WITHER EXPORTS IN THE NEXT FIVE YEARS · 1 Interactive forum on WITHER EXPORTS IN THE NEXT FIVE...

25

1 Interactive forum on WITHER EXPORTS IN THE NEXT FIVE YEARS Organized by EASL Spice Sector FAZAL MUSHIN Director – Exports & Biz Dev. Link Natural Products (Pvt) Ltd Sri Lanka E-mail : [email protected]

Transcript of WITHER EXPORTS IN THE NEXT FIVE YEARS · 1 Interactive forum on WITHER EXPORTS IN THE NEXT FIVE...

1

Interactive forum on

WITHER EXPORTS IN THE NEXT FIVE YEARS

Organized by EASL

Spice Sector

FAZAL MUSHIN Director – Exports & Biz Dev.Link Natural Products (Pvt) LtdSri LankaE-mail : [email protected]

Agricultural sector - 2012

• Total land under cultivation : 2, 645,000 ha (42.2%)

• Agricultural contribution for total GDP : 9.27%

• Spice crop production : 74,104 ha / GDP 0.14%

Cinnamon

Pepper

Clove

Nutmeg & Mace

Cardamom

2

3

Land Extent 2005(Ha)

2012(Ha)

% increase / Decrease

Nutmeg 1,070 978 -9%

Clove 7,779 7,612 -2.1%

Black Pepper 29,156 31,667 9%

Cinnamon 27,895 31,049 11%

Cardamom 2,888 2,798 -3%

Comparison of production of 2005 vs 2012

Production 2005(MT)

2012(MT)

% increase / Decrease

Nutmeg 1,865 2,002 7%

Clove 6,093 4,009 -34%

Black Pepper 14,265 18,604 30%

Cinnamon 15,895 17,165 8%

Cardamom 80 80 0%Source : SAPPTA Annual Report

Source : SAPPTA Annual Report

Growth of Production and export volumeNutmeg

Clove

Black Pepper

Cinnamon

Cardamom

5

Local Consumption - 2012

Commodity Consumption (MT)

Nutmeg 327

Pepper 6,807

Clove 690

Cardamom 64

Cinnamon 5,211

Source : DEA

Productivity in 2012 (Sri Lanka)

6

Commodity kg/Ha kg/Ha

Nutmeg 2,000 5,000

Clove 500 200

Black Pepper 600 1,700 - 2,550

Cinnamon 600 1,200

Cardamom 30 250

Source : SAPPTA Source : DEA Stats

7

Average cost of production - 2012

Average Farm Gate Prices (Rs)

Commodity Cost of Production (Rs/kg)

Cost of Production vs farm gate prices (%)

Nutmeg 249.07 236

Clove 368.61 214

Pepper 230.86 260

Cinnamon 692.9 50

Cardamom 985.0 97

Commodity 2005 2006 2007 2008 2009 2010 2011 2012

Nutmeg 244.88 235.36 278.12 316.23 331.87 459.62 742.53 838

Clove 347.94 480.53 471.97 471.97 484.66 542.99 1,250.35 1,160

Pepper 116.89 165.38 306.6 324.92 287.43 342.14 691.9 832

Cinnamon 395.48 431.09 599.62 664.35 621.95 726.57 921.9 1,042

Cardamom 744.15 716.92 913.25 1,718.27 1,732.32 3,320.96 2,713.12 1,946

Source : DEA

Source : SAPPTA Annual Report

Export performance

8

Export Value 2005(Rs bn)

2012(Rs bn)

% increase / Decrease

Total 9.4 30.2 221%

Export Volume 2005(MT)

2012(MT)

