West Contra Costa USD General Obligation Bond, Election of 2010, Series A Presentation to the...

19

West Contra Costa USD General Obligation Bond, Election of 2010, Series A Presentation to the Facilities Subcommittee November 15, 2011

-

Upload

cecil-beasley -

Category

Documents

-

view

218 -

download

2

Transcript of West Contra Costa USD General Obligation Bond, Election of 2010, Series A Presentation to the...

West Contra Costa USDGeneral Obligation Bond, Election of 2010, Series A

Presentation to the Facilities SubcommitteeNovember 15, 2011

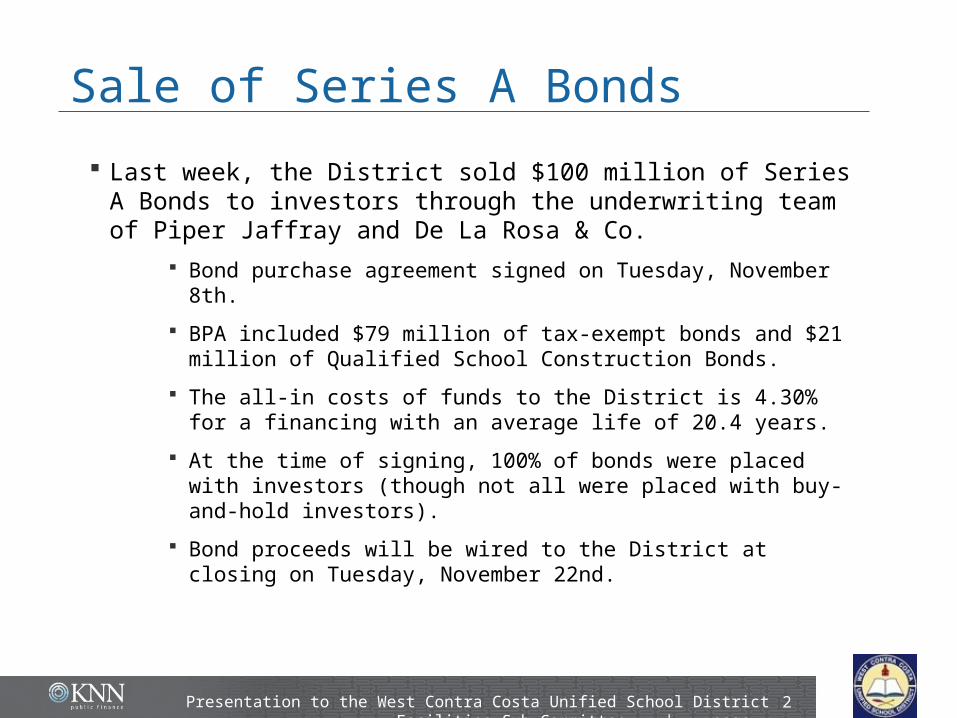

Sale of Series A Bonds

Presentation to the West Contra Costa Unified School District Facilities Sub-Committee | page

2

Last week, the District sold $100 million of Series A Bonds to investors through the underwriting team of Piper Jaffray and De La Rosa & Co.

Bond purchase agreement signed on Tuesday, November 8th.

BPA included $79 million of tax-exempt bonds and $21 million of Qualified School Construction Bonds.

The all-in costs of funds to the District is 4.30% for a financing with an average life of 20.4 years.

At the time of signing, 100% of bonds were placed with investors (though not all were placed with buy-and-hold investors).

Bond proceeds will be wired to the District at closing on Tuesday, November 22nd.

