Weekly Strategic Plan 10152012

of 14

-

Upload

bruce-lawrence -

Category

Documents

-

view

218 -

download

0

Transcript of Weekly Strategic Plan 10152012

-

7/28/2019 Weekly Strategic Plan 10152012

1/14

Liquidity Cycle

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED, CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the reader of this communicati on is not the intended recemployee or agent responsible for delivering to the intended recipient), you are hereby notied that any dissemination, distribution, or copying of this communication is strictly prohibited. If you have received this communication in error, please immediately inform Innium Capital Management, LLC and then disregard and delete this communication. Do nretain any copy of this communication.

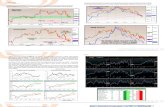

Soggy week for the equity Indices as impatience for more tangible action in Europe has morphed into a kind of is that all there is? mood. Hopeful

risk on enthusiasm threatens to become disappointed risk off liquidation if this past weeks lows are breached. No progress at all has been made

since the big FOMC announcement of QE on Sept 13 and the close Friday in the S&P was below pre-announcement prices. The next few charts will

show some other indications of growing disillusionment among buyers.

The Liquidity Cycle Indicator has turned down and is diverging from the SPX Index again. The last divergence resolved in favor of the Index b

is another cautionary sign.

The tech sector which was leading the upsurge has given way to some caution. Apple needs to resume its charge.

The Dow and the Nasdaq are no better. They have not failed yet, but this would be a good place to nd support or acceleration is likely.

-

7/28/2019 Weekly Strategic Plan 10152012

2/14

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED, CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the reader of this communicati on is not the intended recemployee or agent responsible for delivering to the intended recipient), you are hereby notied that any dissemination, distribution, or copying of this communication is strictly prohibited. If you have received this communication in error, please immediately inform Innium Capital Management, LLC and then disregard and delete this communication. Do nretain any copy of this communication.

Of course this is not helping:

These European markets have held uptrends since June, but momentum is slowing and 50 day averages are being challenged.

The Spanish yield curve which had shown a good deal of improvement from the forceful assurances of Draghi moved up last week reecting dim

expectations as progress seemed to stall and actual bond buying has not begun. That is 100 basis point move the wrong way at the front en

good sign.

There was one small bright spot (very small so far) in this chart of FXI the China Equity ETF which slipped above resistance Thursday and held i

The AAII small investors sentiment measure is fairly neutral rather than over bullish or bearish.

I suspect this merely reects the signicant drop in public

participation in the equity markets compared to pre 2008 years. I know it is fashion

blame high frequency for chasing the public away from the equity markets but, I rather think it was the bloodbath following the 2000 Nasdaq bul

followed by 50 % drop in 2008/09 that is to blame. Twice burned, forever shy for the retiring baby boomers.

-

7/28/2019 Weekly Strategic Plan 10152012

3/14

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED, CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the reader of this communicati on is not the intended recemployee or agent responsible for delivering to the intended recipient), you are hereby notied that any dissemination, distribution, or copying of this communication is strictly prohibited. If you have received this communication in error, please immediately inform Innium Capital Management, LLC and then disregard and delete this communication. Do nretain any copy of this communication.

Sectors

Look at this chart from Mebane Fabers website which he posted without comment: Money is moving away from equity risk and trying to nd yield by

going long term. This will not end well.

Developed Market Equity Index Rankings: Norway, Germany and New Zealand lead.

-

7/28/2019 Weekly Strategic Plan 10152012

4/14

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED, CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the reader of this communicati on is not the intended recemployee or agent responsible for delivering to the intended recipient), you are hereby notied that any dissemination, distribution, or copying of this communication is strictly prohibited. If you have received this communication in error, please immediately inform Innium Capital Management, LLC and then disregard and delete this communication. Do nretain any copy of this communication.

Developing and Emerging Equity Indices Ranking: Egypt, Hungary and Thailand lead. Volatility Environment

-

7/28/2019 Weekly Strategic Plan 10152012

5/14THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED, CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the reader of this communicati on is not the intended recemployee or agent responsible for delivering to the intended recipient), you are hereby notied that any dissemination, distribution, or copying of this communication is strictly prohibited. If you have received this communication in error, please immediately inform Innium Capital Management, LLC and then disregard and delete this communication. Do nretain any copy of this communication.

INDEX

Note that all implied volatility levels are at or near the bottom of their respective 1 year range. That does not imply much fear or buying of downside

protection. On the following page the implied to realized volatilities are in line but many markets have skew in the lower part of the past years range.

That is another sign of little fear.

Currency volatilities too are at the low end of the past years range.

-

7/28/2019 Weekly Strategic Plan 10152012

6/14THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED, CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the reader of this communicati on is not the intended recemployee or agent responsible for delivering to the intended recipient), you are hereby notied that any dissemination, distribution, or copying of this communication is strictly prohibited. If you have received this communication in error, please immediately inform Innium Capital Management, LLC and then disregard and delete this communication. Do nretain any copy of this communication.

