Who is the Boss? Family Control without Ownership in ...€¦ · Who is the Boss? Family Control...

55

Who is the Boss? Family Control without Ownership in Publicly-traded Japanese Firms Morten Bennedsen, a Vikas Mehrotra, b Jungwook Shim, c Yupana Wiwattanakantang d Abstract We document that 50% of public listed Japanese family firms are still under the control by the founding family 50 years after the IPO. The control of top management is persistent even when ownership stakes becomes insignificant and without the use of dual class shares or pyramids. Examples include eponyms such as Casio, Toyota and Suzuki. The families’ reputation, networks of financiers, and talent correlate with longevity of family control. Our results challenge the lifecycle view of corporations in advanced economies and highlights the importance of intangible “family” assets in understanding the evolution of family control. JEL Codes: G32; L26 Keywords: Family control; Ownership; Succession a. Corresponding author. University of Copenhagen, Denmark and INSEAD, Paris, France. E-mail: [email protected] b. University of Alberta School of Business, Edmonton, Canada. E-mail: [email protected] c. Kyoto Sangyo University, Kyoto, Japan. E-mail: [email protected] d. National University of Singapore Business School, Singapore. E-mail: [email protected] We are grateful for helpful comments from Royston Greenwood, Danny Miller and seminar participants at the Entrepreneurship Theory and Practice conference in Bank of Finland Edmonton, and Beijing University, Columbia/INSEAD conference on Family Firms 2018, Conference on Family Firms in Lehigh University, Copenhagen Business School, Development Bank of Japan, European Finance Association meetings, Hanken School of Economics, INSEAD Brown Bag (economics and finance). This project is also benefited from the financial support from Singapore Ministry of Education Academic Research Fund Tier 1 grants (R-315-000-111-112 & R315-000-086-133), the visiting scholar program of the Research Institute of Capital Formation at the Development Bank of Japan, and the Danish National Research Foundation under the Niels Bohr Professorship.

Transcript of Who is the Boss? Family Control without Ownership in ...€¦ · Who is the Boss? Family Control...

WhoistheBoss?FamilyControlwithoutOwnershipinPublicly-traded

JapaneseFirms

MortenBennedsen,aVikasMehrotra,bJungwookShim,cYupanaWiwattanakantangd

AbstractWedocumentthat50%ofpubliclistedJapanesefamilyfirmsarestillunderthecontrolbythefoundingfamily50yearsaftertheIPO.Thecontroloftopmanagementispersistentevenwhenownershipstakesbecomes insignificantandwithout theuseofdualclasssharesorpyramids. Examples include eponyms such as Casio, Toyota and Suzuki. The families’reputation,networksoffinanciers,andtalentcorrelatewithlongevityoffamilycontrol.Ourresultschallengethelifecycleviewofcorporationsinadvancedeconomiesandhighlightstheimportanceofintangible“family”assetsinunderstandingtheevolutionoffamilycontrol.JELCodes:G32;L26Keywords:Familycontrol;Ownership;Successiona. Correspondingauthor.UniversityofCopenhagen,DenmarkandINSEAD,Paris,France.

E-mail:[email protected]. UniversityofAlbertaSchoolofBusiness,Edmonton,Canada.

E-mail:[email protected]. KyotoSangyoUniversity,Kyoto,Japan.

E-mail:[email protected]. NationalUniversityofSingaporeBusinessSchool,Singapore.

E-mail:yupana@nus.edu.sgWearegratefulforhelpfulcommentsfromRoystonGreenwood,DannyMillerandseminarparticipantsattheEntrepreneurshipTheoryandPracticeconferenceinBankofFinlandEdmonton,andBeijingUniversity,Columbia/INSEADconferenceonFamilyFirms2018,ConferenceonFamilyFirms inLehighUniversity,Copenhagen Business School, Development Bank of Japan, European Finance Association meetings,HankenSchoolofEconomics,INSEADBrownBag(economicsandfinance).ThisprojectisalsobenefitedfromthefinancialsupportfromSingaporeMinistryofEducationAcademicResearchFundTier1grants(R-315-000-111-112&R315-000-086-133),thevisitingscholarprogramoftheResearchInstituteofCapitalFormationattheDevelopmentBankofJapan,andtheDanishNationalResearchFoundationundertheNielsBohrProfessorship.

2

“Eversincehewasalittleboy,hismotheralwaystoldhim,‘Onedayyou’llbepresident.’”1AboutToyota’sPresident,AkioToyoda

1. Introduction

Family control of the modern corporation is ubiquitous even in countries with well-

developedcapitalmarkets.2Howfoundingfamilieskeepcontrolovertheirfirmsintheface

ofgrowthimperativesisacontinuingpuzzle.RajanandZingales(1996)suggestthattheease

ofexternalfinancingforcapitalinvestmentsdictatesboththeevolutionoffoundingcontrol

overtime,aswellastherealizedlevelofgrowth.TheircontentionfindssupportinFrank,

Mayer,VolpinandWagner(2011),whoshowthatfamilyownershipdilutionintheUKand

continentalEuropeislargelydeterminedbythefirm’sneedforexternalfinancingforboth

capital investmentsaswell asmergersandacquisitions.These studiesper force focuson

controlderivedfromequityownershipandconcludeinfavouroffinanceasthesinglebiggest,

ifnotthesole,determinantofthelossoffoundercontrolovertime.

Inthisstudy,weextendtheliteratureonfamilycontrolbeyondownershipbystudying

thedilutionofthefoundingfamily’sownershipasdistinctfromalossoftopmanagement

control. We explore the determinants of how families keep control with little or no

ownership. Anecdotal evidence exists fromother advanced countries including the U.S3,

however,theysharetwofeatures:theuseofcontrolenhancingownershipmechanisms,such

asdualclasssharesorpyramids,andagenerallydilutedownershipstructurewithnoother

significantowners.Thus,thisisthefirstlargescalesampletodocumenttheprevalenceof

1 Jason Clenfield and Yuki, Doubting Toyota Prince Defeats Crisis to Prove Self Wrong: Cars, Bloomberg,November21,2013,accessedonJanuary18,2018,http://www.bloomberg.com/news/2013-11-20/doubting-toyota-prince-defeats-crisis-to-prove-self-wrong-cars.html.2 See, for example, La Porta, Lopez-de-Silanes and Shleifer (1999), Morck, Stangeland and Yeung (2000),AndersonandReeb(2003),Morck,Wolfenzon,andYeung(2005),andVillanlongaandAmit(2006).3TheJ.M.SmuckersCompanyhasbeenrunbytheeponymousfamilyforfourgenerationsnow,eventhoughtheSmuckers’familyequitystakeinthefirmisnowlessthan6%.AuniqueaspectoftheirsharestructureisTimePhasedVoting.Underthisset-up,1shareinSmuckersequals1voteifheldforlessthan4yearsandequals10votesifheldformorethan4years.Afewotherwell-establishedcompaniessuchasFordMotorCompanyandtheNewYorkTimesalsohavecontrolinthehandsofthefoundingfamilywithverylittleequityownership,albeitinbothcases,dualvotingsharesprovidethefoundingfamilywithmajoritycontrol.

3

familycontrolwithoutownershipinanadvancedcountrywithlittleuseofcontrolenhancing

mechanisms.

Weemployauniquedatasetofalllistedfirmsinpost-warJapanandbeginbycharting

theevolutionoffamilycontrolfromtheearly1960sthrough2010.Ourpaneldataallowus

tomove beyond static analysis and to document the factors that have allowed founding

familiesinJapantomaintaincontrolovertheirfirmswithorwithoutsignificantownership.

UnliketheU.S.,Japandoesnotpermitdualclassvotingshares,sotheone-share-one-voterule

applies.UnlikeotherAsiancountries,pyramidalfamilygroupownership,asarule,isabsent

in Japan.4Thusvotingcontrolandownershipgohand inhandanda loss inownership is

identicaltoalossinvotingcontrol.Furthermore,ourdataincludefamilycharacteristicssuch

astheeducationalattainmentoftheexecutives,founders,theirheirs,aswellasdetailson

familystructure.Thisallowsustoassesstherelativeimportanceoffinancevs.familyassets

indeterminingthedilutionofcontrolbyfoundingfamiliesinIPOtime.

The literature has used various thresholds such as 25%, 20%, 10% or even 5% of

outstanding shares to define family firms. 5 We find that such cut-offs are ad hoc and

excessivelyrestrictiveindescribingfamilycontrol.Forinstance,basedontheownershipcut-

offdefinition,manyfirmswherethefoundingfamilyholdsthetopmanagementposition,but

hasvery lowownership stakes, riskbeing classifiedasnon-family firms.To illustratewe

highlightthethreeeponymousfamilyfirms,Casio,ToyotaandSuzuki.Familymembershave

takenturnstoholdtheleadershippositionsasPresidentorChairmanforgenerationseven

whenthefamilies’ownershipstakeshavebeendilutedtoinsignificantlevels.Wegeneralize

anddocumentthatbetween10%and30%oflistedJapanesefirmsaremanagedbyheirsof

thefoundingfamilywhohavelittleownershiptoreport.

To our knowledge, this paper is the first documenting the commonplace nature of

familycontrolintheabsenceofmaterialownership.Ourfindingalsoexplainswhyexisting

4 Thefamouspost-warkeiretsusystemisnotafamily-basedstructure(MorckandNakamura,1999&2000)andislargelyseenasawebofhorizontalcross-shareholdings(Nakatani,1984)4. 5See, for e.g., La Porta, Lopez-de-Silanesand Shleifer (1999), Faccio and Lang (2002), Anderson andReeb(2003),VillalongaandAmit(2006),Franks,Mayer,andRossi(2009),andFoleyandGreenwood(2009).

4

studieshavefoundaverylownumberoffamilyfirmsamonglargebusinessesinJapanand

elsewhere(e.g.,Claessens,Djankov,andLang,2000;andMasulis,Pham,andZein,2011).We

showthatincludingfamiliesthatcontrolfirmswithoutownershipmorethandoublestheir

shareamong Japanese listed firms.Wealsodocument the longevityof family involvement

followingthefirm’sIPO–almost50%oflistedfirmsarefamilycontrolled(managedand/or

owned)upto50yearsfollowingtheirIPO.Wearenotawareofcorrespondingstatisticsfrom

othercountries.

Thispaperalsocontributestotheliteraturebyprovidinginsightsintotheimportant

issueofwhyfamiliesexitthefirmstheirancestorshavefounded.Existingempiricalstudies

focusonthedynamicsoffamilyownershipandshowthatfinanceplaysanimportantrolein

thedilutionofownership.Typicallythishappenswhengrowthimperativesrequireexternal

equity infusions, and when equity markets provide a ready source of capital. 6 Well-

functioning equity markets step in to finance growth, and this process is generally

responsibleforthedeclineoffounders’ownershipaftershelistsherfirm.

