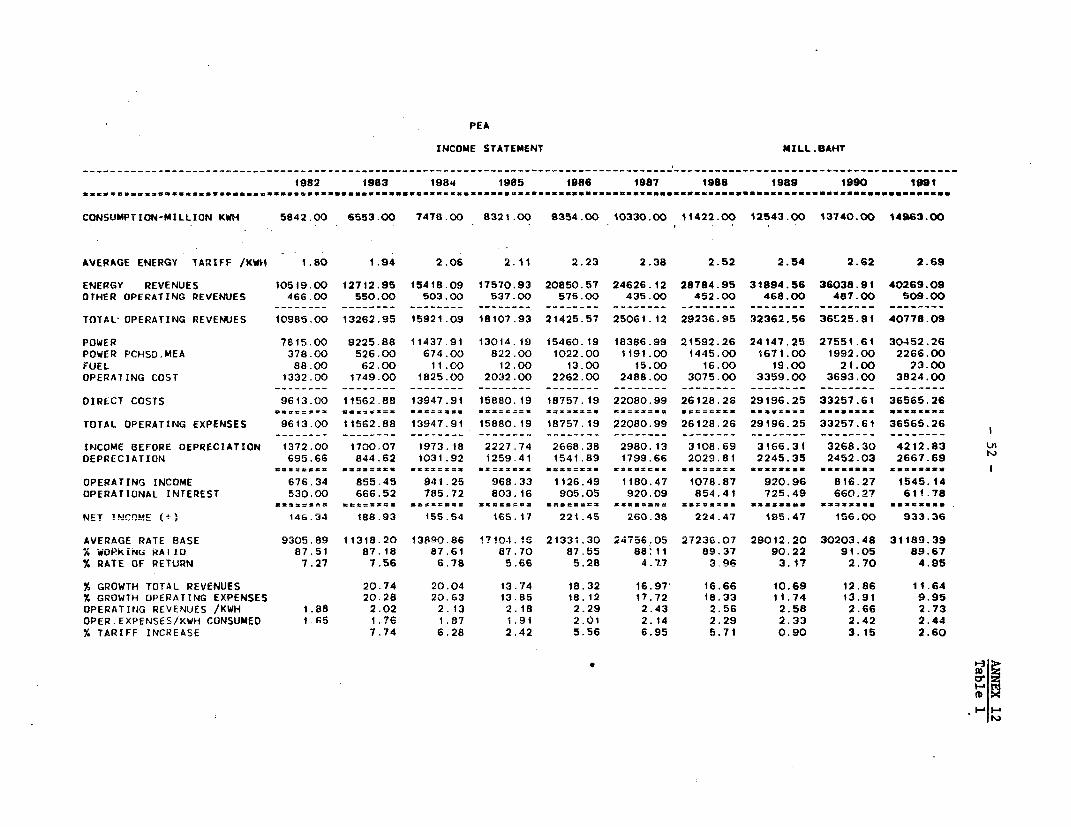

B. Future Profitability

5.08 A summary of PEA's projected income statement is presented inTable 5.4. PEA's rate of return on net revalued assets for FY82 isestimated at 7.3%.

- 30 -

Table 5.4: SUMMARY PROJECTED INCOME STATEMENTS, FY82-FY86(In millions of current Baht)

FY82 FY83 FY84 FY85 FY86

Energy sales (GWh) 5,842 6,553 7,478 8,321 9,354Revenues 10,985 13,263 15,921 18,108 21,425Average tariff B/kWh 1.80 1.94 2.06 2.11 2.23Operating expenditures /a 10,309 12,408 14,980 17,140 20,299Operating income 676 855 941 968 1,126Net income (loss) 146 189 155 165 221Rate of return (revalued) (x) 7.3 7.5 6.8 5.6 5.3Self-financing ratio (X) 17 21 19 18 19

/a Including depreciation on revalued assets.

5.09 Present covenants require EGAT and the sector to produce rates ofreturn on net revalued fixed assets of not less than 2% in FY81 and 8% inFY82 and thereafter, and PEA to earn rates of return consistent with thesector-s requirements. In FY81 the sector rate of return was 8.8% andEGAT's was 8.3%. It is now estimated that for FY82 the rates of returnfor ECAT and the sector will be 9.2% and 8.9% respectively. These covenantsas applicable to future years will be continued in the proposed loan. Underthe assumptions followed, the covenanted rates of return can be accomplishedwith modest tariff increases (para. 5.14). PEA would need to generate fundsequivalent to a rate of return of about 6% during the period FY83 throughFY86 to meet its financial requirements in terms of operating expenditures,investment, debt service and liquidity. After FY86, when the investmentprogram is expected to be substantially smaller, PEA's cash generationrequirements will decrease gradually.

