© Crown copyright 2009 00912-2009PPT-EN-01 Workshop 1 Narrowing gaps – setting the scene.

woodmac.com Trusted Intelligence

Alan Gelder, VP Refining, Chemicals & Oil Markets

Global outlook for refining and olefins Workshop 1 – Setting the scene

2

woodmac.com

Agenda

1 Middle East & Asian refining to 2025

2 Energy Transition

3 Ethylene market outlook

4 Downstream conversion industry

4

woodmac.com

Middle East refined product demand profile (kbd)

The East of Suez region is the key location for refined product demand growth Asian demand growth outpaces the Middle East due to its growing ranks of the middle class, particularly in India

Asian refined product demand profile (kbd)

-

2,000

4,000

6,000

8,000

10,000

12,000

KBD 2010 2015 2020 2025

History: IEA Energy Statistics, Forecast:Wood Mackenzie

-

2,000

4,000

6,000

8,000

10,000

12,000

KBD 2010 2015 2020 2025

History: IEA Energy Statistics, Forecast:Wood Mackenzie

5

woodmac.com

The Middle East is undertaking major refining investments, both in terms of

capacity and quality improvement Major projects are typically delivered slower than their original schedules

Greenfield refinery investments Brownfield refinery investments

Persian Gulf, Iran 480 kb/d, January 2017- 2024

Karbala, Iraq 140 kb/d, January 2021

Jazan, Saudi Arabia 400 kb/d, October 2019

Clean Fuels, Kuwait 64 kb/d, Jan 2020 Al-Zour, Kuwait

615 kb/d, June 2020

Bahrain, Bahrain 93 kb/d, January 2023

Ras Tanura, Saudi Arabia Clean Fuels April 2020

Abadan, Iran New refinery train January 2022

Jebel Ali, UAE Refinery Upgrade January 2020

Bazian, Iraq 50 kb/d, June 2020

Duqm, Oman 230 kb/d, January 2023

Basrah, Iraq 70 kb/d, January 2021

Al-Zour, Kuwait Phase 2 Upgrade January 2025

Laffan, Qatar Zekreet Project January 2019

Rabigh, Saudi Arabia Clean Fuels January 2020

Ruwais, UAE CFP Project January 2023

Bandar Abbas, Iran Clean Fuels April 2019

Riyadh, Saudi Arabia Clean Fuels January 2019

6

woodmac.com

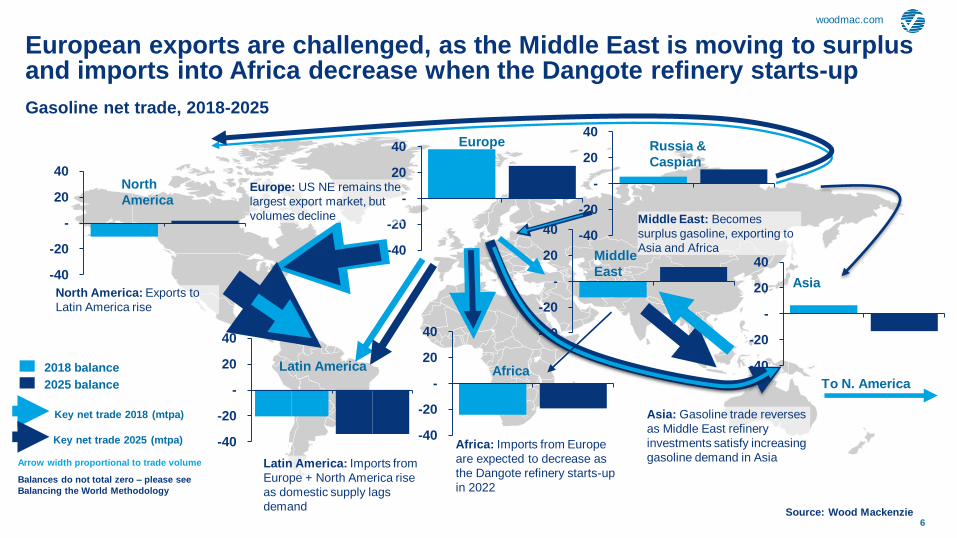

European exports are challenged, as the Middle East is moving to surplus and imports into Africa decrease when the Dangote refinery starts-up

-40

-20

-

20

40

-40

-20

-

20

40

-40

-20

-

20

40

-40

-20

-

20

40

-40

-20

-

20

40

-40

-20

-

20

40

-40

-20

-

20

40

Europe

Latin America

Russia &

Caspian

Middle

East Asia

North

America

Africa To N. America

Key net trade 2018 (mtpa)