-

7/28/2019 Weekly Strategic Plan 10152012

7/14

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED, CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the reader of this communicati on is not the intended recemployee or agent responsible for delivering to the intended recipient), you are hereby notied that any dissemination, distribution, or copying of this communication is strictly prohibited. If you have received this communication in error, please immediately inform Innium Capital Management, LLC and then disregard and delete this communication. Do nretain any copy of this communication.

Commodity volatilities are generally in the lower end of the years ranges except in energy.

Tables on the following page show a mix of implied to realized vols. Soybeans, coffee, Gasoline all appear to be carrying implieds that are wellbelow realized but some of this is likely due to the weekend effect.

We saw some steepening in the Crude Oil curves in both WTI and Brent this week as prices rallied:

WTI above and Brent below.

-

7/28/2019 Weekly Strategic Plan 10152012

8/14

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED, CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the reader of this communicati on is not the intended recemployee or agent responsible for delivering to the intended recipient), you are hereby notied that any dissemination, distribution, or copying of this communication is strictly prohibited. If you have received this communication in error, please immediately inform Innium Capital Management, LLC and then disregard and delete this communication. Do nretain any copy of this communication.

Soybean backwardating attened a bit, corn barely moved, and wheat moved mainly in deferred crop contracts.

Sugar prices fell sharply in the front and modestly at the back end of the curve putting in a slight contango across crop years. The message seems

to be that there is a modestly improved supply picture.

Fixed Income: I have little comment on xed income markets because they are so manipulated by central bank pronouncements that they

a fair game for speculation. They will be again one of these days. In fact they will be the biggest trading futures markets again when the mark

begin to get a whiff of the end of Fed/ECB/BOE/BOJ/whoever easing and possible withdrawal of stimulus. Then holders of Trillions of debt are

to want to put on hedges things will get exciting. If the contributor forecasts below come true those are big moves.

Articles, Charts and Commentary

Perhaps it would be a good idea to get our scal house in order.---- Nah, what could go wrong?

http://www.zerohedge.com/news/2012-10-12/charts-day-why-america-needs-embrace-fiscal-cliff-instead-kicking-can-once-againhttp://www.zerohedge.com/news/2012-10-12/charts-day-why-america-needs-embrace-fiscal-cliff-instead-kicking-can-once-again -

7/28/2019 Weekly Strategic Plan 10152012

9/14

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED, CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the reader of this communicati on is not the intended recemployee or agent responsible for delivering to the intended recipient), you are hereby notied that any dissemination, distribution, or copying of this communication is strictly prohibited. If you have received this communication in error, please immediately inform Innium Capital Management, LLC and then disregard and delete this communication. Do nretain any copy of this communication.

ESM lacks cash for Spanish bailout

The European Stability Mechanism lacks the cash to bail out Spain if the country asks for help before the end of the year, despite the rescue funds

ofcial inauguration last week and the injection by 17 member states of 32bn of capital.

Under ESM rules, paid-in capital due to reach 80bn by 2014 cannot be lent out, but must instead be invested in predominately Double A rated

European assets. That would rule out buying Spanish sovereign bonds, which were downgraded to BBB by Standard & Poors last week.

As a result, the rescue fund would need to raise money from the markets immediately if Spain were to request a bailout. Banking sources close

to the ESM say the fund is not currently planning to visit markets before January, meaning that the body would have to accelerate its borrowing

programme immediately if Spain asked for help soon.

However, one European ofcial with knowledge of internal thinking at the fund dismissed concerns about availability of funds if Spain were to

request a bailout. With 32bn of paid-in money, the ESM can start raising money tomorrow if it wants to, he said.

The ESM Treaty approved by European member states stipulates that paid-in capital must not fall below 15% of any debt issued during the phase-in

period. With 32bn now in its coffers, the ESM could in theory raise about 210bn.

The fund has already appointed Deutsche Bank, Royal Bank of Scotland and Societe Generale to arrange investor meetings across Europe in early

November, with roadshows to take place in London, Frankfurt and Paris.

According to one banking source, the body is unlikely to want to test the market in the traditionally quiet month of December and therefore the

November roadshows suggest a January debut. However, another source suggested that roadshows could be brought forward to late October,

meaning a deal in November might be just about possible.

Market watchers point out one possible way for the ESM to square this circle. The body could buy bonds and then repo them out until such time that

it can enter the market to raise funds. It was for just such a possible purpose that the EFSF asked banks to provide credit lines, although the ESM

has yet to start dicussions about such lines. (See story above).

Competing demand

Raoul Ruparel, head of economic research at think-tank Open Europe, said that if Spain did ask for a bailout in the coming weeks and the ESM did

have to go to the market immediately, this could have a negative impact on the ability of other states to raise money.

This could cause a ood, which could have a distorting effect on the market by impacting the borrowing costs of eurozone members, he said.

Ruparel argues that investors in the sovereign debt of Germany, France and other European countries are likely to be the same as those for any

ESM issues. A bond issue from the fund could therefore reduce demand for seemingly less-safe European debt.

It introduces another potential source of volatility, he added. It is not well planned. They should have foreseen a Spanish request and had a plan

in place to stagger the bond issues.

