WEEK 1 FNSACC507A Management Accounting LESSON 1 ... · Selling Price ! In determining the selling...

65

Welcome to: FNSACC507A Provide Management Accounting Information

Transcript of WEEK 1 FNSACC507A Management Accounting LESSON 1 ... · Selling Price ! In determining the selling...

Welcome to:

FNSACC507A Provide Management Accounting Information

Week 1 – Chapter 1 COST CONCEPTS

FNSACC507A Provide Management Accounting Information

By the end of this lesson, you will be able to…

1. Explain the difference between management accounting and financial accounting and cost accounting

2. Identify and discuss basic cost concepts 3. Use the high-low method of

cost estimation

PART FOCUS 1 Intro. to Management Accounting

2 Management Accounting + Cost concepts

3 Cost estimation using the High-Low Method

1. Management Accounting 1. What is MANAGEMENT ACCOUNTING about? � Definition � Purpose � Tasks � Output 2. How is MANAGEMENT ACCOUNTING different from: � Financial Accounting � Cost Accounting

Management Accounting DEFINITION

The process of producing financial and operating information

regarding the economic activity

engaged in by an organisation. This information needs to be

complete, relevant, timely and accurate.

Management Accounting PURPOSE

This information is provided for decision makers internal to the organisation

e.g. employees and managers.

The management accounting process is driven by the information needs of these decision makers.

Management Accounting TASKS

COLLECT operational and financial data

STORE the information

REPORT the information to end users

PROCESS and CONVERT data to information

e.g. What are our

estimated production quantities?

e.g. What are our

material and labour

requirements?

e.g. How much

profit do we expect to make?

e.g. How much

does a specific product or

activity cost?

Management Accounting

OUTPUT

Management Accounting

How is it different from; 1. Financial Accounting?

2. Cost Accounting?

vs. FINANCIAL ACCOUNTING � Management Accounting à INTERNAL focus � Financial Accounting à EXTERNAL focus

vs. FINANCIAL ACCOUNTING Four (4) main differences:

MANAGEMENT ACCOUNTING FINANCIAL ACCOUNTING

1 Focus is on providing info. to users WITHIN the organisation e.g. Sales Manager.

Focus is on providing info. to users OUTSIDE the organisation e.g. shareholders & gov’t authorities.

2 Not required by law e.g. production forecast.

Required by law e.g. Statutory Accounts to be submitted to ASIC (specific accounting & auditing standards control reporting formats & content).

3 Focus dictated by the info. needs of the business and may be broad or narrow e.g. on a particular product or cost centre of ABC Ltd.

Focus is on the organisation as a whole e.g. ITR for ABC Ltd

4 More concerned about what is likely to happen in the future.

Past performance is the primary focus.

vs. COST ACCOUNTING � Cost accounting à NARROW focus � Management accounting à BROAD focus MANAGEMENT ACCOUNTING includes cost accounting i.e. COST ACCOUNTING is a subset of the management accounting system. COST ACCOUNTING relates to the planning and control of activities across the organisation.

vs. COST ACCOUNTING

MANAGEMENT ACCOUNTING

Budgeting &

forecasting

Cost accounting

Performance reporting

PLAN and CONTROL

FORMULATE corporate GOALS

+ ACTION to be taken to

reach those goals

Continuous COMPARISON of ACTUAL vs. BUDGET or

STANDARD à VARIANCE

Provides basis on which to implement corrective action

vs. COST ACCOUNTING Some EXAMPLES of the different types of TASKS / OUTPUTS for each role…

MANAGEMENT ACCOUNTANT COST ACCOUNTANT

Resource acquisition & disposal analysis

Provide info. about the cost of a product or service

Revenue forecasting Prepare the costings associated with a specific activity, department or cost centre

Project management Analyse the results of historical business operations

Capital investment analysis

2.1 Cost Concepts 1. The relationship between ACTIVITY and COST 2. Cost classification � Fixed costs vs. Variable costs � Unit cost � Service cost � Product cost vs. Period cost � Conversion cost

3. The manufacturing process � Direct vs. Indirect costs � Factory overhead 4. Types of inventories

The relationship between ACTIVITY and COST

The measurement of activities is the key organising principle for studying management accounting

information.

