Working capital Final project II 101230060546 Php app01

202

BACKGROUND OF THE STUDY. “THE MAJOR OBJECTIVE OF THIS STUDY IS FOR THE PROPER UNDERSTANDING OF THE WORKING CAPITAL OF ARABIAN INDUSTRIES LLC AND TO SUGGEST NECESSARY MEASURES TO OVERCOME THE SHORTFALLS IF ANY IN THE INDUSTRY.” The project undertaken is on “Working Capital Management of Arabian Industries LLC.”. It describes about how the company manages its working capital and the various steps that are required in the management of working capital. Cash is the lifeline of a company. If this lifeline deteriorates, so does the company's ability to fund operations, reinvest and meet capital requirements and payments. Understanding a company's cash flow health is essential to making investment decisions. A good way to judge a company's cash flow prospects is to look at its Working Capital Management (WCM). Working capital refers to the cash of a business requires for day-to-day operations or, more specifically, for financing the conversion of raw materials into finished goods, which the company

-

Upload

ankit-chauhan -

Category

Documents

-

view

14 -

download

3

description

Working capital Final project II

Transcript of Working capital Final project II 101230060546 Php app01

BACKGROUND OF THE STUDY.

“THE MAJOR OBJECTIVE OF THIS STUDY IS FOR THE PROPER UNDERSTANDING OF THE WORKING CAPITAL OF ARABIAN INDUSTRIES LLC AND TO SUGGEST NECESSARY MEASURES TO OVERCOME THE SHORTFALLS IF ANY IN THE INDUSTRY.”

The project undertaken is on “Working Capital Management of Arabian

Industries LLC.”. It describes about how the company manages its working

capital and the various steps that are required in the management of working

capital. Cash is the lifeline of a company. If this lifeline deteriorates, so does the

company's ability to fund operations, reinvest and meet capital requirements and

payments. Understanding a company's cash flow health is essential to making

investment decisions. A good way to judge a company's cash flow prospects is

to look at its Working Capital Management (WCM).

Working capital refers to the cash of a business requires for day-to-day

operations or, more specifically, for financing the conversion of raw materials

into finished goods, which the company sells for payment. Among the most

important items of working capital are levels of inventory, accounts receivable,

and accounts payable. Analysts look at these items for signs of a company's

efficiency and financial strength.

The working capital is an important yardstick to measure the company’s

operational and financial efficiency. Any company should have a right amount

of cash and lines of credit for its business needs at all times. This project

describes how the management of working capital takes place at Arabian

Industries LLC..

There are numerous instances in the history of business world where

inadequacy of working capital has led to business failures when a firm finds it

difficult to meetings day to day affairs. Operating expenses essential out lays

may have to be postponed for want of funds, operating plans will go out of gear

& enterprise objectives on investment slumps the suppliers & creditors of the

firm may have to wait longer to raise their dues & will hesitate to extend further

credit to the firm.

Thus efficient management of working capital in an important prerequisite for

successful working of a business concern it reduces the chances of business

failure generates a felling of security and confidence in the minds of personnel

in the organization it assurance solvency of steady of the organization.

STATEMENT OF PROBLEM

In the management of working capital, the firm is faced with two key problems:

1. First, given the level of sales and the relevant cost considerations, what are

the optimal amounts of cash, accounts receivable and inventories that a firm

should choose to maintain?

2. Second, given these optimal amounts, what is the most economical way to

finance these working capital investments? To produce the best possible results,

firms should keep no unproductive assets and should finance with the cheapest

available sources of funds. Why? In general, it is quite advantageous for the

firm to invest in short term assets and to finance short-term liabilities.

Besides this followings are some other problem , a firm is facing. Through this

study we try to find answer for these problems.

1. What are root causes of working capital on business?

2. What are the major effects on accounts receivable?

3. What is the nature of relationship between working capital and capital

employed

4. What steps should be taken to ensure that it effect on the profit of the firm

will not be negative?

5. How can working capital be managed?

6. What make up the working capital cycle?

7. How can debtors be controlled?

NEED AND IMPORTANCE OF THE STUDY.

1.This projects is helpful in knowing the companies position of funds

maintenance and setting the standards for working capital inventory levels,

current ratio level, quick ratio, current asset turnover level & size of current

liability etc.

2. This project is helpful to the managements for expanding the dualism & the

project viability & present availability of funds.

3. This project is also useful as it combines the present year data with the

previous year data and there by it show the trend analysis, i.e. increasing fund or

decreasing fund.

4. The project is done as a whole entirely. It will give overall view of the

organization and it is useful in further expansion decision to be taken by

management.

OBJECTIVES OF THE STUDY

The main objective of the study is to determine the effect of working capital on

business profitability which has to do with:-

1. Maintenance of working capital at appropriate level, and

2. Availability of ample funds as and when they are needed

To accomplishment of these two objectives, the management has consider the

composition of current assets pool. The working capital position sets the various

policies in the business with respect to general operations like purchasing,

financing, expansion and dividend etc,

The subsidiary Objective of Working Capital Management is to provide

adequate support for the smooth functioning of the normal business operations

of a company. This Objective can be sub-divided into 2 parts:-

1. Liquidity

2. Profitability

1) Liquidity

The quantum of Investment in Current Assets has to be made in a manner that it

not only meets the needs of the forecasted sales but also provides a built in

cushion in the form of safety stocks to meet unforeseen contingencies arising

out of factors such as delays in arrival of Raw Material, sudden spurts in

demand etc. Consequently, the investment in current assets for a given level of

forecasted sales will be higher if the management follows a conservative

attitude than when it follows an aggressive attitude. Thus, a company following

a conservative approach is subject to a lower degree of risk than the one

following an aggressive approach. Further, in the former situation the high

amount of Investment in Current Assets imparts greater liquidity to the

company than under the latter situation wherein the quantum of investment in

Current Asset is less. This aspect exclusively covers the liquidity dimension of

Working Capital.

2) Profitability

Once we recognize the fact that the total amount of financial resources at the

disposal of a company is limited and these can be put to alternative uses, the

larger the amount of investment in current assets, the smaller will be the amount

available for investment in other profitable avenues at hand with the company.

A conservative approach in respect of Investment in Current Assets leaves

fewer amounts for other Investments than an aggressive approach does.

HYPOTHESIS

Hypothesis is a conjectural statement of the relationships between two or more

variables. It is testable, tentative problem explanation of the relationship

between two or more variables that create a state of affairs or phenomenon.E,C,

Osuola said hypothesis should always be in declarative sentence form, and they

should relate to them generally or specially variable to variables.

Hypothesis thus:-

1. Explain observed events in a systematic manner

2. Predict the outcome of events and relationships

3. Systematically summarized existing knowledge.

In essence, there exist null hypothesis set up only to nullify the research

hypothesis and the alternative hypothesis, for the purpose of the study. For the

efficiency of the study, the hypothesis is as follows:

H 0

1. Working capital does not help the business concern in maintaining the

goodwill

2. Working capital does not create an environment of security, confidence,

and overall efficiency in a business

H 1

1. Working capital helps the business concern in maintaining the goodwill.

2. Working capital creates an environment of security, confidence, and overall

efficiency in business.

