What Appraisers, Accountants, and Attorneys Need to … Appraisers, Accountants, and Attorneys Need...

49

What Appraisers, Accountants, and Attorneys Need to Know About Business Valuation-Related Issues in Estate Planning November 2, 2011 www.aicpa.org/fvs

Transcript of What Appraisers, Accountants, and Attorneys Need to … Appraisers, Accountants, and Attorneys Need...

What Appraisers, Accountants, and Attorneys Need to Know About

Business Valuation-Related Issues in Estate Planning

November 2, 2011

www.aicpa.org/fvs

Forensic and Valuation Services Section www.aicpa.org/fvs

DISCLAIMERThe views expressed by the presenters do not necessarily represent the views, positions, or opinions of the AICPA or the presenter’s respective organization.

These materials, and the oral presentation accompanying them, are for educational purposes only and do not constitute accounting or legal advice or create an accountant-client or attorney-client relationship.

Forensic and Valuation Services Section 3

PanelistsF.A. "Chip" Brown, CFA, CPA, ABV, CFFWillamette Management [email protected]

Curtis R. Kimball, CFA, ASAWillamette Management [email protected]

www.aicpa.org/fvs

Forensic and Valuation Services Section

Focus of Today’s Presentation

Best practices for estate tax valuationsAppraiser’s potential roles in estate planningValuation issues in the drafting of corporation and partnership documentsRecent valuation discount settlements

www.aicpa.org/fvs 4

Forensic and Valuation Services Section

Best Practices for Estate Tax Valuations

5

Forensic and Valuation Services Section

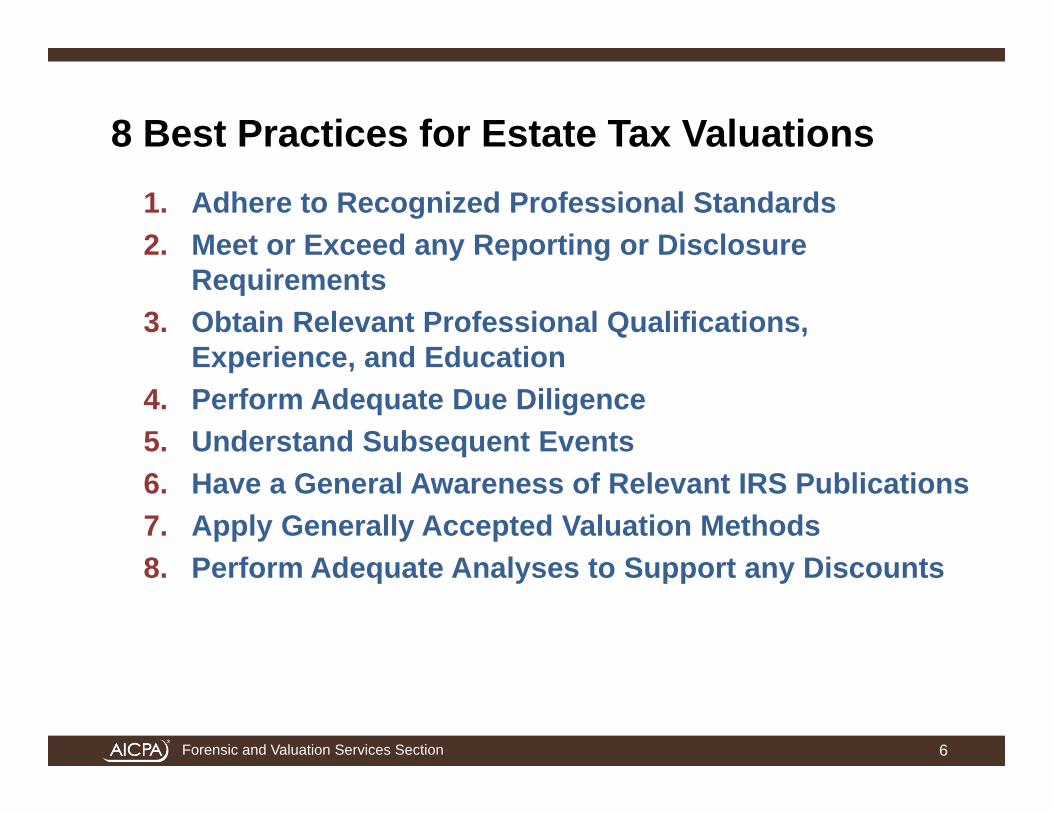

8 Best Practices for Estate Tax Valuations1. Adhere to Recognized Professional Standards2. Meet or Exceed any Reporting or Disclosure

Requirements3. Obtain Relevant Professional Qualifications,

Experience, and Education4. Perform Adequate Due Diligence5. Understand Subsequent Events6. Have a General Awareness of Relevant IRS Publications7. Apply Generally Accepted Valuation Methods 8. Perform Adequate Analyses to Support any Discounts

6

Forensic and Valuation Services Section

Best Practice #1Adhere to Recognized Professional Standards

USPAP• IRS commentaries have indicated that a USPAP-compliant

report will generally be regarded as a qualified appraisal.• Kohler case – Tax Court critical of IRS expert report that “was

not prepared in accordance with all USPAP standards” • Not that high of a hurdle to overcome

SSVS No. 1• AICPA members required to follow this standard when they

perform engagement to estimate value that culminate in the expression of a conclusion of value or a calculated value

Other Valuation Professional Organization Standards

7

Forensic and Valuation Services Section

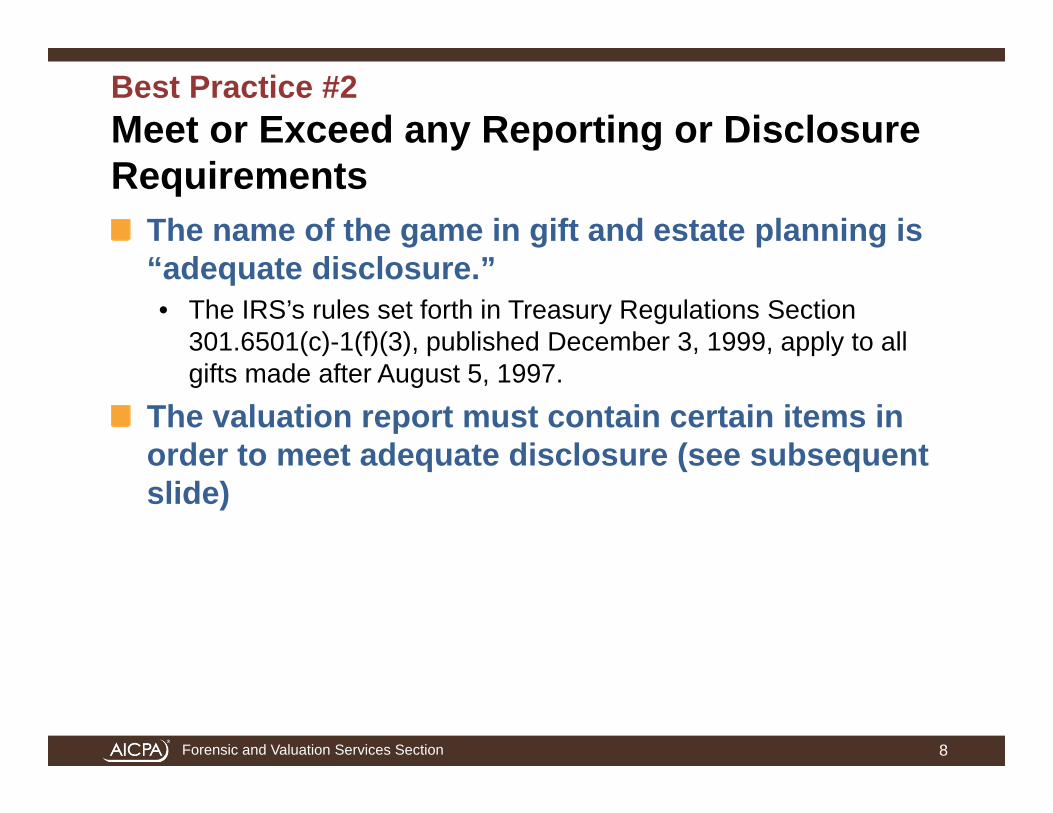

Best Practice #2Meet or Exceed any Reporting or Disclosure Requirements

The name of the game in gift and estate planning is “adequate disclosure.” • The IRS’s rules set forth in Treasury Regulations Section

301.6501(c)-1(f)(3), published December 3, 1999, apply to all gifts made after August 5, 1997.

