What’s Next for Mobile Video

28

What’s Next for Mobile Video IMTC-UCIF All Members Meeting 2014 Ori Modai, CTO

-

Upload

imtc -

Category

Technology

-

view

112 -

download

1

Transcript of What’s Next for Mobile Video

What’s Next for Mobile VideoIMTC-UCIF All Members Meeting 2014

Ori Modai, CTO

22

2003, 2004…

Invented2003-2004

Founded 2003-2004

Launched 2003-2004

Ratified 2003

33

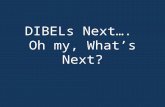

2003 video conferencing reality

44

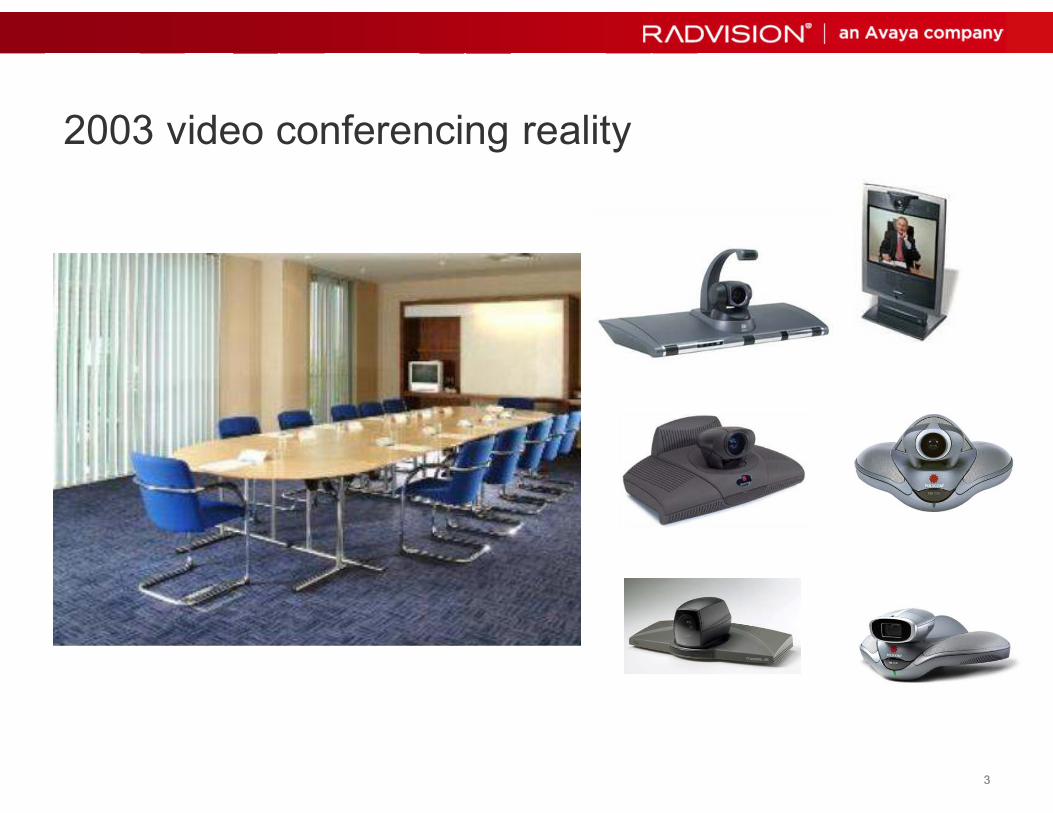

Inflection Points in Video Conferencing

-

500

1,000

1,500

2,000

2,500

3,000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

$M

TP Room Systems Exec Infrastructure

Introduction of HD and

Telepresence

Transition to IP

Personal and

Mobile Video

Conferencing

Source: Wainhouse research

5Radvision - Proprietary. Use pursuant to your signed agreement or Radvision policy.

Why Video? Why Mobile?