METHODOLOGY

Methodology may be a description of process, or may be expanded to include a

philosophically coherent collection of theories, concepts or ideas as they relate

to a particular discipline or field of inquiry. This project requires a detailed

understanding of the concept – “Working Capital Management”. Therefore,

firstly we need to have a clear idea of, what is working capital, how it is

managed in Arabian Industries LLC, what are the different ways in which the

financing of working capital is done in the organization etc.

To recognize the various type of information which are necessary for the study

of working capital management.

The management of working capital involves managing inventories,

accounts receivable and payable and cash. Therefore one also needs to

have a sound knowledge about cash management, inventory management

and receivables management.

Then comes the financing of working capital requirement, i.e. how the

working capital is financed, what are the various sources through which it

is done.

And, in the end, suggestions and recommendations on ways for better

management and control of working capital are provided.

Collection of data from various department of AILLC to analyze the working

capital management of the firm.

COLLECTION OF DATA

There are several ways of collecting both data-Primary and Secondary datas,

which differ considerably in context of money, cost, time and other sources at

the disposable of the researcher.

There are two types of data:

· Primary data

· Secondary data

1-Primary Data

Definition:-

The first handed information/Fresh data collected through various methods is

known as primary data.

In respect of primary data which the researchers are directly collects data

that have not been previously collected.

The primary data was gathered through personal interaction with various

functional heads and other technical personnel. Some information was also

collected by observation.

2-Secondary Data :

Definition:-

The data which have been already collected & comprised for another

purpose. Secondary data was collected various reports, annual reports,

documents charts, management information systems, etc in AI LLC, And also

collected various magazines, books, newspapers etc.

The analysis of the information gathered has been made on the basis of the

clarifications sought during the personal discussions with the concerned people

and perception during the personal visits to the important areas of services.

In marking observations identifying problems and suggesting certain remedies

such emphasis was given on the basis of opinions gathered during the personal

discussions and with the personal experience gained during the academic study

of M.B.A course.

TOOLS EMPLOYED

The data presentation tools are mainly Mathematical tools, Tables and Charts

are used for this study.

The most important parts of tools include;

a) Table numbers

b) Title of the table

c) Caption

d) Stub or the designation of the rows and columns

e) The body of the table

f) The head note or prefatory note or explanatory just before the title.

g) Source note, which refers to the literally or scientific source of the table

has observed that a table has the following merits over a prose

information that;

h) A table ensures an easy location of the required figure;

i) Comparisons are easily made utilizing a table than prose information;

j) Patterns or trends within the figures which cannot be visualized in the

prose information can be revealed and better depicted by a table; and a

table is more concise and takes up a less space than a prose formation:

TIME SPAN

A period of six year i.e. 2004-2009 has been taken for the study.

LIMITATIONS OF THE STUDY.

The following are the various limitations involved in the study.

.

1. The study in limited 4 years (2004-2005) to (2005-2006) performance of the

company.

2. The data used in this study have been taken from published annual report

only.

3. This study in conducted within a short period. During the limited period the

study may not be retailed, full fledged and utilization in all aspects.

4. Financial accounting does not take into account the price level changes.

5. We cannot do comparisons with other companies unless and until we have

the data of other companies on the same subject.

6. Only the printed data about the company will be available and not the back–

end details.

7. Future plans of the company will not be disclosed to us.

8. Lastly, due to shortage of time it is not possible to cover all the factors and

details regarding the subject of study.

LITERATURE REVIEW - AN OVER VIEW

“A literature review is an essay or is part of the introduction to an essay,

research report, or thesis. It provides an overview and critical analysis of

relevant published scholarly articles, research reports, books, theses etc on

the topic or issue to be investigated. A detailed guide to the literature review

is available on the Language and Learning services website. Literature

search: A systematic and exhaustive search for published material on a

specific topic.”

It discusses published information in a particular subject area, and

sometimes information in a particular subject area within a certain time

period. It is a summary of research that has been published about a particular

subject. It provides the reader with an idea about the current situation in

terms of what has been done, and what we know. Sometimes it includes

suggestions about what needs to be done to increase the knowledge and

understanding of a particular problem.

It gives an overview of what has been said, who the key writers are, what are

the prevailing theories and hypotheses, what questions are being asked, and

what methods and methodologies are appropriate and useful. As such, it is

not in itself primary research, but rather it reports on other findings.

Literature reviews can give you an overview or act as a stepping stone. It

also provide a solid background for a research paper's investigation.

A LITERATURE REVIEW MUST DO THESE THINGS:

be organized around and related directly to the thesis or research question

you are developing

synthesize results into a summary of what is and is not known

identify areas of controversy in the literature

formulate questions that need further research

Structuring a literature review

It is often difficult to decide how to organize the huge amount of

information you have collected.

The structure of each dissertation will be different but there are some

general principles and these are really the guidelines you should use for

any piece of academic writing.

Structuring a literature review

Introduction to the literature review

Main part

Conclusions

A literature review is a piece of discursive prose, not a list describing or

summarizing one piece of literature after another.

It's usually a bad sign to see every paragraph beginning with the name of a

researcher. Instead, organize the literature review into sections that present

themes or identify trends, including relevant theory.

ABSTRACT OF LITERATURE REVIEW

The current study contributes to the literature by examining impact of working

capital management on the operating performance and growth of new public

companies. The study also sheds light on the relationship of working capital

with debt level, firm risk, and industry. Using a sample of a manufacturing, the

study finds a significant positive association between higher levels of accounts

receivable and operating performance. The study further finds that maintaining

control (i.e. lower amounts) over levels of cash and securities, inventory, fixed

assets, and accounts payables appears to be associated with higher operating

performance, as well. We find that the firms which are experiencing unusually

high growth tend not to perform as well as those with low to moderate growth.

Further firms which are experiencing high growth tend to hold higher levels of

cash and securities, inventory, fixed assets, and accounts payables. These

findings tend to suggest that firms are willing to sacrifice performance (accept

low or negative operating returns) to increase their growth levels. The higher

level of growth is also associated with higher operating and financial risk. The

findings of this study suggest that perhaps the firms should stay more focused

on their operating performance than on maintaining high growth levels.

INTRODUCTION AND LITERATURE REVIEW

Working capital policy refers to the firm's policies regarding 1) target levels for

each category of current operating assets and liabilities, and 2) how current

assets will be financed. Generally good working capital policy (i.e. under

conditions of certainty) is considered to be one in which holdings of cash,

securities, inventories, fixed assets, and accounts payables are minimized.

The level of accounts receivables should be used as a means of

stimulating sales and other income. Previous literature on working capital

management has found a negative association, overall, between level of

working capital and operating performance as measured by operating returns

and operating margins (Peterson and Rajan, 1997). Under conditions of

certainty (i.e. sales, costs, lead times, payment periods, and so on, are known),

firms have little reason to hold more working capital than a minimum level.

AN ANALYSIS OF WORKING CAPITAL MANAGEMENT RESULTS ACROSS INDUSTRIES :-

INTRODUCTION

The importance of efficient working capital management (WCM) is

indisputable. Working capital is the difference between resources in cash or

readily convertible into cash (Current Assets) and organizational commitments

for which cash will soon be required (Current Liabilities). The objective of

working capital management is to maintain the optimum balance of each of the

working capital components.

