Will Lent, Research & Policy Analyst, Solar Energy...

32

Will Lent, Research & Policy Analyst, Solar Energy Industries Association Andrew Krulewitz, Solar Analyst; Editor, PVNews, GTM Research Cory Honeyman Solar Analyst, GTM Research June 27, 2013

Transcript of Will Lent, Research & Policy Analyst, Solar Energy...

Will Lent, Research & Policy Analyst, Solar Energy Industries Association Andrew Krulewitz, Solar Analyst; Editor, PVNews, GTM Research Cory Honeyman Solar Analyst, GTM Research

June 27, 2013

Antitrust Reminder As a trade association of competitors, SEIA must comply with and be mindful of antitrust laws. It is important that competitively sensitive matters are not discussed on this call, including product prices or costs; sales terms or conditions; production levels; sales territories; marketing plans; industry forecasts; or bid terms. If any such topic is raised, I will stop the conversation and, if necessary, end the call. For more information, SEIA’s antitrust guidelines are available on our website.

June 25, 2013 © 2013 Solar Energy Industries Association® 2

About SEIA • Founded in 1974

• U.S. National Trade Association for Solar Energy • 1,000 member companies from around the world • Members from across 50 states • Largest companies in the world as well as small

installers • Our Mission: Build a strong solar industry to power

America

• Our Goal: 10 gigawatts (GW) of annual installed solar capacity in the U.S. by 2015

June 25, 2013 © 2013 Solar Energy Industries Association® 3

Solar in America: Strong and Getting Stronger • 119,000 American workers in solar – more than double the

number in 2009 – at 5,600 companies across the country

• One of the fastest growing sectors of the U.S. economy – 2012 installations grew 76% over 2011

• Q1 2013 was the largest first quarter on record. PV market installed 723 MW, growing 33% over last year

• Over 8,500 MW of cumulative installed solar electric capacity, enough to power 1.3 million average American homes

June 25, 2013 © 2013 Solar Energy Industries Association® 4

U.S. Solar Business Locations

June 25, 2013 © 2013 Solar Energy Industries Association® 5

Solar Market Insight: Q1 2013 • Detailed data on markets in

top 28 states plus DC available in full report.

• Free executive summary provides national aggregate data on installations, pricing, manufacturing and demand forecasts.

• Full report for sale (50% discount to SEIA members) includes quarterly forecasts as well as detailed market segment and state data.

June 25, 2013 © 2013 Solar Energy Industries Association® 6

SEIA/GTM Research Partnership • Industry need for up-to-date and reliable market data

– Market reports issued every quarter

• Member discount: benefit for SEIA members – Reliable market intelligence

– Member discount makes SMI the most affordable market research available

• Data to support SEIA’s advocacy mission • SEIA-GTM conferences • Email questions to [email protected] or

June 25, 2013 © 2013 Solar Energy Industries Association® 7

Solar Continues to Boom- 723 MW Installed in Q1 2013

June 25, 2013 © 2013 Solar Energy Industries Association® 8

0

1000

2000

3000

4000

5000

6000

2006 2007 2008 2009 2010 2011 2012 2013

Inst

alle

d C

apaci

ty (M

W)

