WELCOME TO COMBATING PROCUREMENT FRAUD · WELCOME TO COMBATING PROCUREMENT FRAUD Colin M Cram FCIPS...

50

Brought to you by WELCOME TO COMBATING PROCUREMENT FRAUD Colin M Cram FCIPS Managing Director Marc1 Ltd [email protected] Tel: +44 (0) 1457 868107 Mob: +44 (0)75251 49611 www.marc1ltd.com © C M Cram FCIPS

Transcript of WELCOME TO COMBATING PROCUREMENT FRAUD · WELCOME TO COMBATING PROCUREMENT FRAUD Colin M Cram FCIPS...

Brought to you by

WELCOME TO COMBATING PROCUREMENT FRAUD

Colin M Cram FCIPSManaging Director Marc1 [email protected]: +44 (0) 1457 868107Mob: +44 (0)75251 49611www.marc1ltd.com

© C M Cram FCIPS

Tweet your questions to the speaker LIVE @SmartProcure

COLIN CRAM: BRIEF HISTORY

• Marine Climatologist• Fraud Investigator (Customs and Excise)• First Director of Benefits Agency Procurement• First Director of North West Universities Purchasing

Consortium• First Director of Research Councils’ Procurement

Organisation• Director North West Centre of Excellence• Consultant/Adviser to Large Private and Public Sector

Organisations• Managing Director Marc1 Ltd

Tweet your questions to the speaker LIVE @SmartProcure

Tweet your questions to the speaker LIVE @SmartProcure

Tweet your questions to the speaker LIVE @SmartProcure

Tweet your questions to the speaker LIVE @SmartProcure

Tweet your questions to the speaker LIVE @SmartProcure

CURRENT POSITIONS• Managing Director Marc1 Ltd• Contributing Editor to Guardian Public Leaders Network• Editor, Procurement Insights (UK and Europe)• Associate Fellow at Manchester Business School (part of University

of Manchester)• Executive Fellow, Bangor University• Associate ResPublica• Adviser to UK Government Committees

• Fellow: Chartered Institute of Purchasing and Supply (CIPS)• Member: IACCM (International Association of Contract and

Commercial Management)• Member: Society of Purchasing Officers• Associate Member: Association of Certified Fraud Examiners• Member: Society of Local Authority Chief Executives

Tweet your questions to the speaker LIVE @SmartProcure

PROGRAMME CONTENT1. International Agreement: Government Responsibilities2. Consequences of Procurement Fraud (Corruption)3. What is Procurement Fraud? 4. What is the Scale of Procurement Fraud in Africa?5. Ways to Commit Procurement Fraud6. How to Identify Procurement Fraud7. How to Prevent Procurement Fraud

- Controls- Culture and Ethics- First Class Organisation- Performance Management

8. Creating an Anti-Fraud Plan

© C M Cram FCIPS

Tweet your questions to the speaker LIVE @SmartProcure

UNITED NATIONS CONVENTION AGAINST CORRUPTION (UNCAC)

Almost Every African Country has Signed UpApplies to Public and Private Sectors

What Must Signatories Do?• A body or bodies to oversee prevention of corruption• Independent judiciary• Merit based civil service• Measures to prevent money laundering• Transparent procurement• Transparency of information• Sound financial management• Conflict of interest avoidance

Tweet your questions to the speaker LIVE @SmartProcure

UNITED NATIONS CONVENTION AGAINST CORRUPTION (UNCAC)

Signatories Must Criminalise• Bribery• Embezzlement• Obstruction of Justice• Money Laundering• Concealing of Assets• Countries should Collaborate to help each other

Tweet your questions to the speaker LIVE @SmartProcure

WHAT ARE THE CONSEQUENCES OF PROCUREMENT FRAUD?• Some People Get Rich• Lost Wars

– Samuel Pepys to the Rescue• Deaths through Collapsed Buildings (2011 Turkey Earthquake)• Famine• Infrastructure Projects not delivered or delivered late• Lack of Confidence in Governments• Reduced Services to Citizens• National Economies Damaged

• Reduced inward investment• Less likely to do business with• Outflow of Money: Can Impoverish some countries

• Price Increases• Poor Morale and Performance in Organisations• Poverty• Reduced Pay• Jobs Lost• Uncompetitive – Companies and Nations

C M Cram FCIPS

Tweet your questions to the speaker LIVE @SmartProcure

SA must deal with corruption as if a cancer – Public Protector

• Tuesday, 03 April 2012 00:00 Written by Polity org.za

• Corruption is endemic in our country – both in the private and public sectors, but by candidly viewing corruption as an illness, South Africans could empower themselves to “deal with it as a nation, the way we would deal with it if it were a cancer afflicting our body," Public Protector Adv Thuli Madonsela said at the 13th WinelandsConference hosted by Stellenbosch University’s School for Public Leadership on Tuesday.

• She said that three essential factors were needed to end corruption. These included strengthening public accountability, which includes empowering civil society to ask questions; transparency, without which accountability is impossible; and ending impunity.

Tweet your questions to the speaker LIVE @SmartProcure

DEFINITIONS

CORRUPTION: The receipt of an inducement or reward which may influence the action of any person to behave dishonestly.

CONFLICT OF INTEREST: A situation where an official’s decisions are influenced by the person’s personal interests.

