World Bank Document - Documents &...

52

Document of The World Bank FOR OFFICIAL USE ONLY Report No. 4622 PROJECT COMPLETION REPORT TANZANIA: KIDATU HYDROELECTRIC PROJECT SECOND STAGE (LOAN 1306-T-TA) Energy Division East Africa Regional Office November 30, 1982 Revised June 17, 1983 This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of World Bank Document - Documents &...

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No. 4622

PROJECT COMPLETION REPORT

TANZANIA: KIDATU HYDROELECTRIC PROJECT SECOND STAGE

(LOAN 1306-T-TA)

Energy DivisionEast Africa Regional Office

November 30, 1982Revised June 17, 1983

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

FOR OFFICIAL USE ONLY

TANZANIA

KIDATU HYDROELECTRIC PROJECT SECOND STAGE

Completion Report

Table of Contents

Page No.

Preface ..................................................... iBasic Data Sheet ............................................ iiHighlights .................................................. v

I. INTRODUCTION .......................................... 1

II. PROJECT PREPARATION AND APPRAISAL. 2

Origin, Preparation, Appraisal and Negotiation 2Project Description ................................... 2Justification. 4Covenants. 5

III. PROJECT IMPLEMENTATION, OPERATION AND COSTS ........... 6

Loan Effectiveness and Project Start-up ............... 6Costs and Related Financing. 7Cost Increases .9Cost Savings ............................ 11Disbursements .............................--. 12Project Implementation .............................-. 13

Physical Problems .............................-... 13Administrative Problems ............................ 15

Ecological Aspects .............................-. 16Performance of Consultants and Contractors .17Main Contracts ........................................ 18Important Changes in Original Design .................. 18

IV. INSTITUTIONAL PERFORMANCE .20

Management and Organization Effectiveness ............. 20Training .......------------------------------ 20

V. FINANCIAL AND RELATED ASPECTS ......................... 21

Financial Arrangements .21Accounting and Audit .................................. 23Financial Performance and Compliance with Covenants ... 23

VI. BANK PERFORMANCE .24

Overall Performance and Working Relationships ......... 24

VII. LESSONS LEARNED ....................................... 24

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

TABLE OF CONTENTS (continued)

Page No.

Annexes

1. Comparison of Revised Cost Estimates with AppraisalCost Estimates ........................................ 27

2. Construction Schedules - Mtera Dam and Powerhouse ....... 283. Statement of Contracts and Works ........................ 304. Internal Rate of Return ................................. 325. Comparison of Alternative Programs - Equalizing

Discount Rate ......................................... 336. Income Statements ....................................... 347. Balance Sheets .......................................... 358. Funds Flow Statements ................................... 369. Comments from the Borrower .............................. 37

- i -

TANZANIA

KIDATU HYDROELECTRIC PROJECT SECOND STAGE

LOAN 1306-T-TA

PREFACE

The project consisted of the construction of a concrete buttressdam at the Mtera site; installation of two additional 50-MW hydro units atthe existing Kidatu powerhouse, the construction of a 220/132-KVtransformer station at Morogoro and necessary consulting services andtraining program. Loan 1306-T-TA for US$30 million was signed in August1976 and became effective in March 1977. The loan has been completelydisbursed and was closed on December 31, 1981. The Project CompletionReport (PCR) was prepared by the East African Regional Office - EnergyDivision, based on the appraisal, president's, supervision and consultant'sreports and other documents in the Bank's files and on discussions with thestaff of Tanzania Electric Supply Company Limited (TANESCO).

The PCR summarizes the main points of the project particularlythose which presented difficulties or resulted in specific accomplishmentsor failures.

Following normal procedures, a draft copy of the report was sentto the borrower (TANESCO) and the Guarantor (Government) for theircomments. Comments were received from TANESCO and have been reflected infinalizing the report. They have also been reproduced as an attachment tothe report (Annex 9).

The project was not audited by the Bank's Operations EvaluationDepartment.

- ii -

TANZANIA

KIDATU HYDROELECTRIC PROJECT SECOND STAGE - LOAN 1306-T-TA

COMPLETION REPORT

Basic Data Sheet

Key Project Data Original Plan Actual

Total Project Cost (US$ million) 1/ 89.0 109Cost Overrun (%) - 25%Loan Amount (US$ million)

Original - Loan 1306-T-TA 30.0 30.0Disbursed (US$ million) 30.0 30.0Cancelled (US$ million) - -Joint Financing

European Economic Community -EEC (US$ million, supplementary,administered by IDA) - 7.0

Germany - KfW (US$ million) 2/ 31.0 28.1Swedish International DevelopmentAuthority - SIDA (US$ million) 18.5 18.5

Date for Completion ofPhysical Components 10/80 08/81

Proportion Completed byAppraisal Target Date (%) 80%

Incremental Financial Rate of Return (%) 23% 18%Financial Performance UnsatisfactoryInstitutional Performance Satisfactory

1/ Based on the average exchange rate between 1976 and 1981.

2/ The final KfW contribution was US$36 million (para. 3.12).

- iii -

Cumulative Estimated and Actual Disbursement(US$ million)

1976 1977 1978 1979 1980 1981

Appraisal Estimate 2.3 7.3 13.1 22.1 28.1 30.0Actual - 3.1 9.3 17.8 30.0 37.0Actual as % of estimate 0 42 71 80 107 123

Other Project Data

Actual ororiginal Revisions Est. Actual

First Mention in Files - - 1966

(together withKidatu I)

Negotiations - - 01/19/76

Board ApprovalLoan 1306-T-TA 04/01/76 - 07/01/76Credit (EEC) - - 02/12/80

Loan AgreementLoan 1306-T-TA - - 08/12/76

Credit (EEC) - - 03/20/80

EffectivenessLoan 1306-T-TA 12/01/76 - 03/01/77Credit (EEC) - - 04/08/80

Closing DateLoan 1306-T-TA 12/31/81 - 12/31/81

Credit (EEC) - - 12/31/81Borrower

Loan 1306-T-TA - - Government of Tanzania

Credit (EEC) - - Government of Tanzania

Executing Agency - - Tanzania Electric Supply

Company Ltd. (TANESCO)Fiscal Year of TANESCO - - Calendar Year

Follow-on Project Name - - Tanzania Fourth Power

Project (draft greencover SAR circulated11/10/82)

- iv-

Mission Data

Month/ No. of No. of DateYear Weeks Persons Manweeks of Report

Appraisal 4/ 75 3 5 13.0 06/02/76

Supervision I 10/76 2 2 4.0 12/15/76

II 01/77 1 2 3.0 03/17/77

III 05/77 2 2 4.0 06/17/77

IV 12/77 2 1 3.0 03/14/78

V 07/78 2 2 4.0 08/15/78

VI 03/79 1 1 3.0 05/03/79

VII 12/79 2 2 4.0 01/15/80

VIII 12/80 2 2 4.0 01/30/81

TOTAL 21 42.0

Currency Exchange Data

Appraisal US$1 = TSh 8.05

Intervening Years Average

1977 US$1 = TSh 8.11978 US$1 = TSh 8.21979 US$1 = TSh 8.31980 US$1 = TSh 8.41981 US$1 = TSh 8.91982 US$1 = TSh 9.4

-v -

TANZANIA

KIDATU HYDROELECTRIC PROJECT SECOND STAGE

LOAN 1306-T-TA

HIGHLIGHTS

Loan 1306-T-TA was for the second phase of the MteraHydroelectric Project that was intended to meet forecast demand up to1987/88. The project's achievements can be rated as an overall success,despite project cost overruns and failure to meet earnings objectives,since it made possible significant savings in oil utilization (estimated200,000 tons in 1982) which are critical to Tanzania's foreign exclhangerequirements. Additionally, the training effort was extremely successfuland should assist considerably in operating performance and decrease inreliance on expatriates.

A construction cost overrun of TSh 188 million (US$17 million)was experienced due to higher than anticipated costs of civil works and toadditional works and studies required during the course of construction.The gross overruns were partially balanced by savings in the costs ofmechanical and electrical plant financed mostly by KfW (PCR paras. 3.09 -3.20).

In general institution performance was satisfactory except in thefinancial area. TANESCO effectively revised and rearranged its practicesand method to accommodate the increasing operational load. It effectivelyutilized a panel of experts to recognize and overcome the difficultiesencountered during construction. Tariffs were increased twice, by 40% inJune 1976 and by 42% in December 1979, However these increases wereinsufficient, except for 1980, to enable TANESCO to achieve the required 7%rate of return on revalued net assets in operation. This, combined with aninability to bill and collect accounts efficiently (due, in part, tocomputer facilities failures), resulted in cash shortages throughout theimplementation period. However, this situation was significantly mitigatedby lower debt service due to longer grace period, and lesser dividendpayments (PCR 4.01-4.03, 5.02, 5.06).

TANZANIA

KIDATU HYDROELECTRIC PROJECT SECOND STAGE

COMPLETION REPORT

I. INTRODUCTION

1.01 The project constituted part of a long-range development programto meet the growing power needs on the interconnected system (coastal grid)and comprised: (a) construction of a concrete buttress dam at Mtera site;(b) installation of two additional 50-MW hydroelectric units at theexisting Kidatu powerhouse; 1/ (c) construction of a 220/132-kVtransformer station at Morogoro; and (d) engineering/consultancy servicesand training.