Organisational activities ACTIVITIES provide the link between spending on resources (people, equipment, materials etc.) and the products or services delivered to customers.

The relationship between ACTIVITY and COST

� Effective methods of cost control involve understanding � what causes costs and � what activities add value.

� A value added activity is one that, if eliminated, would reduce the product's service potential to the customer.

� A non-value added activity is an activity that presents opportunities for cost reduction without reducing the product's service potential to the customer.

The relationship between ACTIVITY and COST

� A COST can be defined as something of value (e.g. money) given up in exchange for something else (e.g. a good or service).

� Costs incurred necessitate the use of scarce resources.

� Therefore, the efficient operation of the organisation depends on management being fully and accurately informed about costs.

Cost Classification (FIXED vs. VARIABLE costs)

FIXED COSTS in total do not vary (in the short run) with changing levels of activity. � The cost per unit decreases as activity increases. � This relationship is constant within the relevant range of activity. � e.g. factory rent

Fixed Costs

Cost Classification (FIXED vs. VARIABLE costs)

VARIABLE COSTS in total vary (in the short run) with changing levels of activity. � Remain the same per unit over the relevant range. � e.g. direct labour

Variable Costs

Cost Classification

UNIT COST = the cost of manufacturing one unit of production. Example:

n Costs incurred for the month amount to $10,000. n During the month 1,000 units are produced. n The unit cost of production for the month is $10.00 per

unit.

Components of unit cost MANUFACTURING

ORGANISATION SERVICE

ORGANISATION

Direct materials Other direct expenses (or costs)

Direct labour Labour costs

Factory overhead Overhead costs

Cost Classification

SERVICE COST usually includes direct labour and overhead costs. The output of a service organisation (e.g. tax advice) has to be used up at the time it is made available, that is, it cannot be stored and sold later on like a manufactured good.

Cost Classification (PRODUCT vs. PERIOD costs)

PRODUCT COST = the cost of converting raw materials into a finished product e.g. toy boxes.

MANUFACTURING or PRODUCT costs include: (1) Direct materials e.g. cardboard (2) Direct labour (3) Factory overhead

Cost Classification (PRODUCT vs. PERIOD costs)

PERIOD COSTS include all other costs associated with the business (i.e. expired costs).

1. Marketing/selling/distribution expenses 2. General and admin. expenses 3. Financial expenses

FLOW OF PRODUCT AND PERIOD COSTS (refer to your text p.44)

Cost Classification PRIME COST

= the DIRECT cost associated with the manufacture of a product = DIRECT material + DIRECT labour

Cost Classification CONVERSION COST

= the cost associated with the conversion of raw materials into finished goods = Direct labour + Factory overhead

The Manufacturing Process

Is about converting raw materials into finished goods with the use of

direct labour and factory overhead.