FRAUD: e.g. Rigging the Market, Not Delivering to Specification

© C M Cram FCIPS

Tweet your questions to the speaker LIVE @SmartProcure

EXAMPLES OF CORRUPT BENEFITS

THE FOLLOWING BENEFITS COULD BE TO THE EMPLOYEE, MEMBERS OF THE EMPLOYEE’S FAMILY OR FRIENDS

• Cash – now or later

• Shares in vendor’s business, now or in future

• Gifts

• Personal loans

• Payment of credit card and other personal bills

• Provision/Transfers of property or cars at less than fair market value or free of charge

• Building works to one’s property

• Vacations

• Sex

© C M Cram FCIPS

Tweet your questions to the speaker LIVE @SmartProcure

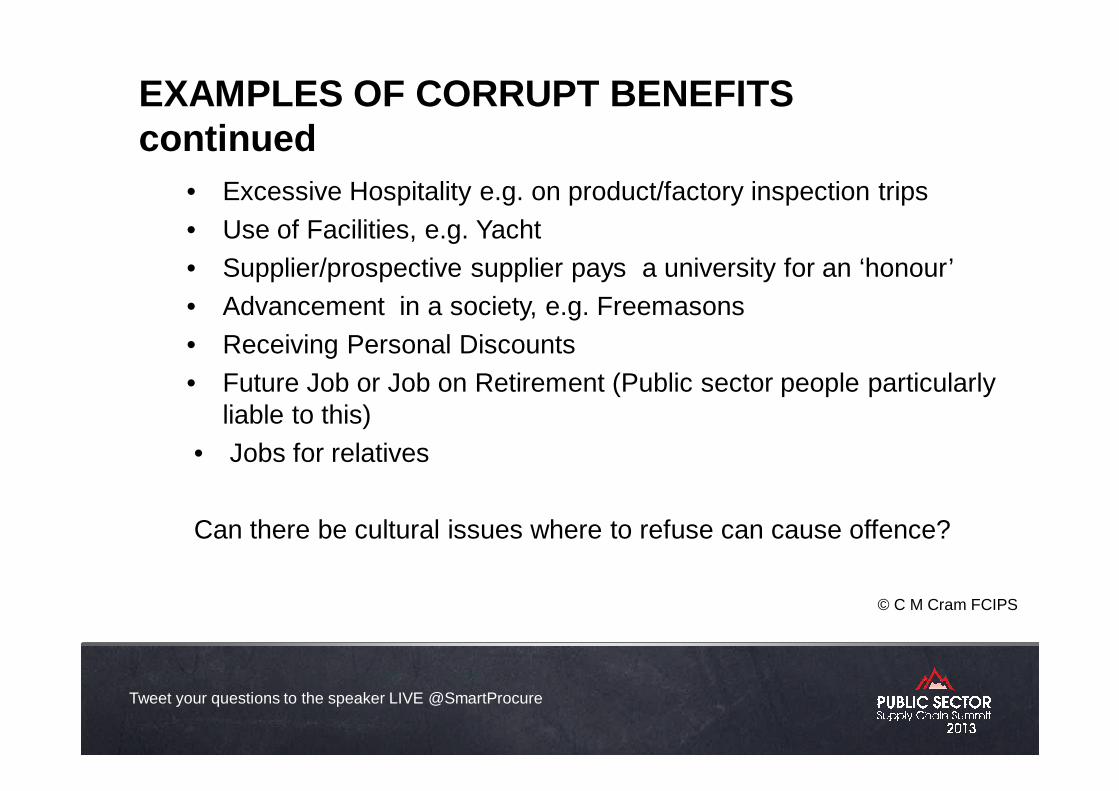

EXAMPLES OF CORRUPT BENEFITS continued

• Excessive Hospitality e.g. on product/factory inspection trips

• Use of Facilities, e.g. Yacht

• Supplier/prospective supplier pays a university for an ‘honour’

• Advancement in a society, e.g. Freemasons

• Receiving Personal Discounts

• Future Job or Job on Retirement (Public sector people particularly liable to this)

• Jobs for relatives

Can there be cultural issues where to refuse can cause offence?

© C M Cram FCIPS

Tweet your questions to the speaker LIVE @SmartProcure

EXTENT OF PROCUREMENT CORRUPTION IN SOUTHERN AFRICA?

US $10bn -$30bn

Globally, Industries Most at Risk:ConstructionDefenceOil and GasDrugs/Healthcare

© C M Cram FCIPS

Tweet your questions to the speaker LIVE @SmartProcure

TRANSPARENCY INTERNATIONAL: Corruption Perceptions

Angola 2.0

Botswana 6.1

Kenya 2.2

Lesotho 3.5

Malawi 3.0

Mozambique 2.7

Namibia 4.4

South Africa 4.1

Swaziland 3.1

Tanzania 3.0

Uganda 2.4

Zambia 3.2

Zimbabwe 2.2

Singapore 8.6 United Kingdom 7.4

Tweet your questions to the speaker LIVE @SmartProcure

WAYS TO COMMIT PROCUREMENT FRAUD

• Contracting• Tender Collusion/Bid Rigging/Cartels• Contracts Management• Cost Plus Contracts• Stock/Warehousing• Finance• Construction

