What is needed to make agriculture Insurance initiatives widely available to farmers in East Africa...

18

What is needed to make agriculture Insurance initiatives widely available to farmers in East Africa Isaac Magina December 6 th 2012

-

Upload

rodney-perkins -

Category

Documents

-

view

218 -

download

2

Transcript of What is needed to make agriculture Insurance initiatives widely available to farmers in East Africa...

What is needed to make agriculture Insurance initiatives widely available to farmers in East Africa

Isaac MaginaDecember 6th 2012

Over 80 years in the Kenyan market

Regional presence

Kenya• 10 branches, 10 satellites

Uganda• Kampala and 4 major towns

South Sudan

Plans to enter other countries in region TZ, RW DRC, Zambia and Ghana

About UAP

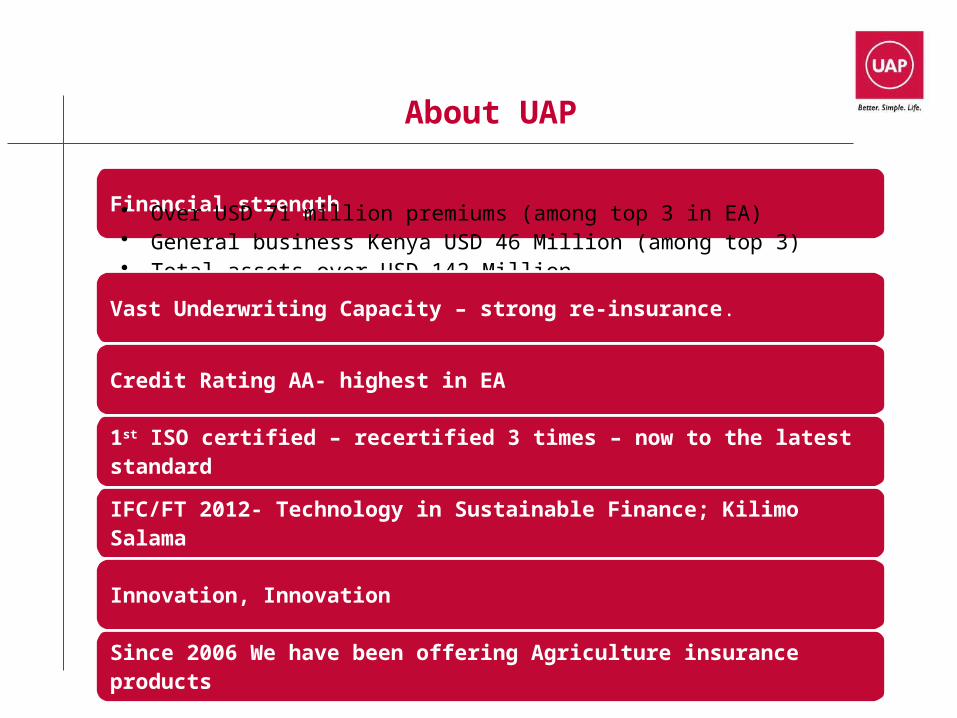

About UAP

Financial strength• Over USD 71 million premiums (among top 3 in EA) • General business Kenya USD 46 Million (among top 3)• Total assets over USD 142 Million• Net assets USD 56 Million – among top 2 in EA

Vast Underwriting Capacity – strong re-insurance.

Credit Rating AA- highest in EA

1st ISO certified – recertified 3 times – now to the latest standard

IFC/FT 2012- Technology in Sustainable Finance; Kilimo Salama

Innovation, Innovation

Since 2006 We have been offering Agriculture insurance products

Why Agriculture Insurance?

In the midst of catastrophes!

