Workshop September 2, 2008 Agenda Consolidation -Important Dates -Reorganization Plan Overview...

34

Workshop September 2, 2008 Agenda Consolidation -Important Dates -Reorganization Plan Overview -Financials Q & A (Board) Public Comments

-

Upload

alexus-sutter -

Category

Documents

-

view

215 -

download

0

Transcript of Workshop September 2, 2008 Agenda Consolidation -Important Dates -Reorganization Plan Overview...

WorkshopSeptember 2, 2008

AgendaConsolidation -Important Dates -Reorganization Plan Overview -FinancialsQ & A (Board)Public Comments

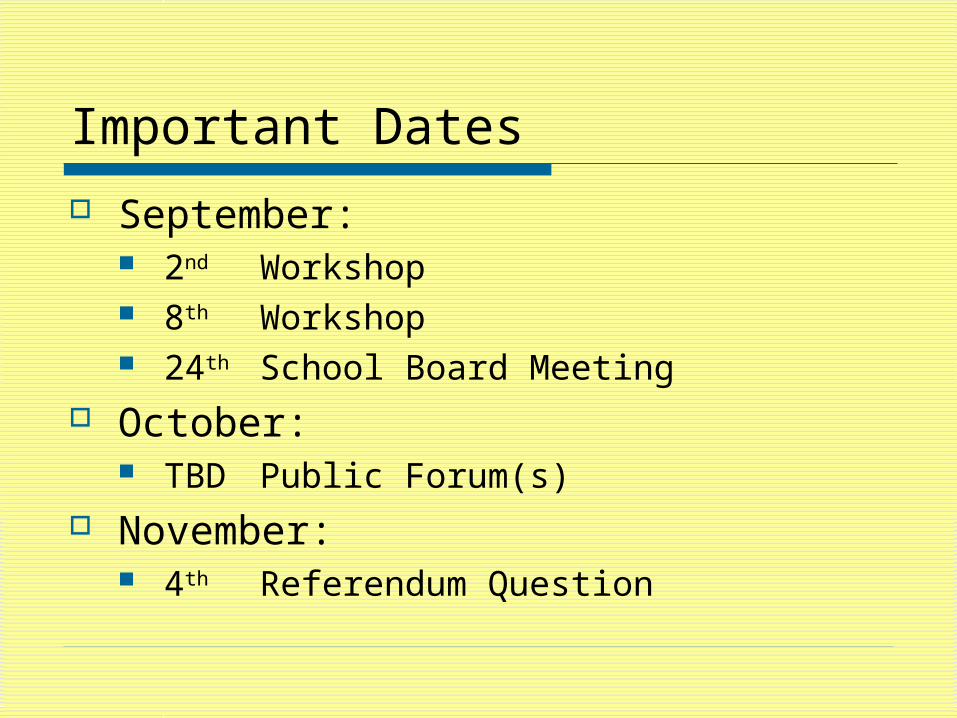

Important Dates

September: 2nd Workshop 8th Workshop 24th School Board Meeting

October: TBD Public Forum(s)