The valuation report must contain certain items in order to meet adequate disclosure (see subsequent slide)

8

Forensic and Valuation Services Section

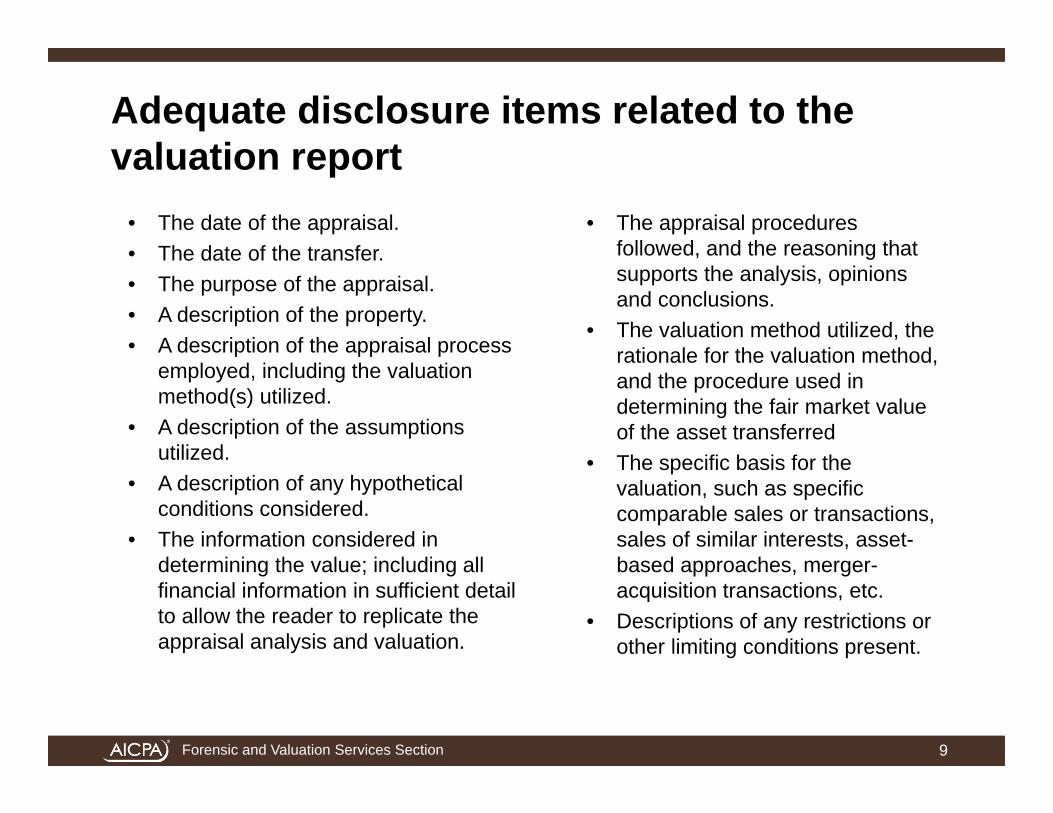

• The date of the appraisal.• The date of the transfer.• The purpose of the appraisal.• A description of the property.• A description of the appraisal process

employed, including the valuation method(s) utilized.

• A description of the assumptions utilized.

• A description of any hypothetical conditions considered.

• The information considered in determining the value; including all financial information in sufficient detail to allow the reader to replicate the appraisal analysis and valuation.

• The appraisal procedures followed, and the reasoning that supports the analysis, opinions and conclusions.

• The valuation method utilized, the rationale for the valuation method, and the procedure used in determining the fair market value of the asset transferred

• The specific basis for the valuation, such as specific comparable sales or transactions, sales of similar interests, asset-based approaches, merger-acquisition transactions, etc.

• Descriptions of any restrictions or other limiting conditions present.

Adequate disclosure items related to the valuation report

9

Forensic and Valuation Services Section

Best Practice #3Obtain Relevant Professional Qualifications, Experience, and Education

At least one business valuation specific credential (ABV, ASA, AVA, CVA, CBA)• Definition of qualified appraiser under IRC Section 170 recently

modified to include “earned an appraisal designation from recognized professional appraiser organization.”

• Kohler case – Tax Court commented favorably that the Estate’s experts were “certified appraisers”

Regularly perform business valuationsExperience in gift/estate tax related mattersContinuing education and training related to gift/estate tax matters

10

Forensic and Valuation Services Section

Best Practice #4Perform Adequate Due Diligence

Site visits (at least periodically) by the valuation analyst to the subject company location(s)Interview management • Kohler case – Court critical of IRS expert for limited due

diligence related to site visit and interviewing management. “we are convinced from his report and trial testimony that [the IRS expert] did not understand Kohler’s business. He spent only 2-1/2 hours meeting with management”

Typical for the respective court to show a keen interest in the level of due diligence that was performed• Kohler case – “[Estate’s experts] spent sufficient time with the

company and management to understand the Kohler business”

11

Forensic and Valuation Services Section

Best Practice #5Understand Subsequent Events

USPAP• Provides guidance regarding subsequent events for retrospective appraisals

(appraisals in which the effective date of the appraisal is prior to the report date).• Based on USPAP, it is reasonable for an analyst to consider data subsequent to

the valuation date but only to confirm historical trends and market expectations as of the valuation date.

SSVS 1• Provides guidance regarding subsequent events. • Based on SSVS 1, an analyst is not required to disclose subsequent events.

However, an analyst may disclose subsequent events in a separate report section for informational purposes.

12

Forensic and Valuation Services Section

Subsequent events (continued)

While in theory any subsequent events should not impact valuation, the IRS often will try to use subsequent events as corroborating evidence for its position. Therefore, it may be helpful to be prepared to reconcile the valuation to subsequent events

13

Forensic and Valuation Services Section

Subsequent events (continued)

A majority of the federal tax cases dealing with subsequent events have concluded that it is inappropriate to use hindsight as direct evidence of value as of the valuation date.However, the Tax Court (and other federal courts) has also opined that certain subsequent events that occur within a reasonable time after the valuation date may be appropriate to consider:• Reasonably foreseeable• Prove reasonableness of expectations • Subsequent sale of subject interest• Subsequent sale of comparable ownership interest

14

Forensic and Valuation Services Section

Subsequent events (continued)

Gimbel case• Subsequent event of the redemption of all estate shares by the

Company. Court found that it was reasonably foreseeable as of the date of death that the company would repurchase a portion (20%) of shares, but not all the shares. Tax Court did not adopt the exact subsequent transaction price or number of shares as a basis for its decision. However, Tax Court was clearly influenced by the subsequent event.

Ringgold Telephone Company case• Tax Court criticized taxpayer expert for failing to consider the

subsequent sale.

