Working Capital Efficiency Benchmarking - Amazon S3 · The measurement of working capital...

32

Jan 2015 Working Capital Efficiency Benchmarking

Transcript of Working Capital Efficiency Benchmarking - Amazon S3 · The measurement of working capital...

Jan 2015

Working Capital

Efficiency Benchmarking

Contents

Introduction Pages 3-4

Section 1 - Accounts Receivable Pages 5-11

Section 2 - Accounts Payable Pages 12-19

Section 3 - Inventory / Working Capital Pages 20-23

Section 4 - Users of the SystemSection 4 - Users of the System Pages 24-31

Auditors

Due Diligence/M&A

Risk Finance

Business Management/KPI's

Contacts Page 32

Copyright 2015 Mantramax Pty Ltd -

All rights reserved2

Introduction

The measurement of working capital efficiencies are covered in many industry white

papers and are most often the most single cause of bankruptcies.

Companies experiencing higher than normal growth can experience cash flow problems

if this critical resource (asset) is not managed properly. Benchmarking against

comparable industry standard/average is common practice.

Section 1 and 2 of this set of publications details benchmarking methods for Accounts

Receivable and Payable using weighted sales/purchase values, taking into account the

relevant payment terms, from the source of the transaction instead of the balance relevant payment terms, from the source of the transaction instead of the balance

sheet information.

Manipulation (intentional or unintentional) of ageing periods is completely eliminated

in this instance and provide an objective and true reflection of the performance of

these functions under Working Capital (Section 3).

Key Performance Indicators (KPI's) formulation and monitoring for each function are

addressed in Section 1,2 and 3.

These KPI's can be applied over groups of employees, divisions or groups.

Copyright 2015 Mantramax Pty Ltd -

All rights reserved3

Measurement Benchmark

Data

Used

Working

Capital Optimum Benchmark Data UsedS

ectio

n

Days Sales

Outstanding

(DSO)

Industry

Average

Debtors

Ageing

Accounts

Receivable

Days Sales

Outstanding

Benchmark (DSOB)

Turnover incl

VAT/Sales Tax,

Weighted by

Payment Term and

Value 1

Days Payables

Outstanding Industry Creditors Accounts

Payable

Days Payables

Outstanding

Purchases incl

VAT/Sales Tax,

Weighted by

Payment Term and Outstanding

(DPO)

Industry

Average

Creditors

Ageing PayableOutstanding

Benchmark (DPOB)

Payment Term and

Value 2

Days Sales of

Inventory (DSI)

Industry

Average

Historical

Cost of

Good

Sold Inventory

Days Forecasted

Sales of Inventory

(DFSI)

Inventory days by

Forcast Cost of

Goods Sold 3

DSO + DSI - DPO =

CCC (days) CCC (Value) 3

DSOB + DFSI -DPOB =

CCCB (days) CCCB (Value) 3

CCC - CCCB $$$$$ 3

Cash Conversion Cycle (CCC)

Cash Conversion Cycle Benchmark (CCCB)

Value locked up in Working Capital Effeciencies

Copyright 2015 Mantramax Pty Ltd -

All rights reserved4

Section 1 - Accounts Receivable

Analysis tools available to measure Accounts Receivable performance :

Measurement Standard Method Preferred Method

Debtors Days

Debtors Balance or Average Debtors /

Annual Sales X 365

Receivables Balance / Annualised Sales for

current and immediate past two month (ie

Sales 3 months X 12/3) X 365

Countback method :

Reducing Receivables balance starting from

current month X days in month. Calculate

Copyright 2015 Mantramax Pty Ltd -

All rights reserved

Days Sales Outstanding

(DSO)

Closing Debtors / Total Credit Sales X

Days in period

current month X days in month. Calculate

until AR balance is exhausted and add up

the different days

Benchmark

Best Possible Days Sales

Outstanding (BPDSO) Current Receivable / Total Credit Sales X Days in period

Average Days Deliquent

(ADD) DSO - BPDSO

Collection Effectiveness

Index (CEI)

(Opening Receivables + Credit Sales in Period - Ending Total Receivables) /

(Opening Receivables + Credit Sales in Period - Ending Current Receivables ) X 100

