WOODSTOCK INSTITUTE | JUNE 2014 Webinar June 18, 2014 Make your voice heard: Commenting on CFPB...

14

WOODSTOCK INSTITUTE | JUNE 2014 Webinar June 18, 2014 Make your voice heard: Commenting on CFPB policies Courtney Eccles | Policy Director Katie Buitrago | Senior Policy and Communications Associate Woodstock Institute | Chicago, Illinois P 312.368.0310 | F 312.368.0316 [email protected] | [email protected] @woodstockin st WoodstockInstitu te

-

Upload

barbara-simmons -

Category

Documents

-

view

213 -

download

0

Transcript of WOODSTOCK INSTITUTE | JUNE 2014 Webinar June 18, 2014 Make your voice heard: Commenting on CFPB...

WOODSTOCK INSTITUTE | JUNE 2014

Webinar

June 18, 2014

Make your voice heard:Commenting on CFPB policies

Courtney Eccles | Policy DirectorKatie Buitrago | Senior Policy and Communications AssociateWoodstock Institute | Chicago, IllinoisP 312.368.0310 | F [email protected] | [email protected]

@woodstockinst

WoodstockInstitute

WOODSTOCK INSTITUTE | JUNE 2014

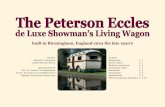

What is the Consumer Financial Protection Bureau?

• Created by the Dodd-Frank Act in 2010• Opened its doors in July 2011• Mission:

Make markets for consumer financial products and services work for

Americans — whether they are applying for a mortgage, choosing among credit cards, or using any number of other consumer financial products.

WOODSTOCK INSTITUTE | JUNE 2014

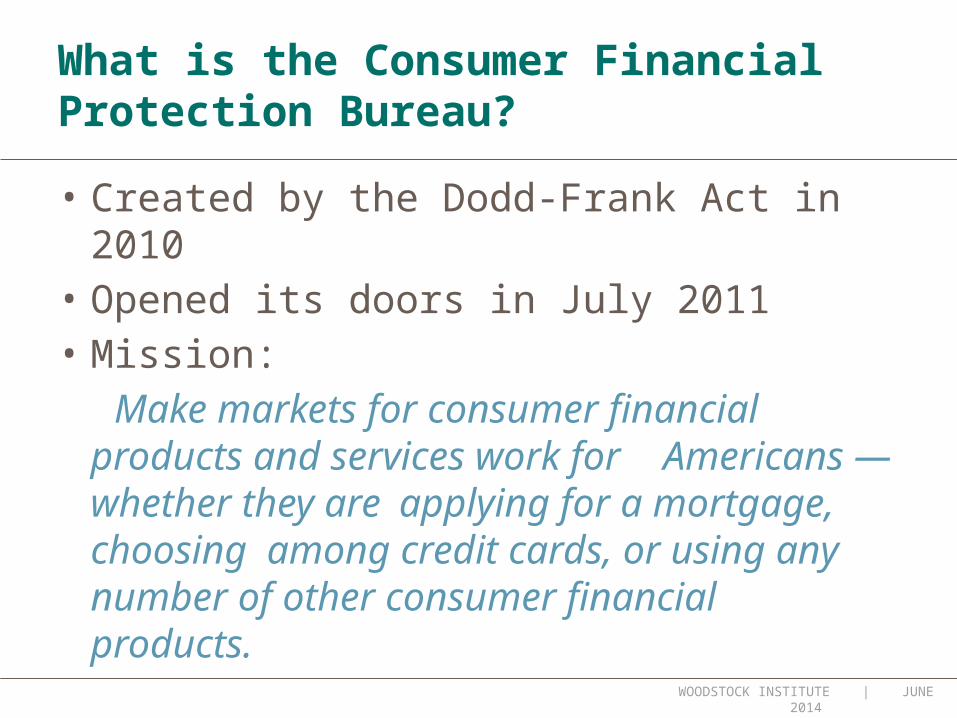

What can the CFPB do?