% increase / Decrease

Nutmeg 1,925 1,551 -19%

Clove 4,198 1,404 -67%

Black Pepper 7,821 10,825 38%

Cinnamon 12,365 14,435 17%

Cardamom 11 9 -18%

Source : SAPPTA Annual Report

Ex Rate 100.49 Ex Rate 127.60

Note: rupee value has been depreciated by 27%

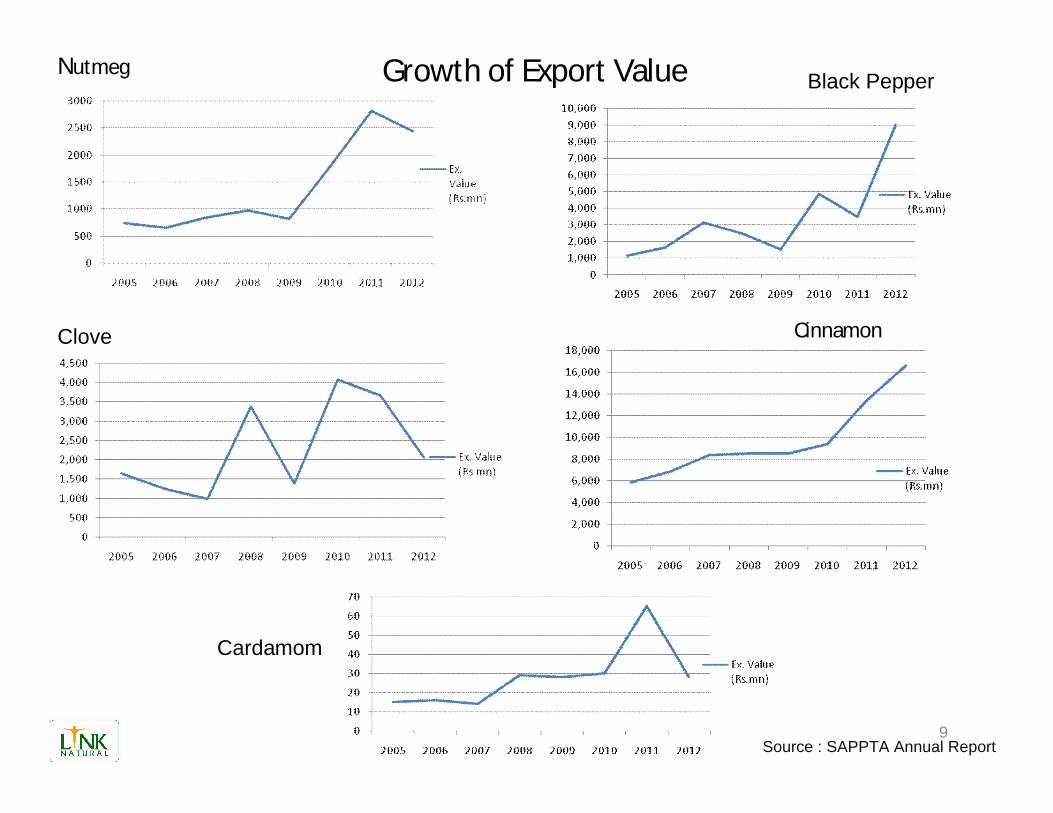

Nutmeg

9

Growth of Export Value

Clove

Black Pepper

Cinnamon

Cardamom

Source : SAPPTA Annual Report

Composition of main spice exports -2012

10

Source : Spice Sector report – CCC

Global Production of Spices and Sri Lanka's Contribution - 2012

Commodity Production (MT) SL contribution %

Pepper (Green, Light, Bold)

White pepper

Pepper light berries

342,590 3

Nutmeg BWP

Nutmeg whole

15,000 13

Cinnamon 15,000 90

Cloves 120,000 3.34

Source : Spice Board of India/ IPC

Growth of Export Volume

12

Commodity 2009(MT)

2010(MT)

2011(MT)

2012(MT)

Nutmeg Oil 23 13 22 25Clove Oil 1.5 14 13 3

Black pepper Oil 0.05 5 8 12Cinnamon Leaf Oil 107 155 231 318Cinnamon Bark Oil 7 7 8 9Cardamom Oil 0 0.3 1 0.8

Growth of Export Value

2009(Rs Mn)

2010(Rs Mn)

2011(Rs Mn)

2012(Rs Mn)

Total 312.5 687.0 1,354 1,430Growth Y/Y % 120 % 97% 6%

Essential Oil

13

Composition of main Essential Oil exports -2012

Source : SAPPTA annual report 12/13

14

Major destinations of Essential oils

15

•USA

•UK

•France

•India

•Germany

Major destinations of Spices

•India

•Germany

•Middle East

• North & South America

Total Spice sector value

16

Sector 2009(Rs Mn)

2010(Rs Mn)

2011(Rs Mn)

2012(Rs Mn)

Spices12,287 20,175 23,446 30,202

Essential oil 312.5 687.0 1,354.0 1,430.0

Total 12,599.5 20,862 24,800 31,632

Growth y/y(%)

65 % 19% 27 %

** The industry vision is to reach 100,000 Mn by 2020

• Increase productivity

• Lack of long term backward integration & collectivization

• Lack of initiatives for moving up the value chain

• Marketing

• Legislative hurdles

17

Challenges in the industry

Challenges in the industry

• Increase productivity

70% are small holder family farms 1 to 2 acers

Acceptable post harvest practices – GMP/ Quality parameters

Better agronomic practices

• Lack of long term backward integration & collectivization

Establishing effective supply chain and linkages between all players in the industry

Producers

Collectors

Exporters

Processers

18

• Lack of initiatives for moving up the value chain

Focused R&D

Cost of Technology inputs

Product development

• Marketing

High cost of establishing brands

Private labeling

Organic products

• Legislative hurdles

19

Challenges in the industry cnt..

