Workshop on Delinquency Management - REM - · PDF fileWorkshop on Delinquency Management ......

12

Workshop on Delinquency Management June 2010 « Credit without discipline is nothing but charity » Pr Yunus

-

Upload

nguyenquynh -

Category

Documents

-

view

218 -

download

1

Transcript of Workshop on Delinquency Management - REM - · PDF fileWorkshop on Delinquency Management ......

Workshop on

Delinquency Management

June 2010

« Credit without discipline is nothing but charity »

Pr Yunus

Service Cost to client

Money and Debt Advice Free

Access to bank accounts Free

Microcredit Business Loans 15-19% Interest Rate

Personal Loans 32 - 39% Interest Rate

+ 5% Admin Fees

Our Business

3

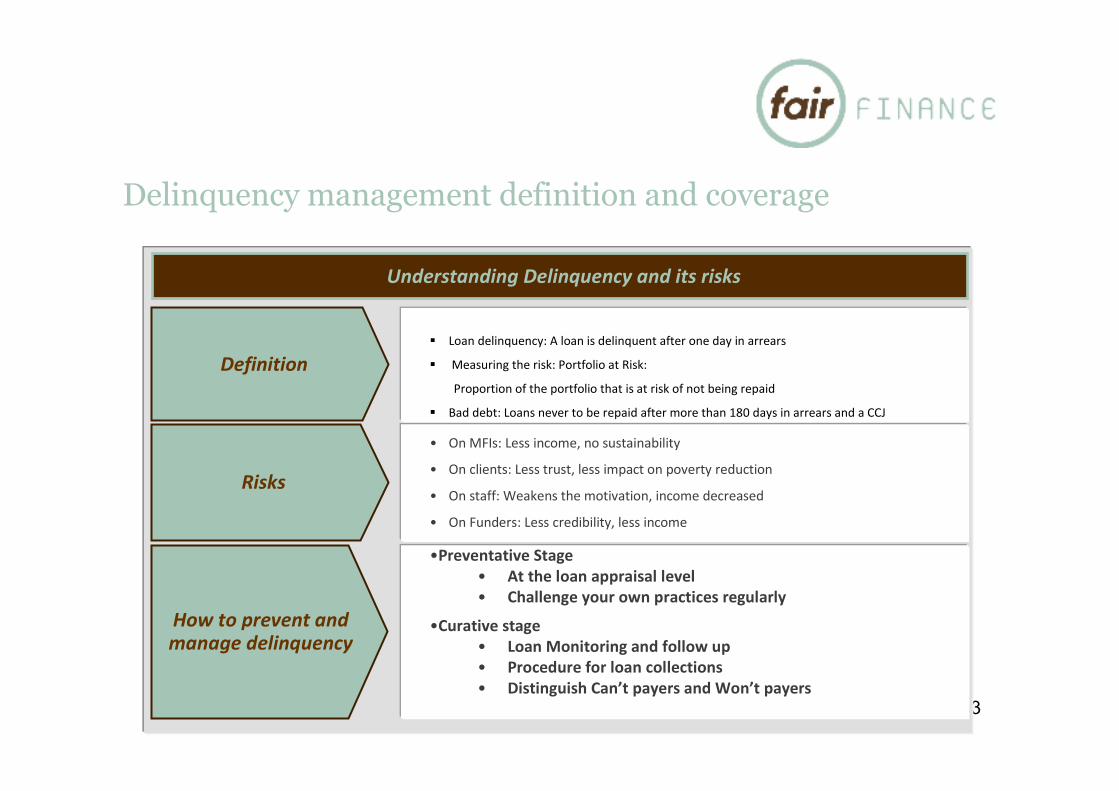

Understanding Delinquency and its risks

� Loan delinquency: A loan is delinquent after one day in arrears

� Measuring the risk: Portfolio at Risk:

Proportion of the portfolio that is at risk of not being repaid

� Bad debt: Loans never to be repaid after more than 180 days in arrears and a CCJ

