Week 1. What we will cover in this course General place of AIS in accounting Conceptual place of AIS...

25

Week 1

-

date post

20-Dec-2015 -

Category

Documents

-

view

214 -

download

0

Transcript of Week 1. What we will cover in this course General place of AIS in accounting Conceptual place of AIS...

Week 1

What we will cover in this course

General place of AIS in accounting Conceptual place of AIS Values and assumptions

Documentation techniques Accounting controls

Concepts—COSO/COBIT and ERM based SOX, in general and as related to controls

Database Concepts of data modeling What do accountants need to know

Business cycles and accounting systems Special topics in accounting systems

Intangibles, formatting, impacts and implications

Announcements

Send me an email. Put ACTG335 in the subject line. Send it from all the email addresses

you may rely on for class info Send it by Friday, September 28th You will be held responsible for

materials I send out by email

Many readings will be put on my website.

How does an AIS fit in an organization?

AIS objectives

Collect and store data Support efficiency and effectiveness

Provide adequate controls Provide information for decision making

Factors influencing AIS design

Strategy Information technology Organizational culture Societal demands

…what do we need to account FOR

Measurement issues

What to measure Measurement attributes What to report Abstractions

What basis for measuring? For whom? To meet what objective(s)?

Accountants are professionals, with a responsibility to serve the public interest.

Accounting Abstraction Model—what does accounting DO?

AIS as a filter

Valuation theory v. Events theory—intro to DB in AIS

Characteristics of information

Useful Relevant Reliable Complete

Usable Understandable Verifiable Credible Timely Accessible

Useful—Relevant

Connected to business objectives Logical, supportable thread from

metrics to objectives Meaningful for the purpose

intended, valid Predictive value (leading)

• Training, investment in IT, advertising

Feedback value (lagging)• ROI, net income, productivity

Lagging Indicators

Measures of output, end-process measures, record effects

Reflect past performance Generally quantitative Example: Quantity of toxic emission; last

year’s percentage of on-time deliveries Strength: Easy to quantify and understand,

preferred by regulators and public—deterministic rather than probabilistic

Weakness: Time lag in feedback, ignore present activities

Leading Indicators

In-process metrics of performance, proactive Reflect current status/activities—for future

performance Quantitative or qualitative Example: percent of facilities conducting self-

audit; training of logistics managers Strength: Represent current actions and future

trends Weakness: Harder to build support for use, harder

to track to performance—probabilistic rather than deterministic

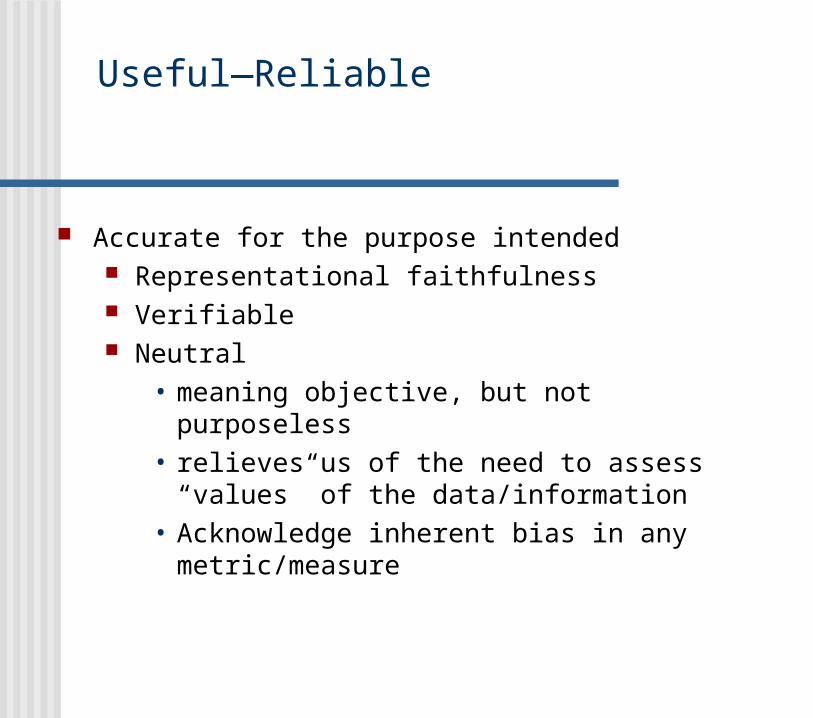

Useful—Reliable

Accurate for the purpose intended Representational faithfulness Verifiable Neutral