The Manufacturing Process

The Manufacturing Process

WORK IN PROGRESS

MATERIALS

LABOUR

OVERHEADS

FINISHED GOODS

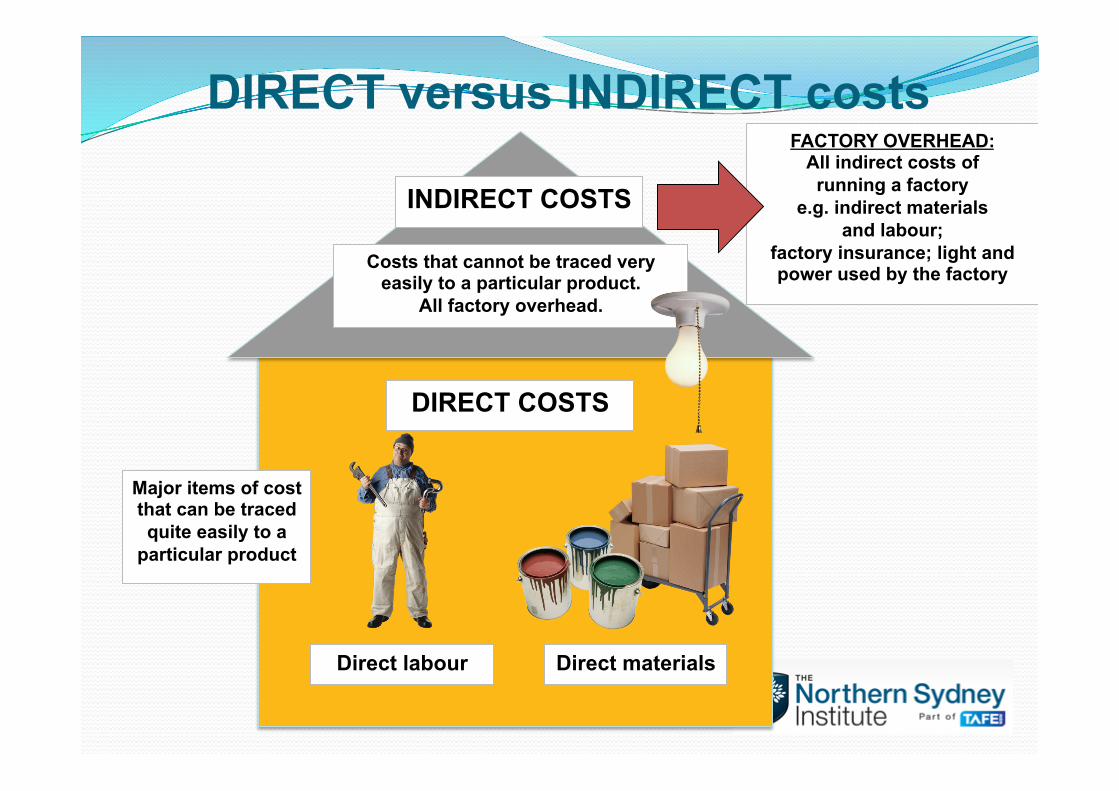

DIRECT versus INDIRECT costs

DIRECT COSTS

Direct labour Direct materials

Costs that cannot be traced very easily to a particular product.

All factory overhead.

INDIRECT COSTS

Major items of cost that can be traced quite easily to a

particular product

FACTORY OVERHEAD: All indirect costs of running a factory

e.g. indirect materials and labour;

