Wenger & Vieli Switzerland - International Tax Review · 2015-03-12 · Switzerland’s corporate...

48

Published in association with: burckhardt Deloitte KPMG Tax Partner AG – Taxand Wenger & Vieli TAX REFERENCE LIBRARY NO 97 Switzerland 4th edition

Transcript of Wenger & Vieli Switzerland - International Tax Review · 2015-03-12 · Switzerland’s corporate...

Published in association with:

burckhardtDeloitteKPMGTax Partner AG – TaxandWenger & Vieli

T A X R E F E R E N C E L I B R A R Y N O 9 7

Switzerland 4th edition

W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M 1

3 BEPSSwiss CTR III: Interaction and alignmentwith BEPSBruno Bächli from Wenger & Vieli looks atthe proposed measures under Switzerland’s cor-porate tax reform package, outlining the extentof BEPS alignment and assessing which meas-ures are likely to be tweaked to become BEPS-compliant.

8 CTR IIISwiss CTR III: Latest developmentsThe consultation procedure for Swiss CorporateTax Reform III (CTR III), the most sweepingSwiss corporate tax reform in more than 50years, ended January 31 2015. Deloitte’sRene Zulauf and Diego Weder provide anupdate what is still to come as part of thereform package, and analyse what changesshould be made in light of stakeholderfeedback.

12 CTR III | NIDCTR III: Recent legislative developments onnotional interest deduction regimeInternational pressure means Switzerland mustharmonise its tax law to ensure the futureattractiveness of the business location. SusanneSchreiber and Maxim Dolder of KPMGSwitzerland provide insight on the future Swissfiscal landscape, focusing on financing activitiesand the proposed notional interest deduction tomaintain competitive conditions for inter-com-pany financing activities.

17 Exchange of informationInternational exchange of information in taxmattersOliver Jaeggi and Stephan Pfenninger, of TaxPartner AG – Taxand, review how Switzerlandis adapting to the latest internationaldevelopments in the area of tax informationexchange, including spontaneous, on requestand automatic.

23 Financial services | VATSwiss VAT treatment of financial services: Anever-ending storyRoland Reding and Marcel Mangold of KPMGSwitzerland analyse a recent decision of theFederal Administrative Court regarding theSwiss VAT treatment of intermediation services(particularly in respect of securities transactions)in the financial services industry and look at theimpact it may have on Swiss financialinstitutions.

28 Intellectual propertyIntroduction of a Swiss Licence Box regimeStefan Kuhn, head of corporate tax at KPMGSwitzerland, looks at intellectual property (IP)taxation in the country, how it compares inter-nationally and how this is set to change withthe introduction of an IP box tax regime.

32 International alignmentThe Swiss construction site: Aligning taxlaw with international standardsIn recent years, Switzerland has confirmed itscommitment to internationally-recognised stan-dards of taxation and the global fight againsttax fraud and tax evasion with a view to safe-guarding the integrity and reputation of thecountry while remaining an attractive businesslocation. Rolf Wüthrich of burckhardt explainsthis process.

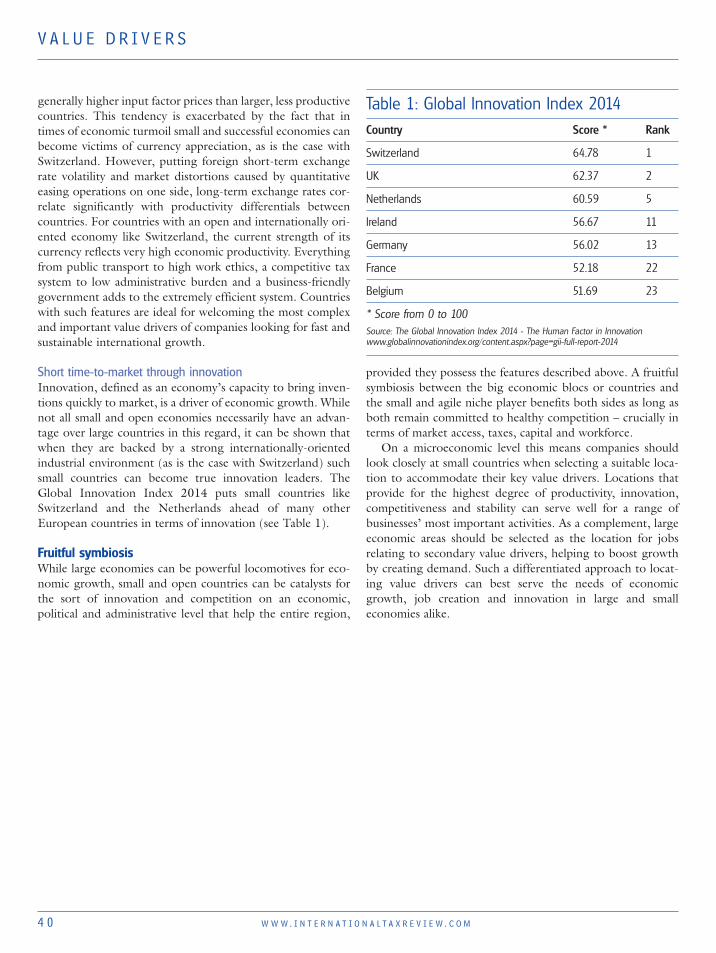

37 Value driversAt the heart of value drivers: Location andthe case for small, open economiesAndré Guedel, of KPMG, analyses businessvalue drivers and the importance of site selec-tion, looking at what lessons can be learnt fromSwitzerland as a small, open economy.

41 VATWhat do foreign suppliers of goods andservices need to know about Swiss VAT?Laurent Lattmann and Patrick Imgrüth of TaxPartner AG – Taxand provide an overview ofthe Swiss VAT system, highlighting the chal-lenges that foreign suppliers of goods and serv-ices need to be aware of, including new andupcoming changes.

Switzerland

E D I T O R I A L

2 W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M

8 Bouverie StreetLondon EC4Y 8AX UKTel: +44 20 7779 8308Fax: +44 20 7779 8500

Managing editor Ralph [email protected]

Editor Matthew [email protected]

Reporter Joe [email protected]

Reporter Meredith [email protected]

Managing editor, TPWeek.com Sophie [email protected]

Reporter, TPWeek.com Sophie [email protected]

Production editor João [email protected]

Publisher Oliver [email protected]

Associate publisher Andrew [email protected]

Online associate publisher Megan [email protected]

Marketing manager Kendred [email protected]

Marketing executive Sophie [email protected]

Subscriptions manager Nick [email protected]

Account manager James [email protected]

Divisional director Greg Kilminster

© Euromoney Trading Limited, 2015. The copyright of all editorialmatter appearing in this Review is reserved by the publisher. No matter contained herein may be reproduced, duplicated orcopied by any means without the prior consent of the holder of thecopyright, requests for which should be addressed to the publisher.Although Euromoney Trading Limited has made every effort toensure the accuracy of this publication, neither it nor anycontributor can accept any legal responsibility whatsoever forconsequences that may arise from errors or omissions, or anyopinions or advice given. This publication is not a substitute forprofessional advice on specific transactions.

Chairman Richard Ensor

Directors Sir Patrick Sergeant, The Viscount Rothermere,Christopher Fordham (managing director), Neil Osborn, Dan Cohen,John Botts, Colin Jones, Diane Alfano, Jane Wilkinson, MartinMorgan, David Pritchard, Bashar AL-Rehany, Andrew Ballingal,Tristan Hillgarth.

International Tax Review is published 10 times a year byEuromoney Trading Limited.

This publication is not included in the CLA license.