Annual Q1 Q2 Q3 Q4 Projected

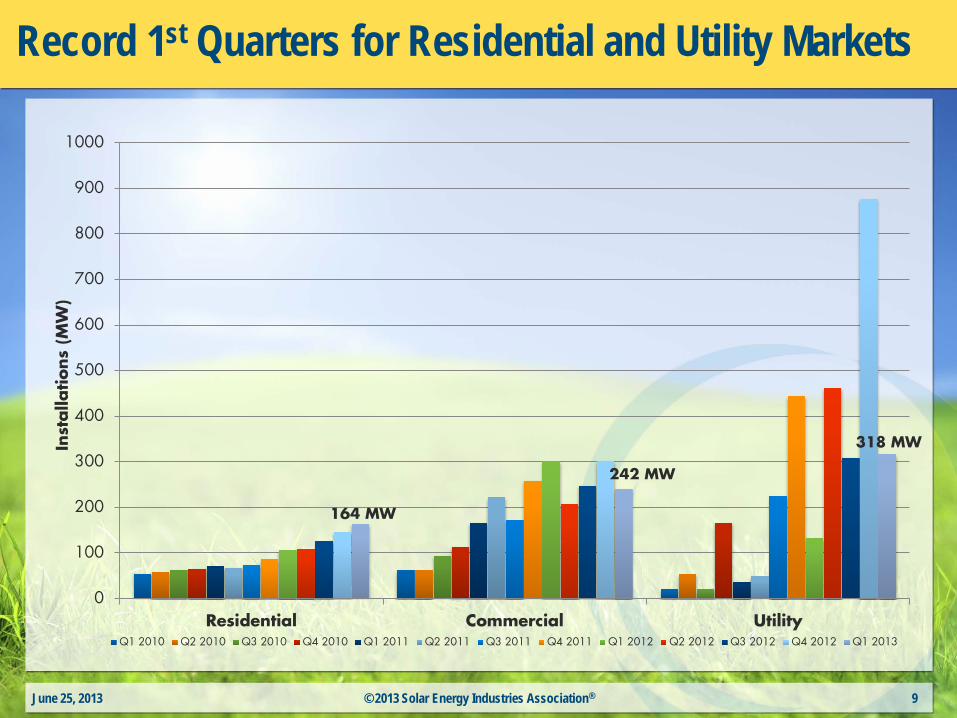

Record 1st Quarters for Residential and Utility Markets

June 25, 2013 © 2013 Solar Energy Industries Association® 9

164 MW

242 MW

318 MW

0

100

200

300

400

500

600

700

800

900

1000

Residential Commercial Utility

Inst

alla

tions

(MW

)

Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013

System Prices Continue to Fall

• Average system prices fell by 24% in the past year

June 25, 2013 © 2013 Solar Energy Industries Association® 10

$-

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013Q1

$/W

Average Weighted System Price

LBNL "Tracking the Sun IV" SEIA/GTM Research

Price Declines Driving Growth

June 25, 2013 © 2013 Solar Energy Industries Association® 11

$-

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Ave

rage

Syst

em P

rice

($/W

)

Inst

alle

d C

apaci

ty (M

W)

Installations Projected Average System Price

Average Residential System Price Below $5.00/W

June 25, 2013 © 2013 Solar Energy Industries Association® 12

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

($/W

)

Average Residential System Price by State- Q1 2013

Average Commercial System Below $4.00/W

June 25, 2013 © 2013 Solar Energy Industries Association® 13

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

($/W

)