factory insurance; light and power used by the factory

Cost Classification Summary

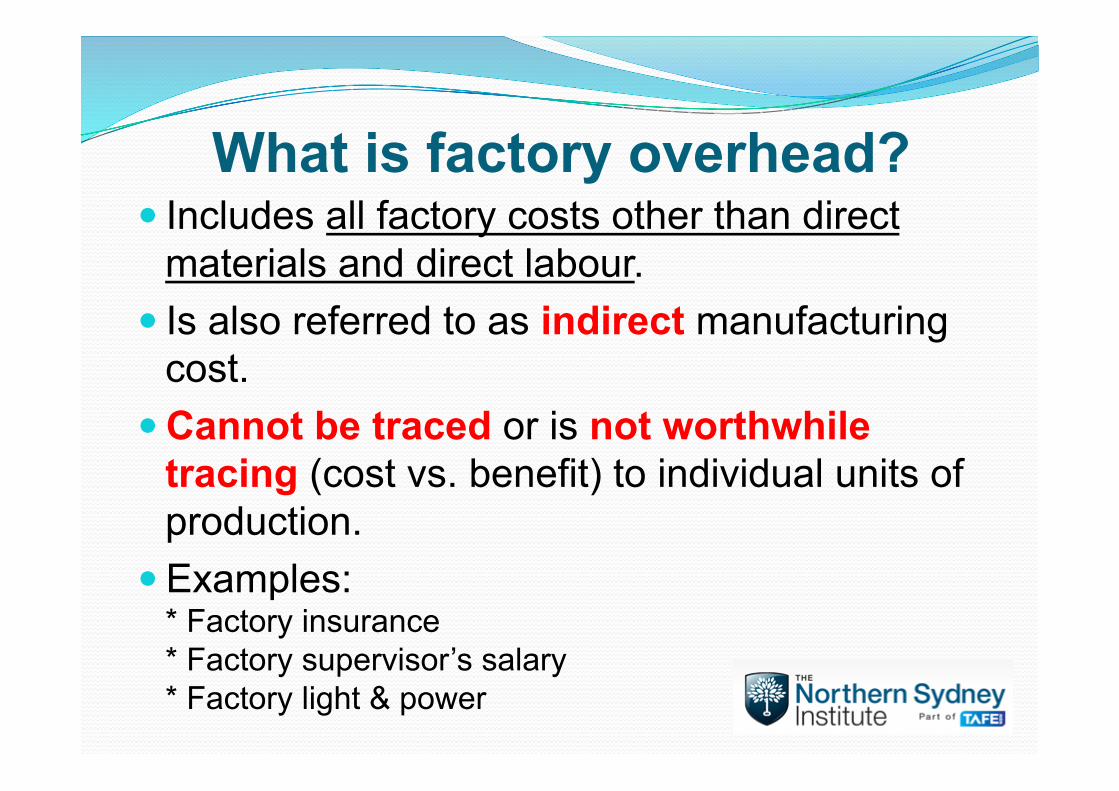

What is factory overhead? � Includes all factory costs other than direct

materials and direct labour. � Is also referred to as indirect manufacturing

cost. � Cannot be traced or is not worthwhile

tracing (cost vs. benefit) to individual units of production.

� Examples: * Factory insurance * Factory supervisor’s salary * Factory light & power

What do we do with factory overhead?

� Although factory overhead costs cannot be traced (or are not worthwhile tracing) to individual units of production, the TOTAL FACTORY OVERHEAD COST incurred MUST BE ALLOCATED to individual units of production REGARDLESS.

� This means that each product has to be charged with an estimated amount of factory overhead which is expected to cover the actual TOTAL cost incurred.

� How do we do this? You’ll find out in week 14…

Types of inventories � Materials includes stocks of raw material and

factory supplies e.g. lubricating oils for machinery.

� Work-in-progress are partly completed goods that will be completed in the future e.g. cardboard pieces cut out and ready to be glued.

� Finished goods are fully completed products ready for sale e.g. toy boxes.

Clip

* STUDENT ACTIVITY * Copy and paste the following URL into your Internet browser and watch

this YouTube Clip which takes you for a tour of the Ferrari Factory in Maranello, Italy. See if you can identify and name at least one example of DIRECT MATERIAL, DIRECT LABOUR and FACTORY OVERHEAD.

http://www.youtube.com/watch?v=La73Oy9ZGVw

2.2 Other Key Concepts 1. Sales Volume 2. Sales Mix 3. Mark-up (calculation of selling price) 4. Contribution margin 5. Contribution margin ratio 6. Gross profit ratio 7. Break-even point

Sales Volume Describes the physical quantity of units sold

Sales Mix Refers to the mix of sales and/or services where a company sells more than one product or provides more than one type of service.

Selling Price � In determining the selling price of a product the firm

aims to recover any costs incurred so that it can make a profit.

� This is why many pricing decisions are made on the basis of cost, with SELLING PRICE being determined using a percentage mark-up on cost.

Calculation of selling price � Some of the things you would consider when

deciding how much to sell a product for: � Any relevant supply and demand considerations. � The likely actions of competitors. � The company’s market share objectives. � The firm’s profit objectives.

Mark-up (and selling price) A method used to determine the selling price of a product is to add a percentage to the original cost of the product. The formula to use is: SELLING PRICE = COST + (COST x MARK-UP %)