November: 4th Referendum Question

Reorganization Plan Overview

RPC Membership Meeting Attendees

Reorganization Plan Overview

District Name Operational Date Units Consolidating Intent

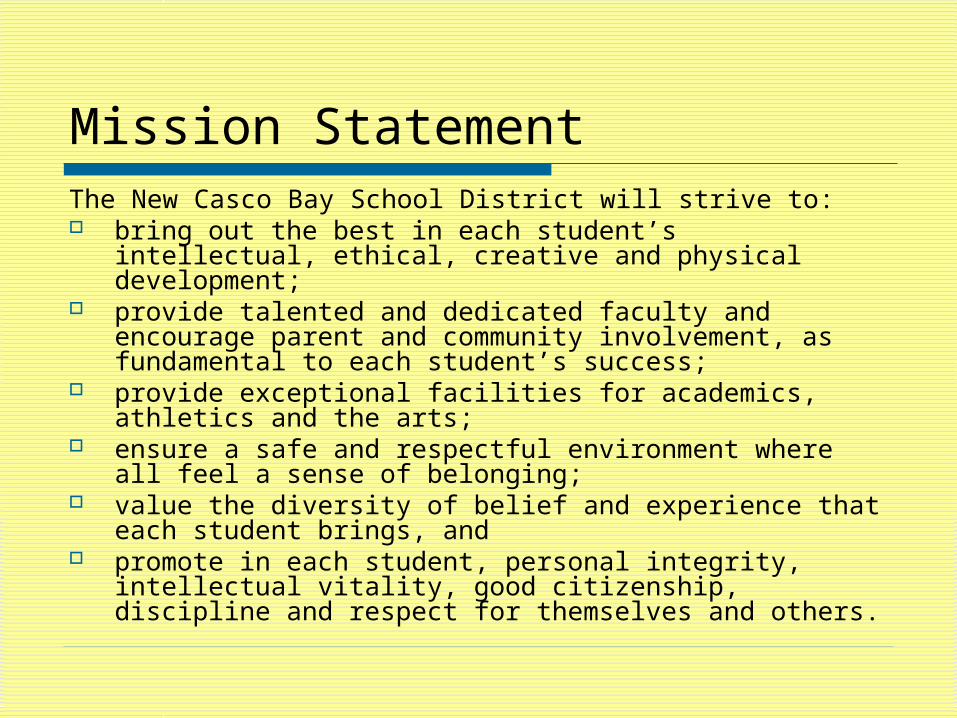

Mission StatementThe New Casco Bay School District will strive to: bring out the best in each student’s intellectual,

ethical, creative and physical development; provide talented and dedicated faculty and encourage

parent and community involvement, as fundamental to each student’s success;

provide exceptional facilities for academics, athletics and the arts;

ensure a safe and respectful environment where all feel a sense of belonging;

value the diversity of belief and experience that each student brings, and

promote in each student, personal integrity, intellectual vitality, good citizenship, discipline and respect for themselves and others.

Reorganization Plan Overview

Potential Educational Program Enhancements (Focus for September 8th Workshop)

Reorganization Plan Overview

Opportunities for Students/Staff (Focus for September 8th Workshop)

Reorganization Plan Overview

Governing Body/Terms/Voting Method Board Composition 3-year Staggered Terms One Person:One Vote

Reorganization Plan Overview

Disposition of Real and Personal School Property Exceptions:

Lunt/Plummer-Motz Campus 12 Acre Parcel at 51 Woodville Road

Reorganization Plan Overview

Disposition of Existing School Indebtedness/Lease Purchase Obligations State Qualified Debt is Assumed by the

RSU Local Debt will stay a Local Responsibility Lease Purchase Obligations become the

Responsibility of the RSU

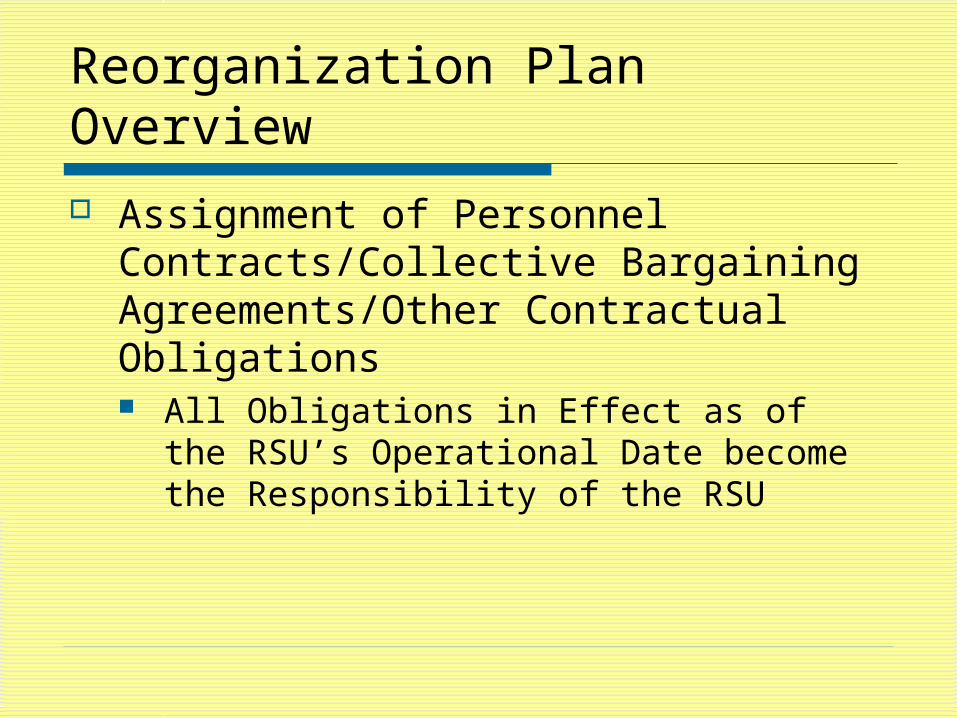

Reorganization Plan Overview

Assignment of Personnel Contracts/Collective Bargaining Agreements/Other Contractual Obligations All Obligations in Effect as of the RSU’s