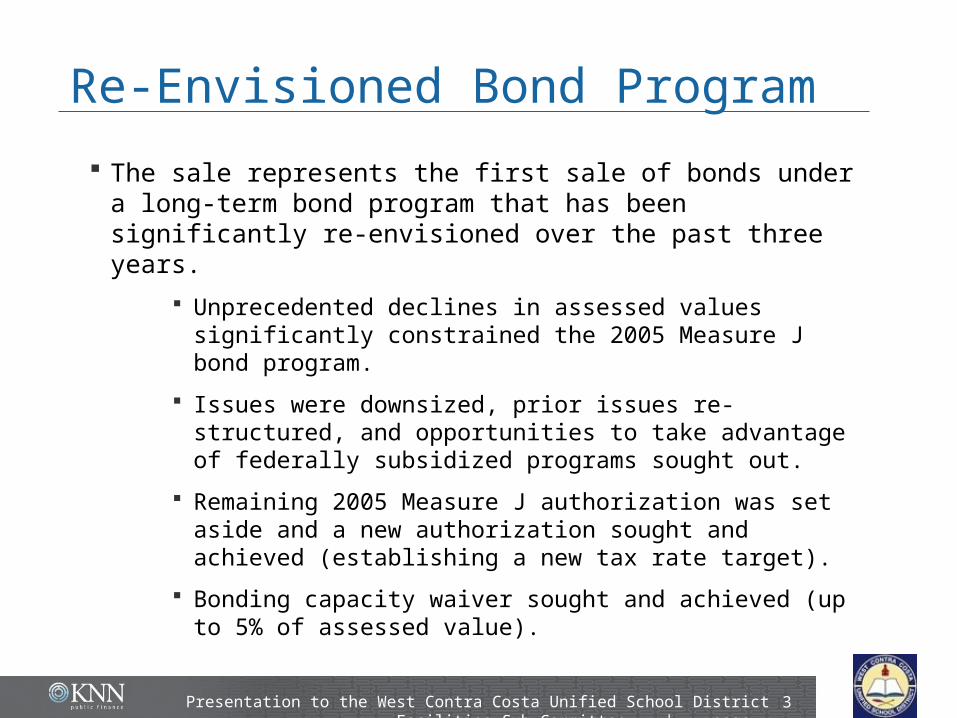

Re-Envisioned Bond Program

The sale represents the first sale of bonds under a long-term bond program that has been significantly re-envisioned over the past three years.

Unprecedented declines in assessed values significantly constrained the 2005 Measure J bond program.

Issues were downsized, prior issues re-structured, and opportunities to take advantage of federally subsidized programs sought out.

Remaining 2005 Measure J authorization was set aside and a new authorization sought and achieved (establishing a new tax rate target).

Bonding capacity waiver sought and achieved (up to 5% of assessed value).

Presentation to the West Contra Costa Unified School District Facilities Sub-Committee | page

3

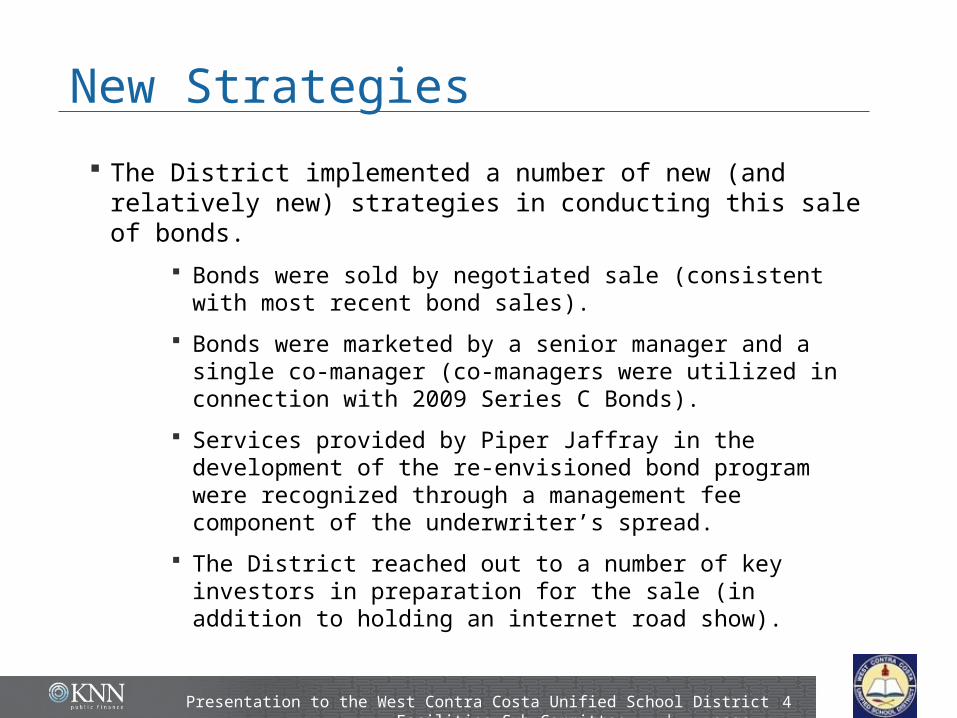

New Strategies

The District implemented a number of new (and relatively new) strategies in conducting this sale of bonds.

Bonds were sold by negotiated sale (consistent with most recent bond sales).

Bonds were marketed by a senior manager and a single co-manager (co-managers were utilized in connection with 2009 Series C Bonds).