Business viability relies on the ability to effectively manage receivables,

inventory, and payables. Firms are able to reduce financing costs and/or

increase the funds available for expansion by minimizing the amount of funds

tied up in current assets. Much managerial effort is expended in bringing non-

optimal levels of current assets and liabilities back toward optimal levels. An

optimal level would be one in which a balance is achieved between risk and

efficiency.

A recent example of business attempting to maximize working capital

management is the recurrent attention being given to the application of Six

Sigma® methodology. When used to identify and rectify discrepancies,

inefficiencies and erroneous transactions in the financial supply chain, Six

Sigma® reduces Days Sales Outstanding (DSO), accelerates the payment cycle,

improves customer satisfaction and reduces the necessary amount and cost of

working capital needs. There appear to be many success stories, including

Jennifer Towne’s (2002) report of a 15 percent decrease in days that sales are

outstanding, resulting in an increased cash flow of approximately 2 million

dollars at Thibodaux Regional Medical Center. Furthermore, bad debts

declined from 3.4 million dollar to o 600,000 dollar.

Even in a business using Six Sigma® methodology, an “optimal” level of

working capital management needs to be identified. Industry factors may impact

firm credit policy, inventory management, and bill-paying activities. Some

firms may be better suited to minimize receivables and inventory, while others

maximize payables. Another aspect of “optimal” is the extent to which poor

financial results can be tied to sub-optimal performance. Fortunately, these

issues are testable with data published by CFO magazine (Mintz and Lazere

1997; Corman 1998; Mintz 1999; Myers 2000; Fink 2001), which claims to be

the source of “tools and information for the financial executive,” and are the

subject of this research.

The following section presents a brief literature review. Next, the research

method is described, including some information about the annual Working

Capital Management Survey published by CFO magazine. Findings are then

presented and conclusions are drawn.

Many researchers have studied working capital from different views and

in different environments. The following are some useful research:

3.1 RELATED LITERATURE

The importance of working capital management is not new to the finance

literature. Over twenty years ago, Largay and Stickney (1980) reported that the

then-recent bankruptcy of W.T. Grant, a nationwide chain of department stores,

should have been anticipated because the corporation had been running a deficit

cash flow from operations for eight of the last ten years of its corporate life. As

part of a study of the Fortune 500’s financial management practices. Following

are the important views of scholars about working capital management.

1 GILBERT AND REICHERT (1995 ) :

Find that accounts receivable management models are used in 59 percent of

these firms to improve working capital projects, while inventory management

models were used in 60 percent of the companies. More recently, Farragher,

`index complete some form of a cash flow assessment, but did not present

insights regarding accounts receivable and inventory management, or the

variations of any current asset accounts or liability accounts across industries.

Thus, mixed evidence exists concerning the use of working capital management

techniques. Theoretical determination of optimal trade credit limits are the

subject of many articles over the years (e.g., Schwartz 1974; Scherr 1996), with

scant attention paid to actual accounts receivable management. Across a limited

sample,

2 WEINRAUB AND VISSCHER (1998) :

Observe a tendency of firms with low levels of current ratios to also have low

levels of current liabilities. Simultaneously investigating accounts receivable

and payable issues, Hill, Sartoris, and Ferguson (1984) find differences in the

way payment dates are defined. Payees define the date of payment as the date

payment is received, while payers view payment as the postmark date.

Additional WCM insight across firms, industries, and time can add to this body

of research. Maness and Zietlow (2002, 51, 496) presents two models of value

creation that incorporate effective short-term financial management activities.

However, these models are generic models and do not consider unique firm or

industry influences. Maness and Zietlow discuss industry influences in a short

paragraph that includes the observation that, “An industry a company is located

in may have more influence on that company’s fortunes than overall GNP”

(2002, 507).

3 ELJELLY, 2004 :

Elucidated that efficient liquidity management involves planning and

controlling current assets and current liabilities in such a manner that eliminates

the risk of inability to meet due short-term obligations and avoids excessive

investment in these assets. The relation between profitability and liquidity was

examined, as measured by current ratio and cash gap (cash conversion cycle) on

a sample of joint stock companies in Saudi Arabia using correlation and

regression analysis.

The study found that the cash conversion cycle was of more importance as a

measure of liquidity than the current ratio that affects profitability. The size

variable was found to have significant effect on profitability at the industry

level. The results were stable and had important implications for liquidity

management in various Saudi companies. First, it was clear that there was a

negative relationship between profitability and liquidity indicators such as

current ratio and cash gap in the Saudi sample examined. Second, the study also

revealed that there was great variation among industries with respect to the

significant measure of liquidity.

4 BERGAMI ROBERT (2007) :

Analysis that that international trade transactions carry inherently more risk than

domestic trade transactions, because of differences in culture, business

processes, laws and regulations. It is therefore important for traders to ensure

that payment is received for goods dispatched and that the goods received and

paid for comply with the contract of sale. One effective way of managing these

risks has been for traders to rely on the letter of credit as a payment method.

However for exporters in particular, the letter of credit has presented difficulties

in meeting the compliance requirements necessary for the payment to be

triggered.

The current rules that govern letter of credit transactions(UCP 500) have been

under review for the past three years and an updated set of rules (UCP 600) is

expected to be introduced on 1July 2007. This paper focuses on the changes

mooted for 2007and compares these main issues with the existing rules and

other associated guidelines and regulations governing this method of payment.

This paper considers the implication to changes of letter of credit transactions

and the sharing of risk. Firstly the paper provides some background to letters of

credit, then comments on existing literature and models, and subsequently an

analysis of the most important changes to the existing rules, before reaching a

conclusion. The conclusion is that the UCP 600 have not paid enough

consideration to traders and service providers and are likely to engender an

environment of uncertainty for exporters in particular.

INTRODUCTION- WORKING CAPITAL MANAGEMENT

“Working capital occupies a peculiar position in the capital structure of a

company. The decision as to the adequacy of working capital is a complicated

and yet a very important decision”.

Working capital is the life-blood of all types of enterprises, manufacturing and

trading both. It is constantly required to buy raw materials for payment of wages

and other day-to-day expenses. Without adequate working capital,

manufacturing operations will be crippled. For trading enterprises, the capacity

to stock a variety of goods for sale depends upon its working capital. It is a base

on which all the activities of business enterprise depend.

Many companies still under estimate the importance of working capital

management as a lever for freeing up cash from inventory, accounts receivable,

and accounts payable. By effectively managing these components, companies

can sharply reduce their dependence on outside funding and can use the released

cash for further investments or acquisitions. This will not only lead to more

financial flexibility, but also create value and have a strong impact on a

company’s enterprise value by reducing capital employed and thus increasing

asset productivity.

High working capital ratios often mean that too much money is tied up in

receivables and inventories. Typically, the knee-jerk reaction to this problem is

to apply the “big squeeze” by aggressively collecting receivables, ruthlessly

delaying payments to suppliers and cutting inventories across the board. But

that only attacks the symptoms of working capital issues, not the root causes. A

more effective approach is to fundamentally rethink and streamline key

processes across the value chain. This will not only free up cash but lead to

significant cost reductions at the same time.

