WMB Write-Up 11-6-10

32

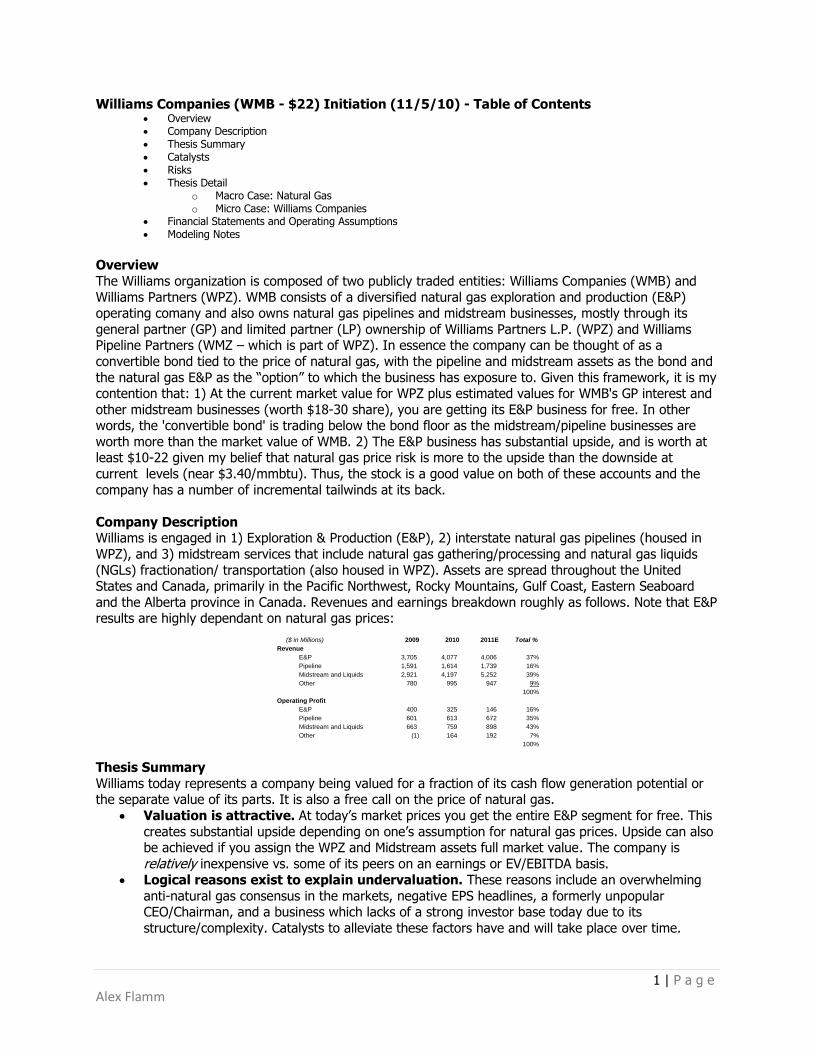

1 | Page Alex Flamm Williams Companies (WMB - $22) Initiation (11/5/10) - Table of Contents Overview Company Description Thesis Summary Catalysts Risks Thesis Detail o Macro Case: Natural Gas o Micro Case: Williams Companies Financial Statements and Operating Assumptions Modeling Notes Overview The Williams organization is composed of two publicly traded entities: Williams Companies (WMB) and Williams Partners (WPZ). WMB consists of a diversified natural gas exploration and production (E&P) operating comany and also owns natural gas pipelines and midstream businesses, mostly through its general partner (GP) and limited partner (LP) ownership of Williams Partners L.P. (WPZ) and Williams Pipeline Partners (WMZ – which is part of WPZ). In essence the company can be thought of as a convertible bond tied to the price of natural gas, with the pipeline and midstream assets as the bond and the natural gas E&P as the “option” to which the business has exposure to. Given this framework, it is my contention that: 1) At the current market value for WPZ plus estimated values for WMB's GP interest and other midstream businesses (worth $18-30 share), you are getting its E&P business for free. In other words, the 'convertible bond' is trading below the bond floor as the midstream/pipeline businesses are worth more than the market value of WMB. 2) The E&P business has substantial upside, and is worth at least $10-22 given my belief that natural gas price risk is more to the upside than the downside at current levels (near $3.40/mmbtu). Thus, the stock is a good value on both of these accounts and the company has a number of incremental tailwinds at its back. Company Description Williams is engaged in 1) Exploration & Production (E&P), 2) interstate natural gas pipelines (housed in WPZ), and 3) midstream services that include natural gas gathering/processing and natural gas liquids (NGLs) fractionation/ transportation (also housed in WPZ). Assets are spread throughout the United States and Canada, primarily in the Pacific Northwest, Rocky Mountains, Gulf Coast, Eastern Seaboard and the Alberta province in Canada. Revenues and earnings breakdown roughly as follows. Note that E&P results are highly dependant on natural gas prices: Thesis Summary Williams today represents a company being valued for a fraction of its cash flow generation potential or the separate value of its parts. It is also a free call on the price of natural gas. Valuation is attractive. At today‟s market prices you get the entire E&P segment for free. This creates substantial upside depending on one‟s assumption for natural gas prices. Upside can also be achieved if you assign the WPZ and Midstream assets full market value. The company is relatively inexpensive vs. some of its peers on an earnings or EV/EBITDA basis. Logical reasons exist to explain undervaluation. These reasons include an overwhelming anti-natural gas consensus in the markets, negative EPS headlines, a formerly unpopular CEO/Chairman, and a business which lacks of a strong investor base today due to its structure/complexity. Catalysts to alleviate these factors have and will take place over time. ($ in Millions) 2009 2010 2011E Total % Revenue E&P 3,705 4,077 4,006 37% Pipeline 1,591 1,614 1,739 16% Midstream and Liquids 2,921 4,197 5,252 39% Other 780 995 947 9% 100% Operating Profit E&P 400 325 146 16% Pipeline 601 613 672 35% Midstream and Liquids 663 759 898 43% Other (1) 164 192 7% 100%

Transcript of WMB Write-Up 11-6-10

1 | P a g e Alex Flamm

Williams Companies (WMB - $22) Initiation (11/5/10) - Table of Contents Overview Company Description Thesis Summary Catalysts Risks Thesis Detail

o Macro Case: Natural Gas o Micro Case: Williams Companies

Financial Statements and Operating Assumptions Modeling Notes

Overview

The Williams organization is composed of two publicly traded entities: Williams Companies (WMB) and

Williams Partners (WPZ). WMB consists of a diversified natural gas exploration and production (E&P) operating comany and also owns natural gas pipelines and midstream businesses, mostly through its

general partner (GP) and limited partner (LP) ownership of Williams Partners L.P. (WPZ) and Williams Pipeline Partners (WMZ – which is part of WPZ). In essence the company can be thought of as a

convertible bond tied to the price of natural gas, with the pipeline and midstream assets as the bond and

the natural gas E&P as the “option” to which the business has exposure to. Given this framework, it is my contention that: 1) At the current market value for WPZ plus estimated values for WMB's GP interest and

other midstream businesses (worth $18-30 share), you are getting its E&P business for free. In other words, the 'convertible bond' is trading below the bond floor as the midstream/pipeline businesses are

worth more than the market value of WMB. 2) The E&P business has substantial upside, and is worth at least $10-22 given my belief that natural gas price risk is more to the upside than the downside at

current levels (near $3.40/mmbtu). Thus, the stock is a good value on both of these accounts and the

company has a number of incremental tailwinds at its back.

Company Description Williams is engaged in 1) Exploration & Production (E&P), 2) interstate natural gas pipelines (housed in

WPZ), and 3) midstream services that include natural gas gathering/processing and natural gas liquids

(NGLs) fractionation/ transportation (also housed in WPZ). Assets are spread throughout the United States and Canada, primarily in the Pacific Northwest, Rocky Mountains, Gulf Coast, Eastern Seaboard

and the Alberta province in Canada. Revenues and earnings breakdown roughly as follows. Note that E&P results are highly dependant on natural gas prices:

Thesis Summary

Williams today represents a company being valued for a fraction of its cash flow generation potential or the separate value of its parts. It is also a free call on the price of natural gas.

Valuation is attractive. At today‟s market prices you get the entire E&P segment for free. This

creates substantial upside depending on one‟s assumption for natural gas prices. Upside can also be achieved if you assign the WPZ and Midstream assets full market value. The company is

relatively inexpensive vs. some of its peers on an earnings or EV/EBITDA basis.

Logical reasons exist to explain undervaluation. These reasons include an overwhelming

anti-natural gas consensus in the markets, negative EPS headlines, a formerly unpopular CEO/Chairman, and a business which lacks of a strong investor base today due to its

structure/complexity. Catalysts to alleviate these factors have and will take place over time.

($ in Millions) 2009 2010 2011E Total %

Revenue

E&P 3,705 4,077 4,006 37%

Pipeline 1,591 1,614 1,739 16%

Midstream and Liquids 2,921 4,197 5,252 39%

Other 780 995 947 9%

100%

Operating Profit

E&P 400 325 146 16%

Pipeline 601 613 672 35%

Midstream and Liquids 663 759 898 43%

Other (1) 164 192 7%

100%

2 | P a g e Alex Flamm

Macro case is compelling: This report provides a comprehensive view that current natural gas

prices under $3.50 are unsustainably low. Prices compared to other energy commodities are at

multi-decade lows. The supply side of gas is constrained and current prices do not justify future investment. Also, demand in the current economic and weather environment is recovering.

Micro case is compelling: Williams' assets are well positioned. The company has a number of

areas where it can excel going forward. The complexity and scope surrounding the company, combined with a weak natural gas environment, has made it easy for the buy side to forget a

number of growth and pricing areas which provide tailwinds to future cash flows.

Catalysts

There are a number of logical catalysts for the company: Higher natural gas prices. Higher natural gas prices are one of the most basic ways to renew

investor interest in the name. My analysis suggest higher prices are coming in 2011 and 2012. Higher NGL prices and margins. This will highlight the value of the midstream assets. Given near-

$90 oil prices, this catalyst is already underway. Asset sale of remaining midstream assets into WPZ. This will continue to lower parent debt and

simplify the business structure. This is partially complete with the $782 mil Piceanse asset drop

down. Other midstream assets like 26% of Gulfstream, will probably undergo similar treatment.

E&P expansion in Marcellus, or into new areas such as Eagle Ford, Bakken and Niobrara.

E&P spin-off. Today the E&P assets are being valued at nothing. A spin off (or partial spin-off)

would give the market a chance to value these assets more fairly. The remaining WMB would a pure holding company - with low debt, little capex and high dividends. In today‟s income craving

investment world, this company would likely find a natural investor base. Management-induced discount continues to close as market gains satisfaction with new CEO and

new Chairman.

Risks

Macro Risks

o Volumes (driven by economic growth). Volume demand supports pricing, production, and

infrastructure needs, while lower demand will drive lower infrastructure construction and earnings growth. On a relative basis, the Pipeline operations are least impacted.

o Natural Gas/NGL Prices. Williams E&P and Midstream segments have direct commodity price exposure. Lower natural gas prices would lower the value of the E&P assets in

excess of the benefit to midstream. While I do not believe the market price of WMB

affords any value to the E&P assets, my estimation of value of the other businesses could be too high. If that is the case, then this risk would become more important. Williams

Gas Pipelines segment has limited direct sensitivity to commodity prices, but sustained lower or higher commodity prices could have a second-order effect on the need for

infrastructure.

o Regulatory. Based on my initial research into the industry, it seems like potential regulatory risks abound. Risks for the sector include diluting or eliminating the tax-

advantaged status of MLPs, increased safety and integrity requirements that raise costs, environmental restrictions which delay or alter construction or result in monetary

penalties, E&P drilling limitations, and adverse decisions by regulators in a rate cases (in the pipeline business). Some of these risks could structurally increase energy prices,

which would have an off-setting positive impact on the business.

Company Specific Risks

o Financial Leverage. Williams‟ Pipeline segment can generally operate at higher leverage metrics due to its more stable cash flows. However, Williams‟ commodity-sensitive

segments (E&P / Midstream) are subject to earning volatility, and leverage is a risk. Luckily, Williams is relatively underleveraged compared to its Peers.

o Execution and Operational Risks. Issues around safety and integrity on existing assets

can increase costs, and reduce volumes and revenues due to unplanned downtime.

3 | P a g e Alex Flamm

Williams Thesis Detail

Valuation is attractive. At today‟s market prices, one can buy WMB‟s entire E&P segment for

free. This implies over 60% upside (varying based on your assumptions, especially natural gas prices). In all but a depressionary crisis, the company looks attractively priced. WMB is also

appears relatively inexpensive as compared to some of its peers.

o Absolute Valuation Based on Sum of the Parts and DCF. As a diversified holding company with high commodity sensitivity, near term consensus GAAP EPS is a weak basis to judge

value. In the midstream and pipeline segment, value can be determined by cash flows (DCF),

which are more stable and easier to predict; asset value; or market value. My projections in this segment use volume and pricing assumptions below management expectations

but in line with the Sell Side. There is upside to these numbers, but the outcome of pipeline expansion projects and rate cases are areas that I do not take a strong view on.