66

Enterprise Video Meets Mobile Collaboration

48% Enterprise Deployed

28% Employees Served

60% UC growth rate driven by personal/

mobile video

40% employees spend >20% of time away from

desk

80% Fortune 100 deploying

iPhones/iPads

of enterprises expect to integrate desktop/mobile video with rooms – Nemertes Research

Over

Market Trends

77

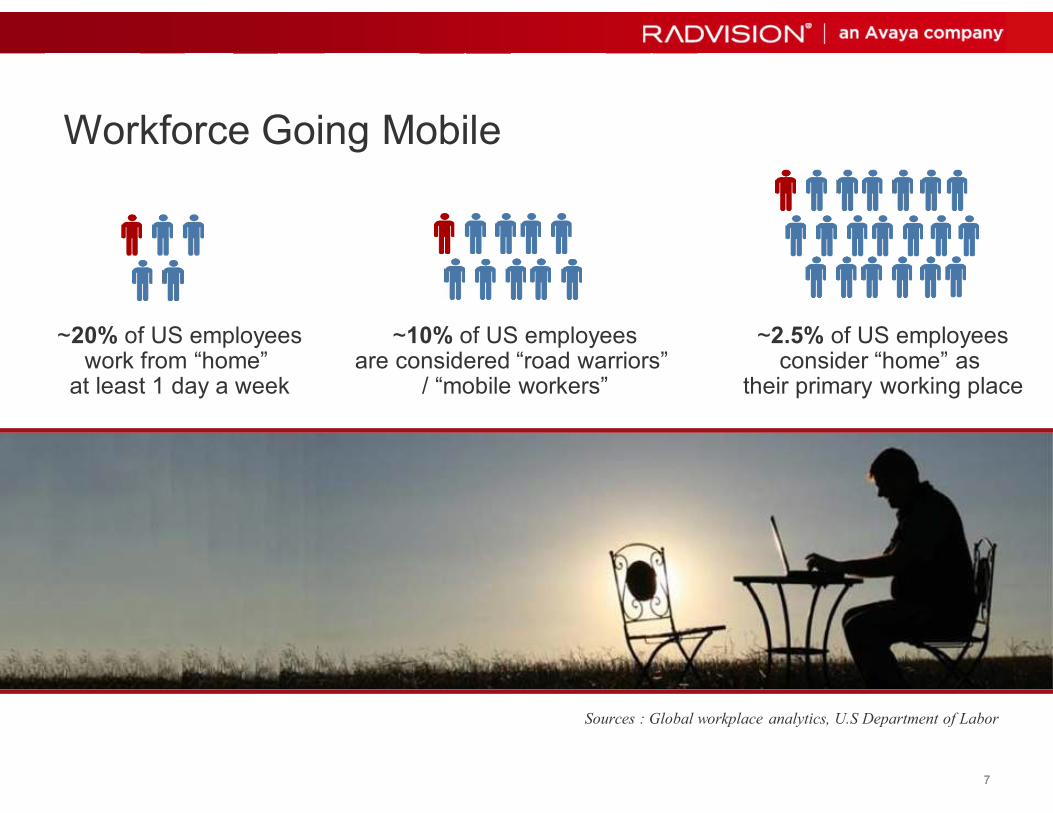

Workforce Going Mobile

Sources : Global workplace analytics, U.S Department of Labor

~20% of US employeeswork from “home”

at least 1 day a week

~10% of US employeesare considered “road warriors”

/ “mobile workers”