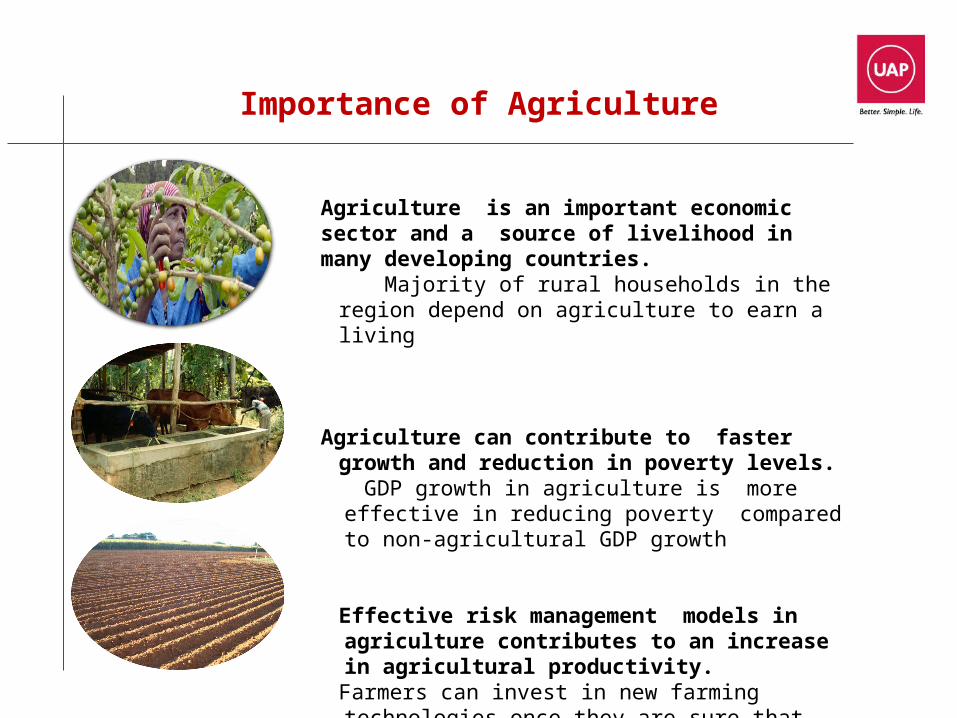

Importance of Agriculture

Agriculture is an important economic sector and a source of livelihood in many developing countries. Majority of rural households in the region depend on

agriculture to earn a living

Agriculture can contribute to faster growth and reduction in poverty levels. GDP growth in agriculture is more effective in reducing poverty compared to non-agricultural GDP growth

Effective risk management models in agriculture contributes to an increase in agricultural productivity.

Farmers can invest in new farming technologies once they are sure that their investments are secured.

6

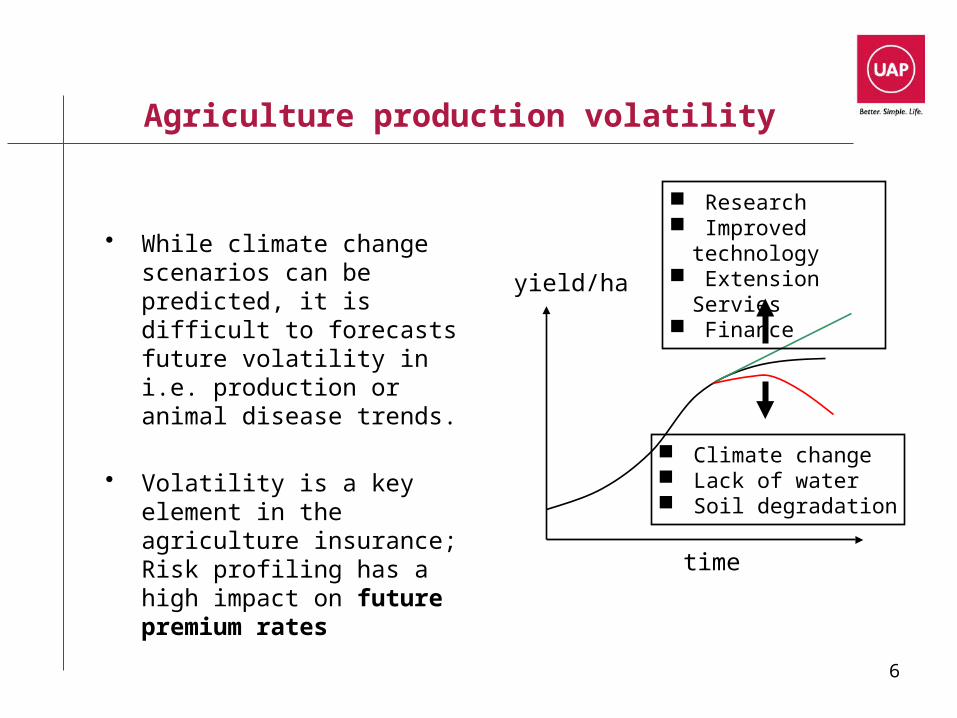

Agriculture production volatility

• While climate change scenarios can be predicted, it is difficult to forecasts future volatility in i.e. production or animal disease trends.

