Welcome to the 9th CEE Summit - clearstream.com · The Scale of CEE Markets –Market Cap to GDP 0...

63

Welcome to the 9 th CEE Summit 18 and 19 April 2013 Prague, Czech Republic 1

Transcript of Welcome to the 9th CEE Summit - clearstream.com · The Scale of CEE Markets –Market Cap to GDP 0...

Welcome to the

9th CEE Summit18 and 19 April 2013Prague Czech Republic

1

2

3

Why CEE

Tomasz GrajewskiGlobal Head GSSUnicredit

5

Agenda

nThe scale of the CEE region

nThe attractions of the CEE region

nThe special features of the CEE region

n The custodian perspective of the CEE

nA vision for the future

6

The Scale of the CEE Regionndash GDP comparison

0100200300400

GDP (EUR b)

010203040

GDP per capita (EUR k)

Source UniCredit CEE Quarterly

The potential for growth is material these are largely emerging and frontier markets

7

0500

10001500200025003000

GDP (EUR b)

010203040

GDP per capita (EUR k)

Source UniCredit CEE Quarterly and UniCredit Economics Research

The Scale of the CEE Region ndash GDP in further context

The gap in GDP per capita is a good indicator of the potential of even the regional ldquotigersrdquo

8

The Scale of the CEE Region ndash Stock Market Size

0100200300400500600700800

Stock market size (EUR billion) versus market capitalization of major global corporates

Source WFSE and FT

9

The Scale of CEE Markets ndash Market Cap to GDP

020406080

100120140160180

Domestic market cap as of GDP

Source WFSE and Unicredit Economics Research

10

The Scale of the CEE Markets

020406080

100120140160

Cap (EUR billions)600

11

The Scale of CEE Markets (Feb turnover EUR)

0

20

40

60

80

100

120

140

160Smaller markets - EUR millions

600

05

101520

Larger markets- EUR billions

12

The Attractions of the CEE Markets

nBest regional economic growth rates

nExporting economies

nCEE adhesion and impact

nIPOrsquos in the future

nGrowing local investor bases

nInfrastructure evolutionary trends

But Very Dependenton EU economies

13

The Attractions of the CEE Region- Economic Growth Ratesn Poor 2012 performance but GDP growth forecast generally ahead of EU average

-3-2-1012345

Austria Czech Hungary Poland Russia Croatia

2011 2012 2013

Source UniCredit CEE Quarterly and Unicredit Economic Research

14

The Attractions of the CEE Region ndash Exporting Economiesn EU is the target of much of exports region still tied

to EU economic performancen Exports are on average 65 of GDP in CEE or CEE

aspirant emerging and frontier markets countries

020406080

100ExportsGDP

Source UniCredit CEE Quarterly

15

The Attractions of the CEE Region ndash CEE adhesion and its impactn EU is a market of 500 mio people ndash 10 CEE countries who

are EU membersaspirants have a population of 110 mio

n EU development and other funds are key drivers for growth

n Euro participation is an emerging issue with currently AT SK and SI being in countries but others plan to join ldquoin the futurerdquo

n And in the securities world harmonisation infrastructure convergence and common regulation are prevailing trends

n The MSI all country index includes AT (developed) RU PL CZ and HU (emerging) from the CEE with most others still classified as ldquofrontierrdquo

16

And the T2S development is attracting both Euro and non Euro markets and is a major enterprise

Austria

Slovakia

Slovenia

Hungary

Romania

Rebuilding platform project plan being implemented details shared with users currently scheduled for phase 3 release

T2S on top of infrastructure total redesign of IT architecture will retain many local unique features currently scheduled for phase 2 release

T2S on top of current architecture upgraded two years ago middleware decision to be made 2Q2013 currently scheduled for phase 3 release

T2S on top of current infrastructure RFP out to allow tender for major market IT re-engineering T2S to cover EUR settlement only (not Florint) currently scheduled for phase 3 release

T2S on top of current infrastructure some enhancements to be adopted T2S to cover EUR settlement only (not Leu) currently scheduled for phase 1 release

17

The Attractions of the CEE Region - IPOrsquos nThe region is moving from state managed to market economies

nWe expect a greater number of new IPOs ndash on averagemarkets could increase market cap by 100 to reach world ldquonormsrdquo

n Some of the IPOrsquos could be substantial (On the WSE in 2011 there were 16 foreign issuers listed of which 12 on the main list)

n Align this with above average GDP growth and a more friendly global environment and market capitalisations could well rise dramatically

nThe region is still complex change is country centric and local knowledge and involvement is key to managing the process

18

The Attractions of the CEE Region ndash Growing Local Investor Base

n A recent CEESEG study showed that just 138 of the domestic stocks held by institutional investors in their four markets are held by domestic institutions the balance by foreign investors with the US (336) UK (188) and France (53) being the major investors

0

10

20

30

40

USA UK Austria France Germany Other

Foreign Investment in CEE

19

The Attraction of the CEE Region - Infrastructure is changing

nThe dominant players in the region are CEESEG and the Warsaw Stock Exchange

0

20

40

60

80

Securities Euro (b) MiFID liquid Int MembersCEESEG WSE

Source CEESEG

20

But The market Infrastructure Is Bound To Change

n MTFrsquos are syphoning off some of the more liquid stock activity to the detriment of the traditional Exchangesn Many regional markets are small many markets have low liquidityn A regional grouping makes sense and the major impediment will be political

Oslash Can it be structured around a CEE regional grouping an expanded CEESEG a hub from Moscow or the sometimes debated PolishAustrian alliance

Oslash Will it be driven by an acquirer from Western Europe such as Deutsche Boerse or Euronext

Oslash Is there enough value to attract a new entrant a buyer from another region

21

The Special Features of the Region

nPolitical and economic factors drive markets (eg electoralchange public policy on savings)

nCost advantage over much of EU exporters (dependent on EU economic performance expanding markets outside EU)

n Markets are adopting EU harmonization (better governance improved transparency but still ldquoexcitingrdquo developing markets)

BUTn Substantial diversity remains across markets ( the region will move

forward at different speeds and will take a decade + long process)

ANDn Unicredit GSS presence countries are 14 states of the CEE

accounting for around 450 of the Deloitte CEE top 500 companies

22

The Custodian Perspective In A Changing Environment

n Infrastructure consolidation likely to be Exchange led with CCPs and CSDs as slow followersn EU legislation being adopted in EU markets and becoming template for best practise elsewheren Harmonisation (eg T+2) with an eye to Western Europen Risk and cost dynamics militate for the regional custody providers with a strong regional asset gathering rolen Although we can think of a ldquosingle marketrdquo for the next generation local presence key in markets with many unique characteristics

23

My Vision For the Future Decade- Exciting Space with ChallengesMacroeconomic perspectivenFaster economic growth

than world or European average

Capital markets perspectiven Stock Exchanges increase

in scale but also align to major Groupings within or outside region nRapid development of

domestic institutional markets

Regional Investments perspectiven Russia Poland Czech Republic

and possibly Hungary will move from emerging to developed in MSI

Infrastructure perspectivenCCP development and

interoperability with major groupings nCSDs use common infrastructures

but retain local presences (notary functions) with CEESEG Warsaw and Moscow retaining independencenAlignment of infrastructures and

adoption of EU laws across much of the region

Why CEE

Tomasz Grajewski

Global Head GSSUnicredit

24

25

The impact of EU legislation on the post-trading industryRafael PlataHead of Derivatives and Post-tradingFederation of European Securities Exchanges (FESE)9th CEE Summit Prague ndash 19th April 2013

FESE represents in total 46 Securities Exchanges (in equities bonds and derivatives) through 21 Full Members from all EU Member States and Iceland Norway and Switzerland as well as 4 Observer Members from European emerging markets

46 Securities Exchanges through 20 Full Members from 30 countries

4 Observer Members from 4 countries

The Federation of European Securities Exchanges (FESE)

Why a trading person in a post-trading panel

TRADING

POST-TRADING

QuestionHow many EU legislations regulated CCPs and CSDs prior to EMIRCSD Legislation

1 None

2 2

3 3

4 5

G20 implementation in the EU for OTC derivatives

OTC Derivatives

Clearing obligation

Trading obligation

Capital RequirementsContracts subject to CCP clearing obligation

Contracts subject to trading obligation RMsMTFsOTFs

G20

CRD IV

EMIR

MiFID

bull Average frequency of tradesbull Average size of tradesbull Number and type of active market participants

