Workshop Risk management Dutch Tax administration Jon Hornstra.

18

Workshop Risk management Dutch Tax administration Jon Hornstra

-

Upload

millicent-reeves -

Category

Documents

-

view

229 -

download

0

Transcript of Workshop Risk management Dutch Tax administration Jon Hornstra.

Workshop Risk management

Dutch Tax administration

Jon Hornstra

Introduction

• Co-ordinator of the supervision process of the regional tax office Utrecht-Gooi.

• Former member of the Management team of the Risk management Organisation

• Specific responsibility for Horizontal Supervision.

Overview• Risk management organisation (RMO) • How to identify Risks

– Regional Approach. – Supporting the risk finding process (RMO)– Random sampling.

• How to minimise the impact of the Risks – Auditing .– Tools and support on detecting non-

compliant taxpayers.– (enforcement) Communication.– Horizontal supervision.

Risk management organisation (RMO 1)

• Responsibilities in the risk finding process.– RMO / (Corporate) income tax– RMO / VAT and wage tax– RMO / Material risks– RMO/ Knowledge

Risk management organisation (RMO 2)

• Responsible for risk finding and selection in the process of supervision.

• Co-operation with regional tax offices (development of risks).

• Gathering and dissemination of risk related knowledge.

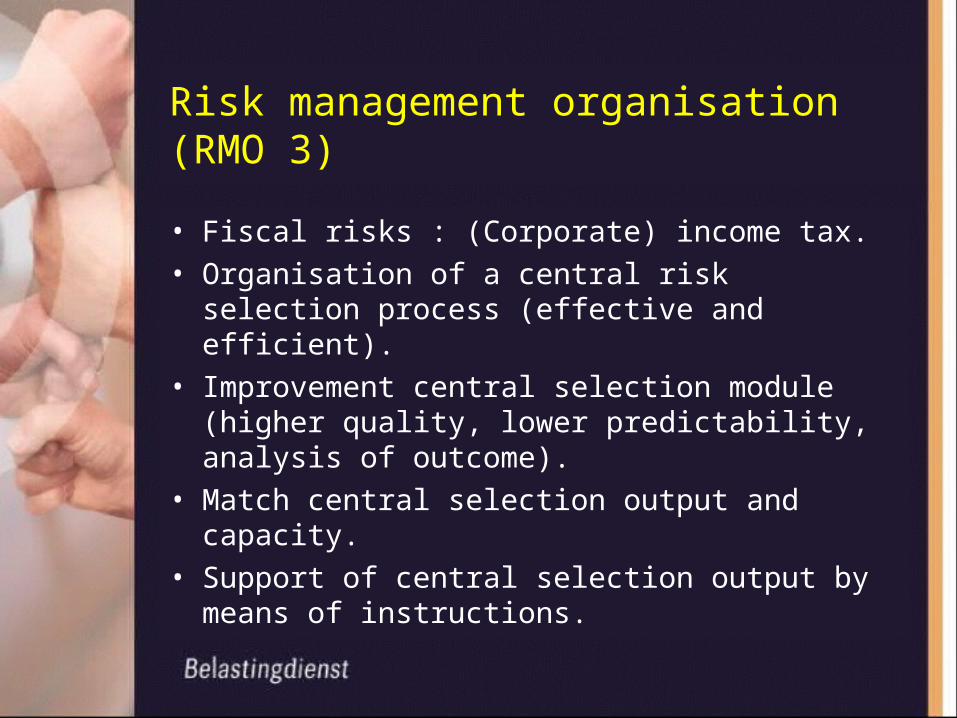

Risk management organisation (RMO 3)

• Fiscal risks : (Corporate) income tax.• Organisation of a central risk selection process

(effective and efficient).• Improvement central selection module (higher

quality, lower predictability, analysis of outcome).• Match central selection output and capacity.• Support of central selection output by means of

instructions.