Only those enterprises which have adequate working capital can survive in

times of depression. The investment in raw materials becomes long- term

investments during depression and cash flow declines due to fall in sale. In such

circumstances only enterprises with adequate working capital can survive.

Excessive working capital is equally unprofitable. The extra working capital is

not utilized in business operations and earns no profit for the firm. It results in

unnecessary accumulation of inventories, leading to inventory mishandling,

waste, theft etc. The abundance of working capital would lead to waste and

inefficiency

Shortage of working capital funds renders the firm unable to avail attractive

credit opportunities etc. The firm loses its reputation when it is not in a position

to honor its short term obligations. As a result, the firm faces tight credit terms.

It stagnates growth.

Definition:-

According to Guttmann & Dougall:-

“Working capital is defined as current assets minus current liabilities”.

A positive position means that a company is able to support its day-to-day

operations. i.e. to serve both maturing short-term debt and upcoming

operational expenses.

1. According to Park & Gladson:-

“The excess of current assets of a business (i.e. cash, accounts receivables,

inventories) over current items owned to employees and others (such as

salaries & wages payable, accounts payable, taxes owned to government)”

“Working capital like many other accounting terms and financial terms has been

used by different people in different senses.”

One school of thought believes that, as all capital resources available to a

business organization – From shareholders, bondholders, and creditors (secured

and unsecured) works up in the business activities to generate revenues and

facilitate future expansion and growth; they are to be considered as ‘working

capital’.

Another school of thought links working capital with current assets and

current liabilities. According to them, the excess of current assets over current

liabilities is to be rightly considered as the working capital of a business

organization.

According to “Shubin” working capital is “the amount of funds

necessary to cover the cost of operating the enterprise. Working capital in a

going concern is a revolving (circulating fund), it consists of cash receipts from

sales which are used to cover the cost of current operations.

“Circulating capital means current assets of the company that are changed in the

ordinary course of business from one form to another, as for example from cash

to inventories, inventories to receivables and receivables to cash.”

“Working capital is descriptive of that capital which is not fixed. But, the more

common use of working capital is to consider it as the difference between the

current assets and the current liabilities”. Current assets and current liabilities

are assets and liabilities which arise in the course of business. The WC

demonstrates the amount of liquid assets that are available to sustain and build

the business by measuring company’s efficiency and short-term financial health.

As such, it carries great value to those who might be interested in investing in

business or even purchasing it.

Working capital, also known as net working capital, is a measurement of

a business’s current assets, after subtracting its short-term liabilities, typically

short term. Sometimes referred to as operating capital, it is a valuation of the

assets that a business or organization has available to manage and build the

business. Generally speaking, companies with higher amounts of working

capital are better positioned for success because they have the liquid assets that

are essential to expand their business operations when required.

Characteristics of Working Capital

Working capital is the life blood and nerve centre of a business. Just as

circulation of blood is essential in the human body for maintaining life, working

capital is very essential to maintain the smooth running of a business. No

business can run successfully with out an adequate amount of working capital.

The features of working capital distinguishing it from the fixed capital are as

follows:

1 Short term Needs:

Working capital is used to acquire current assets which get converted into cash

in a short period. In this respect it differs from fixed capital which represents

funds locked in long term assets. The duration of the working capital depends

on the length of production process, the time that elapses in the sale and the

waiting period of the cash receipt.

2 Circular Movement:

Working capital is constantly converted into cash which again turns into

working capital. This process of conversion goes on continuously. The cash is

used to purchase current assets and when the goods are produced and sold out;

those current assets are transformed into cash. Thus it moves in a circular away.

That is why working capital is also described as circulating capital.

3 An Element of Permanency:

Though working capital is a short term capital, it is required always and forever.

As stated before, working capital is necessary to continue the productive

activity of the enterprise. Hence so long as production continues, the enterprise

will constantly remain in need of working capital. The working capital that is

required permanently is called “permanent or regular working capital”.

4 An Element of Fluctuation:

Though the requirement of working capital is felt permanently, its requirement

fluctuates more widely than that of fixed capital. The requirement of working

capital varies directly with the level of production. It varies with the variation of

the purchase and sale policy; price level and the level of demand also. The

portion of working capital that changes with production, sale, price etc. is called

“variable working capital”.

5 Liquidity:

Working capital is more liquid than fixed capital. If need arises, working capital

can be converted into cash within a short period and without much loss. A

company in need of cash can get it through the conversion of its working capital

by insisting on quick recovery of its bills receivable and by expediting sales of

its product. It is due to this trait of working capital that the companies with a

larger amount of working capital feel more secure.’

6 Less Risky:

Funds invested in fixed assets get locked up for a long period of time and can

not be recovered easily. There is also a danger of fixed assets like machinery

getting obsolete due to technological innovations. Hence investment in fixed

capital is comparatively more risky. As against this, investment in current assets

is less risky as it is a short term investment. Working capital involves more of

physical risk only, and that too is limited. Moreover, working capital gets

converted into cash again and again; therefore, it is free from the risk arising out

of technological changes.

7 Special Accounting System not needed:

Since fixed capital is invested in long term assets, it becomes necessary to adopt

various systems of estimating depreciation. On the other hand working capital is

invested in short term assets which last for one year only. Hence it is not

necessary to adopt special accounting system for them.

Among the most important items of working capital are levels of inventory,

accounts receivable, and accounts payable. Working capital can be expressed as

a positive or a negative number.

“When a company has more debts than current assets, it has negative

working capital; When current assets outweigh debts, a company has

positive working capital”.

A company will try to manage cash by:

Identifying the cash balance that allows it to meet day-to-day expenses

but minimizes the cost of holding cash;

Finding the level of inventory that allows for continuous production but

lessens the investment in raw materials and reduces reordering costs;

Identifying the appropriate source of financing, given the cash-conversion

cycle.

It may be necessary to use a bank loan or overdraft. However, inventory is

preferably financed by credit arranged with the supplier. If a company is not

operating efficiently, this will show up as an increase in the working capital.

This can be judged by comparing the amounts of working capital from one

period to another. Slow collection and inventory turnover may signal an

underlying problem in the company’s operations.

Advantages

Proper management of working capital gives a firm the assurance that it is able

to continue its operations and that it has sufficient cash flow to satisfy both

maturing short term debt and upcoming operational expenses.

Disadvantages

If a company’s current assets do not exceed its current liabilities, then it may

run into trouble paying back creditors in the short term.

A declining working-capital ratio over a longer time period could also be a red

flag that merits further analysis. For example, it could be that the company’s

sales volumes are decreasing and, as a result, its accounts receivable are

diminishing.

FACTORS INFLUENCING WORKING CAPITAL

4.1NEED OF WORKING CAPITAL

Working capital is among the many important things that contribute to the

success of a business. Without it, a business may cease to function properly or

at all. Not only does a lack of working capital render a company unable to build

and grow, but it may also leave a company with too little cash to pay its short-

term obligations. Simply put, a company with a very low amount of working

capital may be at risk of running out of money.