15

Forensic and Valuation Services Section

Best Practice #6Have a General Awareness of Applicable IRS Publications

Federal Tax Law• Internal Revenue Code • Code of Federal Regulation

Internal Revenue Service Publications• Treasury Regulations • Treasury Decisions • Revenue Rulings • Revenue Procedures

Advance Rulings and Determinations• Technical Advice Memorandums• Technical Memorandums

16

Forensic and Valuation Services Section

Best Practice #7Apply Generally Accepted Valuation Methods

Sounds simple, but the devil is in the detailsMeet Daubert standardsSSVS 1 provides a good outline for generally acceptable valuation methodsAICPA Practice Aid – Business Valuations for Estate and Gift Tax Purposes (not yet published, but currently being worked on)

17

Forensic and Valuation Services Section

Best Practice #8 Perform Adequate Analyses to Support any Discounts

Consideration of empirical models/theoretical models/regression models as part of the discount for lack of marketability discountGo beyond the studies and rules of thumbDo not use court cases as support for discountsFind applicable closed-end fundsReview and understand provisions of any partnership/operating agreements that may impact control and/or marketability

18

Forensic and Valuation Services Section

An Appraiser’s Role in the Estate Planning Process

19

Forensic and Valuation Services Section

Coordination Between Estate Attorney and Appraiser

Appraisers should not render a legal opinionRely on attorney in regards to the likely understanding of rights and privileges associated with subject interestA hypothetical willing buyer/seller would likely consult with attorney on similar issuesAny document in the appraiser’s file is subject to being discovered during the audit process or in subsequent valuation litigation. This includes written correspondence, emails, notes and drafts of appraisals.Appraiser should be independent

20

Forensic and Valuation Services Section

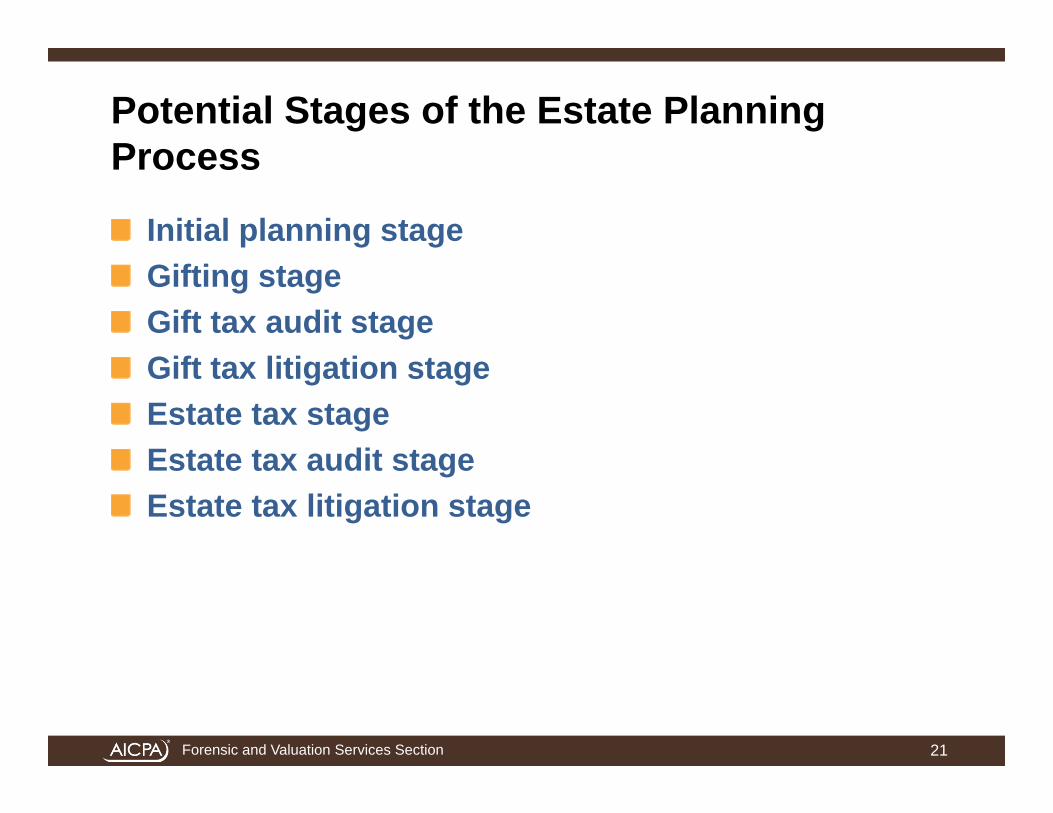

Potential Stages of the Estate Planning Process

Initial planning stageGifting stageGift tax audit stageGift tax litigation stageEstate tax stageEstate tax audit stageEstate tax litigation stage

21

Forensic and Valuation Services Section

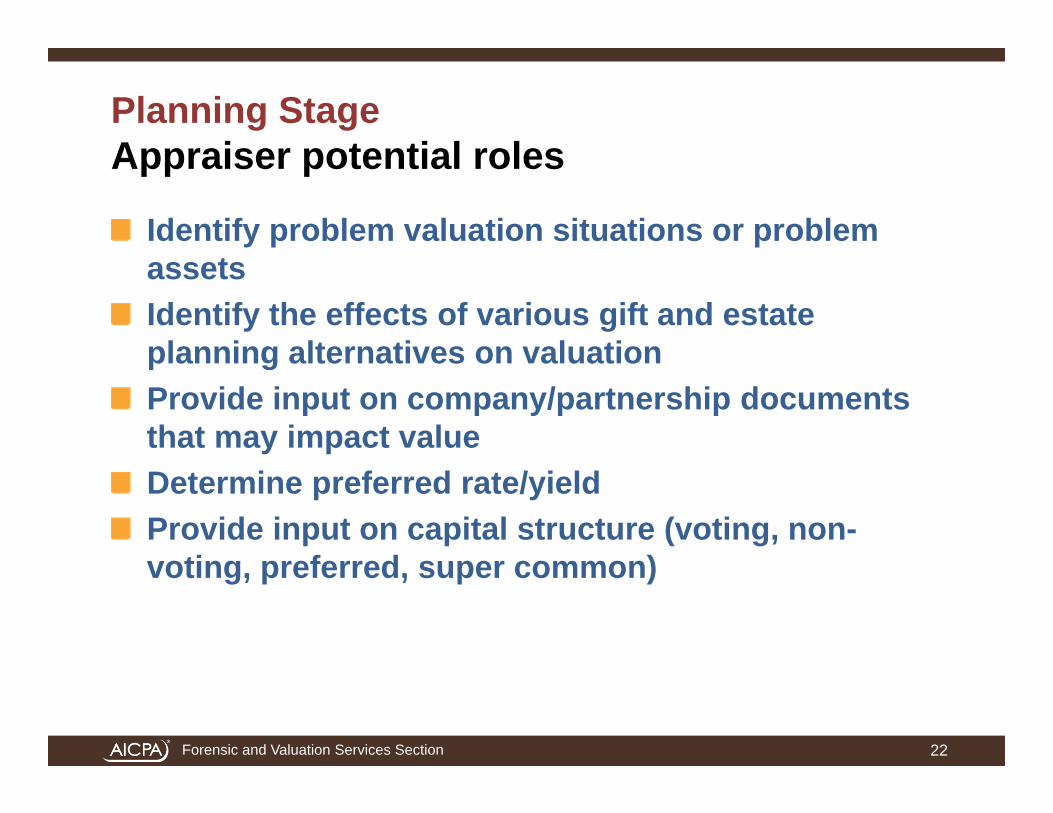

Planning StageAppraiser potential roles

Identify problem valuation situations or problem assetsIdentify the effects of various gift and estate planning alternatives on valuationProvide input on company/partnership documents that may impact valueDetermine preferred rate/yieldProvide input on capital structure (voting, non-voting, preferred, super common)

