Welcome Columbus Investor Forum - SVN Wilson · Columbus Investor Forum May 11, 2017 . Columbus...

33

Welcome Columbus Investor Forum May 11, 2017

Transcript of Welcome Columbus Investor Forum - SVN Wilson · Columbus Investor Forum May 11, 2017 . Columbus...

Welcome Columbus Investor Forum

May 11, 2017

Columbus Investor Forum

Market of Focus:

Columbus, Ohio

Presented by:

Doug Wilson SVN, Managing Director, Columbus

Kristen Wilson Asman SVN, Senior Advisor

“Maximum Competition = Maximum Value”

Columbus Investor Forum

Thank You to our Sponsors:

Jason Wells

Chip Holcombe

Jennifer Alvarez

What to expect…

• Commercial Real Estate Market Overview • What is the “SVN Difference”

• Expansion of Columbus SVN • Presentation of Forum Sponsors:

– Chip Holcomb, Columbus 2020 – Jason Wells, Vice President, Business Banking, Columbus – Jim Havens, Owner & Esquire, Cardinal Title

Robert M. White Jr., CRE, FRICS

US Commercial Real Estate Capital Markets Update April 5, 2017

US CRE TRENDS - ANNUAL

-8%

-100%

-50%

0%

50%

100%

150%

'03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16

Year-Over-Year Change

0

25

50

75

100

125

150

175

200

225

$0

$100

$200

$300

$400

$500

$600

'03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16

Bill

ions

Individual Portfolio Entity CRE Prices*

MOST OF INTEREST INCREASE ABSORBED IN SPREAD

0%

1%

2%

3%

4%

5%

6%

7%

8%

'06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16

Equity spread Debt spread 10yr UST

5%

6%

7%

8%

9%

'11 '12 '13 '14 '15 '16

Off Ret Ind Apt Htl

CAP RATES SLIGHTLY LOWER FOR YEAR, BUT UP IN Q4

Cap Rates, Columbus

Source: Real Capital Analytics

MACRO: US GDP, Jobs & Money

• US GDP IS 70% CONSUMER DEMAND

• 2016 GDP growth @ 1.5% - 2.0%

• 2017 GDP Growth, likely in same range as 2016.

• Political uncertainties = “The Trump Thesis”

• Jobs @ 200K/month

• Consumer debt is declining

• Consumers spending is soft.

• Corporate profits: softening

• Investment markets still flooded with capital

• Expect little inflation + only modest interest rate change

CRE OVERVIEW

• Many Strengths in Mature Market vs 2008

• Slight Sales Volume Decline: Just a Pause; • Still lots of Capital, Confidence.

• Industrial: “Last Mile” to Repurpose Retail

• Office: Suburban Office, Breakout Sector, w/self storage, SFR Portfolio & NNN’s.

• Retail: Lifestyle services, & retail.

• Apts: The “New” Demographics, Europe

• Best Return without Risk: smaller markets

• NMM, Secondary, Tertiary: more growth,

sales, pricing of assets; more investment.

• Bank Restraint in Sales and Construction.

• Private Sector Shows most Confidence.

• 2017 Volume: down 10% from 2016, but

2017.1 shows strong activity

CRE OVERVIEW

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

'06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17

7 / 10 yr Fixed Commercial Mortgage Rate

CAN CHEAP DEBT PUSH FURTHER PRICE GROWTH?