5

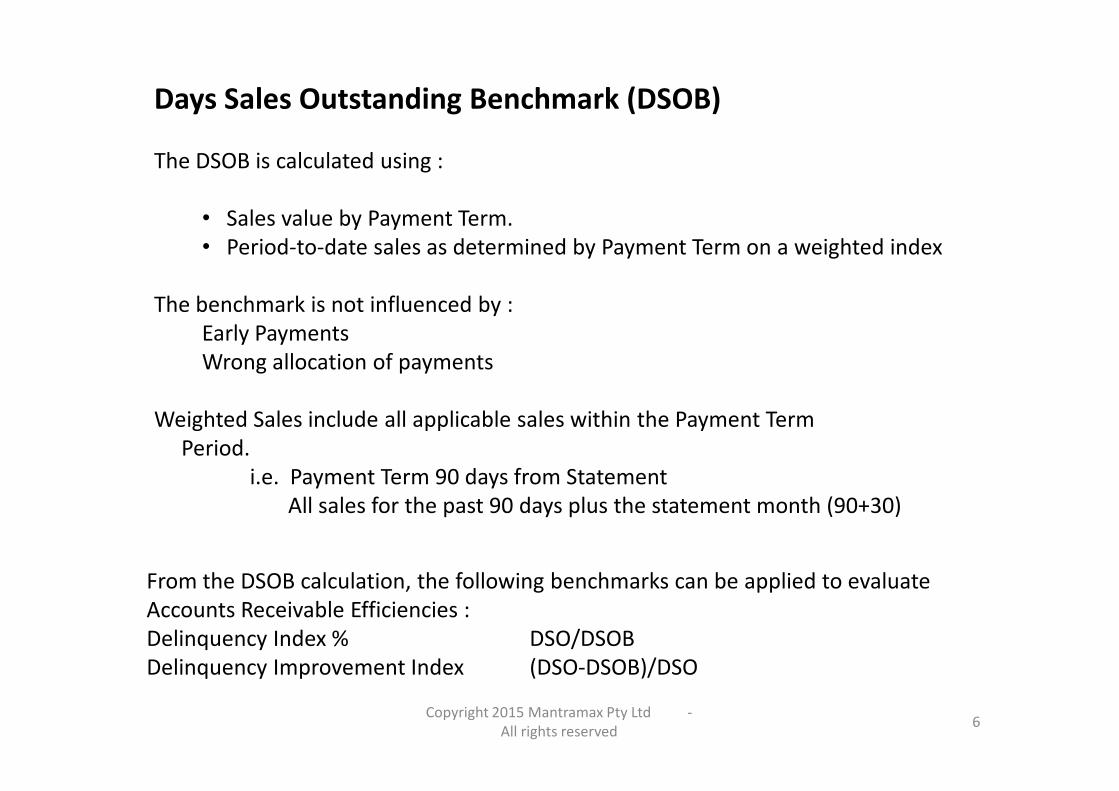

Days Sales Outstanding Benchmark (DSOB)

The DSOB is calculated using :

• Sales value by Payment Term.

• Period-to-date sales as determined by Payment Term on a weighted index

The benchmark is not influenced by :

Early Payments

Wrong allocation of payments

Copyright 2015 Mantramax Pty Ltd -

All rights reserved

Weighted Sales include all applicable sales within the Payment Term

Period.

i.e. Payment Term 90 days from Statement

All sales for the past 90 days plus the statement month (90+30)

From the DSOB calculation, the following benchmarks can be applied to evaluate

Accounts Receivable Efficiencies :

Delinquency Index % DSO/DSOB

Delinquency Improvement Index (DSO-DSOB)/DSO

6

Accounts Receivable Data Required

1. Turnover incl VAT Totals by Payment Term

(Standard report in most accounting packages)

2. Debtors Aged Totals (Standard report)

** Note that no confidential information i.e Client Names are required

If the information in Report 1 is not available, an alternative option is to use Excel

linking Debtors Ageing with Payment Terms (Master file) and sub-total by change

in Payment Term.

Copyright 2015 Mantramax Pty Ltd -

All rights reserved

in Payment Term.

A variance in both value of individual Payment Terms and Total Sales per Month

are used to illustrate the effect on DSOB more effectively.

In the sample only 7 months data were used but the number of historical periods

is unlimited. The more periods used, the better visual impacts of the graphs

shown later.

Current Debtors are based on the current month turnover to show the effect on

BPDSO if not properly aged.

7

Example of Input Format

Copyright 2015 Mantramax Pty Ltd -

All rights reserved8

Accounts Receivable Review (Model Output)

Copyright 2015 Mantramax Pty Ltd -

All rights reserved9

The performance review clearly shows the performance of the Credit Control

function month by month, benchmarked against its internal Credit Policy.

Using an Industry Standard i.e. 60 days (30 days statement) as a general

benchmark against DSO would show a decline in the Credit Control function

where in fact the opposite is true comparing it to the DSOB.

DSOB calculated the fluctuations in sales volume and mix of payment terms on a

monthly basis.

Accounts Receivable Performance Review

Copyright 2015 Mantramax Pty Ltd -

All rights reserved

monthly basis.

Forecasting using the same method can be used to more accurately project Account

Receivables balance in each period and highlight potential cash flow problems due to

a change in sales mix (payment term customers).

10

Setting and Evaluating KPI's

From the same dataset, KPI's can be set for individual Credit Controllers, Credit

Managers, Divisions and Diverse Groups of Companies (various industries).

Copyright 2015 Mantramax Pty Ltd -

All rights reserved

** The Initial Benchmark is set at the start of the incentive program and should remain constant for a set period length (until next

review).

The participant's (i.e. credit controller) performance will be benchmarked monthly against his/her own credit portfolio.

If a monetary incentive is favoured, a suggested method used above calculates the Financial Return of the improved DSOB Index on

the cash flow benefit. If the Credit Book is below the Initial Benchmark, then no benefit will be payable to the participant.

Alternatively, the DSOB Benchmark can be used for annual performance reviews using an average Index over the year.

