What Does It Mean to be “Insured”? - Hilltop · PDF fileSource: KFF/HRET and...

28

What Does It Mean to be “Insured”? Paul Fronstin, Ph.D. Director, Health Research & Education Program Employee Benefit Research Institute UMBC The Changing Health Insurance Market Copyright© - Employee Benefit Research Institute Education and Research Fund, 1978-2006. All rights reserved. The information contained herein is not to be construed as an attempt to provide legal, accounting, actuarial, or other such professional advice. Permission to copy or print a personal use copy of this material is hereby granted and brief quotations for the purposes of news reporting and education are permitted. Otherwise, no part of this material may be used or reproduced without permission in writing from EBRI-ERF.

Transcript of What Does It Mean to be “Insured”? - Hilltop · PDF fileSource: KFF/HRET and...

What Does It Mean to be “Insured”?

Paul Fronstin, Ph.D.Director, Health Research & Education Program

Employee Benefit Research Institute

UMBCThe Changing Health Insurance Market

Copyright© - Employee Benefit Research Institute Education and Research Fund, 1978-2006. All rights reserved.

The information contained herein is not to be construed as an attempt to provide legal, accounting, actuarial, or other such professional advice. Permission to copy or print a personal use copy of this material is hereby granted and brief quotations for the purposes of news reporting and education are permitted. Otherwise, no part of this material may be used or reproduced without permission in writing from EBRI-ERF.

2

Premiums Rising 4-5 Times Faster than Inflation and Wages, 1988-2005

12.0%

18.0%

14.0%12.2%

10.3%8.5%

5.9%

0.8%

9.2%11.2%

13.9%12.9%

10.9%

8.2%

5.3%

0%

5%

10%

15%

20%

1988 1990 1992 1994 1996 1998 2000 2002 2004

Health Insurance PremiumsWorkers EarningsOverall Inflation

Source: KFF/HRET and Bureau of Labor Statistics.

3

Average Worker Monthly Contribution, 1988-2005

$8

$52$34

$124

$37

$122

$28

$138

$30

$150

$38

$174

$42

$201

$47

$222

51

226

$0

$50

$100

$150

$200

$250

Employee-Only Coverage Family Coverage

1988 1993 1996 2000 2001 2002 2003 2004 2005

Source: KFF/HRET.

4

Percentage of Premium Paid by Covered Workers, 1988-2005

11%

29%

20%

32%

20%

27%

14%

26%

14%

26%

16%

28%

16%

27%

16%

28%

16%

26%

0%

10%

20%

30%

40%

Employee-Only Coverage Family Coverage

1988 1993 1996 2000 2001 2002 2003 2004 2005

Source: KFF/HRET.

5

Average Annual Deductibles for Employee-Only Coverage, 1996-2005

(Among Covered Workers With or Without a Deductible)

180

71

175

79

204

92

251

54

275

113

287

210

323

220

0

50

100

150

200

250

300

350

400

450

500

PPO In-Network POS In-Network

1996 2000 2001 2002 2003 2004 2005

Source: KFF/HRET.

6

Physician Office Visit Co-Payments, 2004-2005

(Among Covered Workers With a Co-payment)

57%

39%

48% 49%

0%

10%

20%

30%

40%

50%

60%

70%

$5-$15/visit $20 or more/visit

2004 2005

Source: KFF/HRET.

7

Average Co-Pay for Drugs, 2000-2005

$-

$10

$20

$30

$40

$50

$60

$70

$80

Generic Drugs Preferred Drugs Non-Preferred Drugs Fourth-Tier

2000 2001 2002 2003 2004 2005

Source: KFF/HRET.

8

Drug Plan Incentives for PPO, Firms with 1,000 or More Employees, 1998 &

2003

10%6%Pay difference between generic & brand name

6%10%Higher coinsurance

<1%1%No deductible

69%45%Lower co-payment

20031998Generic Incentive

Source: Hewitt Associates.

9

Drug Plan Incentives for PPO, Firms with 1,000 or More Employees, 1998 &

2003

14%21%Higher coinsurance

8%12%No deductible

67%31%Lower co-payment

20031998Mail Order Incentive

Source: Hewitt Associates.

