What We Are Reading Vol.82

60

Emerging Markets Research 9 July 2015 Asia Themes: India Assembling the building blocks • Increasing fiscal revenue is supporting the government’s medium term agenda of raising infrastructure investment. The focus is likely to be on urbanisation, clearing supply bottlenecks through better logistics, stronger infrastructure and ending power and coal shortages, which can raise India’s trend growth rate. • Railways, highways, ports and urban infrastructure projects are likely to be prioritised. Along with coal and power, we estimate that the government could spend an additional USD190bn in the next five years on these sectors. • Our input output analysis on value addition indicates that India’s potential growth rate could rise by more than 1.4pp on this investment. This implies that India could be enjoying close to double-digit real GDP growth by FY20, even if only 75% of the planned infrastructure investments are realised. • For urbanisation, the government’s smart cities initiative will complement the planned creation of several greenfield cities across the country. Higher investment in urban projects should also improve productivity in next five years. • The government is targeting ‘24x7’ power availability across the country by 2019. We believe that the first obstacle of fuel availability has been resolved, and the nation’s power deficit is shrinking, a trend that looks set to continue, based on planned capacity additions. • The highways construction programme could see additional spending of INR2trn in the next five years, which should strengthen connectivity and fundamentally lower underlying inflation pressures. Railways and ports may see potential additional investments of INR5trn and INR1trn respectively in capacity building, which should further improve economic connectivity and reduce the cost of doing business in India. • We believe execution risks will persist in India, given lack of clarity on land acquisition rules, issues of NPAs in the banking sector, and generally poor demand conditions, both domestically and globally. Headwinds for growth may also increase if the logistical improvements are not coordinated, which may render some investments to be unproductive. Rahul Bajoria +65 6308 3511 [email protected] Barclays Bank, Singapore Siddhartha Sanyal +91 22 6719 6177 [email protected] Barclays Bank, India www.barclays.com PLEASE SEE ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES STARTING AFTER PAGE 23

-

Upload

akhilesh-tripathi -

Category

Documents

-

view

29 -

download

4

Transcript of What We Are Reading Vol.82

Emerging Markets Research 9 July 2015

Asia Themes: India

Assembling the building blocks • Increasing fiscal revenue is supporting the government’s medium term agenda of

raising infrastructure investment. The focus is likely to be on urbanisation, clearing supply bottlenecks through better logistics, stronger infrastructure and ending power and coal shortages, which can raise India’s trend growth rate.

• Railways, highways, ports and urban infrastructure projects are likely to be prioritised. Along with coal and power, we estimate that the government could spend an additional USD190bn in the next five years on these sectors.

• Our input output analysis on value addition indicates that India’s potential growth rate could rise by more than 1.4pp on this investment. This implies that India could be enjoying close to double-digit real GDP growth by FY20, even if only 75% of the planned infrastructure investments are realised.

• For urbanisation, the government’s smart cities initiative will complement the planned creation of several greenfield cities across the country. Higher investment in urban projects should also improve productivity in next five years.

• The government is targeting ‘24x7’ power availability across the country by 2019. We believe that the first obstacle of fuel availability has been resolved, and the nation’s power deficit is shrinking, a trend that looks set to continue, based on planned capacity additions.

• The highways construction programme could see additional spending of INR2trn in the next five years, which should strengthen connectivity and fundamentally lower underlying inflation pressures. Railways and ports may see potential additional investments of INR5trn and INR1trn respectively in capacity building, which should further improve economic connectivity and reduce the cost of doing business in India.

• We believe execution risks will persist in India, given lack of clarity on land acquisition rules, issues of NPAs in the banking sector, and generally poor demand conditions, both domestically and globally. Headwinds for growth may also increase if the logistical improvements are not coordinated, which may render some investments to be unproductive.

Rahul Bajoria +65 6308 3511 [email protected] Barclays Bank, Singapore Siddhartha Sanyal +91 22 6719 6177 [email protected] Barclays Bank, India www.barclays.com

PLEASE SEE ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES STARTING AFTER PAGE 23

70093436

Highlight

70093436

Highlight

70093436

Highlight

Barclays | Asia Themes: India

INFRASTRUCTURE AND GROWTH

Infrastructure spending ramp up likely After slightly more than a year in office, the Narendra Modi-led administration is laying out its key policy areas. At the heart of the government’s growth model is a push for greater urbanisation in India. Calling urbanisation an ‘opportunity’ rather than a threat, the government has outlined a structured approach to increase the share of the urban population through greater connectivity, universal access to basic facilities, and boosting manufacturing and services activity. The government, enjoying a fiscal windfall in the wake of lower oil prices, is prioritising infrastructure investment and has outlined five key areas.

• Urbanisation – With the smart cities initiative in place, along with marquee projects like the Delhi-Mumbai Industrial corridor (DMIC), we estimate that the government will spend an additional INR2trn on urban projects above previous trend levels.

• Power and coal – With coal production rising and the government aiming for universal power access, we estimate that an additional INR2trn may be spent in these areas.

• Highways – The government has a 30km/day road construction goal, and is looking to add 10,000km to the highway network, which could involve investment of INR2trn.

• Railways – A key focus area, we think the government could increase spending on the rail network by INR5.0trn on capacity enhancement projects.

• Ports and freight corridors – Along with the highway and railway networks, projects to enhance connectivity are being prioritised for ports and waterways. Port-related investments could rise by INR1trn and improve the ‘last mile’ of transport links, which is expected to boost exports.

In the next five years, we estimate that the government could spend more than INR12trn (~USD190bn, or ~8.5% of GDP) in the above five areas above levels based on past trends. If executed successfully, we think the government will be able to ‘crowd-in’ private investment, and create a long term boost to the economy’s growth potential. Without these extra initiatives, we estimate that the government would only have channelled roughly 1% of GDP per annum towards investments in these sectors. In this report, we examine the government’s infrastructure push and the possible impact on long-term growth.

FIGURE 1 Our estimates show that planned Infra spending may boost growth in the next five years

Projects (INR bn) FY16 FY17 FY18 FY19 FY20

Electricity 8 16 23 31 171

Urban infrastructure projects 30 30 38 53 285

Railways 44 110 132 154 558

Highways 50 67 100 117 571

Ports 10 17 21 21 285

Logistics/efficiency gains 0 322 644 966 1289

Potential increase in value added 143 562 959 1343 3159

Value added (INR bn) FY16 FY17 FY18 FY19 FY20

Potential scenario (100%) 143 562 959 1343 3159

Potential scenario (75% realisation) 110 507 885 1254 2762

Value added (% of nominal GDP) FY16 FY17 FY18 FY19 FY20

Potential scenario (100%) 0.10 0.35 0.53 0.67 1.40

Potential scenario (75% realisation) 0.08 0.32 0.49 0.62 1.22 Source: CEIC, Barclays Research

Narendra Modi’s government is prioritising urbanisation to drive growth

The government may spend an additional INR12trn in next 5 years on infrastructure

9 July 2015 2

70093436

Highlight

70093436

Highlight

70093436

Highlight

70093436

Highlight

70093436

Highlight

70093436

Highlight

70093436

Highlight

70093436

Highlight

Barclays | Asia Themes: India

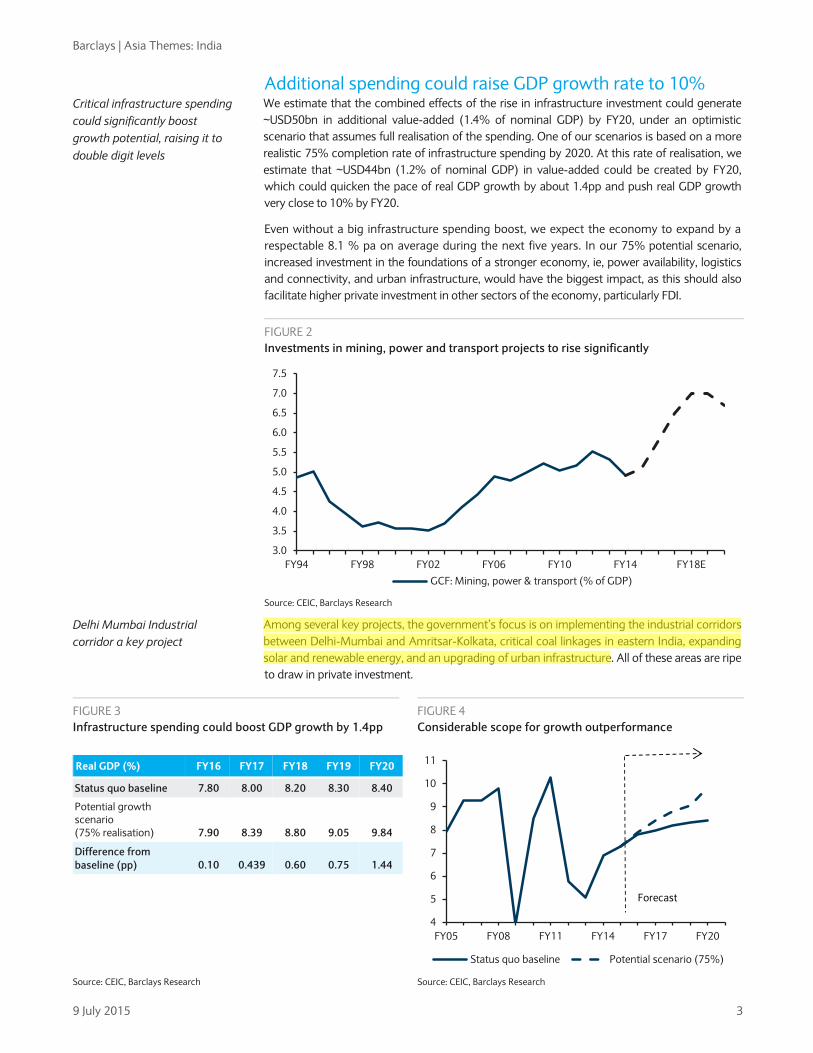

Additional spending could raise GDP growth rate to 10% We estimate that the combined effects of the rise in infrastructure investment could generate ~USD50bn in additional value-added (1.4% of nominal GDP) by FY20, under an optimistic scenario that assumes full realisation of the spending. One of our scenarios is based on a more realistic 75% completion rate of infrastructure spending by 2020. At this rate of realisation, we estimate that ~USD44bn (1.2% of nominal GDP) in value-added could be created by FY20, which could quicken the pace of real GDP growth by about 1.4pp and push real GDP growth very close to 10% by FY20.

Even without a big infrastructure spending boost, we expect the economy to expand by a respectable 8.1 % pa on average during the next five years. In our 75% potential scenario, increased investment in the foundations of a stronger economy, ie, power availability, logistics and connectivity, and urban infrastructure, would have the biggest impact, as this should also facilitate higher private investment in other sectors of the economy, particularly FDI.

Among several key projects, the government’s focus is on implementing the industrial corridors between Delhi-Mumbai and Amritsar-Kolkata, critical coal linkages in eastern India, expanding solar and renewable energy, and an upgrading of urban infrastructure. All of these areas are ripe to draw in private investment.

Critical infrastructure spending could significantly boost growth potential, raising it to double digit levels

FIGURE 2 Investments in mining, power and transport projects to rise significantly

Source: CEIC, Barclays Research

Delhi Mumbai Industrial corridor a key project

FIGURE 3 Infrastructure spending could boost GDP growth by 1.4pp

FIGURE 4 Considerable scope for growth outperformance

Real GDP (%) FY16 FY17 FY18 FY19 FY20

Status quo baseline 7.80 8.00 8.20 8.30 8.40

Potential growth scenario (75% realisation) 7.90 8.39 8.80 9.05 9.84

Difference from baseline (pp) 0.10 0.439 0.60 0.75 1.44

Source: CEIC, Barclays Research Source: CEIC, Barclays Research

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

FY94 FY98 FY02 FY06 FY10 FY14 FY18EGCF: Mining, power & transport (% of GDP)

4

5

6

7

8

9

10

11

FY05 FY08 FY11 FY14 FY17 FY20

Status quo baseline Potential scenario (75%)

Forecast

9 July 2015 3

70093436

Highlight

Barclays | Asia Themes: India

URBANISATION AND SMART CITIES

Growing smartly – ‘Smart’ cities to lead the way Urban areas have powered India’s growth over the past two decades and now generate c63% of India’s GDP – up from c45% in 1990. We believe India’s large population and low GDP per capita indicate that urbanisation trends have significant scope to accelerate further. To facilitate this, the quality of urbanisation needs to be paid attention considered as well. One of the cornerstone projects initiated by Narendra Modi in his first year is the ‘Make in India program’. Behind the ambition of becoming a manufacturing champion, lies a structured approach to increasing urbanisation.