1.02 The project was implemented broadly on schedule and as originallydesigned. Its actual cost, however, was substantially greater than theappraisal estimate for various reasons (paras. 3.03-3.06 and 3.10)concerning the construction of the main civil work (the dam).

1.03 The original loan of US$30 million (Loan 1306-TA), together witha credit of about US$18 million equivalent from the Swedish InternationalDevelopment Authority (SIDA) and a credit of US$24 million equivalent fromKreditanstalt fur Wiederaufbau (KfW) were intended to finance the totalforeign exchange costs and part of the local costs of the project estimatedto cost US$90 million equivalent. Actual cost increased to US$110million. Cost overrun was covered through the increase of KfW funds byabout an additional DM 10 million and a supplementary EEC Special ActionCredit of US$7 million 2/ (Credit 55 through IDA as administrator, para.3.12).

1.04 The Mtera dam, the extension of the Kidatu powerhouse by two50-MW hydroelectric units, and the transmission facilities at Morogorosubstation have been operating successfully since 1981 after overcomingsome initial operating problems such as oil leakages, wrong relayadjustments, etc.

1.05 The actual growth rates in energy and capacity demand of the gridthroughout the period 1976-1981 have been substantially lower thanprojected during the appraisal due mainly to the declining general economicsituation of the country. The commissioning of Kidatu II led to asubstantial reduction in the Tanzania Electric Supply Company Ltd's(TANESCO) thermal generation from oil. Calculated oil savings in 1981 isabout 175,000 tons and estimated savings in 1982 are 200,000 tons. Yearlyoil savings will gradually increase as the system's load builds up and will

1/ The Kidatu powerhouse was originally designed for four 50-MW units.Two 50-MW units were completed in 1975. For further information,please see Project Performance Audit Report (Tanzania KidatuHydroelectric Project - First Stage, Loan 715-TA and Loan 715-2TA) ofDecember 19, 1979 No. 2765.

2/ The SIDA, KfW and EEC Special Action credits were channelled throughthe Government of Tanzania.

- 2 -

reach 375,000 tons per annum in the 1990s. Despite the increase inconstruction costs, Kidatu II is in fact justified as the least costsolution over any tlhermal alternative due to very high fuel prices in theworld markets. Mainly because of lower than expected load growth, therecalculated incremental rate of return on the project is 18%, compared tothe appraisal estimate of 23%.

1.06 TANESCO's financial performance through 1976 was less thansatisfactory. Although the company increased tariffs twice during theproject implementation period, these were not sufficient and, as a result,consistently failed to achieve the required minimum rate (7%) of return onrevalued net fixed assets in operation, perhaps also due to inappropriaterevaluation. This, combined with excessive accounts receivable partly dueto serious breakdowns in the computer, partly to delinquent customers,resulted in cash shortages for the company.

II. PROJECT PREPARATION AND APPRAISAL

Origin, Preparation, Appraisal and Negotiation

2.01 The project was basically a continuation of the First StageKidatu Hydroelectric Project, which was appraised in 1970 and jointlyfinanced by the Bank (Loan 715-TA), SIDA and the Canadian InternationalDevelopment Agency (CIDA). The First Stage was completed according to theoriginal schedule, although with substantial cost overruns, and hasoperated satisfactorily since May 1975. The water intake, headrace tunnel,powerhouse, control room, tailrace tunnel, switchyard, and all relatedcivil works, and the accessories and auxiliaries had been excavated andconstructed according to the ultimate design which included provision forthe Second Stage (the project).

2.02 The history of the development of the Kidatu Hydroelectric Schemebegan almost 15 years ago when the Government asked the Bank for assistancein financing the First Stage. Additional studies needed to determine thebest solution among known alternatives and design of detail were completedin July 1968, and the Kidatu development was recommended to be the mosteconomic scheme. The second stage was prepared on the basis ofreconnaissance and preappraisal missions in May and December 1974, a reporton the geological situation and design by a Bank consultant, and afeasibility study dated February 1975 by TANESCO's engineeringconsultant. The project was appraised in April 1975.

Project Description

2.03 The project components were planned to be constructed at threemain sites, i.e. Mtera, Kidatu and Morogoro. The Mtera site constructionconsisted of the following:

- 3 -

(a) A concrete buttress dam 45 m in height and 260 m in length whichforms a reservoir with a storage capacity of 3.2 billion J (livecapacity) at a drawdown of 8.5 m, which in turn will provide aregulated river flow during dry seasons sufficient for therequirements of the project. A concrete spillway with fourradial gates (each 14 m wide and 11.5 m in height) and about 160m long spillway, a chute, all located on the right bank of theriver. The dam is equipped with a bottom outlet (5.5 m x 6 m)for the purpose of regulation of the water;

(b) About 34 km of road passing over the dam crest to replace astretch of the existing Iringa-Dodoma road which was submergedunder the reservoir;

(c) Employer's village for housing of the operation and maintenancestaff and offices, etc. with all necessary water supply andsewerage systems;

(d) Temporary camps constructed at four locations, comprised of 97blocks of houses with independent water supply and sewer systemsand with accommodation capacity for about 100 senior staff,including expatriates and over 600 workers/junior staff;

(e) A floating boom about 2.3 km in length at about 2 km upstream ofthe dam to catch the floating debris. The debris to be removedby the boat provided for this purpose; 3/

(f) Bush clearance in the reservoir was done up to about 2.3 kmupstream of the dam in the area of about 140 hectares below thefull supply level of the reservoir; 3/ and

(g) Ecological studies and measures including rehabilitation ofrelocated people from the areas to be submerged and extension ofthe Ruaha Game Park boundaries. 3/

2.04 The Kidatu site consists of the construction of the following:

(a) Extension of the existing Kidatu powerhouse by two 50-MWhydroelectric units with vertical Francis-type turbines andgenerators, ventilation, cooling water, drainage and dewateringsystem and all necessary civil works, auxiliary equipment, andlow and high voltage cables;

(b) Penstock intakes by removal of the two temporary concrete plugsand installation of one sliding gate and two cylinder gates (onefor each unit) with appurtenant concrete works at the waterintake area;

(c) Lining of the two existing vertical penstocks with steel andembedding it in concrete;

3/ This item was not included in the original design but adopted on therecommendation of the Bank.

(d) A roadway in the access tunnel; and

(e) Extension of the existing pothead yard, the 220-kV switchyard andconnecting transmission lines including appurtenant civil works.

2.05 The Morogoro site consists of the construction of the following:

(a) Expansion of the existing Morogoro substation for the erection ofa 90-MVA transformer of 220/132 kV; and

(b) A storage building for TANESCO's regional needs. 3/

Justification

2.06 The existing generating facilities of TANESCO before theconstruction of the project consisted of a blend of diesel and hydrogenerating plants with limited pondage provided by Kidatu (125 millionm3). The water flow available at Kidatu for power production was very lowduring the dry months (June-October) of the year. TANESCO needed anadditional generating capacity in 1980/81. The Mtera reservoir provideswater for power generation during the dry years. Thus, TANESCOsuccessfully met the demand in 1980 and can meet the demand up to 1987/88.

2.07 The alternatives to the project were another hydro scheme or athermal station. Some alternative hydro schemes were examined by theconsultants in a series of studies carried out over the previous ten years;most of them were eliminated without even detailed consideration becausethey were too remote, too small, or geologically unsatisfactory. Thechoice was finally narrowed down to three schemes: (a) Pongwe hydro planton the Wami River; (b) Stiegler's Gorge on the Rufiji River; and (c) thesecond stage development of Kidatu project (the project). Stiegler's Gorgewas eliminated because the site could only be economically developed withmuch higher capacity than the TANESCO sysem could absorb for many years tocome. The Wami scheme had been eliminated by the comparative study whichwas jointly prepared by two consultants in 1971 because of higher cost.The Second Stage Kidatu scheme was therefore chosen as the preferred hydrodevelopment and compared with an alternative thermal development based on adiesel station followed by steam units at Dar es Salaam using residual fueloil. The possibility of a coal-fired steam power plant was not a realisticalternative at the time of appraisal because there was no informationregarding the coal deposits, quality, costs and its exploitation; the coalfield was too far from the load centers and transportation was notpractical. The alternative of imported coal was eliminated on the groundsthat the port facilities were already too overloaded.

2.08 The following three (the most realistic) development alternativeswere presented in the appraisal report (Annex 5):

3/ This item was not included in the original design but adopted on therecommendation of the Bank.

- 5 -

Alternative 1: The proposed project followed by the Mtera powerplant, followed by a coal-fired plant;

Alternative 2: Thermal-hydro blend with a postponement of the projectby two years; and

Alternative 3: a solely thermal alternative.

The economic analyses indicated that Alternative 1 (starting with theproject) would be preferred over Alternative 2 (thermal-hydro blend) atdiscount rates up to 14% and that Alternative 3 (all thermal) is the mostexpensive and would only be economic at discount rates higher than 23%.