ESMA OK based on

bull Standardisation of the contractbull Reduction of systemic risk in the financial system (inc lack of transparency on positions)bull Liquidity of contracts

bull Availability of pricing information

ESMA OK based on

EMIR also includes a requirement for derivatives to be reported to Trade Repositories

bull CCP clearing obligationbull Liquidity based on

31

Arrangements for naked CDS trading

Scope

MiFID

EMIR

CRD IV

Post-trading

TradingMarketAbuse

Eq FI Ds

Ds OTCDsEqEq FI DsScope

- Sounder CCPs

- Trade repositories

Gral review + G20 commitments on derivatives

Short SellingCDS

Eq FI Ds

+ Use of CCPs Extension of MAD regime to OTCDerivatives

CSD Reg

Eq FI

- Sounder CSDs

- Settlement Cycles

Eq = Equity FI = Fixed Income Ds = Derivatives

The EU regulatory landscape

EMIR

Equity Fixed Income

Derivatives

`Trading

Clearing

Trade repositories

Trading

Clearing

Settlement

Trading

Clearing

Derivatives Equity Fixed Income

Settlement

EMIR - Provisions

1- CCP clearing obligation

2- CCPs rules and relationship with members

3- Reporting to trade repositories obligation

Question

What percentage of the global OTC interest rate swaps market was cleared at the end of 2009

1 35

2 52

3 70

4 98

Main impacts of EMIR

Safety

Efficiency

Transparency

MarginsCollateral

Paper-work

New infrastructures

Trade Repositories for EU derivatives

DTCC

CDS

DTCC

IRS

DTCC

London

CDS

Copy of the US original

Luxembourg

REGIST-TR

ALL

FXCommodity

DTCC

Equity

London

Access to data by EU supervisors

EUU

S

DTCC

Others

DTCC

CSD Legislation ndash In progress

Market discipline

Settlement cycles

Electronic records

CSD rules

Passport

User choice

Access

More than settlement

Settlement

Safety Efficiency

Safety Efficiency Transparency

QuestionThe need of collateral will increase after the implementation of EU Legislation What are the estimated annual costs of the internal fragmentation of the global collateral management market

1 17 million EUR

2 83 million EUR

3 1 billion EUR

4 4 billion EUR

So what is there for the future

So what is there for the futureReview

EMIR

CSD Legislation

New issues

Communication protocols

CCP services to buy-side

Intraday settlement operating hoursdeadlines

Pre-settlement harmonisation

Registration procedures

Withholding tax procedures

Transaction tax procedures

Exchange Traded Funds (ETFs)

Cross border shareholder transparency

Děkuji

ContactRafael PlataHead of Derivatives and Post-tradingFederation of European Securities Exchanges (FESE)platafeseeu+3225510189

42

Panel discussion

Latest Trends in Eastern Funds Distribution

43

Fidelity Worldwide Investment

April 2013

Adam LessingHead of Austria and Eastern Europe

sect Founded in 1969 serving institutional clients for over 40 years

sect Investment Management is our only business

sect Fundamental research is the foundation of our investments

sect The company is privately held majority owned by the managers who run it and our chairman Ned Johnson and his family have been the single largest shareholders since inception

sectWe have built our business slowly and steadily through organic growth so our culture has remained strong and our business franchise stable

Fidelity Worldwide Investment is a Private CompanyIts only Business is Asset Management

Our interests and our clientsrsquo interests are well aligned

Source Fidelity Worldwide Investment (FIL Limited)

45

Singapore

Sydney

Hong Kong Taipei

Shanghai Tokyo

Seoul

Mumbai

Delhi

Dalian

Fidelity Worldwide InvestmentGlobal research resources

46

71 Portfolio Managers68 Equity Research37 Fixed Income Research11 Other Research

Pan Europe and Americas

10 Portfolio Managers25 Equity Research

Japan

24 Portfolio Managers42 Equity Research11 Fixed Income Research

Asia Pacific (ex Japan)

Emerging Markets

375 Total Investment Professionals

105 Portfolio Managers

194 Research Professionals

26 Traders (ex Fixed Income)

28 Divisional Management

22 Equity Research Support

Global

Europe

United Kingdom

United States

Sector and Country

LondonFrankfurt

MilanParis

Sao Paulo

Research Professional numbers include fixed income analysts and equity (including technical and shorting) analysts Fixed Income Research includes quantitative and credit analysts and traders Other Research includes real estate multi-manager quantitative and derivatives expertsPortfolio Managers include equity fixed income real estate and multi-manager teamsSource FIL Limited 31 December 2012 Data is unaudited

Fidelity Worldwide InvestmentEastern Europe Presence

sect Warsaw

sect Vienna

sect Prague

sect Budapest

sect Bratislava

sect Sales and marketing office Vienna

sect Sales office Warsaw

sect Funds registered in Czech Republic Slovak Republic and Hungary

sect Fund Platform FFB in Germany

sect Fund Platform FFB opening in Austria (Q3 2013)

sect Kronberg

sect

Source Fidelity Worldwide Investment (FIL Limited) as at 3132013

Fidelity Offers a Wide Range of Investment Funds Across all Asset Classes

8 Global EqFds 18 Eur EqFds 4 America Fds 2 Asian Bd Fds 6 Target Fds

2 Property Fds 2 EM Bd Fds 11 Bal Fds

3 euro Bd Fds

4 High Yld Fds

3 Japan Fds

19 Asia Fds

6 Intlsquol Fds

7 Cash Funds

Equities Equities EquitiesEquities

Fixed Income and Cash

FF Global RealAssets FF Euro Blue

Chip

FF ChinaConsumer

FF US High Yield

Source FIL 3062012

FF EuropeanGrowth

Balanced

Local Web and Marketing Support are Key

Source Fidelity Worldwide Investment (FIL Limited)

Important Information

This material is intended for investment professionals and must not be relied upon by private investors This communication is not directed at and must not beacted upon by persons inside the United States and is otherwise only directed at persons residing in jurisdictions where the relevant funds are authorised fordistribution or where no such authorisation is required These figures reflect the resources of FIL Limited and its subsidiaries and FMR LLC and its subsidiariesFIL Limited and FMR LLC are separate companies with some shareholders in common Source FIL and FMR LLC April 2013 Data is unaudited Researchprofessionals include associates analysts country and sector managers who retain research responsibility and technical amp quantitative analysts who are part ofthe research groups Assets and resources as of 31122012 are those of FIL Limited Data is unaudited Issued by FIL (Luxembourg) SA 2a rue AlbertBorschette 1021 Luxembourg Luxembourg Fidelity Worldwide Investment only gives information on its products and does not provide investment advice basedon individual circumstances Any service security investment fund or product outlined may not be available to or suitable for you and may not be available in yourjurisdiction It is your responsibility to ensure that any service security investment fund or product outlined is available in your jurisdiction before any approach ismade regarding that service security investment fund or product The document may not be reproduced or circulated without prior permission and must not bepassed to private investors All views expressed are those of Fidelity Worldwide Investment Fidelity Fidelity Worldwide Investment and the Fidelity WorldwideInvestment logo and currency F symbol are trademarks of FIL Limited FidelityFidelity International means FIL Limited (FIL) and its subsidiary companiesInvestments should be made only on the basis of the current Key Investor Information Document (KIID) current prospectus the annual report and ndash if publishedlater ndash the last semi-annual report They are available along with the current annual and semi-annual reports free of charge from our distributors from ourEuropean Service Centre in Luxembourg FIL (Luxembourg) SA 2a rue Borschette 1021 Luxembourg your financial advisor or for Slovakia from ourrepresentative UniCredit Bank Slovakia as with its registered office at Sancova 1a 813 33 Bratislava for Czech Republic from our representative UnicreditBank Czech Republic as Zeletavska 15251 140 92 Prag 4 ndash Michle or for Hungary from our distributor Raiffeisen Bank Zrt Akademia u 6 1054 BudapestExcept for the KIID these documents are in English Documents include the fund rules and further information regarding the incorporation of the UCITs Furtherinformation regarding the nature of the risk for this fund would be available at the following web pages For Czech Republic wwwfidelitycz for Hungarywwwfidelitycohu for Slovakia wwwfidelitysk MKAT1749

Investičniacute společnost Českeacute spořitelny as

Member of Erste Asset Management GmbH

ISČS Company Presentation26042013 - Page 52

EAM - leading asset manager in CEE region

sect Core competence mutual fundrsquos and individual mandates asset management sect EAMrsquos oldest subsidiary ERSTE-SPARINVEST KAG was founded in Austria in

1965sect Erste Asset Management Group (EAM) has EUR 47 bn AuMsect EAM has 290 employees thereof 85

investment professionalssect Number 1 in Austria Romaniasect Number 2 in Czech Republic