Risk management organisation (RMO 4)

• Fiscal risks : VAT and wage tax.• Development of a central risk selection system.• VAT: ‘parameters’ for restitution of VAT.• Integrated selection for wage tax and social

security contributions.• Support of the fiscal risks.

Risk management organisation (RMO 5)

• Material risks.• Material risks become central activity for all the

regions.• Insight in Regional ‘best practices’.

– a successful multi applicable method– to select and– to minimise– a specific material risk– linked with a limited group of taxpayers

• Development of (regional) material risks for a nation wide approach.

How to identify Risks (1)

• Regional Approach.– Analysing Annual reports (capital

comparison of assets, comparing turnover ratio)

– Local knowledge of business development.– Observations on site (thematic or as part of

a auditing program).– Desk Research (‘traditional and ‘digital’ –

e.g. Xenon-).

How to identify material risks (2)

• Supporting the risk finding process (RMO / Knowledge)– Gathering and providing sector related

information (understanding the business).– Risk related networks (agriculture,

construction industry, real estate).

How to identify material risks (3)

• Supporting the risk finding process (RMO)• Data analyses and third party information

– taxi company’s;– identity related fraud;– real estate;– nation wide co-ordinated observations

on site.

How to identify risks (4)

• Random sampling.– Clear perception;– In practice;– Restriction; Not applicable to search

and find unknown enterprises.