22

Forensic and Valuation Services Section

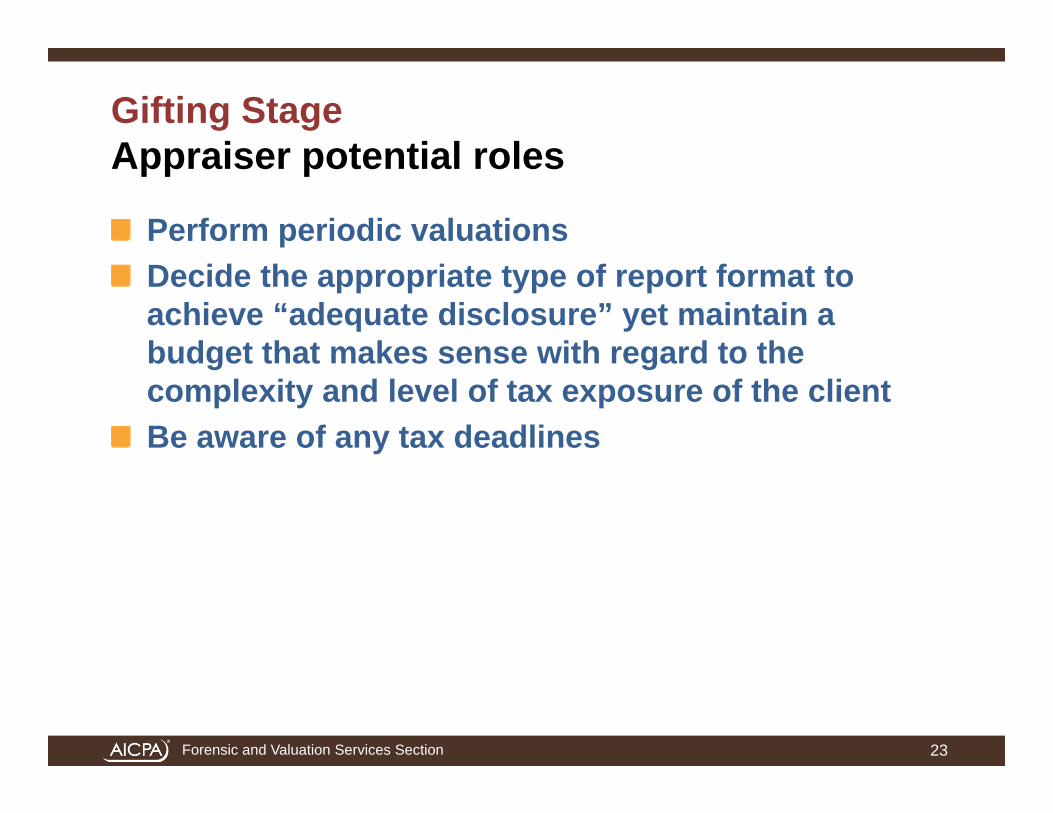

Gifting StageAppraiser potential roles

Perform periodic valuationsDecide the appropriate type of report format to achieve “adequate disclosure” yet maintain a budget that makes sense with regard to the complexity and level of tax exposure of the clientBe aware of any tax deadlines

23

Forensic and Valuation Services Section

Estate Tax StageAppraiser potential roles

Perform valuation as of the date of deathProvide input on whether alternative valuation date should be consideredIf requested/needed, perform valuation as of alternative valuation dateSometimes more than one valuation firm is engaged to perform the valuation

24

Forensic and Valuation Services Section

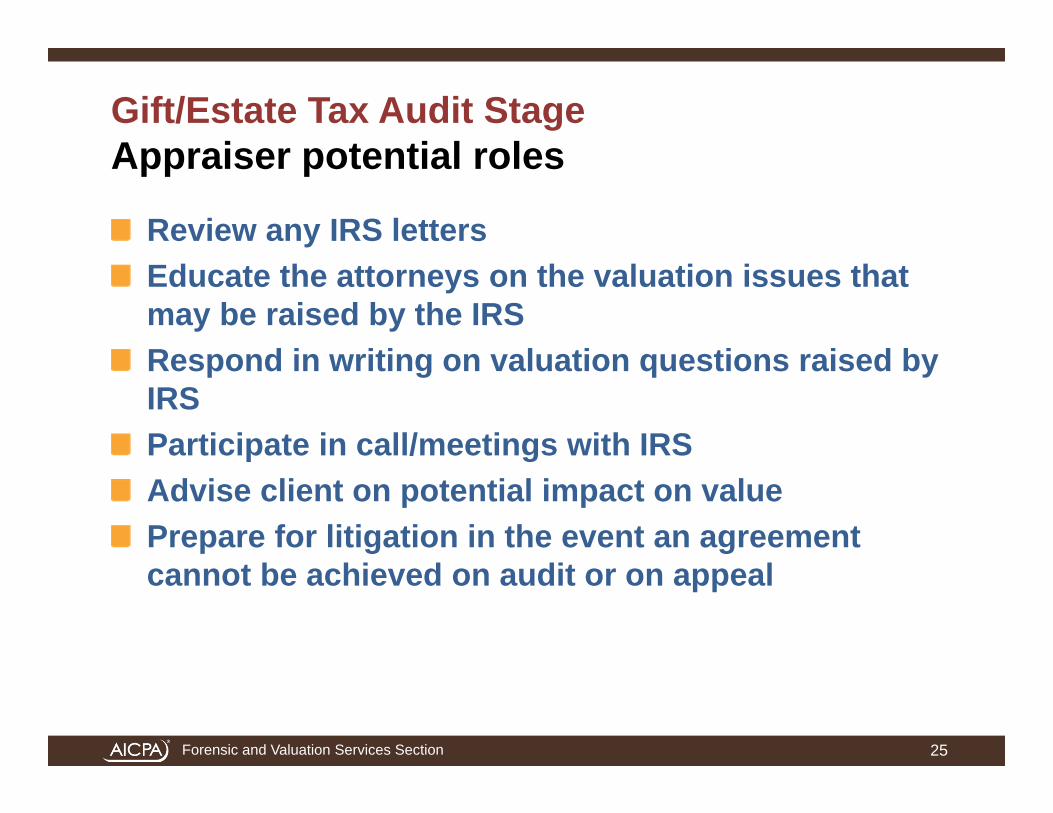

Gift/Estate Tax Audit StageAppraiser potential roles

Review any IRS letters Educate the attorneys on the valuation issues that may be raised by the IRSRespond in writing on valuation questions raised by IRSParticipate in call/meetings with IRSAdvise client on potential impact on value Prepare for litigation in the event an agreement cannot be achieved on audit or on appeal