11

Section 2 - Accounts Payable

Analysis tools available to measure Accounts Payable performance :

Measurement Standard Method Preferred Method

Creditors DaysCreditors Balance or Average Creditors /

Annual Purchases X 365

Payables Balance / Annualised

Purchases for current and immediate

past two month (ie Purchases 3 months

X 12/3) X 365

Days Payables

Countback method :

Reducing Payables balance starting from

current month X days in month.

Copyright 2015 Mantramax Pty Ltd -

All rights reserved

Days Payables

Outstanding (DPO)Closing Creditors / Total Credit Purchases

X Days in period

current month X days in month.

Calculate until AP balance is exhausted

and add up the different days

BenchmarkBest Possible Days

Payables Outstanding

(BPDPO) Current Payables / Total Credit Sales X Days in period

Average Days Deliquent

(ADD) DPO - BPDPO

** It must be noted that a very high ADD could result in loss of discounts or stop

supply from Suppliers.

12

Days Payables Outstanding Benchmark (DPOB)

The DPOB is calculated using :

• Purchases value by Payment Term.

• Period-to-date purchases as determined by Payment Term on a weighted index.

The benchmark is not influenced by :

Early Payments

Wrong allocation of payments

Copyright 2015 Mantramax Pty Ltd -

All rights reserved

Wrong allocation of payments

Weighted Purchases include all applicable sales within the Payment Term

Period.

i.e. Payment Term 90 days from Statement

All purchases for the past 90 days plus the statement month (90+30)

From the DPOB calculation, the following benchmarks can be applied to evaluate

Accounts Payable Efficiencies :

Delinquency Index % DPO/DPOB

Delinquency Improvement Index (DPO-DPOB)/DPO

13

Many analysts use Cost of Sales instead of Purchases to calculate Days Payables

Outstanding. This calculation would not be a correct as there is no relationship between

Accounts Payable and Cost of Sales in a specific month.

Purchases effect the Inventory value and not the Cost of Sales value.

Purchases can be calculated in the following manner :

Purchases = Cost of Sales

– Opening Inventory

Purchases or Cost of Sales

Copyright 2015 Mantramax Pty Ltd -

All rights reserved

– Opening Inventory

+ Closing Inventory

If Accounts Payable transactions include non-stock items i.e Expenses, then the value of

these expenses should be included in the Purchases calculation.

All Purchases must include VAT as the Accounts Payable is inclusive of VAT.

The Purchases value is more complex to calculate compared to revenue because of the

different cost lines applicable. Alternative methods of obtaining the purchases values

are discussed in the next slide.

14

Accounts Payable Data Required

1. Purchases incl VAT Totals by Payment Term

(Standard report in most accounting packages)

2. Creditors Aged Totals (Standard report)

** Note that no confidential information i.e Supplier Names are required

If the information in Report 1 is not available, an alternative option is to use Excel

linking Supplier Ageing with Payment Terms (Master file) and run a transaction

list from Accounts Payable and sub-total by change in Payment Term.

Copyright 2015 Mantramax Pty Ltd -

All rights reserved

list from Accounts Payable and sub-total by change in Payment Term.

A variance in both value of individual Payment Terms and Total Purchases per

Month are used to illustrate the effect on DPOB more effectively.

In the sample only 7 months data were used but the number of historical periods

is unlimited. The more periods used, the better visual impacts of the graphs

shown later.

Current Creditors are based on the current month turnover to show the effect on

BPDPO if not properly aged.

15

Example of Input Format

Data Input Grey Area

Purchases incl VAT/Sales Tax Feb 2014 Mar 2014 Apr 2014 May 2014 Jun 2014 Jul 2014 Aug 2014

COD R 10 000 R 10 000 R 10 000 R 10 000 R 10 000 R 10 000 R 10 000

7 days Invoice

15 days Invoice

30 days Invoice R 100 000 R 100 000 R 30 000 R 120 000 R 500 000 R 150 000

45 days Invoice R 100 000 R 100 000 R 30 000 R 100 000 R 100 000 R 150 000

60 days Invoice R 100 000 R 100 000 R 30 000 R 100 000 R 100 000 R 150 000

75 days Invoice

90 days Invoice

30 days Statement R 100 000 R 200 000 R 200 000 R 100 000 R 150 000 R 100 000 R 150 000

60 days Statement R 100 000 R 200 000 R 200 000 R 200 000 R 150 000 R 15 000 R 100 000

90 days Statement

120 days Statement

Copyright 2015 Mantramax Pty Ltd -

All rights reserved

120 days Statement

150 days Statement

Total Purchases incl VAT/Sales Tax R 510 000 R 710 000 R 500 000 R 630 000 R 310 000 R 825 000 R 710 000

Total Credit Purchases incl VAT/Sales Tax R 500 000 R 700 000 R 490 000 R 620 000 R 300 000 R 815 000 R 700 000