We show that an important and hitherto overseen determinant of future family

ownership and control is the strength of intangible “family assets” as contended by

BennedsenandFan(2014)andBennedsenetal.(2015).Familyassetsaretherelationship

specific(Williamson,1986),andoftenintangible,investmentsmadebythefoundingfamilies

thataddtofirmvalue,muchasorganizationalcapitaldoes.7Keyexamplesoffamilyassets

arethelegacyofthefamilybusinessasembodiedinthefamilynameandreputation,family

networksinbusinessandpolitics,andthefamilytalentpool.

We document how variation in family assets correlate with variation in time

persistenceoffamilyownershipandfamilycontrol.Weincludeanarrayofproxiesforfamily

6Forexample,Frank,Mayer,andRossi(2009)showthatfoundingfamilyequitystakesgotdilutedintheU.K.largelyasaresultofcapitalinvestmentsviaM&Aactivity.Helwege,PirinskyandStulz(2007)showthattheownershipbyblockholdersdeclinesrapidlyaftertheIPO,andthatthishappensfasterforfirmswithmoreliquidstocks.Frank,Mayer,VolpinandWagner(2011)confirmthesefindingsinalargerinternationalsetting,linkingtheeaseofequitydilutionspecificallytoinvestorprotection,againunderscoringtheimportanceoffinanceindeterminingpost-IPOownershipdeclineintheUnitedStates.Finally,Klasa(2007)documentsthatthefoundingfamily’ssaleoftheircontrollinginterestiscorrelatedtopoorperformanceandfirmageamongtheU.S.firms.7See,fore.g.,LevandRadhakrishnan,(2005)andEisfeldtandPapanikolaou(2013,2014).

5

assets and finance variables in exploring the determinants of the decay in the founding

family’s control over time. Our main results are that more profitable firms, and those

managed by younger CEOs, are less likely to transition to lower levels of family control,

whereasfirmsthatneedexternalcapitalaremorelikelytodoso.Weshowthatfamilycontrol

ismorelikelytobemaintainedinfirmsthatbearthefoundingfamilyname,havecapable

heirs8and trusted employees. Families also sustain control through establishing a close

partnership with investors. In short, our evidence underscores the joint importance of

financialandfamilyfactorsintheevolutionofownershipandmanagementcontrol.

Therestofthepaperisorganizedasfollows.Section2presentsthreecasesofCasio,

Toyota and Suzuki to illustrate how families organize control of their companies when

ownershipisdiluted.Section3presentsourdatameasuringtheevolutionofownershipand

controlofpublictradedfirmsinJapan.Section4dividesfirmsintofourcategoriesdepending

onfamiliesbeingdominantownersand/orincontrolofmanagement.Wethendescribethe

evolution of family ownership and family control over management. Section 5 analyses

factorsthatimpactthetransitionoffirmsamongallfourcategoriesofownershipandcontrol

composition.WeconcludeinSection6.

2. Family control in the absence of material ownership: The Casio,ToyotaMotors,andSuzukiMotorsCases

ThethreewellknownJapanesecompanies,Casio,ToyotaMotor,andSuzukiMotorillustrate

howthefoundingfamilymaintainsmanagementcontrolinsituationswheretheyhavevery

littleownership.Thecases illustratehowfamiliesuseparticularandsometimeselaborate

familyassetsandgovernancestructurestosecureandmaintaincontroloftheirfirmseven

whentheydonothavesignificantownershipstakes.

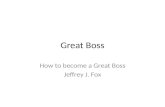

We describe the ownership evolution aswell asmanagement transitions in these

threefirmsoveraforty-yearperiodspanning1960-2000inFigure1.Inallcases,ownership

8Mehrotra,Morck,ShimandWiwattanakantang(2013)describeshowthepracticeofadultadoptions,wherefounders,facedwitheithernon-existentorinadequatebloodheirs,frequentlyadoptoutsidersintothefamilyandappointhimasasuccessor,hasbeenacommongovernancefeatureinJapanesebusinessfamilies.

6

stakesofthefoundingfamiliesarereducedtoinsignificantlevelsbytheendofthesampling

period(andinonecasewereneversignificant)andyet,aswedescribebelow,scionsofthe

founding family continue toholdswayovermanagement in importantways.These three

firms reflect different ways that families retain management control even when their

ownershipisverysmall:First,Casioillustrateshow,evenwhilegrowthandfinancialneeds

dilute familyownership, the founding familykeepscontrol throughalineofverytalented

familymanagers.Second,ToyotaMotorCompanyillustrateshowmanagementcontrolcan

persistviacomplexcrossownershipandmanagementofcompanieswithintheToyotagroup

of firms by the extended family of the founder.9We note that such a structure of inter-

corporate control by the extended Toyoda clan is distinct from the well-known keiretsu

structure,whichrepresentsagroupoffirmstiedbycross-shareholdingsbutlooselylinked

in terms of management. 10 Third, Suzuki Motor Company, where the family never had

significantownership,illustrateshowthepracticeofadultadoptionscanbroadenthetalent

poolforsuccessionpurposesandprovideableandcompetentheirs(Mehrotraetal,2013).

2.1CasioComputerCo.:Ownershipdilutionthroughglobalexpansion.

WestartwithCasio, the iconiccalculatorandelectronicwatchcompany,andshow

how high growth, financed via equity, dilutes founding family ownership over time.We

submitthatfamilytalentneverthelesshaskeptthefoundingfamilyincontroltothisday.

Casiowasfoundedin1946asKashioSeisakujobyateamoffounders,fatherandfour

sonsfromtheKashiofamily.TheKashiomenworkedtogethertodeveloptheworld’sfirst

electroniccalculatorwhichwaslaunchedin1957.Tofinanceexpansion,Casiowentpublicin

1970ontheTokyoStockExchange,withthefamilyretaining61%ofshares.Threeyearslater,

CasioalsolistedontheAmsterdamStockExchange,andontheFrankfurtStockExchangein

1979.Thenetimpactofthesepublicofferingswasasteepdeclineinthefoundingfamily’s

relative share ownership. Indeed, the family’s direct shareholdings in Casio declined

dramatically to 8% in 1990 (see Figure 1). For comparison, we note that the average

9SeeBennedsen,HenryandWiwattanakantang(2016).10See,amongothers,Nakatani(1984),Prowse(1992),Flath(1993)andWeinsteinandYafeh(1995).

7

ownershipbytheleastandmostrestrictivedefinitionsoffamilyfirmsinVillalongaandAmit

(2009) is 16% and 28%. The ownership stake of theKashio family continued to decline

further,dippingunder6%in2000andunder4%in2014.

In reality, however, the Kashio family has always been running Casio. TheKashio

brothers took turns tohold the topmanagementpositions,namely thePresidentand the

Chairman,aswellastoserveonitsboard11.Casio’sfirstpresidentwasthefather,andthen

hisfirstson,Tadao,whosucceededhim.Tadaowithareputationasafinancialwizardserved

aspresidentfor28years,duringwhichperiodhisthreeyoungerbrothersservedonCasio’s

board.Tadaofinallyretiredaspresidentattheageof71in1988andremainedasCasio’s

adviseruntilhisdeath in1993.The secondbrother,Toshio (born in1925),whowas the

inventor of many of Casio’s hit products, became Casio’s Chairman from 1988 until his

retirementin2011attheageof86.

Thethirdbrother,Kazuo(bornin1929),withanexpertiseinsalesandmarketing,led

CasioasitsthirdPresidentfrom1988andassumeddualpositionsasthebothPresidentand

ChairmanafterToshio’sretirementin2011.Thefourthbrother,Yuiko(bornin1930),was

theproductionchiefandservedasvicepresidentfrom1991untilhisretirementin2014at

theageof84.

Kazuoworkedwith the companywell into his 80s to groomhis successorswhich

includedhiseldestsonaswellasthreenephews.InJune2015whenCasio’sprofithitanall-

timehigh,Kazuopromotedhis49-year-oldson,KazuhiroasthePresident,whilehehimself

servedasCasio’sexecutiveChairman.Byspring2019,Kazuowhoturned90andhasbeen

running Casio formore than30 years,has shownno signof disengagement fromCasio’s

management.12

The largest shareholder group in Casio is represented by financial institutions,

followedby foreign investors.Theownershipdilutionof the founding familywasadirect

11SeeCasiohistoryatthecompanywebsite,accessedonJanuary18,2018,https://www.casio.co.jp/company/history/.12ChangingoftheGuard:Casiopresidentsettohandreinstoson,NikkeiAsianReview,May12,2015,accessedonJanuary19,2018,https://asia.nikkei.com/Business/Companies/Casio-president-set-to-hand-reins-to-son.

8

consequenceofCasio’srapidgrowthfinancedbyequitycapital.ThepresenceoftheKashio

foundersandheirs in thetopmanagementcadreofCasiohasnotbeenchallengedbythe

continuederosionoftheirequityownershipinthecompany,andpointstofamilyresources

playinganimportantroleinmaintainingcontrol.

2.2ToyotaMotorCorporation:Controlthroughgroupownershipandstrongfamilyassets

ToyotaMotorisoneoftheworld’slargestautomobilemanufacturers,withamarket

capitalizationatitspeakofUSD220billioninfiscalyear2015.TheToyotacaseillustrates

howcomplexownershipandmanagementstructuresoveragroupoffirmscanempowerthe

family - even when direct family ownership stakes are insignificant. Specifically, Toyota

MotorCompanysatattheapexoftheToyotaGroupwhichcomprisedanetworkofcompanies

connected to each other via cross-shareholdings and shared top executives from the

extendedToyodaclan.

Givenitssizeandstatusasamultinationalcorporation,aswellasextremelylowdirect

ownershipstakesofthefoundingfamily,Toyotadoesnotfitintotheconventionaldefinition

of family firms. Based onwidely accepted ownership thresholds (for e.g., 10% of voting

rights),Toyotawouldbedefinedasawidelyheldfirm.Table1showsToyota’stenlargest

shareholders at six points in time in the last 50 years. Almost none of its 10 largest

shareholdersheldmorethan5%ofoutstandingsharesfrom1950to2000.Toyota’slarge

shareholdersweremostly financial institutionsthatheldtheirshares forseveraldecades.

AmongthetopshareholdersisToyotaIndustriesCorporation,whichheldastakeof5.3%in

2000and6.6%in2015.SettingasidetheownershipinToyotaMotorbyToyotaIndustries,

thefamily’sdirectownershipstakeinToyotaMotorswasandremainsinsignificant.