• Write rules, supervise companies, and enforce federal consumer financial protection laws

• Restrict unfair, deceptive, or abusive acts or practices

• Take consumer complaints• Promote financial education• Research consumer behavior• Monitor financial markets for new risks to

consumers• Enforce laws that outlaw discrimination and other

unfair treatment in consumer financeSource: consumerfinance.gov

WOODSTOCK INSTITUTE | JUNE 2014

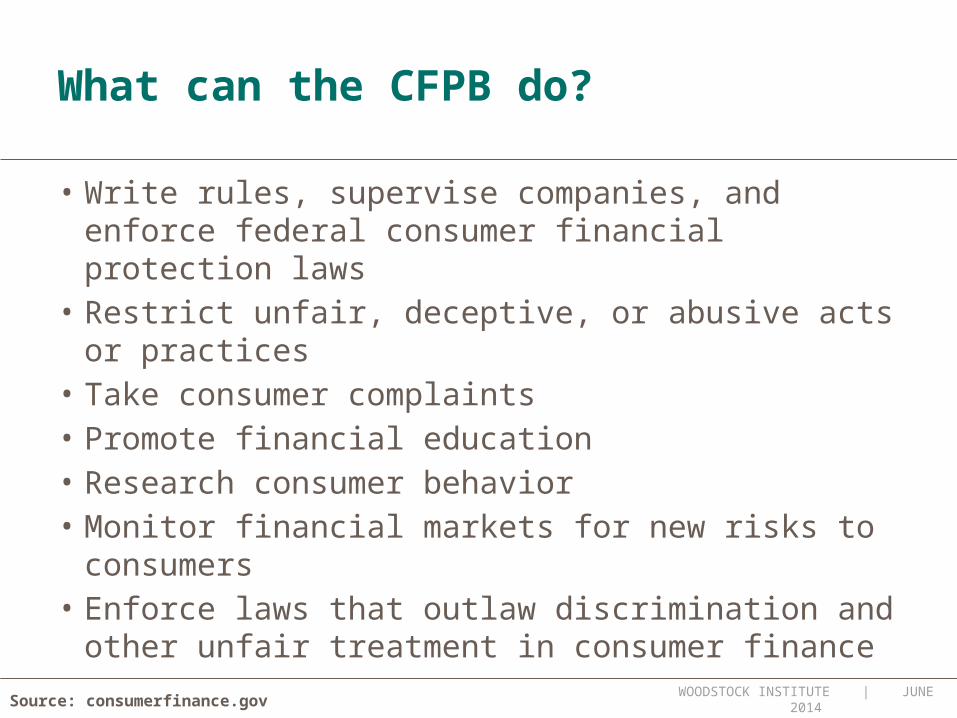

What can the CFPB do?

• Write rules, supervise companies, and enforce federal consumer financial protection laws

• Restrict unfair, deceptive, or abusive acts or practices

• Take consumer complaints• Promote financial education• Research consumer behavior• Monitor financial markets for new risks to

consumers• Enforce laws that outlaw discrimination and other

unfair treatment in consumer financeSource: consumerfinance.gov

WOODSTOCK INSTITUTE | JUNE 2014

How the CFPB makes policy

• Writes rules and regulations regarding implementation of consumer protection laws

• Puts them out for comment in Federal Register

• Usually open for 30-90 days• http://www.consumerfinance.gov/notice-an

d-comment/

WOODSTOCK INSTITUTE | JUNE 2014

Writing comment letters

• Respond to CFPB’s questions• Rely on the strengths of your organization’s

perspective– Data analysis? Policy/legal expertise? Client stories?

• Other options– Use template from Woodstock or another group—

personalize it!– Sign on to another letter

• Let Woodstock know when you comment/file complaints!

WOODSTOCK INSTITUTE | JUNE 2014

Issue: Prepaid cards

• What are prepaid cards?– Network-branded cards that allow users to

load a specified amount of money on them– Often used by underbanked people as an

alternative to a checking account– The industry is largely unregulated broad

variety of cards on the market

WOODSTOCK INSTITUTE | JUNE 2014

Issue: Prepaid cards

• Consumer protection issues– Require clear and comprehensive disclosures

of terms and conditions– Require fees to be reasonable– Prohibit credit on prepaid cards