Average Commercial System Price by State- Q1 2013

Q1 2013 State Performance

• 8 states installed 10 MW or more

• CA had the strongest 1st quarter in history

• NJ’s commercial market rebounded to lead the nation in Q1 2013

June 25, 2013 © 2013 Solar Energy Industries Association® 14

76 MW

44 MW

408 MW

10. Florida

9. Pennsylvania

8. Colorado

7. Tennessee

6. Massachusetts

5. North Carolina

4. Arizona

3. Hawaii

2. New Jersey

1. California

Residential Commercial Utility

What to Expect For the Rest of 2013

• More than 4,400 MW of PV will come online in 2013

• Residential market to show the most significant growth

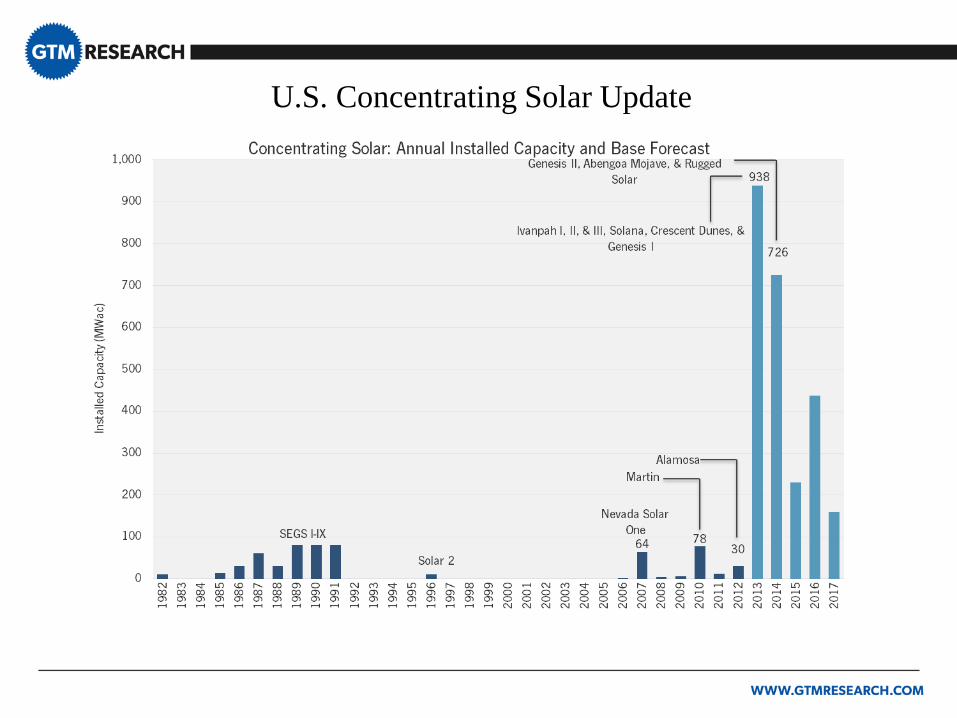

• 2013 will be a record year for CSP as 938 MW is expected to be commissioned

June 25, 2013 © 2013 Solar Energy Industries Association® 15

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2012 2013E

Inst

alle

d C

apaci

ty (

MW

)

2012 vs. 2013E PV Installations

Residential Non-Residential Utility

U.S. PV Market Forecast- 30% Growth in 2013

June 25, 2013 © 2013 Solar Energy Industries Association® 16

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

2010 2011 2012 2013E 2014E 2015E 2016E

Inst

alle

d C

apaci

ty (M

W)

2013 Will Be An Historical Year for CSP

June 25, 2013 © 2013 Solar Energy Industries Association® 17

-

100

200

300

400

500

600

700

800

900

1,000

Inst

alle

d C

ap

aci

ty (

MW

)

U.S. CSP Installations and Forecast

Installations Forecast

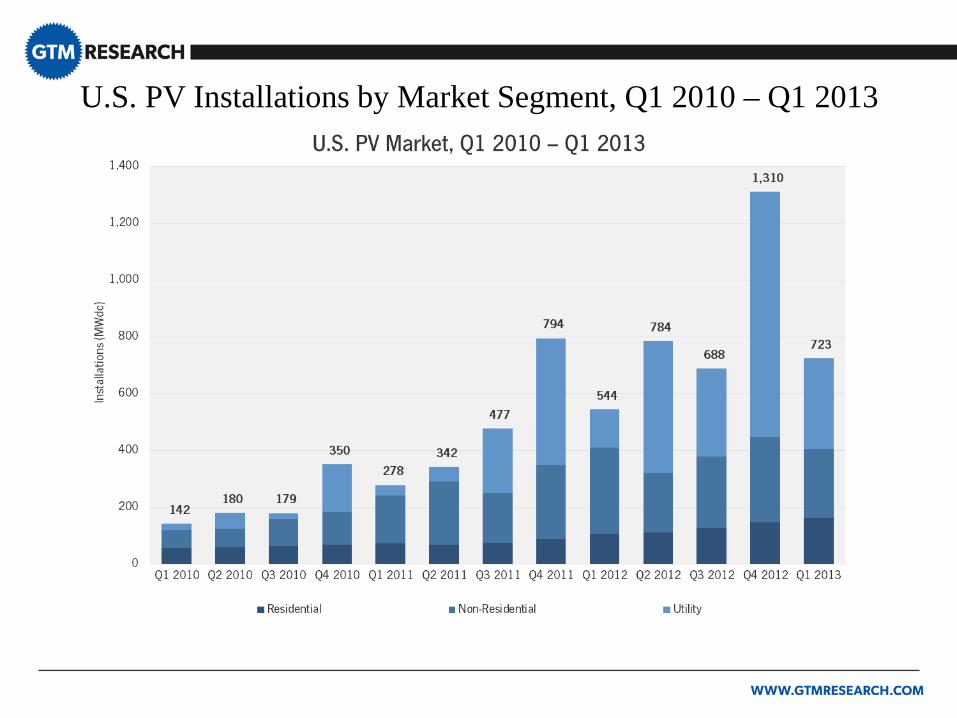

U.S. PV Installations by Market Segment, Q1 2010 – Q1 2013

Market Segment Trends, Q1 2012 – Q1 2013 • The residential market

continued its steady and incremental growth, up 11% quarter-over-quarter

• Commercial installations

dipped 20% compared to last quarter; NJ was the only major market to see growth

• The utility market dropped quarter-over-quarter, primarily supported by 276.8 MW installed in CA