Thegroupname,Toyota,wasderivedfromthefoundingfamilyname,Toyoda.13The

founderwasSakichiToyoda(1867–1930)whoestablishedToyotaIndustriesasasuccessful

loom maker. The second-generation patriarchy was handed to his adopted son-in-law,

Risaburo(born1884),whosebiologicalson,Kiichiro(born1894),wentontostartToyota

MotorCompanytomanufacturecarsin1937.ToyotaMotorwentthroughfinancialdifficulty

13Toyotahistory,Toyota’swebsite:http://www.toyotaglobal.com/showroom/emblem/history/

9

inthe1940sandeventuallywasonthebrinkofbankruptcyin1949.Themainhouse,Toyota

Industries, sent its president, Taizo Ishida, to rescue Toyota Motor. 14 Ishida, who had

inheritedthefounderspirit,actedasthefamily’scaretaker(Hino,2005).Followingthedeath

ofthetwoToyodabrothersinthesameyearin1952,IshidacontinuedrunningToyotauntil

1961,whilegroomingyoungEijiToyoda,thefounder’snephew,asthenextsuccessor.

EijiwasnamedasToyota’s5thPresidentin1967.HeledToyotaasthechairmanand

honorary advisor until his death in 2013 at the age of 100. During his helm, Eiji was

instrumental in transforming Toyota into the world’s top automobile company and

developedwhatbecameknownasthe“ToyotaProductionSystem”.

Toyota’s6thpresidentwasShoichiroToyoda,whowasthe firstsonofKiichiroand

thereforeadesignatedheirbybirth.Astheclan’spatriarch,hegroomedhisyoungerbrother,

Tatsuro, who was promoted to the presidency in 1991. Shoichiro remained as Toyota’s

executivechairmanduring1991-1999,andthenashonorarychairmanandaboardmember

until2009.ShoichiroalsosupervisedotherToyotagroupfirms,servingasAisin’sauditorand

Denso’sboarduntil2015whenheturned90yearsold.

Tatsuro,however,endedhistermshortlyin1995duetohealthproblems.Toyota’s

next threepresidentswere loyal employees (or sararimen)namelyHiroshiOkuda (1995-

1999),KatsuakiWatanabe(1999-2005),andFujioCho(2005-2009).Duringthishighgrowth

decade,Toyotalookedasifithadabsolutelytransformeditselftobecomeanon-familyfirm

runbyprofessionalmanagers.ThetwoToyodaseniors(EijiandShoichiro),however,had

continuedprovidingadviceoncorporatepolicies, inparticular installingToyodascions in

seniormanagementpositions.15Infact,bythistime,twooftheToyodafamilydescendents

werepromotedasToyotaMotor’sboardmembers.

AkioToyoda,theonlysonofShoichiro,wastoldbyhismothersincehewaslittlethat

14Toyotahistoryatthecompanywebsite.15 Family tensions and succession manoeuvring darken Toyota's top ranks, Sentaku, December 2016,accessedonJanuary18,2018,https://www.sentaku.co.jp/articles/view/16445.

10

“Onedayyou’llbepresident.”16ThefamilydreamcametrueinJune2009when49-yearsold

AkiowasnamedasToyotaMotor’s11thPresident.Hisappointmentcameontopofthelargest

recallscandal,Toyota’sworstcrisisinacentury.PerhapsthecompanyneededtheToyoda

nametosignalthatitwasreturningtoitsrootsandwouldrestorethevalues,qualityand

reputationuponwhichthebusinesswasfounded.

TopexecutivesbearingtheextendedToyodaname–uncles,nephews,andcousins

fromthethreefamilybranchesRisaburo,Eiji,andKiichiro–havealsoservedatkeyToyota

groupcompanies.ThreesonsfromtheEijibrnachhaverunothergroupfirmsaspresident

andchairmanfordecades.KanshiroheadedAisin,whileTetsurohasbeeninchargeofToyota

Industries since 2005. The youngest brother, Shuhei, took the leadership at automotive

componentmanufacturerandgroupmemberfirmToyotaBoshokuCorporation(Bennedsen,

Henry,andWiwattanakantang,2016),servingasitsChairmansince2015.

TheToyotagroupillustratesthatthefoundingfamily’scorporatecontrolcanbemuch

more than the size of the family ownership stake alone would warrant. Backed by the

ownershipstakesofthememberfirmsbelongingtotheToyotagroup,managementcontrol

by the Toyoda clan continues unimpeded to present day. Furthermore, the case also

illustratesthattimegapsbetweencapablefamilyleadersareoftenfilledoutbylongserving

employeesthatareloyaltothefamily.

2.3SuzukiMotorCorporation:Controlthroughadultadoptions

SuzukiMotoroffersaninterestingcasethatchallengestheconventionalwisdomoffamily

control.Eversinceitwentpublicinin1949,thefoundingfamilyhasneverbeenlistedamong

the top ten shareholders. Suzuki’s largest shareholders have been banks and insurance

companiesthathavehelditssharesfordecades.

SuzukiMotor,amajorglobalmanufacturerofsmallcars,wasestablishedbyMichio

Suzuki in 1909. Osamu Suzuki, the current patriarch of the Suzuki family, assumed the

16 Jason Clenfield and Yuki, Doubting Toyota Prince Defeats Crisis to Prove Self Wrong: Cars, Bloomberg,November21,2013,accessedonJanuary18,2018,http://www.bloomberg.com/news/2013-11-20/doubting-toyota-prince-defeats-crisis-to-prove-self-wrong-cars.html.

11

leadershippositionin1978.Osamu’sentryintotheSuzukifamilycameaboutcourtesyofhis

marriagetotheeldestdaughterofSuzuki’s2ndPresident,ShunzoSuzuki.Osamuadoptedthe

SuzukisurnameandbeganworkingatSuzukiin1958androsethroughtherankstosenior

management positions. In 1978 when Chairman Shunzo passed away and Suzuki’s 3rd

President,JitsujiroSuzuki,hadhealthproblems,OsamuwaspromotedasthePresidentatthe

ageof48.LikeOsamu,histwopredecessors,ShunzoandJitsujiro,werealsothefounder’s

adoptedsons-in-lawwhotookontheSuzukinameaftermarriage.

Osamufollowedhis family traditionwhenplanning forsuccessionbygroominghis

son-in-law(HirotakaOno)forPresidentbutunfortunately,Onodiedofcancerin2007atthe

youngageof52.17In2008,partlytocopewiththefinancialcrisis,Osamu,aged78atthetime,

assumed the firm’s toppositionsas combinedPresident/CEO/Chairman. In2015,his55-

years old eldest son, Toshihiro Suzuki, was appointed as the President, while Osamu

continuedservingaschairmanandhasshowednosignsofretiringevenasheturned88years

oldin2018.

To sum, the three cases described above illustrate some common themes: First,

Japanese families often retain control over corporations founded by them even without

materialownershipstakes.Second,theheadofthefirmoftenservesinthejointconsolidated

positionsofchairmanoftheboardandtheCEOorpresidency.Third,controlissustainedover

timethroughcrossownershipandtheuseofspecificgovernancemechanismssuchastrusted

sarariman as CEOs during timeswhen there are no suitable familymembers, or adoptee

candidates, to run the firm.These casesmotivateour focusonseparatingownershipand

controlinthefollowinganalysisandinunderstandingtheroleoffinancialconstraintsand

familyassetsindeterminingthetemporalvariationsinfamilyownershipandcontrol.

17Reuters,“SuzukiMotorExec,CEO'sson-in-lawDiesat52,”December13,2007,accessedonJanuary29,2018,https://www.reuters.com/article/suzuki-obit/suzuki-motor-exec-ceos-son-in-law-dies-at-52-idUST4050820071213.

12

3. DataSourcesandDescriptiveStatistics

Westartourdatasetconstructionbyincludingallcompaniesthatwentpublicinthe1949-

2000period.Weexcludeasmallnumberofthefirmswherefinancialorownershipdataare

missing.Thefinalsamplecoversalmosttheentireuniverseofpubliclistedfirmsinpost-war

Japan.

Toidentifyfamilyfirms,wefollowtheprocedureandthedatasetusedbyMehrotraet

al(2013).WeextendtheirsampleastheirsonlyincludesfirmsthatwentIPOpriorto1970.

OurextensioncoversIPOsthrough2000.OwnershipdataarefromtheDevelopmentBankof

Japandatabasefor1981through2000,asareouraccountingdatafrom1962through2000.

TheToyoKeizaidatabaseprovidesinformationonstockpricesandboardcompositionfrom

1989through2000.Forprioryearsandmissingdata,Mehrotraetal(2013)constructedthe

databyhand-collectingownership,boardstructureandfinancialdatafromhardcopyannual

reportsavailableattheInstituteofInnovationResearchofHitotsubashiUniversity.

Ownershipdatadisclosedinannualreportsinclude:(1)thestakeofeachofthetop

tenshareholders,(2)thecombinedstakeofallbanksandotherfinancialsectorfirms,and(3)

the combined stake of all other firms. Board data include detailed information on each

director’seducation(almamater,majorandgraduationyear),birthdate,yearinitiallyhired,

yearappointedtotheboard,yearmadepresident(shacho)orChairman(kaicho),andprior

workexperience.

We identify each firm’s founder by consulting the following sources: (1)

commemorative volumes (shashi) celebrating company anniversaries, (2) Toyokeizai

Shimposha(1995),(3)NihonKeizaiShimbun(2004)and(4)companywebsites.Toidentify

relationships within the founding family, we use various Japanese language sources: (1)

TokiwaShoin(1977)providesthefamilytreesof1002businessleaders,(2)aseriesofbooks

publishedbyZaikaiKenkyusho(1979,1981,1982,1983,1985)providesthenamesoffamily

membersof theboardsof listed firms,and(3)asetof thirty-eightNihonKeizaiShimbun

(2004)volumesprovidesthebiographiesof243prominentpost-warbusinessleaders.

13

Additionalinformationonfamilyrelationshipsisobtainedfromthefollowingsources:

Japanese equivalents of Who’s Who published by Jinjikoshinjo, the Nikkei Telecom 21

database of corporate news items published from 1975 onwards in the Nikkei group of

newspapers(NihonKeizaiShimbun,theNikkeiBusinessDaily,theNikkeiFinancialDailyand

the Nikkei Marketing Journal), company archives, Koyano (2007) and website searches.

Usingallthisinformation,weannotatefamilytreeswiththenamesandbusinessrolesofall

members of each firm’s founding family. This information lets us identify each firm’s

founder(s)andultimateowners,andascertaineachCEO/Chairman’srelationship,ifany,to

thefoundingfamilybyblood,marriage,oradoption.