Indian cities are growing rapidly, but they are also expanding in an unorganised manner. Decades of internal migration have pressured the existing infrastructure systems. In the absence of structured planning and poor execution of actual projects, the quality of living has been declining in many of India’s cities. Under the moniker of ‘smart cities’, the government wants to create new ‘urban clusters’, which are expected to be both a driver of growth and reduce the burden on existing cities. Even if past trends are maintained, we estimate that 35% of India’s population could live in cities by 2020 and contribute 70-75% of its GDP.

India’s urbanisation has increased, but development has been uneven India’s urbanisation rate, as per the 2011 census, stood at 31.6%, up from 27.8% in 2001, with only seven provinces reporting a higher than national average in this period. While Western and Southern India have been urbanising quickly, progress in Northern and Eastern India has been slower. It is in these two regions that we think PM Modi’s smart cities concept could have the greatest impact through reinvigorating urbanisation and industrialisation trends in these states. In this context, we think the dedicated freight corridor planned for Eastern India has potential to correct the country’s urbanisation imbalance, though the greenfield urban clusters under construction or planned have a strong Western India bias. Little progress is visible in terms of planning more ‘urban clusters’ in Eastern or Northern India.

FIGURE 5 Share of GDP produced from urban regions

FIGURE 6 Urban India powered the last decade’s growth acceleration*

Source: McKinsey Global Institute (2012), Ministry of Urban Development (MoUD), Barclays Research

Note: *Chart shows contribution to total GDP growth. Source: RBI, MoUD, Barclays Research

Urban India contributes roughly 63% of total GDP

Cities in India are growing rapidly, and could generate 70-75% of GDP by 2020

India has been urbanising, but in an uneven manner

84

65

7678

63

50

55

60

65

70

75

80

85

90

United States

Western Europe

Latin America

China India

%

1.8 1.4 2.7 3.4

5.7 2.0 1.6

2.6 2.3

1.8

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

1950-51 -1970-71

1970-71 -1980-81

1980-81 -1990-91

1990-91 -2000-01

2000-01 -2009-10

% YoY Urban Rural

9 July 2015 4

70093436

Highlight

70093436

Highlight

Barclays | Asia Themes: India

‘Smart’ cities – From policy to action One of the key themes of Prime Minister Narendra Modi’s election campaign was the use of urbanisation as a catalyst for growth. Apart from resolving infrastructure bottlenecks, the government plans to set up 100 ‘smart’ cities, which involves upgrading the infrastructure in existing tier 1 and tier 2 cities, and setting up new urban clusters to manage the pace and quality of urbanisation. For instance, among the facilities proposed for these cities are such things are the availability of underground parking, adequate digital connectivity, smart power grids, piped gas networks, adequate public transport and environmentally-friendly surroundings to enhance quality of life.

According to a report by the McKinsey Global Institute in 2010 (Urbanisation in India), in the next 20 years India could have 68 cities with a population of more than one million – up from 42 in 2010. Some interesting case studies for the ‘smart cities’ under construction in India are New Raipur (Chhattisgarh), Dholera Investment region (Gujarat) and Lavasa (Maharashtra), which are cities being constructed from scratch with plans to integrate technology in day-to-day management of their infrastructure.

Naya Raipur – A smart city in the making since 2008 Naya Raipur (New Raipur) is an administrative capital being built in Central India, in the state of Chhattisgarh. Construction began in 2008. Administrative capitals are not a new thing in India, and many states have constructed such cities previously (ie, Bhubaneswar, Gandhinagar, and Chandigarh). Built over 80sqkm, the city has already seen INR40bn of investment, and it is expected to have more than half a million resident by 2030. The city is also expected to house the prestigious Indian Institute of Management (IIM) and Indian institute of Technology (IIT), which should help to boost its appeal. The city also possesses one of the best rated cricket stadiums in India.

The proposed Delhi-Mumbai industrial corridor, which could be India’s largest infrastructure project, includes plans for seven new city townships across the states it passes through to promote urbanisation of these areas. Similar projects in Andhra Pradesh (Amravati), Gujarat (Dholera), Rajasthan (Neemrana) and in the North East are expected to get underway in the next few years.

FIGURE 9 Several Greenfield cities/urban clusters already under-way

FIGURE 10 Brownfield city up gradation, a major part of the smart cities initiative

Source: Various media sources, MoUD, Barclays Research Source: Various media sources, MoUD, Barclays Research

Smart cities initiative is largely aimed at planned urbanisation

Several greenfield cities are under construction in India

DMIC itself will have 7 urban clusters, which will be built from scratch

City State Partner Country

Dholera Gujarat Japan

Kochi smart city Kerala -

Lavasa Maharashtra -

Naya Raipur Chhattisgarh -

Amravati Andhra Pradesh Singapore

Shendra Bidkin Maharashtra Japan

GIFT city Gujarat -

Dighi Maharashtra -

Greenfield projects

City State Partner Country

Ajmer Rajasthan US

Allahabad Uttar Pradesh US

Shimla Himachal Pradesh France

Varanasi Uttar Pradesh Japan

Vizag Andhra Pradesh US

Pondicherry Tamil Nadu France

Nagpur Maharashtra France

Delhi Delhi NCR Spain

Brownfield projects

9 July 2015 6

70093436

Highlight

70093436

Highlight

Barclays | Asia Themes: India

Electricity sector – powering up To make the planned smart cities and industrial/manufacturing clusters viable, the government has set an ambitious target of providing 24x7 electricity access to every household by 2019. In order to achieve this target, the government needs to take significant steps not just in generation, but also in the transmission and distribution of power.

FIGURE 11 High growth needs considerable addition in power capacity

Source: CEIC, Barclays Research

Access to reliable electricity supply remains a major issue for India, with only 75% of the population having access to power. An increase in generating capacity and improvement in fuel availability goes a long way in solving the problems of power availability. But transmission and distribution still remain a challenge. India’s power consumption still remains low, as India’s per capita GDP is still very low. While there has been considerable capacity augmentation in the last 10 years, the sector has been plagued by issues of distribution, and fuel shortages, which are being unclogged gradually.

India has been adding ~20GW per year of electricity capacity for last 3-4 years, and this trend may slow down in coming years, especially in conventional generation capacity like coal and gas. India’s per capita power consumption has risen considerably in last two decades, but still remains considerably below its peers, both in the region and globally.

GJ

TNMHHR

MPRJ

CG

KR

JHAP

OD

PN

WB

UP

0

5

10

15

20

25

6.0 7.0 8.0 9.0 10.0

Pow

er c

apac

ity (%

, CA

GR)

GSDP (% growth between FY06-FY15)

Power infrastructure being planned alongside urbanisation

Government is targeting 24x7 power access by 2019

FIGURE 12 Net capacity addition has been rising significantly

FIGURE 13 Bulk of power generation capacity is coal based

Source: CEIC, Barclays Research Source: CEIC, Barclays Research

Power capacity addition is impressive, but utilisation is not

0

5

10

15

20

25

May-05 May-07 May-09 May-11 May-13 May-15

(12m rolling sum, GW)

Thermal HydroOthers Power additional capacity

Thermal70%

Hydro16%

Others14% FY 15

9 July 2015 7

70093436

Highlight

Barclays | Asia Themes: India

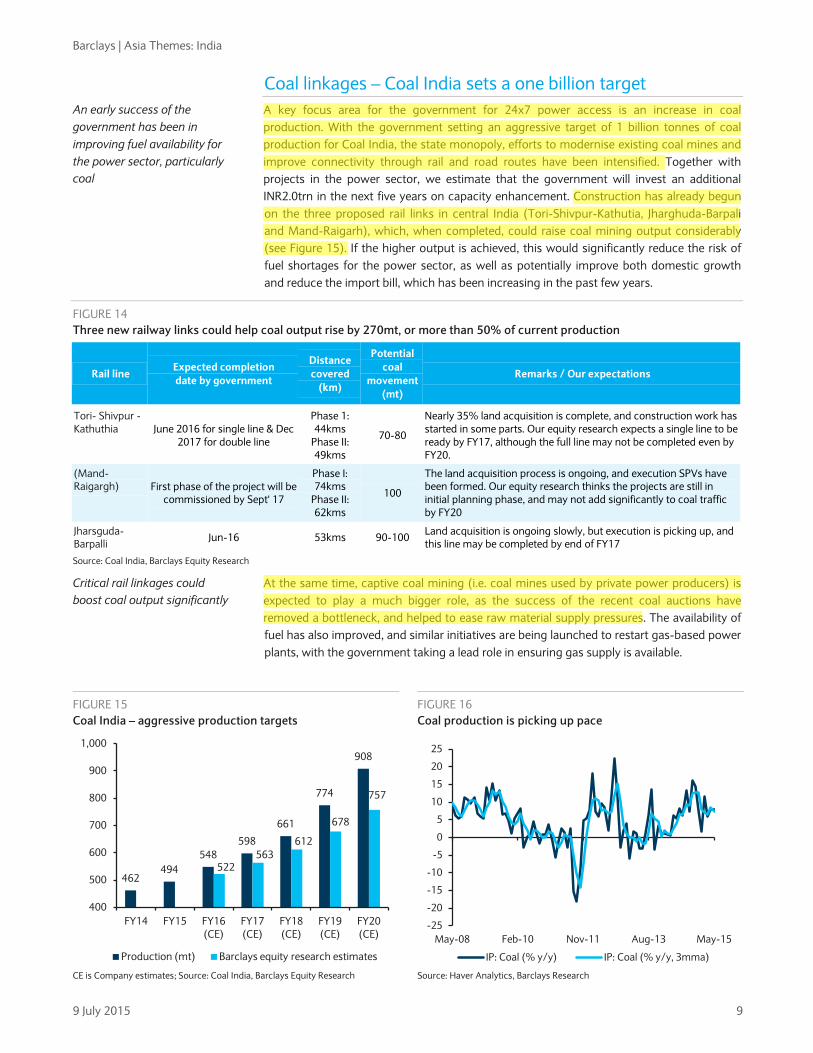

Coal linkages – Coal India sets a one billion target A key focus area for the government for 24x7 power access is an increase in coal production. With the government setting an aggressive target of 1 billion tonnes of coal production for Coal India, the state monopoly, efforts to modernise existing coal mines and improve connectivity through rail and road routes have been intensified. Together with projects in the power sector, we estimate that the government will invest an additional INR2.0trn in the next five years on capacity enhancement. Construction has already begun on the three proposed rail links in central India (Tori-Shivpur-Kathutia, Jharghuda-Barpali and Mand-Raigarh), which, when completed, could raise coal mining output considerably (see Figure 15). If the higher output is achieved, this would significantly reduce the risk of fuel shortages for the power sector, as well as potentially improve both domestic growth and reduce the import bill, which has been increasing in the past few years.

FIGURE 14 Three new railway links could help coal output rise by 270mt, or more than 50% of current production

Rail line Expected completion date by government

Distance covered

(km)

Potential coal

movement (mt)

Remarks / Our expectations

Tori- Shivpur - Kathuthia June 2016 for single line & Dec

2017 for double line

Phase 1: 44kms

Phase II: 49kms

70-80

Nearly 35% land acquisition is complete, and construction work has started in some parts. Our equity research expects a single line to be ready by FY17, although the full line may not be completed even by FY20.

(Mand- Raigargh) First phase of the project will be

commissioned by Sept' 17

Phase I: 74kms

Phase II: 62kms

100

The land acquisition process is ongoing, and execution SPVs have been formed. Our equity research thinks the projects are still in initial planning phase, and may not add significantly to coal traffic by FY20

Jharsguda-Barpalli Jun-16 53kms 90-100 Land acquisition is ongoing slowly, but execution is picking up, and

this line may be completed by end of FY17

Source: Coal India, Barclays Equity Research

At the same time, captive coal mining (i.e. coal mines used by private power producers) is expected to play a much bigger role, as the success of the recent coal auctions have removed a bottleneck, and helped to ease raw material supply pressures. The availability of fuel has also improved, and similar initiatives are being launched to restart gas-based power plants, with the government taking a lead role in ensuring gas supply is available.