Services provided by Piper Jaffray in the development of the re-envisioned bond program were recognized through a management fee component of the underwriter’s spread.

The District reached out to a number of key investors in preparation for the sale (in addition to holding an internet road show).

Presentation to the West Contra Costa Unified School District Facilities Sub-Committee | page

4

Primary Objectives

These new strategies and other efforts of the financing team were intended to accomplish a number of key objectives.

Achieve the lowest possible interest rates for District taxpayers (both on an absolute and spread to MMD basis).

Continue to expand the District’s investor base.

Increase the number of bonds that were sold both uninsured and at an economic benefit.

Presentation to the West Contra Costa Unified School District Facilities Sub-Committee | page

5

Summary of Results

Overall, the financing team can report that the sale met all key objectives.

Absolute yields were very low.

Yields on a spread-to-MMD basis were relatively close to past West Contra Costa USD and recent comparable transactions.

More than $44 million (or 44.2%) of the current transaction were sold without insurance (versus $64 million (or 39.5%) on the 2009 transaction and none of the 2011 refunding bonds).

Presentation to the West Contra Costa Unified School District Facilities Sub-Committee | page

6

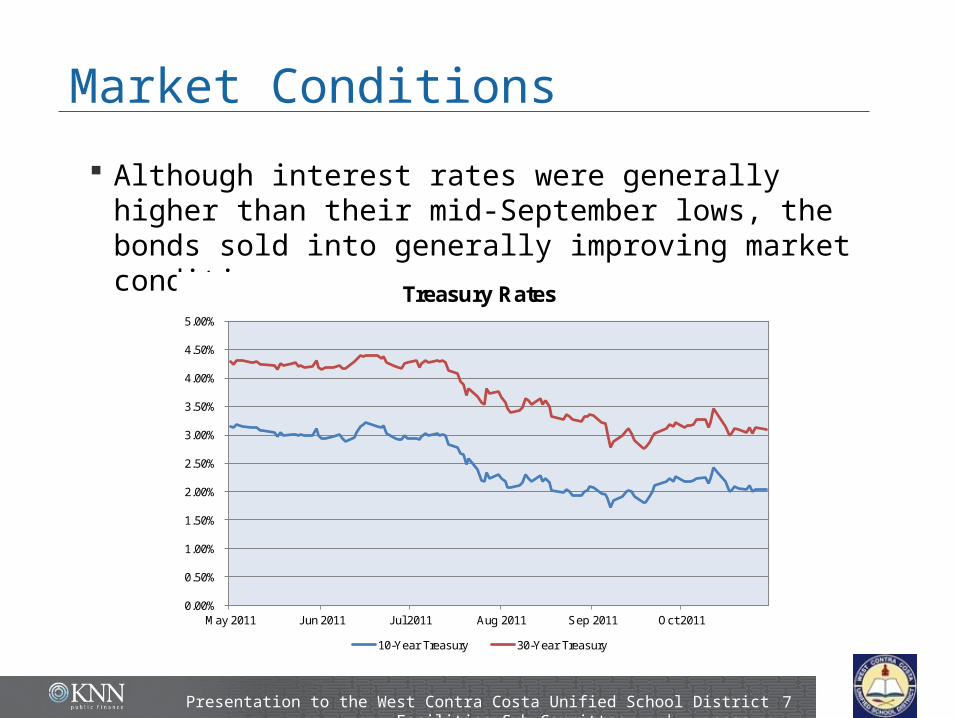

Market Conditions

Although interest rates were generally higher than their mid-September lows, the bonds sold into generally improving market conditions.

Presentation to the West Contra Costa Unified School District Facilities Sub-Committee | page