According to Ruparel, if Spain asks for even a partial bailout now, the ESM will need about 60bn100bn for a bond buying programme.

They should have foreseen a Spanish request and had a plan in place

The necessary approval from eurozone countries to alter the terms of the agreed banking bailout could be another obstacle for the fund. It had

been hoped that Spain could tap a portion of the 100bn bailout for its banks an amount already given the green light by member states under a

sovereign bailout without having to seek approval.

Following recent stress tests, Spain is expected to ask for about 40bn to recapitalise its banks. This money is to come from the agreed 100bn

bank bailout through the EFSF to the Spanish Fund for Orderly Bank Restructuring, and then into the banks the ESM cannot directly recapitalise

banks until the single European supervisor is in place.

New conditions

The money left over from the already agreed 100bn bank bailout cannot be re-purposed, said Ruparel. Reports have suggested that it could

easily be re-purposed and used as part of a bond-buying programme, but that is not correct. It would require new conditions and probably a new,

separate bailout, he added.

This point was made clear by Klaus Regling then head of the EFSF when asked at an investor conference on September 25 whether Spain

could use parts of the 100bn assigned for the banking sector for sovereign purposes.

The Memorandum of Understanding for the Spanish banking system does not allow any other use, said Regling. The ESM declined to comment.

(BBL--- So I guess the Euro will become the new reserve currency anyday now.)

CNBCs Gary Kaminsky pointing out the junkiness of these deals...This is Junk, This is Bad!

Christopher Wood of Greed and Fear newsletter fame.

Greed and Fear

The continuing reality of zero rates, or near zero rates, in so many important markets has led to one by now dramatically self-evident phenom

That is an explosion in corporate bond issuance this year, be in in America, Europe or Asia. This trend is primarily a response to demand rathe

because corporates need to borrow lots of money to fund, say, new investment.

The demand for corporate bonds is coming from investors with capital seeking to generate yield, and often this is being done by taken o

of gearing. Thus, private bankers in Asia have apparently become increasingly aggressive offering gearing on corporate bond purchases to th

clients. And the willingness to lend money in this manner has grown as condence has grown that US short-term interest rates will remain at z

for longer.

The obvious triggers for a rout of leveraged corporate bond investors would be central bank tightening by the likes of the Fed and/or a s

sell-off in the Treasury bond market. But for now there is no sign of either development. The private bankers selling the bonds on leverage can

continue to argue that spreads are not yet at historic lows even if nominal yields on such bonds are at record lows.

US bond mutual fund inows have dramatically exceeded the inows into US equity mutual funds since 2007. Thus, US bond funds hav

recorded US$237bn of inows so far in 2012 and US$1.12tn since 2007, while equity funds have recorded outows of US$78bn year-to-date

US$385bn since 2007.

The next three charts are from Bank Credit Analyst. The rst two illustrate some of the reasons for expecting another bout of dollar weakness

the third is an overlay of copper and crude oil price movement over the last decade.

http://www.zerohedge.com/news/2012-10-11/visualizing-central-bank-mal-investment-driven-excesshttp://www.zerohedge.com/news/2012-10-11/visualizing-central-bank-mal-investment-driven-excesshttp://www.zerohedge.com/news/2012-10-11/visualizing-central-bank-mal-investment-driven-excesshttp://www.zerohedge.com/news/2012-10-11/visualizing-central-bank-mal-investment-driven-excess -

7/28/2019 Weekly Strategic Plan 10152012

10/14

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED, CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the reader of this communicati on is not the intended recemployee or agent responsible for delivering to the intended recipient), you are hereby notied that any dissemination, distribution, or copying of this communication is strictly prohibited. If you have received this communication in error, please immediately inform Innium Capital Management, LLC and then disregard and delete this communication. Do nretain any copy of this communication.

Chinas Economy Shows Signs of Stabilizing as Exports Strengthen

Oct. 15 (Bloomberg) -- Chinas exports and money supply grew more than estimated in September, signaling that the worlds second-biggest

economy may be stabilizing after a slowdown that began in the rst quarter of 2011.

Overseas shipments increased 9.9 percent from a year earlier, the customs administration said Oct. 13 in Beijing. That was more than the 5.5

percent median estimate in a Bloomberg News survey of economists. M2 money supply gained 14.8 percent, the fastest pace since June 2011, a

central bank report showed the same day.

Ination numbers due today and an Oct. 18 report on the third-quarter economy will complete the picture as ofcials assess whether more measures

are needed to sustain growth as the Communist Party prepares for a once-a-decade leadership handover starting next month. At an International

Monetary Fund meeting in Tokyo yesterday, central bank ofcial Yi Gang said that bubble risks remain in housing markets in major cities and

stimulus will be restricted to an appropriate level.

Better-than-expected export growth is likely to help support employment and reduce pressure for more policy easing ahead of the leadership

transition, said Chang Jian, a Hong Kong-based economist at Barclays Plc. Monetary easing has been constrained by concerns about a rebound

in property prices and medium-term ination risks.

The lack of a big scal stimulus also points to concerns about rising government debt, banks non-performing loans, and inefcient investment, she

said.