25

Forensic and Valuation Services Section

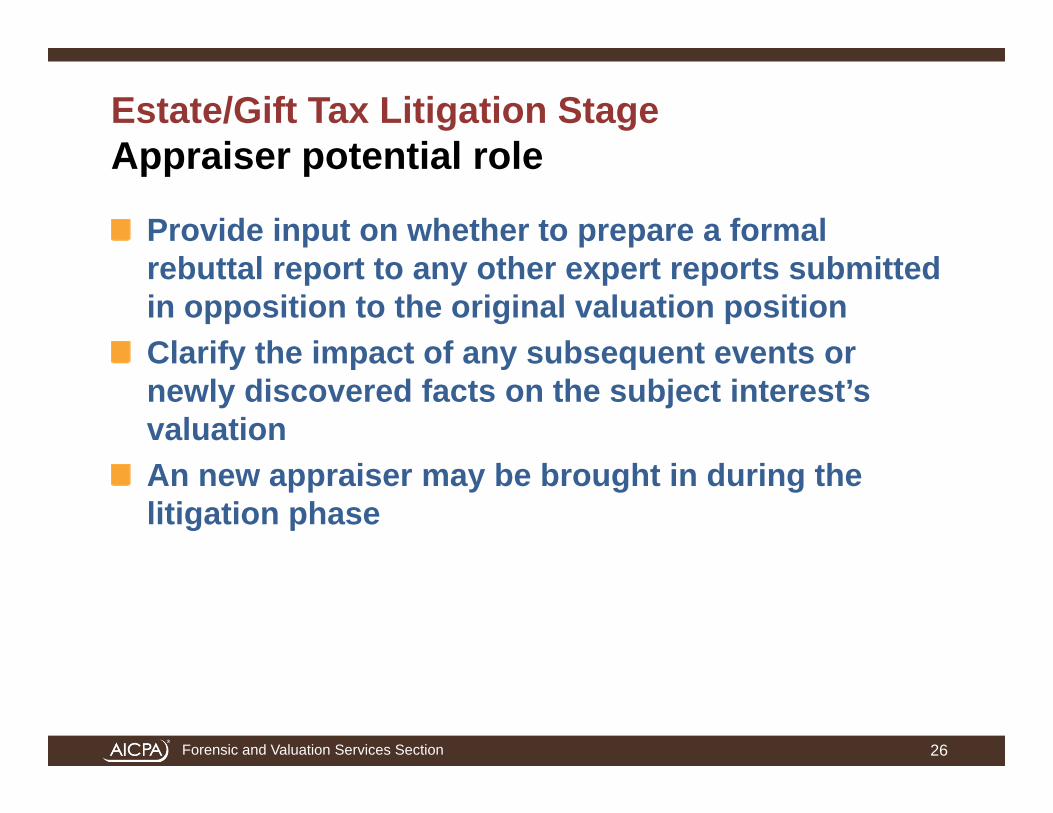

Estate/Gift Tax Litigation StageAppraiser potential role

Provide input on whether to prepare a formal rebuttal report to any other expert reports submitted in opposition to the original valuation positionClarify the impact of any subsequent events or newly discovered facts on the subject interest’s valuationAn new appraiser may be brought in during the litigation phase

26

Forensic and Valuation Services Section

Valuation Issues in the Drafting of Company and Partnership Documents

27

Forensic and Valuation Services Section

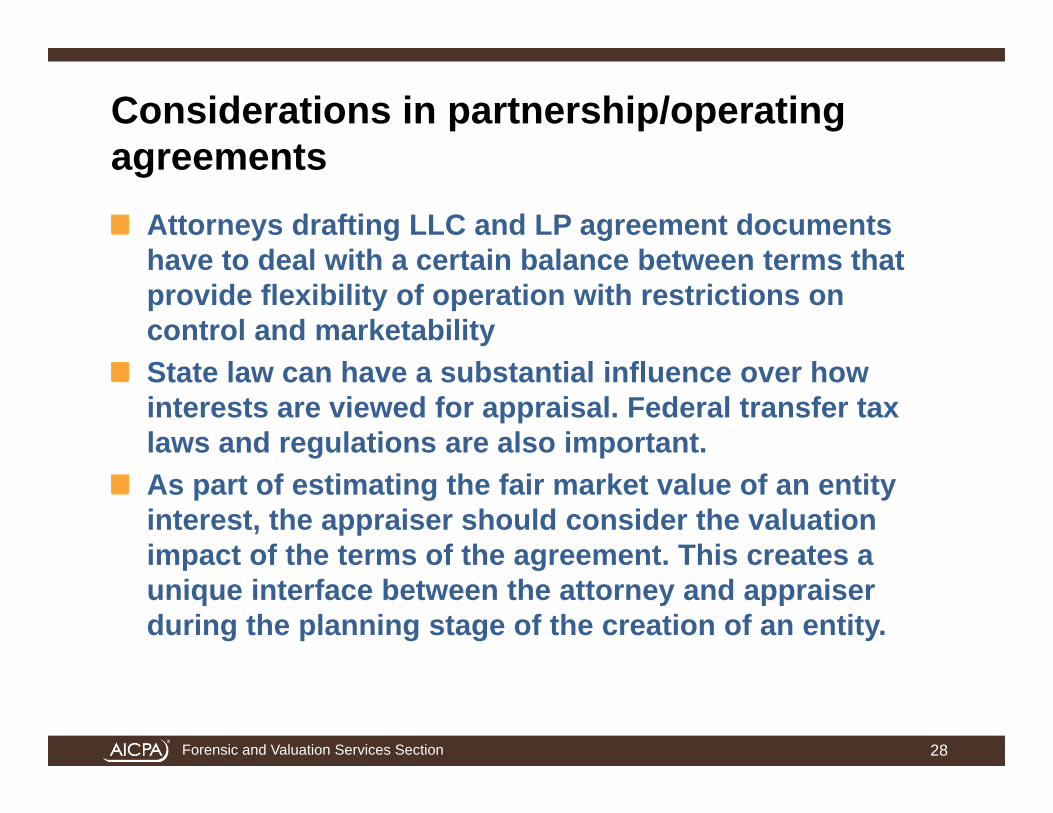

Considerations in partnership/operating agreements

Attorneys drafting LLC and LP agreement documents have to deal with a certain balance between terms that provide flexibility of operation with restrictions on control and marketabilityState law can have a substantial influence over how interests are viewed for appraisal. Federal transfer tax laws and regulations are also important.As part of estimating the fair market value of an entity interest, the appraiser should consider the valuation impact of the terms of the agreement. This creates a unique interface between the attorney and appraiser during the planning stage of the creation of an entity.

28

Forensic and Valuation Services Section

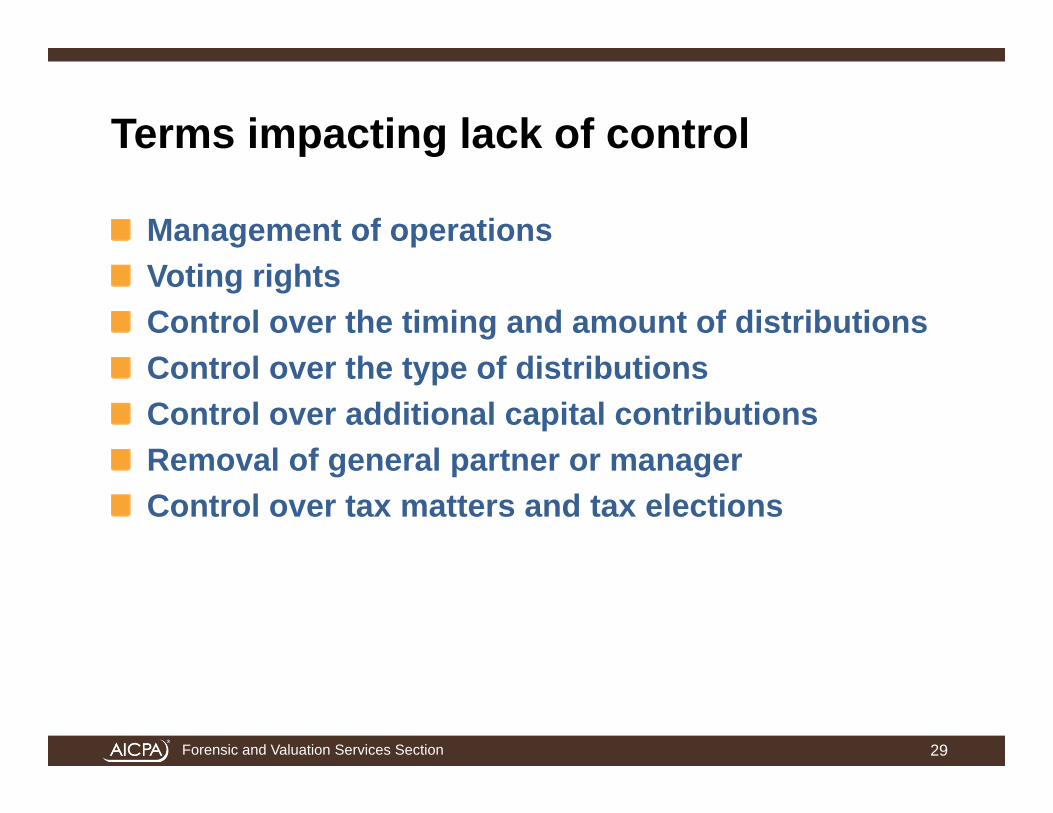

Terms impacting lack of control

Management of operationsVoting rightsControl over the timing and amount of distributionsControl over the type of distributionsControl over additional capital contributionsRemoval of general partner or managerControl over tax matters and tax elections

