Workshop Cum Service Tax Refresher Course Hosted by Baroda Branch of WIRC of ICAI on 08/08/2012 CA...

29

Workshop Cum Service Tax Refresher Course Hosted by Baroda Branch of WIRC of ICAI on 08/08/2012 CA MUKUND CHOUHAN Mumbai & Surat. Email:- [email protected]

-

Upload

alexia-newman -

Category

Documents

-

view

214 -

download

0

Transcript of Workshop Cum Service Tax Refresher Course Hosted by Baroda Branch of WIRC of ICAI on 08/08/2012 CA...

Workshop Cum Service Tax Refresher Course

Hosted by Baroda Branch of WIRC of ICAI on 08/08/2012

CA MUKUND CHOUHANMumbai & Surat.

Email:- [email protected]

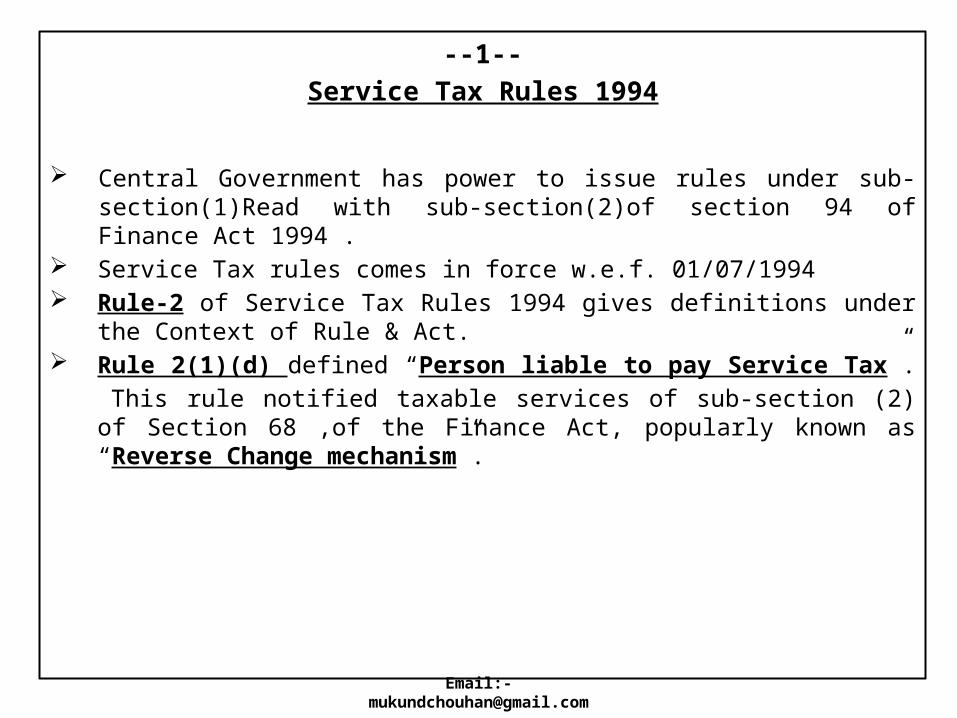

--1--Service Tax Rules 1994

Central Government has power to issue rules under sub-section(1)Read with sub-section(2)of section 94 of Finance Act 1994 .

Service Tax rules comes in force w.e.f. 01/07/1994 Rule-2 of Service Tax Rules 1994 gives definitions under the Context of Rule & Act. Rule 2(1)(d) defined “Person liable to pay Service Tax”.

This rule notified taxable services of sub-section (2) of Section 68 ,of the Finance Act, popularly known as “Reverse Change mechanism”.

Email:- [email protected]