Copying without permission of the publisher is prohibitedISSN 0958-7594

Customer services:+44 20 7779 8610

UK subscription hotline:+44 20 7779 8999

US subscription hotline:+1 800 437 9997

I n previous editions of this guide (and in plenty of other fora),Switzerland has been described as a leading example of a country usingtheir national tax system to attract investment.While some have traditionally viewed the landlocked country as an out-

lier because of a reluctance to conform with international trends, the con-tinuing wave of global tax transparency and information exchangeinitiatives has not bypassed Switzerland, as burckhardt’s article on interna-tional alignment measures indicates.Tax Partner AG – Taxand’s article also picks up on information exchange,

by exploring the circumstances relating to automatic, spontaneous and on-request exchanges. Recent agreements such as February’s signing of a treatywith Italy to combat tax evasion show that this is on the government’s agen-da, and comments from Eveline Widmer-Schlumpf, the Swiss finance minis-ter, about future accords with Germany and others suggest this will continue.Levels of transparency are set to increase even further, and this guide

will help you effectively prepare for the associated compliance burdens.The guide also summarises how the Corporate Tax Reform III (CTR

III) project is being tweaked to ensure it will not require further changespost-implementation when the final outcomes from the OECD’s base ero-sion and profit shifting (BEPS) project become clear.Wenger & Vieli looks at the Swiss position regarding the BEPS project,

while Deloitte analyses CTR III comprehensively. KPMG narrows thatfocus to look at financing activities and the proposed notional interestdeduction under the CTR III umbrella.Of course, plenty of non-tax factors make Switzerland an attractive place

to do business. International tax developments do not affect many of these,while others are set to be improved to maintain a national attractiveness.KPMG looks at value drivers and site selection, shining a light on areas thatother countries could learn from.And as the global shift from direct to indirect taxation continues, VAT

related concerns are moving up the list of taxpayer priorities, not least inSwitzerland. Here, KPMG focuses on the VAT issues relevant for the financialservices sector, while Tax Partner AG – Taxand provides foreign suppliers ofgoods and services everything they need to know to remain VAT compliant. We hope the fourth edition of this Switzerland guide provides useful

insight as taxpayers seek to navigate a constantly-evolving landscape.

Matthew GilleardEditor, International Tax Review

Editorial

B E P S

W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M 3

Swiss CTR III: Interaction andalignment with BEPS

Bruno Bächli fromWenger & Vieli looksat the proposedmeasures underSwitzerland’s corporatetax reform package,outlining the extent ofBEPS alignment andassessing whichmeasures are likely tobe tweaked to becomeBEPS-compliant.

Google, Apple and Amazon under fire in OECD war on tax evasion

Apple faces “billions of euros” costs in tax avoidance probe, report says

Amazon faces European Union tax avoidance investigation

Headlines from newspapers and news portals

T oday’s international corporate taxation is based on the interactionbetween national tax laws and bilateral agreements. The primary pur-pose of the double tax treaties (DTTs), as part of these bilateral agree-

ments, is the avoidance of double taxation. Lately it has increasingly beenbrought to the attention of the general public that these DTTs can be usedto reduce taxation by means of a corresponding coordination with thenational tax laws through international constructions – mainly by multina-tional enterprises (MNEs) – in which profits are separated from the placewhere there is substance and shifted to low-tax jurisdictions. Sometimes itis possible for a double non-taxation (in other words, non-taxation) to beachieved by such constructions. The present developments were made possible by the global increase in

tax transparency. This transparency introduced so-called harmful tax prac-tices of the MNEs to the mainstream media. The world has become small-er as a result of progressive globalisation – and so has the tax world. The 2008 financial crisis, which had an impact on the development of

national budgets, speeded up the transparency process further.Compensation for missing funds needed for national budgets was primari-ly sought on the revenue side. Cuts on the expenditure side are politicallyunattractive and more difficult to enforce. Apart from the EU, the Organisation for Economic Cooperation and

Development (OECD) and the G20 are working on the base erosion andprofit shifting (BEPS) project. The BEPS initiative has the objective ofsecuring taxation of corporate profits in the place where value is created.At the same time, the international non-taxation of profits should be madeimpossible and the erosion of the tax base prohibited. The OECD’s effortsare ultimately aimed at better alignment of place of taxation and locationof economic substance. In future, when management is choosing an appropriate location for

mobile functions of an international group (for example financing, licenceadministration and so on), in addition to the usual evaluation process it willalso need to take the elements of the BEPS initiative into consideration.

B E P S

4 W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M

Just because of the above-mentioned transparency, consider-ations regarding a possible loss of reputation cannot beignored when choosing a location. No manager wants to readheadlines about his company in the press along the lines ofthose cited above. Companies which perform the above-mentioned mobile

functions have hitherto been typically located in so-calledlow-tax countries. Switzerland has also benefitted from thistrend in the past. These companies frequently enjoyed a taxregime which led to privileged taxation of the company or itsactivities. This kind of company in particular is now confront-ed with innovations and questions in connection withCorporate Tax Reform III (CTR III) and BEPS.

Existing corporate tax law and BEPSFrom a Swiss point of view there is no urgent need to amend thecurrently valid corporate tax law. The general tax conditions inSwitzerland are attractive by comparison with other countries.Corporate profits are generally taxed at a low rate. Where a com-pany was able to benefit additionally by using a tax regime, theresult was often a very advantageous level of taxation. The retention of these tax privileges would no doubt have

led to unilateral sanctions by foreign countries (this hasalready happened in some cases) and the supposed advantagesfor the company would have been undermined (for example,by taxation in another country under controlled foreign com-pany (CFC) or similar rules, or the refusal to grant treatyrelief). In this respect, it was right and inevitable thatSwitzerland agreed to the existing tax regimes being aban-doned. The report to the Swiss Federal Finance Departmentfrom the Steering Committee for Corporate Tax Reform III,published in December 2013, takes this up. Although the tax privileges criticised by the EU are going

to be abolished, at this point let us consider whether, and towhat extent, the existing corporate tax law is in harmony withBEPS. In principle, BEPS is not aiming at the level of the tax

rates, that is, the trend to low tax rates in Switzerland is notin itself a problem under BEPS, so that there would be noimmediate need to take action here under BEPS. An element of the BEPS project is to neutralise the

effects of hybrid mismatch constructions. These construc-tions were used to reduce the tax burden by exploiting thelack of coordination between the local tax laws of the corre-sponding countries, so that a deduction could be made inCountry A without this being caught as income in CountryB. Such constructions are basically not possible inSwitzerland, due to corresponding legal provisions. In thisconnection it can be stated that the existing corporate taxlaw already meets the requirements of the approach target-ed under the BEPS project. Switzerland should also score well under the head of meas-

ures to prevent tax treaty abuse, since the Federal Tax

Administration imposes high standards on the applicants withregard to entitlement to claim relief under a DTT. Wheretreaty entitlement is denied, treaty benefits cannot beobtained. With regard to measures for countering harmful tax prac-

tices, Switzerland is in a less favourable position. Six Swissregimes are being reviewed in the light of this measure. Theseare primarily the same regimes which are criticised by the EU.The regimes under attack are hardly compatible with BEPS. With regard to the BEPS project, there is clearly scope for

amendment of the existing corporate tax law. However,notwithstanding some reports in the media on this matter, it isnot the case that the existing corporate tax law would ‘fail thetest” on all aspects of the BEPS project. On the contrary, manyof the aspects which are under discussion should already becovered in Swiss legal provisions or are dealt with correspond-ingly under the existing practice of the Swiss tax authorities.

CTR IIIDue to the abolition of the above-mentioned tax privileges,Switzerland may become less attractive from a tax point ofview. As mentioned, retaining the existing corporate tax law isnot a viable strategy in today’s global tax environment, partic-ularly given the continuing direction of travel. Because of the foreign pressure on Swiss corporate tax law,

the Federal Council launched the consultation on CTR III inSeptember 2014, which lasted until January 31 2015. Theobject of CTR III is to take international developments intoaccount in the Swiss tax system, to develop them further andat the same time to retain Switzerland’s competitive position.The Federal Council suggests abolishing tax privileges whichno longer stand in accordance with international standards.These include the cantonal privileges (holding, domicile andmixed companies), and at federal level principal structures andfinance branches. Despite potentially negative effects, CTR III may also offer

Switzerland an opportunity to be one of the first countries toimplement competitive, internationally accepted and BEPS-compliant corporate taxation and to create or re-create thedesired legal certainty for companies.Even if the OECD and the G20 mention a “level playing

field”, Switzerland is in danger of being a loser under the cur-rent developments, since the large countries can influenceboth the form and the actual territorial implementation of theinternational fiscal framework. In other words, the smallcountries have to accept the requirements of the large coun-tries. Small countries do not have the same political and eco-nomic possibilities to assert themselves as the large ones.

Selected aspects of CTR IIIThe following section deals with selected aspects of CTR IIIand reviews their consistency with the BEPS project.Significant elements of CTR III include:

B E P S

W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M 5

• Introduction of a Licence Box(extended measures shouldbe considered, since the (modified) nexus approach –whereby income from a particular source should be linkedto expense from the same source, for example researchexpenses should be connected with licence income – isbeing pursued;

• Introduction of a notional interest deduction; and• Disclosure of hidden reserves on change of status.