US Presidential Election

DESPITE THE RISING RATE ENVIRONMENT, MORTGAGE RATES ARE STILL LOW

HEADWIND: MORE CAPITAL FLOWING TO DEVELOPMENT

Dollars Invested in Construction

HOWEVER NEW FED SCRUTINY AND REGS ON CONSTRUCTION LOANS SHOULD KEEP BANKS DISCIPLINED…

0

1

2

3

4

5

6

7

8

9

-15

-10

-5

0

5

10

15

20

25

30

35

Q1'14 Q2'14 Q3'14 Q4'14 Q1'15 Q2'14 Q3'15 Q4'15 Q1'16 Q2'16 Q3'16 Q4'16

Bill

ions

Change in Lending Standards Development Site Sales

Net % of Respondents Reporting Tightening Standards Development Site Sales, $B

CONSTRUCTION LENDING PULLING BACK

BUT A SLIGHTLY EASIER TO GET A LOAN INTO Q4’16: SITE SALES RESPONDED

Sources: RCA, Federal Reserve Bank, Senior Loan Officer Survey

6MM Apartment

6MM CBD Office

6MM Industrial

6MM Retail6MM Suburban Office

NMM Apartment

NMM CBD Office

NMM Industrial

NMM Retail

NMM Suburban Office

Hotel

0%

5%

10%

15%

20%

-40% -30% -20% -10% 0% 10% 20%

CP

PIC

han

ge

'16

vs '1

5

Volume Change '16 vs '15

INVESTORS CHASED HIGHER YIELDS IN SECONDARY MARKETS

PRICE AND VOLUME TRENDS BY PROPERTY SECTOR

CMBS LENDING LOST MARKET SHARE IN 2016

AND BANKS OF ALL SORTS GAINED GROUND

12%

19%

28%

25%

22%

8%

8%

9%

7%

5%

21%

20%

19%

18%

27%

12%

12%

10%

11%

13%

7%

7%

7%

10%

7%

18%

16%

13%

17%

14%

20%

16%

12%

11%

9%

2016 ThruQ3

2015

2014

2013

2012

Composition of Buyers

US EQUITY CAPITAL SOURCES

CROSS-BORDER ACQUISITIONS

BUT CROSS-BORDER FLOWS HIGH AND DIVERSE

$0

$20

$40

$60

$80

$100

$120

'01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16

Europe Canada Middle East & Africa Asia Australia Latin America

billions

TRAILING 12 MONTH TOTAL

Columbus Apartments-Price Per Square Foot and Number of Sale Transactions

Source: Xceligent

APARTMENT OVERVIEW:

• Strong Demand vs. Bubble Market?

• Growth of Households still outpacing new construction

• Fundamentals Still Strengthening: – Vacancy 4%, Rent Growth 3.5%

– Population Growth: 22,000/yr in the Columbus MSA

– Millennial Population exceeds Baby Boomer Population

– New Construction mostly single bedroom

– Only entry level housing boom slows apartments

• Large quantities of affordable capital driving investment market

• Columbus Pricing is VERY attractive compared to US average.