Given that WPZ is freely traded and that an investor in WMB could hedge out this

exposure, market value is the most transparent way to assess this segment.

In the E&P segment, long term commodity prices (determined marginal cost and supply/demand – discussed in depth in the natural gas section) are the key to projecting

earnings and determining value. This is why sensitivity is so crucial.

My base case Sum of the Parts (SOTP) is as follows:

My base case DCF is as follows:

The Williams Companies Sum of the Parts Base Case

WMB

The Williams Companies Value ($m)

Price

Basis

Assumed LT

Nat Gas Price

Risked Pot'l

(Bcfe)

Implied

$/mcfe $/Share

Proved Reserves (PV10) $5,556 4% $5.85 4,255 $1.31 $9.5

Resource Potential

Onshore US

Powder River $244 9% $5.85 1,106 $0.22 $0.4

Piceance $802 9% $5.85 5,636 $0.14 $1.4

San Juan $67 9% $5.85 404 $0.17 $0.1

Mid-Continent (Barnett) $158 9% $5.85 611 $0.26 $0.3

Marcellus $473 9% $5.85 5,543 $0.09 $0.8

Green River / International $363 9% $5.85 1,000 $0.36 $0.6

E&P Hedge Book $586 $1.0

Shares APAGF Px

Discount to Market Price 5.0%

Apco Oil and Gas (69% ownership) $735 20.3 $36 $1.3 $15 E&P

Shares GP c/f GP WPZ

(m) ($ m) Multiple Price

Midstream Discount to Market Price 5.0%

WPZ (LP, ~79.4%) $9,715 222 $44 $16.6

WPZ (GP, Based on 2012) $4,955 $330 15.0x $8.5

Net Debt EBIT Multiple

Canada/Olefins/Other/Gulfstream $1,087 -$350 $192 7.5x $1.9 $27 Pipe and Mid

Value per share $42.3

WMB Net Debt (not including WPZ) $1,071 $1.8

Net Equity Value $40

Shares Outstanding (in m) 585

4 | P a g e Alex Flamm

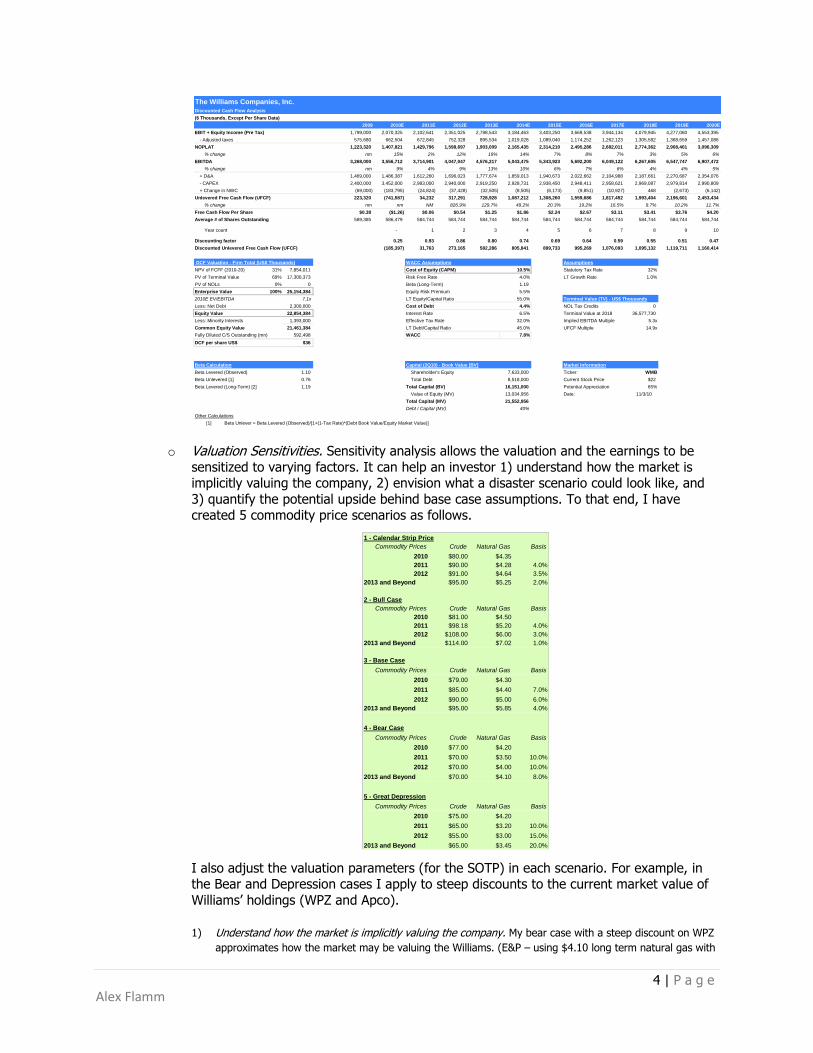

o Valuation Sensitivities. Sensitivity analysis allows the valuation and the earnings to be

sensitized to varying factors. It can help an investor 1) understand how the market is implicitly valuing the company, 2) envision what a disaster scenario could look like, and

3) quantify the potential upside behind base case assumptions. To that end, I have created 5 commodity price scenarios as follows.

I also adjust the valuation parameters (for the SOTP) in each scenario. For example, in the Bear and Depression cases I apply to steep discounts to the current market value of

Williams‟ holdings (WPZ and Apco).

1) Understand how the market is implicitly valuing the company. My bear case with a steep discount on WPZ

approximates how the market may be valuing the Williams. (E&P – using $4.10 long term natural gas with

The Williams Companies, Inc.Discounted Cash Flow Analysis

($ Thousands, Except Per Share Data)

2009 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E

EBIT + Equity Income (Pre Tax) 1,799,000 2,070,325 2,102,641 2,351,025 2,798,543 3,184,463 3,403,250 3,669,538 3,944,134 4,079,945 4,277,060 4,553,395

- Adjusted taxes 575,680 662,504 672,845 752,328 895,534 1,019,028 1,089,040 1,174,252 1,262,123 1,305,582 1,368,659 1,457,086

NOPLAT 1,223,320 1,407,821 1,429,796 1,598,697 1,903,009 2,165,435 2,314,210 2,495,286 2,682,011 2,774,362 2,908,401 3,096,309

% change nm 15% 2% 12% 19% 14% 7% 8% 7% 3% 5% 6%

EBITDA 3,268,000 3,556,712 3,714,901 4,047,047 4,576,217 5,043,475 5,343,923 5,692,200 6,049,122 6,267,605 6,547,747 6,907,472

% change nm 9% 4% 9% 13% 10% 6% 7% 6% 4% 4% 5%

+ D&A 1,469,000 1,486,387 1,612,260 1,696,023 1,777,674 1,859,013 1,940,673 2,022,662 2,104,988 2,187,661 2,270,687 2,354,076

- CAPEX 2,400,000 3,452,000 2,983,000 2,940,000 2,919,250 2,928,731 2,938,450 2,948,411 2,958,621 2,969,087 2,979,814 2,990,809

+ Change in NWC (69,000) (183,795) (24,824) (37,428) (32,505) (8,505) (8,173) (9,851) (10,927) 468 (2,673) (6,142)

Unlevered Free Cash Flow (UFCF) 223,320 (741,587) 34,232 317,291 728,928 1,087,212 1,308,260 1,559,686 1,817,452 1,993,404 2,196,601 2,453,434

% change nm nm NM 826.9% 129.7% 49.2% 20.3% 19.2% 16.5% 9.7% 10.2% 11.7%

Free Cash Flow Per Share $0.38 ($1.26) $0.06 $0.54 $1.25 $1.86 $2.24 $2.67 $3.11 $3.41 $3.76 $4.20

Average # of Shares Outstanding 589,385 586,479 584,744 584,744 584,744 584,744 584,744 584,744 584,744 584,744 584,744 584,744

Year count - 1 2 3 4 5 6 7 8 9 10

Discounting factor 0.25 0.93 0.86 0.80 0.74 0.69 0.64 0.59 0.55 0.51 0.47

Discounted Unlevered Free Cash Flow (UFCF) (185,397) 31,763 273,165 582,286 805,841 899,733 995,269 1,076,093 1,095,132 1,119,711 1,160,414

DCF Valuation - Firm Total (US$ Thousands) WACC Assumptions Assumptions

NPV of FCFF (2010-20) 31% 7,854,011 Cost of Equity (CAPM) 10.5% Statutory Tax Rate 32%

PV of Terminal Value 69% 17,300,373 Risk Free Rate 4.0% LT Growth Rate 1.0%

PV of NOLs 0% 0 Beta (Long-Term) 1.19

Enterprise Value 100% 25,154,384 Equity Risk Premium 5.5%

2010E EV/EBITDA 7.1x LT Equity/Capital Ratio 55.0% Terminal Value (TV) - US$ Thousands

Less: Net Debt 2,300,000 Cost of Debt 4.4% NOL Tax Credits 0

Equity Value 22,854,384 Interest Rate 6.5% Terminal Value at 2018 36,577,730

Less: Minority Interests 1,393,000 Effective Tax Rate 32.0% Implied EBITDA Multiple 5.3x

Common Equity Value 21,461,384 LT Debt/Capital Ratio 45.0% UFCF Multiple 14.9x

Fully Diluted C/S Outstanding (mn) 592,498 WACC 7.8%

DCF per share US$ $36

Beta Calculation Capital (2Q10) - Book Value [BV] Market Information

Beta Levered (Observed) 1.10 Shareholder's Equity 7,633,000 Ticker: WMB

Beta Unlevered [1] 0.76 Total Debt 8,518,000 Current Stock Price $22

Beta Levered (Long-Term) [2] 1.19 Total Capital (BV) 16,151,000 Potential Appreciation 65%

Value of Equity (MV) 13,034,956 Date: 11/3/10

Total Capital (MV) 21,552,956

Debt / Capital (MV) 40%

Other Calculations

[1] Beta Unlever = Beta Levered (Observed)/[1+(1-Tax Rate)*(Debt Book Value/Equity Market Value)]

1 - Calendar Strip Price

Commodity Prices Crude Natural Gas Basis

2010 $80.00 $4.35

2011 $90.00 $4.28 4.0%

2012 $91.00 $4.64 3.5%

2013 and Beyond $95.00 $5.25 2.0%

2 - Bull Case

Commodity Prices Crude Natural Gas Basis

2010 $81.00 $4.50

2011 $98.18 $5.20 4.0%

2012 $108.00 $6.00 3.0%

2013 and Beyond $114.00 $7.02 1.0%

3 - Base Case

Commodity Prices Crude Natural Gas Basis

2010 $79.00 $4.30

2011 $85.00 $4.40 7.0%

2012 $90.00 $5.00 6.0%

2013 and Beyond $95.00 $5.85 4.0%

4 - Bear Case

Commodity Prices Crude Natural Gas Basis

2010 $77.00 $4.20

2011 $70.00 $3.50 10.0%

2012 $70.00 $4.00 10.0%

2013 and Beyond $70.00 $4.10 8.0%

5 - Great Depression

Commodity Prices Crude Natural Gas Basis

2010 $75.00 $4.20

2011 $65.00 $3.20 10.0%

2012 $55.00 $3.00 15.0%

2013 and Beyond $65.00 $3.45 20.0%

5 | P a g e Alex Flamm

elevated basis vs. Henry Hub; Midstream and Pipeline – using a 35% discount to market value). The

market may also be using a higher debt number as debt may grow as the company spends on expansion

projects in upcoming quarters.

2) Envision what the disaster scenario could be. This disaster could take many forms. One possibility is a

liquidity crisis combined with an economic depression where: a) the value of WPZ and Apco slides to half

of current value; and b) the market assumes long term natural gas prices near $3 and the price basis of

over 20% for WMB‟s nat gas production. To top it off, assume higher debt and much lower earnings and

multiples for the WPZ GP and other businesses. This could lead to a market value for WMB of $13-14. This

is consistent with the March 2009 lows, but note that today WMB is less leveraged.