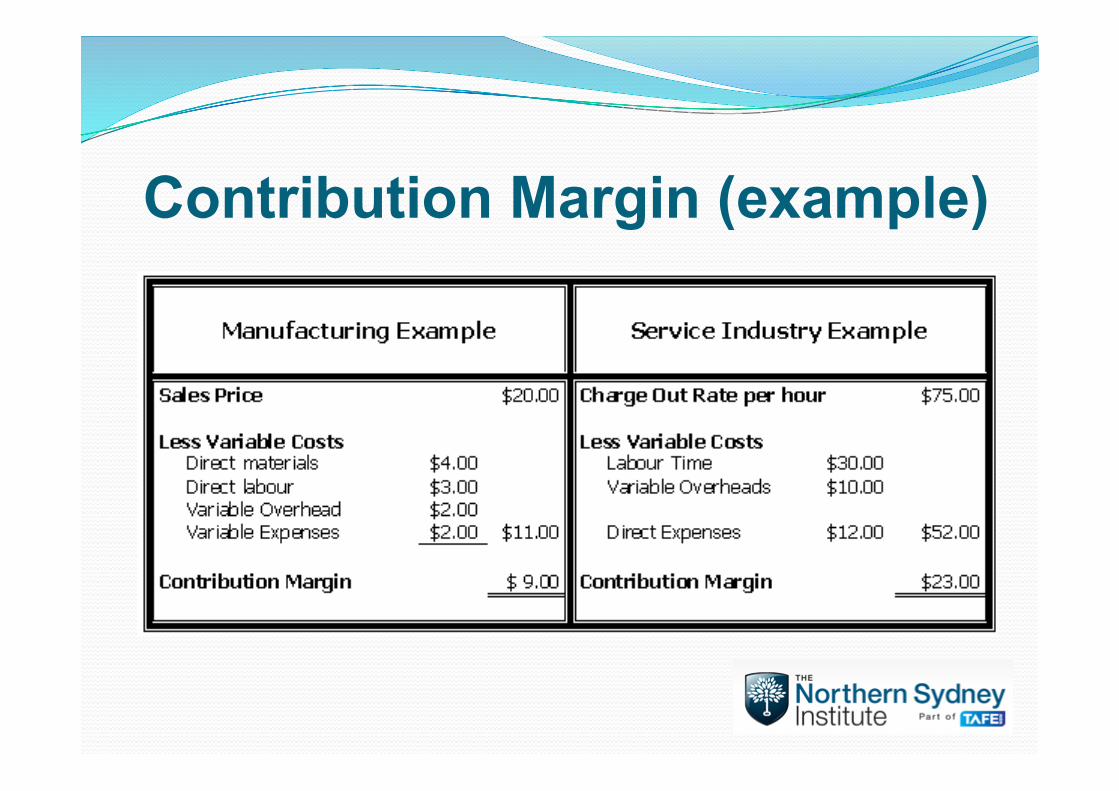

Contribution Margin

CONTRIBUTION MARGIN =

SALES less VARIABLES COSTS

It represents the amount that is available to cover (or contribute towards) FIXED COSTS and NET PROFIT.

Contribution Margin (example)