An early success of the government has been in improving fuel availability for the power sector, particularly coal

Critical rail linkages could boost coal output significantly

FIGURE 15 Coal India – aggressive production targets

FIGURE 16 Coal production is picking up pace

CE is Company estimates; Source: Coal India, Barclays Equity Research Source: Haver Analytics, Barclays Research

462494

548598

661

774

908

522563

612

678

757

400

500

600

700

800

900

1,000

FY14 FY15 FY16 (CE)

FY17 (CE)

FY18 (CE)

FY19 (CE)

FY20 (CE)

Production (mt) Barclays equity research estimates

-25

-20

-15

-10

-5

0

5

10

15

20

25

May-08 Feb-10 Nov-11 Aug-13 May-15

IP: Coal (% y/y) IP: Coal (% y/y, 3mma)

9 July 2015 9

70093436

Highlight

70093436

Highlight

70093436

Highlight

Barclays | Asia Themes: India

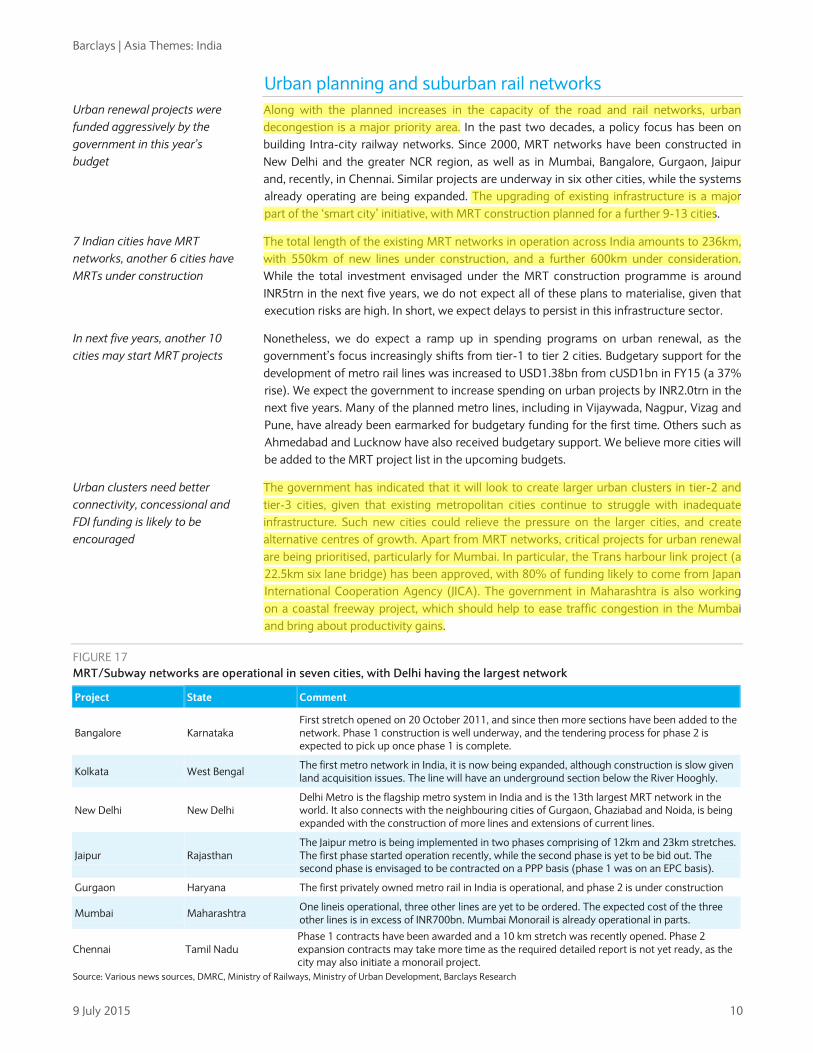

Urban planning and suburban rail networks Along with the planned increases in the capacity of the road and rail networks, urban decongestion is a major priority area. In the past two decades, a policy focus has been on building Intra-city railway networks. Since 2000, MRT networks have been constructed in New Delhi and the greater NCR region, as well as in Mumbai, Bangalore, Gurgaon, Jaipur and, recently, in Chennai. Similar projects are underway in six other cities, while the systems already operating are being expanded. The upgrading of existing infrastructure is a major part of the ‘smart city’ initiative, with MRT construction planned for a further 9-13 cities.

The total length of the existing MRT networks in operation across India amounts to 236km, with 550km of new lines under construction, and a further 600km under consideration. While the total investment envisaged under the MRT construction programme is around INR5trn in the next five years, we do not expect all of these plans to materialise, given that execution risks are high. In short, we expect delays to persist in this infrastructure sector.

Nonetheless, we do expect a ramp up in spending programs on urban renewal, as the government’s focus increasingly shifts from tier-1 to tier 2 cities. Budgetary support for the development of metro rail lines was increased to USD1.38bn from cUSD1bn in FY15 (a 37% rise). We expect the government to increase spending on urban projects by INR2.0trn in the next five years. Many of the planned metro lines, including in Vijaywada, Nagpur, Vizag and Pune, have already been earmarked for budgetary funding for the first time. Others such as Ahmedabad and Lucknow have also received budgetary support. We believe more cities will be added to the MRT project list in the upcoming budgets.

The government has indicated that it will look to create larger urban clusters in tier-2 and tier-3 cities, given that existing metropolitan cities continue to struggle with inadequate infrastructure. Such new cities could relieve the pressure on the larger cities, and create alternative centres of growth. Apart from MRT networks, critical projects for urban renewal are being prioritised, particularly for Mumbai. In particular, the Trans harbour link project (a 22.5km six lane bridge) has been approved, with 80% of funding likely to come from Japan International Cooperation Agency (JICA). The government in Maharashtra is also working on a coastal freeway project, which should help to ease traffic congestion in the Mumbai and bring about productivity gains.

FIGURE 17 MRT/Subway networks are operational in seven cities, with Delhi having the largest network

Project State Comment

Bangalore Karnataka First stretch opened on 20 October 2011, and since then more sections have been added to the network. Phase 1 construction is well underway, and the tendering process for phase 2 is expected to pick up once phase 1 is complete.

Kolkata West Bengal The first metro network in India, it is now being expanded, although construction is slow given land acquisition issues. The line will have an underground section below the River Hooghly.

New Delhi New Delhi Delhi Metro is the flagship metro system in India and is the 13th largest MRT network in the world. It also connects with the neighbouring cities of Gurgaon, Ghaziabad and Noida, is being expanded with the construction of more lines and extensions of current lines.

Jaipur Rajasthan The Jaipur metro is being implemented in two phases comprising of 12km and 23km stretches. The first phase started operation recently, while the second phase is yet to be bid out. The second phase is envisaged to be contracted on a PPP basis (phase 1 was on an EPC basis).

Gurgaon Haryana The first privately owned metro rail in India is operational, and phase 2 is under construction

Mumbai Maharashtra One lineis operational, three other lines are yet to be ordered. The expected cost of the three other lines is in excess of INR700bn. Mumbai Monorail is already operational in parts.

Chennai Tamil Nadu Phase 1 contracts have been awarded and a 10 km stretch was recently opened. Phase 2 expansion contracts may take more time as the required detailed report is not yet ready, as the city may also initiate a monorail project.

Source: Various news sources, DMRC, Ministry of Railways, Ministry of Urban Development, Barclays Research

Urban renewal projects were funded aggressively by the government in this year’s budget

7 Indian cities have MRT networks, another 6 cities have MRTs under construction

In next five years, another 10 cities may start MRT projects

Urban clusters need better connectivity, concessional and FDI funding is likely to be encouraged

9 July 2015 10

70093436

Highlight

70093436

Highlight

70093436

Highlight

70093436

Highlight

Barclays | Asia Themes: India

RAILWAYS, HIGHWAYS AND PORT CONNECTIVITY

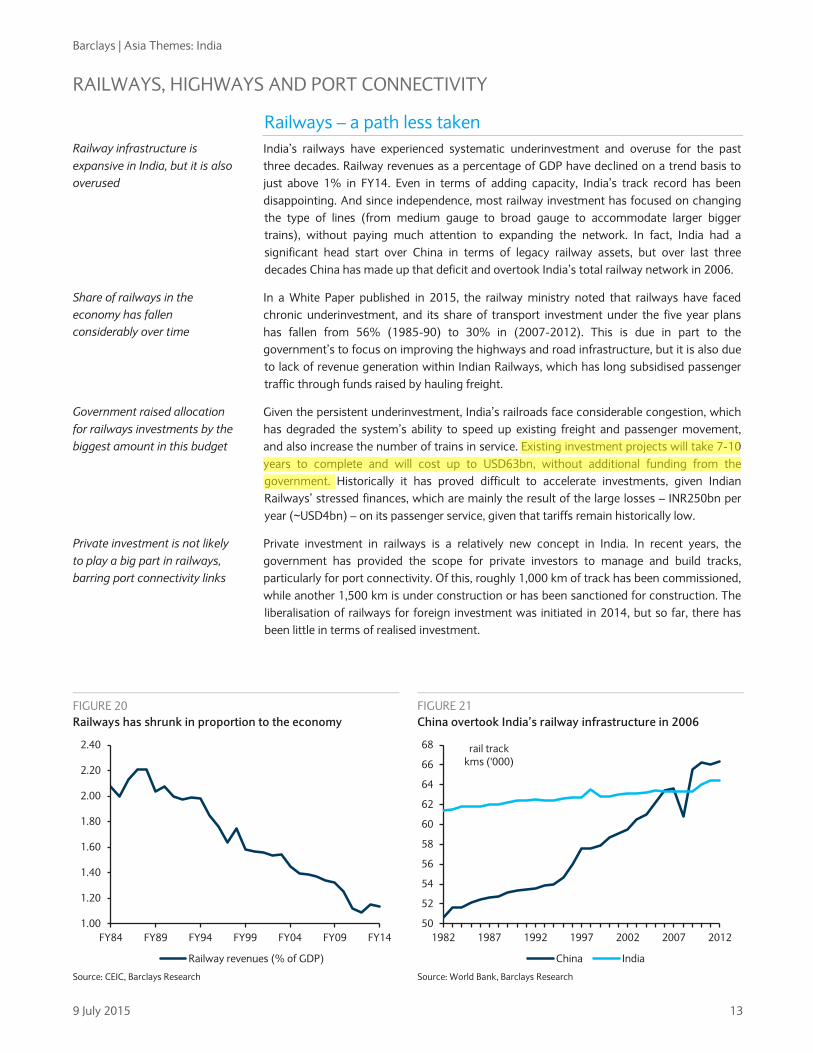

Railways – a path less taken India’s railways have experienced systematic underinvestment and overuse for the past three decades. Railway revenues as a percentage of GDP have declined on a trend basis to just above 1% in FY14. Even in terms of adding capacity, India’s track record has been disappointing. And since independence, most railway investment has focused on changing the type of lines (from medium gauge to broad gauge to accommodate larger bigger trains), without paying much attention to expanding the network. In fact, India had a significant head start over China in terms of legacy railway assets, but over last three decades China has made up that deficit and overtook India’s total railway network in 2006.

In a White Paper published in 2015, the railway ministry noted that railways have faced chronic underinvestment, and its share of transport investment under the five year plans has fallen from 56% (1985-90) to 30% in (2007-2012). This is due in part to the government’s to focus on improving the highways and road infrastructure, but it is also due to lack of revenue generation within Indian Railways, which has long subsidised passenger traffic through funds raised by hauling freight.

Given the persistent underinvestment, India’s railroads face considerable congestion, which has degraded the system’s ability to speed up existing freight and passenger movement, and also increase the number of trains in service. Existing investment projects will take 7-10 years to complete and will cost up to USD63bn, without additional funding from the government. Historically it has proved difficult to accelerate investments, given Indian Railways’ stressed finances, which are mainly the result of the large losses – INR250bn per year (~USD4bn) – on its passenger service, given that tariffs remain historically low.

Private investment in railways is a relatively new concept in India. In recent years, the government has provided the scope for private investors to manage and build tracks, particularly for port connectivity. Of this, roughly 1,000 km of track has been commissioned, while another 1,500 km is under construction or has been sanctioned for construction. The liberalisation of railways for foreign investment was initiated in 2014, but so far, there has been little in terms of realised investment.