Ination Forecast

Ination was 1.9 percent last month, close to a two-year low, according to the median forecast in a Bloomberg News survey. Chinas gross

domestic product expanded 7.4 percent in the third quarter from a year earlier, according to the median in a separate survey, the seventh quarterly

deceleration.

Yi, a deputy governor at the central bank, said yesterday that while this years ination rate is ne and may be 2.7 percent for the full year, longer-

term threats are from agricultural costs and prices for imported raw materials, commodities and energy, which can be driven up by global monetary

easing.

The IMF last week reduced its estimate for Chinas growth this year to 7.8 percent, which would be the weakest pace since 1999, as Europes

debt crisis crimps exports. Alcoa Inc., the largest U.S. aluminum producer, cut its forecast for global consumption of the metal on slowing Chinese

demand.

Limiting Stimulus

China has refrained from implementing stimulus on the scale of the 4 trillion yuan ($586 billion at the time) package it unleashed at the end of 2008

during the global nancial crisis. The response to the latest slowdown has included two cuts in interest rates, three reductions in bank reserve

requirements, lower taxes, higher spending on social welfare and accelerated investment approvals.

The expansion in M2 was driven by the central bank pumping record amounts of cash into the money markets through reverse repurchase

agreements, said Hu Yifan, Hong Kong-based chief economist at Haitong International Securities Group. New lending was below economists

estimates, data showed last week. Analysts median forecast had been for a 13.7 percent gain in M2.

The central banks Oct. 13 report also showed the nations foreign-exchange reserves, the worlds largest, rose t o $3.29 trillion in September from

$3.24 trillion in June.

Economic Momentum

The trade and money supply data suggest economic momentum in China may be picking up, said Zhang Zhiwei, chief China economist with

Nomura Holdings Inc. in Hong Kong. These upside surprises are consistent with other positive signals in recent weeks indicating growth may

rebound this quarter, he said.

Shipments to the European Union fell 10.7 percent last month from a year earlier. At the same time, those to Southeast Asian nations jumped 25.5

percent and sales to the U.S. increased at the fastest pace in three months.

Imports rose 2.4 percent, in line with the median economist estimate, leaving a trade surplus of $27.7 billion, the biggest since June.

In the rst nine months, the surplus widened about 38 percent from a year earlier to $148.3 billion, customs data show. That may provide

ammunition to Republican presidential candidate Mitt Romney, who pledges to designate the nation a currency manipulator if elected, a step the

U.S. government hasnt taken since 1994.

Geithners Take

The trade data indicated that the value of Chinas exports to the U.S. exceeded its imports from the nation by about $21 billion in September. U.S.

Treasury Secretary Timothy F. Geithner said in Tokyo on Oct. 13 that while some progress has been made toward a more balanced economic

relationship with China, more is needed.Anti-China rhetoric may feature in the lead-up to the presidential election on Nov. 6, said Liu Li-Gang, a Hong Kong- based economist with Australia

& New Zealand Banking Group Ltd. The yuan, which touched a 19-year high against the dollar last week, may appreciate until then in response to

the pressure, Liu said. The currency has gained about 2 percent since July 25. It closed last week at 6.2672 per dollar.

Bill Gross and Pimco Article

Cashin Remembers Germanys Hyperination Birthday

If you did not see t his article I suggest you read it about once a month

Seven Varieties of Deation

By Dr. A. Gary Shilling

Ination in the U.S. has historically been a wartime phenomenon, including not only shooting wars but also the Cold War and the War on Pove

Thats when the federal government vastly overspends its income on top of a robust private economyobviously not the case today when

government stimulus isnt even offsetting private sector weakness. Deation reigns in peacetime, and I think it is again, with the end of the Ira

engagement and as the unwinding of Afghanistan expenditures further reduce military spending.

Chronic Deation

Few agree with my forecast of chronic deation. Theyve never seen anything but ination in their business careers or lifetimes, so they think

the way God made the world. Few can remember much about the 1930s, the last time deation reigned. Furthermore, we all tend to have in

biases. When we pay higher prices, its because of the ination devil himself, but lower prices are a result of our smart shopping and bargaini

skills. Furthermore, we dont calculate the quality-adjusted price declines that result from technological improvements in many big-ticket purch

This is especially true since many of those items, like TVs, are bought so infrequently that we have no idea what we paid for the last one. But

sure remember the cost of gasoline on the last ll-up a week ago.

Doubts

Furthermore, many believe widespread deation is impossible and that rampant ination is assured in future years because of continuing hig

federal decits, regardless of any long-run budget reform. And annual decits of over $1 trillion are likely to persist in the remaining ve to sev

years of deleveraging, as I explain in my recent book, The Age of Deleveraging. The 2% annual real GDP growth I see persisting is well below

3.3% needed to keep the unemployment rate stable. So to prevent high and chronically rising unemployment, any Administration and Congre

left, right or centerwill be forced to spend a lot of money to create a lot of jobs.

But big federal decits are inationary only when they come on top of fully-employed economies and create excess demand. Thats obviously

true at present when large decits are reactions to private sector weakness that has slashed tax revenues and encouraged decit spending. I

the slack in the economy in the face of persistent trillion dollar-plus decits measures the huge size and scope of the offsetting deleveraging i

private sector, as noted earlier.