~2.5% of US employeesconsider “home” as

their primary working place

88

Changing Workforce Culture

Digital natives now entering the workforce

99

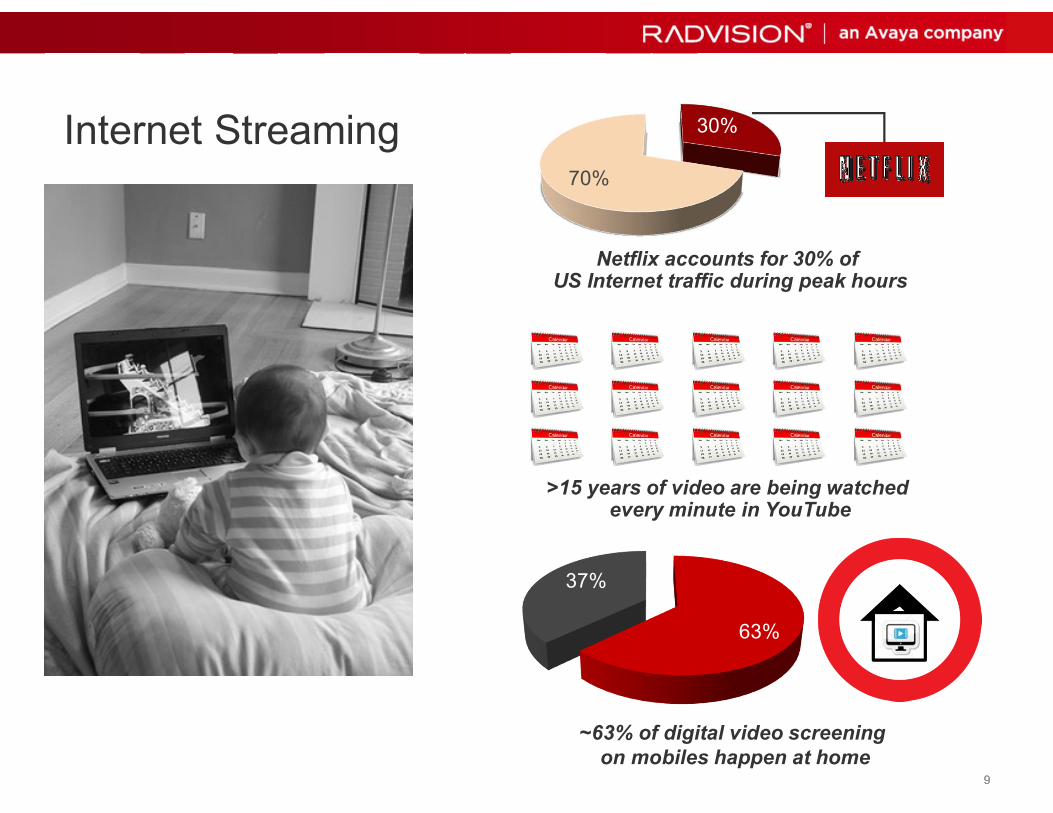

Internet Streaming 30%

70%

Netflix accounts for 30% of US Internet traffic during peak hours

>15 years of video are being watched every minute in YouTube

63%

37%

~63% of digital video screening

on mobiles happen at home

1010

Source: http://www.bandwidthblog.com/tag/skype/

2013 statistics

11Radvision - Proprietary. Use pursuant to your signed agreement or Radvision policy.