2.09 A number of calculations have since been made to determinewhether the project would have been selected over the thermal alternativehad the cost estimates at completion been known at the time of theinvestment decision. With the 1980 upward escalation in fuel oil prices,the equalizing discount rate is now estimated to be about 30%. The projectremains, therefore, the most attractive alternative.

2.10 The internal rate of return on investment for the project isdefined as the discount rate at which the present worth of the estimatedcapital and operating costs of the project, over its useful life, equalsthe present worth of attributable revenues. At the time that the projectwas appraised in 1976, a discounted cash flow calculation regarding theabove rate of return was also determined on the basis of the project'sestimated costs and sales. In that calculation, average revenue from theproject was assumed to be about T4 45 per kWh. A number of calculationshave since been made to determine the revised rate of return on investmentby taking the actual Kidatu II cost and the actual sales intoconsideration. With the increased revenues (T4 65 per kWh), rate of returnfor the scheme is now estimated at 18%, which is lower than the appraisalestimate.

Covenants

2.11 The main covenants concerned employment of consultants, rate ofreturn, revaluation of assets, preparation of tariff study and declarationof dividends. Except for the rate of return covenant, all covenants weremet.

2.12 In revaluing assets the average of the Dar es Salaam Retail PriceIndex for Wage Earners and the Cost of Living Index for Middle Grade CivilServants, with both indices adjusted to include food items, were to beused, but TANESCO has had difficulty in using this formula because thusbased the revalued assets were very high and indicated tariff levels inexcess of economic power supply to obtain the required rate of return.Therefore, in the proposed Tanzania Fourth Power Project (Mtera), a cashgeneration covenant is proposed with the option of returning to the rate ofreturn formula when an acceptable reevaluation formula is agreed to.

- 6 -

III. PROJECT IMPLEMENTATION, OPERATION AND COSTS

Loan Effectiveness and Project Start-up

3.01 After completion of the appraisal mission in April 1975, anissues paper was prepared in May 1975 (dated May 22, 1975) and a decisionmemorandum in June 1975 (dated June 12, 1975). Negotiations were held fromJanuary 19 to 23, 1976. The Bank Board approved the loan (1306-T-TA) onJuly 1, 1976, with a delay of about three months due to delays in thetariff increase which was the condition of Board presentation. The loanagreement was signed on August 12, 1976 and became effective on March 1,1977 with a delay of about three months due to the Government's delay inthe approval of the agreement and other formalities. However, these delaysdid not jeopardize the project construction but it may have affected thecontractors' offers for the main civil works as explained in the followingparagraphs.

3.02 Only three offers were received for the main civil works. Thelowest evaluated bid was about 70% higher than the appraisal cost estimatedue mainly to very big differences in the unit costs for various works.

3.03 The original cost estimate was prepared by TANESCO's engineeringconsultant and a cost estimator/consultant in 1975. Estimates were basedon detailed quantity analysis and carefully calculated unit costs forvarious items in the works. The consultant's cost estimate was recheckedby the Bank consultant during the appraisal and increased contingencies (byabout 25% physical contingencies and 37% for expected price increases) wereadded over and above the original consultants' estimate. In spite of allthese precautions, a substantial cost overrun occurred. In the opinion ofTANESCO and their consultant this substantial higher bid and cost overrunwas due to reasons of lack of contractors' interest and competition due tothe timing. Although bidding was internationally advertised and followedup by the consultant and 14 contractors registered themselves asprospective bidders and also received bid documents, only three of themgave offers as indicated above. In fact, the contractors' offers were veryclose to each other and possibly included a very large risk element notaMticipated by the consultant, TANESCO or the Bank. Other possible reasonscould be construction difficulties due to the design of the consultant,and special risks such as working conditions for expatriates in Tanzania,which had not been suitably evaluated by the consultant during thepreparation of the bid documents and the costs.

3.04 The Bank then suggested that TANESCO employ an independentconsultant to make a realistic project cost estimate and analyze the bidresults in detail; and also review the bid documents with a view toidentifying special risks and making recommendations as to the line ofaction to be followed. TANESCO employed a cost consultant for thispurpose, and solicited yet a third opinion from a similar firm.

3.05 Although initially TANESCO's engineering consultant had thoughtotherwise, both cost consultants had definitely indicated in theirrespective reports that the lowest original offer received for the civil

- 7 -

works should be considered reasonable with which they then agreed. Theprimary cost consultant had also made some recommendations regardingmodification to some design aspects and extension of the constructionprogram.

3.06 In light of TANESCO's consultant's recommendations, the Bank andSIDA recommended that TANESCO cable the three contractors who have givenoffers for the construction of the main civil works to obtain alternativeoffers for (i) a lower standard contractors' camp; (ii) about ten monthsextension of construction schedule; (iii) a new payment schedule fortemporary works; (iv) amended concrete-pouring speed; and (v) use of mildsteel instead of high-tensile steel in the webs of the dam. All threecontractors submitted their alternative offers with some reductions fromtheir original offers for the same civil works. The original lowest bidcontractor kept its lowest position for the alternative offers with areduction of about 12% from its original offer. TANESCO, with theconcurrence of the Bank and SIDA awarded the contract to this contractoraccordingly.

3.07 The above contractor successfully completed the projectsubstantially within the construction schedule. The ten-month extension ofthe schedule did not cause any difficulties because actual power demand inTanzania had proved to be lower than the appraisal forecast (Annex 2).However, if the Bank and SIDA had recommended rebidding, the project wouldhave not been completed on time and it is very likely that the final costswould have been even higher due to delays caused by rebidding.

3.08 The main civil contractor at Mtera was delayed in mobilizationdue mainly to late deliveries of equipment at site. However, with pressureby the Bank, the consultant and TANESCO', the contractor was able to recoverthe initial delays in the working program. There were no other unusualfeatures or events during the project start-up.

Costs and Related Financing

3.09 Comparative cost estimates (appraisal and actual) are given inAnnex 3. The actual costs of almost all of the contracts were within theappraisal estimates except for the main civil works contracts. Totalactual project costs of TSh 919.6 million (US$109 million) were 25% greaterthan the appraisal estimate of TSh 732 million (US$89 million) (Annex 1).

3.10 Contingency allowances estimated at appraisal were generallysufficient to cover the extra costs due to miscellaneous variations in allworks and to price increases except the main civil and mechanical works atMtera.

- 8 -

3.11 The original financing plan based on appraisal report costestimate of TSh 732 million is as follows:

Financing Agency Funds Allocated (TSh million)

IBRD (untied) 246.57 (US$30 million)SIDA( ) 152.15 (SKr 80 million)KfW ( ) 253.97 (DM 60 million)Govt./TANESCO

(to cover local costs) 126.00 (US$15.4 million)

Total Funds 778.69 (US$94.9 million)

3.12 Funds provided by the above arrangement were in excess of theappraisal cost estimate and the colenders thought that the project can beconstructed without any financing risk. However, after receipt of thebids, the financing requirements of the project had gone up considerablyand additional financing had been provided for the completion of theproject from EEC, KfW and Government/TANESCO as shown below:

Financing Agency Funds Received (TSh million)

IBRD 251.67 (US$30 million)SIDA 155.29 (SKr 80 million)EEC 58.72 (US$7 million)KfW 236.13 (DM 55 million) a/Govt/TANESCO 217.82 (US$25.9 million)

Total Funds Used 919.63 (US$109.5 million)

a/ The final KfW contribution was DM 70 million. There was a surplusof DM 15 million, which was used for the purchase of ruralelectrification material and some spare parts for the diesel sets,instrumentation of the dam and load-dispatching communicationequipment.

-9-

Cost Increases

3.13 The main reasons of the cost overruns were:

(a) the initial higher contractors' bids for the construction of themain civil works at Mtera site and other increases due to variousreasons such as differences in design and actual quantities;

(b) additional works incurred during the course of the constructionincluding the implementation of the ecological studies; and

(c) contractors' claims.

3.14 Breakdown of the cost overrun is as follows:

Bank/SIDA Financed Portion Appraisal Actual-TSh million--

Mtera Dam Civil Works 115.00 410.06Mtera Employer's Village and

Road Relocation 29.00 52.48Engineering/Administration 42.00 103.01Contingencies 131.80 -

Subtotal 317.80 565.55

KfW Financed Portion

Kidatu Civil Works 13.00 66.05Kidatu Control Equipment 5.00 15.77Kidatu Switchyard, Connecting Lines

and Morogoro Substation 10.00 37.24Contingencies 17.47 -

Subtotal 45.47 119.06

Taxes 25.00 78.85

TOTAL 388.27 763.46

Total Cost Increases: TSh 375.19 million

The net cost overrun (total cost increases TSh 375.19 million minus totalcost savings TSh 187.56 million) were TSh 187.63 million including the costincrease in the item of "Taxes" of about TSh 53.85 million.