Croatia Serbiasect Number 3 in Hungary Slovakiasect ERSTE-SPARINVEST KAG is GIPS

certified since 2003sect Strong partner Erste Bank (market leader

in AUT CZ RO SK serves 17 million clients employs around 50000 people and operates 3100 branches in 8 countries)

ltErste Asset Management GmbHgt26042013 - page 53

Organizational chart of Erste Asset Management

Erste Asset Management GmbH is owned 100 by Erste Group Bank AG

portfolio unit

International provider with local anchoring

From a personal point of view would you invest into mutual funds

1 Yes I have already invested into mutual funds

2 No but why not in the future

3 Yes but I wonrsquot do it again

4 No and Irsquoll never invest in those products

55

Should you invest into mutual funds what would you primarily look at

1 The brand reputation of the Investment Manager

2 The fundrsquos strategy Theme

3 The risks related to investment policy

4 The costs

56

Investors and products in the area of mutual funds

Martin Rezac CFAErste Asset Management

Funds GDP

Source IMF EFAMA local associations of fund management companies

Funds Capita (in EUR)

Source IMF EFAMA local associations of fund management companies

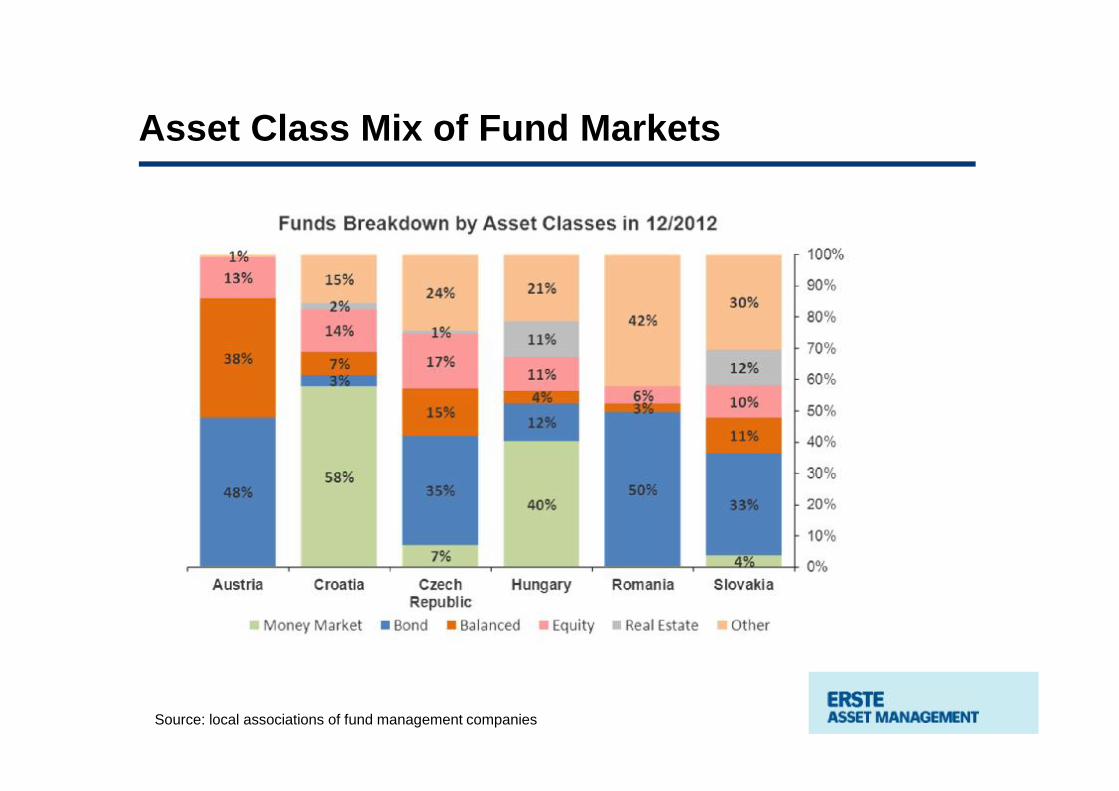

Asset Class Mix of Fund Markets

Source local associations of fund management companies

Banking Development in Transformation Economies

Source Erste Group

62

THANK YOU

63

2

3

Why CEE

Tomasz GrajewskiGlobal Head GSSUnicredit

5

Agenda

nThe scale of the CEE region

nThe attractions of the CEE region

nThe special features of the CEE region

n The custodian perspective of the CEE

nA vision for the future

6

The Scale of the CEE Regionndash GDP comparison

0100200300400

GDP (EUR b)

010203040

GDP per capita (EUR k)

Source UniCredit CEE Quarterly

The potential for growth is material these are largely emerging and frontier markets

7

0500

10001500200025003000

GDP (EUR b)

010203040

GDP per capita (EUR k)

Source UniCredit CEE Quarterly and UniCredit Economics Research

The Scale of the CEE Region ndash GDP in further context

The gap in GDP per capita is a good indicator of the potential of even the regional ldquotigersrdquo

8

The Scale of the CEE Region ndash Stock Market Size

0100200300400500600700800

Stock market size (EUR billion) versus market capitalization of major global corporates

Source WFSE and FT

9

The Scale of CEE Markets ndash Market Cap to GDP

020406080

100120140160180

Domestic market cap as of GDP

Source WFSE and Unicredit Economics Research

10

The Scale of the CEE Markets

020406080

100120140160

Cap (EUR billions)600

11

The Scale of CEE Markets (Feb turnover EUR)

0

20

40

60

80

100

120

140

160Smaller markets - EUR millions

600

05

101520

Larger markets- EUR billions

12

The Attractions of the CEE Markets

nBest regional economic growth rates

nExporting economies

nCEE adhesion and impact

nIPOrsquos in the future

nGrowing local investor bases

nInfrastructure evolutionary trends

But Very Dependenton EU economies

13

The Attractions of the CEE Region- Economic Growth Ratesn Poor 2012 performance but GDP growth forecast generally ahead of EU average

-3-2-1012345

Austria Czech Hungary Poland Russia Croatia

2011 2012 2013

Source UniCredit CEE Quarterly and Unicredit Economic Research

14

The Attractions of the CEE Region ndash Exporting Economiesn EU is the target of much of exports region still tied

to EU economic performancen Exports are on average 65 of GDP in CEE or CEE

aspirant emerging and frontier markets countries

020406080

100ExportsGDP

Source UniCredit CEE Quarterly

15

The Attractions of the CEE Region ndash CEE adhesion and its impactn EU is a market of 500 mio people ndash 10 CEE countries who

are EU membersaspirants have a population of 110 mio

n EU development and other funds are key drivers for growth

n Euro participation is an emerging issue with currently AT SK and SI being in countries but others plan to join ldquoin the futurerdquo

n And in the securities world harmonisation infrastructure convergence and common regulation are prevailing trends

n The MSI all country index includes AT (developed) RU PL CZ and HU (emerging) from the CEE with most others still classified as ldquofrontierrdquo

16

And the T2S development is attracting both Euro and non Euro markets and is a major enterprise

Austria

Slovakia

Slovenia

Hungary

Romania

Rebuilding platform project plan being implemented details shared with users currently scheduled for phase 3 release

T2S on top of infrastructure total redesign of IT architecture will retain many local unique features currently scheduled for phase 2 release

T2S on top of current architecture upgraded two years ago middleware decision to be made 2Q2013 currently scheduled for phase 3 release

T2S on top of current infrastructure RFP out to allow tender for major market IT re-engineering T2S to cover EUR settlement only (not Florint) currently scheduled for phase 3 release

T2S on top of current infrastructure some enhancements to be adopted T2S to cover EUR settlement only (not Leu) currently scheduled for phase 1 release

17

The Attractions of the CEE Region - IPOrsquos nThe region is moving from state managed to market economies

nWe expect a greater number of new IPOs ndash on averagemarkets could increase market cap by 100 to reach world ldquonormsrdquo

n Some of the IPOrsquos could be substantial (On the WSE in 2011 there were 16 foreign issuers listed of which 12 on the main list)

n Align this with above average GDP growth and a more friendly global environment and market capitalisations could well rise dramatically

nThe region is still complex change is country centric and local knowledge and involvement is key to managing the process

18

The Attractions of the CEE Region ndash Growing Local Investor Base

n A recent CEESEG study showed that just 138 of the domestic stocks held by institutional investors in their four markets are held by domestic institutions the balance by foreign investors with the US (336) UK (188) and France (53) being the major investors

0

10

20

30

40

USA UK Austria France Germany Other

Foreign Investment in CEE

19

The Attraction of the CEE Region - Infrastructure is changing

nThe dominant players in the region are CEESEG and the Warsaw Stock Exchange

0

20

40

60

80

Securities Euro (b) MiFID liquid Int MembersCEESEG WSE

Source CEESEG

20

But The market Infrastructure Is Bound To Change

n MTFrsquos are syphoning off some of the more liquid stock activity to the detriment of the traditional Exchangesn Many regional markets are small many markets have low liquidityn A regional grouping makes sense and the major impediment will be political