Mobile Video Drivers

Multi screen experience

1212

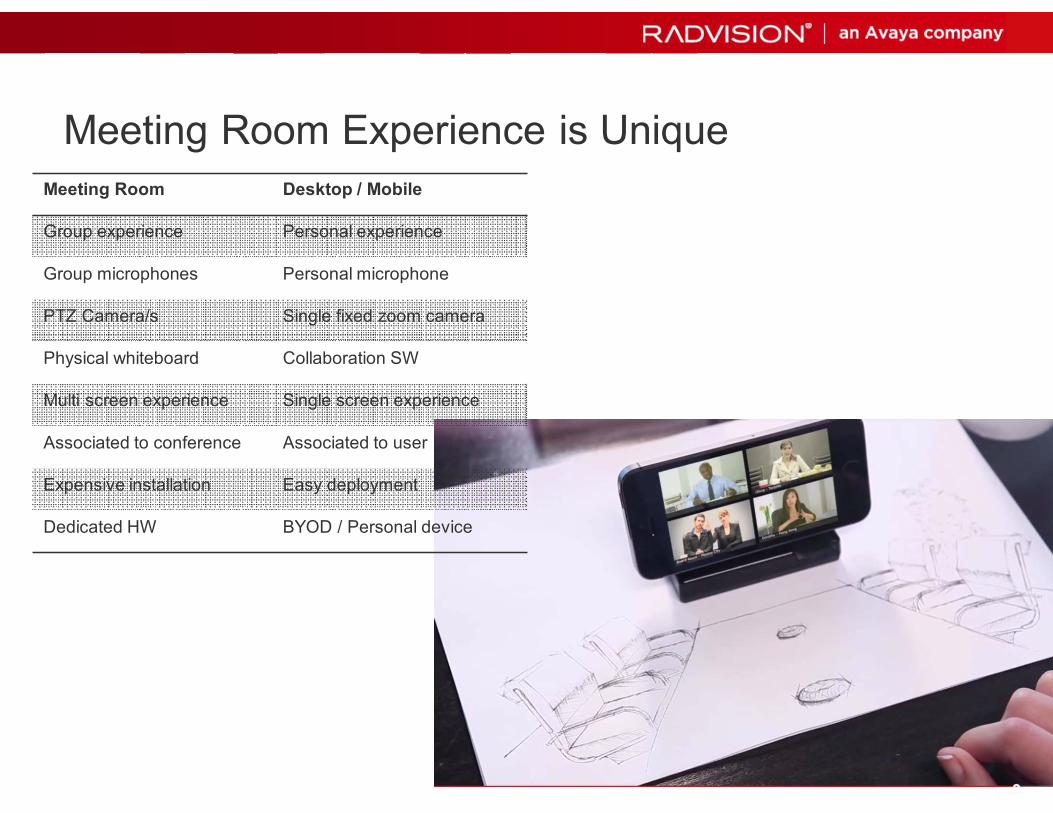

Meeting Room Experience is Unique

Meeting Room Desktop / Mobile

Group experience Personal experience

Group microphones Personal microphone

PTZ Camera/s Single fixed zoom camera

Physical whiteboard Collaboration SW

Multi screen experience Single screen experience

Associated to conference Associated to user

Expensive installation Easy deployment

Dedicated HW BYOD / Personal device

1313

The Class Inversion in Video Conferencing