Licence BoxA Licence Box is to be introduced at cantonal level. Here,reduced taxation would apply to income from intellectualproperty (IP) rights. Many European countries have alreadyhad corresponding arrangements for a while. Switzerlandshould therefore introduce this part of CTR III, also becauseSwitzerland is a country with a very high rate of innovation. The exact form of the Licence Box is under discussion. If the

requirements for the qualifying income are too broad, there isa risk that the arrangement will not be in use for very long, dueto potential international pressure. If the requirements are toostringent, such licence or patent boxes will be used less. TheUK and Germany were involved in a controversy regarding thequalifications for tax privileged income from intellectual prop-erty; a compromise was found at the end of 2014. The UKwanted to continue with its broad Patent Box requirements,while Germany sought to have higher entrance hurdlesrequired for qualifying income under the BEPS project.Agreement was basically reached that a privileged taxation forincome from IP is only allowed if this income is linked to eco-nomic activities of substance. This compromise agreement nowforms the basis for the EU and OECD requirements, whichwere subsequently also approved by the G20. The nexus approach now pursued would not be advanta-

geous for Switzerland, because MNEs which are affected by ithave outsourced a large part of their research and develop-ment (R&D) work to other countries. In particular, the phar-maceutical industry (which is very important in the Swisseconomy) has moved a significant part of its R&D workabroad. To reduce or make up for possible disadvantages of

restricted licence box conditions, a disproportionately highdeduction for R&D costs should be considered. Such deduc-tion should not be a problem from an international point ofview, since various countries have corresponding provisionsalready. Such a deduction would further be positive for theSwiss location, as it would stimulate companies to keepresearch and development jobs in Switzerland or to movethem here.

Notional interest deductionHere, the deduction for interest paid is increased by making aspecial deduction from the taxable profit for notional intereston part of equity (interest-adjusted corporate income tax).

This measure would help to equalise the differences in the taxtreatment of equity and debt.The cantonal tax authorities are critical of this measure, as

they fear a considerable reduction in revenue as a result. Interms of tax theory, this removal or partial neutralisation ofthe different treatment of debt and equity would be accept-able and welcome. Based on the details of the proposednotional interest deduction, this would not go as far as exist-ing solutions in other countries (for example Belgium), sothat from today’s perspective this measure would appear to bea method which should be BEPS-compliant. The OECD stat-ed that it does not regard a notional deduction on equity as ahybrid financing construction.

Step up in valueUnder this measure, a company which was able to benefitfrom a tax regime in the past would be granted the possibili-ty of disclosing the hidden reserves formed during the periodof the privileged taxation (including any internally generatedgoodwill). This suggestion is consistent and correct from a taxtheory point of view. It should also be in line with the grand-fathering concept which is recognised by the OECD and theEU. Due to the grandfathering, which should, in principle, bepermitted by the OECD and the EU, this measure ought tobe in accordance with the BEPS project.

Remaining a location of choiceIf the general set-up after introduction of CTR III andimplementation of the BEPS measures has a negative

Bruno BächliCertified tax expert / PartnerWenger & Vieli AG

Dufourstr. 56, Postfach 1285CH-8034 ZürichTel: +41 (58) 958 58 58 [email protected]

Bruno Bächli specialises in the area of tax advice. His tax practicefocuses on national and international tax law. Bruno has broadexperience in all areas of tax law, including, in particular, counsel-ing medium-sized enterprises and entrepreneurs. His tax practicealso includes succession planning and purchases and sales ofcompanies. His clients include private individuals, medium-sizedbusinesses and national and international groups of companies.From 1993 to 1999, Bruno Bächli worked as a tax adviser at

PwC in Zurich. Later, before joining Wenger & Vieli in 2004, heworked as a tax adviser at Schweizerische Treuhandgesellschaftin Zurich.

B E P S

6 W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M

impact on the tax position, a group which is residentabroad and hitherto has only located a few group functionsin Switzerland, such as group financing or managementfunctions, will have to consider either moving additionalactivities to Switzerland or transferring the existing Swissfunctions abroad. In connection with the current developments in taxation it

can, however, be assumed that non-tax factors will be ofincreasing importance when choosing the location for a com-pany. As Switzerland was hitherto the domicile of numerousmobile activities of international groups, this developmentrepresents a danger, unless Switzerland can continue to beinternationally competitive, and there is a threat that enter-prises could relocate. As a location for business and tax purposes, Switzerland

must be in a position to stand up to international competitionin the long term. Apart from the low taxation, the positive

aspects of Switzerland are legal certainty, the quality of thehuman resources, a good transport infrastructure, the avail-ability of international schools and the generally high qualityof life. Finally, Switzerland‘s central position in Europe can beemphasised as an attractive feature when deciding where tobase operations. The efforts of the OECD, which aim at taxation where

value is created, will ultimately mean that managements mustask in what location value should be created in future, or mustnecessarily be created in view of the nature and function ofthe business. This means that the decision for or against alocation will usually result in a corresponding transfer of func-tions. And yet Switzerland still appears to be a very competi-tive location for a company. If Switzerland can succeed inattracting (additional) activities which create value, the pres-ent upheaval in international and domestic taxation ofSwitzerland may in the long term be an opportunity.

C T R I I I

8 W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M

Swiss Corporate Tax Reform III:Latest developments

The consultationprocedure for SwissCorporate Tax ReformIII (CTR III), the mostsweeping Swisscorporate tax reform inmore than 50 years,ended January 312015. Deloitte’sRene Zulauf andDiego Weder providean update what is stillto come as part of thereform package, andanalyse what changesshould be made in lightof stakeholderfeedback.

Further legislative processes for CTR IIIAs a next step the Swiss Federal Department of Finance (FDF) will analysethe feedback received in the course of the consultation procedure and willissue a report to the Swiss Government, that is, the Swiss Federal Council,summarising the results from the consultation process by March 25 2015at the earliest. The input from the cantons will be given special considera-tion in the report and the FDF will also take into account international taxdevelopments that have occurred in the meantime.

The Federal Council will decide on the report provided by the FDF andon the drafting of the message to the legislation of CTR III on or afterMarch 25 2015.

The message to the legislation in regard to CTR III will be submittedto the Swiss national parliament on or after June 5 2015. The first oppor-tunity for the Swiss national parliament to discuss the draft legislation inregard to CTR III is during the summer session of the parliament, whichlasts from June 1 until June 19 2015.

Since CTR III is a complex and delicate topic and given that the politi-cal parties on all sides – left and right – may have to make concessions thatmay not be palatable to their voters, there could be some reluctance to dis-cuss the draft legislation to CTR III before the general elections of the Swissparliament in October and the Swiss Federal Council in December 2015.Accordingly, there is some likelihood that the Swiss parliament will only dis-cuss the legislation in regard to CTR III in the winter session of 2015,which lasts from November 30 to December 18 2015, or, even more like-ly, during the following spring session (February 29 to March 18 2016).

Once the CTR III legislation has been approved by both chambers ofthe Swiss parliament, anyone can demand a public vote, that is, a referen-dum on the CTR III legislation, as long as they can gather 50,000 signa-tures from Swiss voters within 100 days. Since 50,000 signatures is not abig hurdle, given that this is a controversial topic and that the CTR III leg-islation will likely be a compromise on certain issues that may leave someparties dissatisfied, a referendum seems most likely at this time.

A national vote (referendum) on CTR III would then likely take placein late 2016 or early 2017. Since the cantons need about two years toimplement the CTR III legislation, which is only a framework law, intotheir cantonal laws, the most probable date to expect CTR III to becomelegally effective is January 1 2019. If it takes longer, then the law mightnot become effective before January 1 2020 and, should there be no ref-erendum, the law could theoretically already come into effect in 2018.

C T R I I I

W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M 9

General acceptance of CTR III, but some disagreementon replacement measuresAll interested parties are in agreement that the current taxprivileged regimes, such as the mixed, holding or principalcompany regime, need to be replaced. The majority of stake-holders also agree that there have to be adequate replacementmeasures to maintain, and possibly improve, the tax compet-itiveness of Switzerland as a preferred location for multina-tionals. There is further agreement that all replacementregimes have to be fully in line with international standardsand to be BEPS-proof, that is, to be aligned with the pro-posed measures under the base erosion and profit shifting(BEPS) initiative of the OECD.