3.15 In addition to general reasons for increases in costs explainedabove, there were increases due to additional works not included in theoriginal design. Breakdown of these are given below:

- 10 -

Additional Works Costs (TSh million)

Bush clearing 0.85Supply of towing and rowing boats 0.65

Supply of steel boom barrier 1.78Archaeological survey 0.25Water supply at new village 0.90

4.33

These costs are included in the "Bank and SIDA Financed" portion.

3.16 The main civil contractor had made various claims during the

course of construction. Since these were rejected by the consultant on

various grounds, on completion of the works the contractor presented afinal document in respect of claims under contract. This was divided into:

(i) Those items where the contract provides a remedy in the event ofa specific breach (late payments), further covering itemsnormally recompensed under the provisions of relevant clause ofthe contract in respect of works considered for rerating or

admeasurement; and

(ii) Claims presented pursuant to the provisions of such clauses of

the agreement and subject to evaluation by the consultant inorder to determine if such claims are deemed a contract risk or a

contractor's responsibility.

3.17 The financial implications of the claims under each section were

as follows:

(i) TSh 6.22 million(ii) TSh 21.86 million

Total TSh 28.08 million

3.18 Breakdown of the TSh 6.22 million is as follows:

TSh Million

- Interest on late payments 1.42- Concrete rerating 3.24

- Devaluation of Tanzanian currency 1.56

Total 6.22

- 11 -

Breakdown of the TSh 21.86 million is as follows:

TSh Million

- Port congestion and internal delays 1.44- Shortage of cement in Tanzania 1.08- Adjustment in price for imported cement 2.43- Acceleration costs 6.04

- Price adjustment on expatriate salariesand interest on this 10.87

Total 21.86

3.19 On analysis of the claims, the consultant fully expected thatarbitration would result in an award in favor of the contractor. A jointmeeting was therefore held between the contractor, TANESCO and theconsultant and the following amounts were agreed:

under (i) TSh 5.80 million(ii) TSh 8.20 million

Total TSh 14.00 million

The consultant felt that the above settlement figure reflected a fair andreasonable amount, although had the whole issue been presented forarbitration or to a court, including costs the award could well have beenconsiderably in excess of this amount. The TSh 14.0 million is included in"Bank and SIDA Financed Portion" of TSh 410.06 million above (para. 3.15).

Cost Savings

3.20 Cost savings were related to the costs of mechanical andelectrical plant mostly financed by KfW and to interest duringconstruction. Breakdown of the savings is as follows:

- 12 -

Savings---- TSh million----

Bank/SIDA Financed Portion Appraisal Actual

Mtera mechanical works 46.00 26.57Contingencies -

Subtotal 26.57

KfW Financed Portion

Kidatu steel linings and gates 19.00 13.56Kidatu turbine and pipework 37.00 22.36Kidatu generators 33.00 28.81Kidatu and Morogoro transformers

and Kidatu cables 24.00 31.90Contingencies 70.53

Subtotal 229.53 123.20IDC (Total) 106.00 29.97

TOTAL 335.53 153.17

Total Savings: TSh 182.36 million

Disbursements

3.21 The following table compares actual with forecast disbursements:

Cumulative DisbursementsAppraisal Actual

------US$ million------

FY

1976 2.31977 7.3 3.11978 13.1 9.31979 22.1 17.81980 28.1 30.01981 30.0 37.0

Bank Loan Closing Date 12/31/81 12/31/81

Deviations between appraisal and actual were mainly caused by the extensionof the original construction by about 10 months, late mobilization of themain civil contractor, revised cost estimates (cost overruns), andsuplementary financing (EEC Special Action fund No. 55 for US$7 million).

- 13 -

Project Implementation

3.22 Physical Problems: The bids received for the main civil workswere substantially higher than the estimates made at the time ofappraisal. Therefore, alternative offers were asked from the bidders andthe original construction schedule extended by about 10 months. Other thanthese there were no unusual features and events except the following:

3.23 Spillway Bridge Slab: During the pouring of concrete in thespillway bridge, slab-formwork settled on the downstream side due topartial failure of one of the screwjacks supporting the pipe columns of theformwork. However, the concreting was completed in this portion aftertaking immediate measures to prevent any further displacement. Thecompleted bridge was tested by loading the slab and the results indicatedsome loss of strength in the downstream beam because some shear cracksdeveloped at the ends of the downstream beam of the bridge. The followingmeasures had been taken to increase the strength to its designed level:

(i) additional inclined shear reinforcement steel bars wereplaced at the ends of the beam;

(ii) the chipped cracked concrete in the lower portion of bothends of the beam were replaced by high strength "prepackedconcrete";

(iii) the neoprene bearings under the beam were replaced andrepositioned to reduce the beam span.

Standard load tests made after completion of the above remedial measureshave shown that the behavior of the beams were elastic and the spillwaybridge is safe. The decision by the consultant to retain the bridge slabby shear strengthening instead of demolishing and recasting it had beentaken to enable mechanical contractor to continue with erection of thespillway gates so as to achieve timely completion of the project.TANESCO's panel of experts who were supervising the project from time totime also recommended the above remedial measures instead of recasting(para. 4.02).

3.24 Concrete Quality: From one of the periodical reviews of the testresults of the moulded specimen of concrete blocks on the dam duringconstruction, it was found that some individual pours of concrete werebelow specifications, particularly in regard to compressive strength andpermeability though the actual strength was still within the acceptablelimits from the design's point of view. However, this problem wasinvestigated and rectified immediately. The rectification measuresincluded strict control of water cement ratio and correct assessment ofwater content in the mix so as to compare favorably with the one providedin the mix design. A very strict sampling and sample cube preparationmethod was also established to obtain realistic results from the tests. Inaddition, general improvement on the quality and grading of the aggregateand sand was also made apart from addition of extra cement as a measure ofadditional precaution. Further, to check on the actual strength of thisconcrete as placed in the dam blocks, cores were circled out and tested for

- 14 -

compression strength and permeability. Schmitt Hammer tests were alsoconducted on some of the spillway sill blocks. As a result of all theseinvestigations, it was judged that a few of the concrete test results thatwere lower than specifications do not impair the stability and watertightness of the dam.

3.25 Concrete stoplogs of bottom outlet of the dam: the consultant,in its design of the dam, provided a bottom outlet with a gate to releasethe reservoir water to the downstream power plants during very dry seasonswhen the water level in the reservoir is lower than the sill level of themain spillway gates. The consultant's design also provided concretestoplogs so that the gate can be raised and hooked up during the normaloperation of the spillway gates. The main civil contractor had been introuble during the placing of the concrete stoplogs due to uneven concretesurfaces contiguous to stoplog guides. One of the stoplogs had fallenduring the placement and was damaged. There was no aeration provision forthe conduit between the stoplogs and the outlet gate. During regulation ofwater releases this could actuate jutting out of stoplog seals and increaseleakage, with possibility of displacement of stoplogs. To avoid any damagedue to cavitation to the stoplogs and the bottom outlet structure, theradial gate downstream was closed and the contractor rectified the abovedamage and replaced the logs. There were also difficulties with thestoplog lifting equipment due to poor design. This also was rectified bychanging designs and lifting methods. The above problems have beendiscussed with the engineering consultants and needed improvements would bemade in connection with the Mtera hydropower project construction. In themeantime, no specific risks are expected as water releases through thebottom outlet are not required until reservoir level goes below the deadstorage level.

3.26 Seepage on the left bank of the Mtera dam: After completion ofthe construction of the dam and partial impounding, a seepage of reservoirwater from underneath the buttress dam was noted through an investigationhole located in the monolith. When the reservoir level reached to about80% of the full supply, it increased from 10 liters/min to 45 liters/min.Although this level of seepage is not very important, grouting was carriedout through the inclined grout holes from the downstream side. However,the grouting has not been very successful, so the drainage has been furtherimproved by drilling additional holes through the rock underneath some ofthe monoliths so that water is collected through a pipe and drainage isprovided into the bottom outlet channel. Further, some seepage of waterhas been noted at some points along the left flank downstream of the dam upto about 500 meters. However, there is no evidence of soil particlescoming out with the seeping water and seepage is within safe limits.TANESCO regularly measures the seepage of water at selected points andchecks water quality for dissolved salts periodically. So far, no unusualor important indications have been seen.

3.27 Kidatu powerhouse - cracks in turbine floor: Some cracks on theturbine floor at unit No. 4 were observed after the commission of theunits, and water oozing from them. The consultant did not consider it veryimportant but investigated it further to make its final recommendations.On review TANESCO's panel of experts and the consultant agreed that thecracks which occurred and will occur in the embedment concrete are notharmful and can be controlled by providing proper surface reinforcementsand a joint.

- 15 -

3.28 Administrative Problems: There were important project executionproblems that persisted almost during the entire construction period.There were port congestion, bad access roads to the Mtera site, fuel andcement shortages, travel restrictions, and also some delays in payments.Although none of these was so important as to interrupt the execution ofthe project, all created complications for the contractors, the consultantand TANESCO.

3.29 Port congestion: Port congestion remained very acute during mostof the construction period. The ships stayed at outer anchorage 3 to 6weeks. However, all the authorities concerned were approached to obtainpriority to the ships carrying the project consignments and this did helpto a great extent to get the commodities cleared generally withinreasonable times.