7

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

May 2011 Jun 2011 Jul 2011 Aug 2011 Sep 2011 Oct 2011

Treasury Rates

10-Year Treasury 30-Year Treasury

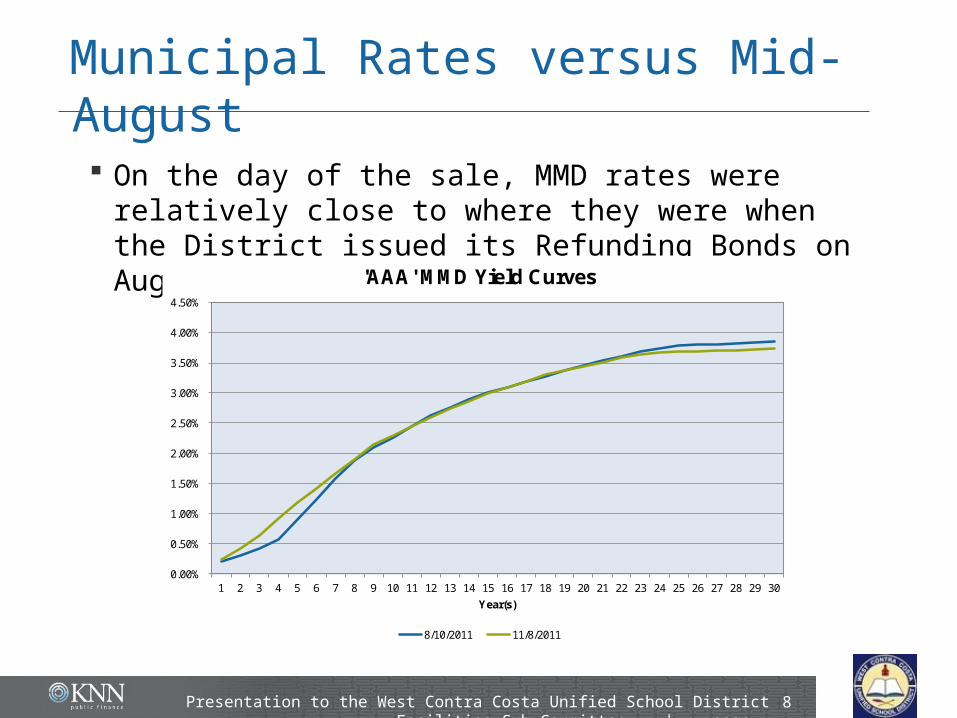

Municipal Rates versus Mid-August On the day of the sale, MMD rates were relatively

close to where they were when the District issued its Refunding Bonds on August 10th.

Presentation to the West Contra Costa Unified School District Facilities Sub-Committee | page

8

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30

Year(s)

'AAA' MMD Yield Curves

8/10/2011 11/8/2011

Refunding Opportunity

The District was not able to refund any additional bonds authorized for refunding this past summer.

Bonds authorized for refunding in July but not refunded in August remained eligible for refunding.

The financing team was prepared to move ahead with the refunding under specific circumstances (if targeted savings levels could be met with an achievable couponing structure and without moving principal payments forward).

Rates were not sufficiently low at the time of sale to recommend a refunding at the time of pricing and have not decreased since the date of pricing.

These and other bonds may become refundable in the future (even if rates don’t decrease further).

Presentation to the West Contra Costa Unified School District Facilities Sub-Committee | page

9

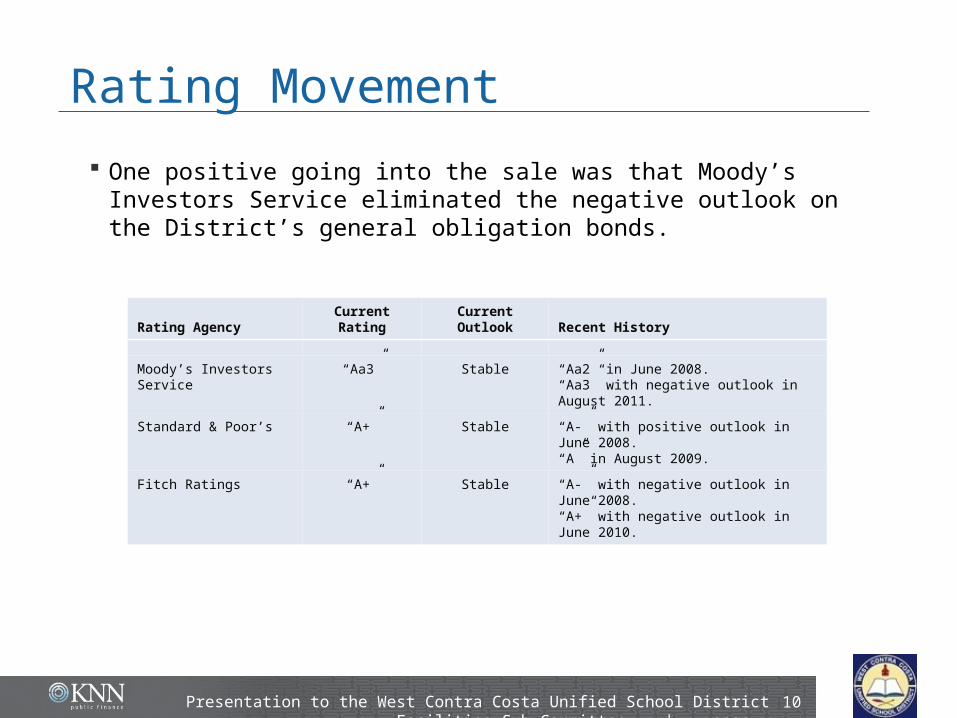

Rating Movement

One positive going into the sale was that Moody’s Investors Service eliminated the negative outlook on the District’s general obligation bonds.