5.10 The financial projections assume that some cross-funding will takeplace among EGAT, PEA and MEA by EGAT charging higher bulk tariffs to MEAthan to PEA.

C. Tariffs

5.11 PEA's Act provides that the Board of Directors has the power tofix the rates it charges for electricity. In practice, the Cabinet decideson the tariff adjustments, based on the recommendations of the Tariff RateCommittee. Under previous loans it was agreed to incorporate a fuel/powerpurchase cost adjustment clause in the Sector's and PEA-s tariff schedules.Such clause will be repeated in the proposed loan.

- 31 -

5.12 Tariffs were increased in February 1980 and, on the basis of aPlan of Action agreed under Loan 1852-TH, were further adjusted on October1, 1980, January 9, 1981 and April 1, 1981. In addition, a surcharge forheavy consumers was established in August 1980. These tariff adjustmentsrepresent an increase of about 158% between February 1980 and April 1981 onthe tariffs charged by EGAT to PEA, MEA and large direct consumers; 111% forPEA's consumers and 131% for users in MEA's service area. To reflect therecent drop in oil prices, minor reductions (about Baht 0.02 per kWh) insome categories of consumers were introduced in April 1, 1983.

5.13 Under Loan 1871-TH PEA agreed to review by April 30 every year theadequacy of its tariffs to produce the required rate of return. Similarly,under Loan 2000-TH the Government undertook to have periodic reviews of thetariffs of the three utilities to ensure that: (a) they are adequate to meetthe covenanted rates of return; and (b) they accomplish the required crossfunding among the three utilities as needed to enable them to carry outtheir respective investment programs. These covenants will be repeated inthe proposed loan.

5.14 The projected tariffs of EGAT, PEA and MEA (Baht per kWh) atcurrent prices are presented in Table 5.5.

Table 5.5: EGAT, PEA AND MEA PROJECTED TARIFFS(B/KWh)

FY82 FY83 FY84 FY85 FY86

EGATCurrent 1.43 1.48 1.57 1.59 1.66Real 1.43 1.38 1.37 1.30 1.28

PEACurrent 1.80 1.94 2.06 2.11 2.23Real 1.80 1.81 1.80 1.72 1.72

MEACurrent 1.85 1.93 2.07 2.09 2.19Real 1.85 1.80 1.81 1.71 1.69

5.15 For comparison purposes, the following are the long run marginalcosts recently estimated for each utility (B/kWh): EGAT 1.25; PEA 2.01 andMEA 1.55.

- 32 -

D. Financing of PEA's Development Program

5.16 PEA's financing plan for the period of implementation of theproposed loan, FY84-FY86, is presented in Table 5.6.

Table 5.6: PEA'S FINANCING PLAN, FY84-FY86

Baht US$ %(million) (million)

SourcesInternal sources 6,869 298.6 56.8Less: debt service 4,865 211.5 40.2

Net Internal Generation 2,004 87.1 16.6

Equity 671 29.2 5.6Borrowings 6,577 285.9 54.4Working capital decreases 1,452 63.1 12.0Other /a 1,373 59.8 11.0

Total Sources 12,077 525.1 100.0

ApplicationsProposed project 1,162 50.5 9.6Other capital expenditures 10,915 474.6 90.4

Total Applications 12,077 525.1 100.0

/a Includes consumers contributions and deposits.

5.17 Under the assumptions followed, PEA-s contribution from internallygenerated funds to its total investment program is expected to be 16.6%.If consumers contributions and deposits are included, the participation ofconsumer-related revenues rises to 27.6% of total investment.

5.18 PEA is expected to continue depending on foreign borrowings tofinance the foreign cost of its projects. Most of these loans have beencontracted, on very favorable terms, with the OECF, KFW, the KFAED, CIDA andOPEC Fund. Excluding CIDA loans which are interest free, interest rates onloans from these sources range from 2% to 6% p.a. Exchange risk on foreignloans is normally assumed by PEA. Because of the short investment period ofmost of its projects, it is PEA's policy not to capitalize! interest duringconstruction.

- 33 -

5.19 PEA expects to use in its investment program part of the inven-tories accumulated in recent years (para. 5.06); this will result in areduction of PEA's working capital.