Payables Age Analysis as at

Monthend

Feb 2014

Monthend

Mar 2014

Monthend

Apr 2014

Monthend

May 2014

Monthend

Jun 2014

Monthend

Jul 2014

Monthend

Aug 2014

1 to 30 days (Current) 500 000 700 000 490 000 620 000 300 000 815 000 700 000

31 to 60 days 0 500 000 700 000 490 000 620 000 300 000 815 000

61 to 90 days 0 0 200 000 280 000 196 000 248 000 120 000

91 to 120 days 0 0 0 100 000 140 000 98 000 124 000

121 to 150 days

151 to 180 days

180+ days

Total Payables Age Analysis R 500 000 R 1 200 000 R 1 390 000 R 1 490 000 R 1 256 000 R 1 461 000 R 1 759 000

16

Accounts Payable Review (Model Output)

Accounts Payable Performance Measurement Feb 2014 Mar 2014 Apr 2014 May 2014 Jun 2014 Jul 2014 Aug 2014

Creditors Days - By Ageing Bucket 30.42 60.83 73.00 79.08 79.08 79.08 79.08

Creditors Days - Average Purchases Method (3 months) 30.00 60.00 74.02 74.09 80.17 75.79 87.22

Days Payables Outstanding (DPO) 28.00 59.00 72.20 77.83 81.57 78.30 86.40

Best Possible Days Payable Outstanding (BPDPO) 28.00 31.00 30.00 31.00 30.00 31.00 31.00

Delinquent Days Payables Outstanding (DDPO) 0.00 28.00 42.20 46.83 51.57 47.30 55.40

Days Payable Outstanding Benchmark (DPOB) 28.00 40.40 50.12 51.20 57.52 47.12 46.55

Copyright 2015 Mantramax Pty Ltd -

All rights reserved

Days Payable Outstanding Benchmark (DPOB) 28.00 40.40 50.12 51.20 57.52 47.12 46.55

Payables Effeciency Index (DPO/DPOB) 100.00% 146.05% 144.07% 152.02% 141.81% 166.17% 185.60%

Payables Effeciency Achievement (DPO to DPOB) 0.00% 31.53% 30.59% 34.22% 29.48% 39.82% 46.12%

Accounts Payables Performance Values

Total Creditors Book Value R 500 000 R 1 200 000 R 1 390 000 R 1 490 000 R 1 256 000 R 1 461 000 R 1 759 000

Payables Effeciency Achievement Value R 0 R 378 374 R 425 159 R 509 840 R 370 327 R 581 757 R 811 265

DPOB Value R 500 000 R 821 626 R 964 841 R 980 160 R 885 673 R 879 243 R 947 735

17

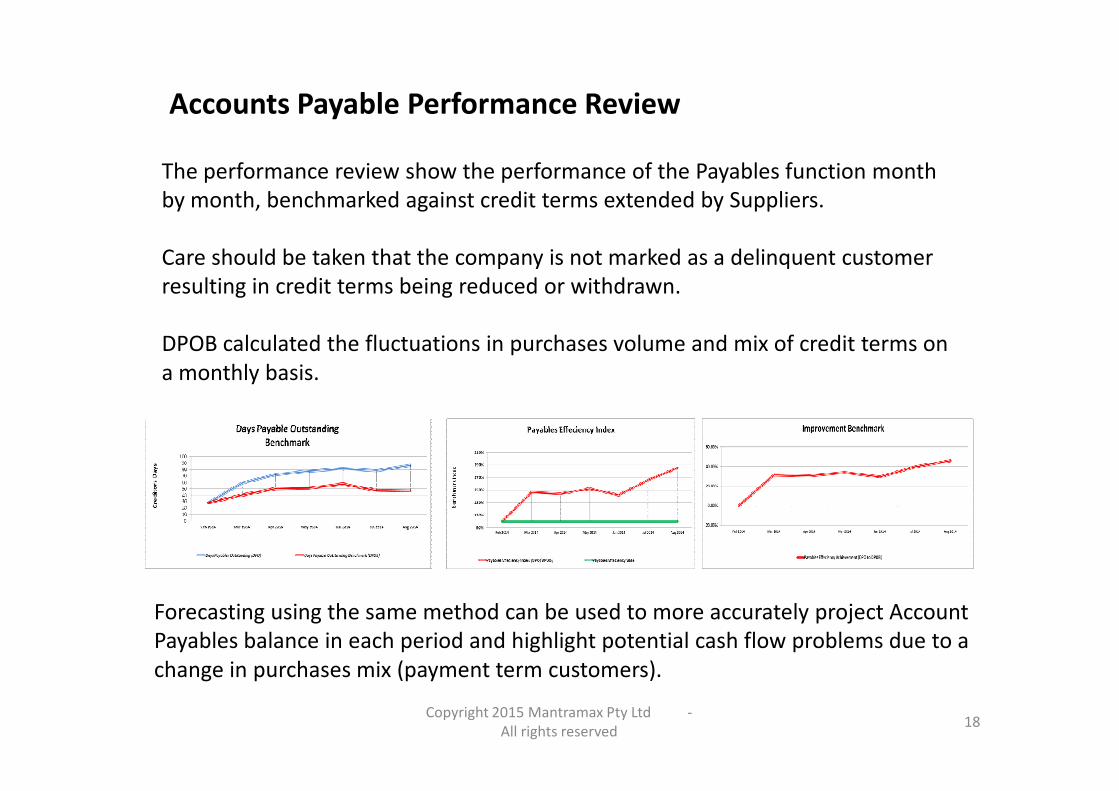

The performance review show the performance of the Payables function month

by month, benchmarked against credit terms extended by Suppliers.