Operational Date become the Responsibility of the RSU

Reorganization Plan Overview Disposition of Existing Funds/Financial

Obligations (Includes: Undesignated Fund Balances/Trust Funds/Other School Funds) Financial Obligations to be met prior to RSU

Formation, as possible Equitable treatment of all municipalities

regarding unsatisfied financial obligations Balances and Remaining Funds Transfer to the

RSU (Falmouth exclusion due to cost-sharing agreement in Reorganization Plan)

Reorganization Plan Overview

Transition Plan Transition Committee as Successor to

RPC Voter Education Budget Preparation Amendments to Plan

Reorganization Plan Overview Transition Timetable

Nov. 4, 2008: Reorganization Plan Referendum; if adopted

Jan., 2009: Election of RSU Board members Thru Spring, 2009: Superintendent hire,

Budget Development, Policy Review/Consolidation

Spring, 2009: B.V.R. (Referendum) for RSU Budget FY ’09-’10

July 1, 2009: New Casco Bay RSU Operational

Reorganization Plan Overview

Transition Plan Components Interim Rules/Officers Selection of Superintendent Budget Development Authority of RSU Board Personnel Policies

Reorganization Plan Overview

Public Hearings November 13, 2007 November 27, 2007 November 29, 2007 January 9, 2008

Reorganization Plan Overview

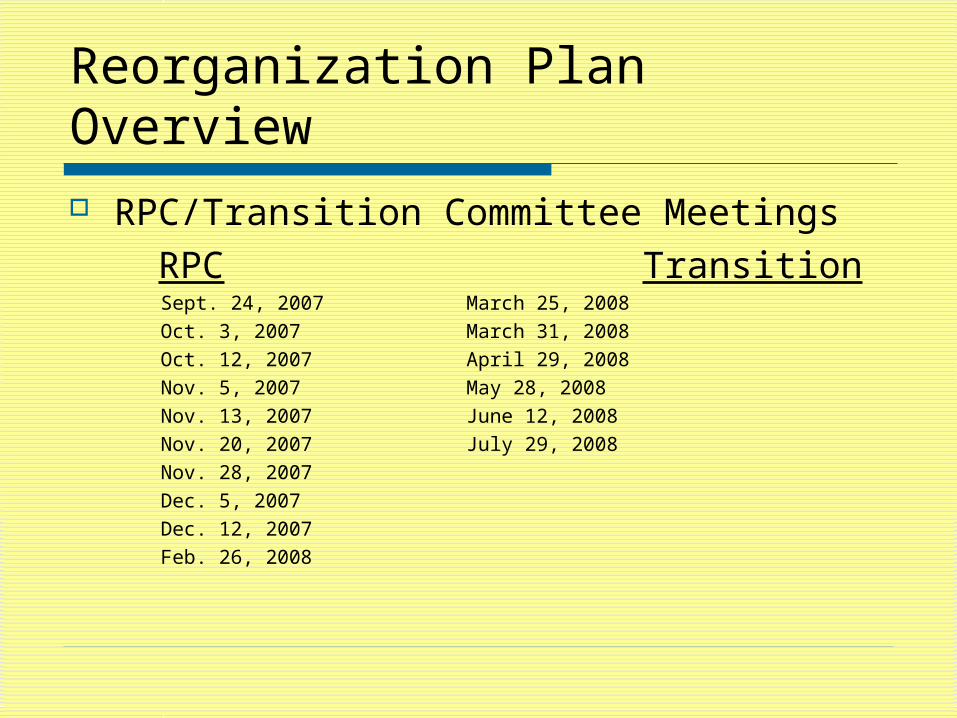

RPC/Transition Committee Meetings RPC Transition Sept. 24, 2007 March 25, 2008 Oct. 3, 2007 March 31, 2008 Oct. 12, 2007 April 29, 2008 Nov. 5, 2007 May 28, 2008 Nov. 13, 2007 June 12, 2008 Nov. 20, 2007 July 29, 2008 Nov. 28, 2007 Dec. 5, 2007 Dec. 12, 2007 Feb. 26, 2008