However, the majority of interested parties are of the viewthat the draft legislation should be trimmed down and be lim-ited to the main replacement measures as below:• Patent box;• Notional interest deduction;• Step-up;• Reduction of cantonal income taxes;• Abolition of the capital issuance tax; and • Reduction/adjustment of capital taxes.

Accordingly, most interested parties believe that other lesscentral replacement measures should not be implemented atthis time as part of CTR III. These measures are, in particu-lar: the change in the participation exemption regime to adirect participation exemption and unlimited loss carry-for-wards. Some parties are also against the abolition of the 1%capital issuance tax on equity contributions.

A majority of cantons do not support the introduction ofa notional interest deduction for fear of losing too much taxrevenue.

Finally, the sole proposed revenue-raising measure – theintroduction of a capital gains tax for individuals combined

with a draconian exit tax for individuals – faces broad-basedopposition. The vast majority realise that such a tax would con-stitute Switzerland shooting itself in the foot, because it woulddiscourage the very same international executives and theirmultinationals that Swiss policy attempts to lure into the coun-try by offering expensive corporate tax concessions. In addi-tion, it is very doubtful that a capital gains tax, in the way it isproposed, would be an effective revenue-raising measure at all.

Patent boxThe introduction of a patent box regime (Swiss Licence Box)has broad-based support and is generally not disputed. TheSwiss business community and the centre-right political par-ties support a patent box that is as liberal and as broad asinternationally accepted.

In addition, the Swiss business community requests theintroduction of R&D incentives, which allow for a multiplededuction of research, development and innovation expensesfor income tax purposes, and which are common in manyEuropean countries.

On the other hand, most of the cantons as well as all thecentre-left political parties support the definition of a nar-rower patent box as it is currently included in the draft leg-islation.

It is, however, clear that the Swiss Licence Box will bewithin the boundaries of whatever the OECD decides onthe topic as it is the consensus that a Swiss patent box hasto be fully in alignment with BEPS and the Swiss LicenceBox legislation would be amended, if necessary, to be‘BEPS–proof ’.

Notional interest deduction (NID)While the NID finds the support of a majority of interest-ed parties, particularly from the Swiss business community,

Rene ZulaufPartner, international taxDeloitte AG, Zürich

Tel: +41 58 279 63 [email protected]

Rene has more than 15 years of experience in the field of inter-national tax structuring, financial services tax and M&A. He spe-cialises in cross-border tax planning and has assisted numerousmultinationals, in particular in the establishment of Swiss financeand IP structures, as well as in the structuring of Swiss tradingand principal/headquarter operations.

Diego WederSenior manager, international taxDeloitte LLP, New York

Tel: +1 917 573 [email protected]

Diego Weder is a senior manager leading the Swiss tax desk atthe International Core of Excellence (ICE) in New York. He hassignificant experience in the area of M&A and in the area ofcross-border structuring (including establishing tax efficient IP andfinancing structures) as well as business reorganisations includ-ing large supply chain transformation projects.

C T R I I I

1 0 W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M

its proposed introduction is rejected by a majority of can-tons and the left-wing parties for fear of a loss in tax rev-enues.

All parties agree that the NID has to be structured reason-ably and in such a way that it will not open the door for taxabuse – for example, no NID should be granted on participa-tions or non-business assets.

Further, the Swiss business community considers a NIDrate tied to the 10-year Swiss government bond as too rigidand only useful as a safe haven rate, instead suggesting thatapplication of arm’s-length NID rates, supported by a trans-fer pricing benchmark study, should be allowed.

Step upA step up for tax purposes would allow companies to push upassets and liabilities to fair market values and to capitalisefuture profits (self-created goodwill) which then can be amor-tised tax effectively over 10 years. Such a step up would begranted: i) upon migration of a foreign company toSwitzerland on both a federal and cantonal level with theintent to attract further multinationals to Switzerland; and ii)on the transition of a tax privileged company, such as a mixedcompany, into ordinary taxation on a cantonal level (as the taxprivilege was granted on a cantonal level only) to allow sucha company to essentially maintain its tax privileged rate foranother 10 years.

A step up is supported by the vast majority of interestedparties. However, certain cantons oppose a step up for fear ofloss in tax revenues and prefer a model under which the intro-duction of a step up is optional for cantons.

Items that need to be clarified are the valuation method tobe applied for the step up, as well as the exact mechanics ofthe step up so that it would not only result in a cash tax ben-efit but also in a corresponding tax accounting benefit underIFRS and US GAAP accounting standards. A working groupcomprised of representatives of the Swiss business communi-ty, the Swiss Federal Tax Administration and Big 4 account-ing firms as well as major law firms is now working on theseissues.

Reduction of cantonal income taxes and capital taxesThe majority of interested parties view the broad-basedreduction of corporate tax rates as one of the key replacementmeasures. The consensus is that the general ETR level (com-bined effective federal/cantonal/communal tax rate) on aver-age will go down to approximately 15% to 16%. However,various cantons are already (or plan to be) significantly belowthese rates.

So far the following cantons have announced a reductionof the ETR (combined effective federal/cantonal/communalrates) or can be expected to keep their current low ETR:

The extent to which the other cantons may reduce theirincome tax rates depends in particular on the specific financialsituation each canton is in, the amount of the contribution bythe Swiss Federation as well as on where other cantons set theirtax rate, that is, on the extent of inter-cantonal competition.

The reduction of the capital taxes is supported by a vastmajority of interested parties.

Legislative outlookThe consultation procedure has shown that CTR III, whichentails the replacement of existing tax privileged regimes byother measures, enjoys the broad support of interested partiesin Switzerland.

The main replacement measures – step up, patent boxregime, NID and a general reduction of corporate tax rates –find the support of a majority. In turn, the introduction of acapital gains tax for individuals is rejected by the vast majority.

Peripheral measures, such as change of the participationexemption regime or unlimited loss carry-forwards, seem notto have sufficient support.

Accordingly, the legislation on CTR III that will bebrought before the Swiss parliament and likely will be votedinto law by the parliament can be expected to be broadly inline with the proposed draft legislation, whereby changes nec-essary to align with the OECD BEPS initiative, in particularin regard to the Licence Box, will be incorporated.

While a subsequent public vote is likely, we deem it alsolikely that the CTR III legislation will pass a referendum, sothat CTR III will come into law in 2019 or 2020.

Appenzell AR: Keep low ETR of 12.7%

Fribourg: 13.72%

Geneva: 13.00%

Lucerne: Keep low ETR of approx. 12% (lowest taxedcommunity 11.5%)

Nidwalden: Keep low ETR of 12.7%

Neuchatel: 15.60%

Schwyz: Keep low ETR of approx. 12% (Freienbach/Wollerau)

Vaud: 13.80%

Zug: 12.00%

C T R I I I | N I D

1 2 W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M

CTR III: Recent legislativedevelopments on notionalinterest deduction regimeInternational pressuremeans Switzerlandmust harmonise its taxlaw to ensure the futureattractiveness of thebusiness location.Susanne Schreiber andMaxim Dolder ofKPMG Switzerlandprovide insight on thefuture Swiss fiscallandscape, focusing onfinancing activities andthe proposed notionalinterest deduction tomaintain competitiveconditions for inter-company financingactivities.

S ince 2007, Switzerland’s privileged taxation of holding, mixed andprincipal companies has been under increasing international pres-sure, in particular from the European Union and the OECD. Thus,

the federal and cantonal governments have reacted and are reshapingthe Swiss tax legislation. After publishing its final report on ‘Measuresto strengthen the competitiveness of the Swiss tax system’ in December2013, the Federal Council initiated the consultation phase onSeptember 22 2014 with the publication of a legislative draft forCorporate Tax Reform III (CTR III). The draft mainly focuses on the provision of legal and investment

security and on generally increasing the competitiveness of the tax sys-tem while abolishing five special tax regimes (holding, mixed, domicil-iary, principal company regime, finance branch regime). The centralendeavours of the reform entail finding appropriate replacement meas-ures to maintain Switzerland’s attractiveness and competitiveness in thefiscal landscape for financing, trading, R&D, intellectual property (IP)and holding or headquarter activities. Among other measures the draftsuggests introducing a notional interest deduction (NID) on a compa-ny’s ‘surplus’ equity which might even help attract new financing activ-ities to Switzerland.