Wedefinefamilyfirmsusingbothownershipandmanagementinformation.Onthe

ownership side we will in most of our analyses define a family firm as one where the

aggregated familyownership isat least5%.Familyownership ismeasuredasbothdirect

ownership by family members and indirect ownership through family foundations and

companies controlled by the family. Our ownership data contains the largest ten

shareholders for each firm in each year. It is therefore theoretically possible that we

underestimate family ownership in situationwhere there are family owners that are not

amongthelargesttenshareholders.Inalmostallcases,thenumber10thlargestshareholder

ownslessthan2%oftheshares,wellbelowourthresholdof5%.Thuswebelievethatthe

potentialerrorinourcategorizationissmall.

Figure2 shows the listingofnew firmsonall fourmajor Japaneseexchanges (the

Tokyo,Nagoya,FukuokaandOsakastockexchanges)inthepost-warperiod,spanning1949-

2000.Wenoticeaspikein1949whentheTokyoStockExchange(TSE)andtheOsakaStock

Exchange(OSE)reopenedafterthewar,andthenagainin1961-62,whenthesecondtierof

the TSEwas opened.We also see a spate of new family firms listings in the late 1990s,

coincidingwithsignsofrenewed,thoughultimatelybrief,lifeintheNikkeiIndex.Wedivide

thefirmsintothosethatwerelistedbyindividualsorfamilies(familyfirms)andthosethat

werelistedbyotherentitiessuchascorporations(non-familyfirms).Inmostofthefollowing

analysiswewillfocusontheformergroupandexaminehowownershipandmanagement

evolveovertime.

14

Table2providesdescriptivestatisticforthefirmsinoursample.Itreportsthemean,

standarddeviation,minimumandmaximumforall30,138firm-yearobservations.Wehave

groupedthevariables intothethreecategories thatwefocuson inthe followinganalysis:

FinanceVariables,FamilyVariablesandControlVariables.Financevariablesincludethose

thatarerelatedtotheneedforcapitalandthusprovidetestsoftheextenttowhichfinance

can explain the evolution of ownership and control.We find that averageROA is 4.75%,

similartothevalueof4.64%documentedinMehrotraetal(2013)andcomparabletothe

figureof3.1%documented foramore recentperiod (1986-2000) inDeliosandBeamish

(2005)basedonJapanesemultinationalfirms.ThemeanTobin’sQratiois1.5,similartothe

valuedocumentedinMehrotraetal(2013)–thecorrespondingQ-ratioforthe1986-2000is

1.30inDeliosandBeamish(2005).Themeanvolatilityofindustrysalesis20.7.Themean

firmsizeinnaturallogis17.345andequals¥34billion.Themeanleverage(basedonthe

long-termdebttoassetsratio)is0.20.Equityissuancehappensonaveragein17.4%ofthe

firmyears,correspondingtoafrequencyofapproximatelyonceeverysixyears.Themean

foreign ownership is 1.02% of outstanding shares, lower than themore recent figure of

11.8%byForeignInstitutionalInvestorsreportedinMiyajimaandHoda(2015).

Thefamilyvariablesareourproxiesforintangiblefamilyassets.Tomeasurefamily

legacyweemployanindicatorvariablethatcapturesifthefirmnameisrelatedtothefamily

name,whichoccursinroughlyone-thirdofthesample(seeBelenzon,ChatterjiandDaley,

2017).Ourproxiesforfamilyresourcesarethepresenceoffamilymembersontheboardof

thecompany,aswellasthepresenceoffamilymemberswitheliteeducationontheboard18.

Alittlemorethan28%offirmshaveafamilymemberontheirboard,while24%offirms

haveamemberwithEliteeducationontheboard,indicatingthatmostfamilymembersthat

serveonthefirm’sboardshaveEliteeducation.

The next variable in this set is stable ownership, defined as the percentage of

shareholdingsbythetop10shareholderswhohaveheldthefirm’ssharesforatleastfive

consecutiveyears.Wesubmitthatstableownershipindicatesthepresenceoffriendlyblock-

18WefollowMehrotraetal(2013)indefiningEliteeducationasadegreefromoneofTop5nationaluniversitiesinJapan.

15

holders.Theaverageshareofstableownershipis24%,whichisaround10%morethanthe

averagefamilyownership.Wenotethatstableownershipmayalsoproxyforentrenchment,

andrecognizethatassuch,itseffectonfirmvaluemaybeambiguous.

Finally, we have a group of control variables that are hypothesized to influence

ownershipandcontrolbutdonotidentifyclearlyasFinanceorFamilyAssets–theseareleft

asControlvariables.TheaverageCEOageiscloseto60years.OnaverageCEOshavebeenin

their position for 12 years and 23% of them have an education from an elite Japanese

university.Wefindthatthemeanfamilyownershipis14%.Whentherearemanyelitenon-

familymembersontheboard,weconjecturethatthereisanimpendingtransitionawayfrom

thefamily.Theaveragenumberofelitenon-familymembersontheboardofdirectorsis0.8.

4.Evolutionoffamilycontrolandfamilyownership

Inthissectionwecategorizefamilyfirmsbasedonownershipthresholdsandmanagement

control and describe the evolution of eachover time.We then explore factors that affect

families’attritionofownershipandlossofmanagementcontrol–thesefactorsincludeboth

FinanceandFamilyvariablesasdiscussedaboveinsection3.

4.1 Categorisingfamilyfirmsaccordingtoownershipthresholdsandmanagementcontrol

We begin the analysis by categorising publicly traded Japanese firms into four groups

according to the size of familyownership and the presence of the founding family in top

management.Ontheownershipsideitiscommontouseparticularownershipthreholdsto

definefamilyfirms.Asdiscussedabove,commoncut-offlevelsintheliteratureare5%,10%

and20%ownership.19Wegowith the lowest cut-off, and repeatall ourtestswithhigher

thresholds as robustness checks.20With respect tomanagementwe define family control

basedonwhethertheCEOposition (thePresidentposition inmost Japanese firms inour

19InJapanthiscorrespondsexactlywithvotingrightsshareaswellsincedualvotingsharesarenotpermitted,andverticalpyramidalownershipstructuresarerare.20Sincetheresultsdonotchangequalitativelyweonlypresenttablesusingthe5%threshold.Resultsusinghigherownershipthresholdsareavailablefromtheauthorsuponrequest.

16

sample)isoccupiedbyamemberofthefoundingfamily.Basedontheabovedualscreens,we

definethefourtypesoffirmsasfollows.

Type 1 firms are the classical closely-controlled family firms where the family’s

ownershipstakeisabovethecut-offlevelandafoundingfamilymemberservesastheCEOof

thefirm.Type2firmsarethosewherethefamilyownershipisbelowthecut-offlevel,buta

familymembernonethelessservesastheCEO.Insection2wesawthatthiswasindeedthe

case for the families behind Toyota, Casio and Suzuki.Type 3 firms are thosewhere the

family’sownershipstake is above the cut-off level,but theCEOposition isoccupiedbya

sararimanCEO.21Type4 categorizesex-family firms,wherethe familyownership isbelow

thecut-offlevelandthefamilynolongerholdsthetopmanagementposition.Itisimportant

tonotethatType4firmswerefamilyfirmsattheIPOdateinoursample.

4.2 Evolutionoffamilyownershipandfamilycontrol

PanelAinFigure3describesthedistributionoffirmsacrossthefourtypesinIPOtime.Atthe

endoftheIPOyear,morethan85%ofthenewlylistedfirmsarecategorizedasType1where

thefamilycontrolstopmanagementandhassignificantownership.Ittakesalmost20years

aftertheIPOtoreduceType1firmstolessthan50%ofalllistedfirms.Itisremarkablethat

theshareofType2firmswithfamilymanagementandnosignificantownershipincreasesin

IPO time.At the IPO timeType2 firmsare rare,but10yearsafter the IPO,Type2 firms

accountformorethan10%ofallfirms,andafter20yearstheyrepresentalmostoneoutof

fivelistedfirms–thisfractionismaintainedfortheremainderofthe50-yearpost-IPOperiod.

Type 3 firms (significant familyownershipwith non-family CEO) show themost stability

followingIPO,varyingbetween10%and15%ofall firmsoverthe50years followingthe

firm’sIPO.Ittakesmorethan10yearsforType4firms(ex-familyfirms)toreachalevelof

10%ofalllistings.Twenty-fiveaftertheIPO,almostoneinfourlistedfirmsisclassifiedas

Type4firms.

21Sarariman,aJapaneseterm,connotesacompanyemployeewhoworksforsalary–weusethetermtodenoteprofessionalmanagersunrelatedtothefoundingfamily.

17

Aswearguedearlier,when family firmsaredefinedbasedonownershipalone, all

Type2 firms riskbeingmis-categorisedasnon-family firms.PanelA showed thatType2

representsalargegroupoffirmsevenwhenweuseanownershipthresholdof5%.Themis-

categorizationisobviouslyevenlargerwhenahigherownershipcut-offisapplied.Weshow

thisinPanelBwhereweapplya20%ownershipcut-off.Notsurprisingly,theshareofType

1firmsdeclinesrelativelyfastervis-à-visPanelA.After10years,Type1firmsrepresent33%

ofalllistings,almosthalfasbigastheirshareunderthe5%ownershipthreshold.After25

yearsType1firmsrepresentonly1in10ofthesample,vs.40%inPanelA.Ontheotherhand,

asexpectedwiththehigherthreshold,Type2firmsaremorecommoninallyearsfollowing

theIPO.After12yearstheshareofType2firmsamonglistedfirmsiscloseto50%.

Wehave alreadynoted that if ownershipalone isusedto identify family control, a

significantunder-reportingbiasagainstfamilyfirmsresults.Anadditionalsourceofpotential

biasincountingfamilycontrolamonglistedfirmscomesfromignoringnewlistingsandde-

listings from theexchange.Toaddress thisbias,weexpand the sample toall listed firms,

includingthosethatwerenotfamilyfirmsatthetimeoftheIPO.Wecallthemneverfamily

firmstodistinguishthemfromType4(ex-family)firms.Were-plotfigure3incalendartime

withthenewdata,firstusinga5%ownershipcut-offlevelandpresenttheplotinfigure4.