• meaning objective, but not purposeless• relieves us of the need to assess “values”

of the data/information• Acknowledge inherent bias in any

metric/measure

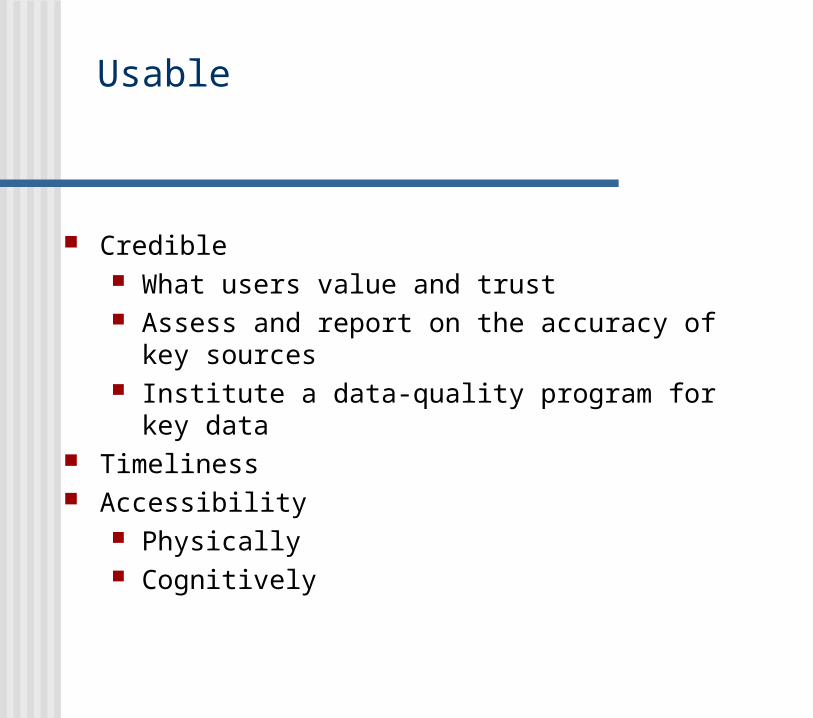

Usable

Credible What users value and trust Assess and report on the accuracy of key

sources Institute a data-quality program for key data

Timeliness Accessibility

Physically Cognitively

Information attributes Information context

Information attributes relate to the specific characteristics of individual units of information (data, really)

Information context relates to understanding how information, as defined, relates to the world in which we live and work.

Definition of context, from Merriam-Webster online dictionary:

1 : the parts of a discourse that surround a word or passage and can throw light on its meaning

2 : the interrelated conditions in which something exists or occurs

Abstractions

Abstraction model—how do we (society/stakeholders) know what happens in an organization?

Values and assumptions

Public interest Stakeholders—what does this mean?

Center for Professional Integrity and Accountability—See Values and Assumptions from the syllabus

What to measure, how to report— influences the interests that are privileged

Chapter 2—AIS processes

Transaction processing system Database

Business cycles

Real business activities for the AIS to capture, process, report

Revenue Expenditure HR Production Financing

Basic Business Processes

Get Cash

Give Cash

Get Ship

Give Cash

GetEmployeeService

Give Cash

Get Silk

Give Cash

Get Cash

Give SilkA set of

Give-Get exchanges

Collect data

Transactions: agreement between two parties to exchange economically measurable goods Capture the data Implement control procedures Record in journals

• General for rare or EOP• Specialized for standardized

Post to ledgers Prepare reports

Computer processing

Master/transaction files Batch/real-time/on-line Queries/reports

I am going to spend little time on this, but expect you to use the terms and concepts pretty readily…ask questions if you need to.

Waren Distributing

Get started.

Quiz on October 15th.