Care should be taken that the company is not marked as a delinquent customer

resulting in credit terms being reduced or withdrawn.

DPOB calculated the fluctuations in purchases volume and mix of credit terms on

a monthly basis.

Accounts Payable Performance Review

Copyright 2015 Mantramax Pty Ltd -

All rights reserved

Forecasting using the same method can be used to more accurately project Account

Payables balance in each period and highlight potential cash flow problems due to a

change in purchases mix (payment term customers).

18

Setting and Evaluating KPI's

From the same dataset, KPI's can be set for Creditors Administrators, Financial

Managers, Divisions and Diverse Groups of Companies (various industries).

KPI Formulation Feb 2014 Mar 2014 Apr 2014 May 2014 Jun 2014 Jul 2014 Aug 2014

Initial Minimum Benchmark Set % over DPOB ** 30.00% 30.00% 30.00% 30.00% 30.00% 30.00% 30.00%

Value in Creditors over Initial Minimum Benchmark

(Cashflow Saving) R 150 000 R 246 488 R 289 452 R 294 048 R 265 702 R 263 773 R 284 321

Cost of Capital (CoC) per Annum 10% 10% 10% 10% 10% 10% 10%

Monthly Financial Benefit of Initial Benchmark R 1 250 R 2 054 R 2 412 R 2 450 R 2 214 R 2 198 R 2 369

Current Optimum Benchmark -30.00% 1.53% 0.59% 4.22% -0.52% 9.82% 16.12%

Incentive Participation % 0.00% 1.53% 0.59% 4.22% 0.00% 9.82% 16.12%

Copyright 2015 Mantramax Pty Ltd -

All rights reserved

** The Initial Benchmark is set at the start of the incentive program and should remain constant for a set period length (until next

review).

If a monetary incentive is favoured, a suggested method used above calculates the Financial Benefit of the achieved DPOB Index.

If the Creditors Value is above the Initial Benchmark, then no benefit will be payable to the participant.

Alternatively, the DPOB Benchmark can be used for annual performance reviews using an average Index over the year.

Total Cashflow Benefiit in Period subject to incentive R 0 R 12 580 R 5 664 R 41 338 R 0 R 86 333 R 152 782

Monthly Financial Return based on CoC R 0 R 105 R 47 R 344 R 0 R 719 R 1 273

Benefit Split 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00%

Company 80.00% 80.00% 80.00% 80.00% 80.00% 80.00% 80.00%

Employee/Manager etc 20.00% 20.00% 20.00% 20.00% 20.00% 20.00% 20.00%

Employee Incentive Value R 0 R 21 R 9 R 69 R 0 R 144 R 255

Company Benefit Value R 0 R 84 R 38 R 276 R 0 R 576 R 1 019

R 0 R 105 R 47 R 344 R 0 R 719 R 1 273

19

Section 3 – Inventory

Analysis tool available to measure Inventory performance :

Inventory consist of :

Raw Materials

Work-in-Progress (WIP)

Measurement Standard Method Preferred Method

Days Sales in Inventory

(DSI) or Inventory Days

Inventory / Historical

Cost of Sales X 365

Inventory / Forecasted 3 month Annualised Cost of Sales

(ie CoS 3 months X 12/3) X 365

Copyright 2015 Mantramax Pty Ltd -

All rights reserved

Work-in-Progress (WIP)

Finished Goods

Benchmarking Inventory performance is difficult due to various influencing factors :

•Supplier Lead Times

•Manufacturing Time

•Product Sales Mix

•Out of Stock (Lost Sales)

Targets should be set by Management based on the forecasted Sales (CoS).

20

Example of Input Format / Inventory Review (Model Output)

Data Input Grey Area Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14

Actual Cost of Sales R 650 000 R 950 000 R 1 550 000 R 1 350 000 R 1 350 000 R 1 350 000 R 1 350 000

Projected Cost of Sales (Forecasting)

Inventory

Raw Material R 162 500 R 162 500 R 237 500 R 387 500 R 337 500 R 337 500 R 337 500

Work-in-Progress R 97 500 R 97 500 R 142 500 R 232 500 R 202 500 R 202 500 R 202 500

Finished Goods R 650 000 R 650 000 R 950 000 R 1 550 000 R 1 350 000 R 1 350 000 R 1 350 000

Other

Total Inventory R 910 000 R 910 000 R 1 330 000 R 2 170 000 R 1 890 000 R 1 890 000 R 1 890 000

Inventory Performance Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14

Days Sales of Inventory (DSI) - Historical 3

Copyright 2015 Mantramax Pty Ltd -

All rights reserved

Days Sales of Inventory (DSI) - Historical 3

months Sales 42.00 34.13 37.58 51.85 40.47 42.93 42.93

Days Forecasted Sales of Inventory (DFSI)