Who is a second class citizen ?

Desktop / Mobile

Roster information

Data collaboration

Slider

Layout flexibility

IM

Conference control

(Context based information)

Meeting Room

F2F

Audio quality

Video quality

Interactivity

1414

Multi Screen ExperienceContextual Awareness

1515

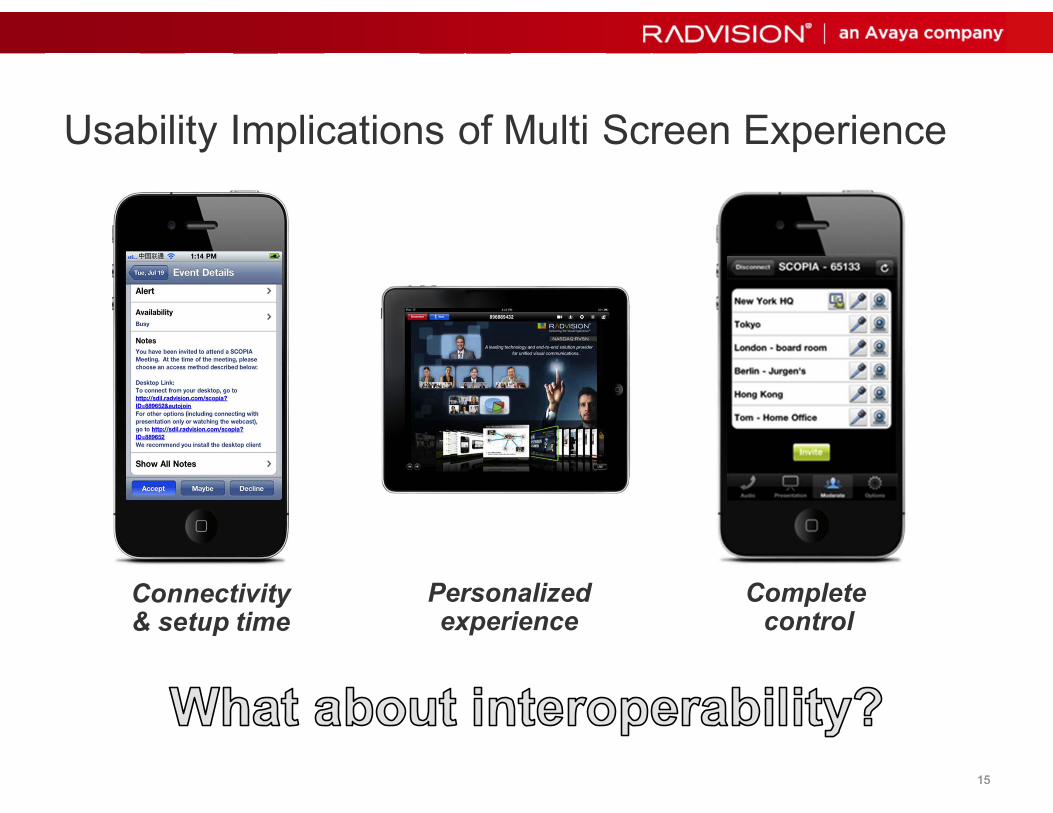

Usability Implications of Multi Screen Experience

Connectivity& setup time

Personalizedexperience

Complete control

16Radvision - Proprietary. Use pursuant to your signed agreement or Radvision policy.