The Williams Companies Sum of the Parts Bear Case

WMB

The Williams Companies Value ($m)

Price

Basis

Assumed LT

Nat Gas Price

Risked Pot'l

(Bcfe)

Implied

$/mcfe $/Share

Proved Reserves (PV10) $3,099 8% $4.10 4,255 $0.73 $5.3

Resource Potential

Onshore US

Powder River $89 13% $4.10 1,106 $0.08 $0.2

Piceance -$186 13% $4.10 5,636 -$0.03 -$0.3

San Juan -$19 13% $4.10 404 -$0.05 $0.0

Mid-Continent (Barnett) $33 13% $4.10 611 $0.05 $0.1

Marcellus -$323 13% $4.10 5,543 -$0.06 -$0.6

Green River / International $121 13% $4.10 1,000 $0.12 $0.2

E&P Hedge Book $950 $1.6

Shares APAGF Px

Discount to Market Price 35.0%

Apco Oil and Gas (69% ownership) $503 20.3 $25 $0.9 $7 E&P

Shares GP c/f GP WPZ

(m) ($ m) Multiple Price

Midstream Discount to Market Price 30.0%

WPZ (LP, ~79.4%) $7,159 222 $32 $12.2

WPZ (GP, Based on 2012) $3,000 $200 15.0x $5.1

Net Debt EBIT Multiple

Canada/Olefins/Other/Gulfstream $350 -$350 $140 5.0x $0.6 $18 Pipe and Mid

Value per share $25.3

WMB Net Debt (not including WPZ) $1,580 $2.7

Net Equity Value $22.6

Shares Outstanding (in m) 585

The Williams Companies Sum of the Parts Disaster Case - Great Depression 2

WMB

The Williams Companies Value ($m)

Price

Basis

Assumed LT

Nat Gas Price

Risked Pot'l

(Bcfe)

Implied

$/mcfe $/Share

Proved Reserves (PV10) $1,723 20% $3.45 4,255 $0.41 $2.9

Resource Potential

Onshore US

Powder River $4 25% $3.45 1,106 $0.00 $0.0

Piceance -$733 25% $3.45 5,636 -$0.13 -$1.3

San Juan -$68 25% $3.45 404 -$0.17 -$0.1

Mid-Continent (Barnett) -$36 25% $3.45 611 -$0.06 -$0.1

Marcellus -$762 25% $3.45 5,543 -$0.14 -$1.3

Green River / International -$14 25% $3.45 1,000 -$0.01 $0.0

E&P Hedge Book $1,206 $2.1

Shares APAGF Px

Discount to Market Price 50.0%

Apco Oil and Gas (69% ownership) $387 20.3 $19 $0.7 $3 E&P

Shares GP c/f GP WPZ

(m) ($ m) Multiple Price

Midstream Discount to Market Price 40.0%

WPZ (LP, ~79.4%) $6,136 222 $28 $10.5

WPZ (GP, Based on 2012) $1,440 $180 8.0x $2.5

Net Debt EBIT Multiple

Canada/Olefins/Other/Gulfstream $100 -$350 $100 4.5x $0.2 $13 Pipe and Mid

Value per share $16.0

WMB Net Debt (not including WPZ) $1,574 $2.7

Net Equity Value $13.4

Shares Outstanding (in m) 585

6 | P a g e Alex Flamm

3) Quantify the potential upside. In my base case the stock is already worth 65-80% above current prices.

However, my base case assumes sub $5 natural gas prices for the next two years and long term prices

below $6, with a continuing basis penalty for WMB‟s realized prices. Many scenarios can be envisioned in

which long term natural gas prices are substantially higher. From December 2002 through January 2009,

natural gas averaged over $7/mmBTU, with an average of $8 for much of that period. Moreover, there is

evidence (described on pages 17-18) of this basis being virtually eliminated. The upside here is seems to

be over $50 per share, or more than 130% above current prices.

o Relative Valuation on Bloomberg Consensus. As a starting point for my valuation analysis,

the company seemed relatively cheap compared its peers. Given that I do not have

dedicated views on most of the peer companies below, to make a more fair comparison, I used Bloomberg consensus assumptions. Moreover, given that I have favorable views

on natural gas, making a relative value “trade” would be challenging, and would require further research and time.

The Williams Companies Sum of the Parts Bull Case

WMB

The Williams Companies Value ($m)

Price

Basis

Assumed LT

Nat Gas Price

Risked Pot'l

(Bcfe)

Implied

$/mcfe $/Share

Proved Reserves (PV10) $7,701 1% $7.25 4,255 $1.81 $13.2

Resource Potential

Onshore US

Powder River $381 5% $7.25 1,106 $0.34 $0.7

Piceance $1,682 5% $7.25 5,636 $0.30 $2.9

San Juan $145 5% $7.25 404 $0.36 $0.2

Mid-Continent (Barnett) $269 5% $7.25 611 $0.44 $0.5

Marcellus $1,180 5% $7.25 5,543 $0.21 $2.0

Green River / International $577 5% $7.25 1,000 $0.58 $1.0

E&P Hedge Book $413 $0.7

Shares APAGF Px

Discount to Market Price 0.0%

Apco Oil and Gas (69% ownership) $773 20.3 $38 $1.3 $22 E&P

Shares GP c/f GP WPZ

(m) ($ m) Multiple Price

Midstream Discount to Market Price 0.0%

WPZ (LP, ~79.4%) $10,227 222 $46 $17.5

WPZ (GP, Based on 2012) $5,760 $360 16.0x $9.9

Net Debt EBIT Multiple

Canada/Olefins/Other/Gulfstream $1,520 -$350 $220 8.5x $2.6 $30 Pipe and Mid

Value per share $52.4

WMB Net Debt (not including WPZ) $1,071 $1.8

Net Equity Value $51

Shares Outstanding (in m) 585

Comparables Analysis Based on Consensus Estimates via Bloomberg

Ticker

Company

Name Price FY1 FY2 FY3 PEG FY1 FY2 FY3

Mkt Cap

($mm)

EV

($mm)

Avg Daily

Volume

($mm)

Net Debt /

Market

Cap

Dividend

Yield

3 Yr Avg

ROE ROA

Operating

Margin

Williams Peer Universe

WMB Williams Cos Inc/The 22.34 18.6x 17.3x 14.7x 1.4x 7.3x 5.9x 5.3x 13,064 19,473 157.0 49.1% 2.2% 12.8% 1.1% 17.9%

C-Corp E&P, MLP Holding Cos

WMB Williams Cos Inc/The 22.34 18.6x 17.3x 14.7x 1.4x 7.3x 5.9x 5.3x 13,064 19,473 157.0 49.1% 2.2% 12.8% 1.1% 17.9%

EP El Paso Corp 13.46 13.4x 12.1x 10.8x 1.1x 7.2x 6.6x 6.2x 9,476 22,709 109.9 139.6% 0.3% -5.0% -2.5% -1.1%

OKE Oneok Inc 51.12 17.0x 16.0x 14.7x 2.2x 8.5x 8.0x 7.6x 5,444 10,899 38.9 100.2% 3.8% 14.7% 2.4% 8.0%

SE Spectra Energy Corp 24.70 16.7x 14.7x 13.5x 1.3x 9.4x 8.4x 8.0x 16,006 25,728 89.6 60.7% 4.0% 15.6% 3.7% 32.2%

EGN Energen Corp 46.34 10.7x 13.1x 12.2x 4.9x 5.3x 5.0x 3,331 3,816 17.6 14.6% 1.1% 18.9% 6.8% 30.2%

OGE Oge Energy Corp 45.74 15.4x 16.4x 13.3x 8.1x 12.1x 11.2x 4,459 6,954 24.9 56.0% 3.2% 13.6% 3.7% 17.2%

XTXI Crosstex Energy Inc 8.89 -48.1x NA NA 7.0x 7.2x NA 417 1,280 4.5 207.0% 3.1% 7.4% 0.7% 1.3%

AHD Atlas Pipeline Holdings Lp 9.65 -47.1x 30.2x 30.6x NA NA 267 1,553 1.8 480.7% 2.1% 0.2% 2.4%

RHI Robert Half International Inc 28.41 65.0x 30.4x 18.6x 23.5x 13.6x 8.7x 4,181 3,817 45.3 -8.7% 1.8% 19.5% 2.8% 2.2%

EEQ Enbridge Energy Management Llc62.69 22.0x 21.6x 21.6x 8.4x 6.6x 5.9x 1,106 6,977 3.0 530.8% 0.0%

EQT Eqt Corp 38.36 25.0x 20.9x 15.5x 0.8x 10.2x 8.6x 7.0x 5,721 7,675 57.9 34.2% 2.3% 16.3% 2.8% 28.1%

PipelinesWPZ Williams Partners Lp 45.73 17.2x 14.8x 14.6x 1.7x 7.5x 6.5x 6.1x 12,804 13,660 19.6 6.7% 6.0% 11.7% 3.8% 21.6%

EPB El Paso Pipeline Partners Lp 34.60 18.0x 15.6x 14.0x 1.2x 12.8x 10.1x 7.9x 5,607 6,947 18.5 23.9% 4.7% 19.4% 10.4% 54.4%

OKS Oneok Partners Lp 81.25 24.3x 21.1x 20.1x 2.1x 14.2x 12.8x 11.7x 8,280 11,884 13.4 43.5% 5.6% 19.3% 5.7% 8.4%

SEP Spectra Energy Partners Lp 35.05 20.6x 19.5x 17.5x 2.3x 18.7x 16.8x 16.3x 2,874 3,279 2.6 14.1% 5.0% 13.1% 8.0% 46.3%

ETP Energy Transfer Partners Lp 51.45 30.3x 19.9x 18.7x 0.7x 10.7x 9.2x 8.6x 10,223 16,366 38.3 60.1% 6.9% 24.3% 7.1% 20.8%

Pure E&PDVN Devon Energy Corp 70.78 11.5x 12.2x 8.7x 0.8x 6.1x 6.2x 4.9x 30,789 37,422 293.4 21.5% 0.9% -2.7% -8.0% 28.1%

SD Sandridge Energy Inc 5.16 28.4x 37.1x 12.8x 0.8x 7.3x 6.1x 4.8x 2,090 4,661 55.4 123.0% 0.0% -55.5% 35.0%

EOG Eog Resources Inc 88.61 77.7x 28.7x 15.0x 0.2x 7.5x 5.4x 4.1x 22,508 24,620 263.4 9.4% 0.7% 17.8% 3.2% 24.9%

PXD Pioneer Natural Resources Co76.32 43.9x 27.0x 17.3x 0.5x 8.5x 7.3x 5.7x 8,860 11,594 147.6 30.9% 0.1% 5.7% -0.6% 14.8%

Industrial and Consumer Basket 14.1x 18.9x 16.7x 1.5x 10.6x 9.2x 8.2x 113.3% 3.3% 14.4% 3.8% 19.3%

P / E EV / EBITDA 2009

7 | P a g e Alex Flamm

Logical and temporary/fixable factors explain undervaluation.

o Bad headlines and management perception. Over the last couple months we‟ve

seen multiple EPS misses/guidance revisions, including a major goodwill write-down, on lower natural gas prices. The market has also seen some high profile management

changes. The former CEO/Chairman was very unpopular and this resulted in a discount; the stock jumped 10% after he announced his retirement in October. Williams is splitting

the roles (of CEO and Chairman) and the market seems enthusiastic about the changes.

The stock may continue to appreciate as the revamped team gains investor credibility. o Natural gas “glut” consensus. Both sellside and buyside seem stone-cold convinced

that natural gas will stay nominally cheap for at least the next 2-4 years. Due to compacted investment horizons, “2-4 years” translates into “forever” in many investors‟

minds and has resulted in negative bias against the company and its peers. Please see natural gas section for more.

o Business structure. Generally speaking, integrated businesses gain investor favor

when an entire sector is doing well. Separated operations gain favor when one business is doing well while another segment struggles. Today, Williams is seen as a confusing

structure of low risk pipeline assets and high risk E&P assets, which is perceived as unattractive to investors.

During a period where investors have a bias against natural gas exposure and a bias for yield, pipeline MLPs are being valued much more generously than natural gas focused E&Ps. The availability of investible pure-play pipeline MLPs (and pure-play oil-focused E&Ps) has lead to the undervaluation of the integrated, natural gas focused WMB.

William‟s structure is also confusing because while is not a pure-play E&P, a pure-play integrated energy company, nor a pure-play pipeline company, it is also not yet a true holding company. It is essentially an operating E&P with holdco assets in pipeline and midstream businesses. The company is moving towards becoming a clean holdco. This will likely unlock value over time.

Macro case is compelling: Natural gas is attractive and historically cheap. The bullet point

summary is below, followed by in depth analysis on the natural gas market.

o Natural gas is historically cheap on a relative basis to energy commodities o The bearish case for natural gas prices is the consensus, with every major Wall

Street firm onboard.

o This case has major holes in it: Supply/demand does not support low prices over the long term.

The shale gas bubble will not last forever. Production has peaked.

The demand factors that pushed down natural gas usage in 2009-2010

should abate in 2011-2012. Cost of production is too high for current prices. New natural gas

production depends on cheap financing and higher natural gas prices. Long term

nat gas prices will be determined by marginal cost, which is over $6/ mcf. Shale/unconventional wells have dramatic decline rates which cause

production to seem prolific in the early years and negligible in the later years. Companies are incentivized to over-state recoverable reserves.

o Shale gas production shows signs of a bubble about to peak. Contrary to bubbles in demand, bubbles in supply cause low near term prices, over extraction, and huge price

increases over the long term.

o Environmental and regulatory risk is not priced into natural gas and may add to marginal cost/ higher prices over the long run.

o Weather risk is not priced into natural gas. Recent weather has been depressive to prices. As someone who covers agriculture I can attest to the fact that investors tend to

extrapolate recent weather patterns and ignore longer term trends and tail risks.

o Peak natural gas on a global basis is a reality. You can‟t argue with geology. There may be no near term price impact but it is important to note and consider.