Oslash Can it be structured around a CEE regional grouping an expanded CEESEG a hub from Moscow or the sometimes debated PolishAustrian alliance

Oslash Will it be driven by an acquirer from Western Europe such as Deutsche Boerse or Euronext

Oslash Is there enough value to attract a new entrant a buyer from another region

21

The Special Features of the Region

nPolitical and economic factors drive markets (eg electoralchange public policy on savings)

nCost advantage over much of EU exporters (dependent on EU economic performance expanding markets outside EU)

n Markets are adopting EU harmonization (better governance improved transparency but still ldquoexcitingrdquo developing markets)

BUTn Substantial diversity remains across markets ( the region will move

forward at different speeds and will take a decade + long process)

ANDn Unicredit GSS presence countries are 14 states of the CEE

accounting for around 450 of the Deloitte CEE top 500 companies

22

The Custodian Perspective In A Changing Environment

n Infrastructure consolidation likely to be Exchange led with CCPs and CSDs as slow followersn EU legislation being adopted in EU markets and becoming template for best practise elsewheren Harmonisation (eg T+2) with an eye to Western Europen Risk and cost dynamics militate for the regional custody providers with a strong regional asset gathering rolen Although we can think of a ldquosingle marketrdquo for the next generation local presence key in markets with many unique characteristics

23

My Vision For the Future Decade- Exciting Space with ChallengesMacroeconomic perspectivenFaster economic growth

than world or European average

Capital markets perspectiven Stock Exchanges increase

in scale but also align to major Groupings within or outside region nRapid development of

domestic institutional markets

Regional Investments perspectiven Russia Poland Czech Republic

and possibly Hungary will move from emerging to developed in MSI

Infrastructure perspectivenCCP development and

interoperability with major groupings nCSDs use common infrastructures

but retain local presences (notary functions) with CEESEG Warsaw and Moscow retaining independencenAlignment of infrastructures and

adoption of EU laws across much of the region

Why CEE

Tomasz Grajewski

Global Head GSSUnicredit

24

25

The impact of EU legislation on the post-trading industryRafael PlataHead of Derivatives and Post-tradingFederation of European Securities Exchanges (FESE)9th CEE Summit Prague ndash 19th April 2013

FESE represents in total 46 Securities Exchanges (in equities bonds and derivatives) through 21 Full Members from all EU Member States and Iceland Norway and Switzerland as well as 4 Observer Members from European emerging markets

46 Securities Exchanges through 20 Full Members from 30 countries

4 Observer Members from 4 countries

The Federation of European Securities Exchanges (FESE)

Why a trading person in a post-trading panel

TRADING

POST-TRADING

QuestionHow many EU legislations regulated CCPs and CSDs prior to EMIRCSD Legislation

1 None

2 2

3 3

4 5

G20 implementation in the EU for OTC derivatives

OTC Derivatives

Clearing obligation

Trading obligation

Capital RequirementsContracts subject to CCP clearing obligation

Contracts subject to trading obligation RMsMTFsOTFs

G20

CRD IV

EMIR

MiFID

bull Average frequency of tradesbull Average size of tradesbull Number and type of active market participants

ESMA OK based on

bull Standardisation of the contractbull Reduction of systemic risk in the financial system (inc lack of transparency on positions)bull Liquidity of contracts

bull Availability of pricing information

ESMA OK based on

EMIR also includes a requirement for derivatives to be reported to Trade Repositories

bull CCP clearing obligationbull Liquidity based on

31

Arrangements for naked CDS trading

Scope

MiFID

EMIR

CRD IV

Post-trading

TradingMarketAbuse

Eq FI Ds

Ds OTCDsEqEq FI DsScope

- Sounder CCPs

- Trade repositories

Gral review + G20 commitments on derivatives

Short SellingCDS

Eq FI Ds

+ Use of CCPs Extension of MAD regime to OTCDerivatives

CSD Reg

Eq FI

- Sounder CSDs

- Settlement Cycles

Eq = Equity FI = Fixed Income Ds = Derivatives

The EU regulatory landscape

EMIR

Equity Fixed Income

Derivatives

`Trading

Clearing

Trade repositories

Trading

Clearing

Settlement

Trading

Clearing

Derivatives Equity Fixed Income

Settlement

EMIR - Provisions

1- CCP clearing obligation

2- CCPs rules and relationship with members

3- Reporting to trade repositories obligation

Question

What percentage of the global OTC interest rate swaps market was cleared at the end of 2009

1 35

2 52

3 70

4 98

Main impacts of EMIR

Safety

Efficiency

Transparency

MarginsCollateral

Paper-work

New infrastructures

Trade Repositories for EU derivatives

DTCC

CDS

DTCC

IRS

DTCC

London

CDS

Copy of the US original

Luxembourg

REGIST-TR

ALL

FXCommodity

DTCC

Equity

London

Access to data by EU supervisors

EUU

S

DTCC

Others

DTCC

CSD Legislation ndash In progress

Market discipline

Settlement cycles

Electronic records

CSD rules

Passport

User choice

Access

More than settlement

Settlement

Safety Efficiency

Safety Efficiency Transparency

QuestionThe need of collateral will increase after the implementation of EU Legislation What are the estimated annual costs of the internal fragmentation of the global collateral management market

1 17 million EUR

2 83 million EUR

3 1 billion EUR

4 4 billion EUR

So what is there for the future

So what is there for the futureReview

EMIR

CSD Legislation

New issues

Communication protocols

CCP services to buy-side

Intraday settlement operating hoursdeadlines

Pre-settlement harmonisation

Registration procedures

Withholding tax procedures

Transaction tax procedures

Exchange Traded Funds (ETFs)

Cross border shareholder transparency

Děkuji

ContactRafael PlataHead of Derivatives and Post-tradingFederation of European Securities Exchanges (FESE)platafeseeu+3225510189

42

Panel discussion

Latest Trends in Eastern Funds Distribution

43

Fidelity Worldwide Investment

April 2013

Adam LessingHead of Austria and Eastern Europe

sect Founded in 1969 serving institutional clients for over 40 years

sect Investment Management is our only business

sect Fundamental research is the foundation of our investments

sect The company is privately held majority owned by the managers who run it and our chairman Ned Johnson and his family have been the single largest shareholders since inception

sectWe have built our business slowly and steadily through organic growth so our culture has remained strong and our business franchise stable

Fidelity Worldwide Investment is a Private CompanyIts only Business is Asset Management

Our interests and our clientsrsquo interests are well aligned

Source Fidelity Worldwide Investment (FIL Limited)

45

Singapore

Sydney

Hong Kong Taipei

Shanghai Tokyo

Seoul

Mumbai

Delhi

Dalian

Fidelity Worldwide InvestmentGlobal research resources

46

71 Portfolio Managers68 Equity Research37 Fixed Income Research11 Other Research

Pan Europe and Americas

10 Portfolio Managers25 Equity Research

Japan

24 Portfolio Managers42 Equity Research11 Fixed Income Research

Asia Pacific (ex Japan)

Emerging Markets

375 Total Investment Professionals

105 Portfolio Managers

194 Research Professionals

26 Traders (ex Fixed Income)

28 Divisional Management

22 Equity Research Support

Global

Europe

United Kingdom

United States

Sector and Country

LondonFrankfurt

MilanParis

Sao Paulo

Research Professional numbers include fixed income analysts and equity (including technical and shorting) analysts Fixed Income Research includes quantitative and credit analysts and traders Other Research includes real estate multi-manager quantitative and derivatives expertsPortfolio Managers include equity fixed income real estate and multi-manager teamsSource FIL Limited 31 December 2012 Data is unaudited

Fidelity Worldwide InvestmentEastern Europe Presence

sect Warsaw

sect Vienna

sect Prague

sect Budapest

sect Bratislava

sect Sales and marketing office Vienna

sect Sales office Warsaw

sect Funds registered in Czech Republic Slovak Republic and Hungary

sect Fund Platform FFB in Germany

sect Fund Platform FFB opening in Austria (Q3 2013)

sect Kronberg

sect

Source Fidelity Worldwide Investment (FIL Limited) as at 3132013

Fidelity Offers a Wide Range of Investment Funds Across all Asset Classes

8 Global EqFds 18 Eur EqFds 4 America Fds 2 Asian Bd Fds 6 Target Fds

2 Property Fds 2 EM Bd Fds 11 Bal Fds

3 euro Bd Fds

4 High Yld Fds

3 Japan Fds

19 Asia Fds

6 Intlsquol Fds

7 Cash Funds

Equities Equities EquitiesEquities

Fixed Income and Cash

FF Global RealAssets FF Euro Blue

Chip

FF ChinaConsumer

FF US High Yield

Source FIL 3062012

FF EuropeanGrowth

Balanced

Local Web and Marketing Support are Key

Source Fidelity Worldwide Investment (FIL Limited)