Presentation to the West Contra Costa Unified School District Facilities Sub-Committee | page

10

Rating Agency Current Rating Current Outlook Recent History

Moody’s Investors Service “Aa3” Stable “Aa2” in June 2008.“Aa3” with negative outlook in August 2011.

Standard & Poor’s “A+” Stable “A-” with positive outlook in June 2008.“A” in August 2009.

Fitch Ratings “A+” Stable “A-” with negative outlook in June 2008.“A+” with negative outlook in June 2010.

Investor Outreach The District reached out to a number of key

investors in preparation for this sale.

Presentation to the West Contra Costa Unified School District Facilities Sub-Committee | page

11

American Century Fund Americo Life Insurance

Columbia Management

Charles Schwab Funds

Neuberger Berman Asset Management

Thornburg Investment Management

Vanguard Wells Capital Management Wells Proprietary Funds

Investor Participation

The bond issue attracted a broad base of institutional investors.

Presentation to the West Contra Costa Unified School District Facilities Sub-Committee | page

12

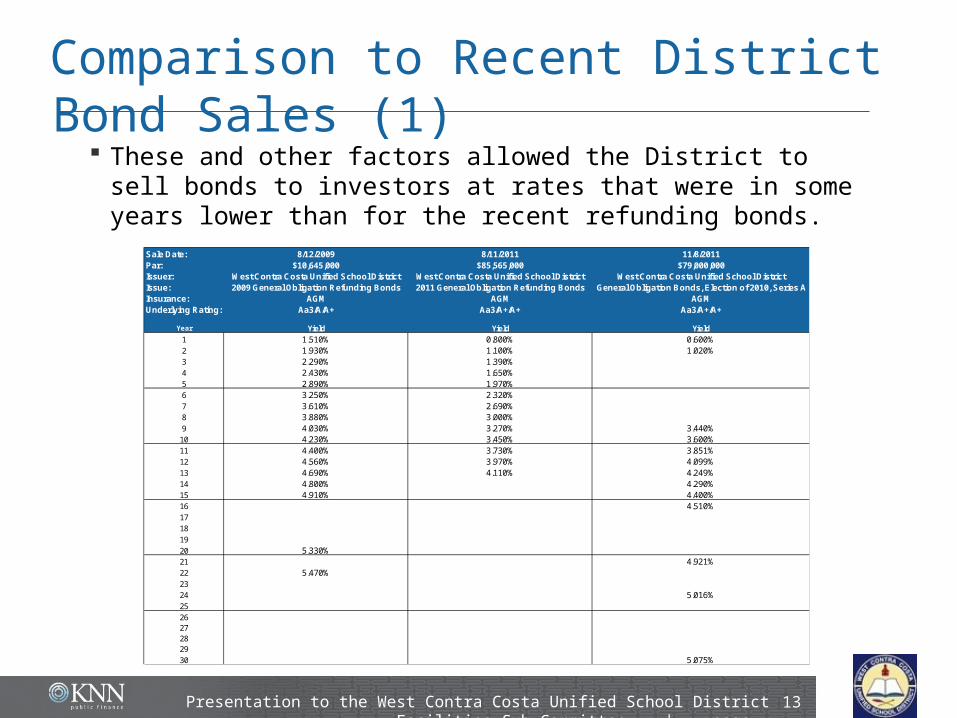

Comparison to Recent District Bond Sales (1)

These and other factors allowed the District to sell bonds to investors at rates that were in some years lower than for the recent refunding bonds.