Key net trade 2025 (mtpa)

2018 balance

2025 balance

Arrow width proportional to trade volume

Balances do not total zero – please see

Balancing the World Methodology

North America: Exports to

Latin America rise

Europe: US NE remains the

largest export market, but

volumes decline

Latin America: Imports from

Europe + North America rise

as domestic supply lags

demand

Asia: Gasoline trade reverses

as Middle East refinery

investments satisfy increasing

gasoline demand in Asia

Middle East: Becomes

surplus gasoline, exporting to

Asia and Africa

Gasoline net trade, 2018-2025

Source: Wood Mackenzie

Africa: Imports from Europe

are expected to decrease as

the Dangote refinery starts-up

in 2022

7

woodmac.com

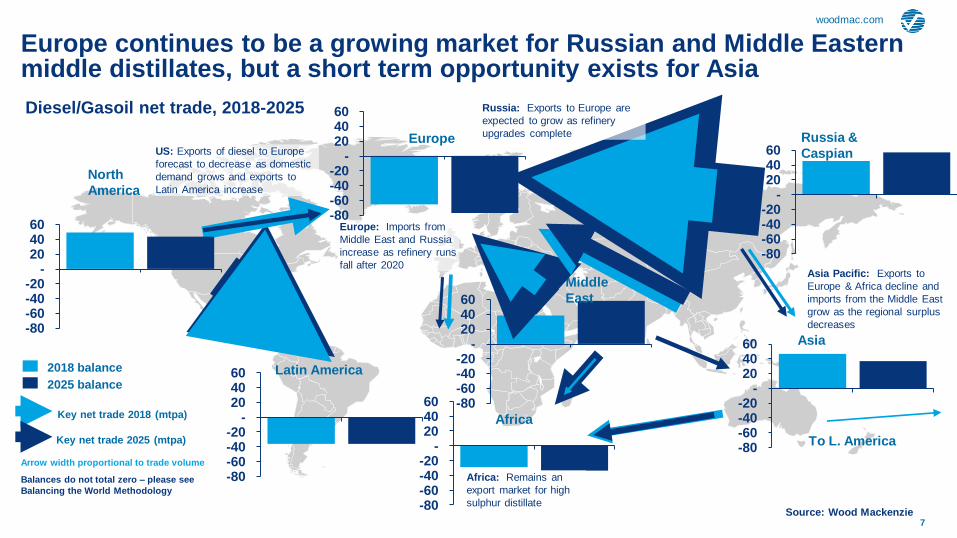

Europe continues to be a growing market for Russian and Middle Eastern middle distillates, but a short term opportunity exists for Asia

-80-60-40-20

-204060 -80

-60-40-20

-204060

-80-60-40-20

-204060

-80-60-40-20

-204060

Russia &

Caspian Europe

Africa

Asia

North

America

Middle

East

To L. America

US: Exports of diesel to Europe

forecast to decrease as domestic

demand grows and exports to

Latin America increase

Russia: Exports to Europe are

expected to grow as refinery

upgrades complete

Europe: Imports from

Middle East and Russia

increase as refinery runs

fall after 2020 Asia Pacific: Exports to

Europe & Africa decline and

imports from the Middle East

grow as the regional surplus

decreases

Key net trade 2018 (mtpa)

Key net trade 2025 (mtpa)

2018 balance

2025 balance

Arrow width proportional to trade volume

Balances do not total zero – please see

Balancing the World Methodology

Diesel/Gasoil net trade, 2018-2025

Source: Wood Mackenzie

Latin America

Africa: Remains an

export market for high

sulphur distillate

-80-60-40-20

-204060

-80-60-40-20

-204060

-80-60-40-20

-204060

8

woodmac.com

Middle East Gross Reference Refining Margins (US$/bbl, real 2018$)

IMO boosts refining margins for 2020, but global refining over-build weakens margins thereafter The IMO uplift is primarily for distillate oriented, deep conversion configurations

-5

0

5

10

15

20

200

1

200

3

200

5

200

7

200

9

201

1

201

3

201

5

201

7

201

9

202

1

202

3

202

5

ME Gulf Dubai FCC $/bbl (Real) ME Gulf Dubai Hydrocracker Coker $/bbl (Real) ME Gulf Dubai Hydroskimming $/bbl (Real)