When a company has too little working capital, it can face financial difficulties

and may even be forced toward bankruptcy. This is true of both very small

companies and billion-dollar organizations. A company with this problem may

pay creditors late or even skip payments. It may borrow money in an attempt to

remain afloat. If late payments have affected the company’s credit rating, it may

have difficulty obtaining a loan at an affordable interest rate.

The need for working capital gross or current assets cannot be over

emphasized. As already observed, the objective of financial decision making is

to maximize the shareholders wealth. To achieve this, it is necessary to generate

sufficient profits can be earned will naturally depend upon the magnitude of the

sales among other things but sales can not convert into cash. There is a need for

working capital in the form of current assets to deal with the problem arising out

of lack of immediate realization of cash against goods sold. Therefore sufficient

working capital is necessary to sustain sales activity. Technically this is refers to

operating or cash cycle.

4.2CONCEPT OF WORKING CAPITAL

There are two concepts of working capital:

1. Gross working capital

2. Net working capital

Grossw Working Capital

“The gross working capital is the capital invested in the total current

assets of the enterprises. Current assets are those Assets which can

convert in to cash within a short period normally one accounting year.”

Constituents of Current Assets.

Current assets are assets which are expected to be sold or otherwise used within

one fiscal year. Typically, current assets include cash, cash equivalents,

accounts receivable, inventory, prepaid accounts which will be used within a

year, and short-term investments.

1 Cash in hand and cash at bank

2 Bills receivables/Sundry debtors

3 Short term loans and advances.

4 Inventories of stock as:

4.1 Raw material

4.2 Work in process

4.3 Stores and spares

4.4 Finished goods

5 Temporary investment of surplus funds.

6 Prepaid expenses

7 Accrued incomes.

8 Marketable securities.

Net Working Capital

“In a narrow sense, the term working capital refers to the net working

capital. Net working capital is the excess of current assets over current

liability”

“NET WORKING CAPITAL = CURRENT ASSETS – CURRENT“NET WORKING CAPITAL = CURRENT ASSETS – CURRENT

LIABILITIES.”LIABILITIES.”

Net working capital refers to the difference between current assets and current

liabilities. Current liabilities are those claims of outsiders which are expected to

mature for payment within an accounting year and include creditors, bills

payable and outstanding expenses. Net working capital can be positive or

negative

Constituents of Current liabilities

Current liabilities are considered as liabilities of the business that are to be

settled in cash within the fiscal year. Current liabilities include accounts payable

for goods, services or supplies, short-term loans, long-term loans with maturity

within one year, dividends and interest payable, or accrued liabilities such as

accrued taxes.

1. Accrued or outstanding expenses.

2. Short term loans, advances and deposits.

3. Dividends payable.

4. Bank overdraft.

5. Provision for taxation, if it does not amount to appropriation of profit.

6. Bills payable.

7. Sundry creditors.

The gross working capital concept is financial or going concern concept

whereas net working capital is an accounting concept of working capital. Both

the concepts have their own merits.

The gross concept is sometimes preferred to the concept of working capital for

the following reasons:

1. It enables the enterprise to provide correct amount of working capital at

correct time.

2. Every management is more interested in total current assets with which it

has to operate then the source from where it is made available.

3. It take into consideration of the fact every increase in the funds of the

enterprise would increase its working capital.

4. This concept is also useful in determining the rate of return on investments

in working capital. The net working capital concept, however, is also

important for following reasons:

1. It is qualitative concept, which indicates the firm’s ability to meet to its

operating expenses and short-term liabilities.

2. IT indicates the margin of protection available to the short term creditors.

3. It is an indicator of the financial soundness of enterprises.

4. It suggests the need of financing a part of working capital requirement out

of the permanent sources of funds.

Working capital, on the one hand, can be seen as a metric for evaluating a

company’s operating liquidity. A positive working capital position indicates that

a company can meet its short-term obligations. On the other hand, a company’s

working capital position signals its operating efficiency. Comparably high

working capital levels may indicate that too much money is tied up in the

business.

The most important positions for effective working capital management are

inventory, accounts receivable, and accounts payable. Depending on the

industry and business, prepayments received from customers and prepayments

paid to suppliers may also play an important role in the company’s cash flow.

Excess cash and no operational items may be excluded from the calculation for

better comparison.

4.3 CLASSIFICATION OF WORKING CAPITAL

Working capital may be classified in to ways:

On the basis of concept.

On the basis of time.

On the basis of concept working capital can be classified as gross working

capital and net working capital. On the basis of time, working capital may

be classified as:

Permanent or fixed working capital.

Temporary or variable working capital

A-Permanent OR Fixed Working Capital.

The operating cycle is a continuous feature in almost all the going concerns and

therefore creates the need for working capital and their efficient management.

However the magnitude of working capital required will not be constant, but

will fluctuate. At any time, there is always a minimum level of current assets

which is constantly and continuously required by a business unit to carry on its

operations. This minimum amount of current assets, which is required on a

continuous and uninterrupted basis, is after referred to as fixed or permanent

working capital. This type of working capital should be financed (along with

other fixed assets) out of long term funds of the unit. However in practice, a

portion of these requirements also is met through short term borrowings from

banks and suppliers credit.

Chart 4-1 Permanent Working Capital

Y

ValuePermanent Current Asset

O XTime

Permanent Working CapitalThe amount of current assets required to meet a firm’s long-term minimum

needs are called Permanent current assets.

For e.g., In a manufacturing unit, basic raw materials required for production

has to be available at all times and this has to be financed without any

disturbance.

B-Temporary OR Variable Working Capital.

Any amount over and above the permanent level of working capital is variable,

temporary or fluctuating working capital. This type of working capital is

generally financed from short term sources of finance such as bank credit

because this amount is not permanently required and is usually paid back during

The amount of Current Assets require to meet a firms long term minimum needs

off season or after the contingency. As the name implies, the level of fluctuating

working capital keeps on fluctuating depending on the needs of the unit unlike

the permanent working capital which remains constant over a period of time.

The Temporary or Variable working capital is the amount of working capital

which is required to meet the seasonal demands and some special exigencies.

Variable working capital can further be classified as Seasonal Working Capital

and Special Working Capital. The capital required to meet the seasonal need of

the enterprise is called seasonal working capital. Special working capital is that

part of working capital which is required to meet special exigencies such as

launching of extensive marketing for conducting research, etc.

Temporary working capital differs from Permanent working capital in the sense

that is required for short periods and cannot be permanently employed gainfully

in the business.

Chart 1-2 Temporary Working Capital

Y

Temporary current assets

Value

Permanent Working Capital

Time

Temporary Working Capital

The amount of Current Asset required

to meet short term minimum needs

4.4DETERMINANTS OF WORKING CAPITAL

Working capital management is an indispensable functional area of

management. However the total working capital requirements of the firm are

influenced by the large number of factors. It may however be added that these

factors affect differently to the different units and these keep varying from time

to time. In general, the determinants of working capital which are common to

all organizations can be summarized as under:

Nature of Business

This is one of the main factors. Usually in trading businesses the working

capital needs are higher as most of their investment is concentrated in stock or

inventory. Manufacturing businesses also need a good amount of working

capital to meet their production requirements. Whereas, those companies that

sell services and not goods, on a cash basis require least working capital

because there is no requirement on their part to maintain heavy inventories.