-

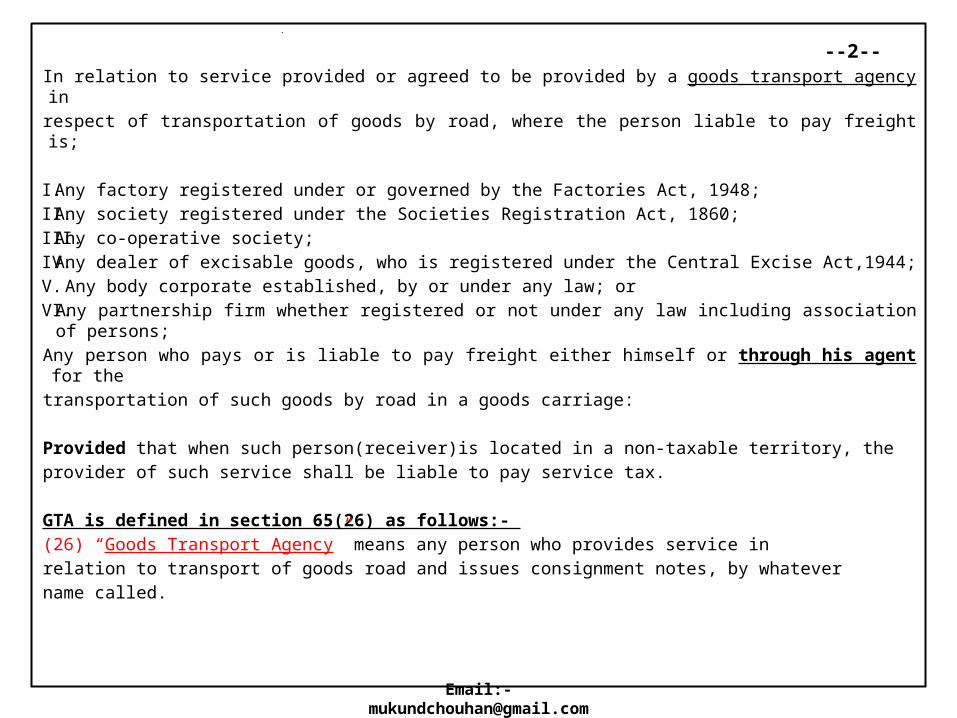

--2--In relation to service provided or agreed to be provided by a goods transport agency inrespect of transportation of goods by road, where the person liable to pay freight is;

I. Any factory registered under or governed by the Factories Act, 1948;II. Any society registered under the Societies Registration Act, 1860;III. Any co-operative society;IV. Any dealer of excisable goods, who is registered under the Central Excise Act,1944;V. Any body corporate established, by or under any law; orVI. Any partnership firm whether registered or not under any law including association of

persons;Any person who pays or is liable to pay freight either himself or through his agent for thetransportation of such goods by road in a goods carriage:

Provided that when such person(receiver)is located in a non-taxable territory, theprovider of such service shall be liable to pay service tax.

GTA is defined in section 65(26) as follows:- (26) “Goods Transport Agency” means any person who provides service inrelation to transport of goods road and issues consignment notes, by whatevername called. Email:- [email protected]

--3--Example:- ABC company is selling coal, lifting from Kutch, to various factories of Surat.

ABC company is arranging the transportation, for the transportation of coal from Kutch to Surat, as a agent for various factories.

ABC company issued invoice to factories and also collected the amount of freight on the face of invoice. After that he made the payment to the transporters on behalf of factory. In this circumstances ABC company is agent of various factories, who are specified person. In this case ABC company take registration of Service Tax (only one registration) and no other factories will take Service Tax registration.

Email:- [email protected]

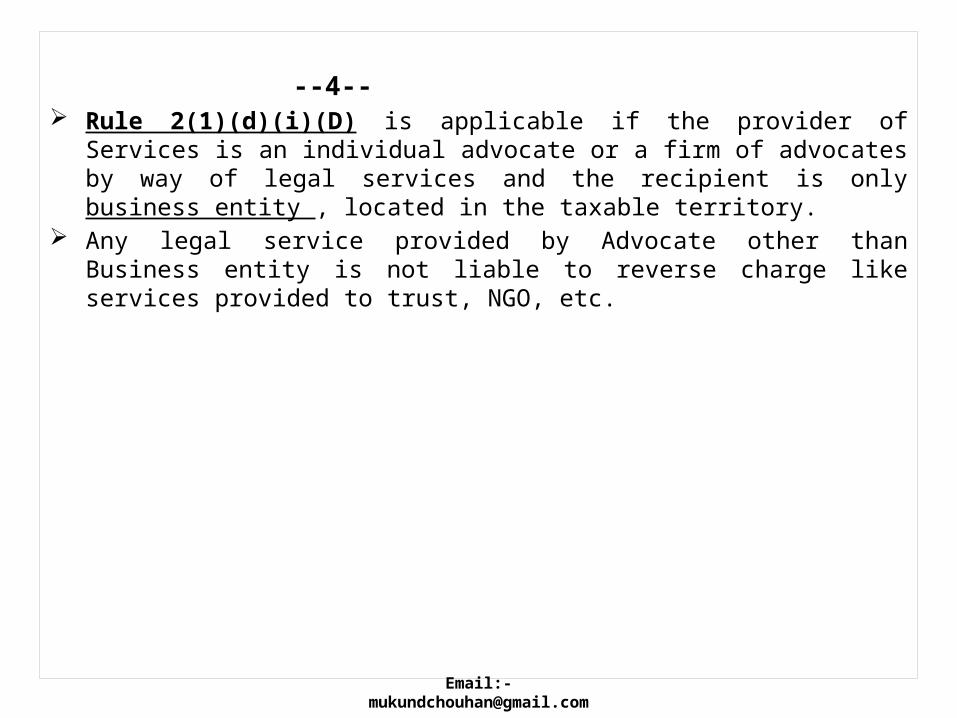

--4-- Rule 2(1)(d)(i)(D) is applicable if the provider of Services is an individual advocate or

a firm of advocates by way of legal services and the recipient is only business entity , located in the taxable territory.

