Why Has Papua New Guinea Been Successful in … Has Papua New Guinea Been Successful in Producing...

22

Why Has Papua New Guinea Been Successful in Producing Oil and Gas Michael McWalter, SEAPEX Exploration Conference 2017, Singapore When we examine the ingredients required for the development of petroleum accumulations, Papua New Guinea has all that is required, though we do not necessarily know the links between all of them. But the evidence of petroleum endowment is manifest, widespread, and substantial. Oil abounds in PNG; we know this from the oil seeps first identified by gold prospectors in 1911 along the Vailala River in the Gulf Province, to the seeps in the Nipa Valley in the Southern Highlands - used traditionally as body paint and as a kerosene substitute, and sold in the local market, and from the Matapau oil seeps in the Wewak Basin of the East Sepik, which hosted PNG’s first oil production pre-World War Two, or the greenish-yellow oil that oozes out of the ground at Wonia, south of the Fly River in the vast Western Province. There is nothing quite like the presence of oil to excite oilmen, and that is what PNG has done for over a hundred years. The commercial oil accumulations and seeps found in the Papuan Basin before 1992 have been attributed to Jurassic sources, with peak generation occurring in the Late Cretaceous prior to the formation of the existing structures. However, in 1992, an oil seep was discovered at Lufa in the Eastern Highlands after a series of earthquakes. This oil is geochemically very different to all the other oils found in the Papuan Basin. It was found to the north and east of the present oil discoveries that occur within the western Papuan Basin and it is indicative of an undiscovered Tertiary source rock, which is currently at or near peak generation. However, most of this likely source rock in the north may be covered by overthrusted allochthonous terrain, and this play remains to be properly explored. There is no doubt that we have plenty of structure as evidenced by the surface topography and terrains, whale-back mountains and the overall formidable geography of the island of New Guinea. The mainland of Papua New Guinea has been formed by interaction between the Australian Plate in the southwest, and the Pacific Plate in the northeast. Between these two major crustal elements: the platform, and the oceanic crust and island arcs, lays a highly-deformed mobile belt. It is arguably one of the most tectonically complex regions of the world and is host to an abundance of the known tectonic processes: including the opening and closing of ocean basins, terrane accretion, ophiolite obduction, subduction reversal, and ultrahigh-pressure rock exhumation. For the oil man, the evidence of extensional systems of late Triassic and Palaeocene age, an extensive Mesozoic passive margin, abundant Palaeogene shelf sedimentation, and Miocene carbonate deposition, all overwritten by late Miocene- Pliocene collision - which produced the present day Papuan Fold and Thrust Belt, and Papuan Foreland provide the essential structural ingredients and key sediments within which oil and gas may accumulate. The late Jurassic/early Cretaceous sands form excellent reservoirs, such as the Toro Sandstone and Digimu Sandstone, as do the vuggy Miocene carbonate reefs. The Pliocene

Transcript of Why Has Papua New Guinea Been Successful in … Has Papua New Guinea Been Successful in Producing...

Why Has Papua New Guinea Been Successful in Producing Oil and Gas

Michael McWalter,

SEAPEX Exploration Conference 2017, Singapore

When we examine the ingredients required for the development of petroleum accumulations, Papua New Guinea has all that is required, though we do not necessarily know the links between all of them. But the evidence of petroleum endowment is manifest, widespread, and substantial.

Oil abounds in PNG; we know this from the oil seeps first identified by gold prospectors in 1911 along the Vailala River in the Gulf Province, to the seeps in the Nipa Valley in the Southern Highlands - used traditionally as body paint and as a kerosene substitute, and sold in the local market, and from the Matapau oil seeps in the Wewak Basin of the East Sepik, which hosted PNG’s first oil production pre-World War Two, or the greenish-yellow oil that oozes out of the ground at Wonia, south of the Fly River in the vast Western Province. There is nothing quite like the presence of oil to excite oilmen, and that is what PNG has done for over a hundred years.

The commercial oil accumulations and seeps found in the Papuan Basin before 1992 have been attributed to Jurassic sources, with peak generation occurring in the Late Cretaceous prior to the formation of the existing structures. However, in 1992, an oil seep was discovered at Lufa in the Eastern Highlands after a series of earthquakes. This oil is geochemically very different to all the other oils found in the Papuan Basin. It was found to the north and east of the present oil discoveries that occur within the western Papuan Basin and it is indicative of an undiscovered Tertiary source rock, which is currently at or near peak generation. However, most of this likely source rock in the north may be covered by overthrusted allochthonous terrain, and this play remains to be properly explored.