- Next 3 months sales 21.75 19.48 30.21 49.29 42.93 42.93 42.47

Days Forecasted Sales of Inventory

Benchmark (DFSIB) 30.00 30.00 30.00 30.00 30.00 30.00 30.00

Inventory Efficiency Index (DFSI/DSIB) 72.48% 64.95% 100.71% 164.31% 143.11% 143.11% 141.56%

Inventory Efficiency Achievement (DFSI to

DSIB) -Below/Above 0.00% 53.97% 0.70% 39.14% 30.12% 30.12% 29.36%

Inventory Performance Values

Total Inventory Value R 910 000 R 910 000 R 1 330 000 R 2 170 000 R 1 890 000 R 1 890 000 R 1 890 000

Inventory Efficiency Achievement Value -R 345 435 -R 491 099 R 9 348 R 849 348 R 569 348 R 569 348 R 554 835

DFSIB Value R 1 255 435 R 1 401 099 R 1 320 652 R 1 320 652 R 1 320 652 R 1 320 652 R 1 335 165

21

Cash Conversion Cycle (CCC)

The Cash Conversion Cycle measures the amount of time it takes a company to convert a

resource into cash.

Using the Benchmarks for Accounts Receivable, Accounts Payable and Inventory, an

index can of the best possible CCC available based on credit terms extended to

Customers and by Suppliers.

From the output models in :

Section 1 (Accounts Receivable),

Section 2 (Accounts Payable) and

Copyright 2015 Mantramax Pty Ltd -

All rights reserved

Section 2 (Accounts Payable) and

Section 3 (Inventory)

it is possible to calculate the Cash Conversion Cycle and Benchmark the result against

the best possible scenario.

Measurement Standard Method Benchmark

Cash Conversion

Cycle (CCC)

Days Sales Outstanding (DSO) +

Days Sales in Inventory (DSI) -

Days Payables Outstanding (DPO)

Days Sales Outstanding Benchmark (DSOB) +

Days Sales in Inventory Benchmark (DSIB) -

Days Payables Outstanding Benchmark

(DPOB)

22

Cash Conversion Cycle Review (Model Output)

Data from AR, AP and Inventory Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14

Days Sales Outstanding (DSO) 28.00 59.00 72.20 77.53 78.40 85.20 88.65

Days Payables Outstanding (DPO) 28.00 59.00 72.20 77.83 81.57 78.30 86.40

Days Forecasted Sales of Inventory (DFSI) - Next 3

months sales 21.75 19.48 30.21 49.29 42.93 42.93 42.47

Days Sales Outstanding Benchmark (DSOB) 28.00 40.47 46.78 56.85 62.46 67.29 74.69

Days Payable Outstanding Benchmark (DPOB) 28.00 40.40 50.12 51.20 57.52 47.12 46.55

Days Forecasted Sales of Inventory Benchmark (DFSIB) 30.00 30.00 30.00 30.00 30.00 30.00 30.00

Total Debtors Book Value R 1 200 000 R 3 000 000 R 5 280 000 R 6 560 000 R 6 940 000 R 7 230 000 R 7 510 000

Total Creditors Book Value R 500 000 R 1 200 000 R 1 390 000 R 1 490 000 R 1 256 000 R 1 461 000 R 1 759 000

Total Inventory Value R 910 000 R 910 000 R 1 330 000 R 2 170 000 R 1 890 000 R 1 890 000 R 1 890 000

Debtors Delinquency Index Target Value R 0 R 942 352 R 1 858 902 R 1 749 789 R 1 411 320 R 1 520 397 R 1 182 772

Payables Efficiency Achievement Value R 0 R 378 374 R 425 159 R 509 840 R 370 327 R 581 757 R 811 265

Inventory Efficiency Achievement Value -R 345 435 -R 491 099 R 9 348 R 849 348 R 569 348 R 569 348 R 554 835

Copyright 2015 Mantramax Pty Ltd -

All rights reserved

Inventory Efficiency Achievement Value -R 345 435 -R 491 099 R 9 348 R 849 348 R 569 348 R 569 348 R 554 835

DSOB Value R 1 200 000 R 2 057 648 R 3 421 098 R 4 810 211 R 5 528 680 R 5 709 603 R 6 327 228

DPOB Value R 500 000 R 821 626 R 964 841 R 980 160 R 885 673 R 879 243 R 947 735

DFSIB Value R 1 255 435 R 1 401 099 R 1 320 652 R 1 320 652 R 1 320 652 R 1 320 652 R 1 335 165

Working Capital Performance

Measurement Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14

Cash Conversion Cycle (CCC) days 21.75 19.48 30.21 49.00 39.76 49.84 44.72

Cash Conversion Cycle Benchmark (CCCB) 30.00 30.07 26.66 35.65 34.94 50.16 58.14

Cash Conversion Cycle Index (CCC/CCCB) 72.48% 64.80% 113.30% 137.43% 113.81% 99.35% 76.92%

Cash Conversion Cycle (CCC) value 1 610 000 2 710 000 5 220 000 7 240 000 7 574 000 7 659 000 7 641 000

Cash Conversion Cycle Benchmark (CCCB) value 1 955 435 2 637 121 3 776 909 5 150 703 5 963 658 6 151 011 6 714 658