8 | P a g e Alex Flamm

Natural Gas Case Study (Macro Thesis) Natural gas is historically cheap compared to oil and coal – it has not kept pace with

other energy commodities, and is at all time modern era lows on a relative basis. On a

standalone basis, it is at low price comparable to its average price over 1999-2010, especially adjusted for inflation (note that charts are nominal). It trading in line with levels seen in 1999

- 2003 – before the energy price spike.

One can also examine relative prices on a per mmBTU basis, leading to the same conclusion:

The bearish case for natural gas prices is well understood and is the consensus on

both the buy side and the sell side. We see this objectively by looking at recent research headlines:

· Global nat gas: When will the flood ebb? (2/26 UBS) · Lowering our price forecasts on the back of surging US production (7/16 GS) · Natural Gas: Fundamentally Oversupplied (10/11 Morgan Stanley) · Natural Gas: Weather Bearish Gas (11/3 Morgan Stanley)

· Navigating the gas downturn (11/4 Macquarie)

There bearish case is that storage levels are near all time highs, and that shale technology

and LNG proliferation will continue to drive production higher. The result is lower prices for at least a few years. I have read a number of these bear natural gas pieces, and do not find the

analysis compelling. Analysis seems to be looking to support current prices which are very depressed. Given that people have gotten hurt going long natural gas in the past 3 years,

there is not much love lost. The warm October/November weather is thus far providing more

short-sighted ammunition to this bearish bias.

$-

$2

$4

$6

$8

$10

$12

$14

$16

$18

$-

$20

$40

$60

$80

$100

$120

$140

$160

$180

Jun

-99

De

c-9

9

Jun

-00

De

c-0

0

Jun

-01

De

c-0

1

Jun

-02

De

c-0

2

Jun

-03

De

c-0

3

Jun

-04

De

c-0

4

Jun

-05

De

c-0

5

Jun

-06

De

c-0

6

Jun

-07

De

c-0

7

Jun

-08

De

c-0

8

Jun

-09

De

c-0

9

Jun

-10

WTI Crude Oil Price $/barrel BSB Coal Price $/st

Qinhuangdao Coal Price $/st HH Natural Gas $/mmbTU (RHS)

$-

$5

$10

$15

$20

$25

$30

Jun

-99

De

c-9

9

Jun

-00

De

c-0

0

Jun

-01

De

c-0

1

Jun

-02

De

c-0

2

Jun

-03

De

c-0

3

Jun

-04

De

c-0

4

Jun

-05

De

c-0

5

Jun

-06

De

c-0

6

Jun

-07

De

c-0

7

Jun

-08

De

c-0

8

Jun

-09

De

c-0

9

Jun

-10

HH Natural Gas $ / mm BTU WTI Crude Oil $/ mmBTU

BSB Coal Adj $ / mmBTU Qinhuangdao Coal Adj $ / mmBTU

9 | P a g e Alex Flamm

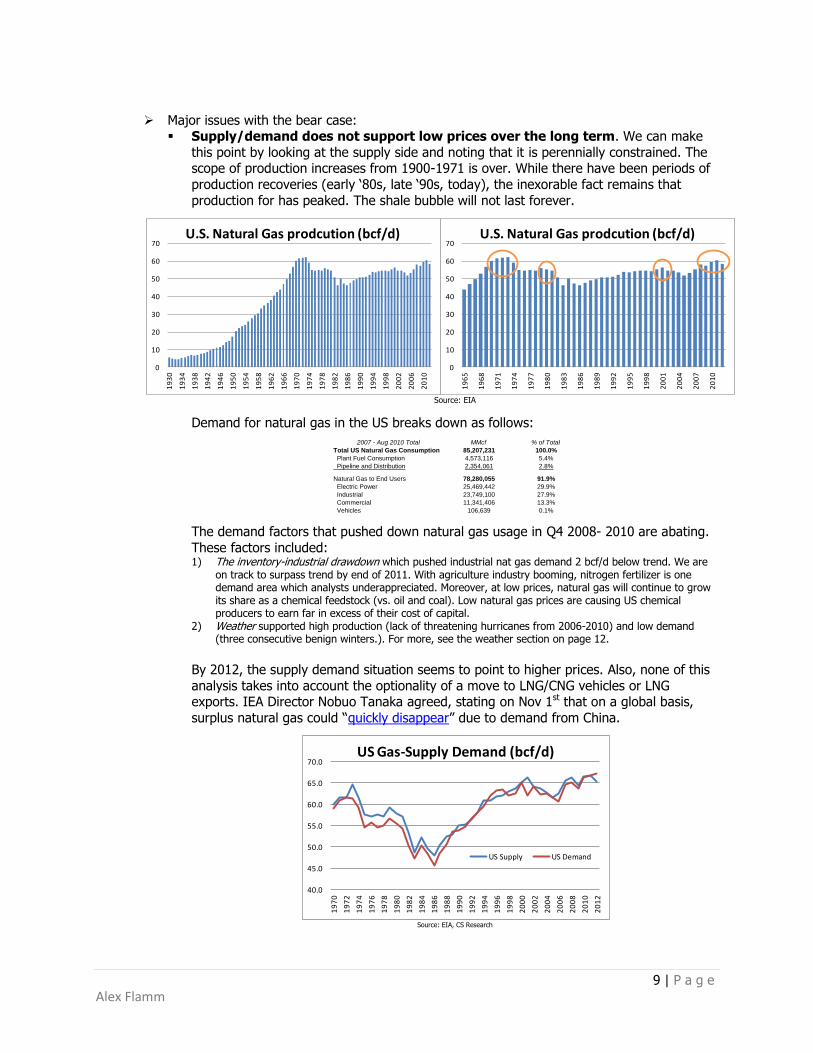

Major issues with the bear case: Supply/demand does not support low prices over the long term. We can make

this point by looking at the supply side and noting that it is perennially constrained. The scope of production increases from 1900-1971 is over. While there have been periods of

production recoveries (early „80s, late „90s, today), the inexorable fact remains that

production for has peaked. The shale bubble will not last forever.

Source: EIA

Demand for natural gas in the US breaks down as follows:

The demand factors that pushed down natural gas usage in Q4 2008- 2010 are abating.

These factors included: 1) The inventory-industrial drawdown which pushed industrial nat gas demand 2 bcf/d below trend. We are

on track to surpass trend by end of 2011. With agriculture industry booming, nitrogen fertilizer is one demand area which analysts underappreciated. Moreover, at low prices, natural gas will continue to grow its share as a chemical feedstock (vs. oil and coal). Low natural gas prices are causing US chemical producers to earn far in excess of their cost of capital.

2) Weather supported high production (lack of threatening hurricanes from 2006-2010) and low demand (three consecutive benign winters.). For more, see the weather section on page 12.

By 2012, the supply demand situation seems to point to higher prices. Also, none of this

analysis takes into account the optionality of a move to LNG/CNG vehicles or LNG exports. IEA Director Nobuo Tanaka agreed, stating on Nov 1st that on a global basis,

surplus natural gas could “quickly disappear” due to demand from China.

Source: EIA, CS Research

0

10

20

30

40

50

60

70

19

30

19

34

19

38

19

42

19

46

19

50

19

54

19

58

19

62

19

66

19

70

19

74

19

78

19

82

19

86

19

90

19

94

19

98

20

02

20

06

20

10

U.S. Natural Gas prodcution (bcf/d)

0

10

20

30

40

50

60

70

19

65

19

68

19

71

19

74

19

77

19

80

19

83

19

86

19

89

19

92

19

95

19

98

20

01

20

04

20

07

20

10

U.S. Natural Gas prodcution (bcf/d)

2007 - Aug 2010 Total MMcf % of Total

Total US Natural Gas Consumption 85,207,231 100.0%

Plant Fuel Consumption 4,573,116 5.4%

Pipeline and Distribution 2,354,061 2.8%

Natural Gas to End Users 78,280,055 91.9%

Electric Power 25,469,442 29.9%

Industrial 23,749,100 27.9%

Commercial 11,341,406 13.3%

Vehicles 106,639 0.1%

40.0

45.0

50.0

55.0

60.0

65.0

70.0

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

US Gas-Supply Demand (bcf/d)

US Supply US Demand

10 | P a g e Alex Flamm

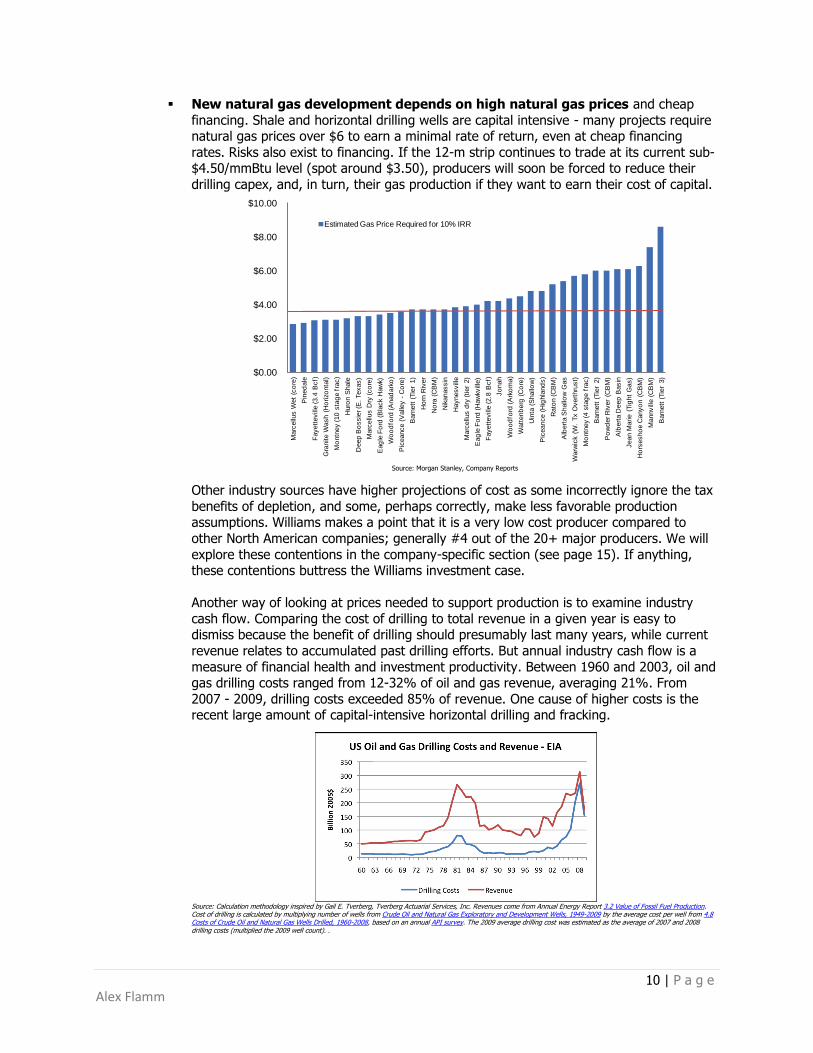

New natural gas development depends on high natural gas prices and cheap

financing. Shale and horizontal drilling wells are capital intensive - many projects require natural gas prices over $6 to earn a minimal rate of return, even at cheap financing

rates. Risks also exist to financing. If the 12-m strip continues to trade at its current sub-$4.50/mmBtu level (spot around $3.50), producers will soon be forced to reduce their

drilling capex, and, in turn, their gas production if they want to earn their cost of capital.

Source: Morgan Stanley, Company Reports

Other industry sources have higher projections of cost as some incorrectly ignore the tax

benefits of depletion, and some, perhaps correctly, make less favorable production assumptions. Williams makes a point that it is a very low cost producer compared to

other North American companies; generally #4 out of the 20+ major producers. We will

explore these contentions in the company-specific section (see page 15). If anything, these contentions buttress the Williams investment case.

Another way of looking at prices needed to support production is to examine industry

cash flow. Comparing the cost of drilling to total revenue in a given year is easy to dismiss because the benefit of drilling should presumably last many years, while current

revenue relates to accumulated past drilling efforts. But annual industry cash flow is a

measure of financial health and investment productivity. Between 1960 and 2003, oil and gas drilling costs ranged from 12-32% of oil and gas revenue, averaging 21%. From

2007 - 2009, drilling costs exceeded 85% of revenue. One cause of higher costs is the recent large amount of capital-intensive horizontal drilling and fracking.