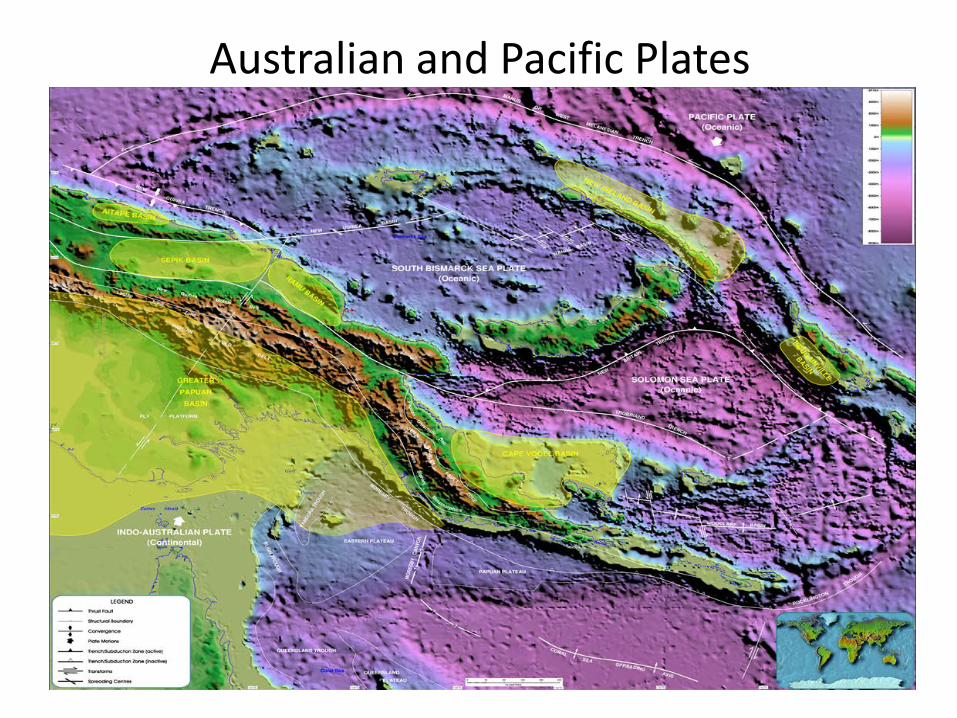

There is no doubt that we have plenty of structure as evidenced by the surface topography and terrains, whale-back mountains and the overall formidable geography of the island of New Guinea. The mainland of Papua New Guinea has been formed by interaction between the Australian Plate in the southwest, and the Pacific Plate in the northeast. Between these two major crustal elements: the platform, and the oceanic crust and island arcs, lays a highly-deformed mobile belt. It is arguably one of the most tectonically complex regions of the world and is host to an abundance of the known tectonic processes: including the opening and closing of ocean basins, terrane accretion, ophiolite obduction, subduction reversal, and ultrahigh-pressure rock exhumation.

For the oil man, the evidence of extensional systems of late Triassic and Palaeocene age, an extensive Mesozoic passive margin, abundant Palaeogene shelf sedimentation, and Miocene carbonate deposition, all overwritten by late Miocene- Pliocene collision - which produced the present day Papuan Fold and Thrust Belt, and Papuan Foreland provide the essential structural ingredients and key sediments within which oil and gas may accumulate.

The late Jurassic/early Cretaceous sands form excellent reservoirs, such as the Toro Sandstone and Digimu Sandstone, as do the vuggy Miocene carbonate reefs. The Pliocene

Orubadi and Upper Cretaceous Ieru Formations provide reasonable seals, though the faulting of these units due to the continued compression and reactivation of deep-seated faults means that their sealing integrity is not always assured.

Having all the ingredients of a petroleum system is a great starting point for our business, but that same geography that arises from the geological history has made onshore Papua New Guinea a formidable place in which to explore for oil and gas.

PNG has been likened to the European Alps where the snow has been removed and the land covered with dense rain forest. The mountains of PNG rise up to more than 4,500 metres above sea level and they are the subject of continued uplift. So, when continuous heavy rainfall amounting to as much as 10,000 millimetres per year in some places are dropped on the land, it is no small wonder that vast deltas and wetlands border much of the mainland..

Into this mix, were placed a strange and wide variety of amphibians, distinct and beautiful Birds of Paradise, one of the world’s greatest variety of insects and the most exotic Australasian fauna. And in some latter-day development, modern man who produced the first polished-stone axes some 15,000 years ago became frozen in isolated, early Neolithic, rival communities throughout the mainland and it surrounding islands. With land bridges gone after the last glacial period, only limited seagoing migration occurred along the coastal areas and life for most communities remain isolated for millennia.

