Why does production have a cost? because.... Scarcity Inputs are scarce. They have opportunity...

19

Why does production have a cost? because ...

-

Upload

shanna-martin -

Category

Documents

-

view

214 -

download

1

Transcript of Why does production have a cost? because.... Scarcity Inputs are scarce. They have opportunity...

Why does production have a cost?

because ...

Scarcity

• Inputs are scarce.

• They have opportunity costs.

What do entrepreneurs want?

• Maximum profit?

• Satisfaction from career?

• To serve others?

• Thrills from competition?

Revenue

• All gains.

• Sales: prices times quantities

• Also from subsidies.

Profit and cost

• Revenue minus cost.

• Cost: foregone opportunity.

• Costs: explicit and implicit.

• Supply costs include all opportunity costs.

Explicit costs

• Paid to someone else.

• Recorded by an accountant or bookkeeper.

• Includes annual depreciation, because the purchase is explicit.

Implicit costs

• Non-recorded opportunity costs.

• Example: highest wage a self-employed person could earn as an employee.

• Example: normal returns to assets, .e.g. interest on bonds.

Two types of profit

• Accounting profit: Revenue minus explicit costs.

• Economic profit: Revenue minus all costs.

• Which is the real profit?

• Which do economists use?

Production

• Short run:

• at least one input is fixed;

• does not vary with output.

• Long run:

• all costs are variable.

The production function

• Q = f (I), I a vector of inputs.

• A physical, not financial, relationship.

• Maximum output obtainable from inputs.

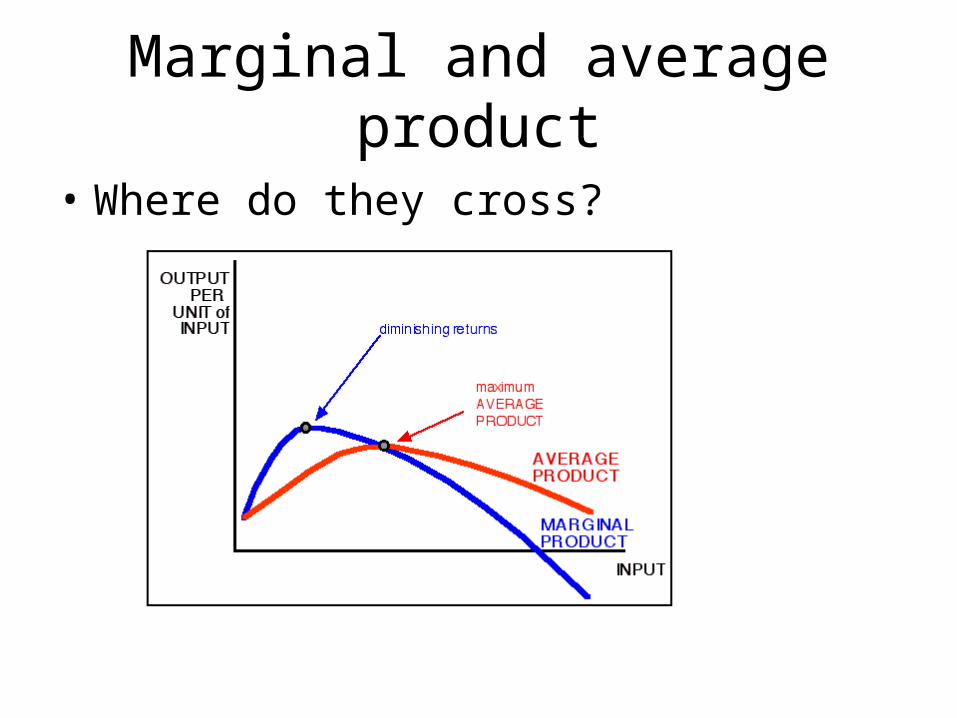

Products

• Average product of a factor: Quantity of output divided by the units of the factor.

• E.g. output divided by workers.

• Marginal product: the additional output from obtaining one more factor unit, all else constant.

The law of diminishing returns

• Only for the short run.

• At least one fixed input.

• As one adds units of a variable input, eventually its marginal product declines.

• The marginal product crosses the average product at the quantity for which ... ?

Marginal and average product

• Where do they cross?

What range?

• At what range of quantity does a profit maximizing firm produce, relative to MP and AP?

.*

Cost and product

• When marginal product is rising,

• marginal cost is falling.

• When average product is rising,

• average cost is falling.

• Marginal cost crosses average cost at its minimum.

Scales

• Scale: the size of a firm or production unit. Not these:

Returns to scale

• Economies of scale: lower average cost with greater scale.

• Diseconomies: greater average cost with greater scale.

• Constant returns to scale: no change in AC when scale increases.

Short and long-run costs• Short-run cost curves are above and

tangent to the long-run curve.