Presentation to the West Contra Costa Unified School District Facilities Sub-Committee | page

13

Sale Date: 8/12/2009 8/11/2011 11/8/2011Par: $10,645,000 $85,565,000 $79,000,000Issuer: West Contra Costa Unified School District West Contra Costa Unified School District West Contra Costa Unified School DistrictIssue: 2009 General Obligation Refunding Bonds 2011 General Obligation Refunding Bonds General Obligation Bonds, Election of 2010, Series AInsurance: AGM AGM AGMUnderlying Rating: Aa3/A/A+ Aa3/A+/A+ Aa3/A+/A+

Year Yield Yield Yield

1 1.510% 0.800% 0.600%2 1.930% 1.100% 1.020%3 2.290% 1.390%4 2.430% 1.650%5 2.890% 1.970%6 3.250% 2.320%7 3.610% 2.690%8 3.880% 3.000%9 4.030% 3.270% 3.440%10 4.230% 3.450% 3.600%11 4.400% 3.730% 3.851%12 4.560% 3.970% 4.099%13 4.690% 4.110% 4.249%14 4.800% 4.290%15 4.910% 4.400%16 4.510%17 18 19 20 5.330% 21 4.921%22 5.470% 23 24 5.016%25 2627282930 5.075%

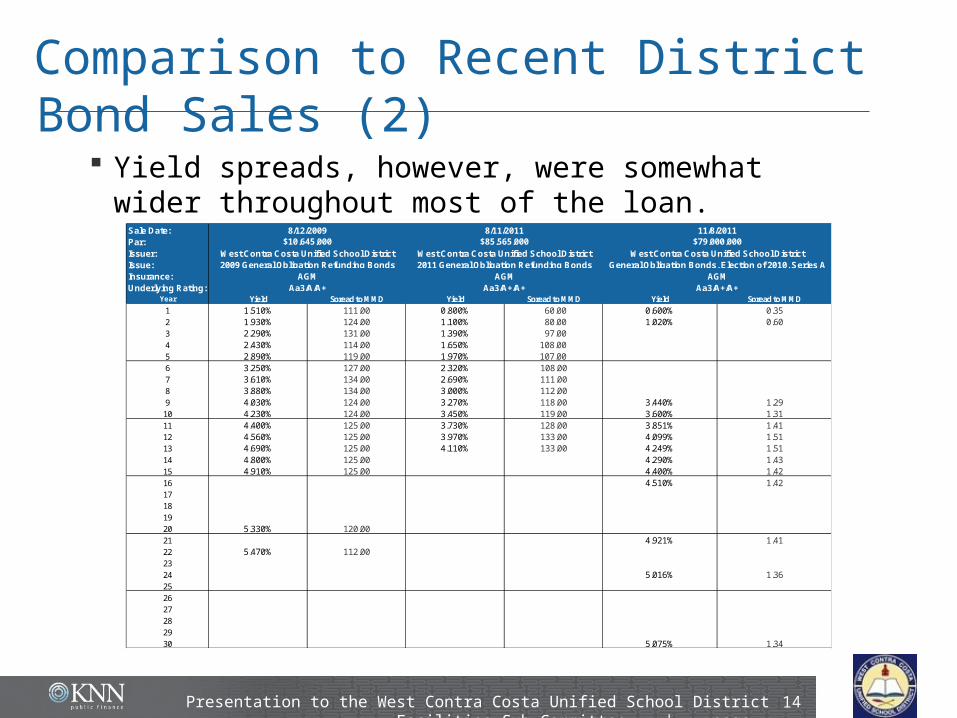

Comparison to Recent District Bond Sales (2)

Yield spreads, however, were somewhat wider throughout most of the loan.

Presentation to the West Contra Costa Unified School District Facilities Sub-Committee | page

14

Sale Date:Par: Issuer:Issue:Insurance:Underlying Rating:

Year Yield Spread to MMD Yield Spread to MMD Yield Spread to MMD

1 1.510% 111.00 0.800% 60.00 0.600% 0.352 1.930% 124.00 1.100% 80.00 1.020% 0.603 2.290% 131.00 1.390% 97.004 2.430% 114.00 1.650% 108.005 2.890% 119.00 1.970% 107.006 3.250% 127.00 2.320% 108.007 3.610% 134.00 2.690% 111.008 3.880% 134.00 3.000% 112.009 4.030% 124.00 3.270% 118.00 3.440% 1.2910 4.230% 124.00 3.450% 119.00 3.600% 1.3111 4.400% 125.00 3.730% 128.00 3.851% 1.4112 4.560% 125.00 3.970% 133.00 4.099% 1.5113 4.690% 125.00 4.110% 133.00 4.249% 1.5114 4.800% 125.00 4.290% 1.4315 4.910% 125.00 4.400% 1.4216 4.510% 1.4217 18 19 20 5.330% 120.00 21 4.921% 1.4122 5.470% 112.00 23 24 5.016% 1.3625 2627282930 5.075% 1.34