FIGURE 20 Railways has shrunk in proportion to the economy

FIGURE 21 China overtook India’s railway infrastructure in 2006

Source: CEIC, Barclays Research Source: World Bank, Barclays Research

Railway infrastructure is expansive in India, but it is also overused

Share of railways in the economy has fallen considerably over time

Government raised allocation for railways investments by the biggest amount in this budget

Private investment is not likely to play a big part in railways, barring port connectivity links

1.00

1.20

1.40

1.60

1.80

2.00

2.20

2.40

FY84 FY89 FY94 FY99 FY04 FY09 FY14

Railway revenues (% of GDP)

50

52

54

56

58

60

62

64

66

68

1982 1987 1992 1997 2002 2007 2012

rail track kms ('000)

China India

9 July 2015 13

70093436

Highlight

Barclays | Asia Themes: India

Railways now focusing on completing legacy projects Railways are a major investment focus for the Modi government. In its first full budget, the government allocated a significantly higher sum of money to the railways. But it did not announce a single new project, focusing instead on expediting the completion of 357 legacy projects worth over INR1.8trn (USD28bn). This focus is critical, in our opinion, as the trend of announcing key projects and then not allocating the necessary resources to complete them has been an issue. As the government described it, “spreading the resources too thinly” has created considerable bottlenecks; therefore, shifting the focus to enhancing capacity through project completions is a welcome step, in our view.

In terms of financing, the government has increased budgetary support and also raised tariffs for goods and passengers in order to raise funds. In addition, promised investments from Life Insurance Co of India of INR1.5trn, captive funding from coal miners for freight linkages and private investment (both domestic and foreign) should ensure a significant increase in investments, potentially to INR8.5trn (USD130bn) over next five years.

Prospectively, if the operating ratio of railways improves further (projected at 88.5% in FY15-16), and foreign investments are seen in high-speed rail corridors, internal financing constraints are likely to ease considerably. We expect the government to spend roughly INR5trn (USD79bn) over and above the historical trends, which would be roughly three times the investment seen in the previous five years. This implies that as the railway network expands and operates with more efficiency, its impact on GDP growth, and consequently GDP size, will be significant.

According to analysis by the government’s Chief Economic Adviser, Arvind Subramanian, every unit of investment in railroads boosts output in other sectors by as much as 7.4x. We believe the funding available for railways has improved drastically, and with focus on cutting costs and involving the private sector, the government’s efforts to revive investment is likely to pay-off, especially with improving fiscal dynamics.

Focus is on expediting completion of legacy projects, and increasing track capacity

Financing of railway investments will be a mix of internal revenues, budgetary support and debt securities

Railways internal revenue generation likely to improve with falling fuel costs

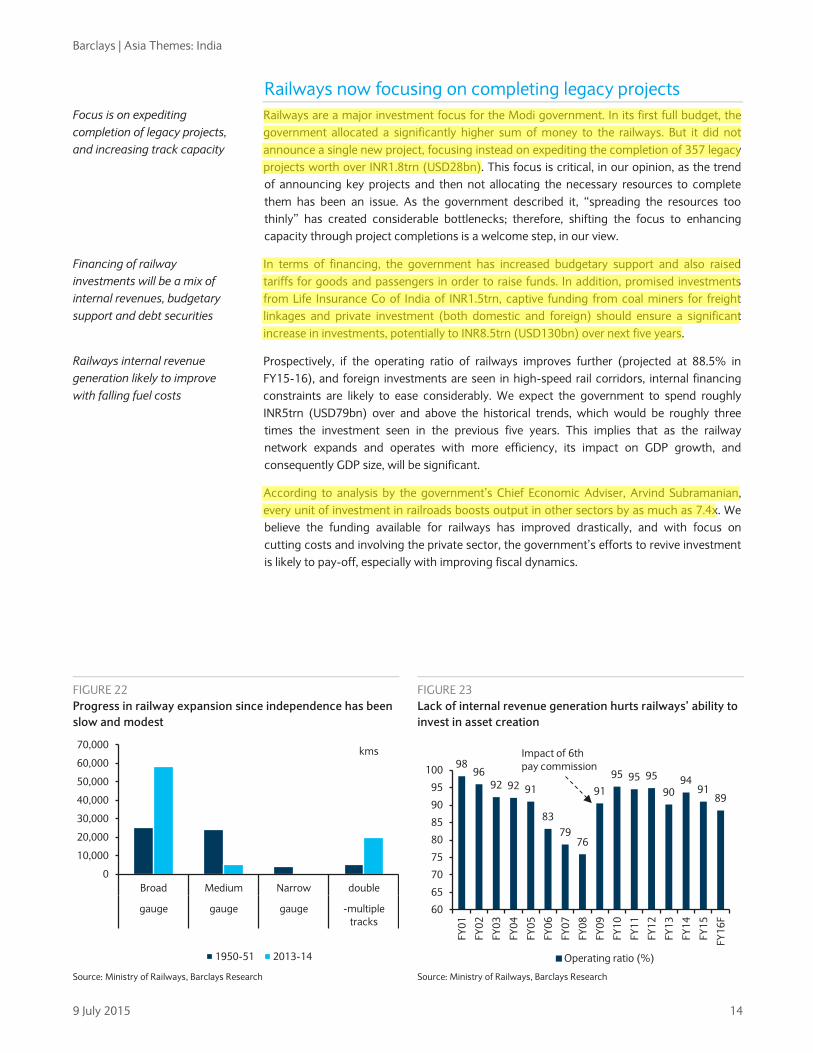

FIGURE 22 Progress in railway expansion since independence has been slow and modest

FIGURE 23 Lack of internal revenue generation hurts railways’ ability to invest in asset creation

Source: Ministry of Railways, Barclays Research Source: Ministry of Railways, Barclays Research

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Broad Medium Narrow double

gauge gauge gauge -multiple tracks

kms

1950-51 2013-14

9896

92 92 91

8379

76

91

95 95 9590

9491

89

60

65

70

75

80

85

90

95

100

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

F

Operating ratio (%)

Impact of 6th pay commission

9 July 2015 14

70093436

Highlight

70093436

Highlight

70093436

Highlight

Barclays | Asia Themes: India

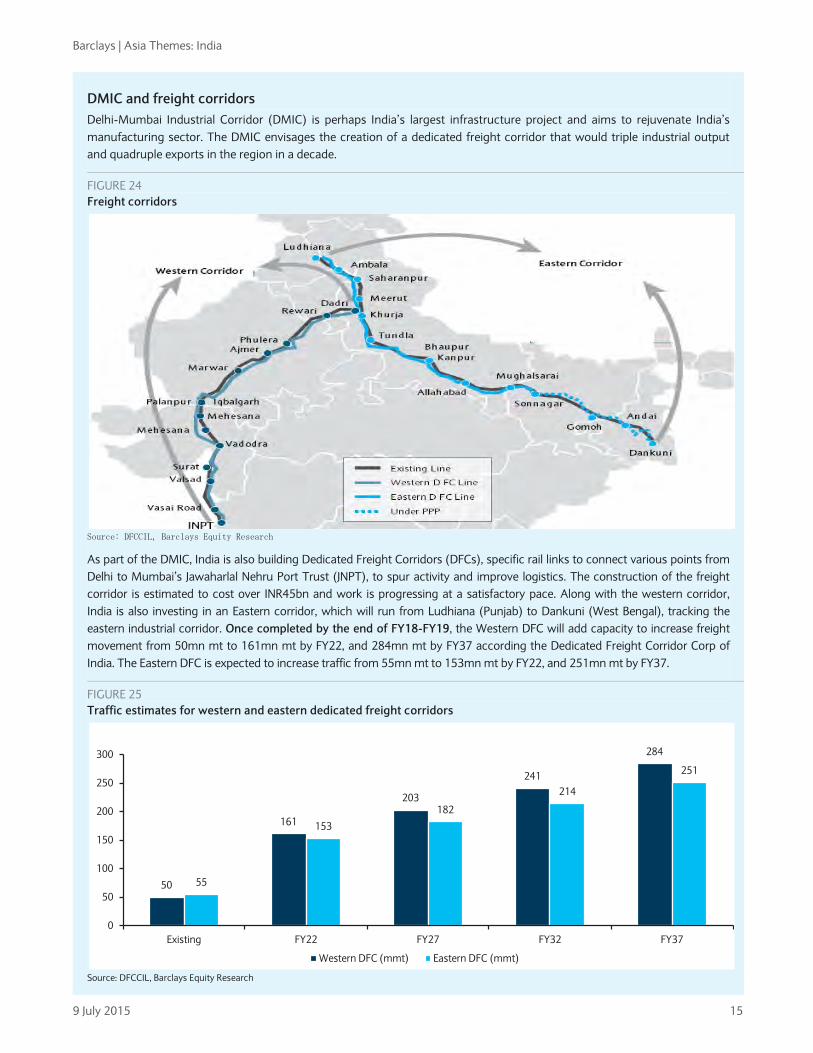

DMIC and freight corridors Delhi-Mumbai Industrial Corridor (DMIC) is perhaps India’s largest infrastructure project and aims to rejuvenate India’s manufacturing sector. The DMIC envisages the creation of a dedicated freight corridor that would triple industrial output and quadruple exports in the region in a decade.

FIGURE 24 Freight corridors

Source: DFCCIL, Barclays Equity Research

As part of the DMIC, India is also building Dedicated Freight Corridors (DFCs), specific rail links to connect various points from Delhi to Mumbai’s Jawaharlal Nehru Port Trust (JNPT), to spur activity and improve logistics. The construction of the freight corridor is estimated to cost over INR45bn and work is progressing at a satisfactory pace. Along with the western corridor, India is also investing in an Eastern corridor, which will run from Ludhiana (Punjab) to Dankuni (West Bengal), tracking the eastern industrial corridor. Once completed by the end of FY18-FY19, the Western DFC will add capacity to increase freight movement from 50mn mt to 161mn mt by FY22, and 284mn mt by FY37 according the Dedicated Freight Corridor Corp of India. The Eastern DFC is expected to increase traffic from 55mn mt to 153mn mt by FY22, and 251mn mt by FY37.

FIGURE 25 Traffic estimates for western and eastern dedicated freight corridors

Source: DFCCIL, Barclays Equity Research

50

161

203

241

284

55

153

182

214

251

0

50

100

150

200

250

300

Existing FY22 FY27 FY32 FY37

Western DFC (mmt) Eastern DFC (mmt)

9 July 2015 15

Barclays | Asia Themes: India

Highways – Reviving the NDA1 legacy The Modi government is prioritising connectivity in railways and highways to boost economic activity. Highway construction, which had gathered significant pace under NDA and UPA1 governments, slowed sharply in recent years. However, with renewed focus and by changing the projects from an “ownership” (BOT) model to a construction project (EPC) model, the government’s tendering process and the pace of construction is improving. This is further aided by a considerable improvement in the fiscal position, which allows the government to transfer some of its higher revenues to the highway construction project.

The government is focusing on three key areas in the highway sector. First, a significant amount of energy is being devoted to removing the bottlenecks on existing projects. According to the ministry of highways, almost one-third of the projects sanctioned during 2011-14 are either behind the schedule or have run into disputes. This means speeding up current projects is a major priority for the government.

Second, the government is focusing on expanding the current network of roads by increasing the number of lanes, from two to up to eight, to increase capacity on existing routes and key national highways. Third, the government is focusing on improving connectivity by taking up critical linkage projects in northeastern and eastern India, and along the country’s borders. The government has set a target of awarding contracts for 10,000 km of roads to be tendered in FY16, up 25% from the previous fiscal year, and the target is likely to increase in the coming years.

Overall, the government intends to spend roughly INR5trn in the next five years on road and highway construction, with a target increase the pace of road construction to 30 km/day, by March 2016. It intends to sustain it until the end of 2019, and we believe the government will spend roughly INR2trn over and above previous estimates. In order to cut costs, the government is also switching to construction of roads made from concrete, rather than bitumen. This will improve the lifecycle of new roads, and for this, the government has launched a centralised cement purchase program (www.inampro.nic.in), through which construction projects can buy cement at 20-30% below market prices. This should help to reduce both costs and graft, by making procurement of raw materials more centralised and transparent.