Tweet your questions to the speaker LIVE @SmartProcure

WAYS TO COMMIT PROCUREMENT FRAUD (1)CONTRACTING• Letting a Contract for a Good or Service that is not Needed• Awarding Business to a Favoured Supplier or Influencing Award of Business• Giving unfair advantage to a supplier e.g. through

• Specifying in a way that suits a particular supplier• Using a supplier’s specification, thus giving it an unfair advantage• Weighting evaluation criteria to give an unfair advantage• Biased evaluation• Amending evaluation of tenders• Accepting non-conforming bids, favouring a particular supplier

• Awarding Business at an Inflated Price• Lobbying on behalf of Supplier• Giving confidential/commercial information to a supplier about another

company’s business• Disclosing competitor bid information• Disclosing Budget to a Supplier• Procurements always ‘urgent’

© C M Cram FCIPS

Tweet your questions to the speaker LIVE @SmartProcure

WAYS TO COMMIT PROCUREMENT FRAUD (2) (C M Cram/OECD)

TENDER COLLUSION/BID RIGGING

• Cartels

• Price fixing – prevalent in construction

• Price/tender collusion

• Cover bidding: A competitor agrees to submit a non-competitive bid that is too high to be accepted or contains terms that are unacceptable to the buyer.

• Bid suppression or withdrawal: A competitor agrees not to bid or to withdraw a bid from consideration.

• Market sharing: A competitor agrees to submit bids only in certain geographic areas or only to certain public organisations.

• Bid rotation: Competitors agree to take turns at winning business while monitoring their market shares to ensure they all have a predetermined slice of the pie.

• Losing bidder always just losing©C M Cram FCIPS

Tweet your questions to the speaker LIVE @SmartProcure

WAYS TO COMMIT PROCUREMENT FRAUD (3)CONTRACTS MANAGEMENT• Diverting payments to one’s own bank account. (This can be done by

creating an account with a similar name to one’s own company)• Inflated Invoices through another vendor (to make the link more difficult

to establish)• Employee creates purchase order and fake invoice for work or supply of

goods services that is not done or delivered. • Agreeing to accept goods services of a specification lower than required

in return for cash/benefits• Sub-standard Products• Defective Product/Product Substitution• Defective Testing• Agreeing to accept reduced quantities in return for cash etc

POST CONTRACT AWARD FRAUDS ARE 6 TIMES AS FREQUENT AS PRE-CONTRACT AWARD FRAUDS

© C M Cram FCIPS

Tweet your questions to the speaker LIVE @SmartProcure

WAYS TO COMMIT PROCUREMENT FRAUD (4)

COST PLUS AND CONSTRUCTION • Falsifying Payment Applications• Billing for Unperformed Work• Sub-contractor Collusion• Manipulating Change Orders• Substituting or Removing Material• Over-stating Costs• False Representations, e.g. about number of people employed

or daily rates for them• Charging for Material, Products, Services not used or procured

STRONG, EXPERT CONTRACTING AND CONTRACTS MANAGEMENT TEAM ESSENTIAL

© C M Cram FCIPS

Tweet your questions to the speaker LIVE @SmartProcure

HOW TO SPOT PROCUREMENT FRAUD

1. People Indicators2. Finance Indicators3. Contracting and Tendering Indicators

Tweet your questions to the speaker LIVE @SmartProcure

GENDER OF PERPETRATOR (Africa) (ACFE)

Gender % of Cases Median LossUS$

Male 87 300KFemale 13 200K

Tweet your questions to the speaker LIVE @SmartProcure

BEHAVIOURAL ‘RED FLAGS’ OF PERPETRATORS (%) (ACFE )

• Unusually Close Relationship with Vendor 46• Living Beyond Means 42• Wheeler-dealer Attitude 28• Financial Difficulties 25• Control Issues and Unwillingness to Share Duties 24• Irritability, Suspiciousness, Defensiveness 14• Divorce/Family Problems 11• Excessive Pressure from within Organisation 11• Past Employment Related Problems 10• Refusal to Take Holidays/Time Off 8• Complained about Inadequate Pay 8• Addiction Problems 7• Past Legal Problems 6• Excessive Family/Peer Pressure for Success 6• Complains about Lack of Authority 6 • Instability in Life Circumstances 5

Tweet your questions to the speaker LIVE @SmartProcure

FINANCE SYSTEM RED FLAGS –ANALYTICS (1)•

ADDRESSES

Common address – employee and vendor

Address doesn’t match that of company

Multiple addresses

Are some addresses ‘mail-drop’ addresses?

VENDORS

Suppliers with similar names, but

•different bank accounts

•similar addresses

•same tax reference numbers

Common telephone number – employee and supplier

More vendors for a particular service or product than one might expect (e.g. Two

suppliers for cleaning instead of one) © CM Cram FCIPS

Tweet your questions to the speaker LIVE @SmartProcure

FINANCE SYSTEM RED FLAGS –ANALYTICS (2)

©C M Cram FCIPSINVOICES and PAYMENTS

Many invoices to one supplier

Round number invoices

Similar or identical to previous invoice

One time payments to vendors (for whom no official account set up)

Invoices for different suppliers with same dollar amount, date and invoice number

(Also check to see if there is any link, e.g. through ownership)

Are invoices consistently just within tolerance limits (i.e. Too high, but only just)? A

small amount repeated many times over can end up being a big fraud

Invoice Number Sequencing:

•Do there appear to be only a few invoices or none to other customers?