Corporate Tax Reform III: Other measuresThe legislative draft contains a variety of measures being considered asreplacements for the current Swiss tax privileges: • A license box to retain and commercialise existing patents, to devel-op new, innovative patented products, and also to encourage compa-nies to relocate related high-value jobs to Switzerland.

• A step-up mechanism aiming to ensure planning certainty both fortaxpayers and the authorities. It shall establish a consistent tax treat-ment of companies relocating to or from abroad, when entering orleaving a license or patent box or another tax exemption or tax priv-ilege.

• Finally, the draft contains further measures, such as the voluntarylowering of cantonal corporate income tax rates, the abolishment ofthe stamp issuance duty on equity, changes to offset loss carry-for-wards for an unlimited period of time, amendments to the participa-tion deduction, introduction of a capital gains taxation for privatelyheld securities, and amendments to the partial taxation of participa-tion income for individuals. If no referendum will be taken, it can be

C T R I I I | N I D

W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M 1 3

assumed that the new legislation will come into force by2019.

Introduction of a notional interest deduction (NID)Swiss entities have an important role for intercompanyfinancing activities, for example as a holding company or aSwiss finance branch for financing foreign group entities.Since such financing activities are often financed with equi-ty and other countries like Belgium or Liechtenstein havealready successfully implemented NID rules, Switzerlandaims to introduce its NID to remain competitive in thisarea.

Improving conditions for financing activities in SwitzerlandFinancing activities and group treasury functions can berelocated to a foreign jurisdiction quite easily. Often, suchactivities are moved first to a foreign jurisdiction to ’test’the new environment. Due to the particularly mobile basisof financing activities the abolishment of Swiss privilegedtax regimes poses the risk of emigrating mobile activitiessuch as financing and trading.Under current Swiss tax law granting a few tax privileges,

although considered being harmful by the EU, holding com-panies are subject to an effective corporate income tax rate of7.83%, Swiss finance branches of only 1%-2%. Also mixedcompanies can benefit from corporate income tax rates forforeign interest income of about 9%-11%. If Switzerland willimplement attractive measures, for example, a NID regime, tocushion the abolishment of Swiss tax privileges, CTR IIImight be able to maintain Switzerland’s appeal and com-petiveness as a financing location. The proposed NID regimemight firstly persuade finance entities or branches carryingout financing activities in Switzerland not to emigrate abroadafter the abolishment of privileged taxation. Secondly, a NIDis an important requirement for Swiss and foreign groups toshift their group financing activities, which might be locatedin other jurisdictions, back to Switzerland or to expandfinancing activities already exercised in Switzerland, for exam-ple cash pooling. The abolishment of the issuance stamp duty– a long discussed topic – would further help to increase theequity financing of Swiss companies and could enable them tobenefit from the NID.

Swiss NID regime according to draft legislationInterest on debt financing is now treated as a tax deductibleexpense. Companies with no debt, but only equity, do notbenefit from such deduction and there is no incentive froma tax perspective to have little debt. The deduction of adeemed interest or notional deduction on equity proposedin the draft of the CTR III legislation would reduce thetaxable basis by notional financing expenses. Since thismeasure is only used for the determination of the tax base,no booking entry in the financial statements is required.

Consequently, NID would simply reduce the tax base in thetax return for corporate income tax purposes. To sum up,the introduction of the NID regime would, at least partly,abolish the discrimination of equity in comparison withdebt financing for income tax purposes.The envisaged NID is limited to the surplus equity.

Hence, a NID would be granted only on the amount ofequity exceeding an appropriate, defined average equity(core capital), giving rise to a requirement that the natureof the equity is long-term and substantial for operatingbusiness activity. The adequacy, to be defined in a circularfrom the tax administration, will be determined based onan individual assessment for each asset class of the respec-tive entity. Therefore, the entire equity would be split intocore and surplus capital. The limitation of NID on surpluscapital is based on the idea that equity and debt should betreated equally for tax purposes and the surplus capitalcould be substituted by debt. In other words, such equityand debt can be seen as alternative sources of funding. Thecore capital, in contrast, is the equity that is necessary forbusiness purposes. It will be assessed asset-by-asset using adefined quota per asset class. The sum of all core capital val-ues per asset class yields the decisive core capital. The corecapital is closely connected to the economic activity and therisk arising therefrom. Following the established Swiss thincapitalisation practice for assessing hidden equity (circular 6

Susanne SchreiberKPMG Switzerland

Tel: +41 58 249 54 [email protected]

Susanne Schreiber is a partner with KPMG’s M&A tax and inter-national corporate tax groups in Zurich. She is a German attor-ney-at-law, German tax adviser and Swiss tax expert. Susannestarted her career more than 13 years ago as a lawyer in theM&A and tax area of an international law firm and joined KPMGin 2006. She focuses on advising clients on the tax aspects of cross-

border transactions, including due diligence, structuring of acqui-sitions or disposals and post-deal integration. Susanne furtheradvises clients in acquisition financing, refinancing structures andtax efficient cross-border financing possibilities. Her client portfo-lio consists of multinational groups and private equity investorsactive in various industries. In addition, Susanne is closelyinvolved in developments of the Swiss corporate tax legislation.

C T R I I I | N I D

1 4 W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M

of Swiss Federal Tax Administration dated June 6 1997),core capital quotas to be confirmed in the circular will besimilarly determined and observe the entity’s assets at bookvalue. This ensures a practical determination of the corecapital as ’reverse’ thin capitalisation rules both for taxpay-ers and tax administration. The following indicative core capital quotas are stated in

the ‘explanatory report to the consultation draft’:

The NID interest rate should not remain constant but becontinuously adjusted to market developments. As current-ly proposed, the notional interest rate would therefore beequal to the 10-year Swiss government bond yield, plus 50basis points, but no less than 2%.The NID regime would be available to both Swiss domi-

ciled companies as well as Swiss branches and permanentestablishments of foreign entities. Due to the NID either a tax loss can arise (that is, NID

exceeds profit before NID) or operative losses before NIDcan be increased. Such losses shall be carried forward intheir entirety.

Please find below a calculation example comparing cur-rent taxation under the Swiss finance branch regime versustaxation under the envisaged NID regime:

Suggested improvementsAs mentioned before the draft legislation states that the appli-cable interest rate for NID calculations should be connectedto the yield on 10-year Swiss government bonds. However,from an international financing perspective this dependence

Core capital quotas for NID calculationAsset category Core capital quota

Cash and cash equivalents 0%

Accounts receivables 40%

Other receivables 40%

Inventory 40%

Other current assets 40%

Domestic and foreign Swiss Francs bonds 35%

Foreign bonds in foreign currency 45%

Listed domestic and foreign shares 100%

Other shares 100%

Investments in subsidiaries 100%

Intercompany loans 15%

Other loans 40%

Factory equipment 75%

Factory properties 55%

Mansions, condominiums, holiday homes andother non business related assets

100%

Building land 55%

Other properties 45%

Intangible assets (without goodwill arisingfrom disclosure of hidden reserves)

55%

Goodwill arising from disclosure of hiddenreserves

100%

Calculation notional interest deduction in mCHF

Assets Core capitalquota

Core capital

Cash 400 0% -

Acc. receivables 200 40% 80

Intercompany loans 1,400 15% 210

Total core capital 290

Taxable equity 2,000

Surplus equity 1,710

Notional interest rate 2%

Notional interest 34.2

Tax calculation in mCHF

Taxation asSwiss finance

branch

TaxationunderCTR III

Interest income 2.7% 37.8 37.8

./. NID Swiss finance branch -31.2

./. NID according to CTR III -34.2

Income before taxes 6.6 3.6

combined tax rate (for mixco) 8.3% -0.5

combined tax rate 12% -0.4

Taxable income 6.0 3.2

Effective tax rate 1.4% 1.1%

Balance sheet in mCHF

Assets Liabilities

Cash 400 Debt -

Acc. receivables 200

Intercompany loans 1,400 Equity 2,000

2,000 2,000

C T R I I I | N I D

W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M 1 5

on government bonds should be treated as a safe havenapproach only. In today’s economic environment, especiallywith regard to cross-border intercompany financing, theunderlying interest rates are regularly significantly highersince exchange and other risks need to be considered whendetermining the corresponding interest rates. Therefore, dif-ferent groups have suggested in their consultation papers toamend the legislative draft to allow the optional usage of riskmargins and risk-appropriate interest rates meeting the arm’s-length principle. As can be seen from the above example, one driver for an

attractive NID regulation lies in the margin between theeffective interest rate (2.7% in the example) and the notionalinterest rate (2%). Whereas the effective tax rate in the Swissfinance branch is rather stable (1.4%), the effective tax ratewould double under the NID in case the interest rate wouldincrease from 2.7% to 3% (from an effective tax rate of 1.1%to 2.2%). Consequently, the wording of the legislative draftshould be amended so that an arm’s-length notional interestrate could be applied for the NID calculation (the taxpayerwould have to substantiate such deviation from the basicnotional interest rate).To mitigate the risk of unintended lower tax revenues in