Value Locked up in Working Capital Efficiencies -345 435 72 879 1 443 091 2 089 297 1 610 342 1 507 989 926 342

23

Section 4 – Users of the System

User Process Benchmarks used

AuditorsYear-end review of Accounts Receivables

Delinquency Index (DSO/DSOB)

Debtors Delinquency Index Target Value

Year-end review of Accounts Payable Payables Efficiency Index (DPO/DPOB)

Due Diligence Investigations /

M&A

Review of risk in Accounts Receivable Delinquency Index (DSO/DSOB)

Review of risk in Accounts Payables Payables Efficiency Index (DPO/DPOB)

Review of trend in Forecasted Cash

Conversion Cycle Cash Conversion Cycle (CCC) days

Calculation of increased cash flow prior to

Acquisition All Efficiency Indexes

Benchmarking the risk portion of Factoring

Accounts Receivable

Days Sales Outstanding (DSO)

Delinquency Improvement Target (DSO to

DSOB)

Days Sales Outstanding Benchmark (DSOB)

Copyright 2015 Mantramax Pty Ltd -

All rights reserved

Risk FinanceAccounts Receivable Days Sales Outstanding Benchmark (DSOB)

Extentions taken in Accounts Payables Payables Efficiency Index (DPO/DPOB)

Business Management /KPI's

Review of Accounting Functions for inclusion

in Monthly Management Report

Delinquency Index (DSO/DSOB)

Payables Efficiency Index (DPO/DPOB)

Inventory Efficiency Index (DFSI/DSIB)

Cash Conversion Cycle Index (CCC/CCCB)

Monthly Benchmarking Accounting Functions

and Review of KPI's

Delinquency Improvement Target (DSO to

DSOB)

Payables Efficiency Achievement (DPO to

DPOB)

Inventory Efficiency Achievement (DFSI to

DSIB) -Below/Above

Forecasting tool for calculation of Working

Capital values in Balance Sheet

Days Sales Outstanding Benchmark (DSOB)

Days Payable Outstanding Benchmark (DPOB)

Days Forecasted Sales of Inventory Benchmark

(DFSIB)

Effect of growth/decline of Sales and

Purchases mix on Cash flow

Days Sales Outstanding Benchmark (DSOB)

Days Payable Outstanding Benchmark (DPOB)

24

Auditors

The risk of delinquency is always a major cause of concern at year-end. The DSOB

provide a benchmark, calculated at source (invoices), of this delinquency risk.

Substantive audit tests should quantify this risk as well but will also increase the

audit fee significantly.

An example using the Doubtful Debt Provision and Provision for Credit Notes can

be illustrated as follows (year-end Aug 2014) :

Balance Sheet Jun-14 Jul-14 Aug-14

Accounts Receivable Balance R 6 940 000 R 7 230 000 R 7 510 000

Copyright 2015 Mantramax Pty Ltd -

All rights reserved

Accounts Receivable Balance R 6 940 000 R 7 230 000 R 7 510 000

Less :

Provision for Doubtful Debts (10% of AR as example) -R 694 000 -R 723 000 -R 751 000

Provision for Credit Notes (5% of Turnover as example) -R 130 000 -R 130 000 -R 130 000

Nett Accounts Receivable Balance R 6 116 000 R 6 377 000 R 6 629 000

Original DSO on Accounts Receivable 78.40 85.20 88.65

Recalculated DSO on Nett Accounts Receivable 69.09 75.15 78.25

Days Sales Outstanding Benchmark (DSOB) 62.46 67.29 74.69

Risk not Provided for in Accounts Receivable (days) 6.63 7.87 3.56

DSOB Value R 5 528 680 R 5 709 603 R 6 327 228

Risk not Provided for in Accounts Receivable (value) R 587 320 R 667 397 R 301 772

25

Due Diligence / M&A

The Working Capital Trend in the period preceding a merger is as important as the

actual valuation done during the Due Diligence.

Early collection of Accounts Receivable and extension of supplier payments in

Accounts Payable in the period just before the effective date of the acquisition, will

place the buyer in a cash negative position and may require additional Working

Capital funding. Use of the AR Delinquency Index and Payables Efficiency Index

trends will indicate the above scenario.

Benchmark Review May-14 Jun-14 Jul-14 Aug-14

Copyright 2015 Mantramax Pty Ltd -

All rights reserved

Benchmark Review May-14 Jun-14 Jul-14 Aug-14

Delinquency Index (DSO/DSOB) 136.38% 125.53% 95.00% 80.00%

Payables Efficiency Index (DPO/DPOB) 152.02% 141.81% 180.00% 250.00%

Debtors Delinquency Index Target Value R 1 749 789 R 1 411 320 R 1 140 639 R 797 195

Payables Efficiency Achievement Value R 509 840 R 370 327 R 630 192 R 1 092 757

Index movement (AR-AP) R 1 239 949 R 1 040 994 R 510 448 R -295 563

Cash flow Implication for Purchaser compared to 4 months ago R -1 535 512

26

Risk Finance

Debtors Factoring is often used by companies to fund current of future cash

flow requirements. The providers of these funds use scoring systems to

evaluate the risk of the ceded or factored Debtors Book.