Important Information

This material is intended for investment professionals and must not be relied upon by private investors This communication is not directed at and must not beacted upon by persons inside the United States and is otherwise only directed at persons residing in jurisdictions where the relevant funds are authorised fordistribution or where no such authorisation is required These figures reflect the resources of FIL Limited and its subsidiaries and FMR LLC and its subsidiariesFIL Limited and FMR LLC are separate companies with some shareholders in common Source FIL and FMR LLC April 2013 Data is unaudited Researchprofessionals include associates analysts country and sector managers who retain research responsibility and technical amp quantitative analysts who are part ofthe research groups Assets and resources as of 31122012 are those of FIL Limited Data is unaudited Issued by FIL (Luxembourg) SA 2a rue AlbertBorschette 1021 Luxembourg Luxembourg Fidelity Worldwide Investment only gives information on its products and does not provide investment advice basedon individual circumstances Any service security investment fund or product outlined may not be available to or suitable for you and may not be available in yourjurisdiction It is your responsibility to ensure that any service security investment fund or product outlined is available in your jurisdiction before any approach ismade regarding that service security investment fund or product The document may not be reproduced or circulated without prior permission and must not bepassed to private investors All views expressed are those of Fidelity Worldwide Investment Fidelity Fidelity Worldwide Investment and the Fidelity WorldwideInvestment logo and currency F symbol are trademarks of FIL Limited FidelityFidelity International means FIL Limited (FIL) and its subsidiary companiesInvestments should be made only on the basis of the current Key Investor Information Document (KIID) current prospectus the annual report and ndash if publishedlater ndash the last semi-annual report They are available along with the current annual and semi-annual reports free of charge from our distributors from ourEuropean Service Centre in Luxembourg FIL (Luxembourg) SA 2a rue Borschette 1021 Luxembourg your financial advisor or for Slovakia from ourrepresentative UniCredit Bank Slovakia as with its registered office at Sancova 1a 813 33 Bratislava for Czech Republic from our representative UnicreditBank Czech Republic as Zeletavska 15251 140 92 Prag 4 ndash Michle or for Hungary from our distributor Raiffeisen Bank Zrt Akademia u 6 1054 BudapestExcept for the KIID these documents are in English Documents include the fund rules and further information regarding the incorporation of the UCITs Furtherinformation regarding the nature of the risk for this fund would be available at the following web pages For Czech Republic wwwfidelitycz for Hungarywwwfidelitycohu for Slovakia wwwfidelitysk MKAT1749

Investičniacute společnost Českeacute spořitelny as

Member of Erste Asset Management GmbH

ISČS Company Presentation26042013 - Page 52

EAM - leading asset manager in CEE region

sect Core competence mutual fundrsquos and individual mandates asset management sect EAMrsquos oldest subsidiary ERSTE-SPARINVEST KAG was founded in Austria in

1965sect Erste Asset Management Group (EAM) has EUR 47 bn AuMsect EAM has 290 employees thereof 85

investment professionalssect Number 1 in Austria Romaniasect Number 2 in Czech Republic

Croatia Serbiasect Number 3 in Hungary Slovakiasect ERSTE-SPARINVEST KAG is GIPS

certified since 2003sect Strong partner Erste Bank (market leader

in AUT CZ RO SK serves 17 million clients employs around 50000 people and operates 3100 branches in 8 countries)

ltErste Asset Management GmbHgt26042013 - page 53

Organizational chart of Erste Asset Management

Erste Asset Management GmbH is owned 100 by Erste Group Bank AG

portfolio unit

International provider with local anchoring

From a personal point of view would you invest into mutual funds

1 Yes I have already invested into mutual funds

2 No but why not in the future

3 Yes but I wonrsquot do it again

4 No and Irsquoll never invest in those products

55

Should you invest into mutual funds what would you primarily look at

1 The brand reputation of the Investment Manager

2 The fundrsquos strategy Theme

3 The risks related to investment policy

4 The costs

56

Investors and products in the area of mutual funds

Martin Rezac CFAErste Asset Management

Funds GDP

Source IMF EFAMA local associations of fund management companies

Funds Capita (in EUR)

Source IMF EFAMA local associations of fund management companies

Asset Class Mix of Fund Markets

Source local associations of fund management companies

Banking Development in Transformation Economies

Source Erste Group

62

THANK YOU

63

3

Why CEE

Tomasz GrajewskiGlobal Head GSSUnicredit

5

Agenda

nThe scale of the CEE region

nThe attractions of the CEE region

nThe special features of the CEE region

n The custodian perspective of the CEE

nA vision for the future

6

The Scale of the CEE Regionndash GDP comparison

0100200300400

GDP (EUR b)

010203040

GDP per capita (EUR k)

Source UniCredit CEE Quarterly

The potential for growth is material these are largely emerging and frontier markets

7

0500

10001500200025003000

GDP (EUR b)

010203040

GDP per capita (EUR k)

Source UniCredit CEE Quarterly and UniCredit Economics Research

The Scale of the CEE Region ndash GDP in further context

The gap in GDP per capita is a good indicator of the potential of even the regional ldquotigersrdquo

8

The Scale of the CEE Region ndash Stock Market Size

0100200300400500600700800

Stock market size (EUR billion) versus market capitalization of major global corporates

Source WFSE and FT

9

The Scale of CEE Markets ndash Market Cap to GDP

020406080

100120140160180

Domestic market cap as of GDP

Source WFSE and Unicredit Economics Research

10

The Scale of the CEE Markets

020406080

100120140160

Cap (EUR billions)600

11

The Scale of CEE Markets (Feb turnover EUR)

0

20

40

60

80

100

120

140

160Smaller markets - EUR millions

600

05

101520

Larger markets- EUR billions

12

The Attractions of the CEE Markets

nBest regional economic growth rates

nExporting economies

nCEE adhesion and impact

nIPOrsquos in the future

nGrowing local investor bases

nInfrastructure evolutionary trends

But Very Dependenton EU economies

13

The Attractions of the CEE Region- Economic Growth Ratesn Poor 2012 performance but GDP growth forecast generally ahead of EU average

-3-2-1012345

Austria Czech Hungary Poland Russia Croatia

2011 2012 2013

Source UniCredit CEE Quarterly and Unicredit Economic Research

14

The Attractions of the CEE Region ndash Exporting Economiesn EU is the target of much of exports region still tied

to EU economic performancen Exports are on average 65 of GDP in CEE or CEE

aspirant emerging and frontier markets countries

020406080

100ExportsGDP

Source UniCredit CEE Quarterly

15

The Attractions of the CEE Region ndash CEE adhesion and its impactn EU is a market of 500 mio people ndash 10 CEE countries who

are EU membersaspirants have a population of 110 mio

n EU development and other funds are key drivers for growth

n Euro participation is an emerging issue with currently AT SK and SI being in countries but others plan to join ldquoin the futurerdquo

n And in the securities world harmonisation infrastructure convergence and common regulation are prevailing trends

n The MSI all country index includes AT (developed) RU PL CZ and HU (emerging) from the CEE with most others still classified as ldquofrontierrdquo

16

And the T2S development is attracting both Euro and non Euro markets and is a major enterprise

Austria

Slovakia

Slovenia

Hungary

Romania

Rebuilding platform project plan being implemented details shared with users currently scheduled for phase 3 release

T2S on top of infrastructure total redesign of IT architecture will retain many local unique features currently scheduled for phase 2 release

T2S on top of current architecture upgraded two years ago middleware decision to be made 2Q2013 currently scheduled for phase 3 release

T2S on top of current infrastructure RFP out to allow tender for major market IT re-engineering T2S to cover EUR settlement only (not Florint) currently scheduled for phase 3 release

T2S on top of current infrastructure some enhancements to be adopted T2S to cover EUR settlement only (not Leu) currently scheduled for phase 1 release

17

The Attractions of the CEE Region - IPOrsquos nThe region is moving from state managed to market economies

nWe expect a greater number of new IPOs ndash on averagemarkets could increase market cap by 100 to reach world ldquonormsrdquo

n Some of the IPOrsquos could be substantial (On the WSE in 2011 there were 16 foreign issuers listed of which 12 on the main list)

n Align this with above average GDP growth and a more friendly global environment and market capitalisations could well rise dramatically

nThe region is still complex change is country centric and local knowledge and involvement is key to managing the process