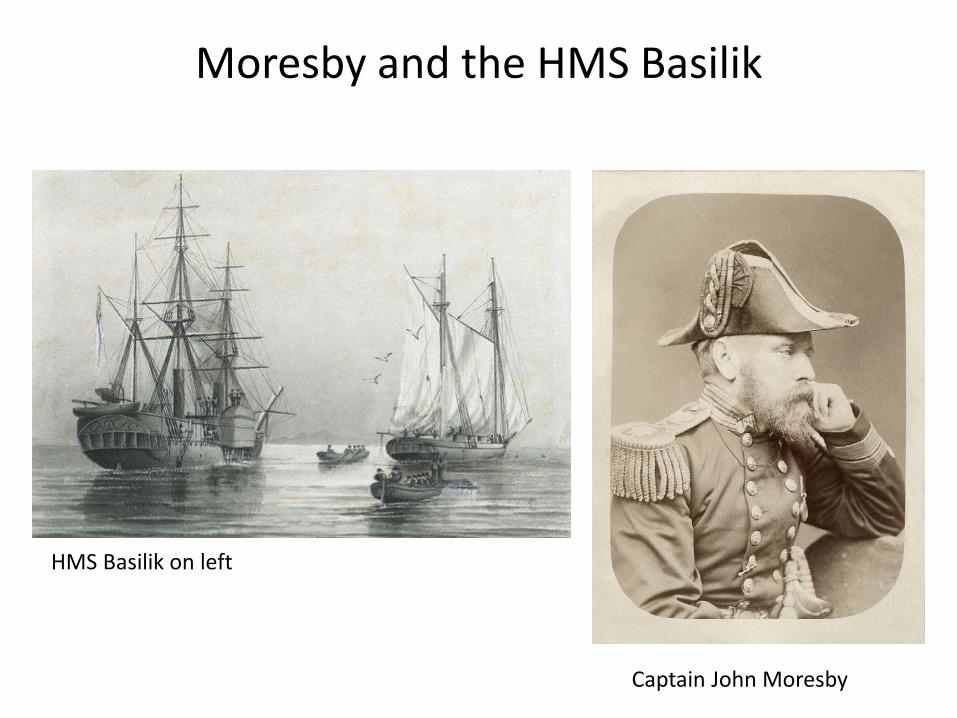

PNG was never conquered, though many navigators came to its shores from both Western and Eastern ports. No settlements were established and many adventurers were repelled by the local people. It was not until 1973, that Captain John Moresby of the Her Majesty’s Ship Basilik, which was conducting hydrographic surveys along the Papuan coast, found a navigable gap in the reef in front of a beautiful nature harbour. He named that harbour after his father, Admiral Sir Fairfax Moresby, calling it Fairfax Harbour - upon the shores of which Port Moresby was established. In 1883, the Government of Queensland annexed the territory for the British Empire. Oddly, the United Kingdom Government refused to ratify the annexation, but in 1884, a Protectorate was proclaimed over the territory, then called British New Guinea and on 18th March 1902, the Territory was placed under the authority of the Commonwealth of Australia. Resolutions of acceptance were passed by the Commonwealth Parliament, who accepted the territory under the name of Papua.

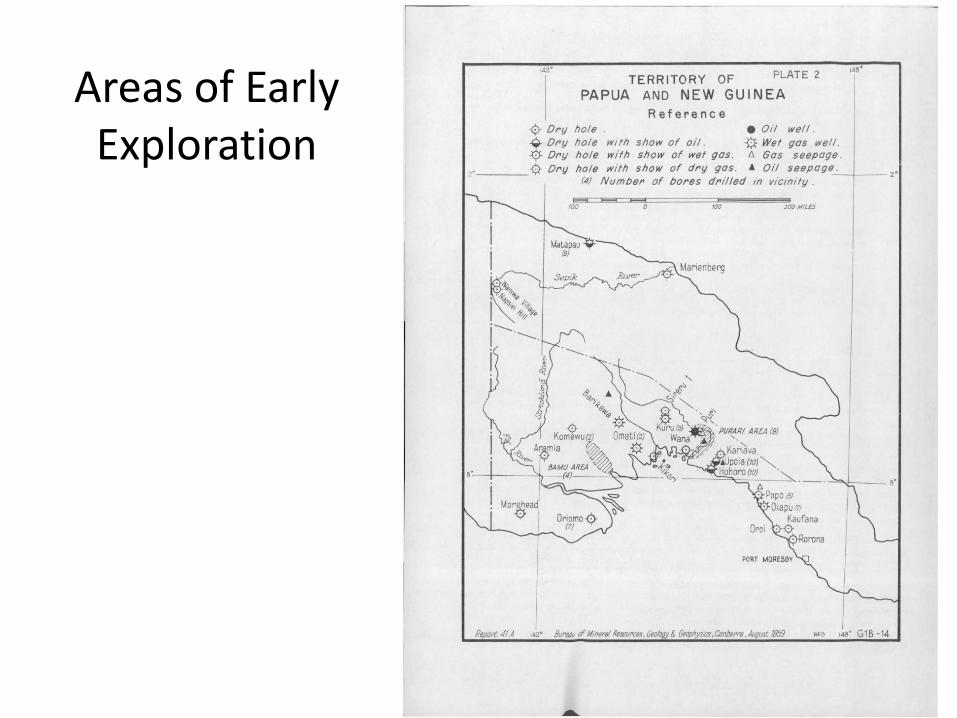

The new territory enticed adventurers and explorers and it was two gold prospectors, McGowan and Swanson, who in 1911 discovered the oil seeps along the lower reaches of the Vailala River. The Australian Government, aware of the success of the Anglo-Persian Oil Company (later called British Petroleum) in what we now call Iran, commissioned a report and engaged them to conduct exclusive oil exploration for the Government until 1929. This proactive approach perhaps endures to this day. Oil Search Ltd of Queensland joined the foray in 1929 becoming incorporated in Papua. Shell started exploring in 1936 and in 1938 Oil Search joined together with Anglo-Persian and Stanvac (Standard Oil of New York and Vacuum Oil which were later to become Mobil) to form the Australasian Petroleum Company which undertook epic and episodic exploration campaigns for decades searching for oil. Indeed, one well was spudded prior to World War Two, suspended for the duration of the War and only plugged and abandoned after the War.

For years, Oil Search raised money from gentlemen who wished to have a wager on finding oil in Papua by the sale of rights issues, but alas the discovery of commercially viable quantities of petroleum would remain elusive for decades more.

There were nevertheless enormous challenges to access those lands that were seen to be prospective for hydrocarbon accumulations, not the least of which was the formidable geography and the associated paucity of transportation infrastructure, but also the fiercely held manner of customary landownership of those lands. Customary or traditional land ownership was not of such concern during the pre-Independence years when the territory of Papua and New Guinea were jointly administered by the Australian Government. Natives were constrained by statutes such as the Native Board Ordinance of 1889, the Native Regulation Ordinance, 1908-1930, and the Native Administration (New Guinea) Ordinance 1951) and a series of Native Administration Regulations, which variously and inter alia provided for: “compulsory gardening in communities; prohibition of employment” and for offenders “whipping in lieu of any other punishment which may be lawfully awarded for that offence.”

IN the pre-Independence days, perhaps subdued by the cadre of Australian philanthropic patrol officers (or kiaps) who were administrators, police, judges and jury - all in one, the traditional landowners provided little resistance to the oil companies in accessing lands for oil exploration operations. This was to change radically once the value of that access to privately-owned land under customary title was to be realised in the post-Independence years, and especially so, once oil production commenced.