Definition

•Preventative Stage

• At the loan appraisal level

• Challenge your own practices regularly

•Curative stage

• Loan Monitoring and follow up

• Procedure for loan collections

• Distinguish Can’t payers and Won’t payers

How to prevent and manage delinquency

Delinquency management definition and coverage

3

Risks

• On MFIs: Less income, no sustainability

• On clients: Less trust, less impact on poverty reduction

• On staff: Weakens the motivation, income decreased

• On Funders: Less credibility, less income

4

•On Client’s situation

•Redundancy

•Unemployment

•Living standard

•Reduced access to Bank

loans, Overdrafts and

credit cards

•For MFIs

•Demand Increase

•Client profile

Impact of the credit crunch on delinquencies

Consequences

•Bad Product design

•Not suitable for client

•Inability to understand

debts

•Credit scoring system

•High level of refusal by

Banks

•Turn to extortionate

lenders and fall in

Overindebtness

Causes of the Credit Crunch in the UK

•No Interest rate cap

•Extortionate Interest rates

•Financial exclusion versus

Over inclusion

•Irresponsible lending

UK context

Credit Crunch

To determine the impact of the Credit Crunch on Delinquency management of UK MFIs, it is essential to

understand the UK context, the causes of the credit crunches and their consequences on both clients and

MFIS

Number of applications Increased by 20%

Refusal rate Increased by 5%

Consequences on the Portfolio at Risk NONE

Consequences on the rescheduled Loans DOUBLED

Client who would never have had to come to us before are now

pushing the door

StatisticsObservable Consequences

6

Case study on Fair Finance

Delinquency Management

(Dealing with arrears responsibly)

Case by Case appraisalLending responsibly

(preventing bad loans)

•Small Loans: less risky

•Step by step approach

•Based on Existing income

•Flexible

•Transparent

•Site visi

•Quick

•Face to face Interview

•No credit Score

•No Collateral

Product design (Understanding the market)

Fair Finance

•Character

•Disposable income

•Income and expenditure

•Finance and Debt Management

•Business Viability

•Credit check

For Can’t payers

•Close monitoring of the portfolio

•No penalty fees for arrears

•Rescheduling/Payment holiday

•Focusing on communication

For won’t payers

•Strong procedure in place: As

responsible lenders

•Taking them up to court

Fair Finance offers a range of adapted products and as such avoided an increase in the portfolio at risk

during the credit crunch. Fair Finance’s clients have been credit crunched for all their life so the institution

has built experience in understanding risk and dealing with it.

2005/06- 2008/9

Total number of clients supported 5000

Personal Loans Made (Over 2000) £1,500,000

Microcredit Loans Made (160) £600,000

Bad Debt Rate 9%

Debt Advice Given 1500

Over indebtedness managed £12m

Bank Accounts opened 120

StatisticsResults

8

8

Outstanding balance variation for the last 3 years for Personal Loans and Business Loans

Outstanding Balance

0

100000

200000

300000

400000

500000

600000

700000

800000

2008 2009 2010

•Number of active loans •Outstanding Balance in Value (£)

0

200

400

600

800

1000

2008 2009 2010

9

9

Personal and Business Loans PAR >30 days for the last 3 years (End of month)

Risk Profile

•Personal Loans•Business Loans

•Bad Debt 9% in 2009

25%

8%

14% 13%

8%

15%12% 11%

0%

10%

20%

30%

Aug 07 Mar-08 Mar-09 Dec-09

10

10

Case studies

Bu

sin

ess

Ap

pli

cati

on

Mini Cafe

�Mrs Jane Draft is divorced and has one dependant child. She lives in Hackney and is tenant of the Council. She is in the process to start her business after having two other loan from 2 other Loan Providers, for a total amount of £10,000. She came to Fair Finance asking for a loan of £5,000 to finish the refurbishment of her premises and buy part of the equipment, in particular the coffee machine with accessories.

Fair Finance – Businesses

Online retail Jewellery

�Mr Paul is married and has been running the business successfully for the past 3 years with his wife.

�He applied for £10,000 to develop it and secure premises.

�Cash Flow realistic and genuine client

�No site visit realised

Please tell us where are the risks, would you give the loan?

www.fairfinance.org.ukOpening Questions Not to be shown•What would have worsen the situation. (the absence of credit bureau see South America)

•What are the next challenges: • Risk of Bad practice in collections• Target driven delinquency management• Challenge the banks on their scoring methods• Avoid a similar crisis in developing countries• What are the differences in management in Europe and the rest ofthe world;

• Are the current PAR in Europe more representative of the reality of the risk?

www.fairfinance.org.uk