$/bbl

Source Wood Mackenzie

$/bbl

Source Wood Mackenzie

$/bbl

10

woodmac.com

Global liquids* demand

Global liquids demand to reach 110 million b/d in 2040, an increase of 11 million b/d from 2018 Annual growth decelerates steadily through mid-2030s, moving into a slow decline after 2037

Source: Wood Mackenzie * liquids includes oil products, NGLs, and biofuels

Annual growth in global liquids demand

-500

-

500

1,000

1,500

2,000

000 b

/d

2020 growth includes one-time 100

kbd increase in total demand caused

by IMO-related shift from marine fuel

oil to gasoil (when measured in

volume terms)

Global GDP growth eases from 3.1%

in 2017 to 2.5% by 2021 as China,

Europe and US lose momentum. Risk

to GDP is to the downside from

US/China trade war

Oil demand

increasingly displaced

by electrified vehicles

and natural gas in

transport

Global liquids demand grows 11

million b/d to 2040

-

20

40

60

80

100

120

2000 2010 2020 2030 2040

millio

n b

/d

H2 update actual linear trend

Source: Wood Mackenzie

11

woodmac.com

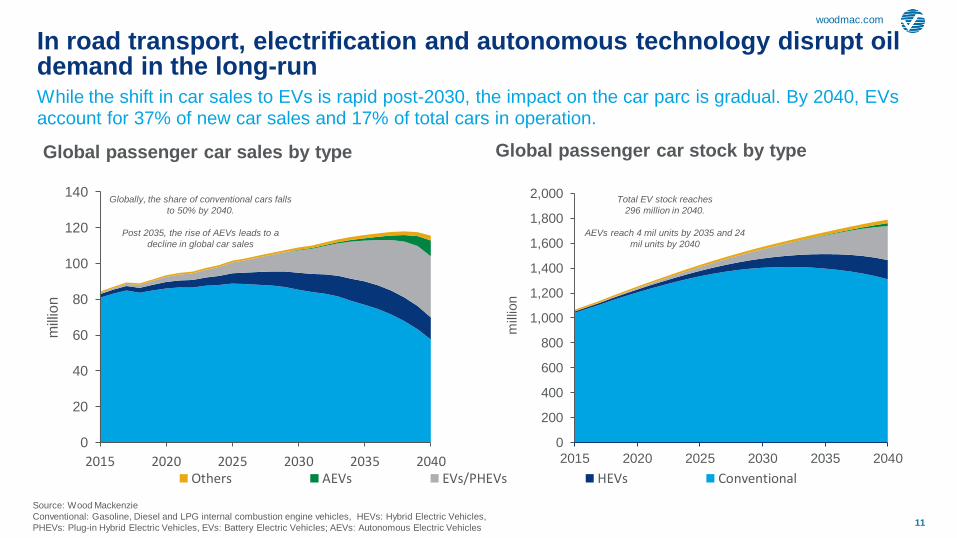

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2015 2020 2025 2030 2035 2040

millio

n

0

20

40

60

80

100

120

140

2015 2020 2025 2030 2035 2040

mill

ion

Others AEVs EVs/PHEVs HEVs Conventional

In road transport, electrification and autonomous technology disrupt oil demand in the long-run While the shift in car sales to EVs is rapid post-2030, the impact on the car parc is gradual. By 2040, EVs account for 37% of new car sales and 17% of total cars in operation.

Global passenger car sales by type

Source: Wood Mackenzie

Conventional: Gasoline, Diesel and LPG internal combustion engine vehicles, HEVs: Hybrid Electric Vehicles,

PHEVs: Plug-in Hybrid Electric Vehicles, EVs: Battery Electric Vehicles; AEVs: Autonomous Electric Vehicles

Global passenger car stock by type

Total EV stock reaches

296 million in 2040.

AEVs reach 4 mil units by 2035 and 24

mil units by 2040

Globally, the share of conventional cars falls

to 50% by 2040.

Post 2035, the rise of AEVs leads to a

decline in global car sales

woodmac.com

12

-40%

-20%

0%

20%

40%

60%

80%

100%

-4

-2

0

2

4

6

8

10

00-05 05-10 10-15 15-20 20-25 25-30 30-35

Che

mic

als

Millio

n B

arr

els

Pe

r D

ay

Transport Petrochemicals

Resid/Comm/Agric Electricity

Other Chemicals Proportion

0%

20%

40%

60%

0

40

80

120

2000 2005 2010 2015 2020 2025 2030 2035

Che

mic

als

Millio

n B

arr

els

Pe

r D

ay

Transport Petrochemicals

Res/Comm/Agri Electricity

Other Chemicals Proportion

Global Crude Oil Demand ABSOLUTE

Peak transport demand for oil changes the investment focus

As transportation demand for crude oil peaks, petrochemicals become more important part of oil companies’ strategies.