Reorganization Plan Overview

Impact of a Unit’s Failure to Approve the RSU

Reorganization Plan Overview

Cost Savings Projections (To Follow in the Financial Presentation)

Cost Sharing Formula/Cost Shift Offset (To Follow in the Financial Presentation)

Reorganization Plan Overview

Election of Initial Board of Directors Tuition Contracts and School Choice Claims/Insurance Vote to Submit Reorganization Plan

Amendments Comprehensive Plan Review

Assumptions/Realities Driving Consolidation at the State Level

Public education approximately 50% of the budget. Economic projections not healthy Citizen pressure to control spending/limit taxes Declining student populations without corresponding

decline in costs Admin costs high compared to national avg. State funds for education now capped at 55% of EPS

model Further funding reductions to EPS model in 08-09

(admin/transpo/facilities)

Assumptions/Realities Driving Consolidation at the Local Level (Falmouth)

Expectation for continuous improvement in services and quality of programs embedded in priorities and planning

Zero-based budgeting and ROI emphasis demands reallocating existing funds and curbing new spending commitments

School administrative costs successfully reduced (approx. 3% of total budget)

Declining enrollment projections over time (11% over next eight years).

Budget increases have been historically/comparatively modest (3.5%, 2.98%, 4.1% in last 3 years)

Absorbed State funding reductions to EPS model (50% system admin, 5% transportation, 5% facilities)

Reaching max-out on “squeezing” for efficiencies without impacting quality of program

Biggest Obstacles to Consolidation

Cost Sharing Model (fair and equitable to all communities)

Cost Savings Model (based on reasonable and rational assumptions)

Cost Sharing Plan (Spencer Model) Developed as an alternative to funding education

solely based on the proportionate share of property tax valuation of member communities

Alternative models sanctioned by State Legislature in April ’08

Assumes State-required local tax commitment for education under EPS stays valuation-driven

Additional local costs – transition from current valuation to per-pupil allocation funding occurs over 4 years

Cost shift to Falmouth (during 4-yr transition to new model) mitigated by offset provisions agreed to by RPC and town reps (fund balances and land assets not transferring to the new RSU)

Cost Sharing ModelSchool Funding Basics:

FPS + =

MSAD51 + =

RSU + =

*RSU model same as above ** funding on a per pupil basis

State’s EPS contribution--------------------------Required local tax commitment for education

Additional local spending

Total School Budget

State’s EPS contribution--------------------------Required local tax commitment for education

Additional local spending

Total School Budget

State’s EPS contribution--------------------------Required local Tax commitment for education*

Additional local spending**

Total RSU Budget

Cost Savings Model Assumes a dynamic and interactive

relationship among:Savings Administrative/business operation efficiencies Transportation efficiencies Facilities efficiencies Non-consolidation penalty avoidance…and Costs/Revenue Reductions Operational and personnel-related expenditures

to consolidate Anticipated reductions in State subsidy (EPS

funding due to enrollment decreases/other)

Cost Savings Estimates – New RSU

Admin/operations Initial system administrative staff savings of

$250,000 per year. Evaluation and implementation of additional

operational efficiencies is expected to increase savings to $450,000 per year by 2013-14.

Transportation Targeted operational savings of 2% ($46,351) in 2010 Additional 2% savings in each of the two successive

years (to FY2012). This goal will offset the State’s 5% reduction to transportation funding in effect as of FY2009.

Our expectation is to increase savings by 1% in each of the following two years.

Cost Savings Estimates – cont. Facilities

RSU is projecting cost savings of 2% ($94,808) in year one of operation. Savings are projected in years two and three at an additional 2% each year, years four and five at an additional 1% each year.

Above savings will help offset the State’s reduction in EPS funding of 5% in effect as of FY09.