18

The Attractions of the CEE Region ndash Growing Local Investor Base

n A recent CEESEG study showed that just 138 of the domestic stocks held by institutional investors in their four markets are held by domestic institutions the balance by foreign investors with the US (336) UK (188) and France (53) being the major investors

0

10

20

30

40

USA UK Austria France Germany Other

Foreign Investment in CEE

19

The Attraction of the CEE Region - Infrastructure is changing

nThe dominant players in the region are CEESEG and the Warsaw Stock Exchange

0

20

40

60

80

Securities Euro (b) MiFID liquid Int MembersCEESEG WSE

Source CEESEG

20

But The market Infrastructure Is Bound To Change

n MTFrsquos are syphoning off some of the more liquid stock activity to the detriment of the traditional Exchangesn Many regional markets are small many markets have low liquidityn A regional grouping makes sense and the major impediment will be political

Oslash Can it be structured around a CEE regional grouping an expanded CEESEG a hub from Moscow or the sometimes debated PolishAustrian alliance

Oslash Will it be driven by an acquirer from Western Europe such as Deutsche Boerse or Euronext

Oslash Is there enough value to attract a new entrant a buyer from another region

21

The Special Features of the Region

nPolitical and economic factors drive markets (eg electoralchange public policy on savings)

nCost advantage over much of EU exporters (dependent on EU economic performance expanding markets outside EU)

n Markets are adopting EU harmonization (better governance improved transparency but still ldquoexcitingrdquo developing markets)

BUTn Substantial diversity remains across markets ( the region will move

forward at different speeds and will take a decade + long process)

ANDn Unicredit GSS presence countries are 14 states of the CEE

accounting for around 450 of the Deloitte CEE top 500 companies

22

The Custodian Perspective In A Changing Environment

n Infrastructure consolidation likely to be Exchange led with CCPs and CSDs as slow followersn EU legislation being adopted in EU markets and becoming template for best practise elsewheren Harmonisation (eg T+2) with an eye to Western Europen Risk and cost dynamics militate for the regional custody providers with a strong regional asset gathering rolen Although we can think of a ldquosingle marketrdquo for the next generation local presence key in markets with many unique characteristics

23

My Vision For the Future Decade- Exciting Space with ChallengesMacroeconomic perspectivenFaster economic growth

than world or European average

Capital markets perspectiven Stock Exchanges increase

in scale but also align to major Groupings within or outside region nRapid development of

domestic institutional markets

Regional Investments perspectiven Russia Poland Czech Republic

and possibly Hungary will move from emerging to developed in MSI

Infrastructure perspectivenCCP development and

interoperability with major groupings nCSDs use common infrastructures

but retain local presences (notary functions) with CEESEG Warsaw and Moscow retaining independencenAlignment of infrastructures and

adoption of EU laws across much of the region

Why CEE

Tomasz Grajewski

Global Head GSSUnicredit

24

25

The impact of EU legislation on the post-trading industryRafael PlataHead of Derivatives and Post-tradingFederation of European Securities Exchanges (FESE)9th CEE Summit Prague ndash 19th April 2013

FESE represents in total 46 Securities Exchanges (in equities bonds and derivatives) through 21 Full Members from all EU Member States and Iceland Norway and Switzerland as well as 4 Observer Members from European emerging markets

46 Securities Exchanges through 20 Full Members from 30 countries

4 Observer Members from 4 countries

The Federation of European Securities Exchanges (FESE)

Why a trading person in a post-trading panel

TRADING

POST-TRADING

QuestionHow many EU legislations regulated CCPs and CSDs prior to EMIRCSD Legislation

1 None

2 2

3 3

4 5

G20 implementation in the EU for OTC derivatives

OTC Derivatives

Clearing obligation

Trading obligation

Capital RequirementsContracts subject to CCP clearing obligation

Contracts subject to trading obligation RMsMTFsOTFs

G20

CRD IV

EMIR

MiFID

bull Average frequency of tradesbull Average size of tradesbull Number and type of active market participants

ESMA OK based on

bull Standardisation of the contractbull Reduction of systemic risk in the financial system (inc lack of transparency on positions)bull Liquidity of contracts

bull Availability of pricing information

ESMA OK based on

EMIR also includes a requirement for derivatives to be reported to Trade Repositories

bull CCP clearing obligationbull Liquidity based on

31

Arrangements for naked CDS trading

Scope

MiFID

EMIR

CRD IV

Post-trading

TradingMarketAbuse

Eq FI Ds

Ds OTCDsEqEq FI DsScope

- Sounder CCPs

- Trade repositories

Gral review + G20 commitments on derivatives

Short SellingCDS

Eq FI Ds

+ Use of CCPs Extension of MAD regime to OTCDerivatives

CSD Reg

Eq FI

- Sounder CSDs

- Settlement Cycles

Eq = Equity FI = Fixed Income Ds = Derivatives

The EU regulatory landscape

EMIR

Equity Fixed Income

Derivatives

`Trading

Clearing

Trade repositories

Trading

Clearing

Settlement

Trading

Clearing

Derivatives Equity Fixed Income

Settlement

EMIR - Provisions

1- CCP clearing obligation

2- CCPs rules and relationship with members

3- Reporting to trade repositories obligation

Question

What percentage of the global OTC interest rate swaps market was cleared at the end of 2009

1 35

2 52

3 70

4 98

Main impacts of EMIR

Safety

Efficiency

Transparency

MarginsCollateral

Paper-work

New infrastructures

Trade Repositories for EU derivatives

DTCC

CDS

DTCC

IRS

DTCC

London

CDS

Copy of the US original

Luxembourg

REGIST-TR

ALL

FXCommodity

DTCC

Equity

London

Access to data by EU supervisors

EUU

S

DTCC

Others

DTCC

CSD Legislation ndash In progress

Market discipline

Settlement cycles

Electronic records

CSD rules

Passport

User choice

Access

More than settlement

Settlement

Safety Efficiency

Safety Efficiency Transparency

QuestionThe need of collateral will increase after the implementation of EU Legislation What are the estimated annual costs of the internal fragmentation of the global collateral management market

1 17 million EUR

2 83 million EUR

3 1 billion EUR

4 4 billion EUR

So what is there for the future

So what is there for the futureReview

EMIR

CSD Legislation

New issues

Communication protocols

CCP services to buy-side

Intraday settlement operating hoursdeadlines

Pre-settlement harmonisation

Registration procedures

Withholding tax procedures

Transaction tax procedures

Exchange Traded Funds (ETFs)

Cross border shareholder transparency

Děkuji

ContactRafael PlataHead of Derivatives and Post-tradingFederation of European Securities Exchanges (FESE)platafeseeu+3225510189

42

Panel discussion

Latest Trends in Eastern Funds Distribution

43

Fidelity Worldwide Investment

April 2013

Adam LessingHead of Austria and Eastern Europe

sect Founded in 1969 serving institutional clients for over 40 years

sect Investment Management is our only business

sect Fundamental research is the foundation of our investments

sect The company is privately held majority owned by the managers who run it and our chairman Ned Johnson and his family have been the single largest shareholders since inception

sectWe have built our business slowly and steadily through organic growth so our culture has remained strong and our business franchise stable

Fidelity Worldwide Investment is a Private CompanyIts only Business is Asset Management

Our interests and our clientsrsquo interests are well aligned

Source Fidelity Worldwide Investment (FIL Limited)

45

Singapore

Sydney

Hong Kong Taipei

Shanghai Tokyo

Seoul

Mumbai

Delhi

Dalian

Fidelity Worldwide InvestmentGlobal research resources

46

71 Portfolio Managers68 Equity Research37 Fixed Income Research11 Other Research

Pan Europe and Americas

10 Portfolio Managers25 Equity Research

Japan

24 Portfolio Managers42 Equity Research11 Fixed Income Research

Asia Pacific (ex Japan)

Emerging Markets

375 Total Investment Professionals

105 Portfolio Managers

194 Research Professionals

26 Traders (ex Fixed Income)

28 Divisional Management

22 Equity Research Support

Global

Europe

United Kingdom

United States

Sector and Country

LondonFrankfurt

MilanParis

Sao Paulo

Research Professional numbers include fixed income analysts and equity (including technical and shorting) analysts Fixed Income Research includes quantitative and credit analysts and traders Other Research includes real estate multi-manager quantitative and derivatives expertsPortfolio Managers include equity fixed income real estate and multi-manager teamsSource FIL Limited 31 December 2012 Data is unaudited