Source: Wood Mackenzie Refined Products Market Service

Global Crude Oil Demand GROWTH

woodmac.com

14

0

5

10

15

20

25

05 10 15 20 25

$/m

mb

tu

Brent Crude Oil US Natural Gas US Ethane

China Naphtha Europe Naphtha

-5

0

5

10

15

05 10 15 20 25

M t

on

, N

ew

Eth

yle

ne

Ca

pa

city

North America West Europe

Middle East Asia (Ex China)

China Other

Energy & Feedstock Price Benchmarks

Ethylene investments are influenced by feedstock advantage and proximity to demand centres

Low natural gas & coal/methanol prices relative to global crude oil prices resulted in many new ethane crackers in North America & MTO/CTO units in China.

Source: Wood Mackenzie Global Ethylene Supply/Demand Analytics Service

New Global Ethylene Investments

North America

Closes

Capacity

North

America

Adds 1st

Wave

Large Asia &

North

America 2nd

Wave

Crude &

Natural

Gas Parity

Crude &

Natural

Gas

Separate

Gas still

Favored,

but closer

woodmac.com

15

North America Ethylene Capacity 1st Wave of Crackers (Built / Firm / Likely): » Debottleneck & expansions of existing facilities

» 2016: Braskem-Idesa – Mexico (1000 kta)

» 2017: Oxychem/Mexichem – Texas (544 kta)

» 2017: DowDupont – Texas (1500 kta)

» 2018: ChevronPhillips – Texas (1500 kta)

» 2018: ExxonMobil – Texas (1500 kta)

» 2018: Indorama – Louisiana (440 kta)

» 2019: Formosa – Texas (1500 kta)

» 2019: Sasol – Louisiana (1500 kta)

» 2019: Shintech – Louisiana (500 kta)

» 2019: Lotte-Westlake – Louisiana (1000 kta)

» 2021: Total/Nova/Borealis – Texas (1000 kta)

» 2022: Shell – Pennsylvania (1500 kta)

2nd Wave of Crackers (pre-FID):

» ExxonMobil/Sabic – Corpus Christi, Texas

» Formosa – St. James, Louisiana

» Motiva – Port Arthur, Texas

» ChevronPhillips – Cedar Bayou, Texas

» PTT/Daelim – Dilles Bottom, Ohio

» Alberta, Canada Petrochemical Diversification Program

North America is making significant ethylene investments

North America is doubling ethylene capacity in two investment waves, with most of this new capacity additions occurring in Texas and Louisiana, with only Shell in Northeast US

Source: Wood Mackenzie Global Ethylene Supply/Demand Analytics Service

0%

25%

50%

75%

100%

0.0

20.0

40.0

60.0

2005 2010 2015 2020 2025

HypotheticalAdditions

Firm & LikelyAdditions

ExistingCapacity (mid-18)

% from Ethane& LPG

Million Tons Alt Feed Proportion

woodmac.com

16

Middle East Ethylene Capacity 2018-2025 Firm & Likely Crackers (6):

» 2019: Ilam PC, Iran (458 kta)

» 2021: Bushehr PC, Iran (1000 kta)

» 2021: Liwa Plastics, Oman (880 kta)

» 2023: Gachsaran PC, Iran (1000 kta)

» 2024: Dehloran Sepehr PC, Iran (500 kta)

» 2024: Aramco/Total, Saudi Arabia (1500 kta)

Post 2024 Hypothetical Pre-FID Crackers:

» KPIC Refinery & Mixed Feed Cracker, Kuwait

» DUQM Refinery & Mixed Feed Cracker, Oman

» QAPCO Ethane Cracker, Qatar

» Borouge/ADNOC Mixed Feed Cracker, UAE

» Saudi Aramco/Sabic JV COTC, Saudi Arabia

» Multiple Projects, Iran

Integrated refinery developments are emerging in the Middle East Slower growth after 2008-2010 investment wave. Iran continues to invest, although uncertainty due to US sanctions. A large volume of oil-to-chemical or mixed feed projects nearing FID.