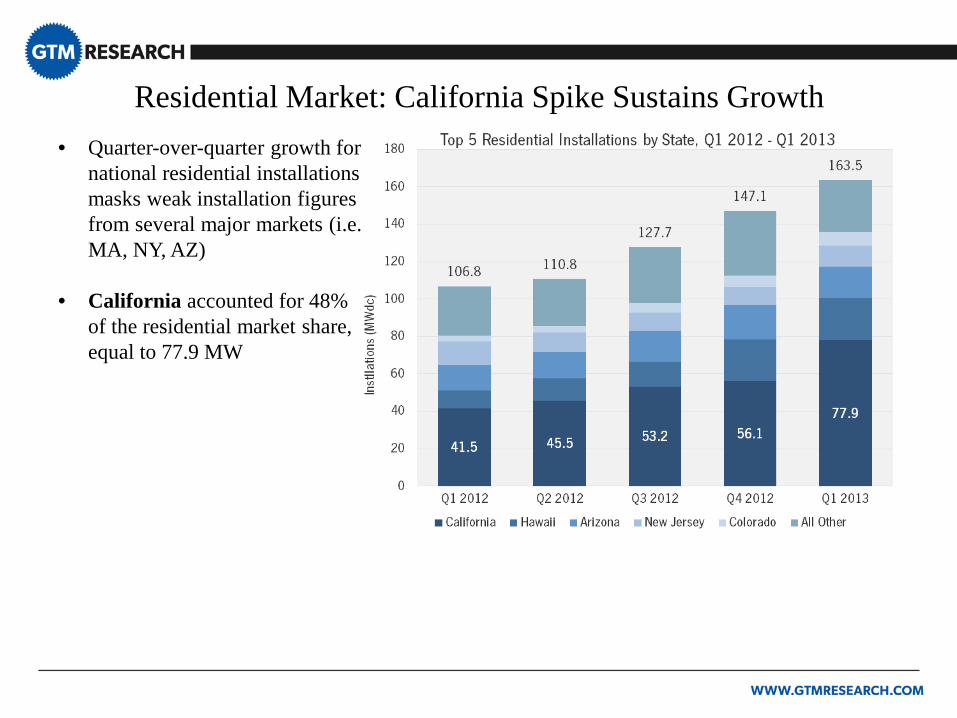

Residential Market: California Spike Sustains Growth

• Quarter-over-quarter growth for national residential installations masks weak installation figures from several major markets (i.e. MA, NY, AZ)

• California accounted for 48% of the residential market share, equal to 77.9 MW

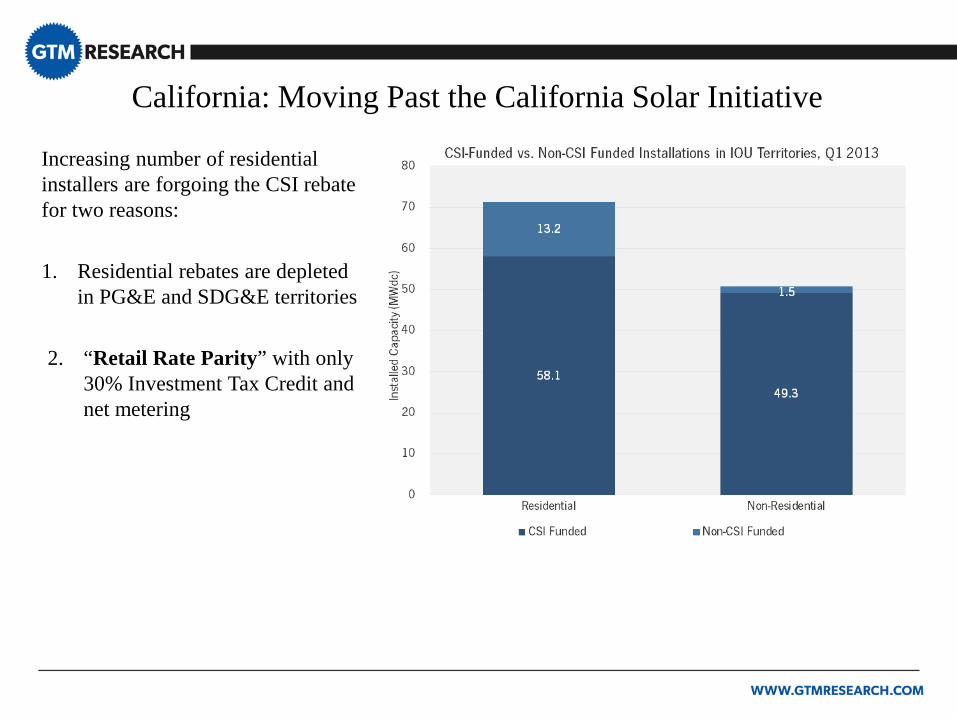

California: Moving Past the California Solar Initiative

Increasing number of residential installers are forgoing the CSI rebate for two reasons: 1. Residential rebates are depleted

in PG&E and SDG&E territories 2. “Retail Rate Parity” with only

30% Investment Tax Credit and net metering

Third-Party Financing Continues to Drive Installs • Prevalence of third-party

owned (TPO) systems continues to drive new residential installations in major state markets