3.30 Roads: Particularly access roads to the Mtera and also Kidatusites were in a very bad shape and this resulted in lots of hazardoussituations such as breakdown of transport vehicles and delays in transit ofplant and/or equipment and material. Here again, TANESCO did manage tosecure some, at least the lowest level, maintenance of these roads from theMinistry of Works and provided the continuation of transportation.

3.31 Fuel shortage: The general fuel shortage in the country becamevery critical for construction at one stage during 1979-80. However,TANESCO and the consultant warned the contractors in time to build theirstorage facilities roughly corresponding to about 3 to 4 weeks requirementsand disruption in progress was prevented.

3.32 Cement shortage: There was a general shortage of cement in thecountry because of frequent breakdowns, of various equipment at the cementfactory (Wazo Hill and also Tanga). TANESCO with the assistance of itsparent ministry, succeeded in securing enough cement on priority basis andalso adequate storage (about 1,500 tons) was available at project sites.However, the main civil contractor at Mtera had to import about 3,000 tonsof cement from Italy out of the total requirement of about 25,000 tons.

3.33 Travel restrictions: The spread of cholera in the country duringthe construction period created some difficulties regarding the travelingof expatriate personnel in epidemic areas in Tanzania. However, TANESCOobtained necessary permits for the movement of the contractors? personnelfrom local authorities.

3.34 Delays in payments: Most of the contracts provided 60 and 45days' period for provisional payment certificates for civil works andplants respectively. These periods proved to be inadequate particularlyfor the local and/or foreign component of the payments that were to be madeby the external financing agencies. Since most of the finances arearranged between the financing agencies and the Government, variousprocedures had to be followed which were lengthy due mainly to intermediatecommercial banks (sometimes three or four intermediate banks) which wereagents of the contractor or financing agency. The contractors sometimeshad difficulties in mobilizing sufficient financing to compensate for suchdelays.

- 16 -

Ecological Aspects

3.35 A general ecological review of the Kidatu site and the Mterareservoir was completed in 1970 (financed by SIDA) in context of theecological aspects of the development of the Great Ruaha Basin. Followingthis general review, an in-depth study of some aspects of the ecology wascompleted in 1972 during the course of construction of the First StageKidatu project. These studies did not indicate negative effects whichwould impair the feasibility of the damming at Kidatu and also at Mtera. Afurther in-depth study was also completed for the Mtera reservoir on about35 ecological subsubjects such as vegetation and wildlife, soil erosionand sedimentation, implanting, limnology, disease ecology, relocation,etc. Recommendations resulting from this study were discussed with theBank and measures were taken to safeguard certain environmental aspects.These are given below (those not included in the original design aredetailed in para. 3.57):

3.36 Relocation: The inhabitants of the areas later submerged by theMtera reservoir were relocated at Migoli village after many investigationsregarding the selection of the best area for resettlement. Migoli villageis about 27 km from the Mtera dam towards Iringa. About 2,000 persons wereresettled at Migoli; apart from some houses, a dispensary, a communityhall, house for medical assistance have been constructed through theproject funds and additional SIDA funds of about $2.0 million. Watersupply, school, etc. mostly financed by SIDA have been provided by theregional authorities.

3.37 Relocation of Iringa-Dodoma road: A stretch of the Iringa-Dodomaroad crossing the river about 6 km upstream of the dam was located belowthe reservoir level. Therefore, about 34 km of this road were relocatedand constructed so as to pass over the crest of the dam before impoundingthe reservoir. The old Iringa-Dodoma bridge about 6 km upstream wasdemolished.

3.38 Extension of the Ruaha National Park: Extension to the RuahaNational Park was recommended by the Bank with a view to protecting thewild animals which would be attracted by the reservoir. The originalboundaries of the park have been expanded to the reservoir by the concernedauthorities (ministries and the local government). The entire reservoirarea has been declared as the game control area.

3.39 Foreshore agriculture: The water shored in the soil when thelake level sinks will be sufficient for development of foreshorecultivation in part of the area. Regional authorities have still toinitiate concrete measures to prepare land use plans and toward research asto the crops that can be grown utilizing holding capacity of the soils.Programs have yet to be worked out for overhead irrigation from thesemi-isolated northern appendix (logi) of the reservoir.

3.40 Fisheries: Action initiated by the federal and local authoritieshas also been taken to tap the fish potential of the lake. Systematicdevelopment of fisheries is underway. A minimum yield of 3,000 tons perannum of fish is expected from the reservoir.

- 17 -

3.41 Soil erosion: No action program has been drawn up by theregional authorities for preventive measures against any soil erosion andconsequent silting of the reservoir. The inflow of about 8 to 10 milliontons per annum of sediment is not significant for the filling of thereservoir by silt soil erosion, but the washing away of agriculturallyvaluable soil is important.

3.42 Disease control: Health hazards due to bilharzia appear to becertain as is the case with the other natural lakes in the vicinity.Adequate arrangements for hygiene and health education are necessary. Noaction program has been worked out so far by the regional authorities dueto budgetary restrictions and other priorities.

3.43 Aquatic weeds: There is a possible menace of aquatic weeds suchas water hyacinth, but necessary preventive measures have not yet beentaken.

3.44 Environmental changes between Mtera and Kidatu: Damming at Mterawill have little influence on human or wildlife, particularly in view ofthe fact that there are only a few settlements at the vicinity of thisstretch of the river. The changes in the hydraulic regime will decreasethe risk of harmful erosion at the bridges and other places because theregulated flow by the reservoir operation will increase the dry seasondischarges while cutting the peak flow of March - April.

Performance of Consultants and Contractors

3.45 Consultants: The main consultant for this project was retainedin April 1975. The consultant prepared the feasibility report, design ofthe project, bid documents, specification, and carried out bidding, bidevaluation, construction supervision and the project management as it didfor the first stage development. The overall performance could beclassified as satisfactory. However, considering the consultant'slong-standing history of professional association with TANESCO, there wereunexpected shortcomings as explained below.

3.46 The consultant's failure to document properly the main civilcontract for the Mtera site, in one case, led to some trouble and gaveadvantage to the contractor to make a claim of TSh 10 million regardingadjustment of expatriate salaries. The consultant had issued an addendumduring the bidding that only 50% of expatriate salary adjustments would becovered by the employer. However, this addendum had not been sent to theprospective bidders by registered mail and this change had not beenindicated in the corrigenda to the addendum. Although it is believed thatall other prospective bidders had received the addendum, the Mtera sitecontractor told the employer that he did not receive the addendum; thereby,claiming the right to have 100% compensation of expatriate salaryincreases as originally indicated in the bid documents.

3.47 The consultant's cooperation with the employer's field office wasreasonably good but there were some interruptions in coordination. Forexample, in respect of variation orders, the consultant usually was notpunctual in submitting its detailed evaluation of variation in the

- 18 -

quantities of works and reratings of unit prices and daily reports fordrilling, grouting, drainage and anchors, etc. This created some strainfrom time to time between the field office of TANESCO and the consultant.

3.48 Detailed geological mapping regarding the geological structureand conditions of the completed foundations before concreting have not beenclearly done though this was a principal work of the consultant. Thesemaps are sketchy and somewhat difficult to interpret.

3.49 Contractors: The performance of all the contractors on thisproject in respect of their tendered works has been reasonablysatisfactory. The only local contractor also made strong efforts tocomplete works as originally scheduled but failed to do so purely due tothe difficulties that local contractors have in importing essential plantand materials and spares. However, delays in completion of its works(relocation of the road and construction of the employer's village) did nothave any negative effect on the final completion date of the project. Theobjectives of all the contracts with respect to the original constructionprogram for various works at Mtera, Kidatu and Morogoro sites weregenerally satisfied.

3.50 The main civil contractor at Mtera took every opportunity to makea claim, though its unit prices offered for the construction of the workswere unusually high compared to other contractors doing similar jobs inother countries.

Main Contracts

3.51 The main contracts are summarized in Annex 3. The importantdesign changes are summarized below.

Important Changes in Original Design

3.52 Before and during appraisal the Bank appraisal team hadrecommended various design modifications to the original design such asincrease of the thickness and a gentler slope of the buttresses, biggerspillway dimensions, etc. After bidding some additional recommendationswere made regarding the expansion of construction schedule and method ofpouring concrete. During construction many modifications had been done tothe final design on the basis of the results of excavations, soil tests,and additional drilling, etc. as usual for this type of construction.However, the most important design modifications are given below.

3.53 In respect of the hydraulic studies as initially done by theconsultant for the design of the spillway, the panel of experts pointed outthat:

(i) model studies dealt more with selection of appropriate costprofile than with important aspects of energy dissipation;

(ii) studies did not indicate to what shape the surface between theend of the chute and the river edge should be trimmed tofacilitate proper flow conditions.

- 19 -

Consultants generally agreed to the suggestions of the panel and repeatedhydraulic model tests to ascertain correct velocities of flow, water

profiles, and information of hydraulic jump, etc. under various flow

conditions and tailwater elevations.