Along with railways, outlays for road construction have been increased significantly

For faster execution, the government has abandoned the PPP model for EPC based construction contracts

FIGURE 29 Recent dip in state highways is due to their reclassification as national highways

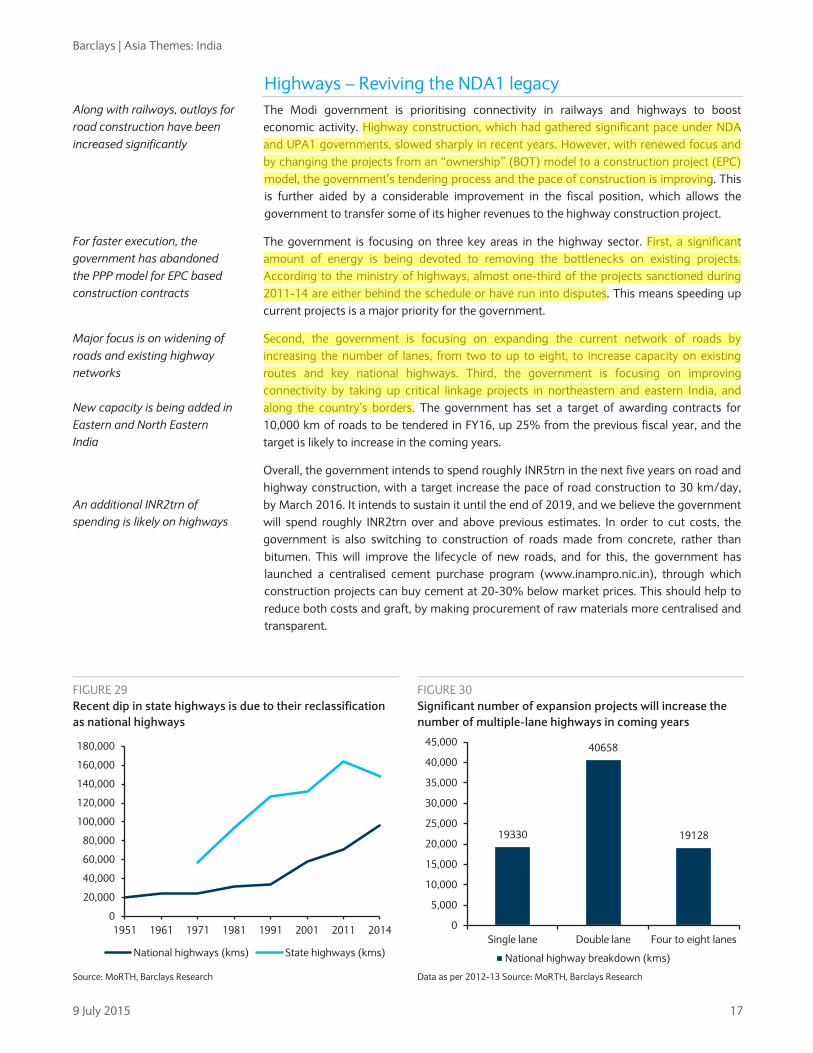

FIGURE 30 Significant number of expansion projects will increase the number of multiple-lane highways in coming years

Source: MoRTH, Barclays Research Data as per 2012-13 Source: MoRTH, Barclays Research

Major focus is on widening of roads and existing highway networks New capacity is being added in Eastern and North Eastern India

An additional INR2trn of spending is likely on highways

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

1951 1961 1971 1981 1991 2001 2011 2014

National highways (kms) State highways (kms)

19330

40658

19128

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Single lane Double lane Four to eight lanes

National highway breakdown (kms)

9 July 2015 17

70093436

Highlight

70093436

Highlight

70093436

Highlight

Barclays | Asia Themes: India

Ports and waterways – Providing ‘last mile’ connectivity A key priority area for the government is to upgrade India’s port infrastructure, to provide ‘last mile’ connectivity, particularly for exporters. Under its Sagar Mala (Ocean’s garland) project, the government plans to modernise, expand or construct 200 commercial ports, including 12 major sea ports, as well as upgrade 101 inland waterways in order to promote cheaper and alternative transportation for both goods and passengers. This blue revolution project is largely focused on eastern India around the River Ganga belt, which accounts for 40% of India’s economic activity.

Work has begun on modernising of key ports, including Mumbai’s JNPT, and more projects are likely to be taken up in coming months. In addition, large satellite ports are likely to be constructed around existing ports – the JNPT, and the ports in Mundra port and Kochin – to ad capacity and ease constraints in these ports. This will be supplemented by investment in private ports, such as the recent announcement of Vizhinjam port in Kerala, an estimated investment of INR40bn. As part of the overall initiative, the ports ministry plans to create 12 new greenfield cities around these major ports, designating them as special coastal economic zones that will have last-mile connectivity with roadways and railways.

These projects are will be connected to economic corridors, such as the DMIC, and should help with the last-stage shipment of goods, largely expected to be for export purposes. The total cost of the upgrade has not been disclosed, but road and rail construction projects, along with expansion of JNPT, already amounts to a total investment of more than USD1bn, with the final cost likely to be several times that figure. Once finished, the sector is likely to see investments of INR1trn more than previously planned. Project funding is likely to be done through a development cess on cargo handled, and also through concessionaire funding from international and national agencies.

FIGURE 32 India’s port upgrades are integrated with its dedicated freight corridors

Source: DFCCIL, Ministry of Shipping, Barclays Research

Haldia

Paradip

Vizag

Ennore

Chennai

TuticorinCochin

Mangalore

Marmagao

JNPT

Mumbai

Kandla

Delhi

Ludhiana

Major government ports -

Freight and industrial corridor

Industrial corridor

India's eastern states have low urbanisation. EDFC will help increase urbanisation

DMIC 's freight corridor connects key ports with manufacturing clusters

India is planning on upgrading 12 major sea ports, along with internal waterways

Work on expansion has already begun in JNPT, India’s largest port

Major ports are likely to be connected to the freight corridors, thus boosting logistics considerably

9 July 2015 19

70093436

Highlight

70093436

Highlight

El

Goldman Sachs Global Investment Research 7

Top of Mind Issue 36

Kenneth Ho and Kinger Lau address equity margin financing and other credit-related threats to China’s growth and financial stability

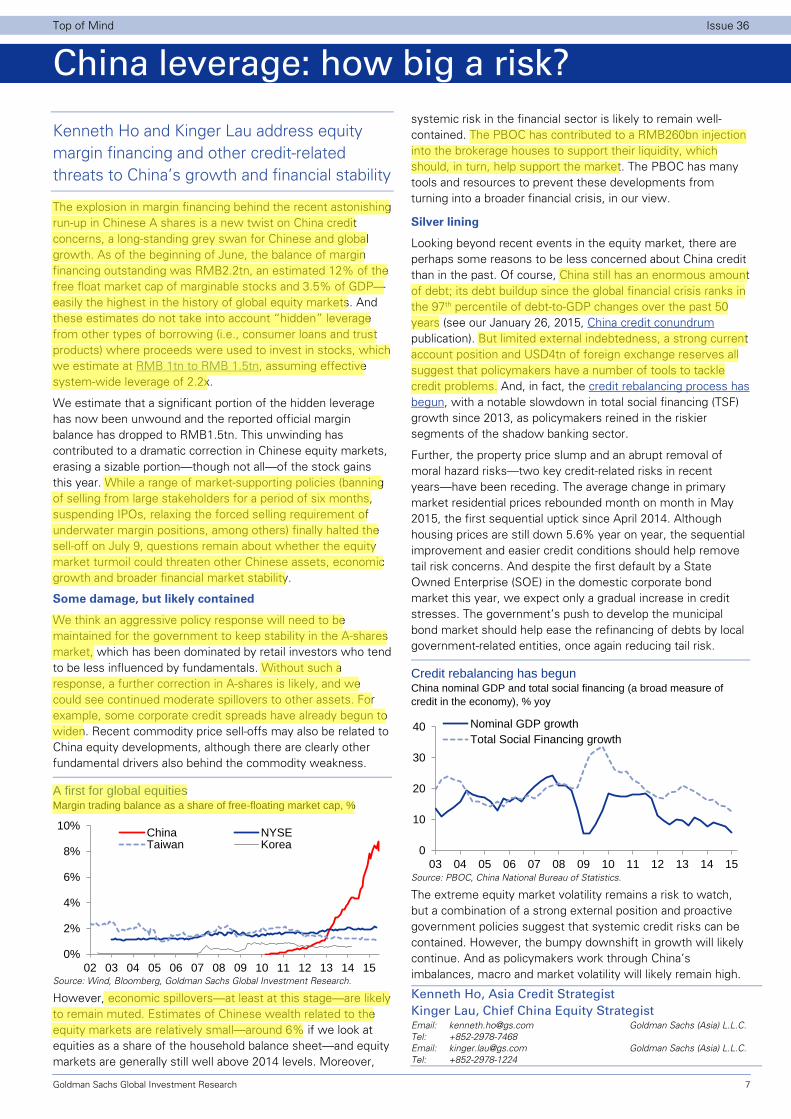

The explosion in margin financing behind the recent astonishing run-up in Chinese A shares is a new twist on China credit concerns, a long-standing grey swan for Chinese and global growth. As of the beginning of June, the balance of margin financing outstanding was RMB2.2tn, an estimated 12% of the free float market cap of marginable stocks and 3.5% of GDP—easily the highest in the history of global equity markets. And these estimates do not take into account “hidden” leverage from other types of borrowing (i.e., consumer loans and trust products) where proceeds were used to invest in stocks, which we estimate at RMB 1tn to RMB 1.5tn, assuming effective system-wide leverage of 2.2x.

We estimate that a significant portion of the hidden leverage has now been unwound and the reported official margin balance has dropped to RMB1.5tn. This unwinding has contributed to a dramatic correction in Chinese equity markets, erasing a sizable portion—though not all—of the stock gains this year. While a range of market-supporting policies (banning of selling from large stakeholders for a period of six months, suspending IPOs, relaxing the forced selling requirement of underwater margin positions, among others) finally halted the sell-off on July 9, questions remain about whether the equity market turmoil could threaten other Chinese assets, economic growth and broader financial market stability.

Some damage, but likely contained

We think an aggressive policy response will need to be maintained for the government to keep stability in the A-shares market, which has been dominated by retail investors who tend to be less influenced by fundamentals. Without such a response, a further correction in A-shares is likely, and we could see continued moderate spillovers to other assets. For example, some corporate credit spreads have already begun to widen. Recent commodity price sell-offs may also be related to China equity developments, although there are clearly other fundamental drivers also behind the commodity weakness.

A first for global equities Margin trading balance as a share of free-floating market cap, %

Source: Wind, Bloomberg, Goldman Sachs Global Investment Research.

However, economic spillovers—at least at this stage—are likely to remain muted. Estimates of Chinese wealth related to the equity markets are relatively small—around 6% if we look at equities as a share of the household balance sheet—and equity markets are generally still well above 2014 levels. Moreover,

systemic risk in the financial sector is likely to remain well-contained. The PBOC has contributed to a RMB260bn injection into the brokerage houses to support their liquidity, which should, in turn, help support the market. The PBOC has many tools and resources to prevent these developments from turning into a broader financial crisis, in our view.

Silver lining

Looking beyond recent events in the equity market, there are perhaps some reasons to be less concerned about China credit than in the past. Of course, China still has an enormous amount of debt; its debt buildup since the global financial crisis ranks in the 97th percentile of debt-to-GDP changes over the past 50 years (see our January 26, 2015, China credit conundrum publication). But limited external indebtedness, a strong current account position and USD4tn of foreign exchange reserves all suggest that policymakers have a number of tools to tackle credit problems. And, in fact, the credit rebalancing process has begun, with a notable slowdown in total social financing (TSF) growth since 2013, as policymakers reined in the riskier segments of the shadow banking sector.

Further, the property price slump and an abrupt removal of moral hazard risks—two key credit-related risks in recent years—have been receding. The average change in primary market residential prices rebounded month on month in May 2015, the first sequential uptick since April 2014. Although housing prices are still down 5.6% year on year, the sequential improvement and easier credit conditions should help remove tail risk concerns. And despite the first default by a State Owned Enterprise (SOE) in the domestic corporate bond market this year, we expect only a gradual increase in credit stresses. The government’s push to develop the municipal bond market should help ease the refinancing of debts by local government-related entities, once again reducing tail risk.

Credit rebalancing has begun China nominal GDP and total social financing (a broad measure of credit in the economy), % yoy

Source: PBOC, China National Bureau of Statistics.

The extreme equity market volatility remains a risk to watch, but a combination of a strong external position and proactive government policies suggest that systemic credit risks can be contained. However, the bumpy downshift in growth will likely continue. And as policymakers work through China’s imbalances, macro and market volatility will likely remain high.

Kenneth Ho, Asia Credit Strategist Kinger Lau, Chief China Equity Strategist Email: [email protected] Goldman Sachs (Asia) L.L.C. Tel: +852-2978-7468 Email: [email protected] Goldman Sachs (Asia) L.L.C. Tel: +852-2978-1224

0%

2%

4%

6%

8%

10%

02 03 04 05 06 07 08 09 10 11 12 13 14 15

China NYSETaiwan Korea 0

10

20

30

40

03 04 05 06 07 08 09 10 11 12 13 14 15

Nominal GDP growthTotal Social Financing growth

China leverage: how big a risk?