Switzerland, the Swiss NID regime may need to be restrict-ed with regard to debt pushdown structures: after abolish-ment of the holding company status, groups could berestructured by selling subsidiaries from the holding tooperating (Swiss) subsidiaries against intercompany loans(debt pushdown), since such sale at fair market value (FMV)would increase the holding’s equity for the NID and at thesame time generate deductible interest for the acquiring(Swiss) entity. Further, intercompany loans would benefitfrom a much lower underlying equity percentage for NIDpurposes (15%) than investments (100%). In case of a debtpushdown (sale of investments at FMV to a subsidiary) theparent company could benefit from a higher NID (on inter-company loans) whereas the (Swiss) subsidiary can deductinterest payments tax effectively. In particular if a full partic-ipation exemption would be implemented (see measureabove), interest payments of the Swiss subsidiary will notdilute the participation exemption quota anymore.Therefore, it has been suggested to restrict the NID onintercompany receivables arising from a sale of investmentsand portfolio equity investments – the interest deductionshould not be affected by this, but would be governed bythe existing limitations (thin capitalisation rules, arm’s-length interest rates). Considering the concerns of a fewcantons in the consultation phase, a second restrictionmight be implemented: non-business related assets, forexample excess cash or reserves, securities, and privateassets, among others, should be excluded from the calcula-tion of the core capital to avoid the contribution or collec-tion of non-business related assets for tax (NID) purposes.

Thus, it has been suggested that receivables coming fromsuch investments, portfolio equity investments and non-business related assets should be backed with a core capitalratio of 100%.It remains to be seen which consultation comments will be

actually reflected in the next draft legislation, also dependingon the developments regarding the other measures, for exam-ple the change of the participation deduction regime to a fullexemption.

Accompanying measures for financing activities Under CTR III cantons are given the opportunity to lowerthe annual capital tax rate on equity with respect to participa-tions, intellectual property and intercompany loans. Thechange in legislation will increase the tax competitionbetween cantons in Switzerland and is likely to result in areduction of annual capital taxes for most companies.However, most cantons have not yet announced whether andto what extent they would reduce capital tax rates. Privileged-taxed companies presently benefit from lower capital taxes.Thus, the anticipated reduction of the base for the annualcapital tax will be important since otherwise significantlyhigher capital taxes may arise, in particular for holding orfinancing companies with very high equity levels. Under CTR III, the 1% stamp issuance tax on equity con-

tributions by direct shareholders should be abolished,strengthening Switzerland’s attractiveness as a financing andinvestment location. Even if this contemplated measurewould not be critical for the success of CTR III (since thereare already possibilities for how to structure equity contribu-

Maxim DolderKPMG Switzerland

Tel: +41 58 249 77 [email protected]

Maxim Dolder is a senior consultant with KPMG’s internationalcorporate tax group based in Zurich. He studied law at theUniversity of Lucerne and joined KPMG Switzerland in 2012 afteran internship in 2010. Maxim provides tax planning, tax accounting, tax consulting

and tax compliance services to various international and Swisscorporates in different sectors, including restructuring projects andfinancing as well as M&A. He has also a broad experience inthe real estate tax sector and is active in KPMG’s working groupfor the Swiss Corporate Tax Reform III.

C T R I I I | N I D

1 6 W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M

tions without triggering the stamp issuance duty) it would bea simplification and could attract further equity investmentsfor Swiss companies.

Debt/equity parityThe NID is designed to incentivise equity-financed companiesby granting a notional interest deduction for tax purposes.Most companies, irrespective of fulfilling the current require-ments of a privileged tax regime, could benefit from the NID

– provided they show surplus equity. The NID regime as pro-posed in the legislative draft reduces or eliminates the discrim-ination of equity against debt financing from a tax perspective.Bearing in mind that the legislative draft may still be adjustedto reflect certain limitations, for example in conjunction withdebt pushdown structures or non-business related assets, theNID regulations would still be an attractive solution forfinance companies and an important measure to retain andattract financing activities in Switzerland.

E X C H A N G E O F I N F O R M A T I O N

W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M 1 7

International exchange ofinformation in tax matters

Oliver Jaeggi andStephan Pfenninger, ofTax Partner AG –Taxand, review howSwitzerland is adaptingto the latestinternationaldevelopments in thearea of tax informationexchange, includingspontaneous, onrequest and automatic.

Extension of tax EoI safeguarding political and fundamental rightsas well as market positionIn the past few years, Switzerland has shown considerable developments inthe field of international exchange of information (EoI) in tax matters. Upto now, Switzerland has signed 50 double tax treaties (DTTs) with anexchange of information clause according to article 26 of the OECDModel Convention (of which 41 have come into force) and seven tax infor-mation exchange agreements (TIEAs, of which three have come intoforce). Further DTTs and TIEAs conforming to OECD standards are onthe horizon.Besides the DTTs and TIEAs Switzerland provides tax information, for

example based on the EU-Swiss agreement on the fight against fraud in thearea of indirect taxation, the EU-Swiss Savings Agreement, the withhold-ing tax agreements with the UK and Austria and the Foreign Account TaxCompliance Act (FATCA) with the US.Switzerland’s developments in the area of EoI are even more remark-

able considering that political rights must be respected when imple-menting such international standards. In contrast to other countries(including most EU member states) Switzerland’s political system isbased on direct democracy under which the people have further politi-cal rights, for example to vote in referendums regarding legislation andinternational treaties with respect to exchange of tax information. Onthe other hand, Switzerland seeks to maintain access to financial marketsand avoid a ‘grey’ or ‘black’ listing and thus wishes to comply withinternational standards.

Exchange of information on requestWith respect to the EoI on request, Switzerland follows the OECD prin-ciples and recommendations based on article 26 of the OECD ModelConvention. In particular, Switzerland also grants exchange of informationfor group requests in line with the OECD standard.With regard to the fundamental rights of taxpayers, certain limitations

must be respected in terms of EoI on request. The information requestedmust be foreseeably relevant for the tax assessment of the requesting state,and no request is granted in case of fishing expeditions. Principles such asthe respect of the ordre public, reciprocity and the proportionality princi-ple must be considered. Finally, Switzerland does not grant EoI accordingto domestic Swiss law if such information was obtained through a criminaloffence (for example in case of stolen bank information).

E X C H A N G E O F I N F O R M A T I O N

1 8 W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M

Moreover, procedural guarantees are granted according tothe Swiss Federal Act on International AdministrativeAssistance in Tax Matters (TAAA), such as the right to beheard and the right to fair treatment in administrative pro-ceedings. The competent authority for administrative assis-tance is the Swiss Federal Tax Administration (FTA). Thetaxpayer concerned must be notified by the FTA about themain parts of the information request, may participate in theprocedure and inspect the files before the FTA transmits theinformation requested to the foreign state. The taxpayer isalso entitled to appeal against the final decree issued by theFTA stating the transmission of the information.Exceptionally, the FTA notifies the person concerned after thetransmission of the information only if the requesting taxauthority demonstrates that the purpose of the administrativeassistance would be defeated and the success of its investiga-tions would be thwarted by advance notification. The recent developments and legislation introduced show

that Switzerland has been in a position to extend its interna-tional EoI standards and at the same time keep its principlesas a democratic and constitutional state.