The deleveraging, especially in the global nancial sector and among U.S. consumers, will be completed in another ve to seven years at the

it is progressing. At that point, the federal decit should fade quickly, assuming a war or other cause of oversized government spending doesn

intervene. The resumption of meaningful economic growth will reduce the pressure for economic stimuli and rising incomes and corporate pro

spur revenues. Serious work on the postwar baby-related bulge in Social Security and Medicare costs will also depress the decit.

Good DeationA decade ago in my two Deation books, I distinguished between two types of deationthe Good Deation of excess supply and the Bad D

of decient demand. Good Deation is the result of important new technologies that spike productivity and output even as the economy grows

rapidly. Bad Deation results from nancial crises and deep recession, which hype unemployment and depress demand.

Ive been forecasting chronic good deation of excess supply because of todays convergence of many signicant productivity-soaked techno

such as semiconductors, computers, the Internet, telecom and biotech that should hype output. Ditto for the globalization of production and th

other deationary forces Ive been discussing since I wrote the two Deation books and The Age of Deleveraging. As a result of rapid product

growth, fewer and fewer man-hours are needed to produce goods and services. The rapid productivity growth so far this decade is likely to pe

(Chart 1).

John Mauldins Outside The Box is the source of this article by Gary Schilling. I suggest each of you go to Mauldin Economics Outside the

for a free subscription.

http://www.pimco.com/EN/Insights/Pages/Damages.aspxhttp://www.zerohedge.com/news/2012-10-11/cashin-remembers-germanys-hyperinflation-birthdayhttp://www.mauldineconomics.com/outsidetheboxhttp://www.mauldineconomics.com/outsidetheboxhttp://www.mauldineconomics.com/outsidetheboxhttp://www.mauldineconomics.com/outsidetheboxhttp://www.zerohedge.com/news/2012-10-11/cashin-remembers-germanys-hyperinflation-birthdayhttp://www.pimco.com/EN/Insights/Pages/Damages.aspxhttp://www.pimco.com/EN/Insights/Pages/Damages.aspx -

7/28/2019 Weekly Strategic Plan 10152012

11/14

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED, CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the reader of this communicati on is not the intended recemployee or agent responsible for delivering to the intended recipient), you are hereby notied that any dissemination, distribution, or copying of this communication is strictly prohibited. If you have received this communication in error, please immediately inform Innium Capital Management, LLC and then disregard and delete this communication. Do nretain any copy of this communication.

After Chinas huge stimulus program in 2009 in response to the global recession and nosedive in exports to U.S. consumers, the economy re

but so did ination. Double-digit food price jumps were especially troublesome in a land where many live at subsistence levels. So in respons

the surge in ination and the real estate bubble, Chinese leaders tightened economic policy, driving down CPI ination to a 2.0% rise in Augu

year earlier. But, in conjunction with the weakening in export growth, that is pushing China toward a hard landing of 5% to 6% economic grow

below the 7% to 8% needed to maintain stability.

Back in the States, inationary expectations, as measured by the spread between 10-year Treasury yields and the yield on comparable Treas

Ination-Protected Securities are narrowing.

Other Varieties

Besides rises or falls in general price levels, which most think about when they hear ination or deation, there are six other varieties, may

more.

Commodity Ination/Deation. In the late 1960s, the mushrooming costs of the Vietnam War and the Great Society programs in an already-ro

economy created a tremendous gap between supply and demand in many areas. The history of low ination rates for goods and services, we

call it CPI ination for short, in the late 1950s and early 1960s, apparently created a momentum of low price advances that kept CPI ination f

exploding until about 1973. But by the early 1970s, commodity prices started to leap and spawned a self-feeding up surge. Worried that theyd

run out of critical materials in a robust economy, producers started to double and triple order supplies to insure adequate inventories. That hy

demand, which squeezed supply, and prices spiked further. That spawned even more frenzied buying as many expected shortages to last for

At the time, even before the 1973 oil embargo, I was lucky enough to realize that what was occurring was not perennial shortages but massiv

inventory-building. I found a parallel in post-World War I when wartime price and wage controls were removed and wholesale prices skyrocke

about 30% in one year as double and triple ordering hyped inventories amid frenzied demand and fears of shortages. Then all those inventor

arrived and sired the 1920-1921 recession, the sharpest on record, and wholesale prices collapsed. Armed with this history, I correctly foreca

1973-1975 recession and said it would be the worst since the 1930s, which it proved to be. Arriving inventories swamped production, especia

late 1974 and early 1975, so production nosedived.

Another Commodity Bubble

Its probably no coincidence that Chinas joining the World Trade Organization at the end of 2001 was followed by the commencement of anot

global commodity price bubble that started in early 2002 (Chart 4). And it has been a bubble, in my judgment, based on the conviction that Ch

would continue to absorb huge shares of the worlds industrial and agricultural commodities. The shift of global manufacturing toward China

magnied her commodity usage as, for example, iron ore that previously was processed into steel in the U.S. or Europe was sent to China ins

While Ive consistently predicted the good deation of excess supply, I said clearly that the bad deation of decient demand could occurdue to

severe and widespread nancial crises or due to global protectionism. Both are now clear threats.