10

Drug Plan Incentives for PPO, Firms with 1,000 or More Employees, 1998 &

2003

6%22%No Generic or Mail Order Incentive

6%2%Pay difference between generic & brand name

1%1%Higher coinsurance

78%32%Lower co-payment

20031998Combination of Generic and Mail Order Incentive

Source: Hewitt Associates.

11

Tiered Provider Networks (TPNs)

• Hospitals & doctors.• Tiers vary with cost & quality.

– Similar to PPO (in vs. out)– Similar to Rx tiers.

• Cost sharing distinctions– Co-payment per hospital day.– Coinsurance rate per stay.– Overall deductible per stay.

12

Use of Tiered Physician or Hospital Networks, 2005

11%13%13%

12%13%

8%

0%

5%

10%

15%

20%

Have Tiered Provider Networks Considered Tiered Networks

HMO PPO POS

Source: KFF/HRET.

13

Consumerism:Potentials & Concerns

Potentials• Lower costs

– Reduction in use– Use of lower cost services

• Better engaged consumer• More satisfied consumer• Better health

outcomes/more appropriate care

• Improve affordability

Concerns• Low health literacy

– Reduce necessary care– Induce demand for

unnecessary care

• Lack of tools & resources to make decisions

• Impact on high cost users uncertain

• One-time savings

14

Evidence So FarFull Replacement HRA Study (McKinsey & Company, 2005)

• CDHP consumers are more engaged than “traditionally insured” in decision making

• Make decisions that may drive sustained decline in trend– Forego less serious care– Shop for most cost effective care when they can– Take greater responsibility for health and wellness

• Seek information to compare treatments, not providers• Are no more likely than employees in traditional plans

to seek quality info• Are less satisfied than with previous plans

15

Evidence So FarAetna Study: Medical Claims

2003: 3.7% YOY Increase

Change in utilization• Inpatient -5.2%• ER Visits -2.6%• Outpatient -14.4%• Office visits -3.3%

– PCP -10.9%– Specialist +3.4%

2004: 6% YOY Increase

Change in utilization• Inpatient -6.7%• ER Visits -15.9%• Outpatient -4.6%• Office visits -3.4%

– PCP -12.3%– Specialist +3.6%

16

Evidence So FarAetna Study: Pharmacy

• Overall Cost Increase – CDHP +13%– PPO +18%

• Generic Use– CDHP +2.1%– PPO +1.3%

• Mail Order– CDHP +3.5%– PPO +1.7%

17

Increase in medications that support chronic conditions

Eight percent decrease in total medical (non-pharmacy) costs

Eight percent increase in medication supply

Decrease in inpatient and outpatient costs

CIGNA Choice Fund StudyKey Findings

Increase in inpatient admits

18

Evidence So Far

• Risk Selection– Humana data studied by Kaiser: based on prior

use and prior claims, HDHP enrollees usage was 50-60% below those not choosing HDHP

– U. of Oregon study: selectivity related to education, income, health status

• Cost savings actions– U. of Oregon study: only difference related to

generic drug substitution• BCBSA Study

19

EBRI/Commonwealth Fund Consumerism in Health Care Survey

• Among adults with plans, lower satisfaction with quality of care, out-of-pocket costs, plan overall; few would recommend plan to friends/co-workers

• High out-of-pocket costs + premiums amount to substantial share of income, especially among those with lower income and health problems

• No differences in service use, but higher reported rates of cost-related delays, avoidance, or skipping care or Rx, esp. lower income and health problems

• More cost-conscious decision making behavior• Little quality/cost information provided by plans