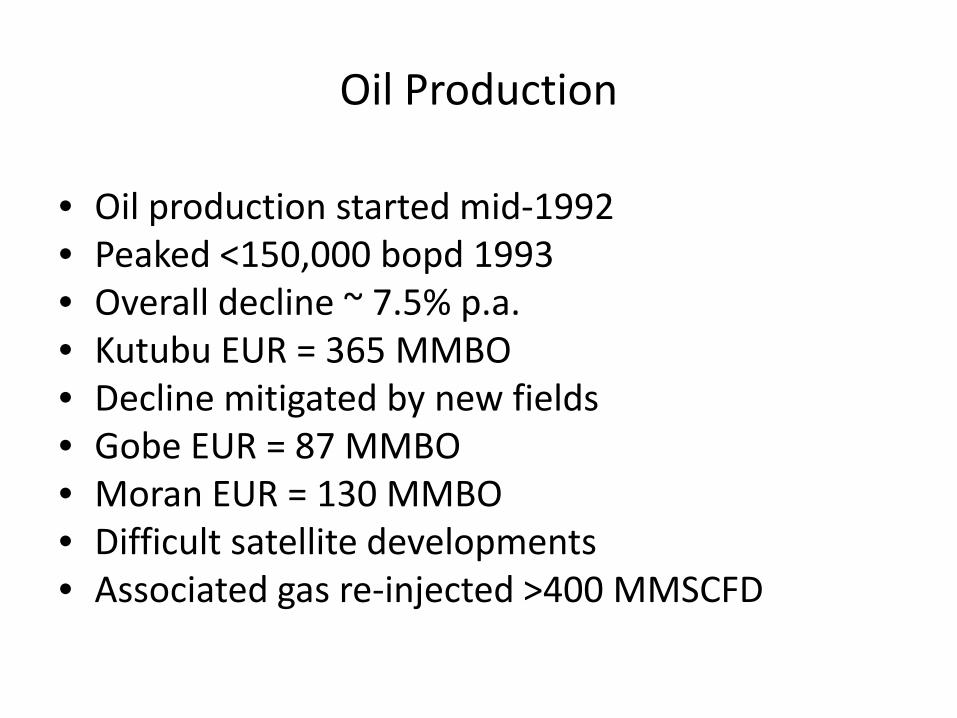

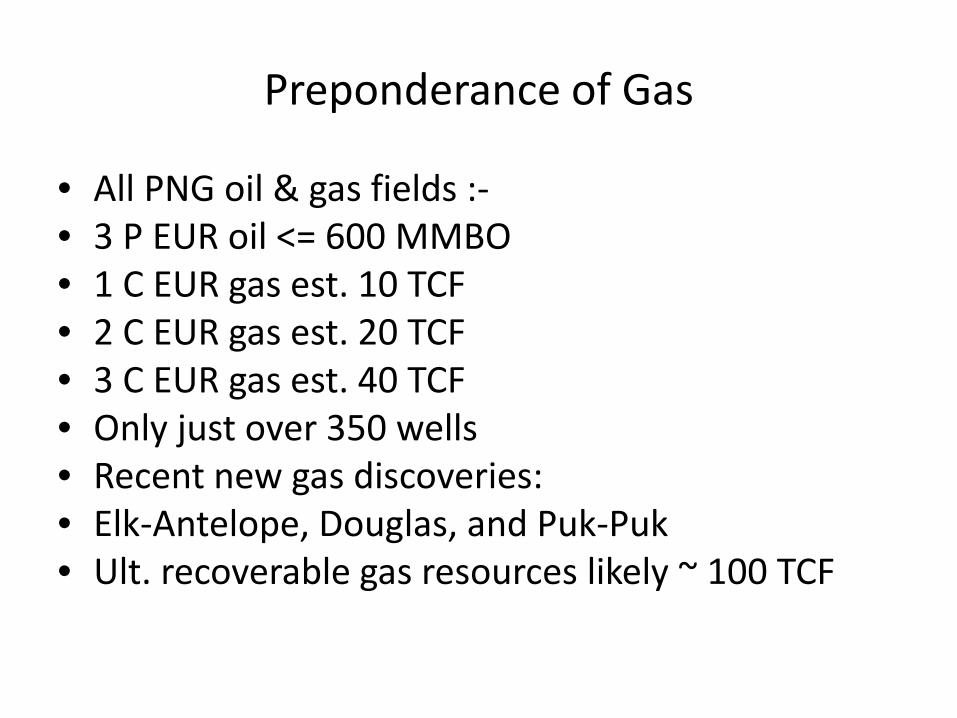

Papua New Guinea had been the subject of enormous exploration investment in many episodes over many decades, but it was only in 1986 that oil was discovered in commercially producible quantities near Lake Kutubu in the Southern Highlands. This discovery at the Iagifu 2-X well underpinned the Kutubu Oil Development Project, which started oil production in June 1992. In the years after the Kutubu discovery, PNG became the subject of great investment interest as many major oil and gas companies scrambled to get Petroleum Prospecting Licences and as many as two dozen new field wildcat wells were drilled per year. However, in the subsequent search for more oil fields, mainly gas was found, which would require much more work to develop. Some additional oil discoveries were, however, made at Gobe and Moran, but alas most of the new discovery wells found natural gas, although that gas was for the most part reasonably rich in natural gas liquids. It rapidly became apparent that the gas endowment was about ten times that of the oil, and with that realisation, exploration waned through the 1990s.