Source: Calculation methodology inspired by Gail E. Tverberg, Tverberg Actuarial Services, Inc. Revenues come from Annual Energy Report 3.2 Value of Fossil Fuel Production. Cost of drilling is calculated by multiplying number of wells from Crude Oil and Natural Gas Exploratory and Development Wells, 1949-2009 by the average cost per well from 4.8 Costs of Crude Oil and Natural Gas Wells Drilled, 1960-2008, based on an annual API survey. The 2009 average drilling cost was estimated as the average of 2007 and 2008 drilling costs (multiplied the 2009 well count). .

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

Marc

ellu

s W

et

(co

re)

Pin

ed

ale

Fayett

evill

e (3.4

Bcf)

Gra

nite W

ash (

Ho

rizo

nta

l)

Mo

ntn

ey (10 s

tag

e f

rac)

Huro

n S

hale

Deep

Bo

ssie

r (E

. Texas)

Marc

ellu

s D

ry (co

re)

Eag

le F

ord

(B

lack

Haw

k)

Wo

od

ford

(A

nad

ark

o)

Pic

eance (

Valle

y -

Co

re)

Barn

ett

(Tie

r 1)

Ho

rn R

iver

No

ra (

CB

M)

Nik

anassin

Haynesvill

e

Marc

ellu

s d

ry (tier

2)

Eag

le F

ord

(H

aw

kvill

e)

Fayett

evill

e (2.8

Bcf)

Jo

nah

Wo

od

ford

(A

rko

ma)

Watt

enb

erg

(C

ore

)

Uin

ta (

Shallo

w)

Pic

eance (

Hig

hla

nd

s)

Rato

n (C

BM

)

Alb

ert

a S

hallo

w G

as

Warw

ick

(W.

Tx O

vert

hru

st)

Mo

ntn

ey (4 s

tag

e f

rac)

Barn

ett

(Tie

r 2)

Po

wd

er R

iver

(CB

M)

Alb

ert

a D

eep

Basin

Jean M

arie (

Tig

ht

Gas)

Ho

rsesho

e C

anyo

n (

CB

M)

Mannvill

e (

CB

M)

Barn

ett

(Tie

r 3)

Estimated Gas Price Required for 10% IRR

11 | P a g e Alex Flamm

Shale gas is untested over long periods of extraction. More importantly these wells

have dramatic decline rates. Companies are incentivized to massively over-state recoverable reserves as this is how they are valued by the market. It‟s a bluff they don‟t

have to own up for many years.

Here is a 2007 projection of output from the Barnett shale fields. Only a few months into production, production falls far short of projections. In 2009, projections were updated to conform to the reality that the parabolic curve of depletion is far steeper than expected.

Source: Aruthur E. Berman, APSO 2009

Recent EIA data illustrates this point. Note below that 2010 saw flattening production from Fayetteville and Woodford, and declining production from Barnett. The explosion in shale production comes from an investment boom and the upfront nature of wells‟ production curves.

Natural gas companies are highly levered and depend on increasing reserve

estimates to justify more production and more debt. This acts to juice ROE and allows companies to grow in an otherwise stagnant industry. Companies are incentivized to

hype discoveries and overproduce (similar to the credit bubble where financial institutions were incentivized to over-lend, make rosy estimates on collateral and grow).

Yet, increasing reserves don‟t show up in production, which grows more slowly.

Source: Company Reports

7James M. Kendell, Houston, TX, October 19, 2010 7James M. Kendell, Houston, TX, October 19, 2010

0

1,000

2,000

3,000

4,000

5,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Barnett Fayetteville Woodford

Haynesville Marcellus Eagle Ford

Shale Production by Basin, 2000-2010

Source: EIA, Lippman Consulting (2010 estimated)

Billion Cubic Feet

$0.0

$2,000.0

$4,000.0

$6,000.0

$8,000.0

$10,000.0

$12,000.0

$14,000.0

$16,000.0

0.0

500.0

1000.0

1500.0

2000.0

2500.0

3000.0

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010E

CHK - Chesapeake Energy

Gas Production (MMcf/d)

"Proved" reserves (MMBOE)

Total Debt ($ mil) - RHS

50%

55%

60%

65%

70%

75%

80%

0.0

500.0

1000.0

1500.0

2000.0

2500.0

3000.0

2002

2003

2004

2005

2006

2007

2008

2009

2010E

CHK - Chesapeake Energy

"Proved" reserves (MMBOE)

% of Reserves Developed

12 | P a g e Alex Flamm

Evidence of a bubble in shale development abounds, including language in the press:

A massive natural-gas discovery here in northern Louisiana heralds a big shift in the nation's energy landscape. After an era of declining production, the U.S. is now swimming in natural gas. - U.S. Gas Fields Go From Bust to Boom, Wall Street Journal, April 30, 2009

Natural gas from shale formations is the new magic phrase in the oil and gas industry, as new technologies have led to stunning increases in potential resources and anticipated profits. – Is Shale Gas the Climate Bill's New Bargaining Chip? New York Times, August 5, 2009

Private equity entry marks the summit? KKR to Invest $400 Million to Develop Shale Gas in Texas, Wall Street Journal, June 13, 2010

Gas boom mints instant millionaires. CNNMoney.com November 2, 2010

The bubble in natural gas development is only accelerating depletion. Contrary to bubbles in

demand, bubbles in supply cause huge price increases over the long term. This fact escapes many analysts. Over exploitation of resources leads to long term under-supply issues.

Environmental and regulatory risks are very real. The deeper and more

unconventional a deposit, the higher the potential for an adverse event. We have recently

seen major ruptures/blowouts in key shale fields, and subsequent calls for banning shale drilling by mainstream politicians. Other politicians are calling for higher royalty taxes.

Considering the above, and in the aftermath of the BP Spill, regulatory hostility towards energy exploration is bullish for prices. Here are some headlines to underscore the point:

Shale Gas Well Blowout Raises Specter of New BP, Bloomberg Markets, June 7, 2010 Sestak Issues call for Gas Drilling Moratorium, The Times Tribune, June 13, 2010 Governor Bans New Gas Wells on State Land, New York Times October 26, 2010 Group protests shale drilling convention, Pittsburgh Post Gazette, November 4, 2010

Weather risk is not priced into natural gas. Investors rarely attempt to understand or think about weather. As someone who covers agriculture I can attest to the fact that

investors tend to extrapolate recent weather patterns and ignore longer term trends and tail risks. Recent weather has been depressive to prices as we have seen low demand, benefited

by three consecutive benign winters, and high production, boosted by a lack of hurricanes

from 2008-2010. However, an analysis of weather trends indicates a high probability of: 1) An extremely cold 2011 winter in North America due to three enormous weather patterns colliding: a

strong La Nina in the Pacific, atmospheric debris from the Northern Pacific volcanoes combined with negative Arctic Oscillation (AO), and the Atlantic Multidecadal Oscillation (AMO).

2) Major hurricanes in 2011 and 2012 due a persistent La Nina, a warm Atlantic (due to AMO), warm tropics and an up-trending hurricane cycle.

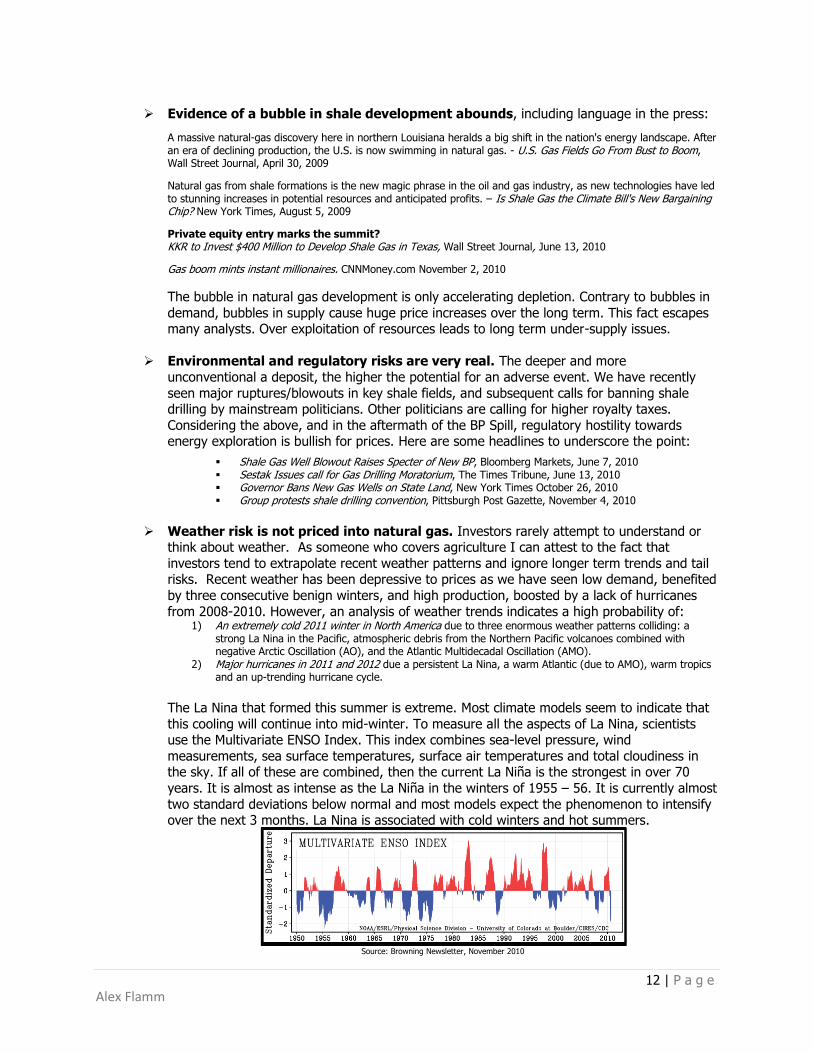

The La Nina that formed this summer is extreme. Most climate models seem to indicate that

this cooling will continue into mid-winter. To measure all the aspects of La Nina, scientists use the Multivariate ENSO Index. This index combines sea-level pressure, wind

measurements, sea surface temperatures, surface air temperatures and total cloudiness in the sky. If all of these are combined, then the current La Niña is the strongest in over 70

years. It is almost as intense as the La Niña in the winters of 1955 – 56. It is currently almost

two standard deviations below normal and most models expect the phenomenon to intensify over the next 3 months. La Nina is associated with cold winters and hot summers.

Source: Browning Newsletter, November 2010

13 | P a g e Alex Flamm

From Russia to Alaska, the volcanoes of the North Pacific have been unusually active over the

past two to three years. Over the past few years, the debris from these eruptions has been

lingering in the air and blocking incoming sunlight. Last year, both Alaska‟s Mt. Redoubt and Russia‟s Sarychev Peak had eruptions that were over 10 miles high. This year, Russia‟s

Kamchatka Peninsula has had up to 6 active volcanoes and two of them, Klyuchevskoy and Sheveluch, have had small-to-medium eruptions all year long. As recently as mid-October,

Klyuchevskoy had an eruption 7.8 km (4.8 miles) high, strong enough to impact the stratosphere. This year may not have had the same giant eruptions as last year, but there is

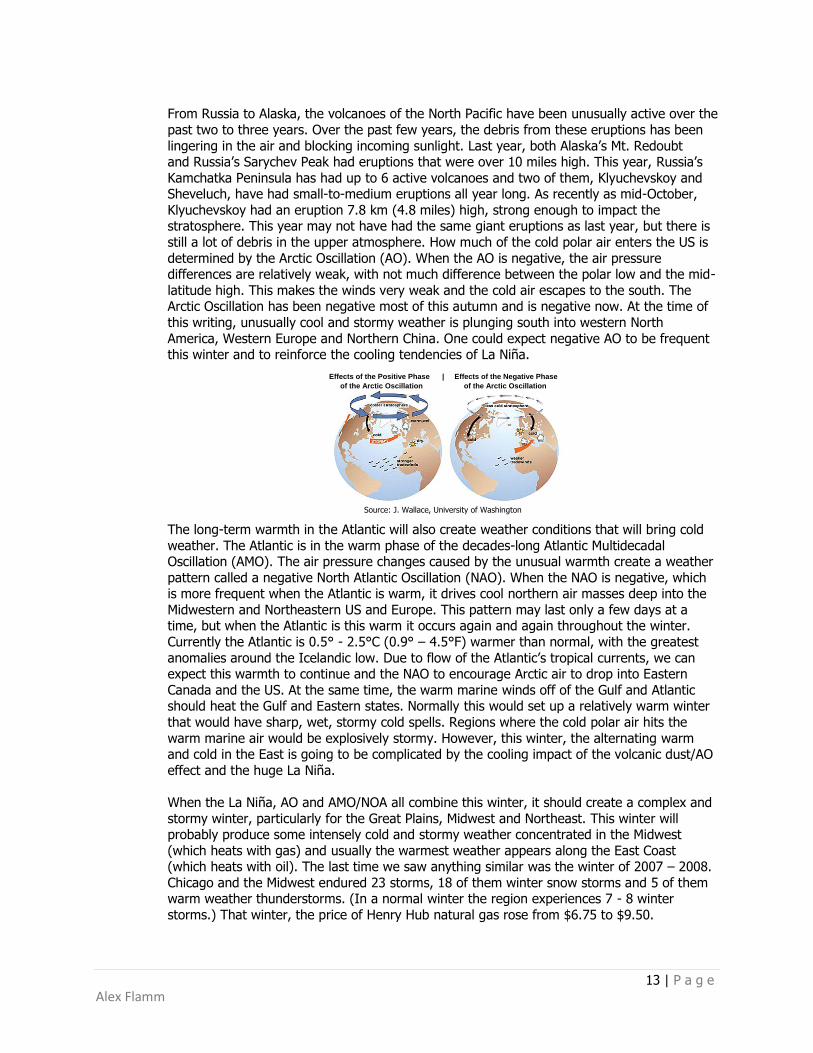

still a lot of debris in the upper atmosphere. How much of the cold polar air enters the US is

determined by the Arctic Oscillation (AO). When the AO is negative, the air pressure differences are relatively weak, with not much difference between the polar low and the mid-

latitude high. This makes the winds very weak and the cold air escapes to the south. The Arctic Oscillation has been negative most of this autumn and is negative now. At the time of

this writing, unusually cool and stormy weather is plunging south into western North

America, Western Europe and Northern China. One could expect negative AO to be frequent this winter and to reinforce the cooling tendencies of La Niña.