Size of Business

In very small company the working capital requirement is quit high due to high

overhead, higher buying and selling cost etc. as such medium size business

positively has edge over the small companies. But if the business start growing

after certain limit, the working capital requirements may adversely affect by the

increasing size.

Credit Terms / Credit Policy

Some time due to competition or custom, it may be necessary for the company

to extend more and more credit to customers, as result which more and more

amount is locked up in debtors or bills receivables which increase the working

capital requirement. On the other hand, in the case of purchase, if the credit is

offered by suppliers of goods and services, a part of working capital

requirement may be financed by them, but it is necessary to purchase on cash

basis, the working capital requirement will be higher.

Credit terms greatly influence working capital needs. If terms are:

buy on credit and sell by cash, working capital is lower

buy on credit and sell on credit, working capital is medium

buy on cash and sell on cash, working capital is medium

buy on cash and sell on credit, working capital is higher.

Prevailing trade practices and changing economic condition do generally

exert greater influence on the credit policy of concern. A liberal credit policy if

adopted more trade debtors would result and when the same is tightened, size of

debtors gets slim.

Credit periods also influence the size and composition of working capital. When longer credit period is allowed to debtors as against the one extended to the firm by its creditors, more working capital is needed and vice versa.

Collection policy is another influencing factor. A stringent collection policy might not only deter away some credit customers, but also force the existing customers to be prompt in settling dues resulting in lower level of working capital. The opposite holds well with a liberal collection policy.

Collection procedure also influences the working capital needs. A decentralized collection of dues from customers and centralized payments to suppliers shall reduce the size of working capital. Centralized collections and centralized payments would lead to moderate level of working capital. But with centralized collections and decentralized payments, the working capital need would be the highest.

Seasonality

Seasonality of Production

Agriculture and food processing and preservation industries have a seasonal production. During seasons, when production activities are in their peak, working capital need is high.

Seasonality in supply of raw materials

This also affects the size of working capital. Industries that use raw materials which are available during seasons only, have to buy and stock those raw materials. They cannot afford to buy these items in a phased way, since either supplies would get reduced or prices would be higher. Also, from the point of view of quality of raw materials, it pays to buy in bulk during the seasons. Hence the high level of working capital needed when season exists for raw materials.

Seasonality of demand for finished goods

In case of products like umbrella, rain-coats and other seasonal items, the demand is high during peak seasons. But the production of these items has to be continuous throughout the year to meet the high demand during peak seasons. Thus, working capital requirement would be higher.

“Since Arabian Industries LLC is a contracting company, the above mentioned seasonal factors do not affect its operation or its business cycle. “

Business Trade Cycle

Trade cycle refers to the periodic turns in business opportunities from extremely peak levels, via a slackening to extremely tough levels and from there, via a recovery phase to peak levels, thus completing a business cycle. There are 4 phases of trade cycle.

Boom Period – more business, more production, more working capital.

Depression period – less business, less production, less working capital.

Recession period – slackening business, stock pile-up, more working

capital.

Recovery period – recouping business, stock speedily converts to sales,

less working capital.

Inflation

Under inflationary conditions generally working capital increases, since with

rising prices demand reduces resulting in stock pile-up and consequent increase

in working capital.

Length of Production cycle

The time lapse between feeding of raw material into the machine and obtaining

the finished goods out from the machine is what is described as the length of

manufacturing process. It is otherwise known as conversion time. Longer this

time period, higher is the volume and value of work-in-progress and hence

higher the requirement of working capital and vice versa.

System of Production process

If capital intensive, high-technology automated system is adopted for

production, more investment in fixed assets and less investment in current assets

are involved. Also, the conversion time is likely to be lower, resulting in further

drop in the level of working capital. On the other hand, if labor intensive

technology is adopted, less investment in fixed assets and more investment in

current assets which would lead to higher requirement of working capital.

Growth and expansion plans

Growth and expansion industries need more working capital than those that are

static.

Profitability

The profitability of the business may be vary in each and every individual case,

which is in turn its depend on numerous factors, but high profitability will

positively reduce the strain on working capital requirement of the company,

because the profits to the extend that they earned in cash may be used to meet

the working capital requirement of the company.

Operating efficiency

If the business is carried on more efficiently, it can operate in profits which may

reduce the strain on working capital; it may ensure proper utilization of existing

resources by eliminating the waste and improved coordination etc.

Apart from the above factors, dividend policy, depreciation policy, price level

changes, operating efficiency and government regulations also influence the

level and the size of working capital.

RESEARCH METHODOLOGY - INTRODUCTION

Research Methodology is a purposeful, precise and systematic search for new

knowledge, skills, attitudes and values, or for the re-interpretation of existing

knowledge, skills, attitudes and values.

Research methodology is a way to systematically solve the research problem. It

may be understood as a science of studying now research is done

systematically. In that various steps, those are generally adopted by a researcher

in studying his problem along with the logic behind them.

Data collection is important step in any project and success of any project will

be largely depend upon now much accurate you will be able to collect and how

much time, money and effort will be required to collect that necessary data, this

is also important step.

Various Steps for Research Methodology

This project requires a detailed understanding of the concept – “Working

Capital Management”. Therefore, firstly we need to have a clear idea of what is

working capital, how it is managed in AI LLC, what are the different ways in

which the financing of working capital is done in the company.

The management of working capital involves managing inventories, accounts

receivable and payable and cash. Therefore one also needs to have a sound

knowledge about cash management, inventory management and receivables

management.

Then comes the financing of working capital requirement, i.e. how the working

capital is financed, what are the various sources through which it is done.

And, in the end, suggestions and recommendations on ways for better

management and control of working capital are provided.

5.1SCOPE OF THE STUDY

This project is vital to us in a significant way. It does have some importance for

the company too. These are as follows:–

This project will be a learning device for the finance student.

Through this project we would study the various methods of the working

capital management.

The project will be a learning of planning and financing working capital.

The project would also be an effective tool for credit policies of the

companies.

This will show different methods of holding inventory and dealing with

cash and receivables.

This will show the liquidity position of the company and also how do

they maintain a particular liquidity position.

5.2TYPES OF DATA COLLECTION

There are two types of data collection methods available.

1. Primary data collection

2. Secondary data collection

5.2.1 Primary data collection method

Primary data is the data which the researcher collects through various

methods like interviews, surveys, questionnaires etc, to support the

secondary data. Some advantages and disadvantages of primary data are

as follows:

5.2.2 Secondary data collection method

Secondary data is data collected by someone other than the user.

Common sources of secondary data for social science include censuses,

surveys, organizational records and data collected through qualitative

methodologies or qualitative research. Primary data, by contrast, are

collected by the investigator conducting the research.

This project is based on primary data collected through personal interview of

head of Finance Department, head of Statistical Quality Control department and

other concerned staff member of finance department. But primary data

collection had limitations such as matter confidential information thus project is

based on secondary information collected through four years annual report of

the company, supported by various books and internet sides. The data collection

was aimed at study of working capital management of the company.