The Kutubu project went ahead and reached a maximum daily production rate of just short of 150,000 barrels per day in 1993. In 1998, the Gobe oil fields and the Moran oil field commenced production. Gobe reached a peak production in 1998 at 34,000 barrels of oil per day, whilst Moran reached 23,000 barrels per day in 2006. These fields helped to keep overall PNG production above 55,000 barrels per day up to 2000, but it declined steadily to 40,000 barrels per day by 2010. The peak production at the Kutubu field was achieved when crude oil prices were relative stable at around US$ 20 per barrel, but as the oil fields of PNG went into decline during the first decade of the new millennium, the world realised extraordinary crude oil prices. Prices surged over an eight-year period from about US$ 25 per barrel to US$ 145 per barrel on 3rd July 2008, only to fall back to US$ 44 per barrel by 15 Dec 2018, and then surge again back to over US$ 100 per barrel by the end of 2008! For a

while, PNG was making excellent revenues from its crude oil production notwithstanding the production rate was only slightly more than a quarter of its peak production, because the price was for a while more than four times the price of the early years of oil production.

This price volatility really tested the petroleum regime of the PNG Government. Due to its prevalence of petroleum income taxes rather than regressive fiscal devices like royalty, it enabled the Government to capture a fair share of the windfalls of higher profits arising from the elevated crude oil price, and yet enable production to continue with reduced taxation when profits were diminished by low crude prices. Indeed, PNG regime has always recognised the significant capital costs of exploration in PNG and has shied away from regressive fiscal terms. The original regime was comprised of a petroleum income tax at 50%, with a 2% royalty paid on wellhead value plus a 22.5% State participating interest in any project paid for on the basis of pro rata sunk costs. The regime also had an Additional Profits Tax set to trigger at the rate of 26% - an impossible rate by today’s standards, but a realistic one for the high interest rates that prevailed in the 1980s. Overall, the regime aimed to provide a net 66.6% take to the Government and 33.3% net take to the investors.

The regime was based on extensive consultations between the oil companies and the Government and an underling White Paper on Petroleum Policy and Legislation formally presented to the Parliament of PNG in 1976. It was a fair deal for a frontier area with enormous physical challenges and tantalising signs of oil and gas. Further, the licensing system was a transparent and well-managed system based on a comprehensive law – the Petroleum Act of 1977. Distinct and well-defined processes for applications for licences, grants of licences and the performance of licensees were established. Moreover, to supplement the Act, it was policy that before the drilling of the first well in each and every Petroleum Prospecting Licence, the licensees were required to negotiate and agree a Petroleum Agreement with the State which provided inter alia for the provision of a 22.5% equity interest in each development project ensuing from the licence, and for any other matters which needed to be agreed between the State and the licensee.

When the Kutubu project was launched in 1990 and an application for a Petroleum Development Licence was made, the fiscal terms were well-defined, procedures for development were in place and the petroleum agreement was pre-negotiated. Not only was the regime ready, but the Government had been steadily building up its technical capacity to manage and regulate the petroleum industry. The Petroleum Resources Assessment Group had been established in 1982 with an initial staff of two officers within the Geological Survey and in 1987 the Petroleum Branch was inaugurated with eleven officers. Then, with Technical Assistance from the World Bank between 1995 and 2000, the integrated Petroleum Division was inaugurated in 1993 with some 29 officers which grew to over 60 by 2004. PNG was rising to the challenge of building the capacity of the Government. Far too many Governments neglect to invest in their side of the petroleum business and then through institutional weakness become prey to politically contrived notions, rather than technically and commercially driven sound plans and policies.

When PNG realised that its petroleum endowment was not so full of oil, but was comprised substantially of nature gas resources, it was recognised that gas would be difficult to develop in the absence of any domestic gas demand from households, commerce or industry, and all the more so being remote from the gas markets of other nations. So in 1992, the Government through the newly-established Petroleum Branch, commissioned a study on all

the discovered oil and gas fields of PNG. This work was conducted by the US firm, Scientific Software Intercom in collaboration with the officers of the Petroleum Branch and sought to assess the extent of the petroleum resources and reserves to proper and systematic standards of reserve reporting then published by the Society of Petroleum Engineers.

Based on summations of the reserves, an economic study was undertaken applying the then prevailing PNG petroleum fiscal regime. The results were presented to the National Executive Council (the Cabinet) showing that if the gas fields discovered to date were aggregated, there could conceivably be a commercially viable gas development based on the export of Liquefied Natural Gas (LNG) to East Asian markets, but more work would be needed to obtain better quantification of gas field development costs and the construction costs of a LNG plant and export facilities.

The Government liked the idea of gas development and embarked on examining its policies for such and began fostering the notion of gas development. Economic and policy studies were conducted and extensive discussions between gas field owners and promoters ensued. In 1995, the Government tabled a Natural Gas Policy before the PNG Parliament. The policy laid down the regulatory and fiscal terms that the Government was willing to consider for the encouragement of investment in gas development. Key features were the introduction of Petroleum Retention Licences (PRLs) to allow the companies to keep their discoveries beyond the period of tenure provided by a normal Petroleum Prospecting Licence. This would be allowed in consideration of an acceptable programme of gas field appraisal and delineation, conduct of commercial studies and development promotion by the licensees. So long as a field was currently not commercially viable, the PRLs would allow retention for up to 15 years.

The gas policy also introduced a single ring-fence for the field development, gas pipeline infrastructure. LNG Plant and marine facilities and based on considerable economic modelling, landed on a concept of 50/50 sharing with of the net value between the developer and the Government. The income tax rate for gas operations was set to 30% of net profits and the State decided it would keep its right to take up to 22.5% equity in the entirety of any development, including the LNG plant and associated facilities. Royalty rates were left at 2% of the wellhead value.