20

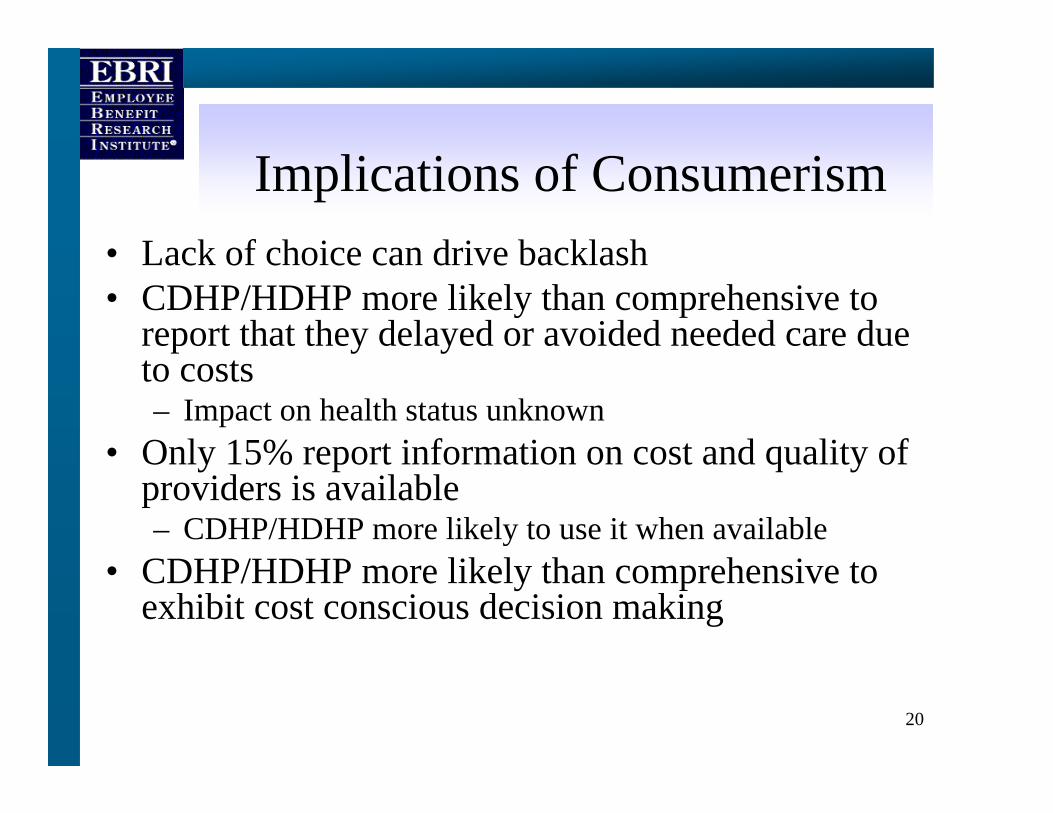

Implications of Consumerism • Lack of choice can drive backlash• CDHP/HDHP more likely than comprehensive to

report that they delayed or avoided needed care due to costs– Impact on health status unknown

• Only 15% report information on cost and quality of providers is available– CDHP/HDHP more likely to use it when available

• CDHP/HDHP more likely than comprehensive to exhibit cost conscious decision making

21

Percentage of Adults who Agree that Terms of Coverage Make Them Consider Cost When Deciding

to Seek Health Care Services

71*60*

38

0

20

40

60

80

Comprehensive HDHP CDHPNote: Comprehensive = plan w/ no deductible or <$1000 (ind), <$2000 (fam); HDHP = plan w/ deductible $1000+ (ind), $2000+ (fam), no account; CDHP = plan w/ deductible $1000+ (ind), $2000+ (fam), w/ account.*Difference between HDHP/CDHP and Comprehensive is statistically significant at p ≤ 0.05 or better.Source: EBRI/Commonwealth Fund Consumerism in Health Care Survey, 2005.

Percent of adults 21-64 who strongly or somewhat agree

22

Cost Conscious Decision-Making, by Insurance Source

27

43

49

19

32*

44*

55*

60*

14

23

0 20 40 60 80

Checked quality rating ofdoctor or hospital

Checked price of service

Asked doctor to recommendless costly prescription drugs

Talked to doctor abouttreatment options & costs

Checked whether plan wouldcover care

Comprehensive

HDHP/CDHP

Note: Comprehensive = plan w/ no deductible or <$1000 (ind), <$2000 (fam); HDHP = plan w/ deductible $1000+ (ind), $2000+ (fam), no account; CDHP = plan w/ deductible $1000+ (ind), $2000+ (fam), w/ account.*Difference between HDHP/CDHP and Comprehensive is statistically significant at p ≤ 0.05 or better.Source: EBRI/Commonwealth Fund Consumerism in Health Care Survey, 2005.

Percent of adults 21-64 who received health care in last twelve months

23

Annual Claims DistributionAdults Ages 18-64, 2001

$0

$10,000

$20,000

$30,000

$40,000

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Percent of Population

Ave

rage

Cos

t Per

Per

son

Average Cost = $2,454

or higher

20% of population that accounts for 80% of spending

Source: EBRI estimates from the 2001 MEPS.