Wefindthat, first, theshareofnever-family firmsamong listed firmsdeclinesover

time.Inthe1950s,itwasmorethan70%,inthe60sand70sitwasmorethan50%andinthe

late90sitfelltolessthan40%.Asignificantjumpinthefractionoffamily-controlledfirms

occursintheearly1960s,withtheopeningofthesecondtieroftheTokyoStockExchange

whentheshareofType1firmsalmostdoublesto30%ofalllistedfirms(andstaysatthis

levelthroughtheendof2000).TheshareofType2firmshasbeenstablearound10%over

mostof the last50yearswithaslightdeclinein thelate90s.Bycomparison, theshareof

familyowned,butprofessionallymanaged,firms(Type3firms)hasbeenincreasingovertime

andrepresentsaround15%ofalllistedfirmsintheyear2000–thismarkstheextentofthe

ChandlertransformationamongJapaneselistedfirms.Finally,andnotsurprisingly,theshare

offormerfamilyfirms(Type4firms)hasalsoincreasedovertimeasfirmsageandfamilies

sellout.

18

InFigure4PanelBwerepeattheexerciseusinga20%ownershipcut-off.Whereas

the share of firms thatwerenever family firms is by definition unchanged,we see a few

interestingvariationsacrosstheothertypes:TheshareofType1firmsdropsto20%inthe

late90swhiletheshareofType2firmsismuchlarger–notethatthesearethefirmsmost

likelytobemis-classifiedasnon-familyfirmsundertheownershipthresholdcriterion.Not

surprisingly,therearealsofewerType3firmsandmoreType4firms.Thisexerciseshows

thetwindangersofusinghigherownershipcut-offsaswellasignoringfamilymanagement

whendefiningfamilyfirms.Thismis-categorizationismaterial.Ifa20%ownershipcut-off

levelisused,morethan20%ofalllistedfirmsinthelastfiftyyearsarecategorizedasnon-

familyfirmsevenwhenafamilymemberservesastheCEO.CountingType1,2and3firmsas

familyfirms,wefindthatapproximatelyfouroutoftenlistedfirmsinJapanqualifyasfamily

firms.Thisnumberhasbeenrelativestablesincethe1960s.Weconcludethatfamiliescontrol

asignificantfractionofpublictradedJapanesefirms,eitherthroughownership,and/orvia

topmanagement.

4.3 Transitionacrossfamilyfirmtypes

AswehaveseeninFigure3,intheyearsaftertheirIPO,alargeshareoffamilyfirms

eitherloosentheircontroloverownership,ortheircontrolovermanagement.Whereasthe

figureprovidesageneralpictureoftransition,itisnotacompletepictureofthepathtowards

exitfromcontrol.Tocomplementthefigure,Table3providesthetransitionmatrixofhow

familyfirmsmovebetweendifferentcategories.Wefindconsiderablemovementacrossthe

fourfirmtypesinourdataset.Wedefinesucheventsasexitswhentheyareassociatedwith

eitheralossofexecutivepositionbyafamilymemberwiththeincomingCEObeingunrelated

tothefoundingfamily,orinvolvethefamilyownershipdecliningtoinsignificantlevels,or

both.Fore.g.,whenafamilyrelinquishesownership,butretainscontrolinanexecutiveoffice,

we have a transition going from Type 1 to Type 2. Retaining ownership but hiring a

professionalCEOresultsinatransitionfromType1toType3firm.Sellingoutcompletely

withnomanagementroleresultsinatransitiontoType4.

Table3,PanelAdescribesfirmsoriginatingasType1firms,PanelBdescribesfirms

originatingasType2firms,andPanelCdescribesfirmsoriginatingasType3firms.PanelA

19

showsthatthemostcommonexitforType1familyfirmsisfrommanagement;thismarksa

transitionwhereafamilyCEOisreplacedwithasararimanCEO(ornon-familyCEO).These

transitionsaccountforalittleoversixoutoftenexitsforType1firms.Morethanthreeout

oftenexits(36%)involvethefamily’sownershipshrinkingbelowthe5%thresholdwhile

retainingmanagement(exitfromType1toType2firms).Interestinglyonly3%ofexitsfrom

Type1firmsaretoType4firms,underscoringthelimitationofrelyingonalossofownership

andmanagementasthedefiningfeatureofexitsbyfamilyfirms.

PanelBdescribestheexitpathforType2firms.Notsurprisingly,100%ofexitsareto

Type4firm,essentiallynotingthatforfamilymanaged(butnotowned)firms,exitinvolves

thelossofmanagementbutnogainofownership.Similarly,panelCdescribesthetransition

pathforType3firms.Wenoticethatthattherearetwotypesoftransitionshere.Firstthere

is thetransitionwhere firmsreplacetheprofessionalmanagerwitha familymemberand

thusgofromType3backtoType1.Thesetransitionssuggestthatfamiliessometimesuse

professional managers as placeholders before ready and capable heirs re-position

themselvesinmanagementroles.Second,andslightlymorefrequently,thefamilygivesup

theownershipofthefirmandmovestoType4.

5.Determinantsoftheevolutionofownershipandmanagement

In this section we analyse factors that influence the evolution of family ownership and

management.Theaimistounderstandwhysomefamiliesendupwithmanagementcontrol

withoutownership(Type2firmsinourclassification);somefamiliesretainownershipand

either keepmanagement control (Type 1 firms) or professionalizemanagement (Type 3

firms);whileothersexitbothontheownershipandthemanagementside(Type4firms).The

existing literaturehas focusedon financialneedsandconstraintsaskeydeterminants for

ownershipdilutionthatwouldberelevantintransitionsfromType1toType2,Type1to

Type4,andType3toType4transitionsthatinvolvealossofmaterialownership

Weshowthatinadditiontofinancialconstraints,relation-specificfamilyassetsare

equallyimportantfactorsinexplainingtheevolutionoffamilyownershipandcontrol.Inthe

20

following subsections we first analyse ownership dilution alone since the literature has

focused on this variable. We provide a cross-sectional analysis of the determinants of

ownershipdilutioninIPOtime,andrepeattheexercisewithanovelmeasureofownership

dilutionbasedontheconceptofhalf-livesdenotingthetimeforownershiptodecaytohalf

its level.We then investigate the twin questions ofwhy firms relinquishmanagement to

outsiders (the Chandlerian professionalization of management), and how families retain

control overmanagement despite having little share ownership.We end this section by

analysingdeterminantsoffamilyexitsfrombothownershipandmanagement.

5.1Univariatedifferencesacrossfamilyfirmtypes

Table4providesfirmyearmeanstatisticforthefourtypesoffirms.Wegroupourvariables

into three categories: Financial variables, family variables and control variables.We have

30,138firmyearswhichinclude14,697Type1firmyears,4,606Type2firmyears,and3,821

Type3firmyears(therestareType4firmyears).Thetablebeginsbyprovidingthemeanof

allvariablesforthevariousfirmtypesandfollowsthisbyprovidingmeandifferencesacross

pairtypes.Fore.g.,thecolumntitledType3-4(readasType3minus4)isthemeandifference

forthevariablebetweenType3andType4firms.

We begin by comparingmean statistics for the financial variables. Looking at the

relationship between family control and operating performance we find that family

ownership on average is correlated with higher accounting performance measured as

operatingreturnoverassets(ROA).ROAforType1firmsisthehighestat5.3%,vs.3.4%for

Type4firms.Type2andType3firmsareinthemiddlewithROAsof4.2%and4.7%.The

pairwisedifferencesacrosseachcategoryarestatisticallysignificant.However,valuations,

basedonQ-ratios,arenotstatisticallydistinguishableacrossthefirmtypes.Likewise,there

islittlevariationamongthefourgroupswhenwelookatthevolatilityofindustrysales.In

general,familyownedfirms(Type1andType3)aresmallerthanType2andType4firms.

Thatisonlynaturalsincefamilyownershipdilutioniscorrelatedwithassetgrowth.Wealso

noticethatinfirmswherefamiliesretainbothmanagementaswellasownership,financial

leverageislowervis-à-visfirmswherethefamilyhaslowerownershipand/ornoexecutive

positions.Lowerfamilyownershipiscorrelatedpositivelywithfirmage–Type4andType2

21

firmstendtobeolderthanType1andType3firms.Foreignownershiptendstobelowacross

alltypesoffirms.SharesheldbyforeignersarethehighestforType4firms,buteventhere

meanownershipbyforeignersislessthan2%.Comparisonswithotherstudiesaremuddied

by the fact that we do not look at non-family firms in our study, which may attract

disproportionateinvestmentfromforeigners.

Next,wefocusonvariableswewilluseasproxiesforfamilyassets.Byconstruction,

theshareoffamilyownershipissignificantlyhigherforType1andType3firmsthanforthe

othertwotypes.Moreinterestingly,familyownershipandinvolvementarehigherinLegacy

firms that share theirnameswith the founding family.Type1 firmsaremore likely tobe

LegacyfirmscomparedtoType2andType4firms,indicatingareluctanceoflegacyheirsto

disengagefromtheirfirms.Forthesamereason,bothType2andType3firmsaremorelikely

tobeLegacyfirmscomparedtoType4firms.Type2andType3firmsaremorelikelytohave

a family member on their board vis-à-vis Type 4 firms; they are also more likely to be

graduates of Elite universities in Japan. These two results point to the unique resources

families bring to the board – when these are not in evidence, the family’s departure is

hastened.ItisworthnoticingthatType2firmsaremorelikelytohaveelitefamilymembers

ontheirboardsthanType1andType3firms.Thisisconsistentwiththeideathatstronger

familyassetsempowerfamiliestocontrolfirmsevenwhentheirownershipstakesaresmall.

Finally,wefocusonthesetofcontrolvariables.Type1firmshavetheyoungestalbeit

longest-servingCEOs,whileCEOsofType4firmshavetheshortesttenuresandtendtobe

the oldest. Type 2 andType 3 firms are situated in themiddle.We note that ownership

bestowsexecutiverolesatanearlyageandtendstobeassociatedwithlongtenureswhenthe

CEOisanheirofthefoundingfamily.WheretheCEOisasarariman,tenuresareshorter,and

suchapositioncomesatamoreadvancedage.ItisalsoclearthatfamilyCEOs(Type1and2)

arelesslikelytohaveeducationfromeliteuniversitiesrelativetonon-familyCEOs(Type3

and4).

22

5.2Determinantsofownershipdilution

Westartbygraphingmeanandmedianfamilyownershipfollowingtheexchangelistingin

Figure5.Attheendofthelistingyear,familyownershipaveragesabout35%.Whiledirect

comparisonwith other countries aremuddied bymeasurement issues, we note that the

ownershipofsharesbyfamilyinthesampleofsell-outsstudiedbyKlasa(2007)is36%,and

ownershipbyCEOs(officersandboardmembers)intheyearoftheIPOis16%(44%).By

year5,meanownershipdeclinesto26.6%,andbyyear10,itis19.6%.Twentyyearsafter

IPO,averageownershipdeclinesfurtherto12.4%,andafterthirtyyears,itis8.9%.Median

ownershipissignificantlysmallerinallyearsindicatingthatthereisagroupoffirmsthat

keeparelativelyhighfamilyownershipforalongertimeafterIPO.