3.54 The consultant's initial design was to leave the spillway chuteunlined. Detailed hydraulic model studies and geological investigations

showed that the spillway chute should be concrete lined to avoid costlyrepairs during the operation.

3.55 During the construction, the panel of experts (para 4.02),

subsequent to their detection of some significant rock fractures exposed in

the near vertical cut walls forming the upstream limits of the excavation,recommended strengthening the left abutment slopes in the vicinity of the

dam. These fractures were roughly parallel to the original ground surface

and about 1 m to 2.5 m below it and steeply dipping towards the river,

which could cause slides in the area immediately upstream and downstream of

the abutment. As a remedial measure, the experts recommended providingtensioned rock bolts of high grade steel at critical locations. This wasaccepted by the consultants and done. About 50 tensioned rock bolts were

installed.

3.56 Instrumentation on the dam such as strain gauges, peizometers,reservoir, water level recorders, thermal probes (to monitor concretetemperatures during setting) and devices for the measurement of drainage

water pressures, recommended by the panel of experts was generally accepted

by the consultants and these were put in place during the construction.

3.57 Moreover, as was mentioned in Chapter 1, the following additional

works were accomplished though these were not included in the consultant'soriginal design.

(a) A floating boom was constructed about 2.3 km in length at about 2km upstream of the dam to catch the floating debris;

(b) Bush was cleared at negligible cost up to about 2.3 km upstream

of the dam in the area of about 140 hectares below the fullsupply level of the reservoir;

(c) The original ecology study recommended that the displacedinhabitants of the project area be resettled at a new villagewhich would be constructed at a new place about 3 km far from the

lake. Water supply would be provided by a well. Duringconstruction water could not be found at the site selected in the

ecological study, and finally the villagers were resettled in theold village of Migoli about 27 km from the Mtera dam towards

Iringa.

- 20 -

IV. INSTITUTIONAL PERFORMANCE

Management and Organizational Effectiveness

4.01 In general, TANESCO has worked with competence and carried outits project preparation, procurement and construction supervisionobligations satisfactorily.

4.02 Apart from the consultant, TANESCO was assisted by a part-time"panel of experts" consisting of three civil engineers (these arespecialists on design, general civil engineering and concrete structures),one geologist/general civil engineering specialists and one claimsadvisor. Moreover, two advisors/experts on general construction andplanning (one at Mtera site and one at the headquarters of TANESCO) hadhelped TANESCO to overcome the difficulties encountered during theconstruction. Costs of the panel and two advisors were covered from theproceeds of the Bank/SIDA joint funds. TANESCO's panel and theadvisors/experts' works were useful and satisfactory.

4.03 TANESCO's operations and the workload of the headquarters haveabout tripled during the last decade. Fortunately, TANESCO hassatisfactorily changed and rearranged practices and methods to overcomeincreasing operational loads.

4.04 The help of the local authorities through the coordination ofTANESCO (Regional Development Directors' headquarters staff at Iringa andDodoma), particularly regarding the implementation of the ecologicalstudies, has also been significant.

4.05 The quarterly reports, prepared by the consultant and TANESCO,and the panel's reports on the progress of the project construction werewell prepared and invaluable to the Bank supervisory staff.

Training

4.06 TANESCO has developed a sound training program with theappropriate objectives for manpower development through the help of SIDAand the Bank Group for many years. It has now a manpower development andtraining unit with four full-time officers at headquarters and regionaltraining officers who would follow up training and personnel activities.TANESCO spends about US$1 to 2 million every year for training.

4.07 TANESCO has a technical institute (TTI) at Kidatu where attechnician level, electricians, general mechanics and diesel mechanics arebeing trained. Forty-eight students per year are admitted (16 in each ofthe three categories) and approximately 42 graduates annually. Since theappraisal about 170 students have graduated from the TTI. The staffconsists of one principal, 13 techical instructors and 6 general academicteachers. There are dormitory facilities for about 180 students.

- 21 -

4.08 From 1978 to 1981, through the project loan (1306-T-TA) the Bankfinanced an overseas management training program for 27 high level TANESCOofficials, of whom 21 have remained with TANESCO. This training programwas mainly carried out by a training consultant and has substantiallyincreased TANESCO's operational efficiency and improved decision-makingpractices. This program covered the training of mid management andprofessional staff in the fields of power planning, design, construction,stock control and supplies, auditing, billing/collection, costaccounting/power company accounting, computer programming,financing/economic analysis, manpower planning and development andstatistics. The Bank missions prepared draft terms of reference of eachtrainee and approved the program as finalized by TANESCO and their trainingconsultant, monitored the program during its implementation, identifiedweaknesses and improved the program as necessary. The Bank missions alsointerviewed trainees to evaluate their knowledge supplemented as necessary,and pointed out documents for further self development.

4.09 During the period of 1977-81, an additional 60 TANESCO staff weretrained funded by the Government and various international financingorganizations other than the Bank Group. TANESCO also has a smallcommercial school in Dar es Salaam established in 1978, which offers basiccourses in accounting, meter reading, storekeeping and procurement. Thisschool has 3 teachers who train about 50 clerks per year.

4.10 In the early 1970s TANESCO employed about 50 expatriates. At thetime of the appraisal there were 17; at the time of project completionthere were only 6 expatriates, whose work is purely technical. This islargely due to the success of the training programs described above, andis a remarkable achievement.

V. FINANCIAL AND RELATED ASPECTS

Financial Arrangements

5.01 A comparison of the actual and the estimated financing of theproject in millions of Tanzania shillings and US dollars, converted at US$1= TSh 8.25, the average exchange rate for the loan, and at the appraisalrate of US$1 = TSh 8.05, is given below. The appraisal estimates have beenadjusted to reflect the longer implementation period, 1975-1981.

- 22 -

Actual Appraisal Estimate Actual over (under)1975-1981 1975-1981 Appraisal Estimate

TS US$ m % TSh m US$m x ThU$m

Application of Furnds

Kidatu Project 889.7 107.8 35.8 626.0 77.8 32.7 263.7 30.0Ongoing Projects and

Other Construction 1,120.1 135.8 45.1 1,021.5 126.9 53.3 98.6 8.92,0C9.8 243.6 80.9 1,647.5 204.7 86.0 362.3 38.9

Interest during Construction 57.7 7.0 2.3 188.7 23.4 9.9 (131.0) (16.4)Total Construction

Expenditures 2,067.5 250.6 83.2 1,836.2 228.1 95.9 231.3 22.5

Increase in Working Capital 326.3 39.6 13.2 79.1 9.8 4.1 247.2 29.8Other 89.5 10.9 3.6 - - 89.5 10.8

Total Application of Funds 2,483.3 301.1 100.0 1,915.3 237.9 100.0 568.0 63.2

Sources of Furxns

Internal Cash Generation 1,029.2 124.7 41.4 1,396.0 173.4 72.8 (366.8) (48.7)Less: Debt Service (393.0) (47.6) (15.8) (508.2) (63.1) (26.5) (115.2) (15.5)

Dividernds (7.8) (0.9) (0.3) (153.5) (19.1) (8.0) (145.7) (18.2)

Net Internal Cash Generation 628.4 76.2 25.3 734.3 91.2 38.4 (105.9) (15.0)

IB8D loan 251.7 30.5 10.1 241.5 30.0 12.6 10.2 0.5SIDA Credit 155.3 18.8 6.3 149.7 18.6 7.8 5.6 0.2KfW Loan 236.1 28.6 9.5 193.2 24.0 10.1 42.9 4.6EFE 58.7 7.1 2.4 - - - 58.7 7.1Existing/Other Loans 526.0 63.8 21.2 353.1 43.9 18.4 172.9 19.9

Total Borrowings 1,227.8 148.8 49.5 937.5 116.5 48.9 290.3 32.3

Equity Contribution 581.3 70.5 23.4 226.7 28.1 11.8 354.6 42.4Consumer Contribution 45.8 5.6 1.8 16.8 2.1 0.9 29.0 3.5

Total Sources of Funds 2,483.3 301.1 100.0 1,915.3 237.9 100.0 568.0 63.2

- 23 -

5.02 Construction expenditures were above estimate for reasonsoutlined in paragraphs 3.13 to 3.19. Net internal cash generation provided23.3% of total financing requirements compared with 38.4% estimated atappraisal (32.2% for 1975-1980). Internal cash generation wassignificantly lower than forecast (paragraphs 5.05 and 5.06) but lower debtservice, reflecting longer grace periods for borrowings on-lent to TANESCOby Government, and small dividend payments, served to offset this.Borrowings, equity contributions by Government and consumer contributionswere above appraisal estmates. Working capital increased substantiallyover the period, reflecting excessive levels of accounts receivable (127days sales in 1980) and of inventories (including a relatively highproportion of obsolete stocks).

Accounting and Audit

5.03 TANESCO's accounting staff are competent and procedures aregood. TANESCO has maintained adequate records and, except in FY80 andFY81, has substantially met the audit covenant which requires its financialstatements to be audited by independent auditors acceptable to the Bank(the Government-owned Tanzania Audit Corporation, TAC) and submitted to theBank within five months after the close of the fiscal year. Since 1980,the computer which TANESCO uses to maintain its records has been operatingeffectively only intermittently and, as a result, billing and otheraccounting procedures have been severely affected and the audited accountsfor the past two years have not been submitted to the Bank as required.Once the new computer, now on order, has been installed, these problems areexpected to be resolved.