24

15 Most Costly Conditions Account for Over 50% of Spending

56%Total spending

1%Kidney

2%Infectious disease

2%Endocrine

2%Skin disorders

2%Pneumonia

2%Cerebrovascular disease

3%Back problems

3%Arthritis

3%Diabetes

4%Hypertension

5%Mental disorders

6%Pulmonary conditions

6%Cancer

7%Trauma

9%Heart disease

25

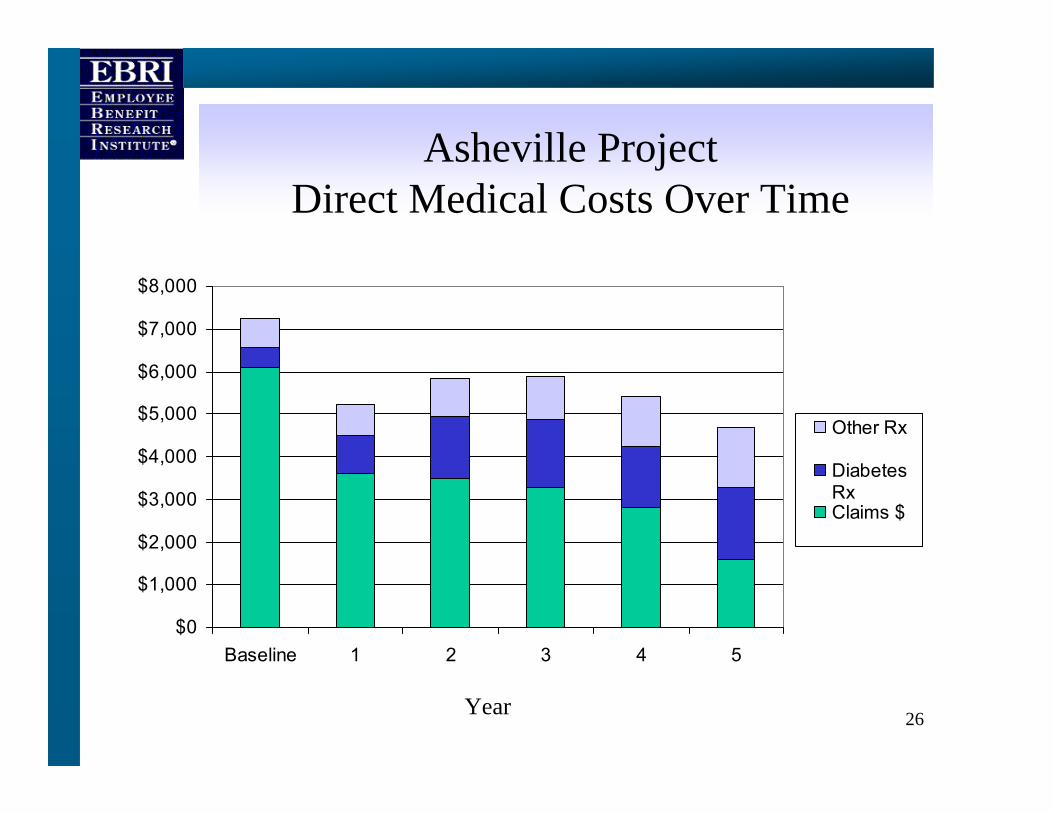

Asheville Project(J. of Amer. Pharma Assoc., 2003)

• No cost meetings with pharmacists– Education, home meter training, physical

assessments• Co-payments for diabetes-specific drugs

and supplies were waived

26

Asheville ProjectDirect Medical Costs Over Time

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

Baseline 1 2 3 4 5

Other Rx

DiabetesRxClaims $

Year

27

Asheville ProjectAve. Annual Sick Days Among Diabetics

12.6

6.0

8.5

5.7 5.8 5.7 6.0

0

2

4

6

8

10

12

14

Baseline 1 2 3 4 5 6

Year

28

Cholesterol Lowering Drugs

• Recent Rand study, Journal of Managed Care• Increase in co-payment from $10 to $20

associated with a 6-10 percentage point reduction in compliance.

• Full compliance associated with 357 fewer hospitalizations in sample studied.

• Elimination of co-payments for certain patients would avert 80,000 hospitalizations and 31,000 ER visits nationally.

• National savings would be more than $1 billion.