•Invoice number irregularities

Invoicing in advance of scheduled delivery of goods/services

Currency exchange rates. Do they appear to be correct?

Invoice Trends: Are the numbers and values increasing over time with a particular

supplier?

Any payments that appear not to be against a valid purchase order? C M Cram FCIPS

Tweet your questions to the speaker LIVE @SmartProcure

FINANCE SYSTEM RED FLAGS (3)

• .•

© C M Cram FCIPS

EXPENDITURE (See also Purchase Spend Analysis)

Orders consistently made with one vendor without getting quotes from other vendors

Patterns of business with suppliers, e.g. if 3 key suppliers, each one seems to get a

contract/purchase in turn

Managers purchasing too frequently close to their authorisation limits

Odd purchase order patterns from an individual cost centre, company unit or company

as a whole

Variance between spend patterns with various suppliers and forecast spend?

EMPLOYEES

Directorships of suppliers by employees – sometimes similar names

Common bank account details – employee and vendor © C M Cram FCIPS

Tweet your questions to the speaker LIVE @SmartProcure

FINANCE SYSTEM RED FLAGS (4)

•

Note: To avoid overload, examine those instances thrown up by several of the analytics indicators

© C M Cram FCIPS

APPROVALS

Unauthorised approvals

Check who approved – segregation breaches?

Processed at night

Maverick buying, i.e. not using approved agreements

Too many ‘urgent’ procurements – that bypass the system

PRICING

Independent checks on market prices – sample checks

Vendor prices always just below those of competitors

Tweet your questions to the speaker LIVE @SmartProcure

TENDERING AND CONTRACTING FRAUD INDICATORS• Pre-tendering Phase: Needs Assessment• Planning and Budgeting• Definition of Requirements• Invitation to Tender• Receipt of Tenders• Evaluation and Analysis of Bids• Post Award Contract Management

IDENTIFY RISKS

Tweet your questions to the speaker LIVE @SmartProcure

PROCUREMENT CYCLE RISKS THAT COULD INDICATE OR INCREASE RISK OF CORRUPTION (2)

PLANNING & BUDGETING © C M Cram FCIPS

Is there a genuine need for the procurement?

Realism about budget:

• Are cost estimates consistent with market rates?

• Attempt to obtain project approval knowing that funds are inadequate, but that once

started, is unlikely to be stopped?

• Excessive budget?

Split purchase to avoid requester/budget holder exceeding their authority limit?

Forged signature requesting procurement?

Capability of the Unit doing the procurement.

Procurement lacks independence from other stakeholders (i.e. no independent reporting

line)

Wrong Form of Competition. Unsuitable procedure for the supply market and procurement.

Waiver of Competition

Contracts management arrangements not built into the planning

Potential unauthorised contact between personnel and possible bidder

Lack of anti-fraud plan

BEWARE: Any part of the organisation that is or claims that it should be exempt from normal

controls.

Tweet your questions to the speaker LIVE @SmartProcure

PROCUREMENT CAN REDUCE SUPPLIERS’ COSTS

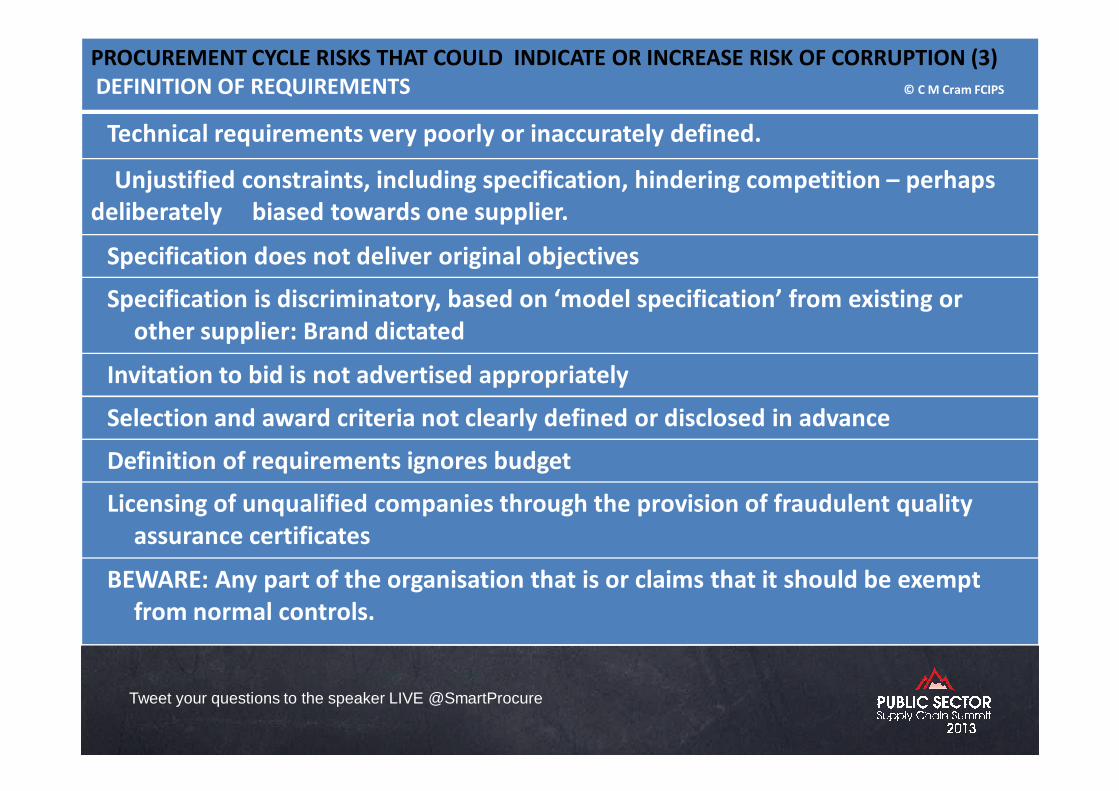

PROCUREMENT CYCLE RISKS THAT COULD INDICATE OR INCREASE RISK OF CORRUPTION (3)

