Welcome. Governance Aspects of the Redesigned Form 990 and What are Best Practices? presented by...

46

Welcome

-

date post

19-Dec-2015 -

Category

Documents

-

view

214 -

download

0

Transcript of Welcome. Governance Aspects of the Redesigned Form 990 and What are Best Practices? presented by...

Welcome

Governance Aspects of the Redesigned Form 990

and What are Best Practices? presented by

Howard Donkin, [email protected]

April 27, 2009

A sustaining resource to the not-for-profit community

Pacific NW Assoc of Independent Schools (PNAIS)

Business Officers Conference

Biographical Information

• Partner, Jacobson Jarvis CPA’s• BA – Accounting - U of W, Seattle• WSCPA - NFP Committee• AICPA EO Tax Resource Panel• AICPA 990 Redesign Task Force• Executive Alliance Public Policy Group• EO Tax Review – Advisory Board

Recent Articles

• “IRS Asks Governance Questions on the New Form 990, JJCo Communiqué.

• “IRS releases revised Instructions for Redesigned Form 990”, JJCo Communiqué

2006 Predictions

• 90% chance your 990 will ask you to gather new information.

• 75% chance you will adopt a conflict of interest policy.

• 35% chance you will file electronically.

#9

Today’s Topics

• What are the Governance Aspects in the

Redesigned Form 990?

• How will they impact your school?

• What are Best Practices?

• What can you do to prepare?

• Your questions?

Optional Topics(if time allows)

• Property tax exemption update

• UPMIFA comes to Washington

• FAS 117-1

• Proposed legislation in Olympia

How did we get here?

2004 Grassley white paper and hearings

2005 Independent Sector panel on accountability

2007 Independent Sector report “Principles for Good Governance and Ethical Practice: Guide for Charities”

2008 ACT Report “IRS Role in Good Governance Issues”

Recent Quotes from IRS Officials

A well-governed charity is more likely to obey the tax laws, safeguard charitable assets, and serve charitable interests than one with poor or lax governance.

The IRS has no interest in telling charities how to run their organizations.

The question is no longer whether the IRS has a role to play in this area, but rather, what the role will be.

Timeline

Another Recent Quote

• “If a governing board tolerates a climate of secrecy or neglect, we are concerned that charitable assets are more likely to be diverted to benefit the private interests of insiders at the expense of public and charitable interests.”

IRS 2/4/08

Another Recent Quote

• “While the tax law generally does not mandate particular management structures, operational policies, or administrative practices, it is important that each charity be thoughtful about the governance practices …..As a measure of our interest in this area, we ask about an organization’s governance.”

IRS 2/4/08

Another Recent Quote

• “Because there is no precedential federal tax law guidance that prescribes the appropriate standards for nonprofit governance, a number of my clients have raised questions about how to comply with the new IRS initiatives.”

Mark Owens, a DC lawyer specializing in nonprofit issues. 1/14/09

How do we comply?

That’s why you are here !

3 things you need to know:

• What are the Governance Requirements?

• What are Best Practices?

• How do you prepare?

What “New” Form 990 ?

?

Redesigned Form 990

11- Page “Core” Form

16 Schedules (A-R)

(Old Sch. A = New Sch. E)

Redesigned Form 990

Some are not new, just same questions in different places, like……

(Old Sch. A = New Sch. E)

Where are the Governance Questions?

?

Handouts

990 Part IV (Core, page 3&4)

Checklist of Required Schedules

Q27 – Grants or assistance to directors?Q28 – Business relationships?

If yes, complete Schedule L, “Transactions with Interested Parties”.

1,2,3

990 Part VI (Core, page 6)

Governance Questions

Section A: Governing Body & Management

Section B: Policies

Section C: Disclosure

4

990 Part VI (Core, page 6)

Governance Question #1

What is the number of voting & “independent” board members?

Section A

4

990 Part VI (Core,page 6)

Governance Question #1

How do you determine Independence?

Section A

IRS Says….

IRS: The organization must make a “reasonable effort” to obtain the necessary information to determine the independence…

For instance, the organization may rely on information it obtains in response to a “questionnaire” sent annually to each member, containing instructions and definitions.

See sample questionnaire

Questionnaire

Purpose: To make a “reasonable effort” to gather information needed to answer questions about conflicts of interest and independence.

Is your board independent?

What is “IRS” Independence?

1. Not a School employee or of a related organization.

2. Didn’t get over $10,000 of pay or other payments, and

3. Wasn’t involved in a transaction reportable on Schedule L (Interested Party)

Independence

Case study: You are a voting member of the board and a partner (more than 5%) in a law firm that charged $120,000 for legal services in a court case? What if you were not a partner?

Answer: Schedule L instructions say greater than 5% ownership and $10,000.

5-6

990 Part VI (Core,page 6)

Governance Question #2

Did any officer, director, trustee or key employee have a family or business relationship?

How do you determine this?

Section A 7

Governance

What is an officer, director, trustee or key employee?

Handout defines TDOKE’s

8-9

Family or Business Relationship

What is a “family” relationship?

What is a “business” relationship?

See Questionnaire for definitions.