70093436

Highlight

70093436

Highlight

70093436

Highlight

70093436

Highlight

70093436

Highlight

70093436

Highlight

70093436

Highlight

70093436

Highlight

70093436

Highlight

70093436

Highlight

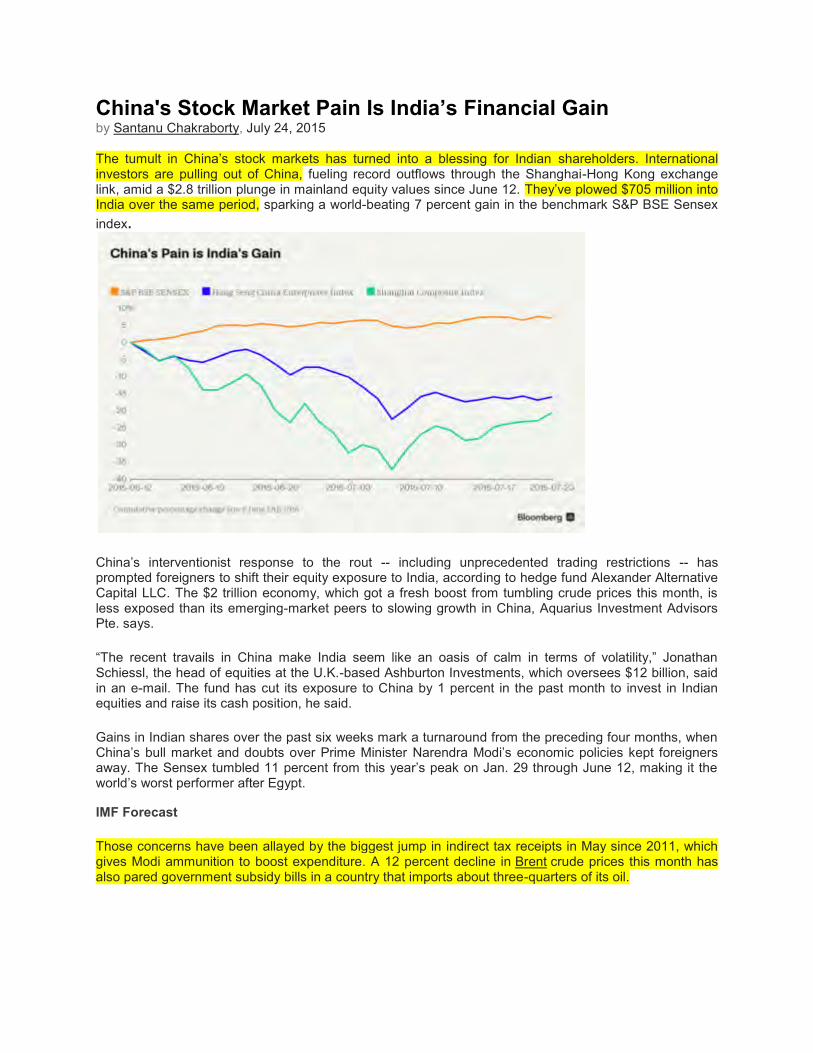

China's Stock Market Pain Is India’s Financial Gain by Santanu Chakraborty, July 24, 2015

The tumult in China’s stock markets has turned into a blessing for Indian shareholders. International investors are pulling out of China, fueling record outflows through the Shanghai-Hong Kong exchange link, amid a $2.8 trillion plunge in mainland equity values since June 12. They’ve plowed $705 million into India over the same period, sparking a world-beating 7 percent gain in the benchmark S&P BSE Sensex index.

China’s interventionist response to the rout -- including unprecedented trading restrictions -- has prompted foreigners to shift their equity exposure to India, according to hedge fund Alexander Alternative Capital LLC. The $2 trillion economy, which got a fresh boost from tumbling crude prices this month, is less exposed than its emerging-market peers to slowing growth in China, Aquarius Investment Advisors Pte. says.

“The recent travails in China make India seem like an oasis of calm in terms of volatility,” Jonathan Schiessl, the head of equities at the U.K.-based Ashburton Investments, which oversees $12 billion, said in an e-mail. The fund has cut its exposure to China by 1 percent in the past month to invest in Indian equities and raise its cash position, he said.

Gains in Indian shares over the past six weeks mark a turnaround from the preceding four months, when China’s bull market and doubts over Prime Minister Narendra Modi’s economic policies kept foreigners away. The Sensex tumbled 11 percent from this year’s peak on Jan. 29 through June 12, making it the world’s worst performer after Egypt.

IMF Forecast

Those concerns have been allayed by the biggest jump in indirect tax receipts in May since 2011, which gives Modi ammunition to boost expenditure. A 12 percent decline in Brent crude prices this month has also pared government subsidy bills in a country that imports about three-quarters of its oil.

India’s economy expanded 7.5 percent in the March quarter, beating China’s 7 percent growth, while the International Monetary Fund predicts India will outpace its neighbor in the current fiscal year.

The longer-term growth outlook is also stronger in India because of its superior demographics, according to Franklin Templeton Templeton Investments. More than 62 percent of the nation’s 1.2 billion people are between age 15 and 59, government data show. China’s pool of workers in this age group is expected to shrink by 61 million by 2030, according to United Nations. That’s about the equivalent of losing the combined working populations of the U.K. and France.

“India is in a phase in which multiple engines of growth can drive GDP from 7-8 percent to 9-10 percent in the next five years,” said Sukumar Rajah, who manages about $9 billion as chief investment officer of Asian Equity at Franklin Templeton in Singapore. “For China, we expect growth to decelerate over the next few years partly because it doesn’t benefit from demographic trends the way that India does.”

State Intervention

Templeton is overweight India and underweight Chinese shares in Hong Kong relative to benchmark indexes, Rajah said. He’s bullish on Indian industrial companies such Larsen & Toubro Ltd. amid signs of increased spending on infrastructure. The Hang Seng China Enterprises Index declined 0.8 percent at 1:19 p.m. in Hong Kong on Friday after a private gauge of Chinese manufacturing unexpectedly fell to the lowest level in 15 months. India’s Sensex lost 0.3 percent in Mumbai trading, poised for a weekly decline.

For overseas money managers, China’s meddling has raised concern about the government’s promise to enact the free-market reforms needed to make mainland shares eligible for MSCI Inc.’s benchmark indexes. Measures to end the rout include a ban on selling by major shareholders, halting initial public offerings and allowing more than 1,400 companies to suspend trading.

“The intervention puts a wet blanket on China’s indices being included in the MSCI gauges,” said Michael Corcelli, chief investment officer of Alexander Alternative in Miami. The steps “are bad for China and definitely good for India,” he said.

Deficient Rainfall

India’s stocks rally may unravel if the strengthening El Nino weather pattern weakens monsoon rains, said Anil Ahuja, the Singapore-based chief executive officer of hedge fund IPEplus Advisors. The June-September rainfall, which was 16 percent above a 50-year average at the end of last month, is now 7 percent below normal, according to the weather office. The monsoon waters more than half of India’s farmland and a shortfall can stoke food prices.

The Sensex gauge trades at 15.9 times 12-month projected profits, compared with a five-year mean of 14.4, data compiled by Bloomberg show. The Hang Seng China Enterprises is valued at 8 times.

“A weak monsoon has not been priced in,” Ahuja said. “Valuation multiples are high versus long-term averages. If earnings don’t begin to justify valuations soon, investors will start to move away.” Indian earnings are projected to grow about seven times faster than China over the next 12 months. Profits at Sensex companies will climb 30 percent, versus 4.3 percent for the Hang Seng China Enterprises Index, analyst estimates compiled by Bloomberg show.

“India’s recent outperformance could be because it has a steady macro-economic picture and is relatively insulated from any slowdown in China compared with other emerging markets such as South Korea and Brazil,” said A.S. Thiyaga Rajan, a Singapore-based senior managing director at Aquarius. “India could see greater interest, now that it is projected to be the fastest-growing major economy.”

The story behind sudden boom in distressed assets

business

Anand Adhikari and Mahesh Nayak July 16, 2015

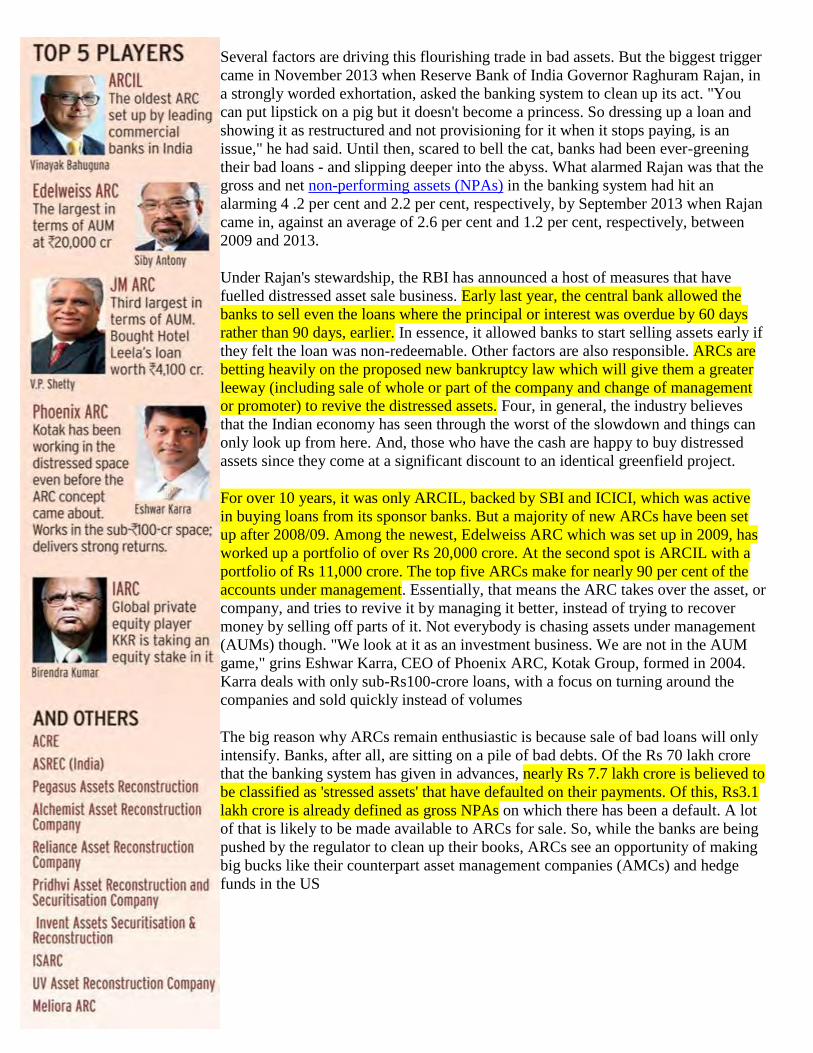

On the 10th of every month, State Bank of India's headquarters at Nariman Point in South Mumbai plays host to

some eager guests. Heads of several of India's 15 asset reconstruction companies (ARCs) make a beeline to

review the 'for sale' bad loans that India's largest bank would be willing to hawk for a price. A similar exercise

takes place at some of India's largest banks, though not necessarily with such regularity.