• Volatility is a key element in the agriculture insurance; Risk profiling has a high impact on future premium rates

Research Improved

technology Extension Servies Finance

yield/ha

time

Climate change Lack of water Soil degradation

Some of our projects in the past five years

Index based Livestock insurance-IBLI• Pilot project to insured pastoralist in Marsabit County Northern

Kenya in partnership with the International Livestock Research Institute and Equity Bank

Index based Crop Insurance Initiative- Kilimo Salama• In partnership with Syngenta Foundation for Sustainable

Agriculture, Currently insuring over 65,000 small holder farmers in Kenya and Rwanda

East African Barley Crop Insurance scheme• Crop insurance scheme for contracted barley growers in 2010/11

crop season

Some of our projects in the past five years

Sugar Cane Fire Insurance Scheme• In partnership with the Kenya Sugar Board and Agriculture

Finance Corporation

Kenya Commercial Bank Livestock Insurance Scheme.• Livestock insurance for all dairy development loans advanced

to KCB customers

Tobacco Crop Insurance Schemes, • Crop insurance cover for farmers contracted by the major

tobacco processing companies

What we have found out?

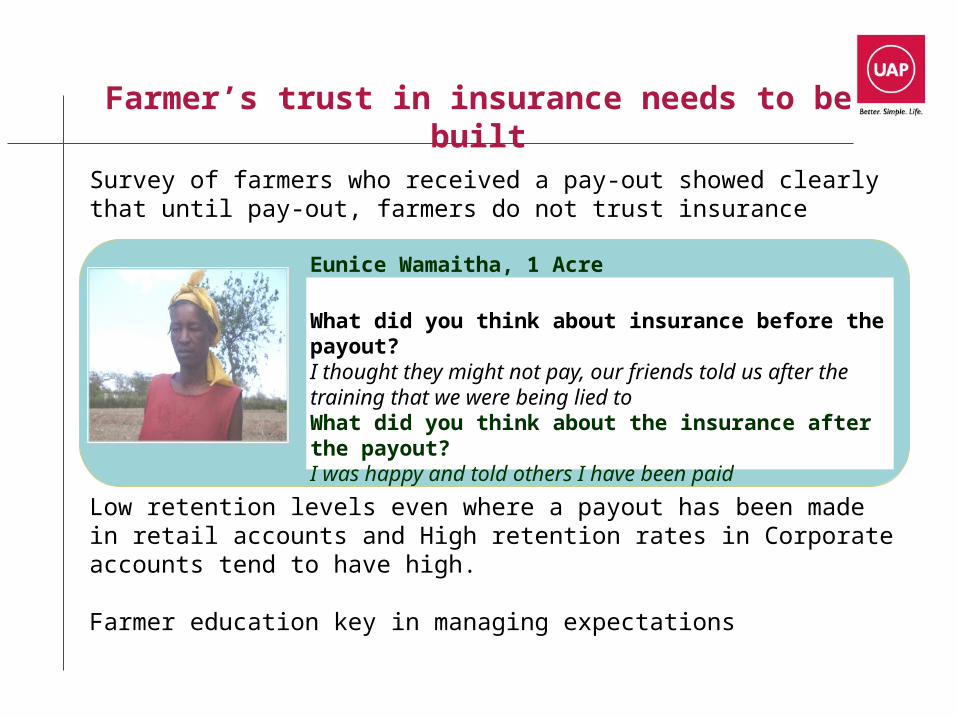

Farmer’s trust in insurance needs to be built

Survey of farmers who received a pay-out showed clearly that until pay-out, farmers do not trust insurance

Eunice Wamaitha, 1 Acre insured

What did you think about insurance before the payout?I thought they might not pay, our friends told us after the training that we were being lied toWhat did you think about the insurance after the payout?I was happy and told others I have been paid

Low retention levels even where a payout has been made in retail accounts and High retention rates in Corporate accounts tend to have high.

Farmer education key in managing expectations

Training is key to uptake and satisfaction

Judging by their questions, farmers can understand insurance:

What if it doesn’t rain on my field and it rains at the station, do I then receive a payout?

92% of farmers who buy insurance are trained about insurance

Timely compensation is key:Farmers expect payout as soon as the contracts endsPayouts were made within 2 weeks after contract ended

Affordability is key: willingness vs ability to pay

• Insurance in high risk areas is expensive: No premium subsidy schemes, Schemes that pay upfront on behalf of the farmers tend to be successful.

• Higher uptake of insurance in commercial farming compared to subsistence farming systems. Farming as a business is a driver to insurance uptake.

• Need to target farmer groups to reduce transaction costs and improve efficiency in contract monitoring

Unique distribution models

• Assumptions; Input retailers are willing to distribute insurance; but the product has to be simple. The input retailer is one of the closest advisors to a farmer

• Input retailers; competition between crop protection product margins and insurance commissions

• Selling insurance through farmer group, aggregator institutions, cooperative societies has potential to reduce transaction costs and increase uptake; Regulatory approvals for alternative distribution channels.