7

Horizontal Relationship

Case Study: Bob & Steve are board members of the school. Bob owns a car dealership and sells Steve a $45,000 car. Did they have a business relationship?

Answer: It is not a reportable relationship because it was in the ordinary course of business at same terms as public.

10, 11

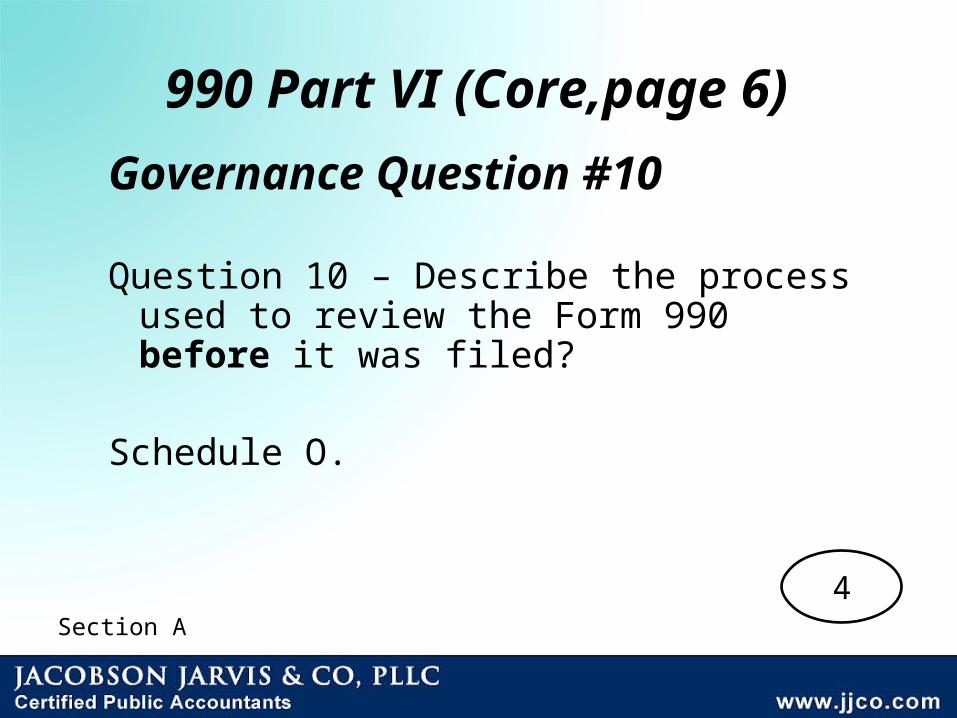

990 Part VI (Core,page 6)

Governance Question #10

Question 10 – Describe the process used to review the Form 990 before it was filed?

Schedule O.

Section A

4

Washington State Law(has a similar requirement)

Washington State Charitable Solicitations Act (RCW 19.09)

Currently in rulemaking (effective 2010).

Issue – Tier 2 independent reviewer must be a person familiar with reviewing 990’s but can’t be a board member.

990 Part VI (Core,page 6)

Policy Question #12Do you have a Written Conflict Policy?

Do you ask directors each year?

Do you monitor and enforce compliance?(Describe on Sch. O )

Section B4

What’s in a Conflict Policy?

• Define conflicts,

• Identify who is covered,

• Facilitate disclosure, and

• Specify procedures for managing a conflict.

IRS model in the instructions for the Form 1023 application. See Handout. 12

990 Part VI (Core,page 6)

Policy Question #13Do you have a written Whistleblower

Policy?

Was the policy in place as of the last day of your tax year?

See IRS instructions page 18-19.

Section B13

990 Part VI (Core,page 6)

Policy Question #14Do you have a written

Document retention and destruction Policy?

See instructions page 18-19.

Section B14

990 Part VI (Core,page 6)

Policy Question #15Do Compensation Decisions

include three things? - Advance approval (independent)- Comparable data- Written decisionDescribe Process on Schedule “O”.

Section B

Rebuttable Presumption

Of Reasonableness1.Compensation is presumed reasonable by

the IRS if you follow the three rules listed above.

2.Use a Checklist3.Think about a Compensation Committee

Section B

15

990 Part VI (Core,page 6)

Policy Question #16(b)Do you have (need) Joint Venture

Policy? Only if you answer yes to 16(a).

If yes, is it written?See IRS instructions page 19

Section B16

Conclusions

• A series of events have come together and changed our world.

• More changes are ahead

• Here are my predictions for you in 2010

#9

2010 Predictions

• 90% chance the IRS 990 instructions will be revised.

• 95% chance your Endowment footnote will be longer.

• 99% chance some of these Best Practices will not be appropriate for your school.

#9

What can you do to prepare?

• Find resources & stay informed

• Evaluate “Best Practices”

• Make a cost-benefit analysis of Best Practices

• Make Policies that fit your needs

• Keep your board informed

#9

Links to Reading

• “Principles for Good Governance – A Guide for Charities” www.nonprofitpanel.org

• “Advisory Committee on Tax – Report on IRS Good Governance Issues” June 11, 2008 www.irs/charities/article/0,,id=98353,00.html

• “IRS Form 990 Instructions” www.irs.gov• “IRS Asks Governance Questions” www.jjco.com• Sample policies at Board Source”

www.boardsource.org