Financial Performance and Compliance with Covenants

5.04 Appraisal estimates and actual Income, Balance Sheets and FundsFlow Statements covering 1975 to 1981 are given in Annexes 6, 7 and 8.

5.05 The following table indicates percentage variations in financialoperating performance compared to appraisal estimates.

1975 1976 1977 1978 1979 1980 1981

Electricity Sales - 2 - 9 -18 -14 -13 -12 -19Ave. Tariff Levels - 1 2 7 -12 -13 6 6Revenues - 3 - 7 -10 -25 -24 - 7 -14Operating Expenses 3 3 - 3 - 7 - 4 1 12

(excl. depreciation)Operating Income -12 -16 -17 -40 -41 -12 -32

(before depreciation)Internal Cash Generation -14 -33 -20 -41 -37 - 9 -29

5.06 Revenues were below forecast due to lower than anticipatedelectricity sales and average tariffs; operating expenses were higherlargely because of increases in fuel costs amounting to nearly 23% perannum. During the project implementation period, TANESCO increased tariffsonly twice: by 40% in June 1976 and by 42% in December 1979. These tariff

- 24 -

adjustments were insufficient to enable TANESCO to achieve the required 7%return on revalued net fixed assets in operation, except in 1980. This,combined with excessive accounts receivable (paragraph 5.02) resulted incash shortages for the company throughout the period. The current ratiohas been positive throughout but is based on inventory figures that containa significant obsolescence factor. The Debt/Equity Ratio has been moreconservative than estimated at appraisal due to larger than expectedgovernment equity contribution. Although internal cash generation has beenlower than estimated, debt service coverage was in line with the forecastbecause of reduced debt service (paragraph 5.02).

VI. BANK PERFORMANCE

Overall Performance and Working Relationships

6.01 The Bank played an important role in the preparation of theprojects and in coordination and negotiation between the colenders. TheBank provided a good project construction supervision unit through thepanel and the two advisor/experts. TANESCO is very satisfied with thepanel and supervision advisors and continued to use them when necessaryeven after completion of the project. The Bank's environmental expert'sinput regarding the implementation of the ecological report was veryhelpful and useful.

6.02 The most important supervisory relationships were those betweenthe Bank and TANESCO and these were generally very good. The Banksupervision missions did help acceleration of the contractor's mobilizationand the Bank provided the supplemental loan on time for the continuation ofconstruction. The Bank has systematically guided and encouraged TANESCO'straining program and the program's achievements show the effects of propercooperation between the implementation agency and the Bank.

VII. LESSONS LEARNED

7.01 The declining general economic situation of the country, whichwas not generally predicted, was the main cause for the actual growth ratein energy and capacity demand of the grid from 1976 to 1981 having beensubstantially lower than projections made during appraisal. The mostimportant lesson relates to the initial cost overrun. In order to preparerealistic cost estimates and a corresponding financing plan, cost estimatesshould be reviewed by an independent cost consultant as early as possiblein the preparation of the project, preferably before the appraisal of theproject. Despite this, the tender prices could still be different from theappraisal estimates because it is difficult to assess in advance thecontractor's or the supplier's cost of doing business in the country at aparticular time.

- 25 -

7.02 Another important lesson is that local indices for the

revaluation of assets should be used with caution in Tanzania. To providea more satisfactory test than a rate of return thus derived, the next

project in this context might include a cash covenant instead of a rate ofreturn covenant. However, a comprehensive study still needs to be carriedto establish the most suitable method in this regard.

7.03 Ihe other important lessons to be learned could be summarized asfollow:

(a) The engineering consultant and the employer should be punctilious

regarding the proper documentation and punctual mailing of thebid documents not to create additional reasons for contractors'claims;

(b) Training is the fundamental means by which technology istransferred to a developing country, thus a training component,including management training should be included in projects;further, the policy for replacement of expatriate personnel bynationals must be fully coordinated with a training program;

(c) Careful and knowledgeable supervision is essential and, apartfrom the main engineering consultant, the services of a panel ofexperts and also some additional advisors should be provided whennecessary; services of the panel and advisors could be part-timeand cost of these services will be very minimal;

(d) Timely payments are very important for the healthy progress ofthe project implementation and bid documents should clearlystipulate the timing between the engineer's certificate and theBank's order for payments to the contractor's intermediate bankagent;

(e) The quality of hydraulic model studies is extremely important insuch projects. Some small design changes might give the borrowersignificant advantages during the operation of the project;

(f) Instrumentation on the dams and the recording of the initialmeasurements regarding seepage and the artesian pressures are

important and these instruments should be included in the biddocuments because unexpected readings can occur even afterconstruction;

(g) The exceptionally large ecological component of the projecttaught that specific supervision of ecological aspects iswarranted from time to time by environmentalists. It is alsoimportant that institutions should be made aware of the long term

objectives of ecological precautions; and

(h) The local engineering staff should be made available ascounterparts to the main engineering consultant in order toacquire necessary knowledge and experience in designing andbuilding power facilities.

TANZANLA

KIDATU HYDROELECTRIC PRWOECT SECOND STAGE

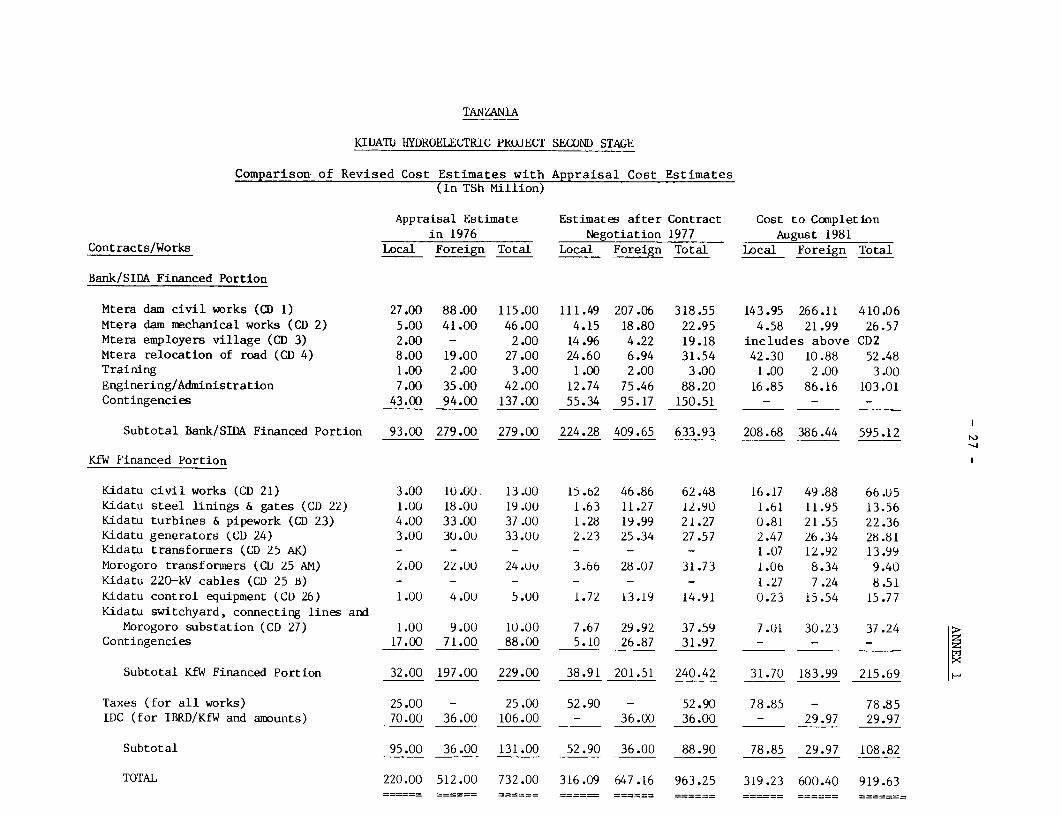

Comparison- of Revised Cost Estimates with Appraisal Cost Estimates(In TSh Million)

Appraisal Estimate Estimates after Contract Cost to Completionin 1976 Negotiation 1977 August 1981

Contracts/Works Local Foreign Total Local Foreign Total Local Foreign Total

Bank/SIDA Financed Portion

Mtera dam civil works (CD 1) 27.00 88.00 115.00 111.49 207.06 318.55 143.95 266.11 410.06Mtera dam mechanical works (CD 2) 5.00 41.00 46.00 4.15 18.80 22.95 4.58 21.99 26.57Mtera employers village (CD 3) 2.00 - 2.00 14.96 4.22 19.18 includes above CD2Mtera relocation of road (CD 4) 8.00 19.00 27.00 24.60 6.94 31.54 42.30 10.88 52.48Training 1.00 2.00 3.00 1.00 2.00 3.00 1.00 2.00 3.00Enginering/Administration 7.00 35.00 42.00 12.74 75.46 88.20 16.85 86.16 103.01Contingencies 43.00 94.00 137.00 55.34 95.17 150.51 - - -