Source: J. Wallace, University of Washington

The long-term warmth in the Atlantic will also create weather conditions that will bring cold

weather. The Atlantic is in the warm phase of the decades-long Atlantic Multidecadal Oscillation (AMO). The air pressure changes caused by the unusual warmth create a weather

pattern called a negative North Atlantic Oscillation (NAO). When the NAO is negative, which is more frequent when the Atlantic is warm, it drives cool northern air masses deep into the

Midwestern and Northeastern US and Europe. This pattern may last only a few days at a time, but when the Atlantic is this warm it occurs again and again throughout the winter.

Currently the Atlantic is 0.5° - 2.5°C (0.9° – 4.5°F) warmer than normal, with the greatest

anomalies around the Icelandic low. Due to flow of the Atlantic‟s tropical currents, we can expect this warmth to continue and the NAO to encourage Arctic air to drop into Eastern

Canada and the US. At the same time, the warm marine winds off of the Gulf and Atlantic should heat the Gulf and Eastern states. Normally this would set up a relatively warm winter

that would have sharp, wet, stormy cold spells. Regions where the cold polar air hits the

warm marine air would be explosively stormy. However, this winter, the alternating warm and cold in the East is going to be complicated by the cooling impact of the volcanic dust/AO

effect and the huge La Niña.

When the La Niña, AO and AMO/NOA all combine this winter, it should create a complex and

stormy winter, particularly for the Great Plains, Midwest and Northeast. This winter will probably produce some intensely cold and stormy weather concentrated in the Midwest

(which heats with gas) and usually the warmest weather appears along the East Coast (which heats with oil). The last time we saw anything similar was the winter of 2007 – 2008.

Chicago and the Midwest endured 23 storms, 18 of them winter snow storms and 5 of them warm weather thunderstorms. (In a normal winter the region experiences 7 - 8 winter

storms.) That winter, the price of Henry Hub natural gas rose from $6.75 to $9.50.

Effects of the Positive Phase | Effects of the Negative Phase

of the Arctic Oscillation of the Arctic Oscillation

14 | P a g e Alex Flamm

Regarding hurricanes, with the elimination of any storm-suppressing El Niño winds this

summer, the probability of hurricanes and intense hurricanes increases. Historically La Nina years are associated with more severe and numerous hurricanes. Also, the AMO cycle

(meaning a warm Atlantic) buttresses this trend too and has led to a general increase in hurricane activity. While 2009-2010 has largely been a low hurricane environment, these two

trends are still in place and portend some upside risk to natural gas prices.

Source: International Research institute for Climate and Society Source: NOAA

Peak natural gas on a global basis is a reality. You can‟t argue with geology. There may be no immediate price impact, but it is important to note that cheaply available

abundant natural gas production has peaked. While less imminent than peak oil production, which seems to be taking place today, peak natural gas production is coming in the next 5-

25 years. Timing depends on the speed and aggressiveness of investment, and the level of economic growth driving consumption. Natural gas production has already peaked in many

countries including the U.K., Romania, Italy, and the U.S. U.S. production has not

experienced a straight decline as the production graph on page 9 indicates. The ability to maintain production has come due to a) high natural gas prices in the late 1990s and 2000s

(encouraging more expensive unconventional exploration), b) huge capital inflows directed toward well development during the late 1990s and late 2000s and c) the advent of and

investment in shale properties in the late 2000s. Such measures extend the peak but

ultimately push up the cost curve and exacerbate decline rates. On a global basis, major gas discoveries - the source of cheap natural gas - have also been declining.

Global Giant Gas Discoveries by Decade, Including Unconventional

Source: EIA

0

1

2

3

4

5

6

7

0

50

100

150

200

250

300

19

50

19

53

19

56

19

59

19

62

19

65

19

68

19

71

19

74

19

77

19

80

19

83

19

86

19

89

19

92

19

95

19

98

20

01

20

04

20

07

20

10

Hurricane Energy and Impacts

Accumulated Cyclone Energy

15 | P a g e Alex Flamm

Micro case is compelling: Williams' assets are well positioned. The company has a number of

areas where it can excel going forward. The complexity and scope surrounding the company,

combined with a weak natural gas environment, has made it easy for the buy side to ignore a number of growth and pricing areas that provide tailwinds to future earnings.

o E&P:

Repeatable, low cost, high quality inventory deserves a premium valuation. Assets such Piceance are low cost and high quality.

Declining Rocky Mountain basis improves revenue and profitability. Analysts are still using basis estimates in excess of 25-30% in the valuation

models which is incorrect.

Growth opportunities are better than average. Williams owns substantial acreage for growth in Piceance, Marcellus shale, PRB, Green River, Barnett shale

and the San Juan Basin. Williams also could announce a new high-profile expansion into other areas including Eagle Ford, Bakken and Niobrara.

Proven adept hedger. While we can only value the hedges currently on the

books, history indicates that Williams has done very well with its hedging actions. E&P spin-off might highlight undervaluation. Given that the market places

$0 value on the E&P segment using today‟s market value of WPZ, a publically traded E&P company, housing WMB‟s assets, might close the valuation gap.

o Midstream and Pipeline:

NGL fundamentals are strong. Williams' NGLs business benefits from

increased nat gas production (drives volume), a better cost position vs. oil-sourced NGLs (drives volume) and higher oil prices (drives pricing).

The location of Williams' midstream assets gives it unique leverage to strong Midstream fundamentals. This business is growing in value as the industry

moves production into complex shale fields with higher liquids content, and as

WPZ exercises its expansion options. Increasing value of natural gas infrastructure provides a tailwind to WMB,

especially given its pipeline growth/expansion opportunities. Pipeline assets are a natural inflation hedge in an inflationary

environment. Williams (via WPZ) owns some of the best pipeline assets in the

country and would be a natural beneficiary of a fed-induced inflationary spiral

Williams Company Discussion (Micro Thesis)

E&P: This segment produces, develops, and manages natural gas reserves primarily located in

the Rocky Mountain (primarily Colorado, New Mexico, and Wyoming), Mid-Continent (Oklahoma and Texas), and Appalachian regions of the United States. It specializes in natural gas production

from tight-sands, shale formations, and coal bed methane reserves in the Piceance, San Juan, Powder River, Arkoma, Green River, Fort Worth, and Appalachian basins. Over 99% of its

domestic reserves are natural gas. It also has international oil and gas interests, which include a

69% equity interest in Apco Oil and Gas International Inc., an oil and gas exploration and production company with operations in South America. The Company‟s proved undeveloped

reserves, as of December 31, 2009, were 1,868 billion cubic feet of gas equivalent (Bcfe). As of December 31, 2009, it had 42 gross (14 net) wells in the process of being drilled. Its properties

include Piceance basin, San Juan basin, Powder River basin and Mid-Continent properties. Its

other properties include interests in the Green River basin in southwestern Wyoming and the Appalachian basin (Marcellus Shale) in Pennsylvania.

It is my contention that this segment has a lot of value – conservatively between $7 to $22 per

share depending on the long term price of natural gas. While one may be bullish on natural gas

16 | P a g e Alex Flamm

in general, it is also my belief that Williams' natural gas assets are better than average due to the

their low cost, improving pricing, and growth opportunities.

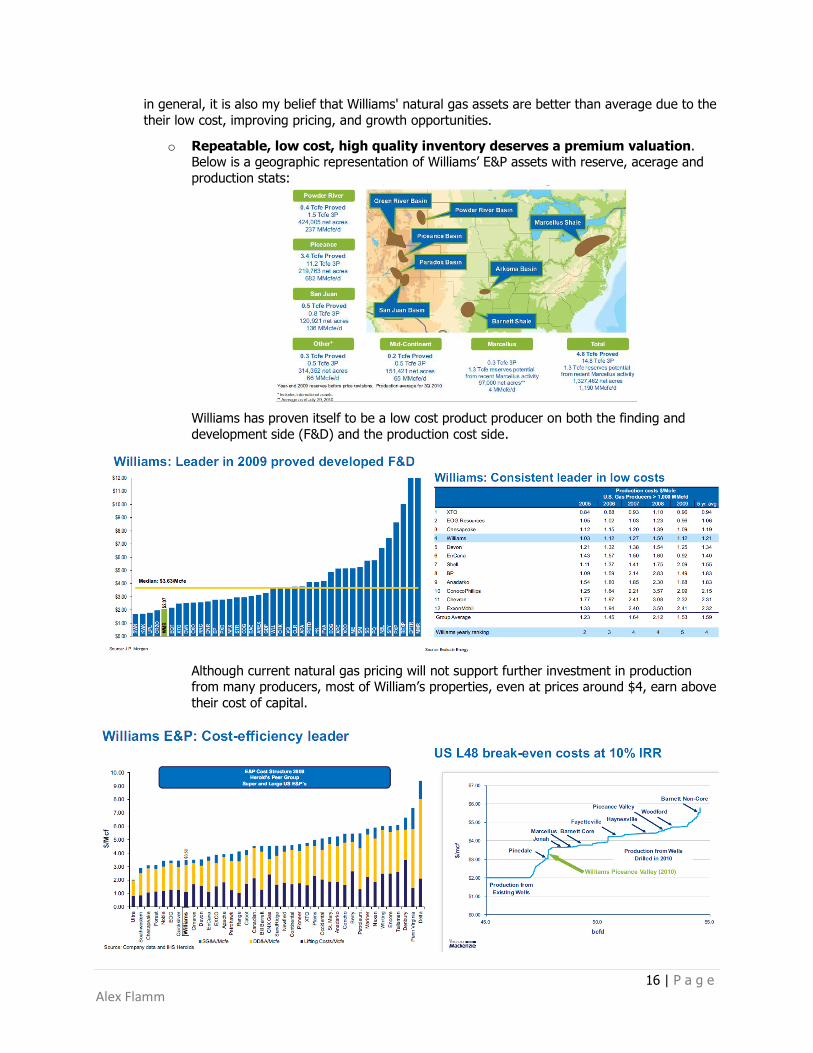

o Repeatable, low cost, high quality inventory deserves a premium valuation. Below is a geographic representation of Williams‟ E&P assets with reserve, acerage and

production stats:

Williams has proven itself to be a low cost product producer on both the finding and

development side (F&D) and the production cost side.

Although current natural gas pricing will not support further investment in production from many producers, most of William‟s properties, even at prices around $4, earn above

their cost of capital.

17 | P a g e Alex Flamm

Data from CS corroborates this contention and our belief that most properties will lose

money with $4 gas (but Piceance will earn in excess of cost of capital).

o Declining Rocky Mountain basis improves revenue and profitability. Historically, the price Rocky Mountain producers, like Williams, could receive for their gas was far

below the national Henry Hub price. Analysts are still using basis estimates in excess of 25-30% in their valuation models which is incorrect. Current basis is close to 0%.