DEFINITION OF REQUIREMENTS © C M Cram FCIPS

Technical requirements very poorly or inaccurately defined.

Unjustified constraints, including specification, hindering competition – perhaps

deliberately biased towards one supplier.

Specification does not deliver original objectives

Specification is discriminatory, based on ‘model specification’ from existing or

other supplier: Brand dictated

Invitation to bid is not advertised appropriately

Selection and award criteria not clearly defined or disclosed in advance

Definition of requirements ignores budget

Licensing of unqualified companies through the provision of fraudulent quality

assurance certificates

BEWARE: Any part of the organisation that is or claims that it should be exempt

from normal controls.

Tweet your questions to the speaker LIVE @SmartProcure

PROCUREMENT CAN REDUCE SUPPLIERS’ COSTS

PROCUREMENT CYCLE RISKS THAT COULD INDICATE OR INCREASE RISK OF CORRUPTION (7)

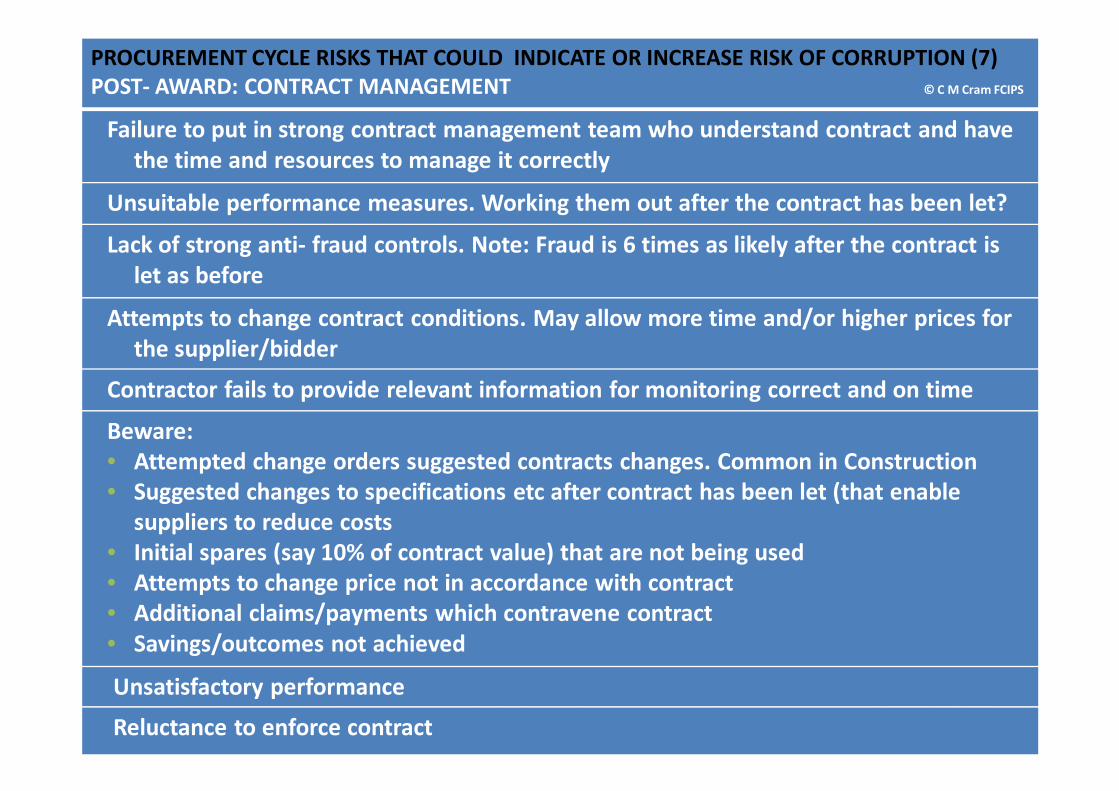

POST- AWARD: CONTRACT MANAGEMENT © C M Cram FCIPS

Failure to put in strong contract management team who understand contract and have

the time and resources to manage it correctly

Unsuitable performance measures. Working them out after the contract has been let?

Lack of strong anti- fraud controls. Note: Fraud is 6 times as likely after the contract is

let as before

Attempts to change contract conditions. May allow more time and/or higher prices for

the supplier/bidder

Contractor fails to provide relevant information for monitoring correct and on time

Beware:

• Attempted change orders suggested contracts changes. Common in Construction

• Suggested changes to specifications etc after contract has been let (that enable

suppliers to reduce costs

• Initial spares (say 10% of contract value) that are not being used

• Attempts to change price not in accordance with contract

• Additional claims/payments which contravene contract

• Savings/outcomes not achieved

Unsatisfactory performance

Reluctance to enforce contract

Tweet your questions to the speaker LIVE @SmartProcure

GENERIC GUIDELINES FOR DETECTING BID RIGGING (OECD)Look for markets that are more susceptible to bid r igging

Look for opportunities that the suppliers/bidders h ave to communicate with each other.