Mobile Video Drivers

Business to consumer relationship

1717

1818

Context is critical

Source: Avaya Collaboration Environment enhanced business applications

19Radvision - Proprietary. Use pursuant to your signed agreement or Radvision policy.

Mobile Video Drivers

Technology and Usability

2020

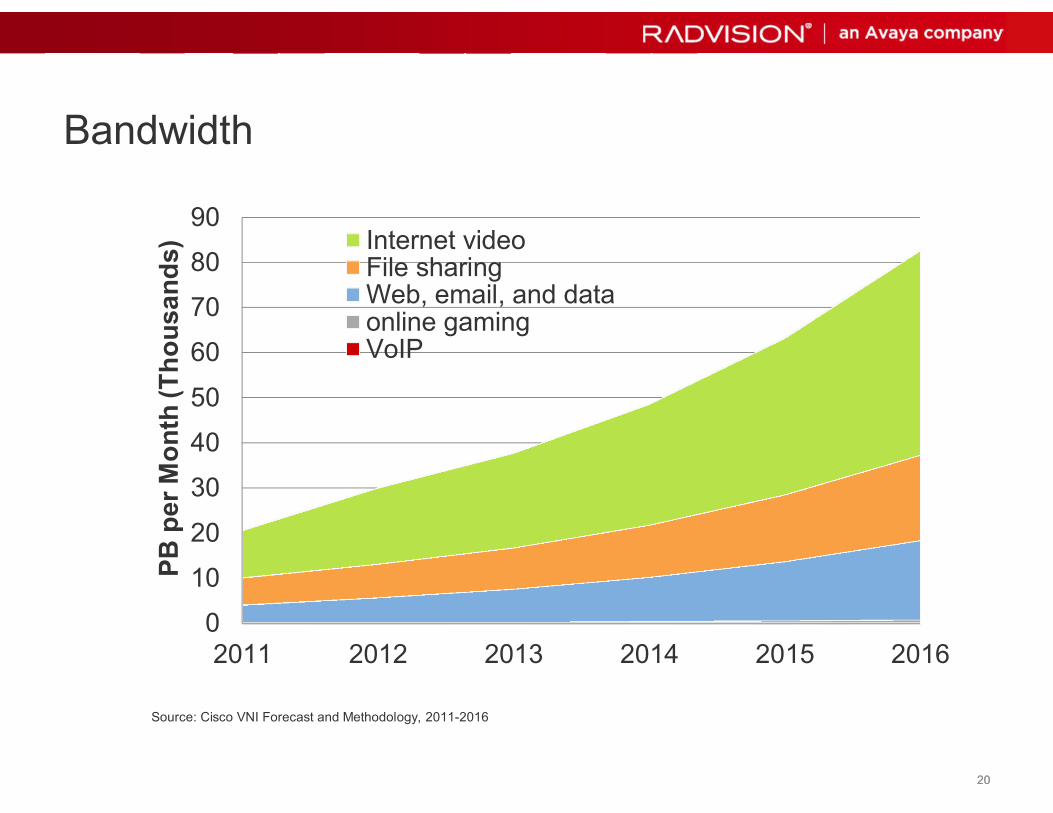

Bandwidth

Source: Cisco VNI Forecast and Methodology, 2011-2016

0

10

20

30

40

50

60

70

80

90

2011 2012 2013 2014 2015 2016

PB

per M

onth

(Th

ousands) Internet video

File sharingWeb, email, and dataonline gamingVoIP

2121

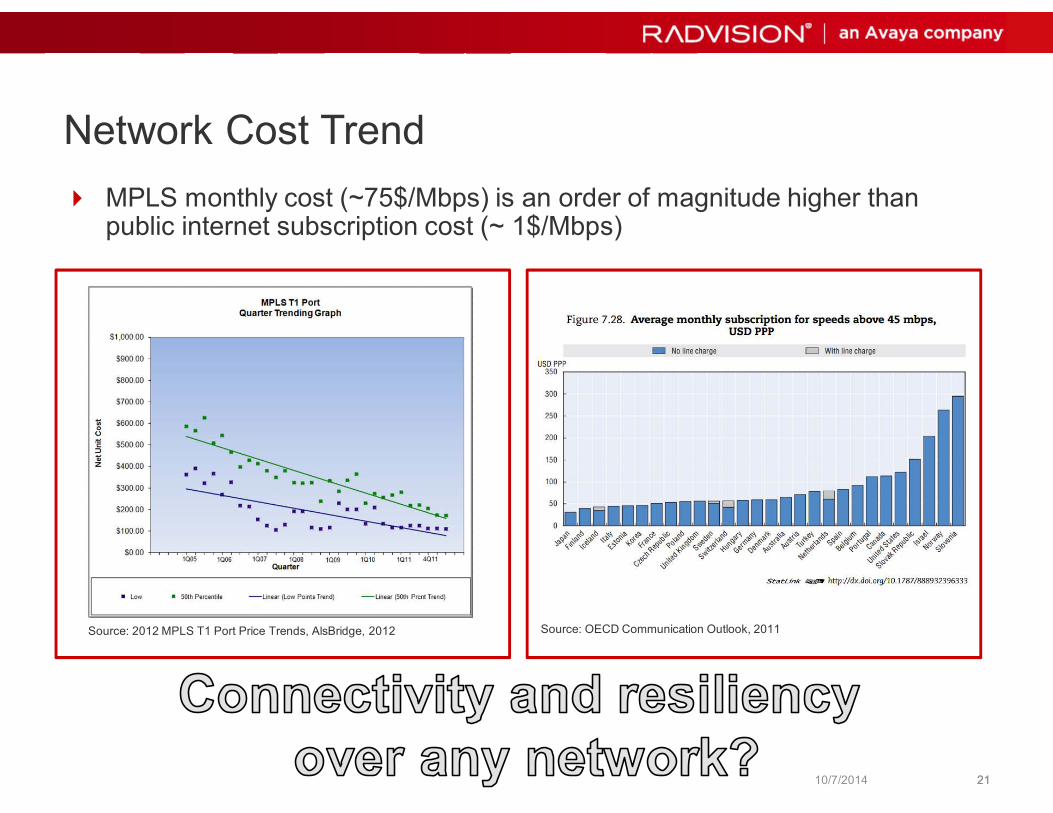

Network Cost Trend

MPLS monthly cost (~75$/Mbps) is an order of magnitude higher than public internet subscription cost (~ 1$/Mbps)

10/7/2014

Source: 2012 MPLS T1 Port Price Trends, AlsBridge, 2012 Source: OECD Communication Outlook, 2011