Any legal service provided by Advocate other than Business entity is not liable to reverse charge like services provided to trust, NGO, etc.

Email:- [email protected]

Partial Reverse Charge New entry under Rule 2(1)(d)(i)(F)

If service provider is individual, HUF, Partnership Firm located in taxable territory.

To a business entity registered as body corporate, located in taxable territory.

Both person, service provider and service receiver will be liable to make the payment of Service Tax to the extent of notified rates.

Three services notified so far:1 (a) In respect of services provided or agreed to be provided by

way of renting of a motor vehicle designed to carry passengers on abated value to any person who is not engaged in the similar line of business

(b) In respect of services provided or agreed to be provided by way of renting of a motor vehicle designed to carry passengers on non abated value to any person who is not engaged in the similar line of business

Nil

60%

100%

40%

2 In respect of services provided or agreed to be provided by way of supply of manpower for any purpose

25% 75%

3 In respect of service provided or agreed to be provided in services portion in execution of works contract

50% 50%

--5--

Email:- [email protected]

--6-- Under Rule 2(1)(d)(i)(G)

In relation to any taxable service provider or agreed to be provided by any person, which is located in a non-taxable and received by any person, located in taxable territory

The recipient of service.

Example :-

i. One tour operator located at Jammu, arrange a tour of Srinagar for the group of people located at Vadodara. In this case group of Vadodara people will have to pay tax on the advance payment and also on final payment. Because the provider of service is located at non- taxable territory and recipient of service is located at taxable territory.

Take service tax registration and pay service tax because no S.S.I. exemption is available.

ii. A civil engineer firm located at London provides the design of business mall, to a businessman located at Delhi.

The businessman of Delhi is liable to take service tax registration and no S.S.I. benefit is available.

Email:- [email protected]

--7--Registration( Rule 4) Every person liable for paying the Service Tax shall make an application, to

superintendent in Form-ST-1 for registration. Within 30 days from the date on which the Service Tax is levied.

Centralize Registration [ under Rule 4(2)] Where a person, liable for paying Service Tax, on a Taxable Service, provides such

service from more than one premises or office and, Having Centralized Billing System or Centralized Accounting System, may register

this premises or office under Centralized Registration. For example SOTC (a tour operator) has number of office all over the country, for the

book of various tours, offered by them. But his Billing System is Centralized at Head Office Mumbai, then he can take Service Tax, single registration at Mumbai and not for all office located all over the country.

The registration will be granted by Commission of Central Excise (not superintendent), in whose Jurisdiction the premises or office is located.

Email:- [email protected]

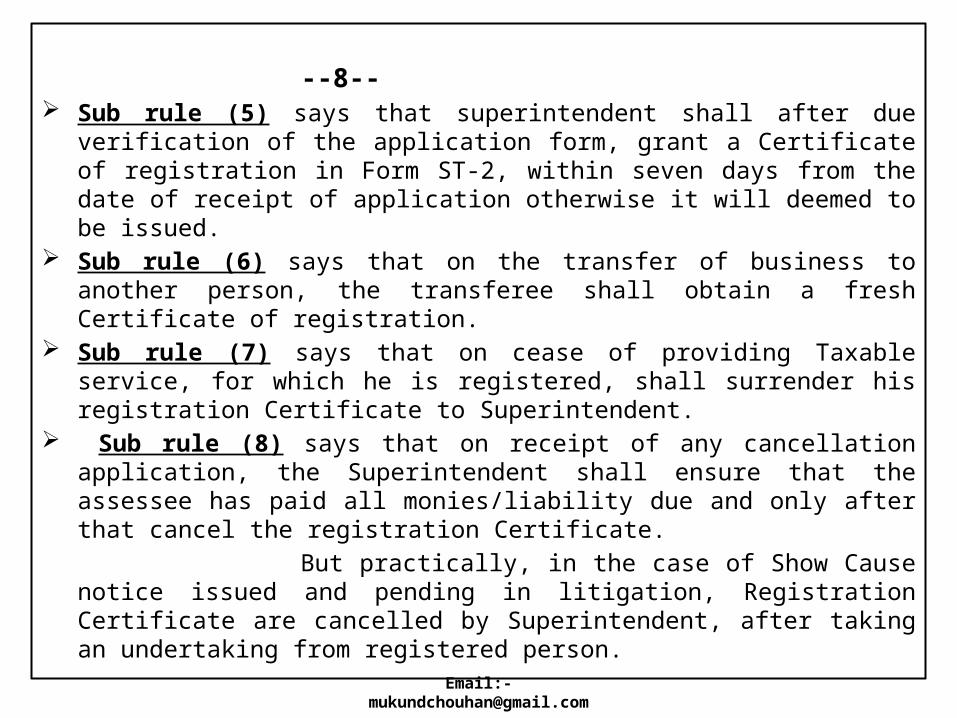

--8-- Sub rule (5) says that superintendent shall after due verification of the application

form, grant a Certificate of registration in Form ST-2, within seven days from the date of receipt of application otherwise it will deemed to be issued.