Lack of takeaway capacity can explain the formerly high basis charged to Rocky

Mountain producers. Essentially, from 2006 to early 2010, export volumes closely pushed

-70.0%

-60.0%

-50.0%

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

$-

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$16.00

$18.00

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10

Negative Rocky Mountain Basis is GoneHenry Hub Price Rocky Mountain Avg Price Rocky Mountain Basis (30 day avg)

-60.0%

-50.0%

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

$-

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$16.00

$18.00

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10

Negative San Juan Basis is Gone

Henry Hub Price San Juan Basin Price San Juan Basis (30 day avg)

18 | P a g e Alex Flamm

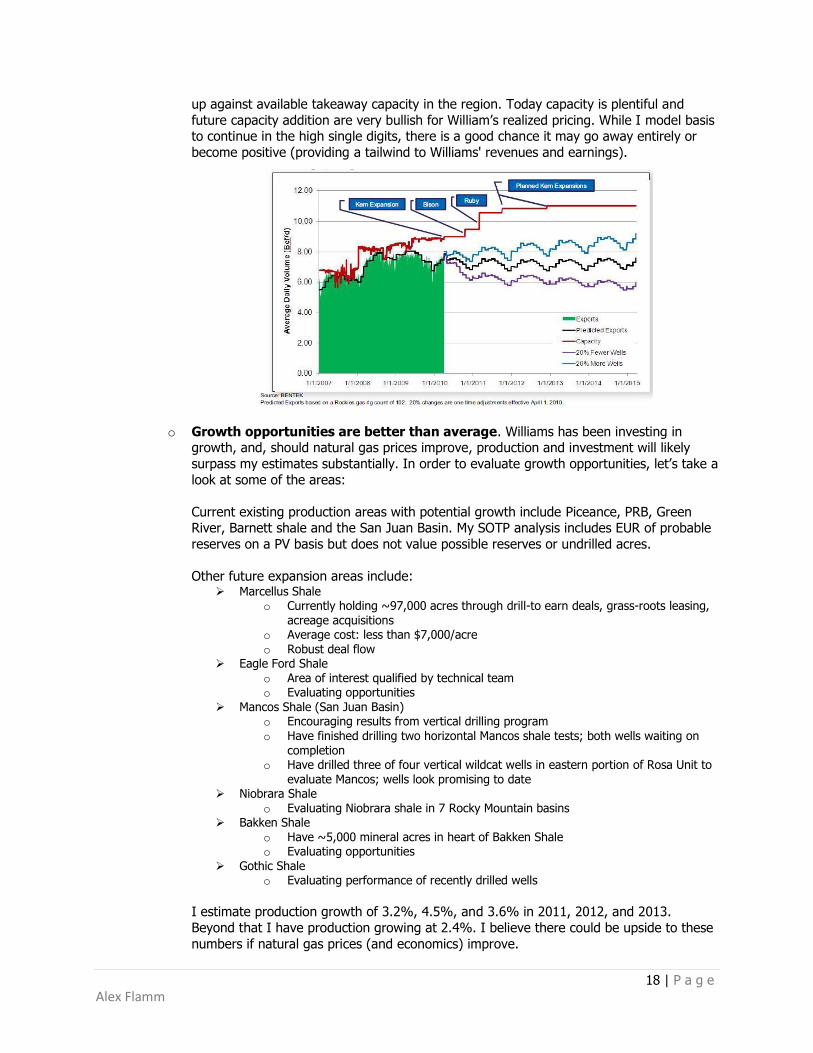

up against available takeaway capacity in the region. Today capacity is plentiful and

future capacity addition are very bullish for William‟s realized pricing. While I model basis to continue in the high single digits, there is a good chance it may go away entirely or

become positive (providing a tailwind to Williams' revenues and earnings).

o Growth opportunities are better than average. Williams has been investing in growth, and, should natural gas prices improve, production and investment will likely

surpass my estimates substantially. In order to evaluate growth opportunities, let‟s take a

look at some of the areas:

Current existing production areas with potential growth include Piceance, PRB, Green River, Barnett shale and the San Juan Basin. My SOTP analysis includes EUR of probable

reserves on a PV basis but does not value possible reserves or undrilled acres.

Other future expansion areas include:

Marcellus Shale o Currently holding ~97,000 acres through drill-to earn deals, grass-roots leasing,

acreage acquisitions o Average cost: less than $7,000/acre o Robust deal flow

Eagle Ford Shale o Area of interest qualified by technical team o Evaluating opportunities

Mancos Shale (San Juan Basin) o Encouraging results from vertical drilling program

o Have finished drilling two horizontal Mancos shale tests; both wells waiting on completion

o Have drilled three of four vertical wildcat wells in eastern portion of Rosa Unit to evaluate Mancos; wells look promising to date

Niobrara Shale o Evaluating Niobrara shale in 7 Rocky Mountain basins

Bakken Shale o Have ~5,000 mineral acres in heart of Bakken Shale o Evaluating opportunities

Gothic Shale o Evaluating performance of recently drilled wells

I estimate production growth of 3.2%, 4.5%, and 3.6% in 2011, 2012, and 2013.

Beyond that I have production growing at 2.4%. I believe there could be upside to these

numbers if natural gas prices (and economics) improve.

19 | P a g e Alex Flamm

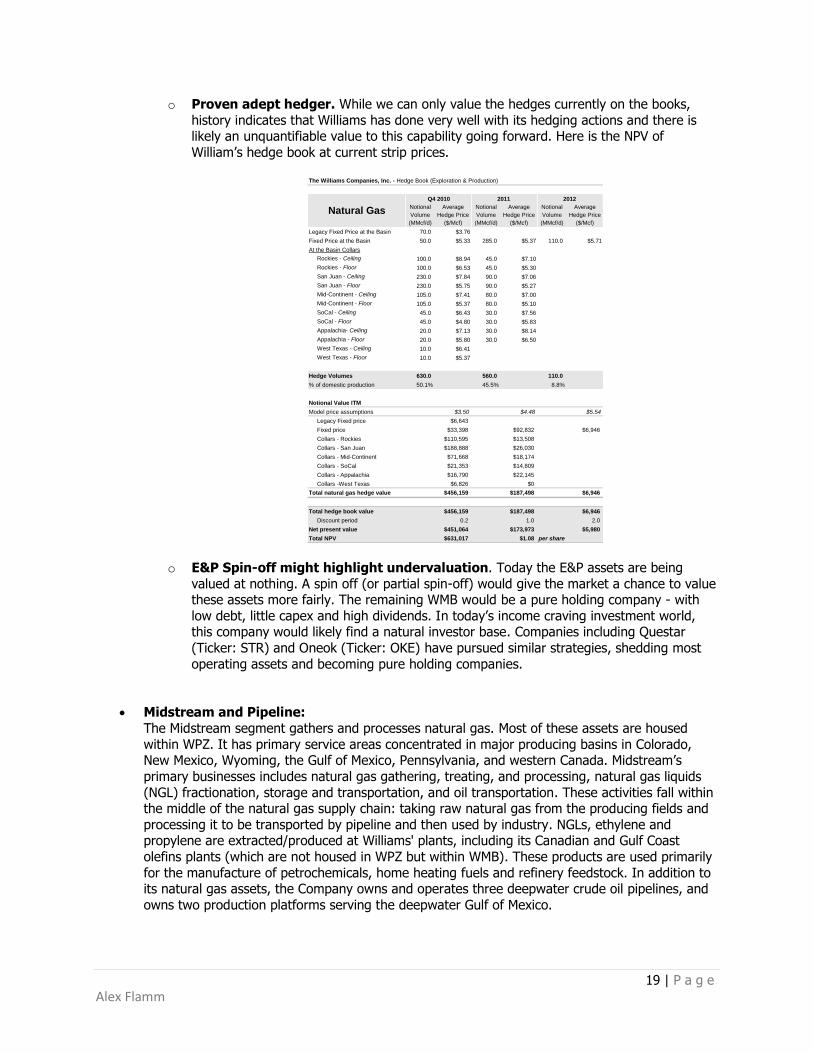

o Proven adept hedger. While we can only value the hedges currently on the books,

history indicates that Williams has done very well with its hedging actions and there is likely an unquantifiable value to this capability going forward. Here is the NPV of

William‟s hedge book at current strip prices.

o E&P Spin-off might highlight undervaluation. Today the E&P assets are being

valued at nothing. A spin off (or partial spin-off) would give the market a chance to value these assets more fairly. The remaining WMB would be a pure holding company - with

low debt, little capex and high dividends. In today‟s income craving investment world, this company would likely find a natural investor base. Companies including Questar

(Ticker: STR) and Oneok (Ticker: OKE) have pursued similar strategies, shedding most

operating assets and becoming pure holding companies.

Midstream and Pipeline:

The Midstream segment gathers and processes natural gas. Most of these assets are housed

within WPZ. It has primary service areas concentrated in major producing basins in Colorado, New Mexico, Wyoming, the Gulf of Mexico, Pennsylvania, and western Canada. Midstream‟s

primary businesses includes natural gas gathering, treating, and processing, natural gas liquids

(NGL) fractionation, storage and transportation, and oil transportation. These activities fall within the middle of the natural gas supply chain: taking raw natural gas from the producing fields and

processing it to be transported by pipeline and then used by industry. NGLs, ethylene and propylene are extracted/produced at Williams' plants, including its Canadian and Gulf Coast

olefins plants (which are not housed in WPZ but within WMB). These products are used primarily

for the manufacture of petrochemicals, home heating fuels and refinery feedstock. In addition to its natural gas assets, the Company owns and operates three deepwater crude oil pipelines, and

owns two production platforms serving the deepwater Gulf of Mexico.

The Williams Companies, Inc. - Hedge Book (Exploration & Production)

Notional Average Notional Average Notional Average

Volume Hedge Price Volume Hedge Price Volume Hedge Price

(MMcf/d) ($/Mcf) (MMcf/d) ($/Mcf) (MMcf/d) ($/Mcf)

Legacy Fixed Price at the Basin 70.0 $3.76

Fixed Price at the Basin 50.0 $5.33 285.0 $5.37 110.0 $5.71

At the Basin Collars

Rockies - Ceiling 100.0 $8.94 45.0 $7.10

Rockies - Floor 100.0 $6.53 45.0 $5.30

San Juan - Ceiling 230.0 $7.84 90.0 $7.06

San Juan - Floor 230.0 $5.75 90.0 $5.27

Mid-Continent - Ceiling 105.0 $7.41 80.0 $7.00

Mid-Continent - Floor 105.0 $5.37 80.0 $5.10

SoCal - Ceiling 45.0 $6.43 30.0 $7.56

SoCal - Floor 45.0 $4.80 30.0 $5.83

Appalachia- Ceiling 20.0 $7.13 30.0 $8.14

Appalachia - Floor 20.0 $5.80 30.0 $6.50

West Texas - Ceiling 10.0 $6.41

West Texas - Floor 10.0 $5.37

Hedge Volumes 630.0 560.0 110.0

% of domestic production 50.1% 45.5% 8.8%

Notional Value ITM

Model price assumptions $3.50 $4.48 $5.54

Legacy Fixed price $6,643

Fixed price $33,398 $92,832 $6,946

Collars - Rockies $110,595 $13,508

Collars - San Juan $188,888 $26,030

Collars - Mid-Continent $71,668 $18,174

Collars - SoCal $21,353 $14,809

Collars - Appalachia $16,790 $22,145

Collars -West Texas $6,826 $0

Total natural gas hedge value $456,159 $187,498 $6,946

Total hedge book value $456,159 $187,498 $6,946

Discount period 0.2 1.0 2.0

Net present value $451,064 $173,973 $5,980

Total NPV $631,017 $1.08 per share

Natural Gas

Q4 2010 2011 2012

20 | P a g e Alex Flamm

Williams‟ Pipeline segment owns and operates a combined total of approximately 13,900 miles of

pipelines with a total annual throughput of approximately 2,700 trillion British thermal units (TBtu) of natural gas and peak-day delivery capacity of approximately 12 million dekatherms

(MMdt) of gas. These assets are entirely housed within WPZ. Gas Pipeline consists of Transcontinental Gas Pipe Line Company, LLC (Transco) and Northwest Pipeline GP (Northwest

Pipeline). Gas Pipeline also holds interests in joint venture interstate and intrastate natural gas

pipeline systems, including a 50% interest in Gulfstream. Gas Pipeline also includes Williams Pipeline Partners L.P. (WMZ) which is owned by WPZ.