Source: Wood Mackenzie Global Ethylene Supply/Demand Analytics Service

0%

25%

50%

75%

100%

0.0

20.0

40.0

60.0

2005 2010 2015 2020 2025

HypotheticalAdditions

Firm & LikelyAdditions

ExistingCapacity(mid-18)

% fromEthane &LPG

Million Tons Alt Feed Proportion

woodmac.com

17

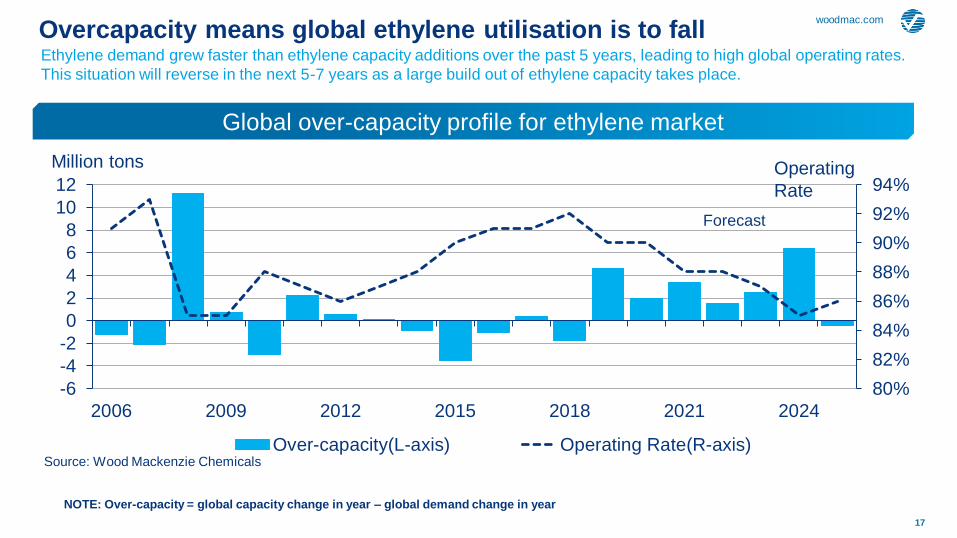

Overcapacity means global ethylene utilisation is to fall Ethylene demand grew faster than ethylene capacity additions over the past 5 years, leading to high global operating rates.

This situation will reverse in the next 5-7 years as a large build out of ethylene capacity takes place.

Global over-capacity profile for ethylene market

NOTE: Over-capacity = global capacity change in year – global demand change in year

80%

82%

84%

86%

88%

90%

92%

94%

-6

-4

-2

0

2

4

6

8

10

12

2006 2009 2012 2015 2018 2021 2024

Over-capacity(L-axis) Operating Rate(R-axis)Source: Wood Mackenzie Chemicals

Million tons

Forecast

Operating

Rate

woodmac.com

18

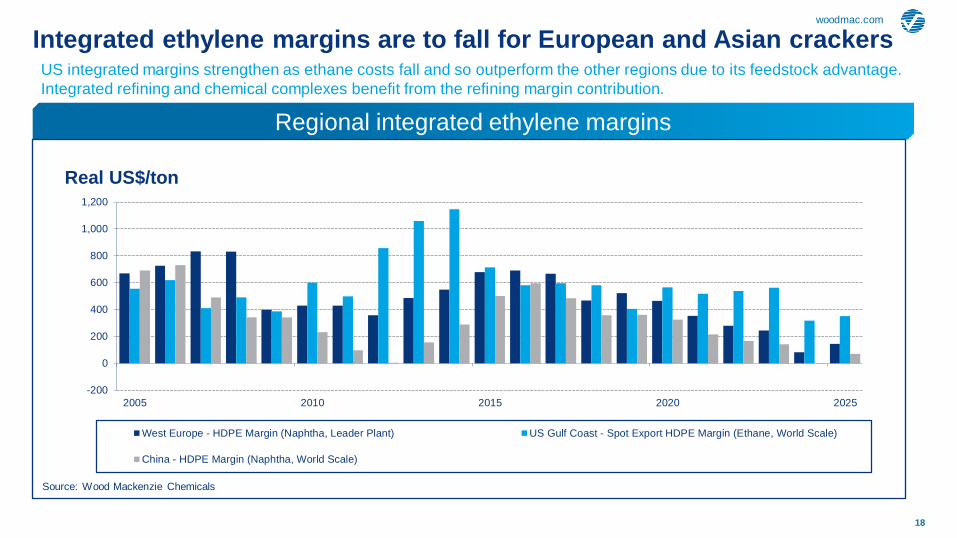

Integrated ethylene margins are to fall for European and Asian crackers US integrated margins strengthen as ethane costs fall and so outperform the other regions due to its feedstock advantage.