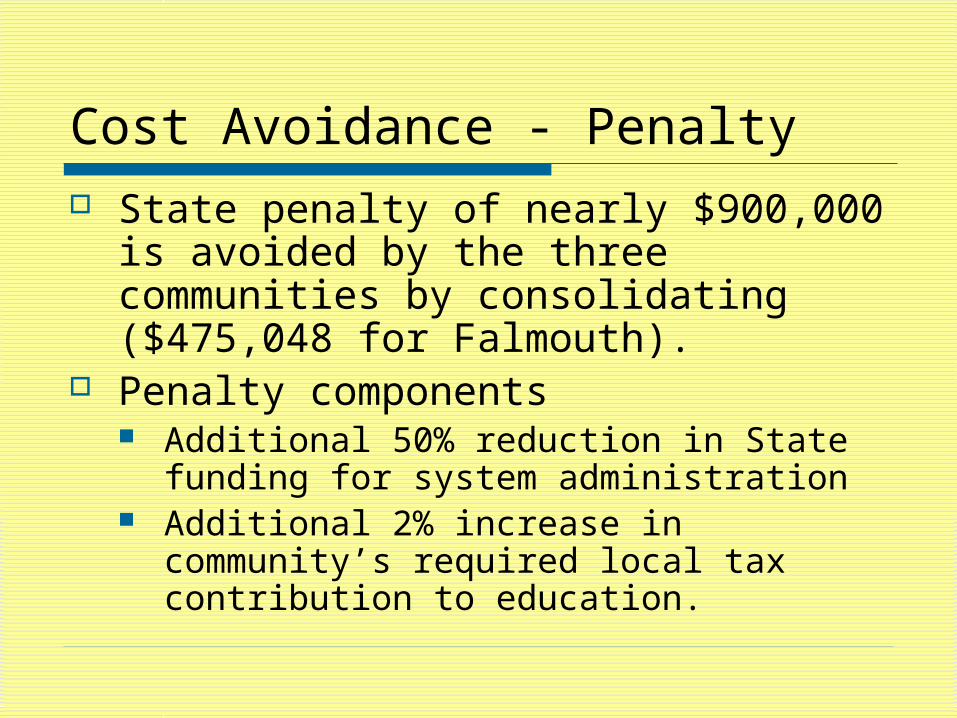

Cost Avoidance - Penalty State penalty of nearly $900,000 is

avoided by the three communities by consolidating ($475,048 for Falmouth).

Penalty components Additional 50% reduction in State

funding for system administration Additional 2% increase in community’s

required local tax contribution to education.

Costs to Consolidate - RSU

Estimated costs are expected to be $500,000 in each of the first three years, and will include: Legal Costs Personnel contract costs Independent & collaborative operational

audits Merging office systems

Projected State Revenue Reductions

State funding for education is closely tied to enrollments.

Projected enrollments in both Falmouth and MSAD 51 are expected to decline by 11% by 2015-2016.

Anticipated decline in State revenue, based solely on enrollments, is estimated to be about $560,000 for Falmouth alone (237 students x $2349 per pupil).

Conservative Estimates of Savings, Costs, Reductions in State Funding, and Penalty Avoidance

Category 2009-2010 2010-2011 2011-2012 2012-2013 2013-2014

A1 – Administration/ Business Operations

250,000 350,000 350,000 450,000 450,000

A2 – Transportation

46,351(2% reduction)

91,775(additional 2%)

138,147(additional 2%)

161,499(additional 1%)

184,618(additional 1%)

A3 –Facilities

94,808(2% reduction)

187,420(additional 2%)

282,969(additional 2%)

329,788(additional 1%)

376,139(additional 1%)

B – Cost of Consolidation

(500,000) (500,000) (500,000) 0 0

C – State Funding (231,175) (308,862) 101,781 (224,343) (128,178)

D – Penalty Avoidance

897,253 897,253 897,253 897,253 897,253

A1: Includes 250,000 in administrative savings and additional administrative and operating savings of $200,000 by 2013-2014A2: Reductions of 8% by 2013 to coincide with reductions in State support for this areaA3: Same assumptions as A2B: Assumes consolidation will be complete within 3 years; estimate includes long-term lease agreements, organizational restructuring as note in Exhibit 12C: State funding for education will decline as resources become increasingly scarce in all sectors; State funding will also decrease in Falmouth and MSAD 51 as enrollments decline in accordance with projections (11% by 2017)D: Penalty includes reduction of State support for administration and an increase in the expected local mil rate contribution

Issues and Challenges Changing “landscapes” of local and

State economics Capturing education finance in an

understandable manner Combating the “Big Promises” when

the reality indicates otherwise Capturing the “Consolidation

Question” accurately (sustainability vs. tax savings)

Sustainability (Long-Term View)

Assumes: Leadership of the new RSU

(Board/Professional) will be as commited to both: School quality improvement Efficiency in operations

Economies of scale will present new opportunities to control rising costs