5.20 Equity contributions are assumed to be limited to the reimburse-ment of the cost of projects sponsored by the Government for defense andsecurity purposes. As in previous loans, assurances were obtained duringnegotiations that the Government will provide adequate funds to cover anyshortfalls in financing the project.

E. Debt Control

5.21 Present covenants provide for the Bank to review PEA's borrowingswhen long-term debt as a percentage of total capitalization exceeds 60%.PEA is also required to limit its short- and medium-term debt (debt whichon issue matures within five years) to 10% of its total debt outstanding.In the past PEA has complied with both covenants and, under the assumptionsfollowed, PEA is expected to remain within these limits. It is intended torepeat both covenants in the proposed loan.

F. Liquidity Position

5.22 Under the assumptions followed, during the forecast period PEA'sliquidity is expected to remain adequate with a current ratio in excessof 1.3.

5.23 Detailed financial projections for PEA, EGAT and MEA arepresented in Annex 12 as well a consolidated projected income statement forthe sector. The assumptions followed are presented in Annex 13.

VI. ECONOMIC ANALYSIS

6.01 The Government of Thailand places a high priority to the ruraldevelopment as a key element supporting its dual objective of promotingeconomic growth and alleviating poverty. In this context, rural electri-fication in Thailand has played a decisive role in promoting economicdevelopment in rural areas. On the other hand, the NREP, by complementingother on-going rural electrification projects which extend the distributionnetwork to formally remote areas, enhances the benefits of the capitalinvestment in those projects.

Economic Rate of Return

6.02 Since the project to be financed under the proposed loan covers atime-slice of PEA's NRE Program, the economic analysis was made for the wholeprogram. The methodology followed is substantially the same as that usedfor evaluating the Second Accelerated Rural Electrification (Loan 1871-TH).

- 34 -

6.03 The economic rate of return of the project (ERR) is the discountrate that equalizes the economic costs and the direct and indirect benefitsattributable to the project over its life. In evaluating Rural electrifi-cation projects, in an attempt to better reflect the benefits of the project,it is customary to include in the ERR not only the direct benefits (derivedfrom the sales of electricity) as is done in other power projects, but alsothe so called indirect benefits. The indirect benefits are an estimate ofthe impact of the project in terms of cost savings and productivityincreases for the different groups of consumers intended to be served by theproject. The ERR so calculated is 14%. Details on the ERR calculation arepresented in Annex 14.

6.04 Sensitivity tests for variations in costs and benefits give thefollowing results:

ERR

(a) On basic assumption 14

(b) Project cost increased by:10% 1320% 12

(c) Energy cost increased by:10% 1320% 11

(d) Direct benefits decreased(due to lower sales than expected) by:

10% 1320% LO

(e) Indirect benefits decreased(due to overestimation of savings) by:

10% 1320% Li

6.05 If only direct benefits are included (including consumers contri-butions), the ERR would be -5%. This is normally the situation in ruralelectrification projects, due to the fact that they serve mostlyresidential consumers in the lower tariff brackets. In the particular caseof Thailand, as mentioned in para. 1.23, although a certain degree of crosssubsidization is desirable, it appears that tariffs for that group ofconsumers are unnecessarily low. This situation is expected to begradually corrected.