• When is the proposed rule coming out?– June 2014

WOODSTOCK INSTITUTE | JUNE 2014

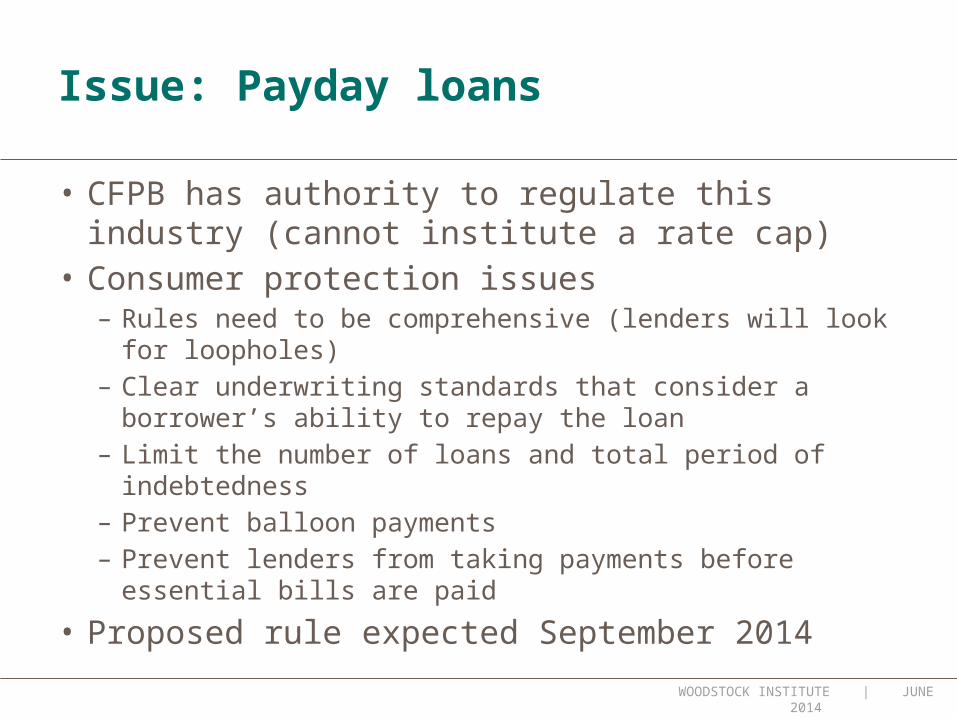

Issue: Payday loans

• What are payday loans?– Traditional payday loans are short-term (2-4

week) loans with balloon payments and high interest rates (in IL, up to 400% APR)

– Regulations vary by state, IL reforms created multiple loan products:

• Traditional Payday Loan• Payday Installment Loan• Small Consumer Loan

Issue: Payday loans

• CFPB has authority to regulate this industry (cannot institute a rate cap)

• Consumer protection issues– Rules need to be comprehensive (lenders will look for

loopholes)– Clear underwriting standards that consider a borrower’s

ability to repay the loan– Limit the number of loans and total period of indebtedness– Prevent balloon payments– Prevent lenders from taking payments before essential bills