Sub rule (6) says that on the transfer of business to another person, the transferee shall obtain a fresh Certificate of registration.

Sub rule (7) says that on cease of providing Taxable service, for which he is registered, shall surrender his registration Certificate to Superintendent.

Sub rule (8) says that on receipt of any cancellation application, the Superintendent shall ensure that the assessee has paid all monies/liability due and only after that cancel the registration Certificate.

But practically, in the case of Show Cause notice issued and pending in litigation, Registration Certificate are cancelled by Superintendent, after taking an undertaking from registered person.

Email:- [email protected]

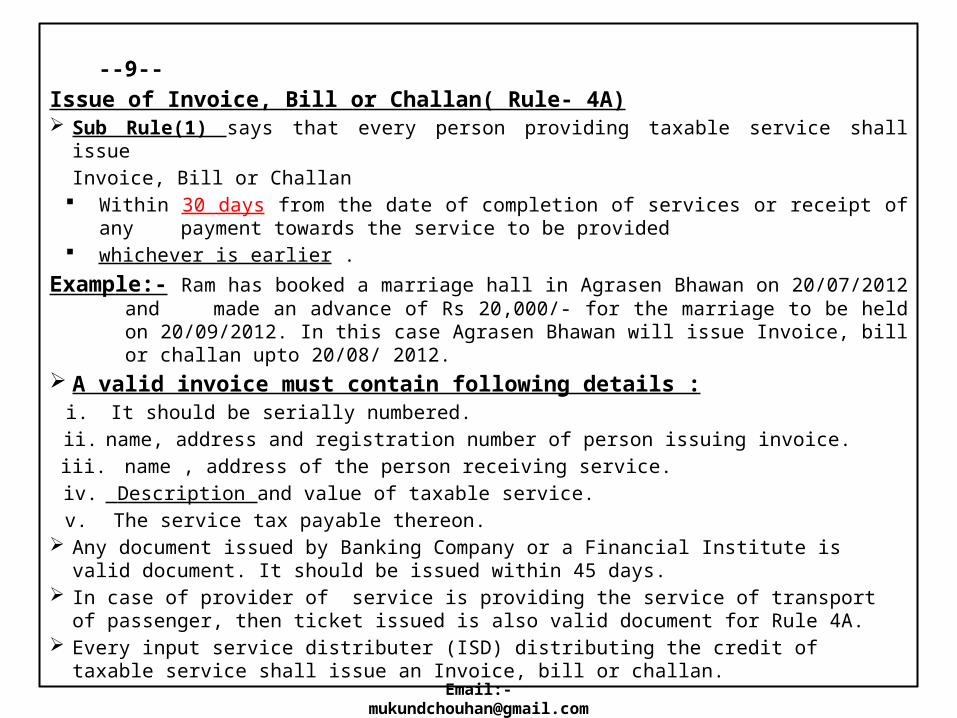

--9--Issue of Invoice, Bill or Challan( Rule- 4A) Sub Rule(1) says that every person providing taxable service shall issue

Invoice, Bill or Challan Within 30 days from the date of completion of services or receipt of any payment

towards the service to be provided whichever is earlier .

Example:- Ram has booked a marriage hall in Agrasen Bhawan on 20/07/2012 and made an advance of Rs 20,000/- for the marriage to be held on 20/09/2012. In this case Agrasen Bhawan will issue Invoice, bill or challan upto 20/08/ 2012.

A valid invoice must contain following details :i. It should be serially numbered.ii. name, address and registration number of person issuing invoice.iii. name , address of the person receiving service. iv. Description and value of taxable service.v. The service tax payable thereon.

Any document issued by Banking Company or a Financial Institute is valid document. It should be issued within 45 days.

In case of provider of service is providing the service of transport of passenger, then ticket issued is also valid document for Rule 4A.

Every input service distributer (ISD) distributing the credit of taxable service shall issue an Invoice, bill or challan.

Email:- [email protected]

--10--Records Rule – 5 Sub-rule (1) - The records including computerized data, maintained by an assessee,

in accordance with other law, shall be acceptable. Sub-rule (2) - Every assessee shall furnish to superintendent at the time of filling of

first return, in duplicate, a list of records maintained by him in the course of business. Sub-rule (3) - All such records shall be preserved for a period of FIVE years,

immediately after the financial year to which such records pertain.

Access to a registered premises Rule-5A An officer authorized by the commissioner in this behalf shall have access to any

registered premises. Every assessee shall, on demand, make available to the officer or the audit party or C

& AG of India, within a reasonable time, not exceeding 15 days, the records declared (maintained) by them along with trail balance and audited balance sheet.