Till fairly recently, such meetings

were infrequent and resulted in

one-off transactions. But, of late,

the intensity of deals emerging out

of such exchanges is soaring. And

that, in turn, is giving rise to an

unprecedented boom in India's

distressed assets business. In the

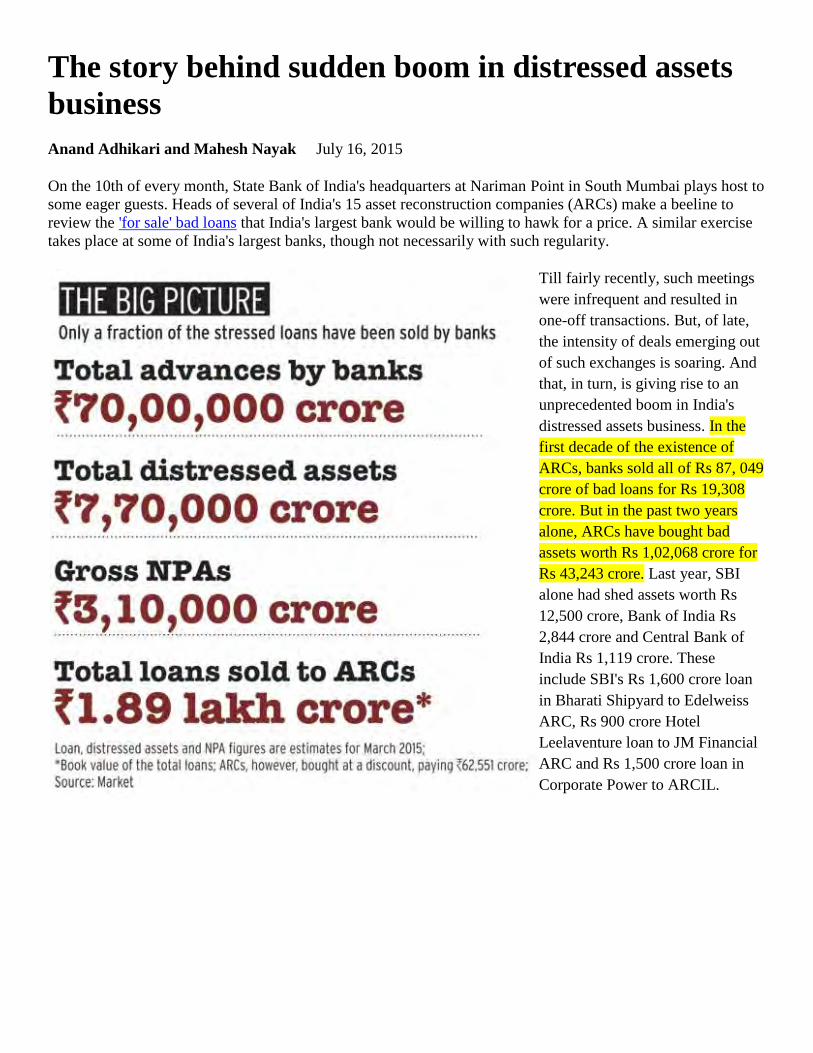

first decade of the existence of

ARCs, banks sold all of Rs 87, 049

crore of bad loans for Rs 19,308

crore. But in the past two years

alone, ARCs have bought bad

assets worth Rs 1,02,068 crore for

Rs 43,243 crore. Last year, SBI

alone had shed assets worth Rs

12,500 crore, Bank of India Rs

2,844 crore and Central Bank of

India Rs 1,119 crore. These

include SBI's Rs 1,600 crore loan

in Bharati Shipyard to Edelweiss

ARC, Rs 900 crore Hotel

Leelaventure loan to JM Financial

ARC and Rs 1,500 crore loan in

Corporate Power to ARCIL.

Several factors are driving this flourishing trade in bad assets. But the biggest trigger

came in November 2013 when Reserve Bank of India Governor Raghuram Rajan, in

a strongly worded exhortation, asked the banking system to clean up its act. "You

can put lipstick on a pig but it doesn't become a princess. So dressing up a loan and

showing it as restructured and not provisioning for it when it stops paying, is an

issue," he had said. Until then, scared to bell the cat, banks had been ever-greening

their bad loans - and slipping deeper into the abyss. What alarmed Rajan was that the

gross and net non-performing assets (NPAs) in the banking system had hit an

alarming 4 .2 per cent and 2.2 per cent, respectively, by September 2013 when Rajan

came in, against an average of 2.6 per cent and 1.2 per cent, respectively, between

2009 and 2013.

Under Rajan's stewardship, the RBI has announced a host of measures that have

fuelled distressed asset sale business. Early last year, the central bank allowed the

banks to sell even the loans where the principal or interest was overdue by 60 days

rather than 90 days, earlier. In essence, it allowed banks to start selling assets early if

they felt the loan was non-redeemable. Other factors are also responsible. ARCs are

betting heavily on the proposed new bankruptcy law which will give them a greater

leeway (including sale of whole or part of the company and change of management

or promoter) to revive the distressed assets. Four, in general, the industry believes

that the Indian economy has seen through the worst of the slowdown and things can

only look up from here. And, those who have the cash are happy to buy distressed

assets since they come at a significant discount to an identical greenfield project.

For over 10 years, it was only ARCIL, backed by SBI and ICICI, which was active

in buying loans from its sponsor banks. But a majority of new ARCs have been set

up after 2008/09. Among the newest, Edelweiss ARC which was set up in 2009, has

worked up a portfolio of over Rs 20,000 crore. At the second spot is ARCIL with a

portfolio of Rs 11,000 crore. The top five ARCs make for nearly 90 per cent of the

accounts under management. Essentially, that means the ARC takes over the asset, or

company, and tries to revive it by managing it better, instead of trying to recover

money by selling off parts of it. Not everybody is chasing assets under management

(AUMs) though. "We look at it as an investment business. We are not in the AUM

game," grins Eshwar Karra, CEO of Phoenix ARC, Kotak Group, formed in 2004.

Karra deals with only sub-Rs100-crore loans, with a focus on turning around the

companies and sold quickly instead of volumes

The big reason why ARCs remain enthusiastic is because sale of bad loans will only

intensify. Banks, after all, are sitting on a pile of bad debts. Of the Rs 70 lakh crore

that the banking system has given in advances, nearly Rs 7.7 lakh crore is believed to

be classified as 'stressed assets' that have defaulted on their payments. Of this, Rs3.1

lakh crore is already defined as gross NPAs on which there has been a default. A lot

of that is likely to be made available to ARCs for sale. So, while the banks are being

pushed by the regulator to clean up their books, ARCs see an opportunity of making

big bucks like their counterpart asset management companies (AMCs) and hedge

funds in the US

Globally, the distressed assets market began to emerge in the

late 80s and early 90s in the US. In fact, most of the modern

day private equity firms - KKR, WL Ross and JC Flower - owe

their existence to early successes in the distressed assets

business. By now, the US is also a major market for the

ancillary industry around distressed assets, including trade in

bonds of distressed companies and turnaround funds which buy

completely broke companies, take over their managements,

turn them around and then sell them. In Asia, the distress

industry grew post the East Asian currency crisis in the late

90s. Early distress investors, such as Clearwater, Cerberus

Capital, GE and Loan Star Funds, have made significant gains

from such junk assets. Over the years, hedge funds have

become rich and powerful enough to intervene in sovereign

debt as Argentina is beginning to discover in the bitter dispute

between two New York hedge funds Gramercy Funds

Management LLC and Elliott Management Corp. In fact,

Elliott even impounded an Argentine Navy vessel for non-

payment, while the Argentine President Cristina Fernandez de

Kirchner has vowed never to negotiate with the fund calling it "vultures".

A Hard Job

Despite the enthusiasm around distressed assets, it is not a job

for the faint hearted.

ARCs are a breed born out of the Securitisation and

Reconstruction of Financial Assets and Enforcement of

Security Interest (SARFAESI) Act of 2002. The objective, says

former finance minister Yashwant Sinha, "was to enable the

banks to acquire the

securities which had

been pledged and sell

them without the

interference of the

courts". Sinha adds:

"We did away under

this Act with the

jurisdiction of civil

courts and gave a huge

power to the banks to deal with the issue of NPAs."

Not everything has panned out exactly as planned. Several legal and

regulatory hurdles have meant that ARCs were unable to exercise the

kind of freedom to turn around these bad assets. "We have such a

decrepit system for enforcing securities. In theory, it should be easier to

enforce a pledge to sell a company and kick the management out, but

most company managements will not go easily, and buyers don't want

to get into this trouble. He will buy only if you are giving it to him 100

per cent in an uncontentious manner," says Harsh Pais, Partner,

Trilegal, a Delhi-based law firm.

Take the case of Bharati Shipyard. A year after Edelweiss ARC bought Bharati Shipyard's Rs 4,570 crore loan

from 12 of its 23 bankers, there awaited a surprise. As many as nine winding up petitions appeared out of the

blue in the Bombay High Court thwarting the attempts of Edelweiss to turn around the cash-strapped ship

building firm. Surprisingly, insurance giant Life Insurance Corporation (LIC) was also one of the petitioners

despite being a secured creditor.

Yet, Edelweiss group chairman and CEO Rashesh Shah remains bullish. Shah, who began his career with the

ICICI group when it was still a development finance institution and had not turned into a bank, believes he

knows how to deal with stressed assets. "Very often a distressed company is still viable, but it is just that it is

indebted," says Shah.

Last year, SBI and Bank of India jointly sold a

loan of a distressed commercial mall in upmarket

Bangalore. Phoenix ARC and Edelweiss ARC

acquired the loans at different points in time from

three banks and they agreed to work together to

revive the Mall. It was a semi-finished mall with a

loan outstanding of Rs 400 crore. The project also

had ready tenants on papers, but because of lack

of funds, the mall's work was suspended

indefinitely. The banking channel refused to lend

and non-banking financial institutions (NBFCs)

were circumspect. The two ARCs acted swiftly by

bringing in an additional Rs 70 crore to complete

the project. "The stalled mall had no value, but by

infusing additional funds, we will increase the

value of the fully occupied mall to Rs600 crore

based on the annual lease rental income of over

Rs 60 crore," says Shah. If it goes according to

plan, both Edelweiss and Phoenix ARC will make

supernormal profits in this distressed asset. The

lending banks, too, will get their money back.

Phoenix ARC's Karra says resolution works for

him as the company boasts the highest 70 per cent redemption record of security receipts issued to banks in

exchange of bad assets. Shah is, however, looking at the restructuring route by working with promoters

alongside: "We see this as a resolution business, while many of our peers are looking at it as a recovery

business," he says, adding: "Resolution business is more of aggregating debt, fresh infusion of capital,

identification of non-core assets, and bringing in a strategic partner. This requires a good mix of financing

background, investment banking capabilities and also an understanding of the equity market." Edelweiss ARC

is manned by IDBI Bank's former executive director Siby Antony.

Sale of loan to ARCs, however, is the last resort for banks. Unlike retail defaulters where banks are known to

hire musclemen for quick recovery, corporate loan recovery is a different ball game. At times, there are labour

unions demanding their pound of flesh; statutory authorities like income tax to excise jump in to claim their

dues; employees approach the court for bankruptcy proceedings. But in most cases it is the deposed

promoters/management that pose the biggest hurdle in a revival.

Sitting at the Edelweiss House in a Mumbai suburb, Antony is strategising to push the Bharati Shipyard

winding up petition out of his way. Bharati has promised to repay the unsecured creditors in 12-15 months.

Antony has also engaged with Bharati Shipyard's promoters PC Kapoor and Vijay Kumar, and other lending

banks which did not sell their loans.

Not far away from Edelweiss' suburban headquarters is the 17th floor office of

P.K. Malhotra, Deputy Managing Director (Stressed Assets Management) of

State Bank of India. Malhotra, a veteran of banking with over three decades of

experience, cannot seem to hide his smile. SBI had even hired consultant

Alvarez & Marsal to turn around Bharati, but with no success. In fact, a

corporate debt restructuring could not save Bharati. Malhotra, who spends most

of his time identifying the bad loans for auction, is making sure that the bank

has exercised all its options before parting with the loan. Banks' options start

with a CDR package, suggesting one time settlement, exiting non-core assets,

infusing additional funds, bringing in strategic investors and then suggesting

complete takeover by another player.

For Malhotra, keeping bad loans in

SBI's books is like feeding a white

elephant. The ARC route gives the

bank 15 per cent (earlier 5 per

cent) of the negotiated sale amount as upfront cash, while the

remaining stays in the book as investment in security receipts

(SRs), which gets redeemed over a period of five to eight years,

depending on the ARCs' ability to recover. Past records show that

ARCs returned 50 per cent of the SRs issued to banks. Clearly,

Bharati is off Malhotra's back today. It is now the headache for

Antony. The company founded by two technocrat-cum-

entrepreneurs from IIT Kharagpur - Kapoor and Kumar - has been

making huge losses for the last three years.

Any setbacks, such as that of Bharati's, haven't deterred top ARCs

from buying big. ARCIL, the oldest ARC, bought another whopper

of a deal in April this year. It acquired the Rs 3,000 crore bad loans

of Corporate Power, a company belonging to Nagpur-based

Abhijeet Group.