Look for indications that the suppliers/bidders hav e communicated with each other.

Look for any relationships among the bidders after the successful bid is announced.

Look for suspicious bidding patterns.

Look for unusual behaviour.

Look for similarities in the documents submitted by differentsuppliers/bidders.

Tweet your questions to the speaker LIVE @SmartProcure

FRAUD PREVENTION

• Effectiveness of Controls• Creating an Anti-Fraud Culture• Creating First Class Procurement

– Organisation– Ethics– Performance Management– Procurement Cycle Reviews

Tweet your questions to the speaker LIVE @SmartProcure

FRAUD DETECTION IN AFRICA (%) (ACFE)

• Whistle Blower/Tip 43• Internal Audit 14• Management Review 11• By Accident 9• External Audit 6• Account Reconciliation 5• Document Examination 4• Surveillance/Monitoring 3• Confession 2• Notified by Police 2• IT Controls 1

Tweet your questions to the speaker LIVE @SmartProcure

EFFECTIVENESS OF FRAUD CONTROLS (From ACFE data)

With Control %Reduction in Value

Hotline 59Employee Support Programme 54Surprise Audits 51Fraud Training 50Job Rotation/Mandatory Vacation 47Code of Conduct 47Anti-Fraud Policy 40Management Review 40External Audit of Internal Controls 35Internal Audit 31Independent Audit Committee 30Management Certification of Finance System 25External Audit of Finance System 25Rewards for Whistle-blowers 23

People controls seem more effective than Process on es.

Tweet your questions to the speaker LIVE @SmartProcure

INTERNAL CONTROLS MODIFIED IN RESPONSE TO FRAUD(C M Cram from ACFE data)

Internal Control Percentage Importance Basedof Organisations on Percentage

Reduction with Control in Place

Increased Segregation of Duties 61 N/AManagement Review 51 40Surprise Audits 22 52Fraud Training 15 50Job Rotation/Mandatory Vacation 14 47Internal Audit 12 31Anti-Fraud Policy 12 40Code of Conduct 9 47External Audit of Fin Systems 9 25Hotline 8 59External Audit of Internal Controls 8 35Independent Audit Committee 6 30Management Cert of Finance Systems 6 25Rewards for Whistle-blowers 4 23Employee Support Programmes 2 17

Some of the most effective controls do not find fav our

Tweet your questions to the speaker LIVE @SmartProcure

CREATING AN ANTI-FRAUD CULTURE1. Is the management climate/tone at the top one of , hard

work, modesty, honesty and integrity at work and in their private lives?

2. Create first class procurement organisation with respect in market for one’s team/personnel

3. Strategic• Clarify goals of procurement and procurement ethics• Balance priorities and values in view of available

capability and resources• Simplify and streamline procurement system4. Is on-going anti-fraud training provided to all employees

of the organisation?5. Is an effective fraud reporting mechanism in place?© C M Cram FCIPS

Tweet your questions to the speaker LIVE @SmartProcure

ANTI-FRAUD CULTURE continued6. Are fraud risk assessments performed to identify

proactively and mitigate the company’s vulnerabilities to internal and external fraud?

7. Does the internal audit department, if one exists, have adequate resources and authority to operate effectively and without undue influence from senior management?

8. Are employee support programmes in place to assist employees struggling with addictions, mental/emotional health, family or financial problems?

9. Is an open door policy in place that allows employees to speak freely about pressure, providing management the opportunity to alleviate such pressures before they become acute?

© C M Cram FCIPS

Tweet your questions to the speaker LIVE @SmartProcure

CHARTERED INSTITUTE OF PURCHASING AND SUPPLY ETHICAL CODEhttp://www.cips.org/aboutcips/whatwedo/codeofprofes sionalethics /

As a member of the Chartered Institute of Purchasin g & Supply, I will• maintain the highest standard of integrity in all my business relationships• reject any business practice which might reasonably be deemed improper• never use my authority or position for my own personal gain• enhance the proficiency and stature of the profession by acquiring and

applying knowledge in the most appropriate way• foster the highest standards of professional competence amongst those for

whom I am responsible• optimise the use of resources which I have influence over for the benefit of

my organisation• comply with both the letter and the intent of:

- the law of countries in which I practise- agreed contractual obligations - CIPS guidance on professional practice

• declare any personal interest that might affect, or be seen by others to affect, my impartiality or decision making

Tweet your questions to the speaker LIVE @SmartProcure

CIPS Ethical Code Continued

• ensure that the information I give in the course of my work is accurate• respect the confidentiality of information I receive and never use it for

personal gain• strive for genuine, fair and transparent competition• not accept inducements or gifts, other than items of small value such as

business diaries or calendars• always to declare the offer or acceptance of hospitality and never allow

hospitality to influence a business decision• remain impartial in all business dealing and not be influenced by those

with vested interests• Use of the Code• Members of CIPS are required to uphold this code and to seek

commitment to it by all those with whom they engage in their professional practice.

• Members are expected to encourage their organisation to adopt an ethical purchasing policy based on the principles of this code and to raise any matter of concern relating to business ethics at an appropriate level.