29

Forensic and Valuation Services Section

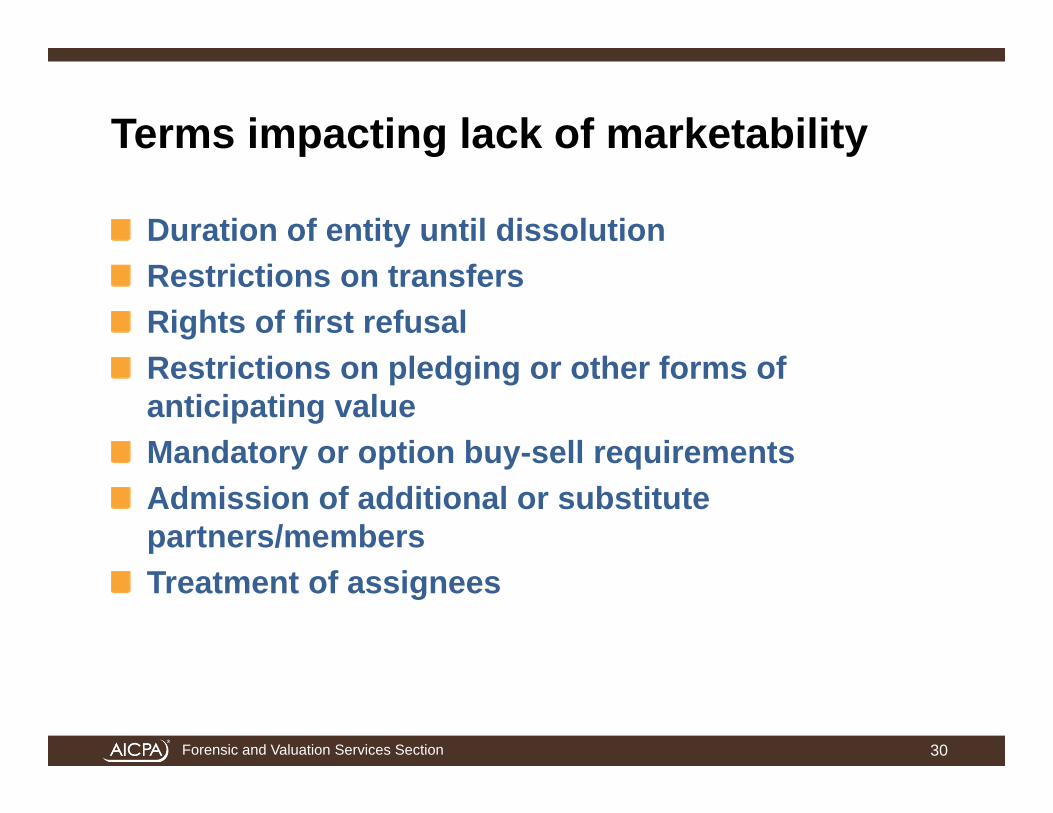

Terms impacting lack of marketability

Duration of entity until dissolutionRestrictions on transfersRights of first refusalRestrictions on pledging or other forms of anticipating valueMandatory or option buy-sell requirementsAdmission of additional or substitute partners/membersTreatment of assignees

30

Forensic and Valuation Services Section

Terms impacting other adjustments

Built-in gains and the Section 754 election adjustment• Built-in gains that result when a buyer of a partnership interest

cannot adjust his share of the basis of the assets in apartnership to their present value has a detrimental impact onthe marketability of the entity’s interests.

• Ownership interests that cannot compel the management of theentity to enter into this election tend to have larger marketabilitydiscount adjustments to reflect the fewer number of buyerswilling to take the risk that an election will be made in the futureat the appropriate time.

• Some entity agreements make the party requesting the 754election bear the costs of compliance. This contingent costburden also results in an incremental additional discount.

31

Forensic and Valuation Services Section

Terms impacting other adjustments (continued)

Loss of a key manager – rules for successor management• Some agreements have complicated successor appointment

terms which could slow down the ability of the entity to respondto business opportunities or risks during a time when the entityhas lost a key manager. This factor can result in an increaseddiscount adjustment.

32

Forensic and Valuation Services Section

Terms impacting other adjustments (continued)

Greater restrictions in the terms of an entity agreement may result in loss of present interest status • Estate of Hackl

- The judge viewed what he concluded were overly-broad provisionsin the operating agreement of the LLC that had the effect ofeliminating any meaningful economic benefits to the immediateuse, possession, or enjoyment of the subject LLC intereststransferred under the annual exclusion gift under Section 2503(b).

• Some commentators have suggested providing a limited (in time) rightof redemption or put right for minority interests whereby the interestcould be redeemed by the entity at fair market value, applying all theappropriate discount adjustments, in order to substantiate that theinterest has a present economic benefit.

33

Forensic and Valuation Services Section

Recent Discount Settlements

34

Forensic and Valuation Services Section

Recent discount settlements

The following data was compiled by Curtis Kimball and members of Willamette from our own case files and from materials presented by othersSettlement data is interesting because it shows what the IRS and taxpayers have agreed to as fair market value in cases that are similar in nature to valuation engagements in which one may be currently involvedThese are out of court settlements