For almost two years, its bankers had been negotiating with

potential buyers, such as SREI, JSW, NTPC, TATA and the

Adanis, to sell the loan, but with little success. SREI Infra was the

first to show interest, but the deal couldn't go through because

bankers were not ready for a major haircut. They believed that the

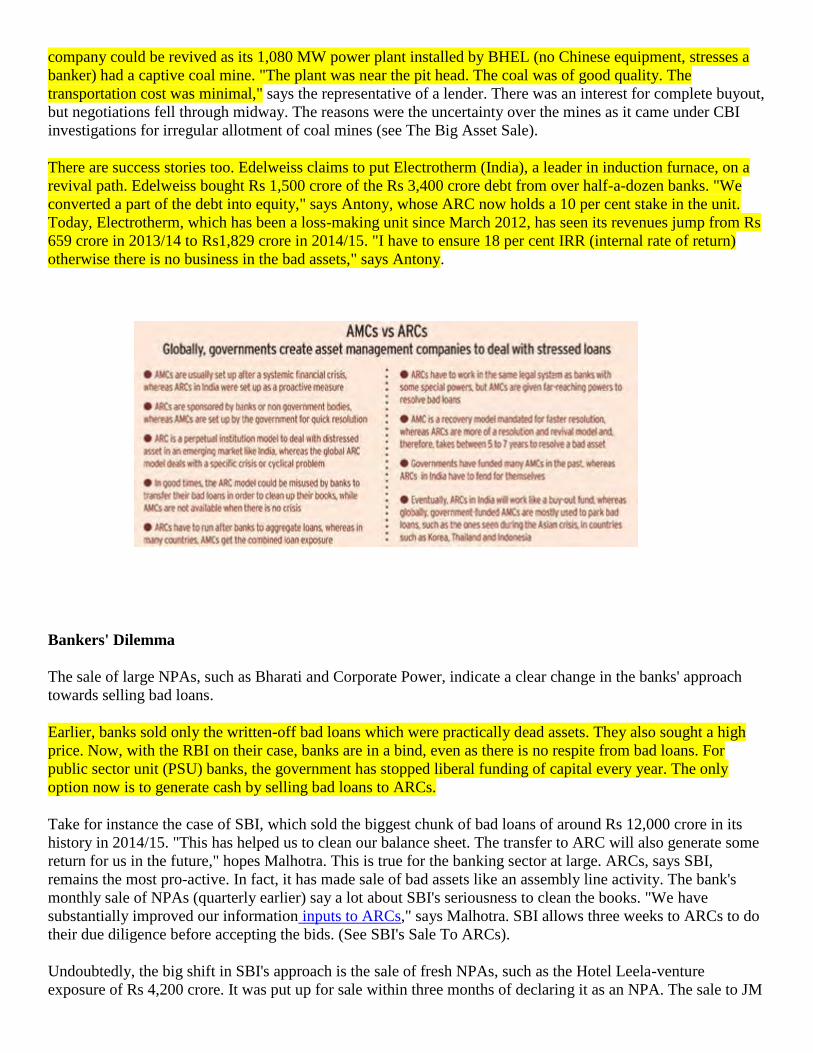

company could be revived as its 1,080 MW power plant installed by BHEL (no Chinese equipment, stresses a

banker) had a captive coal mine. "The plant was near the pit head. The coal was of good quality. The

transportation cost was minimal," says the representative of a lender. There was an interest for complete buyout,

but negotiations fell through midway. The reasons were the uncertainty over the mines as it came under CBI

investigations for irregular allotment of coal mines (see The Big Asset Sale).

There are success stories too. Edelweiss claims to put Electrotherm (India), a leader in induction furnace, on a

revival path. Edelweiss bought Rs 1,500 crore of the Rs 3,400 crore debt from over half-a-dozen banks. "We

converted a part of the debt into equity," says Antony, whose ARC now holds a 10 per cent stake in the unit.

Today, Electrotherm, which has been a loss-making unit since March 2012, has seen its revenues jump from Rs

659 crore in 2013/14 to Rs1,829 crore in 2014/15. "I have to ensure 18 per cent IRR (internal rate of return)

otherwise there is no business in the bad assets," says Antony.

Bankers' Dilemma

The sale of large NPAs, such as Bharati and Corporate Power, indicate a clear change in the banks' approach

towards selling bad loans.

Earlier, banks sold only the written-off bad loans which were practically dead assets. They also sought a high

price. Now, with the RBI on their case, banks are in a bind, even as there is no respite from bad loans. For

public sector unit (PSU) banks, the government has stopped liberal funding of capital every year. The only

option now is to generate cash by selling bad loans to ARCs.

Take for instance the case of SBI, which sold the biggest chunk of bad loans of around Rs 12,000 crore in its

history in 2014/15. "This has helped us to clean our balance sheet. The transfer to ARC will also generate some

return for us in the future," hopes Malhotra. This is true for the banking sector at large. ARCs, says SBI,

remains the most pro-active. In fact, it has made sale of bad assets like an assembly line activity. The bank's

monthly sale of NPAs (quarterly earlier) say a lot about SBI's seriousness to clean the books. "We have

substantially improved our information inputs to ARCs," says Malhotra. SBI allows three weeks to ARCs to do

their due diligence before accepting the bids. (See SBI's Sale To ARCs).

Undoubtedly, the big shift in SBI's approach is the sale of fresh NPAs, such as the Hotel Leela-venture

exposure of Rs 4,200 crore. It was put up for sale within three months of declaring it as an NPA. The sale to JM

Financial ARC, however, came as a big surprise to the promoters of the luxury hotel chain. The bank reasons

that there was no hope of generating cash in the next four to five years.

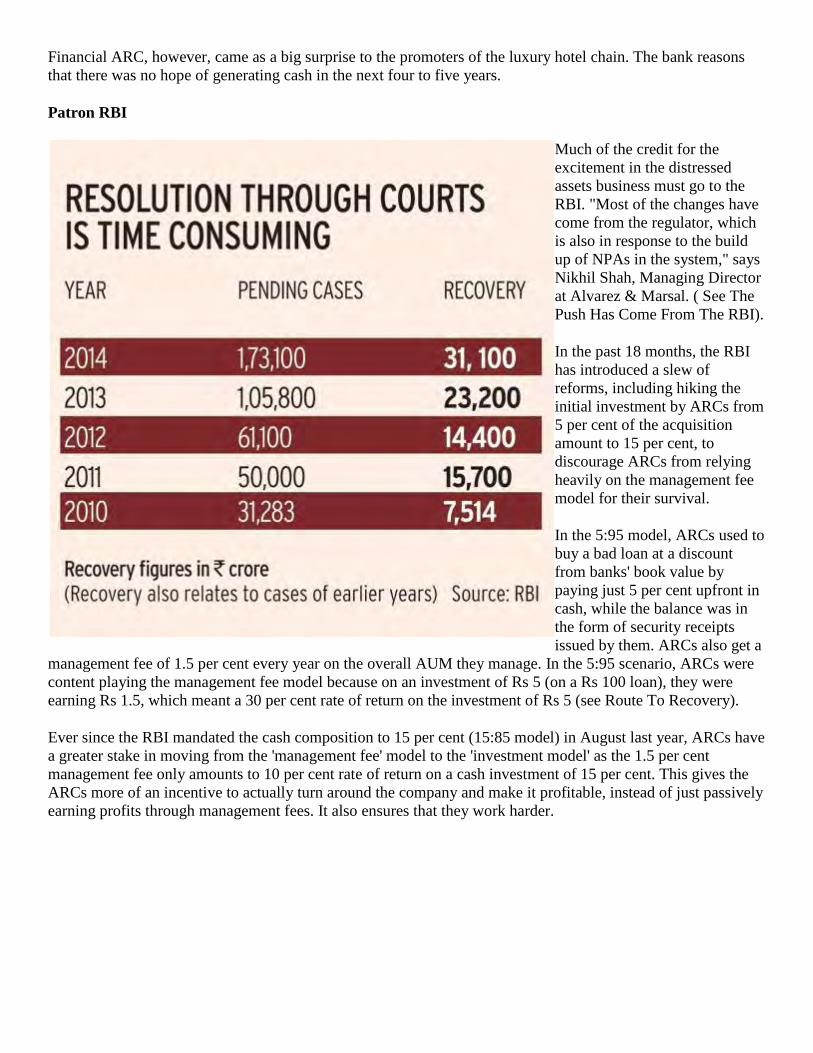

Patron RBI

Much of the credit for the

excitement in the distressed

assets business must go to the

RBI. "Most of the changes have

come from the regulator, which

is also in response to the build

up of NPAs in the system," says

Nikhil Shah, Managing Director

at Alvarez & Marsal. ( See The

Push Has Come From The RBI).

In the past 18 months, the RBI

has introduced a slew of

reforms, including hiking the

initial investment by ARCs from

5 per cent of the acquisition

amount to 15 per cent, to

discourage ARCs from relying

heavily on the management fee

model for their survival.

In the 5:95 model, ARCs used to

buy a bad loan at a discount

from banks' book value by

paying just 5 per cent upfront in

cash, while the balance was in

the form of security receipts

issued by them. ARCs also get a

management fee of 1.5 per cent every year on the overall AUM they manage. In the 5:95 scenario, ARCs were

content playing the management fee model because on an investment of Rs 5 (on a Rs 100 loan), they were

earning Rs 1.5, which meant a 30 per cent rate of return on the investment of Rs 5 (see Route To Recovery).

Ever since the RBI mandated the cash composition to 15 per cent (15:85 model) in August last year, ARCs have

a greater stake in moving from the 'management fee' model to the 'investment model' as the 1.5 per cent

management fee only amounts to 10 per cent rate of return on a cash investment of 15 per cent. This gives the

ARCs more of an incentive to actually turn around the company and make it profitable, instead of just passively

earning profits through management fees. It also ensures that they work harder.

Restructure, Resolve and

Deliver

ARCs have no magic wand to

revive a sick unit. They mostly

use the bilateral route by

working alongside the promoter

to de-leverage the business. "We

are financial restructuring

specialists. We are not business

restructuring experts," says

Eshwar Karra, CEO of Phoenix

ARC. Players like ARCIL and

Edelweiss are playing in big

loans where dozens of banks are

involved. Loan aggregation is a

huge challenge and the

resolution strategy centres

around restructuring of loans to revive a unit.

JM Financial, which bought the Leelaventure loan, is in a bind. Loss-making Leela is asset-rich with well-run

hotel properties. JM is still in dialogue with the company's management, which is asking for certain concessions

in interest and repayment terms from JM Financial. Meanwhile, Leela has also approached the government to

provide concessions to the hotel industry, in terms of loan refinancing. "We have represented to the government

for longer term loan for hotel industry by including existing hotels in the refinancing scheme. We are awaiting

response," says Vivek Nair, Chair-man and Managing Director, Hotel Leelaventure.

Three months ago, JM had put out an advertisement for the sale of Hotel Leela's Chennai and Goa properties to

reduce the debt burden. "They are yet to zero in on the sale. In this difficult environment selling a large hotel

property is very difficult," says a banker. In May this year, the company decided to mobilise Rs 1,000 crore

through equity or debt. "Ultimately, Hotel Leela will be a strategic sale to a big hotel chain," says a rival ARC

official. JM Financial refused to participate in the story.

Edelweiss ARC, on its part, is arranging Rs 600 crore from high networth individuals (HNIs) to complete its

order for delivering a couple of ships to Bharati Shipyard. Unlike banks, Edelweiss ARC has the flexibility to

reduce the interest rates drastically, whereas banks cannot lend below their base rates. Similarly, Edelweiss

could convert part of Bharati's debt into equity, whereas such decisions by banks would come under scrutiny.

ARCs actually have no such worries. "Our short-term plan is to revive the company in 24-30 months," says

Antony. There are some who say new investors (generally private equity) demand priority over existing lenders

as they are taking a bigger risk. "This preference is not acceptable to those banks who have not sold their loans,"

says a market observer.

While ARCs try to identify and take only those assets which can be made viable, it does not always play out

that way. The oldest, ARCIL finally got the Corporate Power loan at a hefty discount, but the entire economics

of the project has now turned on its head. The coal mine was re-auctioned recently to another player. Now, the

coal mine advantage does not exist any more. Another big negative is the location of the unfinished plant. The

Corporate Power plant is in Chandwa in Latehar district of Jharkhand, which is a Naxalite-affected region. "We

are working towards a resolution. We have to finish it. We have to get coal linkages. We have to also get the

power purchase agreement (PPA) revised," says an official of ARCIL.

"Banks generally have factory buildings or land as security, but what about the other assets in a business which

are not subject to security, such as business licenses, contracts, customers, employees, etc.? How do you

transfer these assets under SARFAESI? There is a big hurdle in transferring the continuity of the business," says

Haigreve Khaitan, Partner at Khaitan & Company.

In cases where an ARC decides to opt for the asset-stripping route without the consent of the promoters, there is

lot of resistance. ARCIL has struggled to sell Tulip Star Hotel (erstwhile Centaur near Mumbai's Juhu beach)

for many years. The company has successfully challenged the SARFAESI notice of ARCIL in the past. Board

for Industrial and Financial Reconstruction (BIFR) is yet another escape route where, after the failure of a