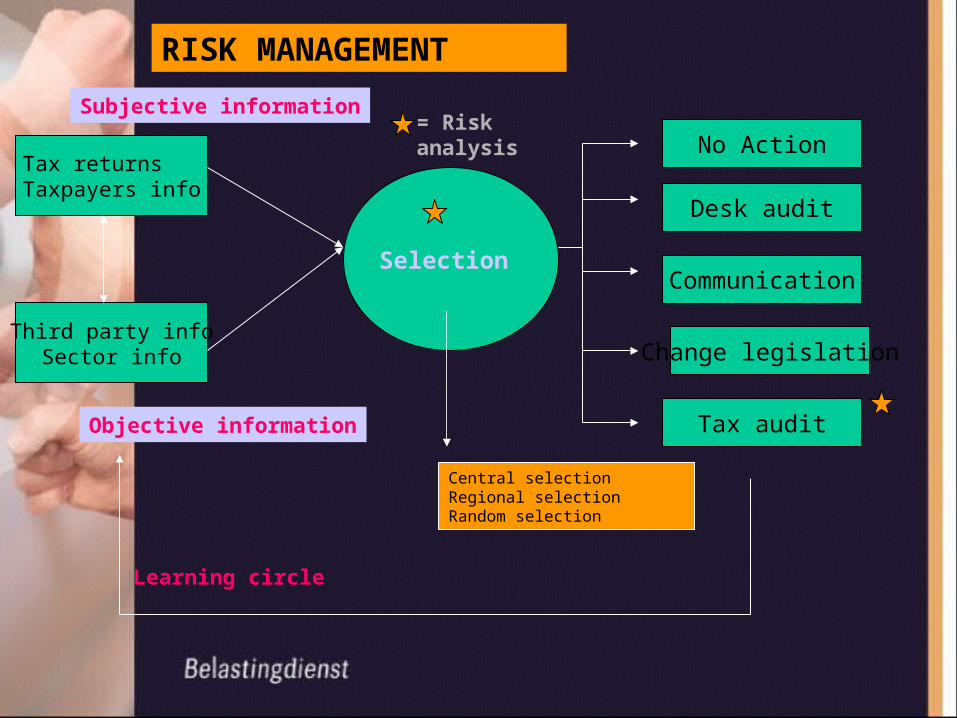

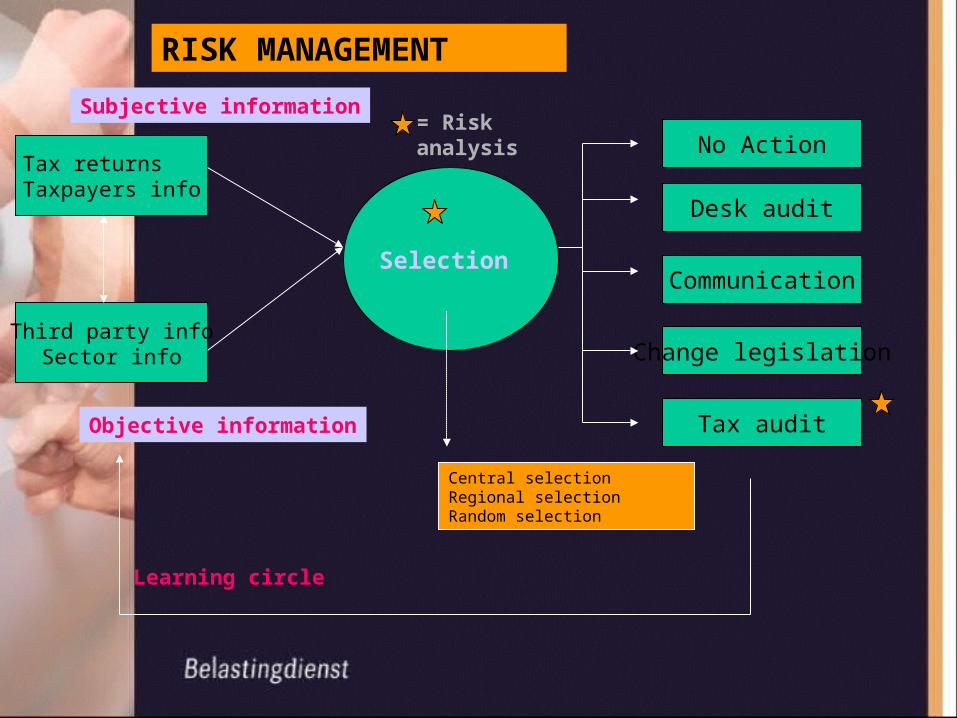

Tax returns Taxpayers info

Third party infoSector info

Selection Communication

Subjective information

RISK MANAGEMENT

Learning circle

= Risk analysis

Desk audit

No Action

Objective information

Change legislation

Central selectionRegional selectionRandom selection

Tax audit

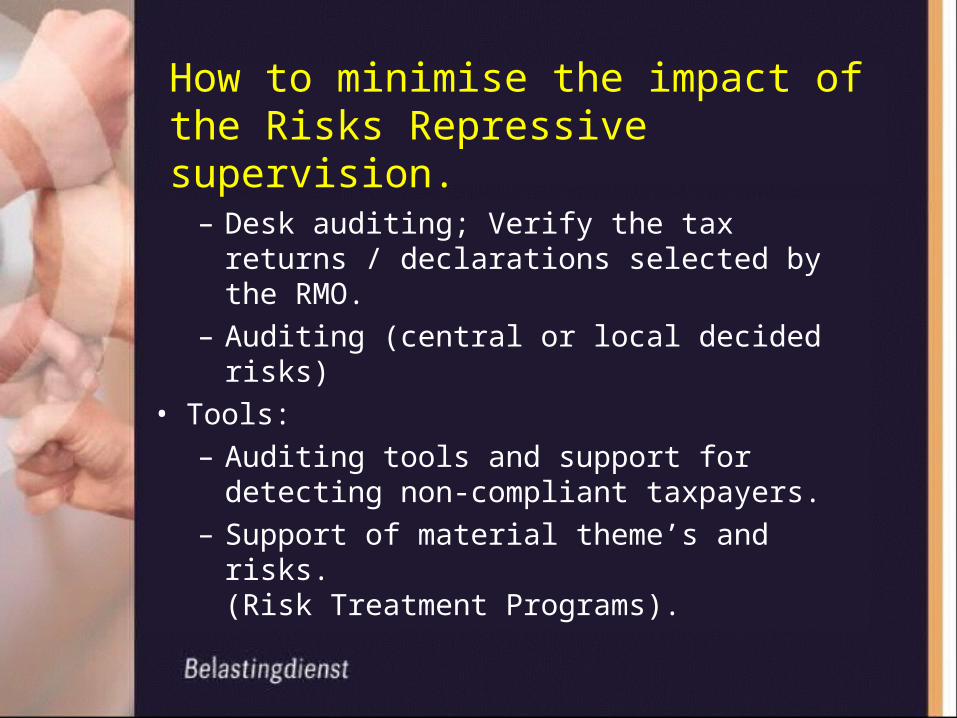

How to minimise the impact of the Risks Repressive supervision.