Further important developmentsIn the coming months and years, further important develop-

ments in the area of EoI in tax matters are to be expected inSwitzerland.In January 2015, the Federal Council initiated two consul-

tations in the field of the international EoI in tax matters, thefirst regarding the OECD / Council of Europe Conventionon Mutual Administrative Assistance in Tax Matters (MAC)and the second regarding the automatic exchange of informa-tion (AEoI). The Swiss Federal Council will presumably pres-ent its reports in the summer of 2015 so that the Parliamentmay discuss the draft legislation as of the 2015 autumn session.The Federal Council’s decision to sign the MAC and

implement the global AEoI standard is in line with the strat-egy for a competitive Swiss financial centre, which includesaligning with international standards in the tax area and par-ticularly those concerning transparency and EoI. In addition,on a political level Switzerland’s implementation of the AEoIwill have a positive knock-on effect on other proposals, forexample in terms of international acceptance on the currentCorporate Tax Reform III in Switzerland.Furthermore, in October 2014, the Federal Council

launched the consultation procedure on the Federal Act onthe Unilateral Application of the OECD standard on theexchange of information (GASI). The new law provides theunilateral application of the OECD EoI standard to all DTTs

Swiss framework of international exchange of information in tax matters

EU Savings,tax fraud,

withholding tax A /UK agreements

MACon request,

spontaneous andautomatic

AEOI / FATCAre financialaccount

information

BEPSTax rulings,

Transfer Pricing

DTT / TIEAon request

Exchange ofinformation intax mattersSwitzerland

E X C H A N G E O F I N F O R M A T I O N

W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M 1 9

if the counterparty grants reciprocity. The amendment of eachbilateral DTT would be very time-consuming. Under theGASI, Switzerland plans to extend the exchange of informa-tion in particular with non-European countries, which are notparty to the MAC. However, it is not certain whether the par-liament will pass this legislation. Some political parties criticisesuch unilateral application of exchange of information.

New spontaneous EoI based on the MAC as of 2018The MAC has been signed by 69 states and implemented by43 and is part of the standard for international cooperation intax matters. The MAC provides three forms of informationexchange in tax matters: exchange of information on request,spontaneous exchange of information and automaticexchange of information.Besides the DTTs with OECD standard, the TIEAs and

possibly the new unilateral GASI legislation, the MAC will bethe legal basis for EoI on request. In addition, the MAC will introduce the spontaneous

exchange of information as a new form for Switzerland.Spontaneous EoI is the provision of information that is foresee-ably tax relevant to another state and which has not been pre-viously requested by such state. The wording of article 7 of theMAC provides spontaneous EoI under the following circum-stances:• Grounds for suspecting that there may be a significant lossof tax in another country;

• A person liable to tax obtains a reduction in, or an exemp-tion from, tax in one country which could give rise to anincrease in tax liability in another country;

• Business dealings between a person liable to tax in a countryand a person liable to tax in another country are conductedthrough one or more countries in such a way that a savingin tax may result in one of the other countries or in both;

• A country has grounds for suspecting that a tax saving mayresult from artificial transfers of profits within groups ofenterprises; and

• Information forwarded to a country by another countryhas enabled information to be obtained which may be rel-evant in assessing liability to tax in another country.The Federal Council will settle the conditions for the spon-

taneous exchange of information in an ordinance in accor-dance with the international standard and practice in otherstates. For drafting the corresponding ordinance, the FederalCouncil has set up a task group. The 2006 OECD manual oninformation exchange (module 2 on spontaneous EoI) pro-vides technical and practical guidance in this regard and men-tions scenarios where a spontaneous EoI may be useful.Finally, the MAC will also be the basis for the introduction

of the AEoI. As expressly stated in the preamble to the MAC, funda-

mental principles entitling every person with a proper legalprocedure shall be recognised and the states should endeav-

our to protect the legitimate interests of taxpayers. As men-tioned above, the Swiss legislation TAAA grants proceduralguarantees such as, for example, the previous notification ofthe person concerned, the right to participate and to inspectfiles and the possibility to appeal against final decrees of theFTA. These principles will be applicable in the exchange ofinformation on request as well as in the spontaneousexchange of information (but not in the case of the automat-ic exchange of information).Furthermore, the MAC provides rules to protect the con-

fidentially of the information exchanged. If personal data isprovided, the state receiving it shall treat it in compliance notonly with its own domestic law, but also with the safeguardsthat may be required to ensure data protection under thedomestic law of the supplying state. In this regard, theFederal Council will be entitled to conclude respective agree-ments. The minimal standard shall correspond to the FederalAct on Data Protection. Under the conditions of the MAC states may make reser-

vations regarding the taxes covered and the type of assistance.The Swiss Federal Council proposes excluding social securitycontributions and taxes other than income tax and net wealthtax (for example, inheritance and gift tax, taxes on immovableproperty, VAT). In addition, certain administrative assistanceshall be excluded, for example with respect to the executionand enforcement of tax claims of a foreign state in Switzerlandand for the service of documents. Only direct postal deliveryof documents will be possible between the foreign state andSwitzerland. Finally, Switzerland should not allow foreignauthorities to be present at tax audits in Switzerland. Should the MAC enter into force as per January 1 2017 or

later in 2017, the exchange of information under the MAC willbe possible for tax periods beginning on January 1 2018. In thecase of tax offences committed deliberately and subject to crim-inal sanctions, retroactive application of the MAC should berestricted to three years before the MAC will enter into force(that is, limited to tax periods beginning on January 1 2014).

AEoI as of 2018Switzerland signed the Multilateral Competent AuthorityAgreement on the Automatic Exchange of Financial AccountInformation (MCAA) on November 19 2014. The MCAA isbased on the MAC and aims to achieve the uniform implemen-tation of the OECD’s AEoI standard (common standard onreporting and due diligence for financial account information).The automatic exchange of information involves the systemat-ic and periodic transmission of financial account information. Itallows for a level playing field in the competition between finan-cial centres. The exchanged information should be used solelyfor the agreed purpose (principle of speciality), the informationshould be reciprocal and data protection must be ensured. Thescope of the AEoI in terms of the reportable accounts is verywide and also includes trusts and foundations.

E X C H A N G E O F I N F O R M A T I O N

2 0 W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M

The countries with which Switzerland should establish theAEoI will be determined separately at a later stage. The pri-mary focus will be on the EU member states, the US andother selected countries.Should the legislation be approved by the Parliament and

in the public vote in case of a referendum, the first automaticexchange of information between Switzerland and a foreigncountry will take place from 2018.

Further EoI in the frame of the BEPS ProjectEoI is also an important measure in the frame of the OECD’sproject on base erosion and profit shifting (BEPS).Switzerland is represented in the different working parties ofthe BEPS Project and will put into practice the measures rec-ommended according to the BEPS Action Plan.In the BEPS report to action 5 published in September

2014 regarding the countering of harmful tax practices, theOECD intends to introduce a compulsory spontaneous EoI

on tax rulings relating to preferential tax regimes. Theexchange of rulings shall take place with any affected country(including the source country, the country of the direct par-ent company and of the ultimate parent company and in caseof transactions the country in which the other party is resi-dent). The legal framework will be the bilateral DTTs, TIEAsor the MAC. The Forum on Harmful Tax Practices (FHTP)intends to issue a progress report on the status of the imple-mentation in 2015. Furthermore, in February 2015, the OECD and G20

agreed to increase transparency through transfer pricing doc-umentation standards – including the use of a country-by-country reporting (CbCR). The new guidelines to action 13of the BEPS Project require multinationals generatingturnover above €750 million ($825 million) in their countriesof residence to provide tax administrations with CbCR (onrevenues, taxes accrued and paid). The exchange of country-by-country reports will be made through automatic exchange

Stephan PfenningerTax Partner AG – Taxand

ZurichTel: +41 44 215 [email protected]

Stephan Pfenninger, attorney at law, has more than 20 years’experience of local and international tax. Stephan started hiscareer as a corporate lawyer in Zurich. Later he moved to a Big4 firm, working in the areas of financial and tax law. Stephanhas been a partner of Tax Partner AG since 1998.

Besides national and international corporate tax law,Stephan’s activities are mainly focused on real estate tax man-dates. He is a tax adviser for listed and non-listed Swiss and for-eign institutional real estate investors (for example, investmentcompanies, pension funds, insurance companies, banks) as wellas for individual investors in the area of tax efficient structuringof real estate transactions, current tax optimisation of real estateportfolios and the creation of tax efficient real estate investmentproducts, among others. He is a speaker and lecturer at signifi-cant tax seminars, and has published various articles on interna-tional and national real estate tax.