My forecast is that the unfolding global slump will initiate worldwide chronic deation. A number of indicators point in that direction. Sure, much of

the recent weakness in the PPI and CPI has been due to falling energy and food prices. Excluding these volatile items, prices are still rising but at

slowing rates (Charts 2 and 3). Consumer price ination is also falling abroad in the U.K. and the eurozone.

Peak Oil

Crude oil has been the darling of the commodity-shortage crowd, and when its price rose to $145 per barrel in July 2008, many became conv

that the world would soon run out of oil.

But they discounted the f act that reserves are often underestimated since oil elds produce more than original conservative estimates. Nor di

they expect conventional and shale natural gas, liqueed natural gas, the oil sands in Canada, heavy oil in Venezuela and elsewhere, oil shal

coal, hydroelectric power, nuclear energy, wind, geothermic, solar, tidal, ethanol and biomass energy, fuel cells, etc. to substitute signicantly

petroleum.

Recent Weakness

The weakness in commodity prices, starting in early 2011, no doubt has been anticipating both a hard landing in China and a global recession

my view, the foundation of the decade-long commodity bubble is crumbling, and the unfolding of a hard landing in China and worldwide reces

will depress commodity prices considerably, even from current levels, as disillusionment replaces investor enthusiasm.

-

7/28/2019 Weekly Strategic Plan 10152012

12/14

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED, CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the reader of this communicati on is not the intended recemployee or agent responsible for delivering to the intended recipient), you are hereby notied that any dissemination, distribution, or copying of this communication is strictly prohibited. If you have received this communication in error, please immediately inform Innium Capital Management, LLC and then disregard and delete this communication. Do nretain any copy of this communication.

Financial Asset Ination/Deation. Perhaps the best recent example of nancial asset ination was the dot com blowoff in the late 1990s. It

culminated the long secular bull market that started in 1982 and was driven by the convergence of a number of stimulative factors. CPI inatio

peaked in 1980 and declined throughout the 1980s and 1990s. That pushed down interest rates and pushed up P/Es. American business

restructured and productivity leaped.

A Secular Down Cycle

The robust economy upswing that drove the 1982-2000 secular bull market ended in 2000, as shown by basic measures of the economys he

Stocks, which gauge economic health as well as fundamental sentiment, have been trending down since 2000 in real terms (Chart 7). At the r

that deleveraging worldwide is progressing, it will take another ve to seven years to be completed with equity prices continuing weak on bala

during that time. Employment also peaked out in 2000 even after accounting for lower although rising labor participation rates by older Americ

Household net worth in relation to disposable (after-tax) income has also been weak for a decade.

Wage-Price Ination/Deation. A second variety of ination is a particularly virulent form, wage-price ination in which wages push up prices, which

then push up wages in a self-reinforcing cycle that can get deeply and stubbornly embedded in the economy. This, too, was suffered in the 1970s

and accompanied slow growth. Hence the name, stagation. As with commodity ination, it was spawned by excess aggregate demand resulting

from huge spending and the Vietnam War and Great Society programs on top of a robust economy.

Back then, labor unions had considerable bargaining strength and membership. Furthermore, American business was relatively paternalist, with

many business leaders convinced they had a moral duty to keep their employees at least abreast of ination. Most didnt realize that, as a result,

ination was very effectively transferring their prots to labor. And also to government, which taxed underdepreciation and inventory prots. The

result was a collapse in corporate prots share of national income and a comparable rise in the share going to employee compensation from the

mid-1960s until the early 1980s.

The Peak

The wage-price spiral peaked in the early 1980s as CPI ination began a downtrend that has continued. Voters rebelled against Washington,

elected Ronald Reagan and initiated an era of government retrenchment. The percentage of Americans who depend in a signicant way on income

from government rose from 28.7% in 1950 to 61.2% in 1980, but then f ell to 53.7% in 2000. Furthermore, the Fed, under then-Chairman Paul

Volcker, blasted up interest rates, and negative real borrowing costs turned to very high positive levels.

As ination receded, American business found itself naked as the proverbial jaybird with depressed prots and intense foreign competition. In

response, corporate leaders turned to restructuring with a will. That included the end of paternalism towards employees as executives realized they

were in a globalized atmosphere of excess supply of almost everything. With operations and jobs moving to cheaper locations offshore and with the

economy increasingly high tech and service oriented, union membership and power plummeted, especially in the private sector.

In todays unfolding deation, the wage-price spiral has been reversed. Contrary to most forecaster expectations, but forecast in my two Deation

books, wages are actually being cut and involuntary furloughs instituted for the rst time since the 1930s. In ination, oversized wages can be cut

to size by simply avoiding pay hikes while ination erodes real compensation to the proper level. But with deation, actual cuts in nominal pay are

necessary. Note that as wage cuts and furloughs become increasingly prevalent, the layoff (Chart 5) and unemployment numbers (Chart 6) will

increasingly understate the reality of the declines in labor compensation.