Themodelweusetostudythedeterminantsofpost-IPOownershipdecayisgivenin

equation(1).!",$isthefamilyownershipinfirmiandattimet,x’sareexplanatoryvariablessuchasROA,Q-ratio,Familylegacy,Stableownership,z’sarecontrolvariablessuchasfirm

age,CEOage,CEOtenureandCEOeliteness.a’sandb’sarecoefficientestimates,c1’sarefixed

yeareffects,ande’srepresenterrorterms.Weclusterstandarderrorsatthefirmlevel,and

includefixedyeareffectsinallregressionspecifications.

%&,' = ∑ *++ ,+,&,' + ∑ .// 0/,&,' + 123' + 4&,' Eq.[1]

InTable5PanelAwepresentthefirstresultsonownershipdecay.InColumn1we

testtheFinanceexplanationsforownershipdecay.First,weexpectmoreprofitablefirmsto

retainfamilyownershipforalongerperiod,whilefirmsthatneedexternalfinancefacefaster

ownershipdecay.WefindthatROAandTobin’sQarebothhighlypositivelycorrelatedwith

family ownership, confirming that families tend tomaintain controlovermore profitable

firms.Firmsinindustrieswithhighervolatilityofsaleshavesmallerfamilyownershipstakes.

Letting industry volatility of sales be a measure of competition, this is consistent with

competitiveindustrieshasteningtheexitoffamilyownership.Largerfirmsandfirmswith

23

higherlevelsofleveragehavelowerlevelsoffamilyownership.Thisisconsistentwiththe

ideathatfirmswithhigherleverageandgreaterpastgrowth(resultingincurrentlargersize)

havelowerfamilyownership.Similarly,firmsthathaveissuedequityinthepriortwoyears

areassociatedwithfasterownershipdecayduetothedilutiveeffectsoftheequityoffering.

Overall our results confirm the importance of Finance in explaining the dynamics of

ownershipinthepost-IPOperiod,andareconsistentwiththenarrativeandresultsinRajan

andZingales(1996).

Inallregressionswecontrolforfirmage,theageandtenureoftheCEO,andtheelite-

nessof theCEO,measuredasan indicatorvariable if theCEOhasadegree fromanelite

university.InallTableswefindthatfirmage,CEOageandhavingeliteCEOsarecorrelated

withlowerlevelsoffamilyownershipwhileCEOtenureispositivelycorrelated.Thelatter

canbeexplainedbythefactthatfamilyCEOsingeneralhavelongertenurethannon-family

CEOsandthathavingafamilyCEOiscorrelatedwithlargerfamilyownership.

Column2analyses the importanceof familyassets inexplainingownershipdecay.

First,weaffirmtheimportanceoffamilylegacy–firmseponymouswiththefoundingfamily

tendtohavehigherfamilyownership.Second,thepresenceoffamilymembersonthefirm’s

boardisassociatedwithhigherfamilyownership,asisthepresenceoffamilymembersfrom

EliteUniversities.Bycontrast,thepresenceofElitenon-familymembersonthefirm’sboard

isassociatedwithalowerleveloffamilyownership.Stableownership,whichwedefineas

sharesheldbygroupfirmsthathavenotchangedhandsinthelastfiveyears,isassociated

withhigherfamilyownership.Alltheseresultsarestronglysignificantinstatisticalterms.

ThesplitbetweenfinanceandfamilyvariablesinColumn1and2makesitpossibleto

doahorse racebetween the twoexplanations.Wedo thisby comparing thevariation in

familyownership that eachof the twomodels canexplainasmeasuredby thepseudoR2

statistic.ItisinterestingtonotethattheexplanatorypowerofthefamilymodelinColumn2

ishigher(PseudoR2=34.1)thanforthefinancemodel(PseudoR2=20.7).

Column3estimatesthedecayinownershipaddingbothfinancialandfamilyvariables

in the samemodel. This only has amarginal impact on the coefficients. For the financial

24

constraintswenoticethattheresultsarealmostidenticaltowhenwerunthefinancialmodel

without the familyvariable.For the familyvariables,wealsonotice that all variablesare

significantinstatisticallytermsandhavethesamesignasinColumn2.

Overall,we find support forboth familyaswell financevariables inexplaining the

cross-sectionalvariationinfamilyownership.Whiletheroleoffinancehasbeenexplicitly

noted in the literature, our results point to the hitherto overlooked importance of family

assetsindeterminingthedynamicnatureoffamilyownership.

InPanelB,we repeat the regressionsusingownershiphalf-livesas thedependent

variable.Wedefineownershiphalf-lifeasthetimeinwhichfamilyownershipdeclinestohalf

itsvalueatthatpointintime(measuredinpost-IPOyears).

LetownershipatanytimetbeWt,withinitialownership=W0

Assumingadecayingownershipfunction,thehalf-life,5,attimetiscalculatedasfollows:

5=t1/2=t.log(2)/log(W0/Wt) Eq.[2]

Totestthevariationinhalf-lifeacrosstimewereplacetheactualownershiplevelwith

thehalf-lifemeasuredefinedaboveinEquation(1).ResultsareprovidedinTable5PanelB.

TheyareingeneralverysimilartotheresultsinTable5PartA.Column1showsthatfinancial

constraintsmatter.First,ROAisassociatedwithlongerhalf-livesforownership,indicating

thatalossofprofitabilityisanimportantdriverofownershipdilution.However,Tobin’sQis

notsignificantlyrelatedtoownershipdecay;neither is thevolatilityof the firm’s industry

sales.Second,bothfirmsizeandleveragearecorrelatedwithshorterhalftimes,confirming

thattheneedforfinance(tosupportgrowth)isakeyfactorforownershipdilution.Third,

foreign ownership is negatively correlated with ownership half-lives, indicating that

foreignerstendtobeassociatedwithfasterdecayoffamilyownership.Equityissuancehas

noimpactonthehalf-lifeofownershipdecay–notethatthisisakeyFinancevariablesince

25

it implies thatownershipdilution ishastenedvia saleof equity tooutsiders.Thehalf-life

resultsdonotsupportsucharoleforFinance.

Column 2 presents a model based on proxies for family assets. Family legacy

(measuredaseponymous firmsandfamilies) isstronglypositivelycorrelatedwith longer

half-lives,affirmingourconjecturethatfamilylegacytendstoprolongfamilycontrol.Family

and Elite Family members on the board and business networks (measured by stable

ownership) are also positively correlatedwith longer half-lives. Finally having elite non-

familymembersoftheboardisnegativelycorrelatedwithhalf-lives.Theseresultsportray

the followingpicture–ownershipdecay ishastenedby thepresenceof smartnon-family

membersonthefirm’sboardandretardedbythepresenceofsmartfamilymembersonthe

firm’sboardandbytheimportancefamiliesplaceonlegacy.Allfamilyassetsvariablesare

statisticallysignificantatconventionallevels.

Column3presentstheresultsofincludingbothfinancialandfamilyvariablesinthe

samemodel.TheresultsaresimilartothepartialanalysisinColumn1and2.Forthefinancial

variableswenoticethatthecoefficientshaveverysimilarsizeandstatisticalsignificance.For

thefamilyvariables,wenotethatEliteNon-familymembersontheboardlosessignificance

bothineconomicandstatisticalterms.Fortheothervariableswenoticeamarginalincrease

inthestrengthofthecoefficients.Inallthreecolumnswenoticethatolderfirms,olderCEOs

andCEOElitenessincreasethespeedofownershipdecay.

To sum, Table 5 shows that family ownership decay over time is related to both

financial needs and the strength of family assets. Relative to existing literature we have

documentedthatintangiblefamilyassetsareimportantfactorsinunderstandinghowand

whenfamiliesexittheirownershipstakes.

5.3Determinantsofprofessionalization

InTable6,weanalyse thedeterminantsof familiesexiting frommanagementof the firm

whileretainingownership–theso-calledprofessionalizationofmanagementtalkedabout

by Chandler (1977). Strong family assets leverage the value of family management

(Bennedsenetal2014).Thus,thelossoffamilyassetsinbusinessfamiliesshouldpredictthat

26

familiesaremorelikelytoprofessionalizethefamilyfirm.Bycontrast,inthetransitionfrom

Type1toType3,ownershipremainsunchanged.Hence,wepredictthatfamilyassetsproxies

aremoreimportantthanfinancialvariablesinunderstandingthetransitionfromType1to

Type3.

This is to a large extent confirmed in Table 6,Model 1,with two exceptions. First

accountingperformanceisnegativelycorrelatedwithprofessionalization.Thisisconsistent

withthe ideathatacrisis isoftenthetrigger for implementingprofessionalization.When

profits are strong, it is easier to postpone the decision to give up the private benefits

associatedwithrunningthefirm.However,whendeficitsaccumulate,thepressuretobring

in professional managers increases. Second, we also note that more valuable firms are

correlatedwithtransitiontoprofessionalmanagement.

InModel 2we again focus on family variables. First, we notice that strong family

ownershipmakesprofessionalizationmorelikely.Thisisconsistentwiththeideathatthe

familiesretainsufficientpowerviaownershiptodelegatemanagementdecisionswithoutthe

fearoflosingcontrol.Wealsonotethesignificantinfluenceoffamilymembersontheboard

of the firm.Thus,when the family is able to controlprofessionalmanagers through their

board presence, it is also easier to embark on a professionalization path. Finally, stable

ownershipisnegativelycorrelatedwithprofessionalization.Thisisconsistentwiththeview

thatnewownersandchangesinthedistributionofownershipmayincreasethepressureon

familytogiveupthemanagementposition,whilestableownershippreservesthestatusquo.

With respect to the controlvariableswenotice thatbothCEOageandCEO tenure

(whicharecorrelated)arepositivelycorrelatedwithprofessionalization.Thus,olderCEOs

aremorelikelytoretire,andthismaybethetimingforwhichthefamilydecidestoputanew-

nonfamilyCEO.

InModel3weaddbothfinancialandfamilyvariablesinthesamemodel.Theresults

are similar but emphasize the importance of family variables for understanding the

professionalizationprocess.Wenoticethatfirmageisnotstatisticallysignificantanymore.