Subtotal Bank/SIDA Financed Portion 93.00 279.00 279.00 224.28 409.65 633.93 208.68 386.44 595.12

KfW Financed Portion

Kidatu civil works (CD 21) 3.00 10.00. 13.00 15.62 46.86 62.48 16.17 49.88 66.05Kidatu steel linings & gates (CD 22) 1.00 18.00 19.00 1.63 11.27 12.90 1.61 11.95 13.56Kidatu turbines & pipework (CD 23) 4.00 33.00 37.00 1.28 19.99 21.27 0.81 21.55 22.36Kidatu generators (CD 24) 3.00 30.Ou 33.00 2.23 25.34 27.57 2.47 26.34 28.81Kidatu transformers (CD 25 AK) - - - - - - 1.07 12.92 13.99Morogoro transformers (CD 25 AM) 2.00 22.00 24.Uu 3.66 28.07 31.73 1.06 8.34 9.40Kidatu 220-kV cables (CD 25 i3) - - - - - - 1.27 7.24 8.51Kidatu control equipment (CD 26) 1.00 4.0U 5.00 1.72 13.19 14.91 0.23 15.54 15.77Kidatu switchyard, connecting lines and

Morogoro substation (CD 27) 1.00 9.00 10.00 7.67 29.92 37.59 7.01 30.23 37.24 >Contingencies 17.00 71.00 88.00 5.10 26.87 31.97 - - -

Subtotal KfW Financed Portion 32.00 197.00 229.00 38.91 201.51 240.42 31.70 183.99 215.69 a

Taxes (for all works) 25.00 - 25.00 52.90 - 52.90 78.85 - 78.85IDC (for IBRD/KfW and amounts) 70.00 36.00 106.00 - 36.00 36.00 - 29.97 29.97

Subtotal 95.00 36.00 131.00 52.90 36.00 88.90 78.85 29.97 108.82

TOTAL 220.00 512.00 732.00 316.09 647.16 963.25 319.23 600.40 919.63

TANZANIAKIDATU HYDROELECTRIC PROJECT

SECOND STArE DEVELOPMIENTCONSTRUCTION SCHEDULE

IMTERA DAM)

ACTIVITIES YEAR OF CONSTRUCTION 7 9s1791go19

TEMPORARY WORK& RIICbI 'C,IKOI,a.p.OE I0oo.

RE L CEC.. AT s, IEO2

DODOM. - I INGA --

ROAD E--.RIO

MCCHAIJICAE.....ORWS

SPILLWVAY CPil~ d ln.,505

OTER NIAWORKS G-5TI.cav 'R

SPILLWAY Cmure ..-d 01- 1. .4 ""~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~AWR002I75

N A 0 r- - i F X 3t X =~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~t lP- -

> o X I 0 1 t 0 0 l 1 0 1 f l I 0

41 ~ ~~~ - - -_ - - - --- '.,-,.,,-. ',','''-- - -- -lll ___ I lu l= i

Inc00 PWWS Ui -n SI m4EOWG

ncdC,d 111 1 1 1~W- ' l I 1 - - - I I

pWOdO, di_ r,0 C ISf ~W j

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~1 ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ 0-

--W-, M..-o ,. Si00 ! ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~C G.,-

3SflOH)t3AOd IlflY 4 1 J tO NOISN3IX3)3fl0)HC.S-, NOIiDfMlHSNOD

IN tWdO13A3O 3DV15 cINOJ3S

VtNVZNVlN

TANZANIA

GREAT RUAHA PROJECT - PHASE II

Statement of Contracts and Works

Tendered CompletionContract No. Sum Cost Scope of the Works

CD 1 363,554,247 410,054,611 Temporary Works: Staff camps, labor camp, communitycenter, school, dispensary, police station, postoffice, and other temporary facilities.

Works Ftera Dam: Concrete structure of the buttress typewith connecting gravity dam at the right bank, crestlength 260 meters, crest width 10 meters and maximumheight 45 meters.

Road: Relocation of the northern and southern parts ofIringa-Dodoma road (northern part - about 9 km) andsouthern part (about 3.3 km).

Miscellaneous: Civil works pertainirg to floatingsteel boom, new settlement public facilitybuildings, etc.

DC 2 - Mtera Mechanical Works 24,448,277 26,571,028 Four radial gates with hoists and embedded parts, one 0bulkhead gate and four sets of embedded parts, onegantry crane with rails and beam, one bottom outletgate with hoist and one set of embedded parts forconcrete stoplogs.

CD 3 & 4 - Employers Village & 56,216,233 52,483,851 (a) Fourteen family houses, guest house (2 blocks) withRelocation of Road swimming pool, few employers office (2 blocks),

ancillary works (sanitary, electricalinstallations, etc.)

(b) Relocation of southern part of Iringa-Dodoma road(22 kms), access road including bituminoussurfacing to the employers village and ancilliarytemporary works.

CD 5- Bush clearance 0.95 0.85 Bush clearance up to 2.3 km upstream of the dam below xthe reservoir level (about 150 hectares).

1.76 1.78 Supply of steel booms. 00.64 0.65 Supply of towing and rowing boats.0.20 0.25 Archaelogical survey/salvage in the submergence area of

the Mtera reservoir.1.20 0.90 Water supply investigations for new settlement.

CD 21 68 ,475,995 66,052,554 Concrete lining of cylinder gate shafts 3 & 4 and

removal of temporary concrete walls in intakes 3 &4, installation of permanent drainage pipes inpenstock 3 & 4, concrete structures forinstallation of generators 3 & 4 together withappurtenant finishes, extension of cable culvertsand foundations for connecting lines at pothead,concreting roads in the access tunnels.

CD 22 - Penstock Steel Linings 14,100,046 13,562,554 Two penstock steel linings, one sliding gate withand Gates lifting wires on a drum and spares, two cylinder

gates with hoists and appurtenant equipment andspares.

CD 23 - Turbines and Pipework 22,765,320 22,351,637 Two complete turbine units with governors with allappurtenant equipment, all necessary pipes, valves,supports, etc. for supply of cooling water, twopumps, pipes, valves for dewatering of draft tubeswith all appurtenant equipment.

CD 24 - Generators 29,072,719 28,809,905 Two complete vertical shaft salient pole generatorswith excitor and with all appurtenant equipment.

CD 25 AK - Transformers for Kidatu 13,968,630 13,993,420 Seven single-phase, set-up generator transformers,complete with all appurtenant equipment for Kidatupower plant (20 MVA, 10.5 kV - 220 kV).

CD 25 AM - Transformers for Morogoro 10,368,100 9,394,700 Four single-phase, 30 MVA transformers with allappurtenant equipment plus two 20-MVA regulatingtransformers all for Morogoro.

CD 25 B - 220 kV cables 9,394,986 8,509,631 Six single-phase, 220 kV cables with potheads,including fire protection measures.

CD 26 - Generator switchgear, control 16,407,100 15,767,743 Generator switchgear, control equipment, extension ofequipment, local power and lighting local power and lighting installation.

CD 27 - 220 kV switchyard, connecting 40,088,630 37,237,117 220-kV lightning arresters and pull-off structure for

lines, Morogoro S/S the pothead, 220-kV switchyard at Kidatu, 220-kVconnecting lines with all civil works, Morogorosubstation with civil works.

TANZANIA

KIDATU HYDROELECTRIC PROJECT STAGE II

PROJECT COMPLETION REPORT

Internal Rate of Return

(TSh Million)

Attributable Operation Deflated 2/Kidatu Distribution & and Total

Years II Transmission Maintenance Cost Benefits 1/ Deflator Cost Benefits Net Benefits- …-- Costs…

1976 2 2 0 57.7 3 0 - 31977 48 48 0 61.0 79 0 -791978 210 210 0 74.6 281 0 -2811979 250 22 272 0 82.4 330 0 -3301980 283 23 306 0 85.0 360 0 -3601981 15 25 6 46 62 90.1 51 69 181982 29 7 36 86 100.0 36 86 501983 33 9 42 178 116.0 42 153 1111984 9 9 262 116.0 9 226 2171985 11 11 342 116.0 11 295 2841986 13 13 384 116.0 13 331 3181987 15 15 424 116.0 15 365 3501988 15 15 465 116.0 15 401 3561989 15 15 502 116.0 15 433 4181990-2009 15 15 502 116.0 15 433 4182010 80 15 15 502 116.0 95 433 3382011-2020 15 15 502 116.0 15 433 418

Rate of Return: 18.1%

1/ On the basis of 20% system losses.2/ Based on T¢65 per kWh in 1981 and 1982 and T¢97.5 per kWh in 1983 and thereafter due to expected tariff

increase of 50% in 1983. Rate of return on the basis of T¢65 per kWh for the entire period is 15.5%.

-33 - ANNEX 5

KIDATU HYDROELECTRIC PROJECT STAGE II

PROJECT COMPLETION REPORT

Comparison of Alternative Programs

Equalizing Discount Rate(TSh Million)