Email:- [email protected]

--11--Payment of Service Tax – Rule 6 The service tax shall be paid to the credit of government

i. By the 6th day of the month, if paid through internet.ii. By the 5th day of the month, in any other case immediately following the

calendar month, which the service is deemed to be provided. In case of an individual, or proprietorship firm or partnership firm, the service tax is

liable to pay, immediately after the completion of quarter. And in other case after the completion of month.

Service tax liability for the month or quarter ending on MARCH shall be paid by the 31st MARCH.

w.e.f. 01/04/2012, in case of individuals and partnership firm, whose aggregate value of the taxable services provided is Rs 50 lakh or less in the previous financial year, shall have the option to pay tax, on taxable service provided or agreed to be provided by him upto a total of Rs 50 lakh in the current financial year, on receipt of payment basis.

In case of an assessee, who has paid total service tax of Rs 10 lakh or more, including from CENVAT Credit, in the preceding financial year, then he shall deposit the service tax, electronically through internet.

Email:- [email protected]

--12-- If the assessee deposits the service tax by cheque, the date of presentation of

cheque to the bank shall be deemed to be the date on which service tax has been paid, subject to realization of cheque.

Sub rule(3) - where an assessee has issued an invoice or received any payment, against a service provided or agreed to be provided either wholly or partly, for any reason, the amount is negotiated due to deficient provision of service, then the assessee can take the credit of excess service tax paid by him, if the assessee

has refunded the payment or part thereof, so received has issued a credit note for the value of the service not so provided.

Example :-i. Booking of air conditioned hall for marriage ceremony and A.C. was not

working properlyii. Due to fault in repairing of generator and after few month, whole amount

refunded.

Email:- [email protected]

--13-- Sub rule- (4A) - where an assessee has paid to the credit of Central Government

any amount in excess required to be paid towards Service Tax liability for a month or quarter, as the case may be, the assessee may adjust such excess amount paid by him against his service tax liability for the succeeding month or quarter, as the case may be, other than the excess payment made due to interpretation of law, taxability,

valuation or applicability of exemption.

Export of Services- Rule 6AAny services provided or agreed to be provided shall be treated export of service, iffollowing condition satisfied:-

the provider of service is located in the taxable territory. the recipient of service is located outside India. the service is not a service specified in negative list. the place of provision of service in outside India. the payment for such service has been received in convertible foreign

currency. Sub- rule(2) - Rebate & Refund on export of service is available to provider of

service.Email:- [email protected]

--14--Returns – Rule – 7 Sub-rule-(1) every assessee shall submit a half-yearly return in Form-ST-3 alongwith

copy of TR-6 Challan in Triplicate. Sub-rule-(2) every assessee shall submit the half-yearly return by the 25th of the

month, following a particular half year. Sub-rule(3) w.e.f. 01.10.2010, every assessee shall submit the half-yearly return

electronically.

Revision of return Rule 7-B An assessee may submit a revised return in Form ST-3, in triplicate to correct a

mistake or omission , within a period of 90 days, from the date of submission of original return.

Penalty for delay filing of Return Rule 7-C Delay of 15days – penalty Rs 500/- Delay of 15 days to 30 days- Penalty Rs 1000/- Delay beyond 30 days and upto the date of delayed submission- Penalty Rs 1000/-

Plus Rs 100/- for every day. Subject to maximum of Rs 20,000/-

Email:- [email protected]

--15--Point of Taxation Rules 2011 (POT)Point of taxation means the point in time when a service shall be deemed to have been provided.

Rule 3 It is a general rule for determining the point in time, when the liability for payment of Service Tax arises.

a. If the invoice has been issued within 30 days , from the date of completion of serviceDate of invoice OR which ever is earlier Receipt of payment

b. If the invoice is not issued within 30days, from the date ofcompletion of service.Date of completion of service OR which ever is earlierReceipt of payment

Email:- [email protected]

Sr.No.

Date of Completion of service

Date of Invoice

Date on which Amount received

Point of Taxation

Remarks

1. May 10, 2012

May 20, 2012

June 30, 2012 May 20, 2012

Invoice issued with in 30 days and before receipt of payment

2. May 10, 2012

July 26, 2012

June 30, 2012 May 10, 2012

Invoice not issued within 30 days and payment received after completion of service

3. May 10, 2012

May 20, 2012

April 15, 2012 April 15, 2012

Invoice issued with in 30 days but payment received before invoice

4. May 10, 2012

June 16, 2012

April 5, 2012 (part) and June 25, 2012 (remaining)

April 5, 2012 and May 10, 2012 for respective amounts

invoice not issued with in 30 days. Part payment before completion, remaining later.

--16--

Email:- [email protected]

--17--Rule-2(c) – “continuous supply of service” means any service which is provided , or

[agreed] to be provided continuously [or on recurrent basis, under a contract, for a period exceeding three months with the obligation for payment periodically or from time to time], or where the Central Government, by a notification in the Official Gazette, prescribes provision of a particular service to be continuous supply of service, whether or not subject to any condition.