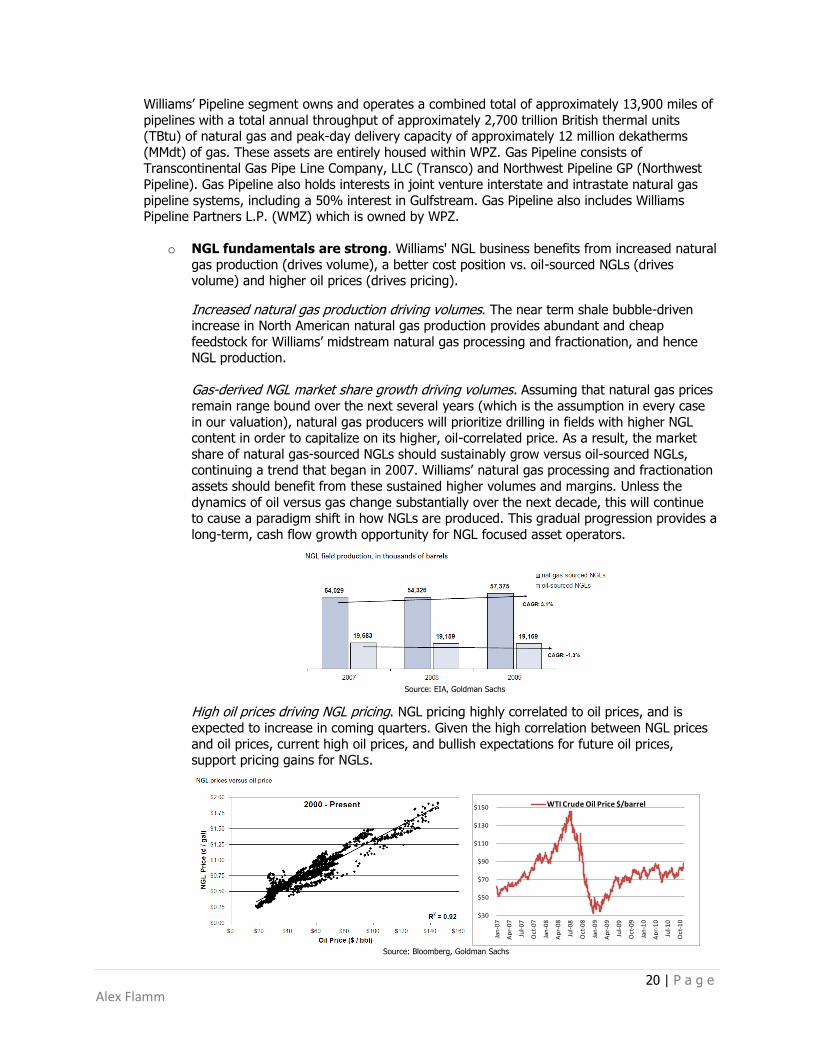

o NGL fundamentals are strong. Williams' NGL business benefits from increased natural

gas production (drives volume), a better cost position vs. oil-sourced NGLs (drives volume) and higher oil prices (drives pricing).

Increased natural gas production driving volumes. The near term shale bubble-driven increase in North American natural gas production provides abundant and cheap

feedstock for Williams‟ midstream natural gas processing and fractionation, and hence NGL production.

Gas-derived NGL market share growth driving volumes. Assuming that natural gas prices

remain range bound over the next several years (which is the assumption in every case

in our valuation), natural gas producers will prioritize drilling in fields with higher NGL content in order to capitalize on its higher, oil-correlated price. As a result, the market

share of natural gas-sourced NGLs should sustainably grow versus oil-sourced NGLs, continuing a trend that began in 2007. Williams‟ natural gas processing and fractionation

assets should benefit from these sustained higher volumes and margins. Unless the

dynamics of oil versus gas change substantially over the next decade, this will continue to cause a paradigm shift in how NGLs are produced. This gradual progression provides a

long-term, cash flow growth opportunity for NGL focused asset operators.

Source: EIA, Goldman Sachs

High oil prices driving NGL pricing. NGL pricing highly correlated to oil prices, and is

expected to increase in coming quarters. Given the high correlation between NGL prices

and oil prices, current high oil prices, and bullish expectations for future oil prices, support pricing gains for NGLs.

Source: Bloomberg, Goldman Sachs

$30

$50

$70

$90

$110

$130

$150

Jan

-07

Ap

r-0

7

Jul-

07

Oct

-07

Jan

-08

Ap

r-0

8

Jul-

08

Oct

-08

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

WTI Crude Oil Price $/barrel

21 | P a g e Alex Flamm

NGL Margins have been strong over the last four quarters. Today, oil prices are at 4 year highs and margins should continue to improve.

Also note that Q3 production was negatively impacted by the (temporary) Golf of Mexico

drilling moratorium.

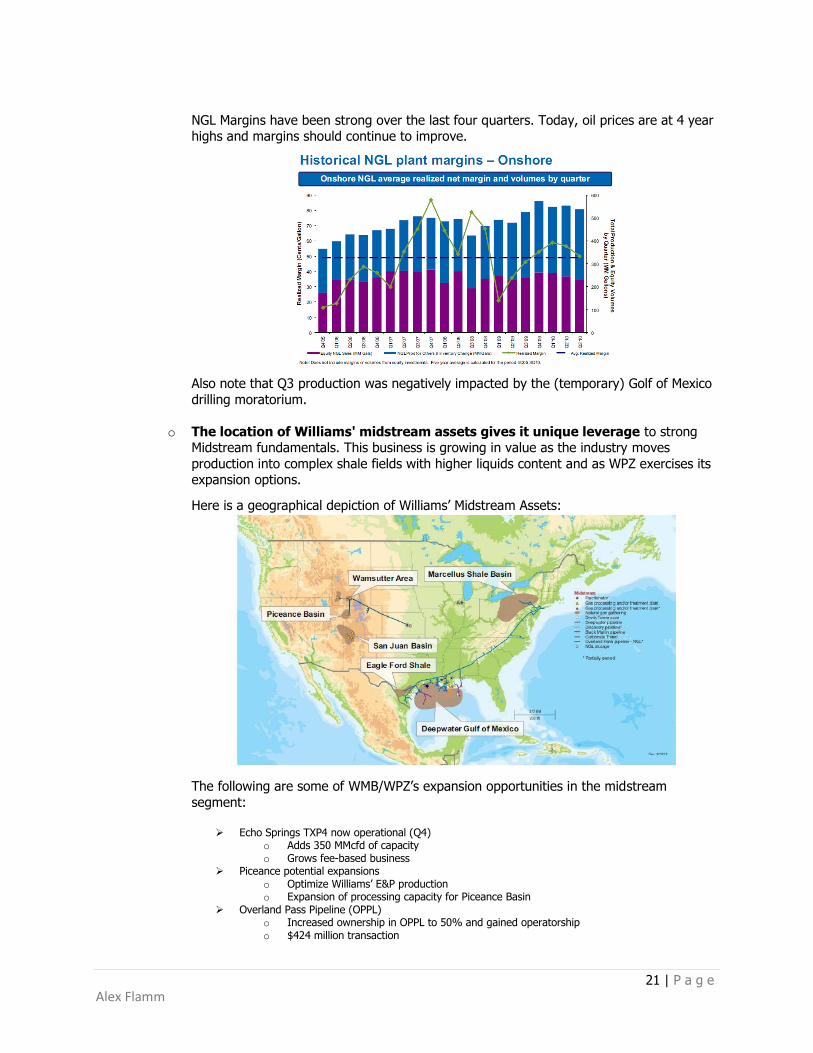

o The location of Williams' midstream assets gives it unique leverage to strong Midstream fundamentals. This business is growing in value as the industry moves

production into complex shale fields with higher liquids content and as WPZ exercises its expansion options.

Here is a geographical depiction of Williams‟ Midstream Assets:

The following are some of WMB/WPZ‟s expansion opportunities in the midstream

segment:

Echo Springs TXP4 now operational (Q4) o Adds 350 MMcfd of capacity o Grows fee-based business

Piceance potential expansions o Optimize Williams‟ E&P production o Expansion of processing capacity for Piceance Basin

Overland Pass Pipeline (OPPL) o Increased ownership in OPPL to 50% and gained operatorship o $424 million transaction

22 | P a g e Alex Flamm

o 760-mile NGL pipeline from Opal to Conway, along with 150- and 125-mile extensions into the Piceance and DJ Basins in Colorado

o Nearly full now; expandable to 255,000 bbls o Partnership will work together to facilitate expansions

Marcellus and Surrounding Region o Own storage facilities and compressor stations in the Marcellus. o Laurel Mountain Midstream

WPZ-Midstream has a 51% ownership interest in LMM Operated by Williams 1,000 miles of intrastate gathering lines in Western Pennsylvania for Atlas Energy

and other third parties Ultimately building 400 miles of 6-inch to 24-inch diameter gathering pipeline

targeting Marcellus production, providing LMM with over 1.5 Bcfd of capacity Provides gathering service to anchor customer – Atlas Energy– for 4,620

producing wells Atlas has announced a drilling program of approximately 1,000

horizontal wells over the next 5 years. Current system has average throughput of approximately 105-120 MMcfd Shamrock compressor station will add 60 MMcfd of capacity, expandable to 350

MMcfd Ongoing evaluation of new project opportunities in the area of interestOwn

Laurel Mountain Midstream piece o Springville Gathering System

Extends our existing Marcellus position into NE Pennsylvania and brings additional volumes into Transco

Long-term agreement to provide high pressure gathering and transportation services to Cabot Oil & Gas

Building a 32.5-mile, 24-inch natural gas gathering pipeline 100% of the right-of-way has been acquired Initial volumes to be gathered from central delivery point from third-party low

pressure gathering system in Susquehanna County; will deliver to Transco pipeline in Luzerne County

Expected in service in mid-2011 o Significant opportunities to service third-party producers as Marcellus production grows o Identified more than 85 potential counterparties, mostly producers in the Marcellus

Approximately 30 confidentiality agreements in place o Gas processing, NGL logistics and gas blending o Keystone Connector Pipeline

Drive value to WPZ-Gas Pipeline Gulf Of Mexico

o Perdido Norte 265 MMcf/d, 107 Mile, 18” Deepwater Gas Gathering 150 MBbls/d, 77 Mile, 18” Deepwater Oil Gathering 200 MMcf/d expansion at Markham Plant Major customers

BP Chevron Shell

Eagle Ford o Markham processing facility (off Transco) well positioned to capture Eagle Ford Shale

volumes via McMullen lateral pipeline extension

o Increased demand for and value of natural gas infrastructure provides a tailwind to the parent company. Given that permitting, sighting, and building energy

infrastructure assets has become increasingly difficult in recent years, Williams‟ pipeline

infrastructure assets and its growth opportunities are unique and increasingly valuable.

Williams' Pipeline Segment:

Transco is the nations largest gas pipeline system. It is an interstate natural gas transportation company that owns and operates a 10,000 mile natural gas pipeline system extending from Texas, Louisiana, Mississippi and the offshore Gulf of Mexico through Alabama, Georgia, South Carolina, North Carolina, Virginia, Maryland, Pennsylvania, and New Jersey to the New York City metropolitan area. The mainline is fully contracted/subscribed. Assets include

o 8.6 Bcf/d of peak-design capacity

23 | P a g e Alex Flamm

o Provide 50% of firm contract capacity into New York City o Rate base $2.9 billion (RP 06-569) o New pipeline and storage interconnects totaling 18.8 Bcf/d (2006 - 10), including Barnett,

Haynesville, Eagle Ford and Marcellus shales Transco expansion projects include Sentinel Expansion Project, Mobile Bay South Expansion Project, Mobile Bay South II Expansion Project, 85 North Expansion Project, Mid-South Expansion Project, Mid-South Expansion Project, Mid-Atlantic Connector Project and Rockaway Delivery Lateral Project.

85 North Phase II o Expansion from Station 85 to markets in Zone 5 adding 218.5 MDth/d of

capacity o Major customers: Southern Company, Progress Energy, Duke; Average

Contract term: 19 years o Target in-service: May 2011 (Phase II); Total estimated cost: Approximately

$205.5 million o Phase I (Constellation; 90 MDth/d; $34.5MM) placed into service July 2010

Bayonne Delivery Lateral o Delivery Lateral from Transco mainline in Essex County, N.J. to the

proposed Bayonne Energy Center in Bayonne, N.J. o Target in-service: June 2011; Total estimated cost: Approximately $20

million (Reimbursable) Mobile Bay South II

o Additional expansion of north to south capacity from Station 85 to Gulfstream of 380 MDth/d

o Target in-service: May 2011; Total estimated cost: Approximately $36 million

Northwest Pipeline is an interstate natural gas transportation company that owns and operates a natural

gas pipeline system extending from the San Juan basin in northwestern New Mexico and southwestern Colorado through Colorado, Utah, Wyoming, Idaho, Oregon, and Washington to a point on the Canadian border near Sumas, Washington. Northwest Pipeline provides services for markets in California, Arizona, New Mexico, Colorado, Utah, Nevada, Wyoming, Idaho, Oregon, and Washington directly or indirectly through interconnections with other pipelines. As of December 31, 2009, Northwest Pipeline‟s system, having long-term firm transportation agreements including peaking service of approximately 3.7 Bcf of natural gas per day, was composed of approximately 3,900 miles of mainline and lateral transmission pipelines and 41 transmission compressor stations having a combined sea level-rated capacity of approximately 473,000 horsepower. Assets include:

o 3,900 miles of pipeline and 41 compressor stations o 2 storage facilities o Rate base $1.5 billion (RP 06-416) o 13 Bcf of capacity o 709 MMcf/d of withdrawal capability

Northwest Pipeline expansion projects include Colorado Hub Connection Project and Sundance Trail Expansion.

24 | P a g e Alex Flamm

Sundance Trail

o 16 mile, 30-inch loop between Green River, Wyo., and Muddy Creek, Wyo., compressor stations

o Upgrade and replace compression at the Vernal compressor station to enhance system reliability

o 150 MDth/d capacity from Meeker/Greasewood, Colo., hubs to Opal, Wyo., hub for a contract term of 12 years

o Major customers: Williams Gas Marketing o Total estimated cost: Approximately $56 million o Target in-service: Nov. 2010