2222

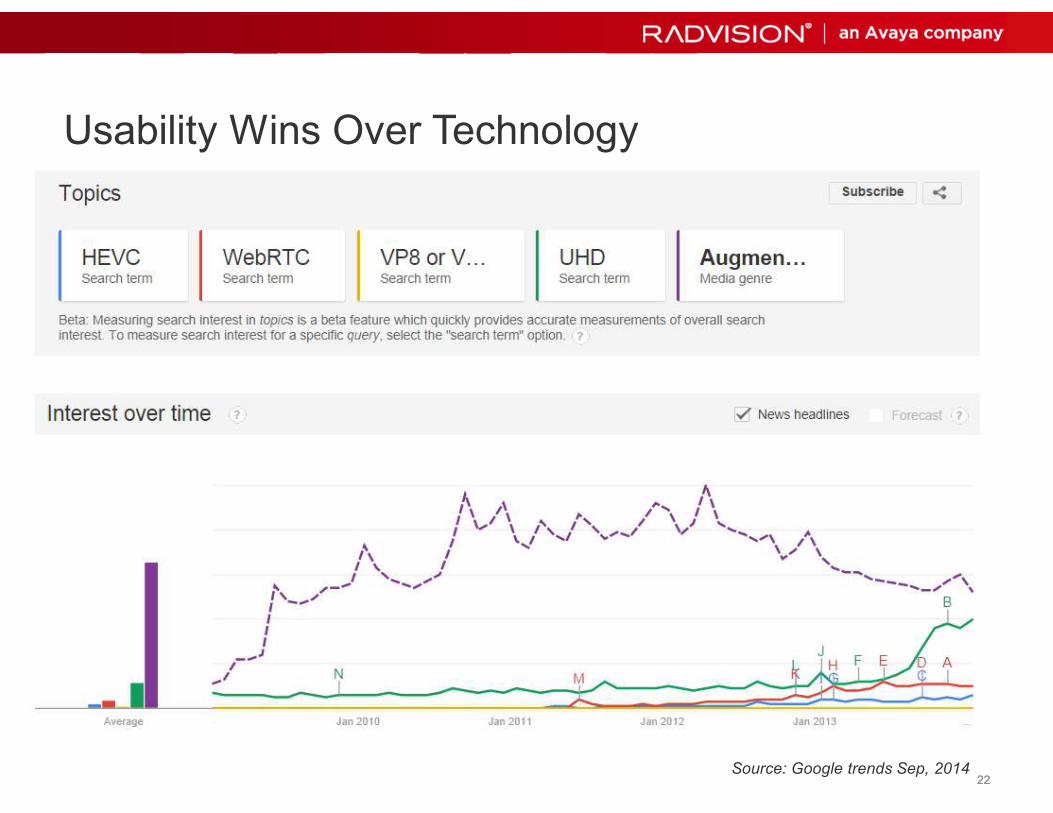

Usability Wins Over Technology

Source: Google trends Sep, 2014

2323

Augmented Reality

2424

Natural User Interfaces

2525

Voice?!

2626

Video!

2727

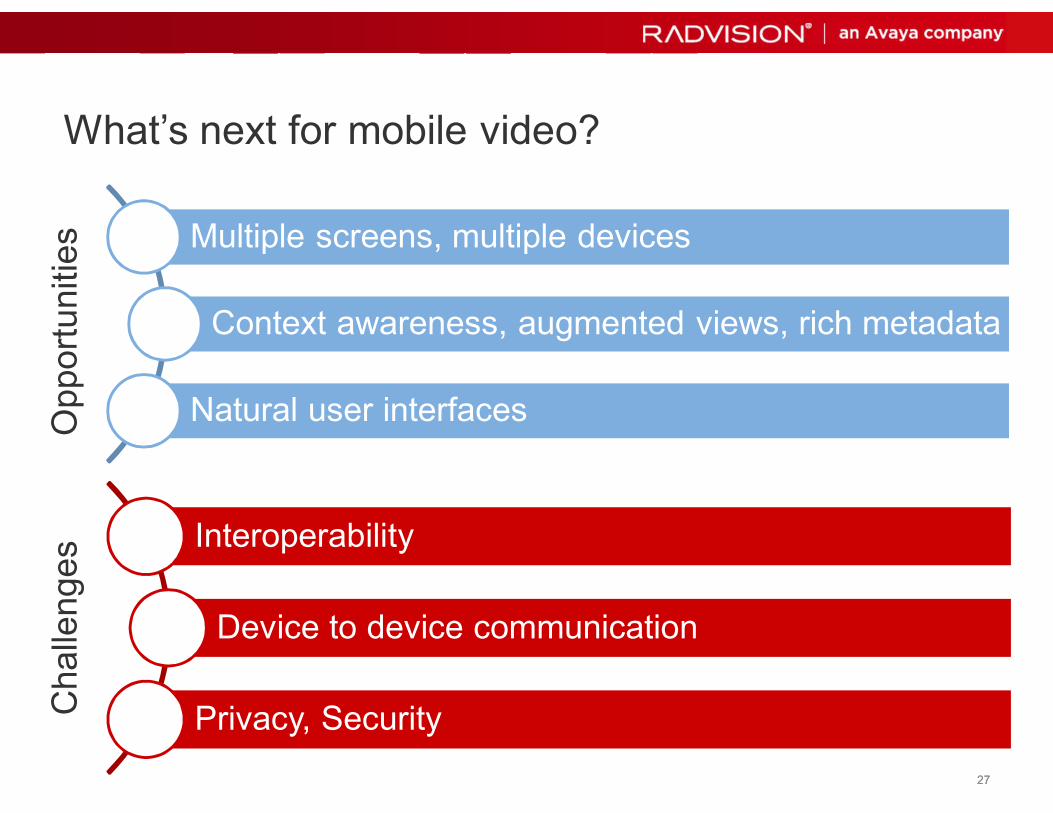

What’s next for mobile video?

Multiple screens, multiple devices

Context awareness, augmented views, rich metadata

Natural user interfaces

Interoperability

Device to device communication

Privacy, Security

Opport

unitie

sC

halle

nges