• CO hit a U.S. record

TPO market share of 91%

• Despite diminishing rebates in states like CA, HI, and MA, residential solar is increasingly competitive with retail electricity rates

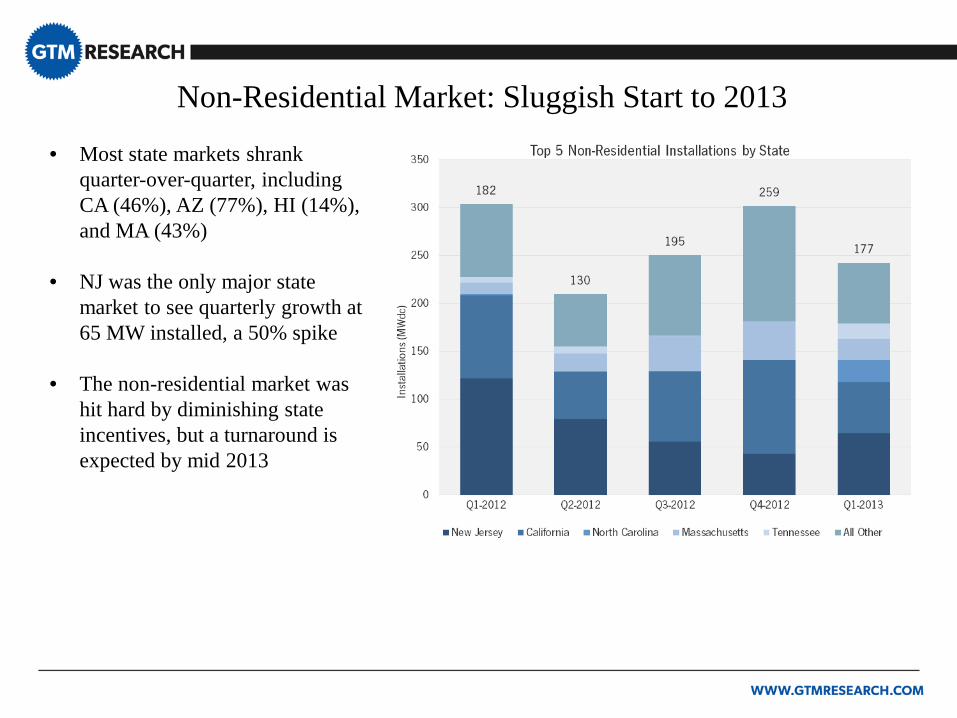

Non-Residential Market: Sluggish Start to 2013

• Most state markets shrank quarter-over-quarter, including CA (46%), AZ (77%), HI (14%), and MA (43%)

• NJ was the only major state market to see quarterly growth at 65 MW installed, a 50% spike

• The non-residential market was hit hard by diminishing state incentives, but a turnaround is expected by mid 2013

U.S. Utility Market – Top 10 Q1 Projects Completed

Project Name Developer Capacity (MWdc) State Power Offtaker EPC Firm

Antelope Valley Solar Ranch One – Phase II First Solar 79 CA Pacific Gas &

Electric First Solar

Alpine Solar Project NRG Energy 76 CA Pacific Gas & Electric First Solar

Catalina Solar – Phase I EDF Renewable Energy 67 CA San Diego Gas &

Electric Bechtel

Borrego Springs Solar I NRG Energy 30 CA San Diego Gas & Electric

Sunora Energy Solutions

SPS Atwell Island Samsung America, ENCO 23 CA Pacific Gas &

Electric Quanta Services

APS AZ Sun – Foothills Solar Plant – Phase 1

Arizona Public Service 15 AZ Arizona Public

Service AMEC

Fuquay Farm Strata Solar, Canadian Solar 6 NC Progress Energy

Carolinas Strata Solar

Kalaeloa Solar One Keahole Solar Power 6 HI Hawaiian Electric

Company -

Belwood Solar Farm Strata Solar 5 NC Duke Energy Carolinas Strata Solar

Southern Vermont Energy Park Solar

SVEP Solar Project Company 3 VT - RGS Energy

U.S. Utility Market Pipeline

• 318 MW of utility scale solar were installed in Q1 2013

• 24 projects became operational, ranging from 1 MW to 79 MW

• Four of the top five installations were early phases of larger projects to be completed over the next two years