Tweet your questions to the speaker LIVE @SmartProcure

CREATING FIRST CLASS PROCUREMENT1. Creating a Capable Organisation2. Performance Management

Evaluate Procurement Models against Key Objectives

Tweet your questions to the speaker LIVE @SmartProcure

FIRST CLASS PROCUREMENT• Authority• Capability• Independence• Reputation and Respect: Within the company and with markets

and suppliers• High Morale – Self Belief, Mutually Supportive, High

Expectations• Objectives in Line with those of the Company• Performance Management• Sound Systems• Comprehensive Understanding of Procurement Spend• Market Intelligence• Involvement in Key Commercial Decision

© C M Cram FCIPS

Tweet your questions to the speaker LIVE @SmartProcure

FIRST CLASS PROCUREMENT :CAPABILITY

• Critical Mass– Sufficiently Resourced– Sustainable– Knowledge transfer– Learning Environment

• Expertise– Category– Markets and Competitors– Contracting– Contract Management– Procurement– Projects and Project Management– First Class Procurement Techniques:

• Taking Cost out of Supply Chain• Value Analysis • Market Management• E-auctions• Other up to date techniques e.g. ‘twitter’

© C M Cram FCIPS

Tweet your questions to the speaker LIVE @SmartProcure

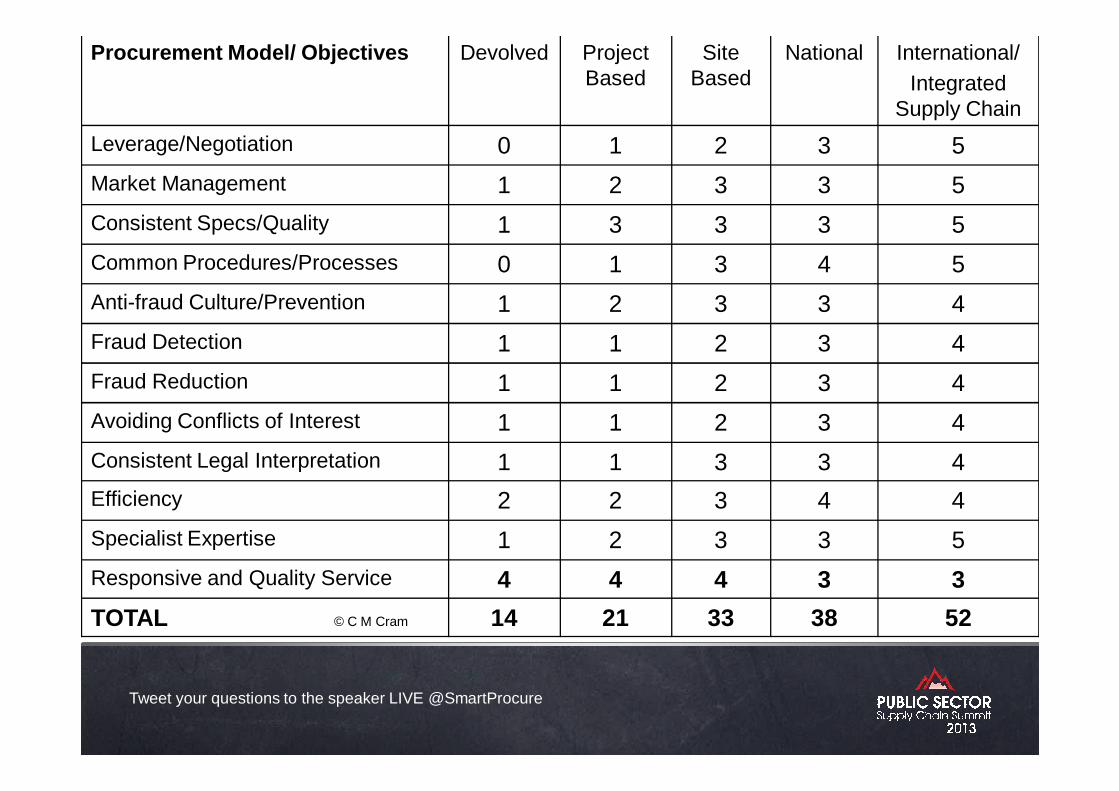

Procurement Model/ Objectives Devolved Project Based

Site Based

National International/Integrated

Supply Chain

Leverage/Negotiation 0 1 2 3 5

Market Management 1 2 3 3 5

Consistent Specs/Quality 1 3 3 3 5

Common Procedures/Processes 0 1 3 4 5

Anti-fraud Culture/Prevention 1 2 3 3 4

Fraud Detection 1 1 2 3 4

Fraud Reduction 1 1 2 3 4

Avoiding Conflicts of Interest 1 1 2 3 4

Consistent Legal Interpretation 1 1 3 3 4

Efficiency 2 2 3 4 4

Specialist Expertise 1 2 3 3 5

Responsive and Quality Service 4 4 4 3 3

TOTAL © C M Cram 14 21 33 38 52

Tweet your questions to the speaker LIVE @SmartProcure

PERFORMANCE MANAGEMENTSOME OR ALL OF THE FOLLOWING: Approximations may be adequate• Total Purchase Spend• Spend by Organisation/Country• Spend by Supplier• Top 100 Suppliers• Number of Purchase Spend Orders placed with Suppliers in each