Project is based on:

Financial Report of Arabian Industries LLC – 2004-2005-2006-2007-2008-

2009

5.3OBJECTIVES OF THE STUDY.

This research is focusing on working capital management and its effects on

profitability for a sample of Omani firm. Study of the working capital

management is important because unless the working capital is managed

effectively, monitored efficiently planed properly and reviewed periodically at

regular intervals to remove bottlenecks if any the company can not earn profits

and increase its turnover. With this primary objective of the study, the following

further objectives are framed for a depth analysis.

5.3.1 The Main objectives of the studies are:

1. To study the way and means of working capital finance of the company.

2. To estimate the operating cash cycle and working capital requirement of

the company.

3. To establish a relationship between Working Capital Management and

Profitability over a period of five years of the company..

4. To find out the effects of different components of working capital

management on Profitability

5. To establish a relationship between the two objectives of liquidity and

profitability of the Omani firm.

6. To find out the relationship between debt used by Arabian Industry LLC

and its Profitability

7. To draw conclusion about relationship of working capital management

and profitability of the company.

8. To study the optimum level of current assets and current liabilities of the

company.

9. To study the liquidity position through various working capital related

ratios.

10. To study the working capital components such as receivables accounts,

cash management, Inventory position

5.3.2 Analysis Used in Study : Descriptive analysis .

Descriptive Statistics are used to describe the basic features of the data in a

study. They provide simple summaries about the sample and the measures.

Together with simple graphics analysis, they form the basis of virtually

every quantitative analysis of data. With descriptive statistics you are simply

describing what is, what the data shows

5.3.3 Research Design

STEP 1 - To study the Financial Statement of Arabian Industries LLC

STEP 2 – Data Analysis of working capital through Estimation of

Working Capital.

STEP 3 – Analysis of Inventory Management of Arabian Industries

LLC.

STEP 4 – Comparison of base year data’s with previous years datas.

5.3.4 Data Collection

5.3.4.1 The information is collected through the Primary Source like:-

Interviewing the employees of the department.

Getting information from MIS department.

Discussion with the head of the Finance department and

Procurement department.

5.3.4.2 The Data was collected from following Secondary Sources like:-

Corporate department

Procurement department

Finance department

Logistic Department

5.4SCOPE AND LIMITATIONS OF THE STUDY

5.4.1 Scope of the study

The scope of the study is identified after and during the study is conducted.

The study of working capital is based on tools like trend Analysis, Ratio

Analysis, working capital leverage, operating cycle etc. Further the study is

based on last 5 years Annual Reports of Arabian Industries LLC, and even

factors like competitor’s analysis, industry analysis were not considered

while preparing this project.

Limitations of the study

Following limitations were encountered while preparing this project:

1) Limited data:-

This project has completed with annual reports; it just constitutes one part of

data collection i.e. secondary. There were limitations for primary data

collection because of confidentiality.

2) Limited period:-

This project is based on five year annual reports. Conclusions and

recommendations are based on such limited data. The trend of last five year

may or may not reflect the real working capital position of the company

3) Limited area:-

Also it was difficult to collect the data regarding the competitors and their

financial information. Industry figures were also difficult to get.

Working Capital level

The guiding principle for working capital is called the hedging principle or

principle of self-liquidating debt or matching principle (different from the

matching principle used in measuring accounting profit).

It is an accepted belief in business that the term of a funding arrangement must

match the term of the investment itself. This means that any funds used for

short-term assets or purposes should be financed from short-term sources.

Likewise investments in long term-assets should be funded from long-term

sources.

Therefore a key criterion for acquiring additional finance is matching up the life

of the assets acquired with the term of the loan or other method of funding. For

example, the buying of an unusually large quantity of inventory should be

financed by a loan, or credit, with a repayment period of less than one year.

The level of any long-term assets funded by short-term debt shows the firm's

level of 'aggression' in its financing policy. Although this type of action may

increase profits (due to the lower cost of short-term debt) it greatly increases the

risk of cash shortages if short-term financing can't be renewed.

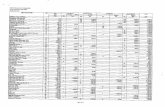

Table 6.1- Size of Working Capital

SOURCE: COMPANY REPORT

EXTRACTED FROM AUDITED BALANCE SHEET OF ARABIAN INDUSTRIES LLC

2004 2005 2006 2007 2008 2009CURRENT ASSET

Bank Balances

45,595

196,78

6

67,900

562,828

143,351

1,892,37

2

Trade Debtors

2,188,3

48

2,921,7

99

7,702,72

7

12,543,1

78

20,194,2

01

13,437,9

81

Inventory

112,63

9

459,40

4

160,412

373,118

563,989

724,145

Work in Progress

1,758,7

19

2,142,7

70

2,773,63

5

1,275,52

3

1,422,62

5

2,274,69

0

Dues from Related Parties

-

-

214,325

191,658

316,956

4,632,78

9

Other Receivables

349,38

8

52,319

725,857

512,228

336,700

99,243 TOTAL CURRENT ASSETS

4,454,6

89

5,773,0

78

11,644,8

57

15,458,5

33

22,977,8

22

23,061,2

19

- - - - - - CURRENT LIABILITIES

-

-

-

-

-

-

Short-term Borrowings

340,86

7

900,67

6

2,049,74

5 -

2,015,75

3

553,812 Current Portion of Long Term loan

147,49

3

184,71

7

498,801

1,436,56

7

1,503,56

9

2,188,44

6

Trade Creditors

1,171,3

01

3,013,7

26

5,154,02

3

6,840,68

8

10,293,7

95

6,186,85

4

Dues to Related Parties

449,84

2

2,043

23,504

31,073

1,499,97

3

420,900 Provisions - Tax

-

27,422

182,064

175,183

402,530

922,451

Other Payables

1,217,5

74

1,533,5

52

3,489,97

0

6,652,45

4

6,948,03

5

5,588,56

9 TOTAL CURRENT LIABILITIES

3,327,0

77

5,662,1

35

11,398,1

06

15,135,9

65

22,663,6

55

15,861,0

31 NET

WORKING CAPITAL -

(A-B)

1,127,612

110,943 246,751 322,568 314,167 7,200,18

8

1.1 WORKING CAPITAL TREND ANALYSIS

Trend analysis is an improvement over the year to year analysis. When a

comparison of Financial Statements covering more than 3 years is undertaken,

the year to year analysis becomes cumbersome. In trend analysis, the changes

are calculated for several successive years instead of two or three years.

Therefore the trend analysis is a company's financial position over a long period

of time. Trend analysis is important as it may point to basic changes in the

nature of business and also helps in drawing meaningful conclusions regarding

the operating performance over several years and the financial position of the

enterprise. It is based on the idea that what has happened in the past gives an

idea of what will happen in the future.

In working capital analysis the direction at changes over a period of time is of

crucial importance. Working capital is one of the important fields of

management. It is therefore very essential for an annalist to make a study about

the trend and direction of working capital over a period of time. Such analysis

enables as to study the upward and downward trend in current assets and current

liabilities and it’s effect on the working capital position.

In the words of S.P. Gupta “The term trend is very commonly used in day-

today conversion trend, also called secular or long term need is the basic

tendency of population, sales, income, current assets, and current liabilities

to grow or decline over a period of time”.