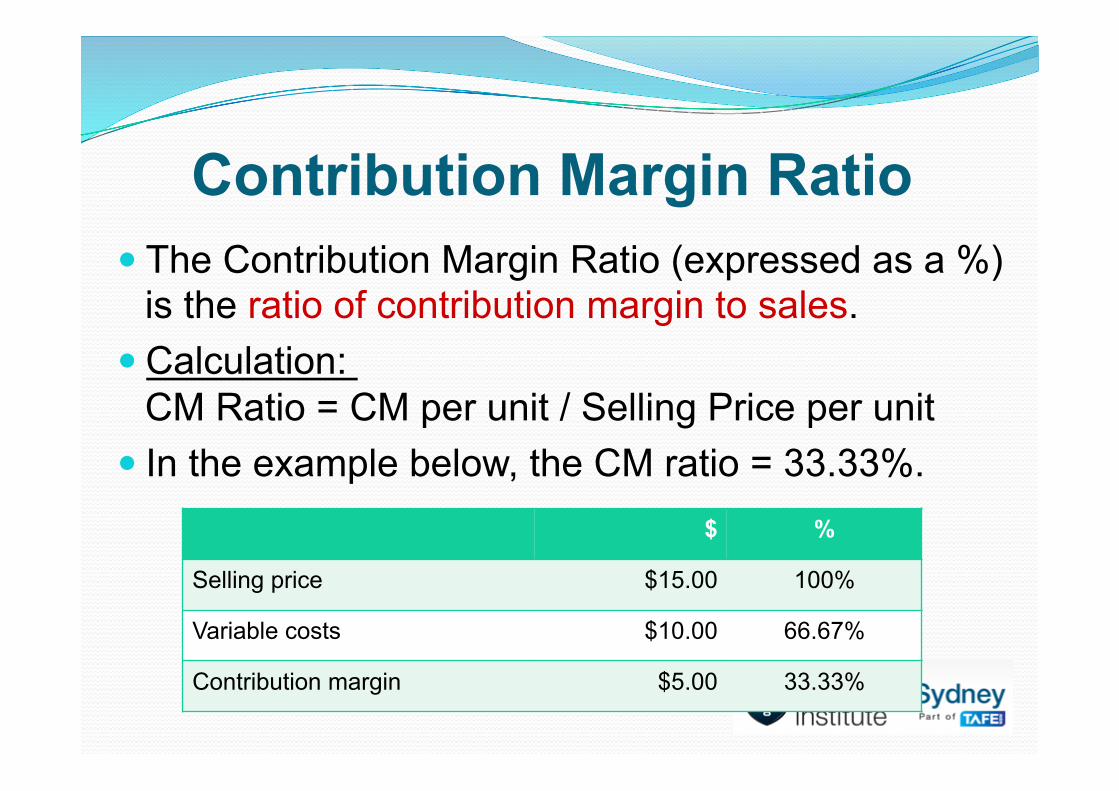

Contribution Margin Ratio � The Contribution Margin Ratio (expressed as a %)

is the ratio of contribution margin to sales. � Calculation:

CM Ratio = CM per unit / Selling Price per unit � In the example below, the CM ratio = 33.33%.

$ %

Selling price $15.00 100%

Variable costs $10.00 66.67%

Contribution margin $5.00 33.33%

Gross Profit Rate � The Gross Profit Rate (expressed as a %)

discloses the GROSS PROFIT as a percentage of SALES REVENUE.

� Calculation: GP rate = Gross Profit / Sales Revenue

Gross Profit Rate (example) In the example below, the GROSS PROFIT RATE = 40%."

Break-Even Point � This is the point at which

TOTAL REVENUES = TOTAL COSTS resulting in no profit or loss for the organisation.

� We will cover this in more detail when we do CHAPTER 8.

COSTS REVENUES

3. Cost Estimation High Low Analysis

Understanding the basics about cost estimation � Mixed costs have both a fixed portion and a variable portion. � Various methods are used to separate mixed costs out into these two manageable groups – this is what is referred to as cost estimation. � By separating mixed costs out into these two manageable groups, we can then use these cost groups to prepare budgets (planning) and predict and control costs (control) because we understand how these costs behave at various activity levels within the relevant range.