It appears that only ROA and firm value from the set of finance variables correlatewith

27

professionalization.Ontheotherhand,wefindthathavingelitenon-familymembersonthe

boardincreasestheoddsofreplacingthefamilyCEOwithanoutsider.Overall,theresults

affirmtheimportanceoffamilyassetsinadditiontotheroleplayedbyfinanceindetermining

theoddsofprofessionalizationofthefamilyfirm.

5.4Determinantsofcontrolwithoutownership

Perhapsthemostpuzzlingfindinginthisstudyisthelargefractionoffirmswherefamilies

retainthetopmanagementjobevenwhentheirownershipstakebecomesinsignificant.In

Table7weexplorethedeterminantsofsuchType1toType2transitions.Wefollowthesame

analyticalpathasinTable6bypresentingtwopartialanalysesandonethatcombinesboth

financialandfamilyvariables.Bydefinition,thistransitionisaboutlossofownership.Aswe

saw in our three cases the dilution of ownership hasmuch to dowith the imperative of

financing growth. Thus, a priori,we expect the finance variables to be important for this

transition.

AsModel1shows,severalfinancevariablesdomatter.AsinTable5,wefindapositive

correlationbetweenfirmsizeandtheoddsoftransitioningfromType1toType2.Thisis

consistentwith larger firms needingmore capital for their investments. Leverage is also

positively correlated with ownership transition, underscoring a rising need for external

capitalforfirmswithtighterbalancesheets.Finally,equityissuanceisalsoseenashastening

theexit fromType1toType2 firms.Contrastingthiswiththe insignificantcoefficienton

EquityIssuanceinTable6,weconcludethatequityissuanceisrelatedtothelossoffamily

ownership,butnottothelossoffamilymanagerialcontrol.

Undertheassumptionthatfamilyresourcescreatevaluethroughactivemanagement,

andsinceType1toType2transitionspreservefamilymanagement,wedonotexpectthem

tobedirectlyrelevantinthesetransitions.Nevertheless,familyresourcesmaybeimportant

in allowing families to retain controlwithoutownership in Type 2 firms, and hencemay

indirectlyberelevantinthelikelihoodofthesetransitions.Weletthedatatellthestory.

Indeed,Model2inTable7showsthattheonlyfamilyvariablesthataresignificantare

familyownershipandstableownership.Unsurprisingly,whenfamilyownershipissmallitis

28

morelikelythatagivenreductionpushesthefamilyunderthe5%threshold,whichtriggers

thetransitiontoType2.However,networksdomatter.Itisinterestingtoobservethatwhen

thefamilyhasastrongnetworkasmeasuredbythestabilityofownership,theyarealsoless

likelytodilutetheownership.Lookingatthecontrolvariables,wenoticethatyoungerCEOs

aremorelikelytobeaskedtostayonasCEOsevenasownershipdeclinesintoinsignificance.

Ontheotherhand,CEOtenureispositivelycorrelatedwiththetransition–foragivenCEO

age,tenureonthejobincreasestheoddsofbeingretainedastheCEO.Puzzlingly,CEOsfrom

Elite universities are less likely to be associated with these transitions. We would have

thought that such CEOs are more likely to be retained as ownership levels became

insignificant.PerhapsmoretalentedCEOsfindopportunitieselsewhereastheirownership

stakeisreducedtozero.InModel3weaddbothfinancialandfamilyvariablesinthesame

Model. The results are robust.Wenotice thatnow firm age is negatively correlatedwith

ownershipdilutionand thatelite familymemberson theboardaremarginally correlated

withownershipdilution.Elsetheresultsareverysimilartothetwopartialmodels.

5.5 Determinantsofexitpaths.

Table8exploresthetransfertototalexit(toType4)regardlessofwhetherthefirmis

Type1,Type2orType3.MostoftheseexitsoriginateinType2andType3firms,veryfew

firmsaresoldwhenthefamilycontrolsbothownershipandmanagement,aswedocumented

inTable3.

Model1focusesonfinancialvariables.Consistentwiththeexistingliterature,wefind

thatprofitablefirmsarelesslikelytoexit.Itmaybethatprofitablefirmsareabletobothraise

outsidecapitalforinvestments,aswellasfinanceinvestmentsviaretainedearnings.Larger

firmsaremorelikelytobesold.Thisisconsistentwiththenotionthatlargerfirmshavemore

interestedbuyersandhavecapitalneedsthatexceedthatoffamilies’privatewealth.Wealso

noticethatfirmswithhigherleveragearemorelikelytobesold.Leverageputspressureon

the family to find new capital and oneway to do that is through sale of equity. Foreign

ownershipappearstoexpediteexitsaswell–wecannotdistinguishifthisisbecauseofa

selectionbiaswhereforeigninvestorsshunfirmswithfamilyownership,orifforeignowners

somehowactivelyadvocateforanexit.Alloftheseeffectsarebotheconomicallyrelevantand

29

statisticallysignificantataonepercentlevel.Interestingly,theequityissuancedummyisnot

significant.This iscontraryto theextantliteraturethathasarguedthatequity issuance is

relatedtothedilutionofownershipbyfounders(seeforexampleHelwege,PirinskyandStulz,

2007,whoshowthatbothequityissuanceaswellassalesofsharesbyinsidersexplainthe

declineinpost-IPOfounderownership).

Model 2 explains exit using the set of variables that proxy for family assets. Not

surprisingly,wefindthatfamilyownershiplowerstheoddsofanexitforacoupleofreasons.

First,higherfamilyownershipmayrepresentayoungerearlierstageofthesefirmswhenexit

islesslikely,asinKlasa(2010).Second,totheextentinsiderstakesfacedilutionfromequity

issuance, smaller stakes aremore likely to risk falling belowour5% threshold following

equityissuesthanlargerstakes.

Perhapsmore interestingly,we find thatourproxy for family legacy–eponymous

firms–issignificantlyassociatedwithalowerlikelihoodofexit.Thisisconsistentwiththe

viewthatthepresenceandvisibilityofthefamilycreatesvalueinfirmswherefamilylegacy

isanactivepartofthebusinesshistoryandthebusinessbrandingBelenzon,Chatterji,and

Daley (2017). Alternately, it could be also true that founders who name the firm after

themselvesplaceahighervalueoncontrol.

Weemploytwomeasurestogaugetheintensityoffamilyresourcesassociatedwith

the firm. The first variable is an indicator variable to checkwhether one ormore family

membersserveasboardmembers.Thesecondproxyisanindicatorvariablethatmeasures

whether the familyboardappointeehasadegree fromanelite Japaneseuniversity– this

variablehasbeenusedasaproxy for talent inPerez-Gonzales(2006)andMehrotraetal

(2013).Wefindthatingeneralhavingfamilymembersontheboardreducesthelikelihood

of exit, and, furthermore, the interaction of board presence with elite education, is also

negative.Thisindicatesthatbothmonitoringandtalentareimportantfamilyresourcesthat

havetheeffectofdelayingexits.Webelievethatwhilemonitoringconsiderationshavebeen

addressedintheliterature,theideathattalentasafamilyresourceplaysaroleincontrolis

anovelone.

30

Finally,weinvestigatewhetherstableownershipretardsthelikelihoodofexits.We

basethisontheassertionthatstrongfamilynetworksengenderstableblockholdersthatcan

preserve the status quo for a longer time. The results inTable 8 do not support such an

assertion–infact,wefindthatstableownershipisassociatedwithahigherlikelihoodofexit.

Wedonot investigate further the reasonsbehind this–perhaps it ispossible that stable

blockholders facilitate sale of equity by insiders or allow families to retainmanagement

positionsdespiteownershiploss.

Inallregressionspecifications,wenoticethatsuccessionconcernsloomlarge–the

presenceofolderCEOsincreasestheoddsofanexit.Thishasbeennotedintheliterature

(seeKlasa,2010)and indeed, succession isoften seenas theAchilles’heelof family firm

longevity.Similarly,CEOtenureisseenasinverselyrelatedtoexits–thisisnotsurprising

since a longer tenure has the natural effect of postponing exits. The last of the control

variables is theeducational attainmentof theoutgoingCEO.We find thatCEOswithelite

universitypedigrees seems to facehigheroddsof exits.This isperplexingsincewewere

expecting that smarterCEOs (thosewithelitedegrees)wouldbeassociatedwitha lower

likelihoodofexits.Asnotedabove,perhapseliteCEOsfindsuperiorcareeroptionselsewhere

andarenotbeholdentothefirmsfoundedbytheirancestors.

ItisinterestingtonoticethatwhenwecomparetheFinanceandFamilymodels,they

haveverysimilarR-squares–thisisnoteworthysincetheliteraturehaslargelyfocusedon

Financeasapropellerofexits.OurresultsshowthatFamilyisequallyimportant(indeed,

Model2hasamarginallyhigherpseudoR2thanModel1)inexplainingexits.Theliterature’s

focusonFinancehastheeffectofmissingoutonasetoffamilyfactorsthatarestatistically

similarintheirabilitytojointlyexplaintheexitprobabilities.Inprinciple,omittingthefamily

variablescouldalsobiastheobservedcoefficientsontheFinancevariables.Weincludeboth

setsofvariablesinthethirdspecificationpresentedinModel3.

Barringafewdifferences,theresultsareverysimilartothepartialanalysisinModel

1and2.However,firmsizeisnolongersignificantinexplainingexitlikelihood.Thismaybe

duetofirmsizeandfamilyownershipbeingcorrelatedandomittingeithervariablehasthe

potentialtointroducebiasintheestimatedcoefficients.Similarly,wealsonoticethatfirm

31

ageisnowsignificant,suchthatolderfamilyfirmsareseenaslesslikelytoexit,controlling

forthesetofFinanceandFamilyvariables.ThisisinterestingsinceitimpliesthatFirmAge

per se is not a handicap for family control – rather, it may be other variables that are

correlatedwithFirmAgethatarefundamentallymoreimportantindeterminingexits.Our

measureoffamilylegacyisnolongersignificantatthe5%level,thoughthepointestimateis

similar in magnitude to that in Model 1. Finally, we note that the impact of the control

variablesremainsunchanged.

In Table 8 Panel Bwe split up the starting points and look independently on the

transferfromType1toType4,Type2toType4andType3toType4.Thefirstmodelisless

interestingsinceitisbasedononly18observationsindicatingthatadirectexitofafamily-

ownedandcontrolledcompanyisrareinJapan.Whenfamiliesexitbygivingupmanagement,

wenoticethatfamilylegacy,andfamilyandelitefamilymembers’presenceontheboard,

significantlyreducetheoddsofexit.SimilarobservationscanbenoticedwhenType3firms

(professionalizedfirms)aresold.