– Desk auditing; Verify the tax returns / declarations selected by the RMO.

– Auditing (central or local decided risks)• Tools:

– Auditing tools and support for detecting non-compliant taxpayers.

– Support of material theme’s and risks.(Risk Treatment Programs).

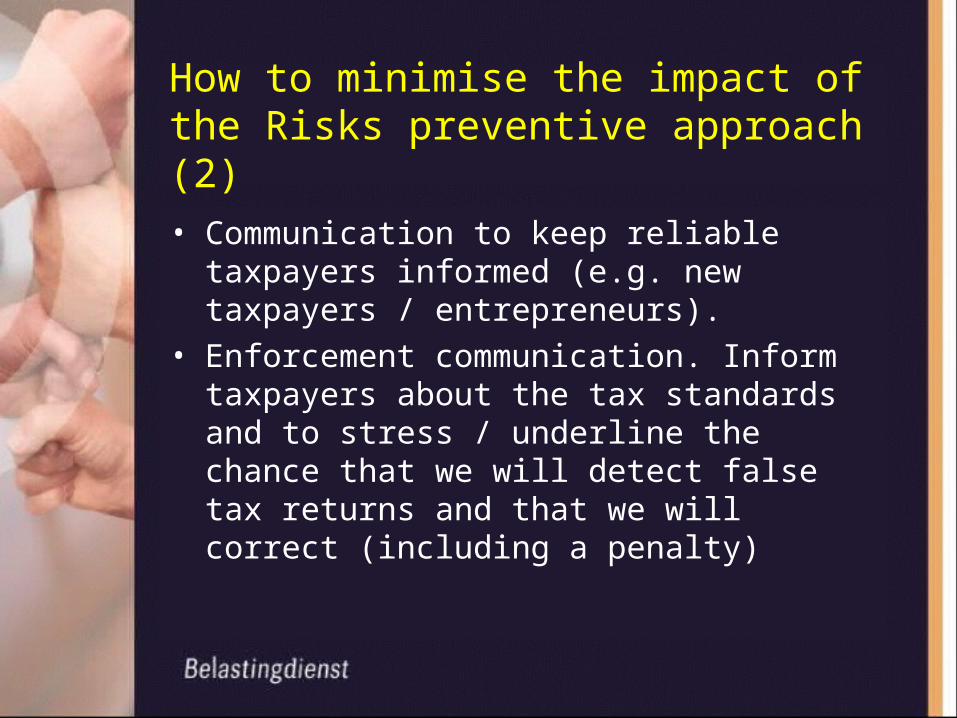

How to minimise the impact of the Risks preventive approach (2)

• Communication to keep reliable taxpayers informed (e.g. new taxpayers / entrepreneurs).

• Enforcement communication. Inform taxpayers about the tax standards and to stress / underline the chance that we will detect false tax returns and that we will correct (including a penalty)

How to minimise the impact of the Risks(prevention and risk transfer)

• To change legislation – to simplify (less mistakes) – to skip rules which can not be controlled.

• Horizontal supervision.– Individual– sector organisations– intermediary / tax consultants / tax

counsellor

Tax returns Taxpayers info

Third party infoSector info

Selection Communication

Subjective information

RISK MANAGEMENT

Learning circle

= Risk analysis

Desk audit

No Action

Objective information

Change legislation

Central selectionRegional selectionRandom selection

Tax audit

Thank you for your attention