3. Cost Estimation High Low Analysis

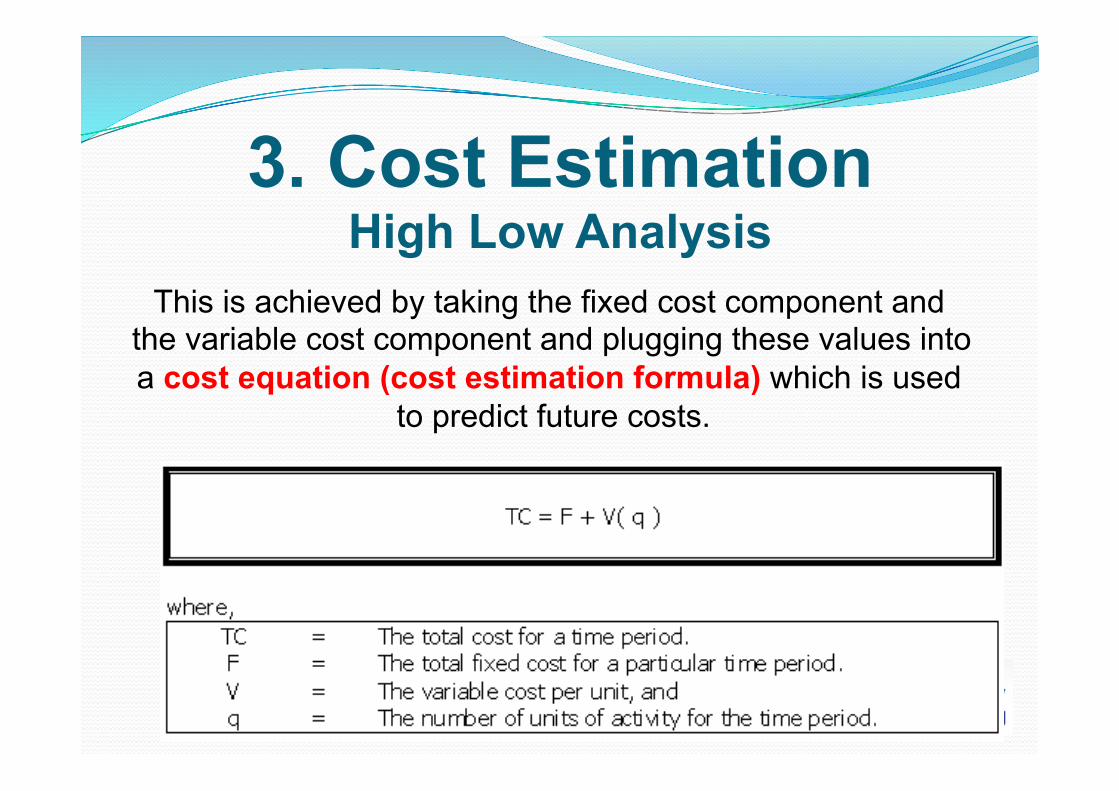

This is achieved by taking the fixed cost component and the variable cost component and plugging these values into a cost equation (cost estimation formula) which is used

to predict future costs.

3. Cost Estimation High Low Analysis

We are going to learn how to use what is called the

HIGH-LOW METHOD of cost estimation.

3. Cost Estimation High Low Analysis

Understanding how the high-low method of cost estimation works � The high-low method uses the highest and lowest activity levels over a period of time and within the relevant range to estimate the portion of a mixed cost that is variable and the portion that is fixed. � The amounts determined for each are only estimates. � Because it uses only the high and low activity levels to calculate the variable & fixed costs, it may be misleading if the high and low activity levels are not representative of the normal activity and this may distort the actual expectation of costs in the future. � The high-low method is most accurate when the high and low levels of activity are representative of the majority of the other points given.

3. Cost Estimation High Low Analysis

What do we mean by the term ‘relevant range’? This is the range of activity over which the firm expects a set of cost behaviour patterns to hold. e.g. a relevant range of activity may be between 10,000 and 20,000 units. Within this range, certain costs are expected to remain fixed while others will vary.

3. Cost Estimation High Low Analysis

Estimates of fixed and variables costs apply only if the desired level of activity is within the relevant range. If the firm considers an alternative at level of activity outside the relevant range, then the breakdown of overhead cost into its fixed and variables components needs to be worked out again.

High Low Analysis : Example At full capacity, Print ‘n Run can produce 4,000 units weekly at a total manufacturing cost of $50,000. Current production level is 3,000 units per week. The total manufacturing cost at this production level is $40,000. Required: 1. Use the high-low method to calculate:

1.1 Variable cost per unit 1.2 Total fixed cost per week

2. Calculate the expected total weekly cost if 3,600 units were produced.

High Low Analysis : SOLUTION PART 1.1 Activity Cost Highest activity 4,000 units $50,000 LESS: Lowest activity 3,000 units $40,000 Difference 1,000 units $10,000 Variable cost per unit = $10,000 / 1,000 units = $10.00 per unit

PART 1.2 Highest Lowest Total cost $50,000 40,000 LESS: Variable cost $40,000

($10 x 4,000 units) $30,000

($10 x 3,000 units) Fixed cost per week $10,000 $10,000

High Low Analysis : SOLUTION PART 2 Variable cost ($10 per unit x 3,600 units)

$36,000

Fixed cost $10,000 Total weekly cost $46,000

This week’s homework � Get a copy of the textbook � Read chapter 1 à Cost Concepts � Complete homework questions (chapter 1)

(ref. STUDENT ONLINE STUDY GUIDE)

You are now ready to start the next lesson on:

Chapter 3

Manufacturing &

Trading Statements

![ASA-CICBV Business Valuation Conference Deferred Revenue ... · Power Holdings, Inc] ... party’s stand alone selling price, management’s best estimate of stand along selling price,](https://static.fdocuments.us/doc/165x107/5fb0e86061ef096cc67e2d76/asa-cicbv-business-valuation-conference-deferred-revenue-power-holdings-inc.jpg)