Tax Partner is one of the leading tax firms in Switzerland. Nowwith 34 professionals, the firm has been advising multinationaland national corporate clients as well as individuals. Tax Partnerco-founded Taxand in 2005 – the first global network of morethan 2,000 tax advisers and more than 400 partners from inde-pendent member firms in nearly 50 countries.

Oliver JaeggiTax Partner AG – Taxand

Tel: +41 44 215 77 [email protected]

Oliver Jäggi is an attorney and a certified Swiss tax expert. Hiscareer started in the corporate tax department of KPMG in Zurichin 2000, where he worked as a tax manager on national andinternational projects until 2007. Following this, he joined TaxPartner and is now a senior adviser.

Oliver has more than 13 years’ experience of local and inter-national tax. He is mainly involved in tax planning, restructuringand transactions of national and international corporations andentrepreneurs. He also works on real estate planning, tax litiga-tions and for private clients. Oliver has published various articlesin the field of tax and speaks fluent German, French, English andSpanish.

Tax Partner is one of the leading tax firms in Switzerland. Nowwith 34 professionals, the firm has been advising multinationaland national corporate clients as well as individuals. Tax Partnerco-founded Taxand in 2005 – the first global network of morethan 2,000 tax advisers and more than 400 partners from inde-pendent member firms in nearly 50 countries.

E X C H A N G E O F I N F O R M A T I O N

2 2 W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M

of information based on the bilateral DTTs, TIEAs or theMAC.

Future challengesThe international exchange of information in tax matters is,and will continue to be, based on a complex legal frameworkof bilateral and multilateral agreements, domestic legisla-tion, international standards and court decisions. Due to thebroad exchange of information and in particular to the

AEoI, taxpayers and countries will be much more transpar-ent. Millions of tax notifications will be exchanged betweencountries. For the countries involved, includingSwitzerland, the challenges of this important flow of infor-mation will be the efficient set-up and correct processing ofthis information as well as the granting of data protectionand fundamental rights to the taxpayers. In addition, byfully complying with these standards, Switzerland will saveits strong position in the financial markets.

F I N A N C I A L S E R V I C E S | V A T

W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M 2 3

Swiss VAT treatment of financialservices: A never-ending story

Roland Reding andMarcel Mangold ofKPMG Switzerlandanalyse a recentdecision of the FederalAdministrative Courtregarding the SwissVAT treatment ofintermediation services(particularly in respectof securitiestransactions) in thefinancial servicesindustry and look atthe impact it may haveon Swiss financialinstitutions.

O n October 23 2014, the Federal Administrative Court (the Court)issued a significant decision, ref. A-4913/2013 (Decision), regard-ing the Swiss VAT treatment of intermediation services by Swiss

financial institutions.

The Decision The Court had to decide whether services rendered by a Swiss bank qual-ified as Swiss VAT-exempt intermediation services in respect of transactionsin securities or whether the bank provided client introduction services sub-ject to Swiss VAT. The Court finally concluded that the requirements fora VAT-exempt turnover (intermediation in respect of securities) were notfulfilled, as the bank did not explicitly act in the name and on the accountof its clients. In the view of the Court, the bank provided client introduc-tion services which were independent of the concrete securities transac-tions. Hence, the commission fee received by the bank, a so-called finder’sfee, did not qualify for the VAT exemption. The Swiss tax authority haslodged an appeal against the Decision with the Federal Supreme Court. The Decision does not provide any details regarding the specific activi-

ties performed by the bank. The Decision nevertheless contains someremarkable statements that will have far-reaching consequences for theentire financial industry if the Decision is confirmed by the FederalSupreme Court. In particular, the Court stated that the Swiss VAT treat-ment of intermediation services as applied by the Swiss tax authority anddescribed in its practice statement on VAT questions for the finance indus-try, Brochure 14, is contrary to the clear wording of the law and thereforenot permissible. Based on the unambiguous statement of the Court, aSwiss financial institution only provides VAT-exempt intermediation serv-ices if it acts in the name and on the account of its clients. If this condition is not fulfilled, the commission received by the Swiss

financial institution is not VAT-exempt but subject to VAT or (if the serv-ice recipient is a non-Swiss counterparty) zero-rated. The Court furtherexpressly stated that the VAT concept of “acting as intermediary” in thefinancial services industry is different in Switzerland compared with therules applied in the EU and the jurisdiction of the Court of Justice of theEuropean Union (CJEU) in this context is not relevant for the Swiss judges.

Legal provisions and the practice of the Swiss tax authorityAccording to the current Swiss VAT law valid as from January 1 2010, “theturnovers (spot and forward transactions), including intermediation, of

F I N A N C I A L S E R V I C E S | V A T

2 4 W W W . I N T E R N A T I O N A L T A X R E V I E W . C O M

securities, rights and derivatives and of interests in companiesand other forms of associations” are exempt from Swiss VAT(i.e. exempt-without-credit). This legal provision is identicalto the old VAT law applicable until the end of 2009. As nei-ther the old nor the new law defines what is meant by inter-mediation of securities, the Swiss tax authority published itsown interpretation of the concept of “acting as intermediary”in its Brochure 14. Based on the old version of Brochure 14relating to the old VAT law, the term “intermediation” wasrestricted to transactions where the intermediary acts in thename and on the account of another party, i.e. the intermedi-ary needed to have a direct proxy. This interpretation was alsoconfirmed by the Federal Supreme Court on various occa-sions. However, the tax authority’s rules were not appliedconsistently in practice. Although the text of the law remained unchanged, the tax

authority changed its practice regarding “acting as intermedi-ary” under the new law. According to the amended Brochure14, valid from January 1 2010, the tax authority no longerrestricts the term “intermediation” to transactions where theintermediary expressly acts in the name and on account ofanother party. The tax authority now understands “interme-diation” as the activity of an intermediary whose role is toprocure the completion of, and negotiate the terms of, atransaction on behalf of one of the parties. As such, interme-diation is a service rendered to, and remunerated by, a con-tractual party, as a distinct act of mediation. It may consist,

among other things, in pointing out suitable opportunitiesfor the conclusion of such a contract, contacting anotherparty or negotiating, in the name and on behalf of a client, thedetails of a contract. The intermediary does all that is neces-sary for two parties to enter into a contract, without himselfhaving any interests in the contract. In drafting the newBrochure 14, the tax authority was inspired by – or has in factcopied – the definition of the judicature of the CJEU in itsprominent decisions in CSC Financial Services (C-235/00)and Volker Ludwig (C-453/05). In its Decision, the Court ruled that the Swiss tax author-

ity’s change of practice is not acceptable. As the legal provi-sions under the old and the new VAT law remainedunchanged in this respect, there was no legal basis for the taxauthority to change its interpretation of the law. Indeed, theCourt confirmed that the previous practice as per the oldBrochure 14 is still applicable, meaning that the commissionreceived by the intermediary is only exempted from SwissVAT if it formally acts in the name and on account of anoth-er party.

Who is affected by the Decision?The Decision could have a widespread impact on Swiss finan-cial institutions. However, based on explicit legal provisionsand longstanding practice, the following two types of incomewhich also refer to intermediary services within the financialservices industry are not affected by the Decision:

Fund distributionThere are clear and separate legal provisions and an estab-lished practice with regard to the fund business. Commission(including recurring trailer fees) for the distribution of unitsin collective investment funds is VAT-exempt provided that:(1) the fund is a Swiss fund subject to regulatory provision ora non-Swiss fund which is subject to distribution authorisa-tion in Switzerland, particularly retail funds for non-qualifiedinvestors; (2) the parties have the necessary regulatory autho-risation to distribute funds; and (3) a proper documentation(for example, distribution agreement) exists.

Finder’s fees / retrocessionsFinder’s fees are subject to VAT according to the establishedSwiss VAT practice. The typical case is the following: a cliententers into a discretionary asset management agreement withan external asset manager. A bank acts as the client’s custodi-an and broker. The asset manager instructs the bank to buy orsell securities (for example bonds or equities) on behalf of theclient. The bank charges brokerage fees to the client’s custodyaccount. Further, the bank pays a commission to the assetmanager (a retrocession) of, for example, 50% of the broker-age fee and the client has agreed that the asset manager neednot pass on the retrocession to the client. A Swiss-domiciledasset manager must declare and pay 8% Swiss VAT on the