With the foundations for the gas defined for the gas regulatory and fiscal regime, Exxon and BP pursued their LNG development plans based on the large Hides gas field with notions of taking the gas to the PNG north coast and a deep water plant site at Madang. However, these plans faltered due to the Asian financial crisis in 1997 and the consequent sudden reduction in East Asian LNG demand and the terrible tsunami that occurred in 1998 at Aitape on the north coast. The tsunami demonstrated that whilst placing any LNG facilities nearer to markets, any north coast located LNG facility would have to be built to more exacting standards to cater for the additional seismic risk. The Petroleum Division mindful of the seismic hazards of the New Guinea part of PNG had earlier commissioned a PNG Seismic Hazard Study, which was published around the time of the tsunami. It clearly defined the risk and indicated that a southern coast location for a LNG plant and facilities would be preferable.

When the amendments to the Petroleum Act were being prepared for gas development pursuant to the Gas Policy, the results of policy studies on landowner benefits (both royalty

an equity sharing), strategic access to pipelines and processing facilities and elementary domestic gas business provisions became available and an effort was made to incorporate them into the amendments. The Government was intent in providing statutorily defined benefits to communities hosting any future oil and gas development together with proper processes of consultation and liaison with communities. For such benefits the Government devised the idea of a separate Development Agreement between the community parties and the State, which would be agreed in formally convened development forums after proper research had been made as to land matters through the conduct of social mapping and landowner identification studies conducted by the licensees.

Significant and specific political lobbying arose from the Southern Highlands Province, home to the major oil and gas fields, for there to be a separate Gas Act for gas operations. In the resulting compromise, the Government agreed at the political level to introduce some of the reforms suggested by the Province, but only if the Act would remain intact, though it was now agreed that the new Act would be rebranded as the Oil and Gas Act, whilst referring to petroleum for the most part. Thus, the Oil and Gas Act, No 49 of 1998 was born. It represented a major restatement of the former Petroleum Act and has paved the way for improved participation by communities and their sharing in benefits.

Later BP withdrew from PNG and took their ideas about PNG LNG development to West Papua in Indonesia where they successfully launched the Tangguh LNG Project. Then Chevron realising that they were handling increasing volumes of associated gas in their operation of the Kutubu oil fields (as much as 400 million standard cubic feet of gas per day MMSCFD) bought out the commercial notions that the International Petroleum Corporation (the early Lundin company) had about developing their offshore Pandora gas field in the Gulf of Papua, and sending gas to Townsville to supply a 200 megawatt power plant.

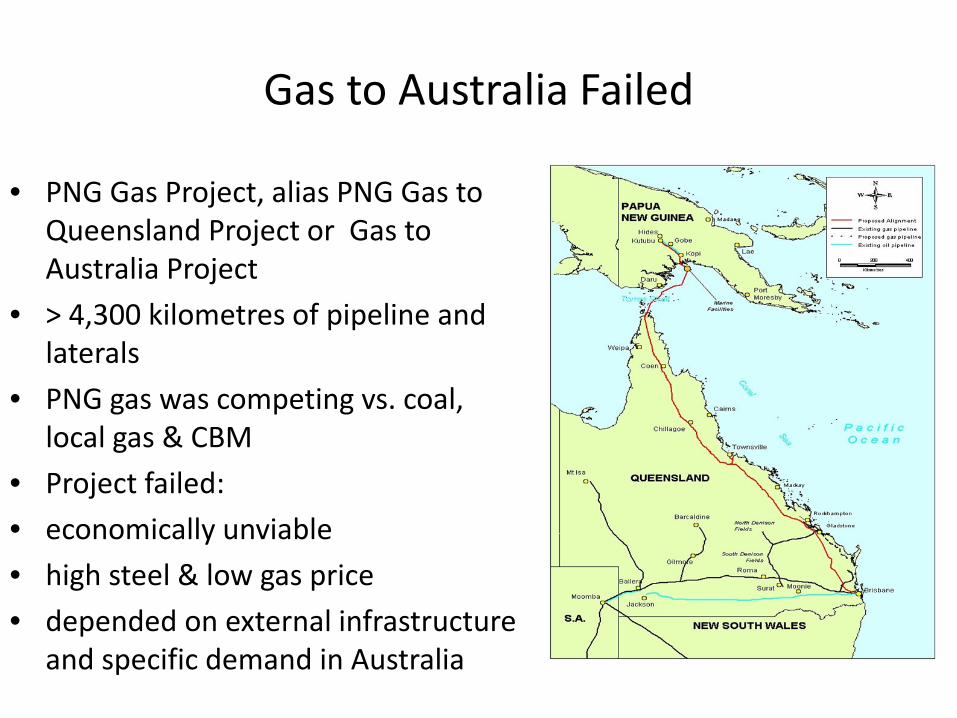

There then ensued a period when all development notions were focused on transmitting gas to Australia from the producing oil fields plus the undeveloped gas fields. Chevron departed the venture, selling its PNG interests to Oil Search and over the course of several years, the schemes waxed and waned. The PNG Gas Project, alias PNG Gas to Queensland Project or Gas to Australia Project ended up with over 4,300 kilometres of trunk gas pipelines and laterals hanging off the PNG gas sources. Most of that infrastructure was in the north eastern quadrant of Australia and was to be expensed against the supply of gas to a wide and quixotic range of Australian gas customers. With low gas prices, high steel prices and the emergence of coal seam methane development ideas in Australia finally it was realised that PNG might end up giving its gas away for nothing and that the only value for PNG might remain in the natural gas condensates extracted in PNG. The PNG Gas Project for the supply of gas to Australia failed. An abrupt turn was made to change all the development notions toward supplying a LNG plant to be located on the Papuan South coast and an effort made to market the gas as LNG to East Asian markets.