Benchmarking against Industry Standards is the most common used method.

Although this provide a broad industry benchmark, the monthly fluctuations in

revenue as well as the customer mix in respect of credit terms within a

company can obscure this comparison.

Copyright 2015 Mantramax Pty Ltd -

All rights reserved

company can obscure this comparison.

The Delinquency Index provide an accurate risk index of the Debtors Book on a

monthly basis using each customer’s individual credit term calculated from

invoiced turnover.

The Delinquency Index Target Value also give a monetary value of risk of the

Debtors Book provided as security for the funding.

27

Risk Finance (2)

An illustration of the monthly comparison between DSO, Industry Standard

and DSOB :

Risk Scoring May-14 Jun-14 Jul-14 Aug-14

Days Sales Outstanding (DSO) 77.53 78.40 85.20 88.65

Industry Benchmark (60 days or 30 Days statement) 60.00 60.00 60.00 60.00

Days Sales Outstanding Benchmark (DSOB) 56.85 62.46 67.29 74.69

Copyright 2015 Mantramax Pty Ltd -

All rights reserved

Index DSO to Industry Standard 129.22% 130.67% 142.01% 147.76%

Index DSOB to Industry Standard 94.75% 104.09% 112.14% 124.49%

Total Debtors Book Value R 6 560 000 R 6 940 000 R 7 230 000 R 7 510 000

Risk value DSO to Industry Standard R 1 483 474 R 1 628 776 R 2 138 681 R 2 427 310

Debtors Delinquency Index Target Value R 1 749 789 R 1 411 320 R 1 520 397 R 1 182 772

Difference in Risk Value between methods -R 266 315 R 217 455 R 618 283 R 1 244 538

28

Business Management / KPI’s

The major benefit from using the benchmarks is for management of

companies and the formulation of employee incentives. The metric is against

the performance of the company as an operating entity and its internal credit

policies and that of its suppliers.

Monthly Performance Indicators available for use by Management :

Management Reviews Benchmark

Key Performance Indicator

(KPI) Performance Group

Accounts Receivable

Copyright 2015 Mantramax Pty Ltd -

All rights reserved

Days Sales Outstanding (DSO)

Days Sales Outstanding

Benchmark (DSOB)

Debtors Delinquency Index

Target Value Credit Controller

Credit

Manager Company

Division/

Group

Accounts Payable

Days Payables Outstanding

(DPO)

Days Payable Outstanding

Benchmark (DPOB)

Payables Efficiency

Achievement Value

Creditors

Admini

Financial

Manager Company

Division/

Group

Inventory

Days Forecasted Sales of

Inventory (DFSI) - Next 3

months sales

Days Forecasted Sales of

Inventory Benchmark

(DFSIB)

Inventory Efficiency

Achievement Value Buyer

Operations/

Financial

Manager Company

Division/

Group

Working Capital

Cash Conversion Cycle (CCC)

days

Cash Conversion Cycle

Benchmark (CCCB)

Value Locked up in Working

Capital Efficiencies Company

Division/

Group

29

Business Management (2)

Using the DSOB and DPOB as guidelines, an accurate value for Accounts

Receivable and Accounts Payable can be forecasted.

This will highlight potential cash flow problems in the future year.

An example of the calculated Forecast Accounts Receivable value :

Sep 2014 Oct 2014 Nov 2014 Dec Onward

Credit Turnover incl VAT/Sales Tax by

Payment Term R 100 000 R 400 000 R 300 000

Copyright 2015 Mantramax Pty Ltd -

All rights reserved

Payment Term R 100 000 R 400 000 R 300 000

DSOB Value calculated based on above 80.00 90.00 85.00

Average Prior 3 Month Delinquency Index

(suggested) at start of budget process 123.62% 123.62% 123.62%

Accounts Receivable Forecast Value R 329 644 R 1 435 546 R 1 050 740

The Delinquency Index can be reduced or increased in future months based on

management’s estimate of effectiveness of the Credit Control department.

The same method can be used to calculate Accounts Payable.

30

Information Required

All information required for the calculation of the benchmarks in this publication

should be readily available from any accounting system.

Report/Information required Alternative Report

Accounts Receivable

Turnover incl VAT by Payment Term AR Module Invoice register + AR Master Payment Term

Debtors Age Analysis or Ageing Report AR Module Standard Report

No Customer Names required

Copyright 2015 Mantramax Pty Ltd -

All rights reserved

No Customer Names required

Accounts Payable

Purchases incl VAT by Payment Term AP Module Invoice register + AP Master Payment Term

Accounts Payable Age Analysis AP Module Standard Report

No Supplier Names required

Inventory

Inventory Valuation IC Module Standard Report

31

Contact information for Initial Reviews and Monthly

Reports :

Wessel Roux

Cape Town, South Africa

Copyright 2015 Mantramax Pty Ltd -

All rights reserved

Cape Town, South Africa

Cell +27 (0) 82 852 9924

Fax +27 (0) 86 689 1093

Email [email protected]

32