According to R.C.Galeziem “The trend is defined as smooth irreversible

movement in the series. It can be increasing or decreasing.”

Emphasizing the importance of working capital trends, Man Mohan and Goyal

have pointed out that “analysis of working capital trends provide as base to

judge whether the practice and privilege policy of the management with regard

to working capital is good enough or an important is to be made in managing

the working capital funds.

Further, any one trend by it self is not very informative and therefore

comparison with Illustrated their ideas in these words, “An upwards trends

coupled with downward trend or sells, accompanied by marked increase in plant

investment especially if the increase in planning investment by fixed interest

obligation”

One of the main goals of trend analysis is to forecast future values of the series.

It allows a researcher to look at a pattern of change over a long period of time

rather than at a single discrete point in time or over a short time so that better

conclusions can be drawn.

Table 6.2 – Working Capital Variance Analysis.

ANALYSIS OF VARIANCE OF

WORKING CAPITAL

YEARS 2004 2005 2006 2007 2008 2009

TOTAL

CURRENT

ASSETS

4,454,6

89

5,773,0

78

11,644,8

57

15,458,5

33

22,977,8

22

23,061,2

19

TOTAL

CURRENT

LIABILITIES

3,327,0

77

5,662,1

35

11,398,1

06

15,135,9

65

22,663,6

55

15,861,0

31

NET

WORKING

CAPITAL - (A-

B)

1,127,6

12

110,94

3246,751 322,568 314,167

7,200,18

8

W-C

VARIATION –

in %

100% 9.84% 21.88% 28.61% 27.86%638.53

%

(“Index = 100 X Index Year Amount / Base Year Amount”)

Chart-6.1- Working capital index

WORKING CAPITAL INDEX

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

2004 2005 2006 2007 2008 2009

YEARS

VA

LUE

TOTAL CURRENTASSETS

TOTAL CURRENTLIABILITIES

NET WORKINGCAPITAL - (A-B)

W-C VARIATION –in%

Table 6.3-Working capital size

ANALYSIS OF VARIANCE OF

WORKING CAPITAL

YEARS 2004 2005 2006 2007 2008 2009

TOTAL

CURRENT

ASSETS

4,454,6

89

5,773,0

78

11,644,8

57

15,458,5

33

22,977,8

22

23,061,2

19

TOTAL

CURRENT

LIABILITIES

3,327,0

77

5,662,1

35

11,398,1

06

15,135,9

65

22,663,6

55

15,861,0

31

NET

WORKING

CAPITAL - (A-

B)

1,127,6

12

110,94

3246,751 322,568 314,167

7,200,18

8

W-C

VARIATION –

in %

100% 9.84% 21.88% 28.61% 27.86%638.53

%

The computation of a series of Index Numbers requires the choice of a

base year that will for all times have an index number of 100. The base period

should be a normal year with regard to business conditions, since the base year

used as a reference should be representative. Generally, the earliest year is

selected as a base year. However, where the earliest year is selected as the

normal year then another year is chosen. All Index numbers are computed with

reference to the base year using this formula

1.1.1 OBSERVATIONS

It was observed that major source of liquidity problem is the mismatch between

current payments and current receipts from the Comparison of funds flow

statements of AI LLC for six years. It was observed that in the year 2005

current assets increased by around 29.6% compared to 2004 and current

liabilities increased by 70.18% which affect as working capital reduced by

9.84% in the year 2005 compared to 2004.because the net working capital was

OMR 1,127,612/- in 2004 but in 2005 it was reduced to OMR 110,943/- in the

year 2005 due to the increase in current liability of 70% compared to 2004. In

2004 current liability was OMR 3,327,077, where as in 2005 it was increased by

OMR 2,335,058/-; a total liability of OMR 5,662,135/- in 2005.

In the year 2006, 2007, 2008 a tremendous increase we can see in current

liability by 172.4%, 112.35%, and 226.26% res. and current asset also increased

accordingly compared to 2004 like 131.8%, 85.61% and 168.79% during the

year 2006, 2007, 2008. In the year 2009 we can see the growth of current asset

is very less compared to 2004 with a percentage of only 1.87% where as in the

current liability we can see there is a slop of -2004.46% compared to 2004,

where as an increase in current asset for 73.478% compared to 2004 and a good

nest asset (WC reserve) is with the firm for an increased percentage of 638.53%

in the year 2009.

The position of working capital is very good in 2009 because the bank balance

in 2008 was only 143,351/- OMR where as in 2009 it is increased to OMR

1,892,372/-; ie. 1220% compared to 2008, which is quite good and also we can

see that there is receivable from related parties is 4,632,789/- in the year 2009,

where as in 2008 it was only OMR 316,956/-; that means an increase is for

1361% in the year 2009 compared to 2008. That means the fund position is

quite good for 2009.

While compared to 2004 current assets have been increased by 417.68% and

current liabilities have been increased by 376.73%. But compared to 2008 and

2009 there is a short fall of -30.02% in current liabilities, where as an increase

in current asset is only an increase of .36%. The bank balance is increased to

OMR 1,892,372/- in 2009 from OMR 143,351/- in the year 2008.It shows that

management is using only it’s own fund for the short term requirements and

WC has been increased to OMR 7,200,186/- in the year 2009-A growth of

638.53%. This two together pushed down the net working capital to the present

level. The increase in working capital is a clear indication that the company is

utilizing its own funds and resources with efficiency.

Table 6.4 –Variance Analysis of Current Asset and Current Liability.

OBSERVATION OF WORKING

CAPITAL YEARS 2004 2005 2006 2007 2008 2009TOTAL CURRENT ASSETS

529853 686666 1385071 1838680 2733045 2742964

YEARLY VARIATION 100 156813 698405 453609 894365 9920GROWT COMPARED TO 2004

100 29.60 131.81 85.61 168.79 1.87

YEARLY GROWTH IN %

100 29.60 101.71 32.75 48.64 0.3

6

TOTAL CURRENT LIABILITIES

395732 673470 1355722 1800313 2695677 1886554

YEARLY VARIATION

395732 673470 1355722 1800313 2695677 1886554

GROWTH COMPARED TO 2004

100

70.18

172.40 112.35 226.26 (204.46

)

YEARLY GROWTH IN %

100

70.18 101.30 32.79 49.73 (30.02)

NET WORKING CAPITAL - (A-B)

134121 13196 29349 38367 37368 856410

WORKING CAPITAL SIZE

100 9.84 21.88 28.61 27.86 638.53

TOTAL CURRENT ASSETS 100

156812.76

855218.25

1308827.295

2203192.035

2213111.565

VARIATION COMPARED TO 2004 100 29.6 161.41 247.02 415.81 417.68TOTAL CURRENT LIABILITIES 100

277738.2

959990.265

1404581.445

2299945.455

1490822.82

VARIATION 100 70.18 242.59 354.93 581.19 376.73

COMPARED TO 2004

1.2CURRENT ASSETS

A balance sheet item which equals the sum of cash and cash equivalents,

accounts receivable, inventory, marketable securities, prepaid expenses, and

other assets that could be converted to cash in less than one year. A company's