The dependence on external infrastructure and specific gas demands in Australia was not seen as either politically attractive or sustainable. Thus, was born the PNG LNG project.

PNG LNG has many factors in its favour as a distinct source for LNG for supply to East Asian markets. PNG is a non-aligned Christian nation; it is not an Islamic nation. PNG is desirous of investment and keen for development based on commercial fiscal terms. PNG as a nation has open-ocean access and does not rely on any strategic straits. It has a

Westminster-style Government and observes the principles of law and contract. PNG is favourably positioned to supply the Australasian region, but can reach out to serve Asian, Pacific and American markets. With diminishing oil production and the absence of new oil finds, PNG’s explorers needed to capitalise on prior exploration investments that failed to find oil. Gas in the new century was no longer a hindrance and could be profitably developed even extending the life of the oil fields.

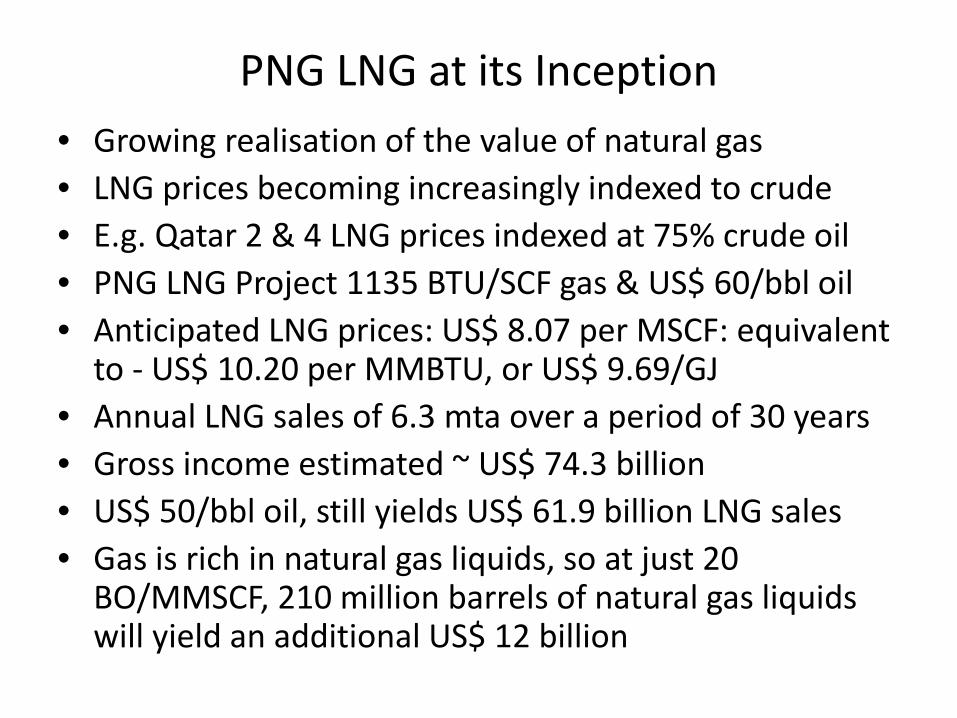

The PNG LNG project was projected to export LNG at a heating value of 1,135 BTU/SCF gas and the liquids were forecast to sell at US$ 60/barrel. Anticipated LNG prices were: US$ 8.07 per MSCF: equivalent to US$ 10.20 per MMBTU, or US$ 9.69/GJ. The original plant design was upgraded early on from.6.3 million tonnes per annum to 6.9 million tonnes per annum for production over a 30-year period. Gross income was estimated to be ~ US$ 74.3 billion. Even at US$ 50/barrel oil, the project was still forecast to yield US$ 61.9 billion in LNG sales. The gas is rich in natural gas liquids, so at just 20 BO/MMSCF, some 210 million barrels of natural gas liquids were forecast to yield an additional US$ 12 billion of sales revenue.

And so, in May 2014, PNG became an LNG exporter, and is now producing about 8+ mta LNG per annum to customers in China, Japan and Taiwan - well above the nameplate capacity of the LNG Plant. It got there because of fine operatorship on the part of ExxonMobil of a coherent joint venture. ExxonMobil was able to market the gas to top quality customers and obtain superior project financing. The only major disappointment has been the collapse in the crude oil prices below projections, and hence the LNG prices due to the indexing with crude oil. For the first year, some elevated prices were obtained, but clearly the fall of crude oil below US$ 30 per barrel hurt the project economics.

Access to lands for the project development came with resounding landowner consent after enormous development forums were held at project level in Kokopo in New Britain and at licence level in each licence area. During the forums, the sharing of the benefit streams of the 2% royalty, 2% free equity from the State, 2% development levy, and other project grants including business development and infrastructure grants were discussed. Oddly, whilst some grants have been paid, the royalties and equity benefits have yet to be distributed due to some remaining uncertainties about landownership. But notwithstanding this situation, the landowners have been extremely patient and almost three years into LNG production and export they remain stoical. Indeed, they have recently been negotiating with the Government for the vendor financing of the additional equity of about 4.2% that was promised to them in the main benefit forum in Kokopo. These equity holdings will be most valuable once the project finance has been paid down, and the fact that the landowners see that value needs to be recognised.