• Columbus apartments are on the radar of National Investors

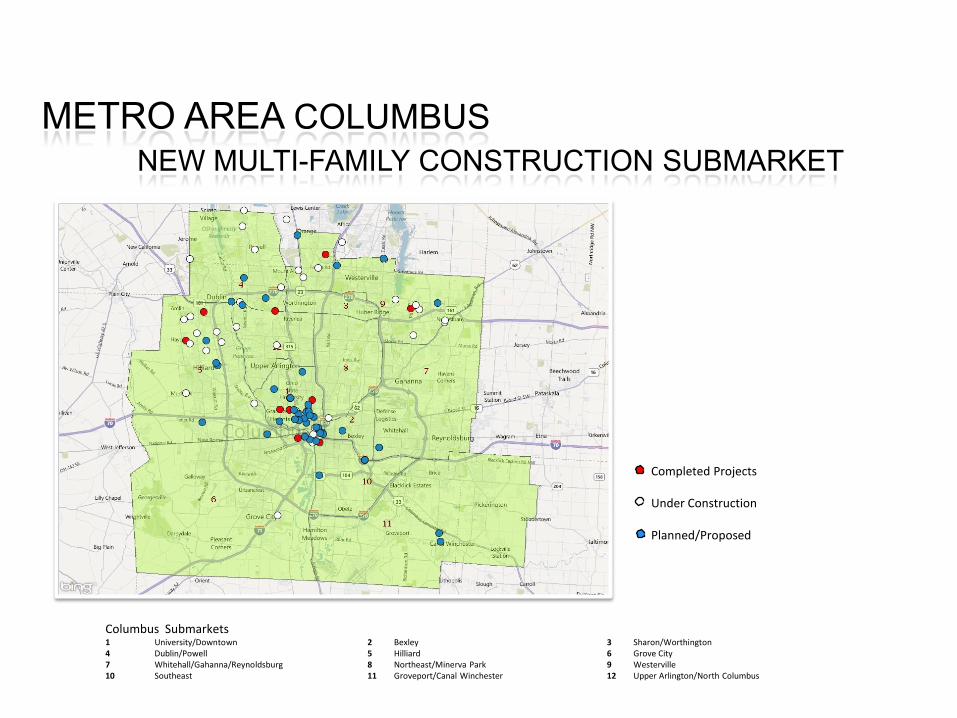

Completed Projects Under Construction Planned/Proposed

Columbus Submarkets 1 University/Downtown 2 Bexley 3 Sharon/Worthington

4 Dublin/Powell 5 Hilliard 6 Grove City

7 Whitehall/Gahanna/Reynoldsburg 8 Northeast/Minerva Park 9 Westerville

10 Southeast 11 Groveport/Canal Winchester 12 Upper Arlington/North Columbus

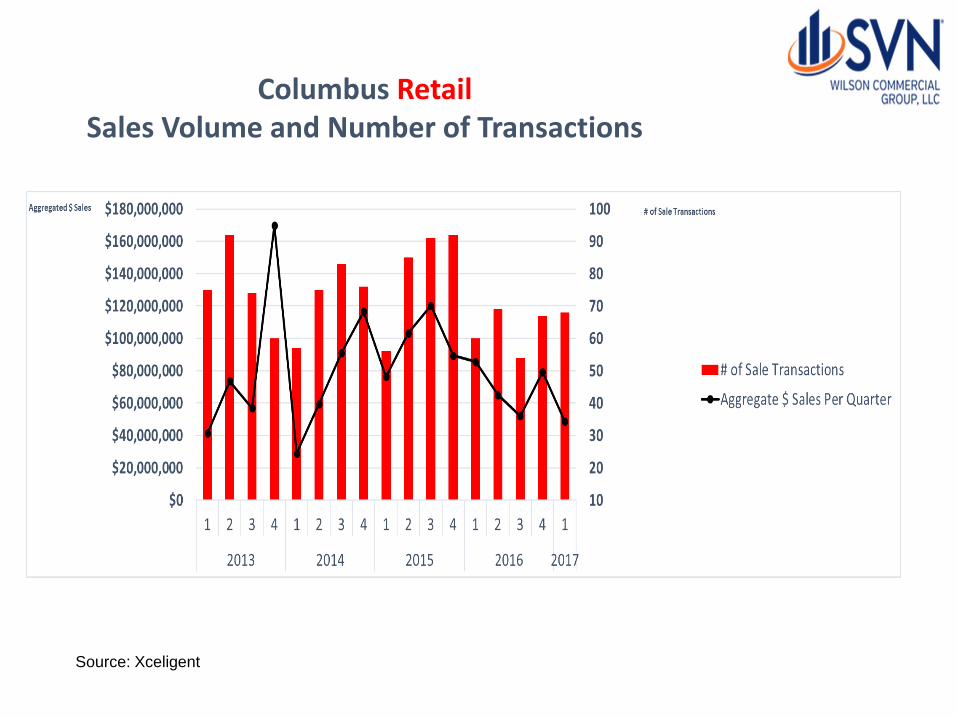

Columbus Retail Sales Volume and Number of Transactions

Source: Xceligent

RETAIL OVERVIEW: • Construction Levels Slowing • What to do with Big Box, Malls? • Occupancy high with destination, service and food tenants. • Cap Rates Falling: Dearth of New Construction combined with

Job Growth • Local Market is Strong Fundamentally.

Columbus Office Sales Volume and Number of Transactions

Source: Xceligent

OFFICE OVERVIEW:

• Fundamentals Improving, Finally

• Vacancy Beginning to Wane, especially CBD

• Mixed Use Transactions Increasing, Especially CBD

• Suburban Transactions Increase, very little construction

• Cap Rates high and Prices very competitive Locally

• Institutional Buyers Active in Columbus “hyper markets” Now – Grandview Yard

– Easton

– Polaris

Columbus Industrial Sales Volume and Number of Transactions

Source: Xceligent

INDUSTRIAL OVERVIEW:

• 1st quarter 2017 shows strong sales of portfolios

• CAP Rate reflects compression pricing from low vacancy and little speculative construction.

• Amazon Fullfillment centers spur growth in Industrial sector.

So What?. . . The Near Future and you…

• Cap Rate Compression:

− Less with Multifamily, but more compression otherwise

− But with high BPS spreads vs. T-Bills…

• Affordable capital still available…

• Record number of investors…

• Low capital gain rate unchanged for <$450k Income, 15%

• Vacancy % moving in right direction…

• Supply and demand always in play…

• Lack of alternative asset investments…

Real Estate National Outlook

• Real estate remain asset class of choice for at least next decade:

– .5%: Savings Accounts

– 1.0 – 1.5%: CD’S

– 3.5 – 4.0%: Corporate Bonds

– 5%: Stock Market

– 7% - 10%: Investment Real Estate (REAL ASSETS!).

The bottom line…

• Buy product you understand

• Buy in a market you understand

• Tolerate RISK on your terms

• Don’t buy and sell the same way

• Sell to outside “capital”

• Do not try to “finitely” time the market

• Diversify

Wilson Commercial Group

Doug Wilson, Managing Director Tim Treasure, Managing Broker

Kristen Asman, Senior Advisor Steven Heiser, Senior Advisor

Jack Turner, Senior Advisor Chris Salomone, Senior Advisor

Nail Dawaher, Senior Advisor Mike Bockbrader, Advisor

Rick Bergman, Advisor Beth Long, Advisor

Toyia Devine, Advisor Michele Reynolds, Advisor

Joe Smiley, Advisor Ann Lhota, Advisor

240 Offices Nationally, 1500 Advisors

“Local Listings with World Class Marketing”

GROWING TO MEET THE NEEDS OF CLIENTS AND THE COMMUNITY

4200 Regent Drive, Suite 200, Columbus, Ohio, 43219, 614-206-3881