Fidelity Worldwide InvestmentEastern Europe Presence

sect Warsaw

sect Vienna

sect Prague

sect Budapest

sect Bratislava

sect Sales and marketing office Vienna

sect Sales office Warsaw

sect Funds registered in Czech Republic Slovak Republic and Hungary

sect Fund Platform FFB in Germany

sect Fund Platform FFB opening in Austria (Q3 2013)

sect Kronberg

sect

Source Fidelity Worldwide Investment (FIL Limited) as at 3132013

Fidelity Offers a Wide Range of Investment Funds Across all Asset Classes

8 Global EqFds 18 Eur EqFds 4 America Fds 2 Asian Bd Fds 6 Target Fds

2 Property Fds 2 EM Bd Fds 11 Bal Fds

3 euro Bd Fds

4 High Yld Fds

3 Japan Fds

19 Asia Fds

6 Intlsquol Fds

7 Cash Funds

Equities Equities EquitiesEquities

Fixed Income and Cash

FF Global RealAssets FF Euro Blue

Chip

FF ChinaConsumer

FF US High Yield

Source FIL 3062012

FF EuropeanGrowth

Balanced

Local Web and Marketing Support are Key

Source Fidelity Worldwide Investment (FIL Limited)

Important Information

This material is intended for investment professionals and must not be relied upon by private investors This communication is not directed at and must not beacted upon by persons inside the United States and is otherwise only directed at persons residing in jurisdictions where the relevant funds are authorised fordistribution or where no such authorisation is required These figures reflect the resources of FIL Limited and its subsidiaries and FMR LLC and its subsidiariesFIL Limited and FMR LLC are separate companies with some shareholders in common Source FIL and FMR LLC April 2013 Data is unaudited Researchprofessionals include associates analysts country and sector managers who retain research responsibility and technical amp quantitative analysts who are part ofthe research groups Assets and resources as of 31122012 are those of FIL Limited Data is unaudited Issued by FIL (Luxembourg) SA 2a rue AlbertBorschette 1021 Luxembourg Luxembourg Fidelity Worldwide Investment only gives information on its products and does not provide investment advice basedon individual circumstances Any service security investment fund or product outlined may not be available to or suitable for you and may not be available in yourjurisdiction It is your responsibility to ensure that any service security investment fund or product outlined is available in your jurisdiction before any approach ismade regarding that service security investment fund or product The document may not be reproduced or circulated without prior permission and must not bepassed to private investors All views expressed are those of Fidelity Worldwide Investment Fidelity Fidelity Worldwide Investment and the Fidelity WorldwideInvestment logo and currency F symbol are trademarks of FIL Limited FidelityFidelity International means FIL Limited (FIL) and its subsidiary companiesInvestments should be made only on the basis of the current Key Investor Information Document (KIID) current prospectus the annual report and ndash if publishedlater ndash the last semi-annual report They are available along with the current annual and semi-annual reports free of charge from our distributors from ourEuropean Service Centre in Luxembourg FIL (Luxembourg) SA 2a rue Borschette 1021 Luxembourg your financial advisor or for Slovakia from ourrepresentative UniCredit Bank Slovakia as with its registered office at Sancova 1a 813 33 Bratislava for Czech Republic from our representative UnicreditBank Czech Republic as Zeletavska 15251 140 92 Prag 4 ndash Michle or for Hungary from our distributor Raiffeisen Bank Zrt Akademia u 6 1054 BudapestExcept for the KIID these documents are in English Documents include the fund rules and further information regarding the incorporation of the UCITs Furtherinformation regarding the nature of the risk for this fund would be available at the following web pages For Czech Republic wwwfidelitycz for Hungarywwwfidelitycohu for Slovakia wwwfidelitysk MKAT1749

Investičniacute společnost Českeacute spořitelny as

Member of Erste Asset Management GmbH

ISČS Company Presentation26042013 - Page 52

EAM - leading asset manager in CEE region

sect Core competence mutual fundrsquos and individual mandates asset management sect EAMrsquos oldest subsidiary ERSTE-SPARINVEST KAG was founded in Austria in

1965sect Erste Asset Management Group (EAM) has EUR 47 bn AuMsect EAM has 290 employees thereof 85

investment professionalssect Number 1 in Austria Romaniasect Number 2 in Czech Republic

Croatia Serbiasect Number 3 in Hungary Slovakiasect ERSTE-SPARINVEST KAG is GIPS

certified since 2003sect Strong partner Erste Bank (market leader

in AUT CZ RO SK serves 17 million clients employs around 50000 people and operates 3100 branches in 8 countries)

ltErste Asset Management GmbHgt26042013 - page 53

Organizational chart of Erste Asset Management

Erste Asset Management GmbH is owned 100 by Erste Group Bank AG

portfolio unit

International provider with local anchoring

From a personal point of view would you invest into mutual funds

1 Yes I have already invested into mutual funds

2 No but why not in the future

3 Yes but I wonrsquot do it again

4 No and Irsquoll never invest in those products

55

Should you invest into mutual funds what would you primarily look at

1 The brand reputation of the Investment Manager

2 The fundrsquos strategy Theme

3 The risks related to investment policy

4 The costs

56

Investors and products in the area of mutual funds

Martin Rezac CFAErste Asset Management

Funds GDP

Source IMF EFAMA local associations of fund management companies

Funds Capita (in EUR)

Source IMF EFAMA local associations of fund management companies

Asset Class Mix of Fund Markets

Source local associations of fund management companies

Banking Development in Transformation Economies

Source Erste Group

62

THANK YOU

63

Why CEE

Tomasz GrajewskiGlobal Head GSSUnicredit

5

Agenda

nThe scale of the CEE region

nThe attractions of the CEE region

nThe special features of the CEE region

n The custodian perspective of the CEE

nA vision for the future

6

The Scale of the CEE Regionndash GDP comparison

0100200300400

GDP (EUR b)

010203040

GDP per capita (EUR k)

Source UniCredit CEE Quarterly

The potential for growth is material these are largely emerging and frontier markets

7

0500

10001500200025003000

GDP (EUR b)

010203040

GDP per capita (EUR k)

Source UniCredit CEE Quarterly and UniCredit Economics Research

The Scale of the CEE Region ndash GDP in further context

The gap in GDP per capita is a good indicator of the potential of even the regional ldquotigersrdquo

8

The Scale of the CEE Region ndash Stock Market Size

0100200300400500600700800

Stock market size (EUR billion) versus market capitalization of major global corporates

Source WFSE and FT

9

The Scale of CEE Markets ndash Market Cap to GDP

020406080

100120140160180

Domestic market cap as of GDP

Source WFSE and Unicredit Economics Research

10

The Scale of the CEE Markets

020406080

100120140160

Cap (EUR billions)600

11

The Scale of CEE Markets (Feb turnover EUR)

0

20

40

60

80

100

120

140

160Smaller markets - EUR millions

600

05

101520

Larger markets- EUR billions

12

The Attractions of the CEE Markets

nBest regional economic growth rates

nExporting economies

nCEE adhesion and impact

nIPOrsquos in the future

nGrowing local investor bases

nInfrastructure evolutionary trends

But Very Dependenton EU economies

13

The Attractions of the CEE Region- Economic Growth Ratesn Poor 2012 performance but GDP growth forecast generally ahead of EU average

-3-2-1012345

Austria Czech Hungary Poland Russia Croatia

2011 2012 2013

Source UniCredit CEE Quarterly and Unicredit Economic Research

14

The Attractions of the CEE Region ndash Exporting Economiesn EU is the target of much of exports region still tied

to EU economic performancen Exports are on average 65 of GDP in CEE or CEE

aspirant emerging and frontier markets countries

020406080

100ExportsGDP

Source UniCredit CEE Quarterly

15

The Attractions of the CEE Region ndash CEE adhesion and its impactn EU is a market of 500 mio people ndash 10 CEE countries who

are EU membersaspirants have a population of 110 mio

n EU development and other funds are key drivers for growth

n Euro participation is an emerging issue with currently AT SK and SI being in countries but others plan to join ldquoin the futurerdquo

n And in the securities world harmonisation infrastructure convergence and common regulation are prevailing trends

n The MSI all country index includes AT (developed) RU PL CZ and HU (emerging) from the CEE with most others still classified as ldquofrontierrdquo

16

And the T2S development is attracting both Euro and non Euro markets and is a major enterprise

Austria

Slovakia

Slovenia

Hungary

Romania

Rebuilding platform project plan being implemented details shared with users currently scheduled for phase 3 release

T2S on top of infrastructure total redesign of IT architecture will retain many local unique features currently scheduled for phase 2 release

T2S on top of current architecture upgraded two years ago middleware decision to be made 2Q2013 currently scheduled for phase 3 release

T2S on top of current infrastructure RFP out to allow tender for major market IT re-engineering T2S to cover EUR settlement only (not Florint) currently scheduled for phase 3 release

T2S on top of current infrastructure some enhancements to be adopted T2S to cover EUR settlement only (not Leu) currently scheduled for phase 1 release