What is next: there is talk of additional LNG trains being added to the existing plant and of new plant joining alongside. Some have dared to talk that a LNG output of 20 million tonnes per annum is possible for PNG within the foreseeable future. However, new problems have arisen: a failing economy; gas development competition, and an inability to manage the generous benefits awarded to customary landowners. PNG can still be successful in producing oil and gas, but it has to learn that it takes more than oil and gas reserves to create a viable and sustainable production industry. A review of its past successes should indicate what it needs to do. It has the natural gas in volumes enough to fill at least two more LNG trains, but it must continue to be proactive in all aspects of gas development planning,

promotion and participation. A lapse into baseless nationalistic policies demanding domestic market obligations in the absence of any domestic markets, strategic designation of pipelines when the principals for such are already in the Oil and Gas Act, or the declaration of unobtainable benchmarks for local content could readily spoil what is essential a very good framework for continued gas development investment.

4281 words

Michael McWalter is a certified petroleum geologist and technical specialist in upstream petroleum industry regulation, administration, and institutional development. He was Resident Adviser to the PNG Department of Petroleum and Energy until 2014, having previously been Director of the Petroleum Division until 1997, and since 2004 has undertaken frequent assignments to various oil and gas ministries, departments and authorities of Governments for development agencies such as the World Bank, ADB and USAID within the Asia-Pacific and African regions. He is a Director of the Board of the Transparency International - PNG, a member of the Catholic Bishops Conference of PNG Finance Board, a Vice President of the Circum-Pacific Council and Treasurer of the Asia-Pacific Regional Council of the AAPG. He was recently appointed as an Officer of the Order of Logohu by the Governor General of Papua New Guinea for service to commerce through contribution to the regulation and development of the oil and gas industry of PNG and the community.

Why Has Papua New Guinea Been Successful in Producing Oil and Gas

Michael McWalter,

SEAPEX Exploration Conference 2017, Singapore

Seeps

Australian and Pacific Plates

Papua New Guinea

Moresby and the HMS Basilik

HMS Basilik on left

Captain John Moresby

Areas of Early Exploration

Oil Production

• Oil production started mid-1992 • Peaked <150,000 bopd 1993 • Overall decline ~ 7.5% p.a. • Kutubu EUR = 365 MMBO • Decline mitigated by new fields • Gobe EUR = 87 MMBO • Moran EUR = 130 MMBO • Difficult satellite developments • Associated gas re-injected >400 MMSCFD

Preponderance of Gas

• All PNG oil & gas fields :- • 3 P EUR oil <= 600 MMBO • 1 C EUR gas est. 10 TCF • 2 C EUR gas est. 20 TCF • 3 C EUR gas est. 40 TCF • Only just over 350 wells • Recent new gas discoveries: • Elk-Antelope, Douglas, and Puk-Puk • Ult. recoverable gas resources likely ~ 100 TCF

Towards Gas Development

• Past exploration efforts disappointing • Few new oil fields found • Exploration found gas • 1992 Reserves Study • Government fostered gas development • Government established Gas Policy in 1995 • Laid the foundation for regulatory & fiscal regime • Exxon and BP pursued LNG plans, based on Hides

Towards Gas Development - 2

• Initial considerations of LNG development failed • Asian financial crisis 1997 reduced LNG demand • North coast Aitape tsunami emphasised risks • Further sector policy development took place • Oil & Gas Act, 1997 and subsequent amendments • Gas development schemes reviewed • Alternate development schemes considered

Gas to Australia Failed

• PNG Gas Project, alias PNG Gas to Queensland Project or Gas to Australia Project

• > 4,300 kilometres of pipeline and laterals

• PNG gas was competing vs. coal, local gas & CBM

• Project failed: • economically unviable • high steel & low gas price • depended on external infrastructure

and specific demand in Australia

Gas Agreement

• LNG re-examined in late 2006 • LNG markets robust and strong

demand • Globally, gas consumption

growing 7.4% p.a. in 2010 • LNG business was about 220 mta • More nations involved: • 1995 - 8 sellers & 8 buyers • 2010 19 sellers & 22 buyers • Many new LNG projects > 94 mta

in Australasia region

The former Prime Minister of PNG, the Right Hon. Grand Chief Sir Michael Somare signing the PNG LNG Gas Agreement with ExxonMobil et al on 22 May 2008

Benefits of PNG LNG • PNG LNG has many factors in its favour: • PNG is a non-aligned nation • PNG is a Christian, non-Islamic nation • PNG is desirous of investment • PNG is keen for development • PNG has open ocean access • PNG is not dependent on strategic straits • PNG has a Westminster-style Government • PNG observes principles of law and contract • PNG is favourably positioned to supply region • PNG can serve Asian, Pacific and American markets • PNG’s explorers need to capitalise on prior exploration

investments that failed to find oil

PNG LNG at its Inception • Growing realisation of the value of natural gas • LNG prices becoming increasingly indexed to crude • E.g. Qatar 2 & 4 LNG prices indexed at 75% crude oil • PNG LNG Project 1135 BTU/SCF gas & US$ 60/bbl oil • Anticipated LNG prices: US$ 8.07 per MSCF: equivalent

to - US$ 10.20 per MMBTU, or US$ 9.69/GJ • Annual LNG sales of 6.3 mta over a period of 30 years • Gross income estimated ~ US$ 74.3 billion • US$ 50/bbl oil, still yields US$ 61.9 billion LNG sales • Gas is rich in natural gas liquids, so at just 20

BO/MMSCF, 210 million barrels of natural gas liquids will yield an additional US$ 12 billion