The Federal Reserves Survey of Consumer Finances, just published for 2007-2010, reveals that median net worth of families fell 39% in thos

years from $126,400 to $77,300, largely due to the collapse in house prices. Average household income fell 11% from $88,300 to $78,500 in t

years with the middle-class hit the hardest. The top 10% by net worth had a 1.4% drop in median income, the lowest quartile lost 3.7% but the

second quartile was down 12.1% and the third quartile dropped 7.7%.

Households reacted to too much debt by reducing it. In 2010, 75% of households had some debt, down from 77% in 2007, according to the F

survey. Those with credit card balances fell from 46.1% to 39.4% but late debt payments were reported by 10.8% of households, up from 7.1%

2007. With house prices collapsing, debt as a percentage of assets climbed to 16.4% in 2010 from 14.8% in 2007. Financial strains reduced t

percentage that saved in the preceding year from 56.4% in 2007 to 52% in 2010.

Nevertheless, the gigantic policy ease in Washington in response to t he stock market collapse and 9/11 gave the illusion that all was well and

the growth trend had resumed. The Fed rapidly cut its target rate from 6.5% to 1% and held it there for 12 months to provide more-than ample

monetary stimulus. Meanwhile, federal tax rebates and repeated tax cuts generated oceans of scal stimulus as did spending on homeland s

Afghanistan and then Iraq.

As a result, the speculative investment climate spawned by the dot com nonsense survived. It simply shifted from stocks to commodities, fore

currencies, emerging market equities and debt, hedge funds, private equityand especially to housing. Homeownership additionally benete

low mortgage rates, loose lending practices, securitization of mortgages, government programs to encourage home ownership and especially

conviction that house prices would never fall.

Investors still believed they deserved double-digit returns each and every year, and if stocks no longer did the job, other investment vehicles w

This prolongs what I have dubbed the Great Disconnect between the real world of goods and services and the speculative world of nancial a

Treasuries

I hope youll recall my audacious forecast of 2.5% yields on 30-year Treasury bonds and 1.5% on 10-year Treasury notes, made at the end of

year when the 30-year yield was 3.0%. Those levels were actually reached recently (Chart 8), and I now believe the yields will fall to 2.0% and

1.0%, respectively, for the same reasons that inspired my earlier forecasts. The global recession will attract money to Treasurys as will deatio

their safe-haven status. Sure, Treasurys were downgraded by Standard & Poors last year, but in the global setting, theyre the best of a bad l

-

7/28/2019 Weekly Strategic Plan 10152012

13/14

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED, CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the reader of this communicati on is not the intended recemployee or agent responsible for delivering to the intended recipient), you are hereby notied that any dissemination, distribution, or copying of this communication is strictly prohibited. If you have received this communication in error, please immediately inform Innium Capital Management, LLC and then disregard and delete this communication. Do nretain any copy of this communication.

Housing Woes

House prices have been deating for six years, with more to go (Chart 10). The earlier housing boom was driven by ample loans and low inte

rates, loose and almost non-existent lending standards, securitization of mortgages which passed seemingly creditworthy but in reality toxic a

on to often unsuspecting buyers, and most of all, by the conviction that house prices never decline.

The deation in interest rates has spawned signicant side effects. Its a zeal for yield that has pushed many individual and institutional investors

further out on the risk spectrum than they may realize. Witness the rush into junk bonds and emerging country debt. Recently, investors have

jumped into the government bonds of Eastern European countries such as Poland, Hungary and Turkey where yields are much higher than in

developed lands. The yield on 10-year notes in Turkish lira is about 8% compared to 1.4% in Germany and 1.6% in the U.S.

The inow of foreign money has pushed up the value of those countries currencies, adding to foreign investor returns. And some of these

economies look solid relative to the troubled eurozonePoland avoided recession in the 2008-2009 global nancial crisis. But the continuing

eurozone nancial woes and recession may well drag the zones Eastern European trading partners down. And then, as foreign investors ee and

their central banks cut rates, their currencies will nosedive much as occurred in Brazil.

Tangible Asset Ination/Deation. Booms and busts in tangible asset prices are a fourth form of ination/deation. The big ination in commercial

real estate in t he early 1980s was spurred by very benecial tax law changes earlier in the decade and by nancial deregulation that allowed nave

savings and loans to make commercial real estate loans for the rst time. But deation set in during the decade due to overbuilding and the 1986

tax law constrictions. Bad loans mounted and the S&L industry, which had belatedly entered commercial real estate nancing, went bust and had to

be bailed out by taxpayers through the Resolution Trust Corp.

Nonresidential structures, along with other real estate, were hard hit by the Great Recession and remain weak as capacity remains ample and

prices of commercial real estate generally persist well below the 2007 peak. The two obvious exceptions are rental apartments and medical ofce

buildings. Returns on property investments recovered from the 2007-2009 collapse, but are now slipping.