In the case of continuous supply of service, on the completion of event, in terms of contract.

Example:- XYZ & company is dealer of Reliance Industry and getting commission @ 1% of sale value of yarn. As per agreement XYZ & company will raise the bill on the 1st day of each month, for the commission generated on sale of earlier month. In this case the point of taxation is event date i.e. 1st day of each month.

Email:- [email protected]

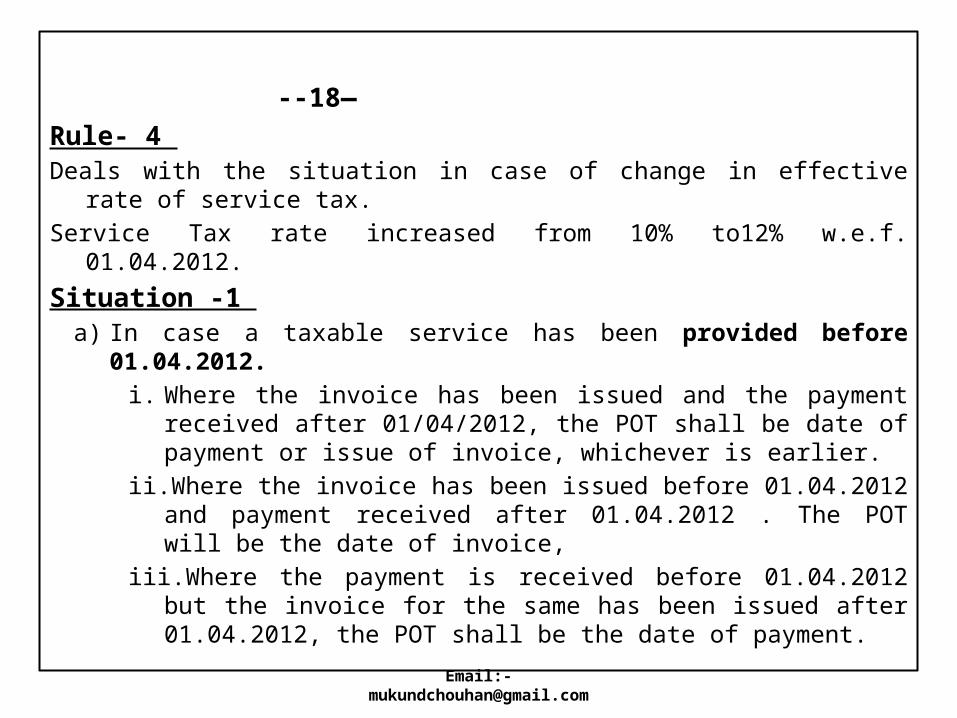

--18—Rule- 4 Deals with the situation in case of change in effective rate of service tax.Service Tax rate increased from 10% to12% w.e.f. 01.04.2012.

Situation -1 a) In case a taxable service has been provided before 01.04.2012.

i. Where the invoice has been issued and the payment received after 01/04/2012, the POT shall be date of payment or issue of invoice, whichever is earlier.

ii. Where the invoice has been issued before 01.04.2012 and payment received after 01.04.2012 . The POT will be the date of invoice,

iii. Where the payment is received before 01.04.2012 but the invoice for the same has been issued after 01.04.2012, the POT shall be the date of payment.

Email:- [email protected]

--19--Example:

Situation Date of Completion of Service

Invoice Date

Amount Received date

Date of Tax Rate Change

POT Date Rate of duty applicable

i) 10.03.2012 05.04.2012 15.04.2012 01.04.2012 05.04.2012 12%

ii) 10.03.2012 20.03.2012 10.04.2012 01.04.2012 20.03.2012 10%

iii) 10.03.2012 10.03.2012 20.03.2012 01.04.2012 20.03.2012 10%

Email:- [email protected]

--20--Situation- 2(b) In case a taxable service has been provided after 01/04/2012.

i. Where the invoice has been issued before 01.04.2012 but the payment received after 01.04.2012 . The POT shall be the date of payment.

ii. Where the invoice has been issued and the payment also received before 01/04/2012, the POT shall be the date of receipt of payment or date of issuance of invoice, which ever is earlier.

iii. Where the payment is received before 01.04.2012 but the invoice has been raised after 01.04.2012 . The POT shall be the date of issue of invoice.

Email:- [email protected]

--21--Example:

Situation Date of Completion of service

Invoice Date

Amount Received date

Date of Tax Rate Change

POT Date Rate of duty applicable

i) 05.04.2012 26.03.2012 20.04.2012 01.04.2012 20.04.2012 12%

ii) 05.04.2012 20.02.2012 25.03.2012 01.04.2012 20.02.2012 10%

iii) 05.04.2012 10.04.2012 20.03.2012 01.04.2012 10.04.2012 12%

Email:- [email protected]

--22--Rule-5 Payment of Tax in case of New ServiceSub- rule- (1) - No tax shall be payable to the extent the invoice has been issued and

the payment receipt, against such invoice before such service becometaxable.