Integrated refining and chemical complexes benefit from the refining margin contribution.

Regional integrated ethylene margins

-200

0

200

400

600

800

1,000

1,200

2005 2010 2015 2020 2025

West Europe - HDPE Margin (Naphtha, Leader Plant) US Gulf Coast - Spot Export HDPE Margin (Ethane, World Scale)

China - HDPE Margin (Naphtha, World Scale)

Source: Wood Mackenzie Chemicals

Real US$/ton

woodmac.com

20

Polyolefin supply by end use segment

The Middle East conversion industry is growing strongly, but the required regional transformation is starting

The common themes are regional growth, innovation and diversification, but recent global developments have added complexity to investment considerations.

0

2

4

6

8

10

12

2005 2010 2015 2020 2025

millio

n tons

Blow Moulding Cable/Wire Extrusion Extrusion Coating Fibre Extrusion Film Extrusion Injection Moulding

Other Processes Pipe/Tube Extrusion Raffia Rotational Moulding Sheet Extrusion

Source: Wood Mackenzie

Key opportunities

• Move further downstream via product

diversification

• Grow partnerships with European and Asian

specialty players

• Step change in chemicals supply via crude to

chemicals

woodmac.com

21

Key challenges are:

Global economic health: The risk of a global economic recession are rising, which challenges

the funding available to Middle East governments. Nonetheless, petrochemical margins are

forecast to weak through to 2025

Regional shift towards a heavier feed slate: This challenges the magnitude of the regional

cost advantage and its availability down the value chain

Attracting and Developing Talent: There is a serious concern about the talent available in the

region to manage and operate petrochemical projects. Many of the projects are located in

remote places so difficult to staff

The growth of the Middle East downstream conversion industry is not without its challenges

Many of the regional governments are also following similar strategies, so developing a differentiated offer is essential

22

woodmac.com

Connect with

Alan Gelder

VP Refining, Chemicals and Oil Markets Downstream Global Content Lead Biography

Alan

+44 20 3060 0520

Alan is VP Refining, Chemicals and Oil Markets. As Downstream Global Content Lead,

he is responsible for formulating Wood Mackenzie’s research outlook and integrated

cross-sector perspectives on this global sector.

Alan Gelder joined Wood Mackenzie’s Downstream Consulting team in 2005 and became

global head in 2009. He transitioned into research upon his return from Houston in 2011 and

was Global Head of Refining and Chemicals.

Prior to joining Wood Mackenzie, Alan had 10 years of industry consulting after working for

ExxonMobil in a variety of project planning and technical process design roles.

Alan has a first class Master Degree in Chemical Engineering from Imperial College, London,

supplemented by an MBA from Henley Management College.

23

woodmac.com

Disclaimer

Strictly Private & Confidential

These materials, including any updates to them, are published by and remain subject to the copyright of the Wood Mackenzie group ("Wood

Mackenzie"), and are made available to clients of Wood Mackenzie under terms agreed between Wood Mackenzie and those clients. The use of

these materials is governed by the terms and conditions of the agreement under which they were provided. The content and conclusions contained

are confidential and may not be disclosed to any other person without Wood Mackenzie's prior written permission. Wood Mackenzie makes no

warranty or representation about the accuracy or completeness of the information and data contained in these materials, which are provided 'as is'.

The opinions expressed in these materials are those of Wood Mackenzie, and nothing contained in them constitutes an offer to buy or to sell

securities, or investment advice. Wood Mackenzie's products do not provide a comprehensive analysis of the financial position or prospects of any

company or entity and nothing in any such product should be taken as comment regarding the value of the securities of any entity. If,

notwithstanding the foregoing, you or any other person relies upon these materials in any way, Wood Mackenzie does not accept, and hereby

disclaims to the extent permitted by law, all liability for any loss and damage suffered arising in connection with such reliance.

Copyright © 2018, Wood Mackenzie Limited. All rights reserved. Wood Mackenzie is a Verisk business.

Wood Mackenzie™, a Verisk business, is a trusted intelligence provider, empowering decision-makers with unique insight

on the world’s natural resources. We are a leading research and consultancy business for the global energy, power and

renewables, subsurface, chemicals, and metals and mining industries. For more information visit: woodmac.com

WOOD MACKENZIE is a trademark of Wood Mackenzie Limited and is the subject of trademark registrations and/or

applications in the European Community, the USA and other countries around the world.

Europe

Americas

Asia Pacific

Website

+44 131 243 4400

+1 713 470 1600

+65 6518 0800

www.woodmac.com