35

Forensic and Valuation Services Section

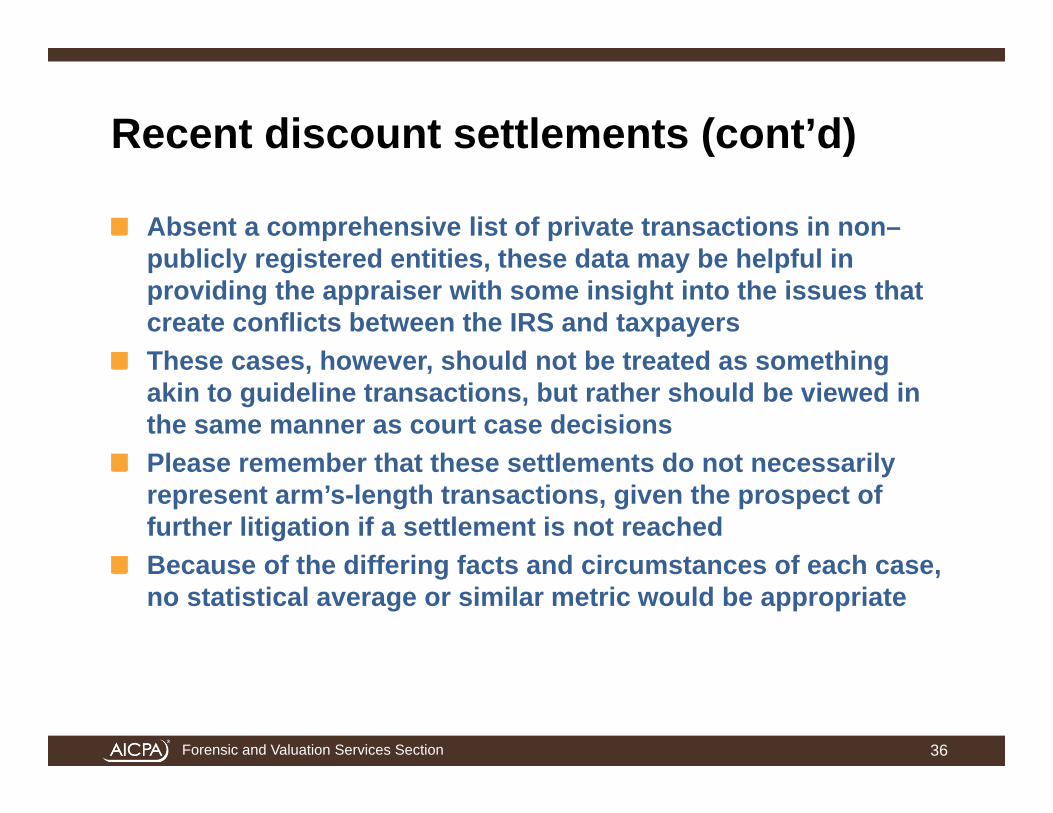

Recent discount settlements (cont’d)

Absent a comprehensive list of private transactions in non–publicly registered entities, these data may be helpful in providing the appraiser with some insight into the issues that create conflicts between the IRS and taxpayersThese cases, however, should not be treated as something akin to guideline transactions, but rather should be viewed in the same manner as court case decisionsPlease remember that these settlements do not necessarily represent arm’s-length transactions, given the prospect of further litigation if a settlement is not reached Because of the differing facts and circumstances of each case, no statistical average or similar metric would be appropriate

36

Forensic and Valuation Services Section

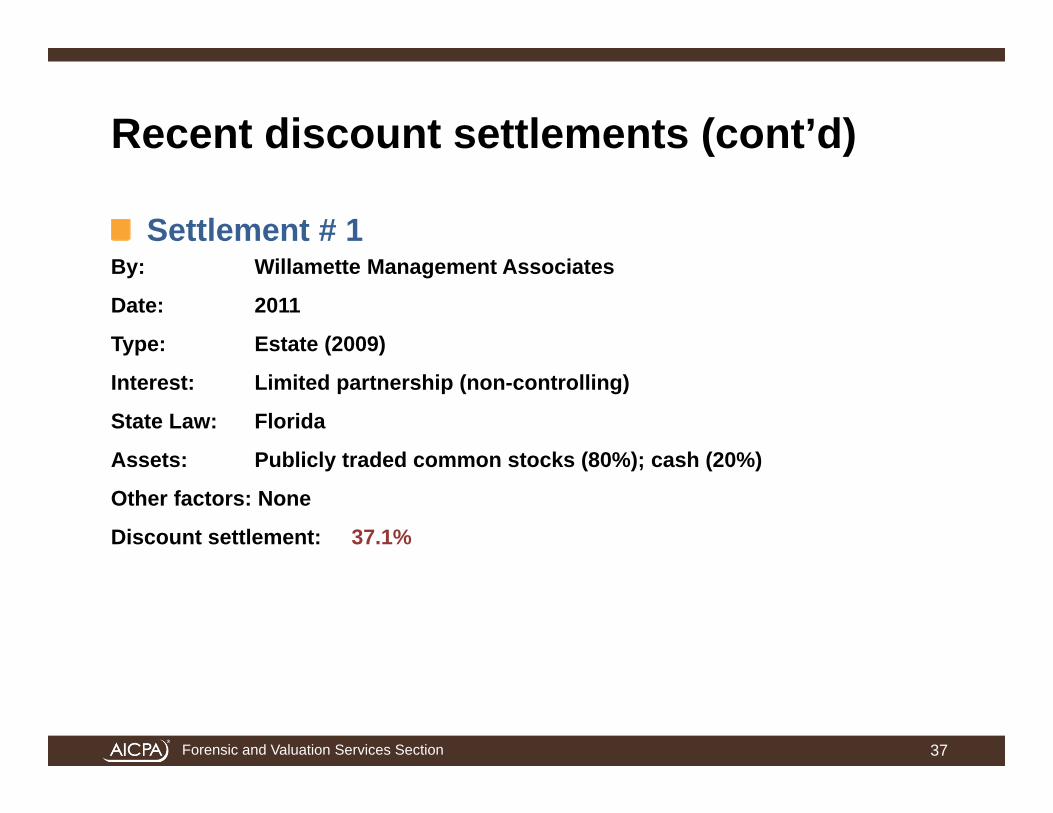

Recent discount settlements (cont’d)

Settlement # 1By: Willamette Management Associates

Date: 2011

Type: Estate (2009)

Interest: Limited partnership (non-controlling)

State Law: Florida

Assets: Publicly traded common stocks (80%); cash (20%)

Other factors: None

Discount settlement: 37.1%

37

Forensic and Valuation Services Section

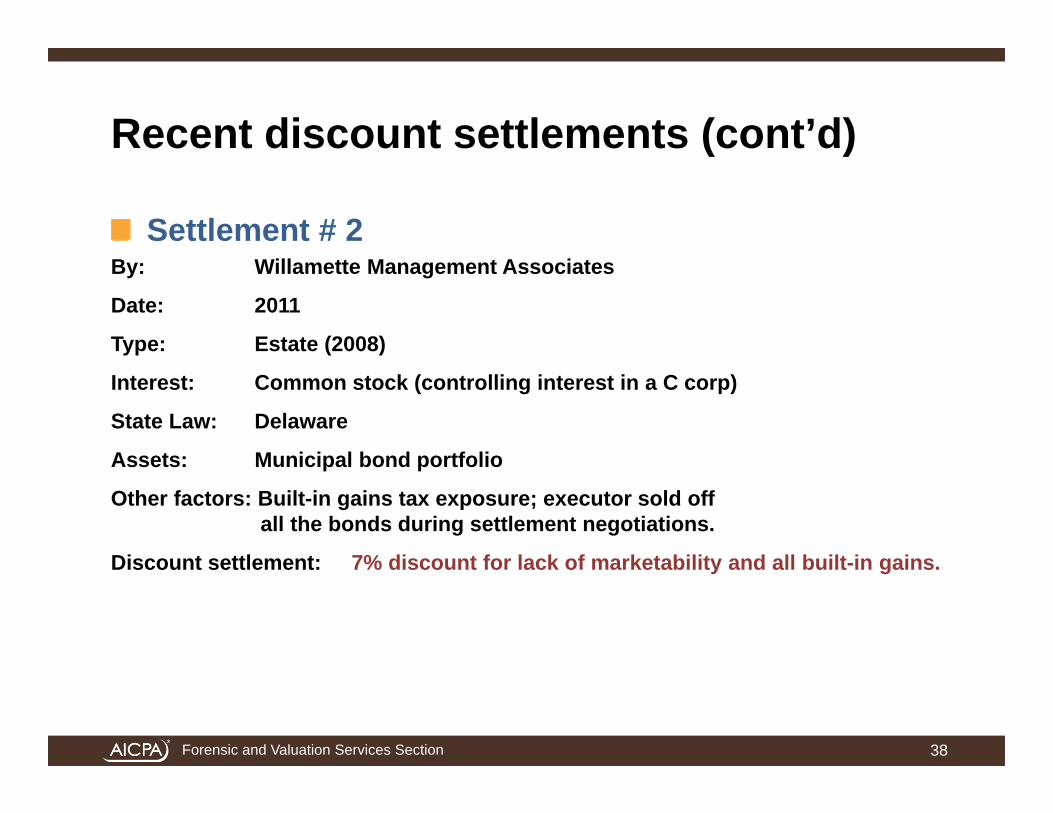

Recent discount settlements (cont’d)

Settlement # 2By: Willamette Management Associates

Date: 2011

Type: Estate (2008)

Interest: Common stock (controlling interest in a C corp)

State Law: Delaware

Assets: Municipal bond portfolio

Other factors: Built-in gains tax exposure; executor sold off all the bonds during settlement negotiations.