Example:- Amitabh Bachchan signed a film for Rs 5 crore on 01/01/2012.Hereceived in advance Rs 2 crore on 01/02/2012 and issued his bill to producer on 01/06/2012 . Acting in movie, become first time taxable w.e.f. 01/07/2012. So service tax will not be levied on the amount of Rs 2 crores but the balance amount received after 01/07/2012, so the balance amount of Rs 3 crore is liable to Service Tax.

Sub-rule-(2) - No tax shall be payable if the payment has been received before the service becomes taxable and the invoice has been issued within 14days,

of the date when the service is taxed for the first time.

Example:- In the above example if Amitabh Bachchan received payment of Rs 5 crore before 01/07/2012 and the invoice is issued upto 14/07/2012 (within 14 days when the service is taxed first time) then no service tax is leviable.

Email:- [email protected]

--23--Rule-7 POT in case of specified services or persons Notwithstanding anything contained in these rules, the POT in respect of the

persons required to pay tax as recipient of service (under reverse charge mechanism) as notified under sub-section(2) of Section 68 of the Act, shall be the date on which payment is made.

Example:- ABC Company Private Ltd had taken a service of Advocate and Bill of Rs. 50,000/- was issued by Advocate, individual or firm (not company) in the month of April on 01/04/2012. ABC Company made the payment in the month of July on 25/07/2012 . Under reverse charge mechanism ABC Company Private Ltd will have to pay tax on the service received from advocate. Hence in this case ABC Company Private Ltd will pay service tax considering POT in the month of July and the liability can be discharged upto 5th of the August.

Email:- [email protected]

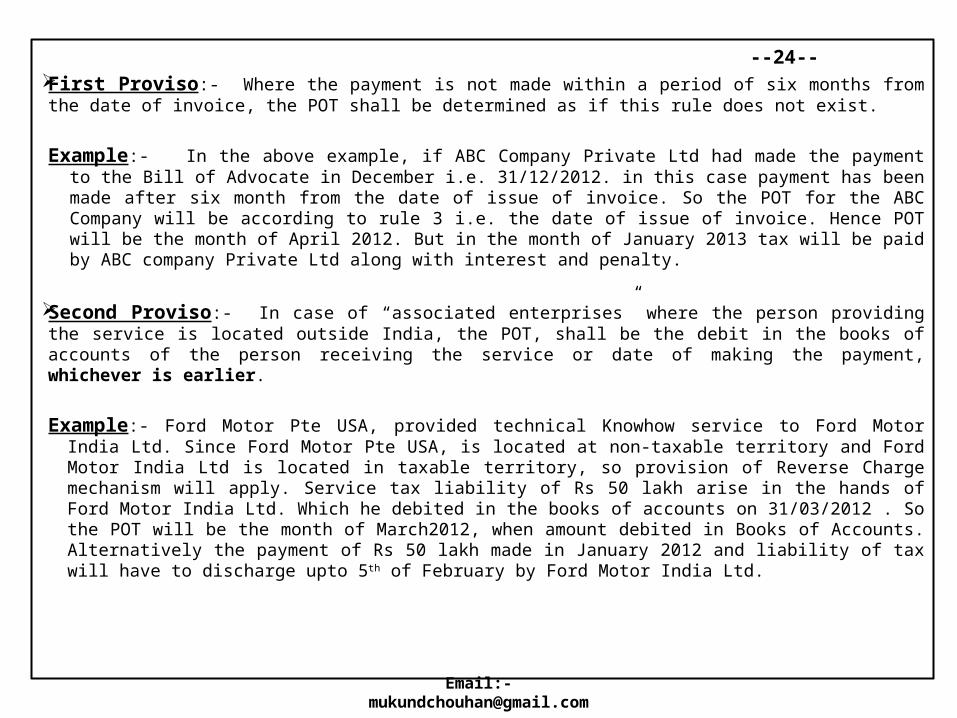

--24-- First Proviso:- Where the payment is not made within a period of six months from the date of

invoice, the POT shall be determined as if this rule does not exist.

Example:- In the above example, if ABC Company Private Ltd had made the payment to the Bill of Advocate in December i.e. 31/12/2012. in this case payment has been made after six month from the date of issue of invoice. So the POT for the ABC Company will be according to rule 3 i.e. the date of issue of invoice. Hence POT will be the month of April 2012. But in the month of January 2013 tax will be paid by ABC company Private Ltd along with interest and penalty.

Second Proviso:- In case of “associated enterprises” where the person providing the service is located outside India, the POT, shall be the debit in the books of accounts of the person receiving the service or date of making the payment, whichever is earlier.