• Increasing productivity

• Product diversification - Identify emerging new products / markets

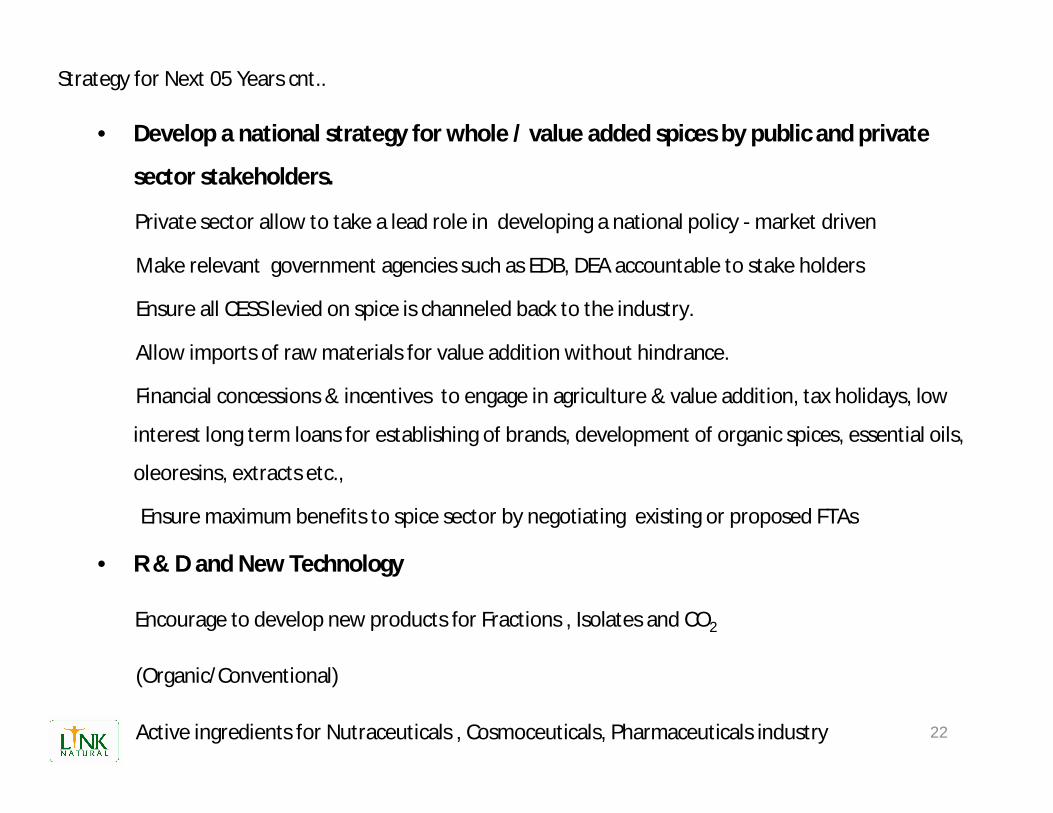

• Develop a national strategy for whole / value added spices by public and private sector stakeholders.

• R & D and New Technology

20

Strategy for Next 05 Years

Strategy for Next 05 Years

• Increasing productivity

Engage plantation companies to grow new crops and expanding the existing cultivation in

spices.

Introduce better agronomic practices to small holder farmers.

• Product diversification & Marketing - Identify emerging new products / markets

Market research

Establishment of brands & financial support

Private labeling contracts

Ground Spices , Spice mixes, beverages

Continuous support of participation in sectoral & brands (not the country wise)

21

• Develop a national strategy for whole / value added spices by public and private

sector stakeholders.

Private sector allow to take a lead role in developing a national policy - market driven

Make relevant government agencies such as EDB, DEA accountable to stake holders

Ensure all CESS levied on spice is channeled back to the industry.

Allow imports of raw materials for value addition without hindrance.

Financial concessions & incentives to engage in agriculture & value addition, tax holidays, low

interest long term loans for establishing of brands, development of organic spices, essential oils,

oleoresins, extracts etc.,

Ensure maximum benefits to spice sector by negotiating existing or proposed FTAs

• R & D and New Technology

Encourage to develop new products for Fractions , Isolates and CO2

(Organic/Conventional)

Active ingredients for Nutraceuticals , Cosmoceuticals, Pharmaceuticals industry 22

Strategy for Next 05 Years cnt..

Coleus Sandalwood Patchouli

Turmeric VetiverDavanaGinger

Potential new crops23

Value added products

24

FAZAL MUSHIN Director – E & BDLink Natural Products (Pvt) LtdSri LankaE-mail : [email protected]

THANK YOU

25