Locality/Region/Nation• Value of Business Placed with Suppliers in each Locality/Region/Nation• Identify Spend with Suppliers common to more than one Organisation/Nation• Purchase Orders per Commodity• Purchase Spend by Commodity• Spend/Orders with Foreign Suppliers

TRENDS• Prices• Expenditure• Spend With Particular Suppliers• Commodity Volumes• Variations within Year• Against Reported Market Prices/Trends• Prices Versus Volumes © C M Cram FCIPS

Tweet your questions to the speaker LIVE @SmartProcure

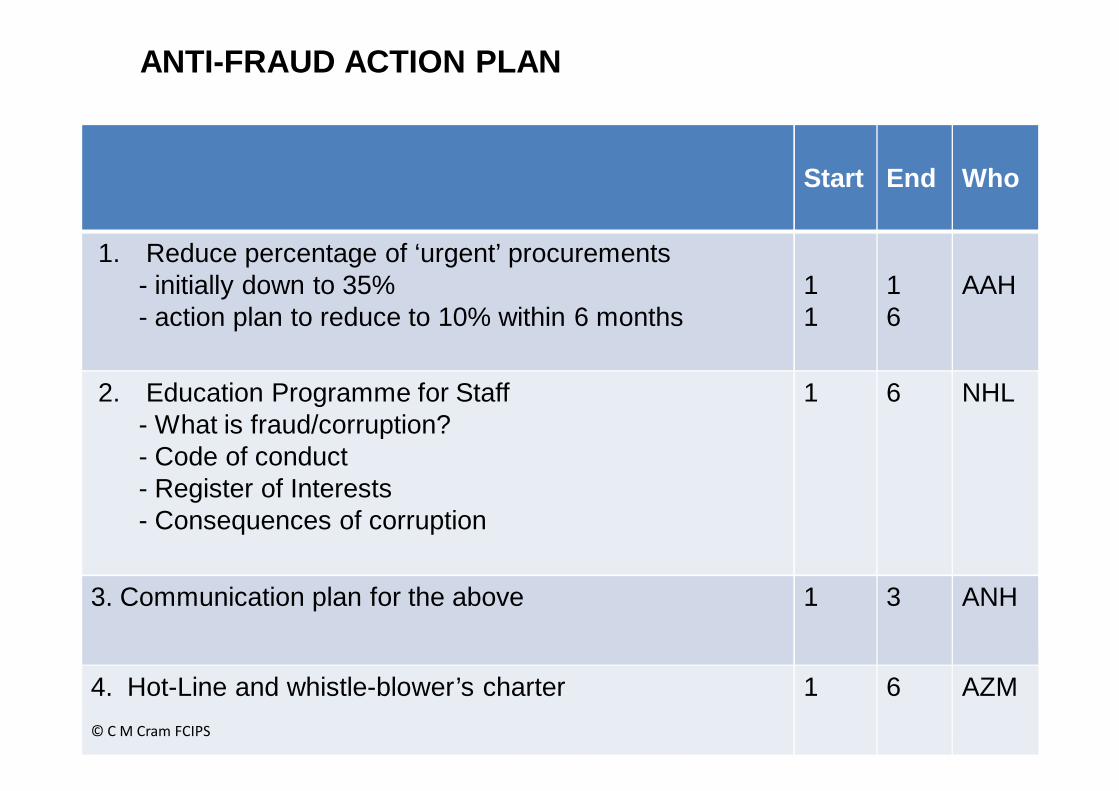

ANTI-FRAUD ACTION PLAN

Start End Who

1. Reduce percentage of ‘urgent’ procurements- initially down to 35%- action plan to reduce to 10% within 6 months

11

16

AAH

2. Education Programme for Staff- What is fraud/corruption?- Code of conduct- Register of Interests- Consequences of corruption

1 6 NHL

3. Communication plan for the above 1 3 ANH

4. Hot-Line and whistle-blower’s charter

© C M Cram FCIPS

1 6 AZM

Tweet your questions to the speaker LIVE @SmartProcure

ANTI-FRAUD ACTION PLAN5. Re-Define Role of Internal Audit in relation to fraud control/prevention

1 6 MBU

6. Surprise Audits and programme of types of checks e.g. where there is no competition

1 6 MBU

7. Terms and Conditions of Contract: Modify to take account of new anti-fraud clauses

1 1 SJP

8. Introduce Code of Conduct, Conflict of Interest Code, Register of Interests, Ethical Code and annual sign off by staff

1 6 MBU

9. Strategic Objectives of Procurement to be determined by CEO 1 1 CEO

10. Review Structure of Procurement (including ‘contracts’ in the light of the above Strategic Objectives)

1 6 CODO

11. Set up Procurement Board? Key parts of organisation to be represented

1 2 CEO

13. Introduce Performance Measures for Procurement 1 ? CSO

14A Decide Metrics to help identify if fraud or improper approach to contracting/proc14B Implement Metrics …………

1 6 -12

MAEMAE

15. Forward plan for procurements © C M Cram FCIPS

1 6 ASH

Brought to you by

MANY THANKS

GREAT TO MEET YOU

VERY BEST WISHES FOR THE FUTURE

Colin M Cram FCIPS

Tel: +44(0)1457 868107

Mob: +44(0)075251 49611

www.marc1ltd.com