Overall,theresultsintables5through8providenewinsightsintowhyfamiliesexit

theircorporation.First,acrossallpanels,wefindthatbothfamilyandfinancevariablesare

importantinexplainingthepartialexitprobabilities(basedoncomparingpartialR-squares

frommodel1andmodel2acrossthethreetables).Second,wenoticethatfinancialvariables

seemtoberelativelymoreimportantinexplainingownershipdilution(thetransitionfrom

Type1toType2)whereasfamilyvariablesarerelativelymoreimportantinthedecisionto

professionalizethefamilyfirm(thetransitionfromType1toType3).Thisisconsistentwith

theargumentsputforwardinBennedsenandFan(2014)whoarguethatfamilyassetsare

keyindeterminingtheoptimalmanagementstructureoffirms,whereasfinancialroadblocks

arekeytounderstandingafirm’sownershipstructure.

6. Conclusion

Usinganoveldatasetfortheevolutionofownershipandcontrolofpubliclytraded

firmsinJapanweshowthatintangiblefamilyassetsareimportantfactorsinunderstanding

32

thepersistenceoffamilycontrol.Infact,wefindthatfamiliesexercisecontrolovercorporate

assetsevenintheabsenceofmaterialshareownership–aidedinpartbyanexusoffriendly

andstableinvestorsaroundthem,andinpartbywhatarebestdescribedassoftfamilyassets

suchasafamily’snameandreputation.ThebottomlineisthatfamilycontrolinJapanismore

persistentthantheverylowequityownershipbyfoundingfamilieswouldindicate.

Wealso conclude that familyand financial factors jointlydetermine thedilutionof

familyownershipandlossofmanagementcontrol.Wefindsuggestiveevidencethatfinancial

variablesaremoreimportantinexplainingthedilutionofownership,whereasfamilyassets

arerelativelymoreimportantinexplainingthedecisiontodelegatethetopmanagementjob

tooutsiders.

33

References

Anderson, R.C., & Reeb, D.M., 2003, Founding family ownership and firm performance:EvidencefromtheS&P500,JournalofFinance,58(3),1301-1328.

Belenzon, Sharon, Aaron Chatterji, and Brendan Daley, 2017, Eponymous Entrepreneurs,AmericanEconomicReview,107(6):1638-55.

Bennedsen, Morten, Kasper Meisner Nielsen, Francisco Pérez-González and DanielWolfenzon,2007,InsidetheFamilyFirm:TheRoleofFamiliesinSuccessionDecisionsandPerformance,QuarterlyJournalofEconomics122(2),647-691.

Bennedsen,MortenandJosephP.H.Fan,2014,TheFamilyBusinessMap:FamilyAssetsandRoadblocksinLongTermPlanning(Prentice-MacMillian).

Bennedsen,Morten,JosephP.H.Fan,MingJianandYin-HuaYeh,2015,TheFamilyBusinessMap: Framework, Selective Survey, and Evidence from Chinese Family FirmSuccession,JournalofCorporateFinance33:212-226.

Bennedsen,Morten and Nicolai J Foss, 2015, Family-driven innovation strategies: Familyassetsand liabilities in the innovationprocess,CaliforniaManagementReview,Fall,65-81.

Bennedsen,Morten,BrianHenry, andYupanaWiwattanakantang,2016,Toyota:AFamilyHeirSteersCarmakeroutofCrisis,INSEADCasePublishing.

Bertrand,MarianneandAntoinetteSchoar,2006,TheRoleofFamilyinFamilyFirms,JournalofEconomicPerspectives20(2),73-96.

Bhide,Amar,1993,Thehiddencostofstockmarketliquidity,JournalofFinancialEconomics34(1),31-51.

Burkart,Mike,FaustoPanunzi,andAndreiShleifer,2003,Familyfirms,JournalofFinance,58(5),2167-2201.

Chandler,Alfred,1977,TheVisiblehand:TheManagerialRevolutioninAmericanBusiness.(Cambridge,Mass.:HarvardUniversityPress).

Claessens,Stijn,SimeonDjankov,andLarryLang,2000,TheSeparationofOwnershipandControlinEastAsianCorporations,JournalofFinancialEconomics58(1-2),81-112.

DeephouseDavidL.andPeterJaskiewicz,2005,DoFamilyFirmsHaveBetterReputationsThanNon-FamilyFirms?AnIntegrationofSocioemotionalWealthandSocialIdentityTheories,JournalofManagementStudies,503,337-360.

Delios,AndrewandPaulW.Beamish,2005,RegionalandGlobalStrategiesofJapaneseFirms,ManagementInternationalReview,45(1),19-36.

34

Flath, David, 1993, Shareholding in the Keiretsu, Japan's Financial Groups, Review ofEconomicsandStatistics,75(2),249-257.

Foley,C.Fritz,andRobinGreenwood,2009,TheEvolutionofCorporateOwnershipafterIPO:TheImpactofInvestorProtection,ReviewofFinancialStudies23(3),1231-1260.

Franks, Julian, Colin Mayer, and Hideaki Miyajima, 2014. The Ownership of JapaneseCorporationsinthe20thCentury,ReviewofFinancialStudies27(9),2580-2626.

Franks,Julian,ColinMayer,andStefanoRossi,2005,SpendingLessTimeWiththeFamily:TheDeclineofFamilyOwnership in theUnitedKingdom, inRandallMorck(ed.),AHistory of Corporate Governance around the World: Family Business Groups toProfessionalManagers,(ChicagoandLondon:UniversityofChicagoPress),581-607.

Franks,Julian,ColinMayer,andStefanoRossi,2009,Ownership:EvolutionandRegulation,ReviewofFinancialStudies22(10),4009-4056.

Franks, Julian, ColinMayer, Paolo Volpin andHannes F.Wagner, 2011. The Life Cycle ofFamilyOwnership:InternationalEvidence,ReviewofFinancialStudies25(6),1675-1712.

Franks,Julian,ColinMayer,HideakiMiyajima,2014.TheOwnershipofJapaneseCorporationsinthe20thCentury,ReviewofFinancialStudies27(12),2581–2625.

Helwege,Jean,ChristoPirinskyandRenéM.Stulz,2007,WhyDoFirmsBecomeWidelyHeld?AnalysisoftheDynamicsofCorporateOwnership,JournalofFinance62(3),995-1028.

Hino,Satoshi,2005,InsidetheMindofToyota:ManagementPrinciplesforEnduringGrowth,(Tokyo:ProductivityPress).

Klasa, Sandy, 2007, Why Do Controlling Families of Public Firms Sell Their RemainingOwnershipStake?,JournalofFinancialandQuantitativeAnalysis,42,339-368.

LaPorta,Rafael,FlorencioLopez-de-Silanes,andAndreiShleifer,1999,CorporateOwnershipAroundtheWorld,JournalofFinance54,471-517.

Miyajima,HideakiandTakaakiHoda,2015.OwnershipStructureandCorporateGovernance:Has an Increase in Institutional Investors’ Ownership Improved BusinessPerformance? InPolicyResearchInstitute,MinistryofFinance, Japan,PublicPolicyReview,Vol.11,No.3,July2015.

Masulis,RonaldW.,PeterKienPham,andJasonZein,2011,FamilyBusinessGroupsaroundtheWorld:FinancingAdvantages,ControlMotivations, andOrganizationalChoices,ReviewofFinancialStudies24(1),3556-3600.

Mehrotra, Vikas, Randall Morck, Jung-Wook Shim, and YupanaWiwattanakantang, 2013,Adoptive Expectations: Rising Sons in Japanese Family Firms, Journal of FinancialEconomics108,840–854.

35

Miller Danny, and Isabelle Le Breton-Miller, 2005,Managing for the Long-run: Lessons inCompetitive Advantage from Great Family Businesses (Boston: Harvard BusinessSchoolPress).

Miller,Danny, IsabelleLeBreton-Miller,RichardLesterandAlbertCannella, Jr.,2007,AreFamilyFirmsReallySuperiorPerformers?JournalofCorporateFinance13,829-858.

Morck Randall, David Stangeland, and Bernard Yeung, 2000, Inherited wealth, corporatecontrol, and economic growth: The Canadian Disease?, in Concentrated CorporateOwnership,inRandallMorck(ed.),(ChicagoandLondon:UniversityofChicagoPress),319-372.

MorckRandall,DavidStangeland,andBernardYeung,2005,CorporateGovernance,EconomicEntrenchment,andGrowth.JournalofEconomicLiterature43(3),655-720.

Nakatani, I., 1984, The economic role of corporate financial grouping, in M. Aoki, ed.:EconomicAnalysisoftheJapaneseFirm(Elsevier,NewYork).

Perez-Gonzales, Francisco, 2006, Inherited Control and Firm Performance, AmericanEconomicReview96(5),1559-1588.

Prowse,Stephen,1992,TheStructureofCorporateOwnershipinJapan.JournalofFinance,47(3),1121-1140.

Rajan,RaghuramG.andLuigiZingales,1996.FinancialDependenceandGrowth,AmericanEconomicReview,88(3):559-586.

Smith, Brian F. and Ben Amoako-Adu, 2005, Management Succession and FinancialPerformance of Family Controlled Firms, in RobertWatson (ed.), Governance andOwnership,(Elgar:Cheltenhamfort),314-341.

Villalonga, Belen and Raphael Amit, 2006,How do family ownership, control, andmanagementaffectfirmvalue?JournalofFinancialEconomics,80(2),385-417.

Weinstein, David and Yishay Yafeh, 1995, Japan's Corporate Groups: Collusive orCompetitive?AnEmpirical Investigationof KeiretsuBehavior. Journal of IndustrialEconomics,43(4),359-376.

WilliamsonOliverE.,1985,TheEconomicInstitutionofCapitalism,(NewYork:FreePress).

WilliamsonOliverE.1975,MarketsandHierarchies:AnalysisandAntitrustImplications,(NewYork:FreePress).

36

Figure1FamilyOwnershipofCasio,ToyotaMotor,SuzukiMotor(1960-2000)

ThisfigurepresentsthefoundingfamilyownershipofCasio,ToyotaMotorandSuzukiMotor.Thepercentageoffamilyshareholdingsincludestheownershipbythemembersofthefoundingfamilyaswellasbygroupcompanies.Verticalaxisnumbersareinpercent.

4.88 6… 6.977.17

4.35

60.22

55.86

49.85

43.27

34.5132.29

29.76

25.69

18.415.35 12.44

11.43 8.24 8.06 7.375.66

0

10

20

30

40

50

60

70

19601961196219631964196519661967196819691970197119721973197419751976197719781979198019811982198319841985198619871988198919901991199219931994199519961997199819992000

Toyota

Suzuki

Casio

37

Figure2

NewlistingsontheJapaneseStockExchanges(1949-2000)