17

The Attractions of the CEE Region - IPOrsquos nThe region is moving from state managed to market economies

nWe expect a greater number of new IPOs ndash on averagemarkets could increase market cap by 100 to reach world ldquonormsrdquo

n Some of the IPOrsquos could be substantial (On the WSE in 2011 there were 16 foreign issuers listed of which 12 on the main list)

n Align this with above average GDP growth and a more friendly global environment and market capitalisations could well rise dramatically

nThe region is still complex change is country centric and local knowledge and involvement is key to managing the process

18

The Attractions of the CEE Region ndash Growing Local Investor Base

n A recent CEESEG study showed that just 138 of the domestic stocks held by institutional investors in their four markets are held by domestic institutions the balance by foreign investors with the US (336) UK (188) and France (53) being the major investors

0

10

20

30

40

USA UK Austria France Germany Other

Foreign Investment in CEE

19

The Attraction of the CEE Region - Infrastructure is changing

nThe dominant players in the region are CEESEG and the Warsaw Stock Exchange

0

20

40

60

80

Securities Euro (b) MiFID liquid Int MembersCEESEG WSE

Source CEESEG

20

But The market Infrastructure Is Bound To Change

n MTFrsquos are syphoning off some of the more liquid stock activity to the detriment of the traditional Exchangesn Many regional markets are small many markets have low liquidityn A regional grouping makes sense and the major impediment will be political

Oslash Can it be structured around a CEE regional grouping an expanded CEESEG a hub from Moscow or the sometimes debated PolishAustrian alliance

Oslash Will it be driven by an acquirer from Western Europe such as Deutsche Boerse or Euronext

Oslash Is there enough value to attract a new entrant a buyer from another region

21

The Special Features of the Region

nPolitical and economic factors drive markets (eg electoralchange public policy on savings)

nCost advantage over much of EU exporters (dependent on EU economic performance expanding markets outside EU)

n Markets are adopting EU harmonization (better governance improved transparency but still ldquoexcitingrdquo developing markets)

BUTn Substantial diversity remains across markets ( the region will move

forward at different speeds and will take a decade + long process)

ANDn Unicredit GSS presence countries are 14 states of the CEE

accounting for around 450 of the Deloitte CEE top 500 companies

22

The Custodian Perspective In A Changing Environment

n Infrastructure consolidation likely to be Exchange led with CCPs and CSDs as slow followersn EU legislation being adopted in EU markets and becoming template for best practise elsewheren Harmonisation (eg T+2) with an eye to Western Europen Risk and cost dynamics militate for the regional custody providers with a strong regional asset gathering rolen Although we can think of a ldquosingle marketrdquo for the next generation local presence key in markets with many unique characteristics

23

My Vision For the Future Decade- Exciting Space with ChallengesMacroeconomic perspectivenFaster economic growth

than world or European average

Capital markets perspectiven Stock Exchanges increase

in scale but also align to major Groupings within or outside region nRapid development of

domestic institutional markets

Regional Investments perspectiven Russia Poland Czech Republic

and possibly Hungary will move from emerging to developed in MSI

Infrastructure perspectivenCCP development and

interoperability with major groupings nCSDs use common infrastructures

but retain local presences (notary functions) with CEESEG Warsaw and Moscow retaining independencenAlignment of infrastructures and

adoption of EU laws across much of the region

Why CEE

Tomasz Grajewski

Global Head GSSUnicredit

24

25

The impact of EU legislation on the post-trading industryRafael PlataHead of Derivatives and Post-tradingFederation of European Securities Exchanges (FESE)9th CEE Summit Prague ndash 19th April 2013

FESE represents in total 46 Securities Exchanges (in equities bonds and derivatives) through 21 Full Members from all EU Member States and Iceland Norway and Switzerland as well as 4 Observer Members from European emerging markets

46 Securities Exchanges through 20 Full Members from 30 countries

4 Observer Members from 4 countries

The Federation of European Securities Exchanges (FESE)

Why a trading person in a post-trading panel

TRADING

POST-TRADING

QuestionHow many EU legislations regulated CCPs and CSDs prior to EMIRCSD Legislation

1 None

2 2

3 3

4 5

G20 implementation in the EU for OTC derivatives

OTC Derivatives

Clearing obligation

Trading obligation

Capital RequirementsContracts subject to CCP clearing obligation

Contracts subject to trading obligation RMsMTFsOTFs

G20

CRD IV

EMIR

MiFID

bull Average frequency of tradesbull Average size of tradesbull Number and type of active market participants

ESMA OK based on

bull Standardisation of the contractbull Reduction of systemic risk in the financial system (inc lack of transparency on positions)bull Liquidity of contracts

bull Availability of pricing information

ESMA OK based on

EMIR also includes a requirement for derivatives to be reported to Trade Repositories

bull CCP clearing obligationbull Liquidity based on

31

Arrangements for naked CDS trading

Scope

MiFID

EMIR

CRD IV

Post-trading

TradingMarketAbuse

Eq FI Ds

Ds OTCDsEqEq FI DsScope

- Sounder CCPs

- Trade repositories

Gral review + G20 commitments on derivatives

Short SellingCDS

Eq FI Ds

+ Use of CCPs Extension of MAD regime to OTCDerivatives

CSD Reg

Eq FI

- Sounder CSDs

- Settlement Cycles

Eq = Equity FI = Fixed Income Ds = Derivatives

The EU regulatory landscape

EMIR

Equity Fixed Income

Derivatives

`Trading

Clearing

Trade repositories

Trading

Clearing

Settlement

Trading

Clearing

Derivatives Equity Fixed Income

Settlement

EMIR - Provisions

1- CCP clearing obligation

2- CCPs rules and relationship with members

3- Reporting to trade repositories obligation

Question

What percentage of the global OTC interest rate swaps market was cleared at the end of 2009

1 35

2 52

3 70

4 98

Main impacts of EMIR

Safety

Efficiency

Transparency

MarginsCollateral

Paper-work

New infrastructures

Trade Repositories for EU derivatives

DTCC

CDS

DTCC

IRS

DTCC

London

CDS

Copy of the US original

Luxembourg

REGIST-TR

ALL

FXCommodity

DTCC

Equity

London

Access to data by EU supervisors

EUU

S

DTCC

Others

DTCC

CSD Legislation ndash In progress

Market discipline

Settlement cycles

Electronic records

CSD rules

Passport

User choice

Access

More than settlement

Settlement

Safety Efficiency

Safety Efficiency Transparency

QuestionThe need of collateral will increase after the implementation of EU Legislation What are the estimated annual costs of the internal fragmentation of the global collateral management market

1 17 million EUR

2 83 million EUR

3 1 billion EUR

4 4 billion EUR

So what is there for the future

So what is there for the futureReview

EMIR

CSD Legislation

New issues

Communication protocols

CCP services to buy-side

Intraday settlement operating hoursdeadlines

Pre-settlement harmonisation

Registration procedures

Withholding tax procedures

Transaction tax procedures

Exchange Traded Funds (ETFs)

Cross border shareholder transparency

Děkuji

ContactRafael PlataHead of Derivatives and Post-tradingFederation of European Securities Exchanges (FESE)platafeseeu+3225510189

42

Panel discussion

Latest Trends in Eastern Funds Distribution

43

Fidelity Worldwide Investment

April 2013

Adam LessingHead of Austria and Eastern Europe

sect Founded in 1969 serving institutional clients for over 40 years

sect Investment Management is our only business

sect Fundamental research is the foundation of our investments

sect The company is privately held majority owned by the managers who run it and our chairman Ned Johnson and his family have been the single largest shareholders since inception

sectWe have built our business slowly and steadily through organic growth so our culture has remained strong and our business franchise stable

Fidelity Worldwide Investment is a Private CompanyIts only Business is Asset Management

Our interests and our clientsrsquo interests are well aligned

Source Fidelity Worldwide Investment (FIL Limited)

45

Singapore

Sydney

Hong Kong Taipei

Shanghai Tokyo

Seoul

Mumbai

Delhi

Dalian

Fidelity Worldwide InvestmentGlobal research resources

46

71 Portfolio Managers68 Equity Research37 Fixed Income Research11 Other Research

Pan Europe and Americas

10 Portfolio Managers25 Equity Research

Japan

24 Portfolio Managers42 Equity Research11 Fixed Income Research

Asia Pacific (ex Japan)

Emerging Markets

375 Total Investment Professionals

105 Portfolio Managers

194 Research Professionals

26 Traders (ex Fixed Income)

28 Divisional Management

22 Equity Research Support

Global

Europe

United Kingdom

United States

Sector and Country

LondonFrankfurt

MilanParis

Sao Paulo