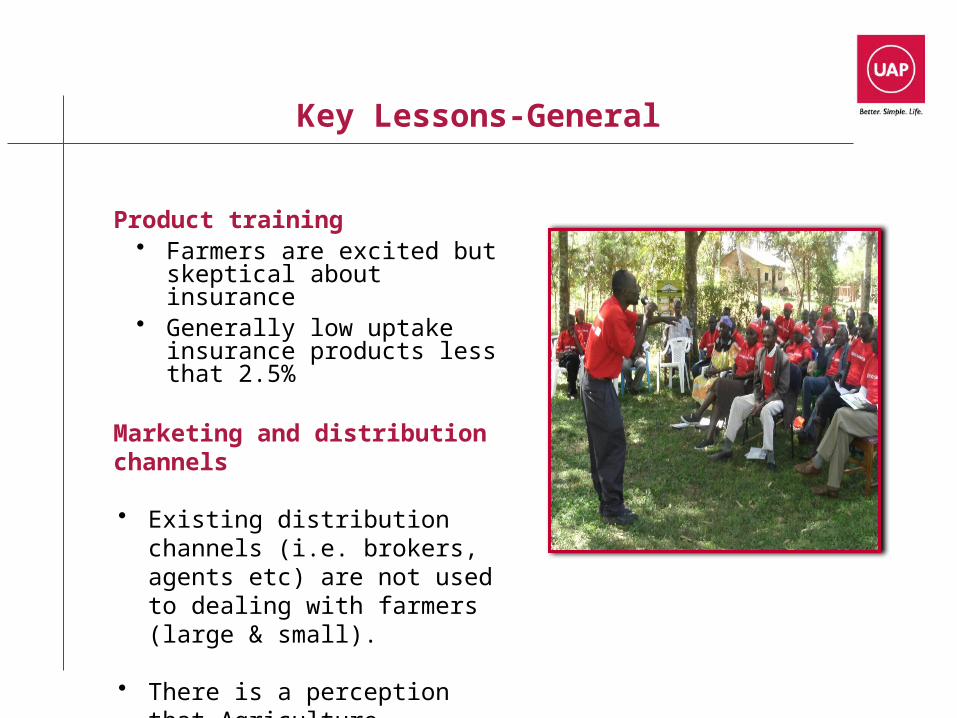

Key Lessons-General

Product training• Farmers are excited but skeptical

about insurance• Generally low uptake insurance

products less that 2.5%

Marketing and distribution channels

• Existing distribution channels (i.e. brokers, agents etc) are not used to dealing with farmers (large & small).

• There is a perception that Agriculture insurance is complicated to sell.

Key Lessons-General

The Product• Indemnity based vs Index Insurance

Products. • Livestock insurance indemnity vs Index

based• Adoption of suitable weather proxies for

agric risks e.g. NDVI, CCD or ET indices

Weather data/ infrastructure• Insufficient historical weather data,

small number of automatic weather stations and weather data analysis.

• Role of Meteorological services; business vs regulatory

players in agriculture insurance market.

• Farmers and farmer organization; need to understand attributes and benefits of agriculture insurance products

• Insurance company; caries the risks and product development champion.

• Re-insurance; support in product design, market development, global experience and carry the risk

• Insurance distribution- Brokers, Agents, Baccasurance, Farmers association and co-operative societies

• Financial institutions; banks, micro finance, development banks-to provide agri-credit and pre-finance premiums

• Development agencies; non governmental organizations in product development and marketing

• Government and Government agencies; policy formulation, regulation, market development and insured

• Research institutions: product design, service providers

models of government support to agric insurance

Number of Players Product Diversification

FullyIntervened

System

Public–Private

Partnership

Pure MarketBased

• Normally High Penetration (compulsory)• Well Diversified Portfolios• Social over Technical criteria• Monopoly. Issues with the service• Government assumes full liability

• High Penetration• Well Diversified Portfolios• Technical over commercial criteria• Competition for service• Government adds stability to the system• Private Sector adds “know how”

• Low to moderate penetration• Low risk diversification• Commercial over technical

criteria• Competition for price

Leve

l of G

over

nmen

t Int

erve

ntion

UAP, Bishops Garden Towers, Bishops Road, PO Box 43013-00100, Nairobi, Kenya. Tel 2850000, Fax 2719030, E-mail [email protected]

www.uapkenya.com