Aa3/A/A+ Aa3/A+/A+ Aa3/A+/A+

11/8/2011$79,000,000

West Contra Costa Unified School DistrictGeneral Obligation Bonds, Election of 2010, Series A

AGM

8/11/2011$85,565,000

West Contra Costa Unified School District2011 General Obligation Refunding Bonds

AGM

8/12/2009$10,645,000

West Contra Costa Unified School District2009 General Obligation Refunding Bonds

AGM

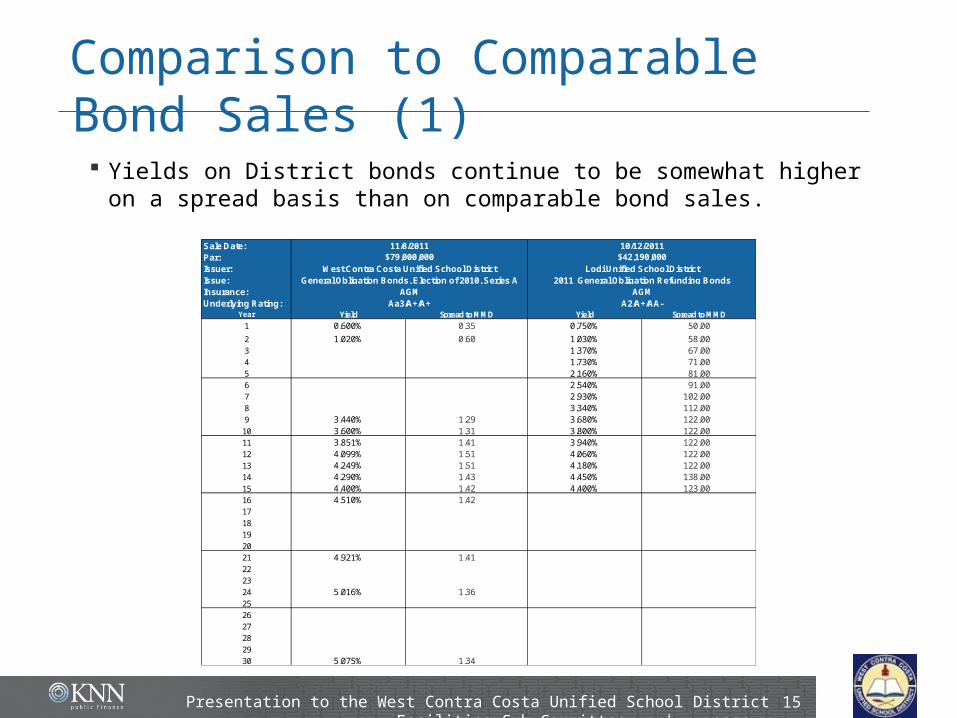

Comparison to Comparable Bond Sales (1) Yields on District bonds continue to be somewhat higher

on a spread basis than on comparable bond sales.

Presentation to the West Contra Costa Unified School District Facilities Sub-Committee | page

15

Sale Date:Par: Issuer:Issue:Insurance:Underlying Rating:

Year Yield Spread to MMD Yield Spread to MMD

1 0.600% 0.35 0.750% 50.00

2 1.020% 0.60 1.030% 58.003 1.370% 67.004 1.730% 71.005 2.160% 81.006 2.540% 91.007 2.930% 102.008 3.340% 112.009 3.440% 1.29 3.680% 122.0010 3.600% 1.31 3.800% 122.0011 3.851% 1.41 3.940% 122.0012 4.099% 1.51 4.060% 122.0013 4.249% 1.51 4.180% 122.0014 4.290% 1.43 4.450% 138.0015 4.400% 1.42 4.400% 123.0016 4.510% 1.4217181920 21 4.921% 1.4122 23 24 5.016% 1.3625 2627282930 5.075% 1.34

Lodi Unified School District

AGMAGMA2/A+/AA-Aa3/A+/A+

10/12/2011

West Contra Costa Unified School District2011 General Obligation Refunding BondsGeneral Obligation Bonds, Election of 2010, Series A