Example:- Ford Motor Pte USA, provided technical Knowhow service to Ford Motor India Ltd. Since Ford Motor Pte USA, is located at non-taxable territory and Ford Motor India Ltd is located in taxable territory, so provision of Reverse Charge mechanism will apply. Service tax liability of Rs 50 lakh arise in the hands of Ford Motor India Ltd. Which he debited in the books of accounts on 31/03/2012 . So the POT will be the month of March2012, when amount debited in Books of Accounts. Alternatively the payment of Rs 50 lakh made in January 2012 and liability of tax will have to discharge upto 5th of February by Ford Motor India Ltd.

Email:- [email protected]

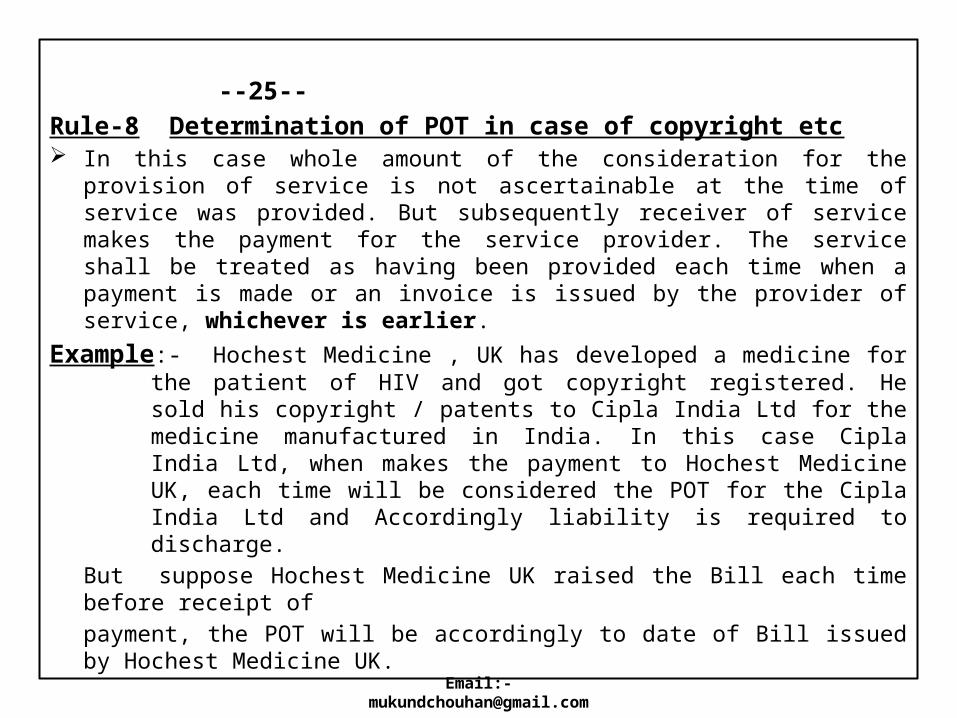

--25--Rule-8 Determination of POT in case of copyright etc In this case whole amount of the consideration for the provision of service is not

ascertainable at the time of service was provided. But subsequently receiver of service makes the payment for the service provider. The service shall be treated as having been provided each time when a payment is made or an invoice is issued by the provider of service, whichever is earlier.

Example:- Hochest Medicine , UK has developed a medicine for the patient of HIV and got copyright registered. He sold his copyright / patents to Cipla India Ltd for the medicine manufactured in India. In this case Cipla India Ltd, when makes the payment to Hochest Medicine UK, each time will be considered the POT for the Cipla India Ltd and Accordingly liability is required to discharge.

But suppose Hochest Medicine UK raised the Bill each time before receipt ofpayment, the POT will be accordingly to date of Bill issued by Hochest Medicine UK.

Email:- [email protected]

--26--Rule-8A Determination of POT by Best Judgement This rule can be invoked when POT cannot be determined, as per this rule, as the

date of invoice or the date of payment or both are not available . In this circumstances, the Central Excise Officer will demand to produce such

accounts, documents, or other evidences as he may deem necessary. The officer after taking into account such material and effective rate of tax prevalent

at different points of times, shall pass on speaking order in writing, after giving an opportunity of being heard, determine the POT to the best of his judgement.

Example:- A raid occurred in the office of firm providing Security Service. The service provider was illiterate person. So he did not take registration and also did not properly maintained records. Details of receipt of payment in bank was found by Bank Statement. In this circumstances officer will determine POT and total tax liability as per his best judgement.

Email:- [email protected]

--27--

Rule-9 Transitional Provisions Nothing contained in these rules shall be applicable

i. Where the provision of service is completed or ii. Where invoices are issued

Prior to 30/06/2011. In above situation, the payment is receipt after 30/06/2011, the POT shall be at the

option of tax payer. This rule has not much importance now.

Email:- [email protected]

Email:- [email protected]