are paid

• Proposed rule expected September 2014WOODSTOCK INSTITUTE | JUNE 2014

WOODSTOCK INSTITUTE | JUNE 2014

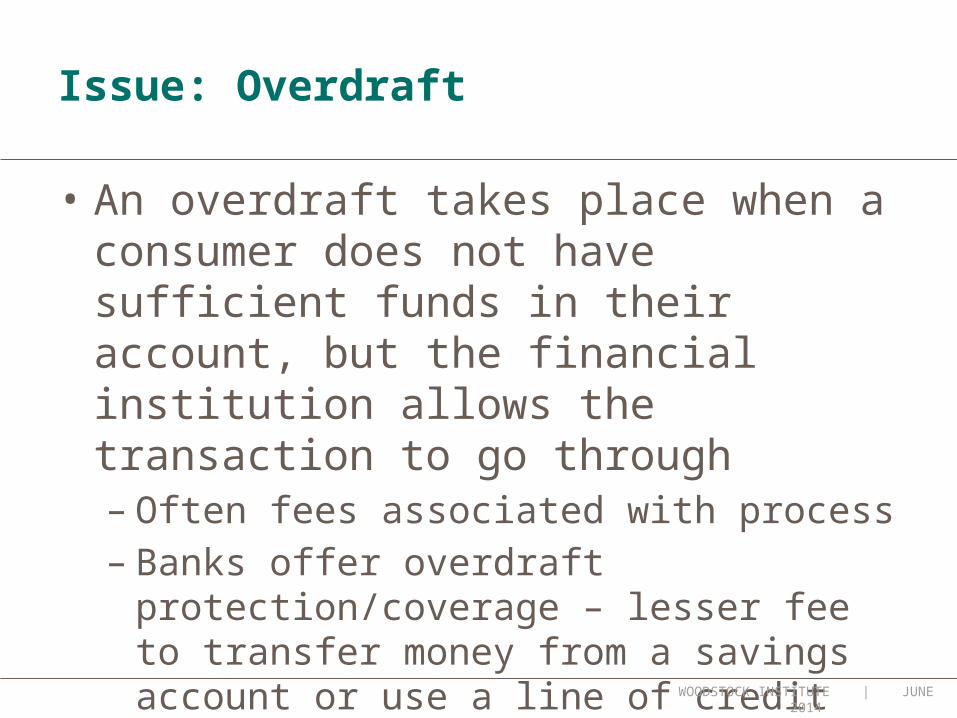

Issue: Overdraft

• An overdraft takes place when a consumer does not have sufficient funds in their account, but the financial institution allows the transaction to go through– Often fees associated with process – Banks offer overdraft protection/coverage –

lesser fee to transfer money from a savings account or use a line of credit

Issue: Overdraft

• Federal law requires customers to “opt-in” for overdraft with ATM and debit transactions

• Process for checks and auto-bill pay differs by institution

• Despite changes to opt-in vs. opt-out, financial institutions generate substantial revenue from overdraft and NSF fees

WOODSTOCK INSTITUTE | JUNE 2014

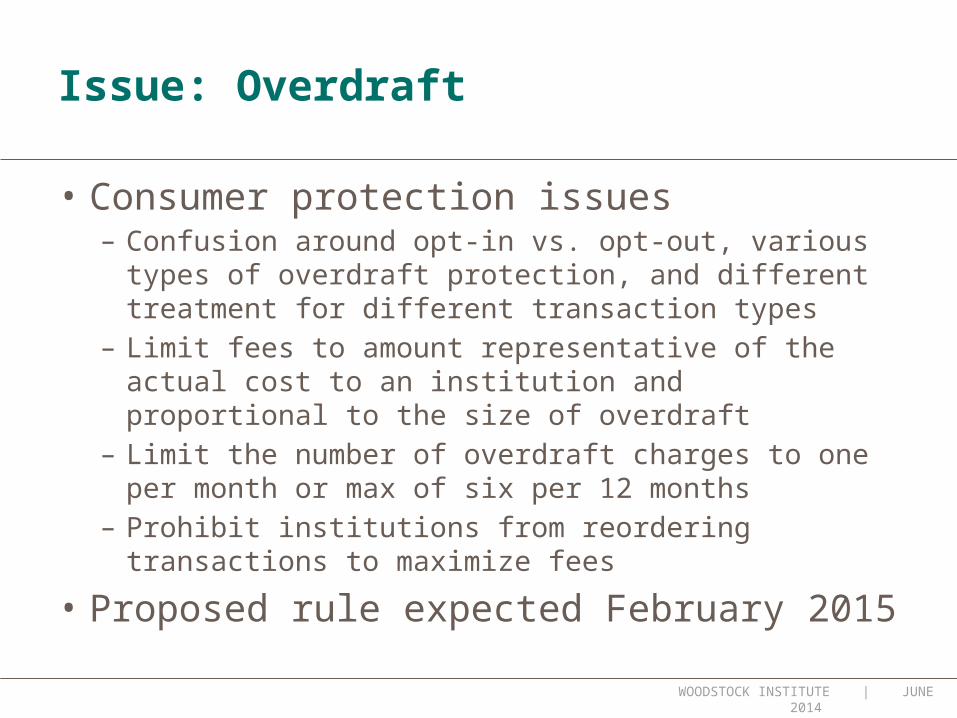

Issue: Overdraft

• Consumer protection issues– Confusion around opt-in vs. opt-out, various types of

overdraft protection, and different treatment for different transaction types

– Limit fees to amount representative of the actual cost to an institution and proportional to the size of overdraft

– Limit the number of overdraft charges to one per month or max of six per 12 months

– Prohibit institutions from reordering transactions to maximize fees

• Proposed rule expected February 2015

WOODSTOCK INSTITUTE | JUNE 2014

WOODSTOCK INSTITUTE | JUNE 2014

Webinar

June 18, 2014

Make your voice heard:Commenting on CFPB policies

Courtney Eccles | Policy DirectorKatie Buitrago | Senior Policy and Communications AssociateWoodstock Institute | Chicago, IllinoisP 312.368.0310 | F [email protected] | [email protected]

@woodstockinst

WoodstockInstitute