Retail vacancy rates remain high (Chart 9) due to cautious consumers and growing online sales. Rents remain about at. Ditto for ofce vacancies

due to weak employment and the tendency of employers to move in the partitions to pack more people into smaller ofce spaces. The ofce

vacancy rate in the second quarter was 17.2%, the same as the rst quarter, down slightly from the post-nancial crisis peak of 17.6% in the third

quarter of 2010 but well above the 2007 boom level of 13.8%. In the second quarter, ofce space occupancy rose just 0.12% from the previous

quarter compared to 0.18% in the rst quarter.

I expect another 20% decline in single-family median house prices and, consequently, big problems in residential mortgages and related

construction loans. In making the case for continuing housing weakness, Ive persistently hammered home the ongoing negative effect of exc

inventories on house sales, prices, new construction and just about every other aspect of residential real estate.

Spreading Effects

That further drop would have devastating effects. The average homeowner with a mortgage has already seen his equity drop from almost 50%

the early 1980s to 20.5% due to home equity withdrawal and falling prices. Another 20% price decline would push homeowner equity into sing

digits with few mortgagors having any appreciable equity left. It also would boost the percentage of mortgages that are under water, i.e., with

mortgage principals that exceed the houses value, from the current 24% to 40%, according to my calculations. The negative effects on consu

spending would be substantial. So would the negative effects on household net worth, which already, in relation to after-tax income, is lower th

the 1950s.

Currency ination/deation. We all normally talk about currency devaluation or appreciation. This is, however, another type of ination/deatio

like all the others, it has widespread ramications. Relative currency values are inuenced by differing monetary and scal policies, CPI inati

deation rates, interest rates, economic growth rates, import and export markets, safe haven attractiveness, capital and nancial investment

opportunities, attractiveness as trading currencies, and government interventions and jawboning, among other factors. In recent years, Japan

South Korea, China and Switzerland have all acted to keep their currencies from rising to support their exports and limit imports.

The U.S. dollar has been strong of late, resulting from its safe haven status in the global nancial crisis. Furthermore, the U.S. economy, whil

slipping, is in better shape than almost any otherthe best of the bunch. I believe the global recession will persist and the greenback will con

serve this role. Furthermore, the greenback is likely to remain strong against other currencies for years as it continues to be the primary intern

trading and reserve currency. The dollar should continue to meet at least ve of my six criteria for being the dominant global currency:

1. After deleveraging is complete, the U.S. will return to rapid growth in the economy and in GDP per capita, driven by robust productivity.

2. The American economy is large and likely to remain the worlds biggest for decades.

3. The U.S. has deep and broad nancial markets.

4. America has free and open nancial markets and economy.

5. No likely substitute for the dollar on the global stage is in sight.

6. Credibility in the buck has been in decline since 1985, but may revive if long-run government decits are addressed and consumer retrench

and other factors shrink the foreign trade and current account decits.

Ination By Fiat. Way back in 1977, I developed the Ination by Fiat concept, which gained media attention in that era of high wage-price ina

This seventh form of ination encompassed all those ways by which, with the stroke of a pen, Congress, the Administration and regulators rai

prices.

The continual rises in the minimum wage is a case in point. So, too, are high tariffs on imported Chinese tires. Agricultural price supports kee

prices above equilibrium. As a result, the producer price of sugar in the U.S. is 28 cents per pound compared to the 19 cents world price. Fed

contractors are required to pay union wages, which almost always exceed nonunion pay, as noted earlier, another example of ination by at.

-

7/28/2019 Weekly Strategic Plan 10152012

14/14

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED, CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the reader of this communicati on is not the intended recemployee or agent responsible for delivering to the intended recipient), you are hereby notied that any dissemination, distribution, or copying of this communication is strictly prohibited. If you have received this communication in error, please immediately inform Innium Capital Management, LLC and then disregard and delete this communication. Do nretain any copy of this communication.

--Bruce Lawrence Oct 14, 2012

Environmental protection regulations may improve the climate, but they increase costs that tend to be passed on in higher prices. The

Administration says its new fuel-economy standards of 54.5 miles per gallon by 2025 will cost $1,800 per vehicle but industry estimates put it at

$3,000. The cap and t rade proposal to reduce carbon emissions is estimated to cost each American household $1,600 per year, according to the

Congressional Budget Ofce. Pay hikes for government workers must be paid in higher taxes sooner or later, and can spill over into private wage

increasesalthough state and local government employee pay is moving back toward private levels, as discussed earlier. Increases in Social

Security taxes raise employer costs, which they try to pass on in higher selling prices.

There was some deation by at in the 1980s and 1990s. One of the biggest changes was requiring welfare recipients to work or be in job-

training programs. That reduced the welfare rolls from 4.7% of the population in 1980 to 2.1% in 2000, while the overall number that depended on

government for meaningful income dropped from 61.2% to 53.7%. But now, as an angry nation and left-leaning Congress and Administration react

to the nancial collapse, Wall Street misdeeds and the worst recession since the Great Depression, the increases in government regulation and

involvement in the economy have been substantial. And with them, more ination by atat least unless there is a major change of government

control with the November elections.

(Excerpted from Gary Shillings INSIGHT newsletter. For more information, visitwww.agaryshilling.com)

http://www.agaryshilling.com/http://www.agaryshilling.com/