11/8/2011$42,190,000$79,000,000

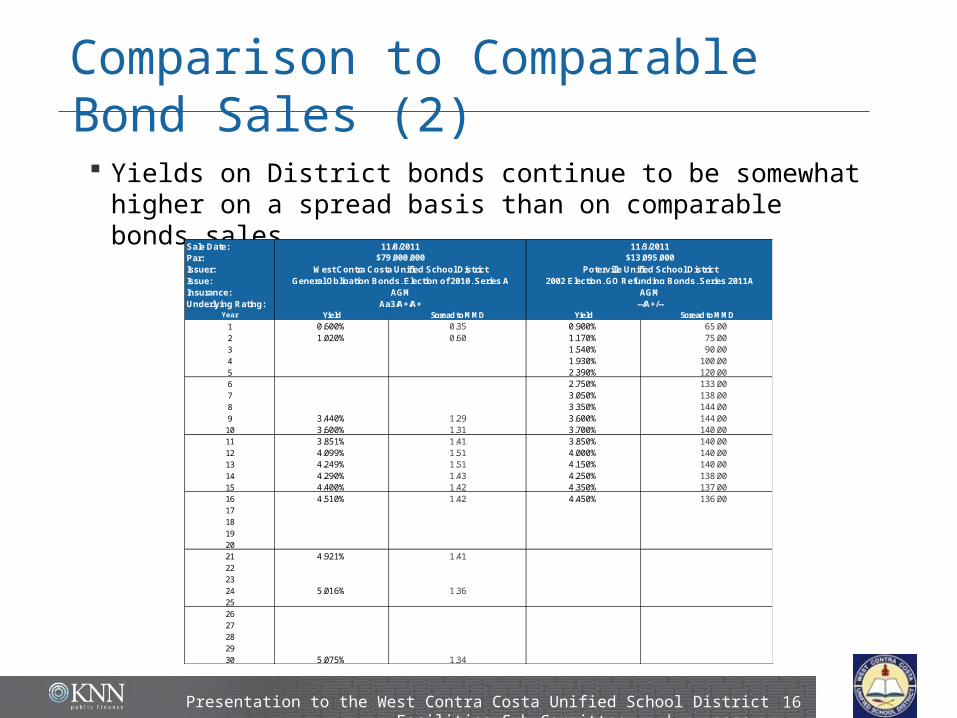

Comparison to Comparable Bond Sales (2) Yields on District bonds continue to be somewhat

higher on a spread basis than on comparable bonds sales.

Presentation to the West Contra Costa Unified School District Facilities Sub-Committee | page

16

Sale Date:Par: Issuer:Issue:Insurance:Underlying Rating:

Year Yield Spread to MMD Yield Spread to MMD

1 0.600% 0.35 0.900% 65.002 1.020% 0.60 1.170% 75.003 1.540% 90.004 1.930% 100.005 2.390% 120.006 2.750% 133.007 3.050% 138.008 3.350% 144.009 3.440% 1.29 3.600% 144.0010 3.600% 1.31 3.700% 140.0011 3.851% 1.41 3.850% 140.0012 4.099% 1.51 4.000% 140.0013 4.249% 1.51 4.150% 140.0014 4.290% 1.43 4.250% 138.0015 4.400% 1.42 4.350% 137.0016 4.510% 1.42 4.450% 136.0017181920 21 4.921% 1.4122 23 24 5.016% 1.3625 2627282930 5.075% 1.34

AGM AGMAa3/A+/A+ --/A+/--

West Contra Costa Unified School District Poterville Unified School DistrictGeneral Obligation Bonds, Election of 2010, Series A 2002 Election, GO Refunding Bonds, Series 2011A

11/8/2011 11/3/2011$79,000,000 $13,095,000

Qualified School Construction Bonds The District also sold $21 million of qualified school

construction bonds. QSCBs were authorized in connection with the LPS-

Richmond project.

District had until November 30th to issue QSCBs and now will have until November 22nd, 2014, to expend proceeds.

QSCBs were sold as taxable bonds maturing on 8/1/28 at a yield of 6.25% (220% of the comparable treasury bond yield).

Federal subsidy rate of 4.91% will reduce the net cost to the District to 1.34%.

The QSCB portion of this financing will require ongoing management (from both a subsidy and tax rate management perspective).

Presentation to the West Contra Costa Unified School District Facilities Sub-Committee | page

17

QSCB Investors

The District’s QSCBs attracted a high level of buy-and-hold investors.

Presentation to the West Contra Costa Unified School District Facilities Sub-Committee | page

18

Moving Ahead

The financing team will continue to address challenges to the bond program in the year ahead.

Existing bond programs are based on the assumption of long-term tax base growth.

Current 2010 Measure D financing plan assumes that bonds will be issued in alternate years of approximately equal amounts through.

Projects continue to straddle bond issuances.

The District should continue to communicate positive status about the bond program.

Presentation to the West Contra Costa Unified School District Facilities Sub-Committee | page

19