- 35 -

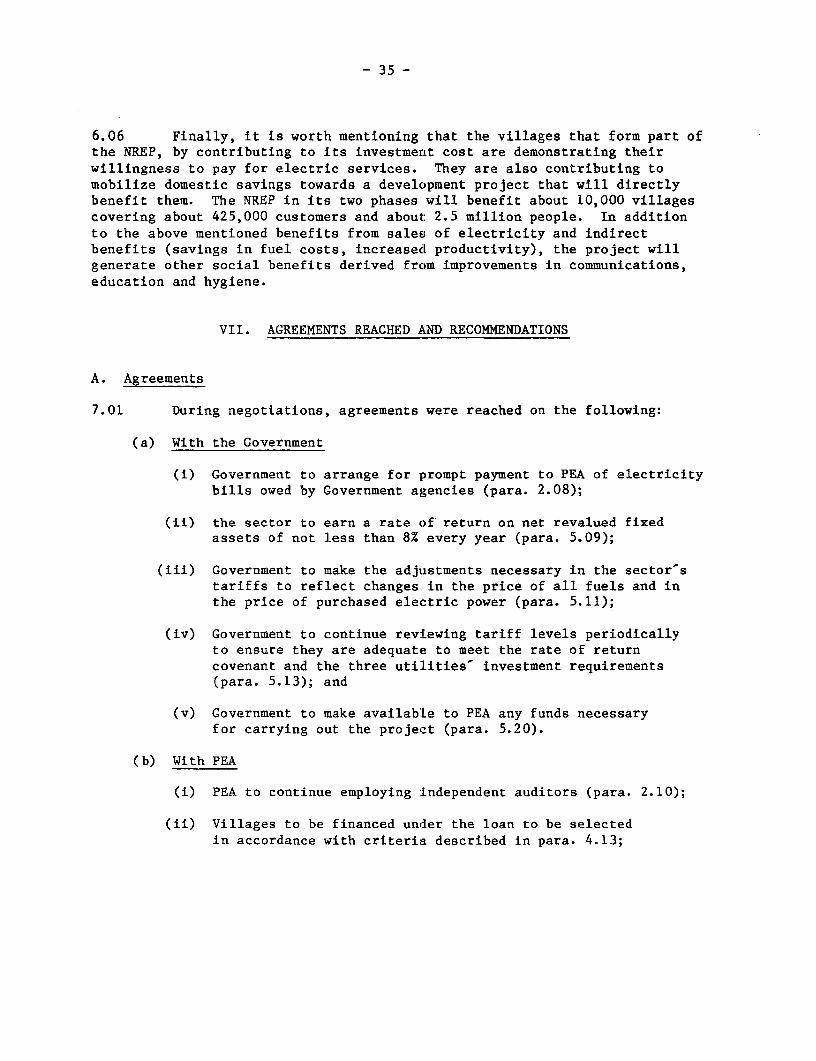

6.06 Finally, it is worth mentioning that the villages that form part ofthe NREP, by contributing to its investment cost are demonstrating theirwillingness to pay for electric services. They are also contributing tomobilize domestic savings towards a development project that will directlybenefit them. The NREP in its two phases will benefit about 10,000 villagescovering about 425,000 customers and about: 2.5 million people. In additionto the above mentioned benefits from sales of electricity and indirectbenefits (savings in fuel costs, increased productivity), the project willgenerate other social benefits derived from improvements in communications,education and hygiene.

VII. AGREEMENTS REACHED AND RECOMMENDATIONS

A. Agreements

7.01 During negotiations, agreements were reached on the following:

(a) With the Government

(i) Government to arrange for prompt payment to PEA of electricitybills owed by Government agencies (para. 2.08);

(ii) the sector to earn a rate of return on net revalued fixedassets of not less than 8% every year (para. 5.09);

(iii) Government to make the adjustments necessary in the sector'stariffs to reflect changes in the price of all fuels and inthe price of purchased electric power (para. 5.11);

(iv) Government to continue reviewing tariff levels periodicallyto ensure they are adequate to meet the rate of returncovenant and the three utilities' investment requirements(para. 5.13); and

(v) Government to make available to PEA any funds necessaryfor carrying out the project (para. 5.20).

(b) With PEA

(i) PEA to continue employing independent auditors (para. 2.10);

(ii) Villages to be financed under the loan to be selectedin accordance with criteria described in para. 4.13;

- 36 -

(iii) in the event that the grant from the ADAB cloes not materializeby September 30, 1983 PEA to prepare a Plan of Action tointroduce improvements in its operation and to submit suchPlan for Bank-s comments by December 31, 1983 (para. 4.17);

(iv) PEA to earn a rate of return consistent with the sector-srequirements (para. 5.09);

(v) PEA to continue the fuel/power purchased ccst adjustmentclause in its tariffs schedule (para. 5.11);

(vi) PEA to continue reviewing the adequacy of its tariffsby April 30 each year (para. 5.13); and

(vii) PEA to secure Bank's approval if long-term debt exceeds60% of the sum of equity and debt and to limit itsshort- and medium-term debt to 10% of its total debtoutstanding (para. 5.21).

B. Recommendations

7.02 With the agreements reached on the above, the project forms asuitable basis for a loan to PEA of US$30.6 million for a period of 20 yearsincluding 6 years grace, with the guarantee of the Royal Thai Government.

37 ANNEX 1

THAILAN!D

PROVINCIAL POWER DISTRIBUTION PROJECr

Highlights of EGAT, MEA and PEA Operations

FY75 FY76 FY77 FY78 FY79 FY80 FY81