Emerging Demand: New State Solar Incentive Programs

State Administrator Program Type Program

Size Compliance

Period Qualifying Facilities Bids/Incentiv

e/Funding Levels

California Utility: LADWP

Feed-in Tariff 150 MW 2013 10-14 MW Bid Cap: $0.14/kWh

Utility-Scale RFP 200 MW 2013 50 MW Bid Cap: $0.85/kWh

Colorado Utility: Xcel Energy

Annual Compliance Plan 33.6 MW 2013

Residential – Customer Owned (<10 kW)

Incentive: $0.11/kWh

Residential – Third Party Owned (<10 kW)

Incentive: $0.07/kWh

Massachusetts Government Solar Carve-Out (State RPS) 1,600 MW 2014-2020

Residential (<6 MW) SREC Market Non-Residential (<6 MW) SREC Market

Minnesota Government Solar Carve-Out (State RPS) 450 MW 2014-2020

120% of DG customer's on-site annual electric energy consumption

Funding: $5 million/year (next 5 years)

120% of DG customer's on-site annual electric energy consumption (in-state manufactured system)

Funding: $15 million/year (next 10 years)

Four Year PV Market Outlook

Four Year PV Market Outlook by Market Segment

Average Installed Prices Continue to Decline

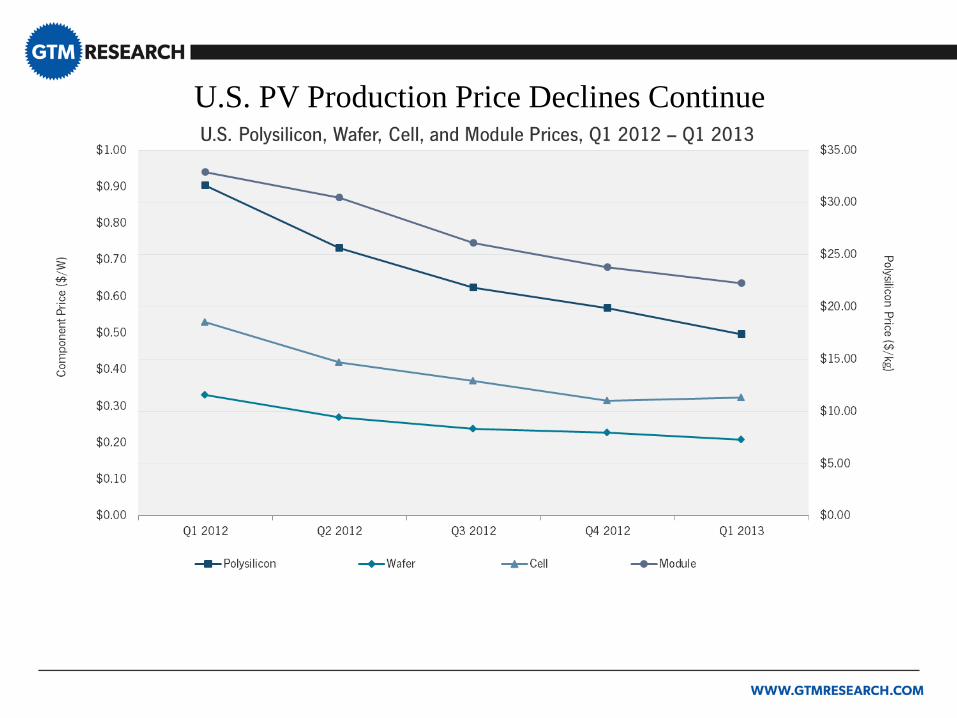

U.S. PV Production Price Declines Continue

U.S. Concentrating Solar Update

Thank You & Contact Info

Justin Baca, Director of Research Will Lent, Research and Policy Analyst

Contact: [email protected]

Andrew Krulewitz, Solar Analyst Cory Honeyman, Solar Analyst Contact: [email protected]

For more information about purchasing the full SEIA/GTM Research U.S. Solar Market Insight Q1 2013™ report, please visit www.gtmresearch.com/ussmi or email Justin Freedman ([email protected])