Discount settlement: 7% discount for lack of marketability and all built-in gains.

38

Forensic and Valuation Services Section

Recent discount settlements (cont’d)

Settlement # 3By: Willamette Management Associates

Date: 2011

Type: Estate (2007)

Interest: Limited liability company (non-controlling)

State Law: Delaware

Assets: Diversified bond portfolio

Other factors: Graegin note exposure

Discount settlement: 25% (Graegin note interest allowed)

39

Forensic and Valuation Services Section

Recent discount settlements (cont’d)

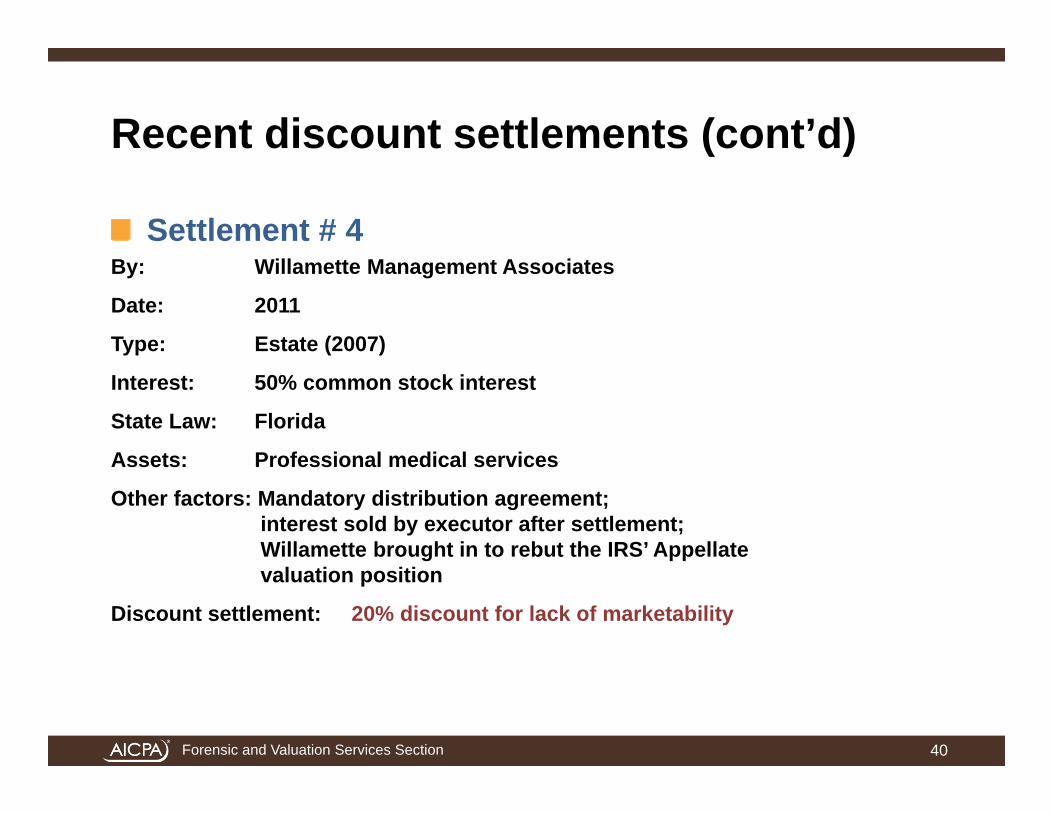

Settlement # 4By: Willamette Management Associates

Date: 2011

Type: Estate (2007)

Interest: 50% common stock interest

State Law: Florida

Assets: Professional medical services

Other factors: Mandatory distribution agreement; interest sold by executor after settlement; Willamette brought in to rebut the IRS’ Appellate valuation position

Discount settlement: 20% discount for lack of marketability

40

Forensic and Valuation Services Section

Recent discount settlements (cont’d)

Settlement # 5By: Willamette Management Associates

Date: 2011

Type: Estate (2009)

Interest: Three LP and LLC interests (all 49% non-controlling interests)

State Law: Florida

Assets: Publicly traded diversified stock and bond portfolio

Other factors: Each LLC was the general partner of one of the LPs

Discount settlement: 35.5% to 36.3%

41

Forensic and Valuation Services Section

Recent discount settlements (cont’d)

Settlement # 6By: Willamette Management Associates

Date: 2010

Type: Estate (2007)

Interest: Limited Partnership

State Law: Oregon

Assets: Commercial Real Estate

Other factors: Some exposure on valuation of underlying real estate

Discount settlement: 39%

42

Forensic and Valuation Services Section

Recent discount settlements (cont’d)

Settlement # 7By: Willamette Management Associates

Date: 2010

Type: Estate (2008)

Interest: Limited Liability Company (non-controlling)

State Law: North Carolina

Assets: Timberlands, croplands, farm house (57%); public securities - mostly stock and bond funds (43%)

Other factors: Real estate consisted of undivided interests

Discount settlement: 31.7%, plus 40% discount for undivided interests (total discount approximately 50.6%)

43

Forensic and Valuation Services Section

Recent discount settlements (cont’d)

Settlement # 8By: Willamette Management Associates

Date: 2010

Type: Estate (2007)

Interest: Limited Partnership

State Law: Florida

Assets: Stocks (50%); Bonds (50%)

Other factors: Section 2036 exposure; powers of appointment

Discount settlement: 23% for one LP block; 30.8% for other LP block (taxed under two different sections of the IRC; see Mellinger case)

44

Forensic and Valuation Services Section

Questions

www.aicpa.org/fvs 45

Forensic and Valuation Services Section

AICPA Business Valuation Web Seminar Series: Core Competencies from the Nation’s Leading Experts

www.aicpa.org/fvs 46

Upcoming Web Seminars:• Valuation for Employee Stock Ownership Plans November 17, 2011• Valuations for Financial Statement Reporting Purposes December 6, 2011• Principles of Valuation for Marital Dissolution Purposes December 15, 2011• Valuations for Dissenting Stockholder & Minority

Oppression Actions January 5, 2012• Pass-through Entity Valuation 2012: Research & Methods January 19, 2012• Forensic Analysis Expert Witness Testimony: Defending

Your Expert Report and Expert Testimony February 2, 2012

For more information visit: www.aicpa.org/BVSeries

Forensic and Valuation Services Section

See You at the Event!

Visit www.aicpa.org/FVS_CPE_Events to register for the following face-to face educational opportunities:

AICPA National Business Valuation Conference• New in 2011 – PRACTICAL APPLICATIONS TRACK!• November 6-8, 2011 in Las Vegas, NVAICPA National Healthcare Industry Conference• New in 2011 – VALUATIONS SPECIALIZATION TRACK!• November 17-18, 2011 in Baltimore, MD

www.aicpa.org/fvs 47

Forensic and Valuation Services Section

For additional information, please visit:

Forensic and Valuation Services (FVS) Sectionwww.aicpa.org/fvs

Accredited in Business Valuation (ABV) Credential Overview

www.aicpa.org/abvCertified in Financial Forensics (CFF) Credential Overview

www.aicpa.org/cff

48www.aicpa.org/fvs

Thank You!

www.aicpa.org/fvs