Webcast 1Q10

20

1 1 Conference Call / Webcast Almir Guilherme Barbassa CFO and Investor Relations Officer May 18 th , 2010 Results Announcement 1 st Quarter 2010 (Brazilian Corporate Law)

-

Upload

petrobras -

Category

Investor Relations

-

view

511 -

download

0

Transcript of Webcast 1Q10

11

Conference Call / Webcast

Almir Guilherme Barbassa CFO and Investor Relations OfficerMay 18th, 2010

Results Announcement1st Quarter 2010

(Brazilian Corporate Law)

22

DISCLAIMERDISCLAIMER

The presentation may contain forecasts about future events. Such forecasts merely reflect the expectations of the Company's management. Such terms as "anticipate", "believe", "expect", "forecast", "intend", "plan", "project", "seek", "should", along with similar or analogous expressions, are used to identify such forecasts. These predictions evidently involve risks and uncertainties, whether foreseen or not by the Company. Therefore, the future results of operations may differ from current expectations, and readers must not base their expectations exclusively on the information presented herein. The Company is not obliged to update the presentation/such forecasts in light of new information or future developments.

The United States Securities and Exchange Commission permits oil and gas companies, in their filings with the SEC, to disclose only proved reserves that a company has demonstrated by actual production or conclusive formation tests to be economically and legally producible under existing economic and operating conditions. We use certain terms in this presentation, such as oil and gas resources, that the SEC’s guidelines strictly prohibit us from including in filings with the SEC.

CAUTIONARY STATEMENT FOR US INVESTORS

33

o EBITDA was R$ 15.1 billion increasing 5% when compared 1Q10 vs 4Q09. Net Income increased 4% in comparison to 4Q09, achieving R$ 7.7 bilhões

o Higher production with daily oil and LGN production record of 2,084 thous. in April

o Total Capex in this quarter reached R$ 17,753 million

o Start up of EWT in Tiro and Sídon, Santos Basin (03/2010)

o Oil discoveries in post-salt and pre-salt in Barracuda field (Campos Basin - 02/2010) and light oil in Piranema field (Sergipe Basin - 03/2010)

o Approval of CAPEX range between US$ 200-220 billion for 2010-2014 Business Plan (03/2010) and capitalization process by Board of Directors to be completed by July/2010

HIGHLIGHTS:HIGHLIGHTS:First quarter highlightsFirst quarter highlights

4

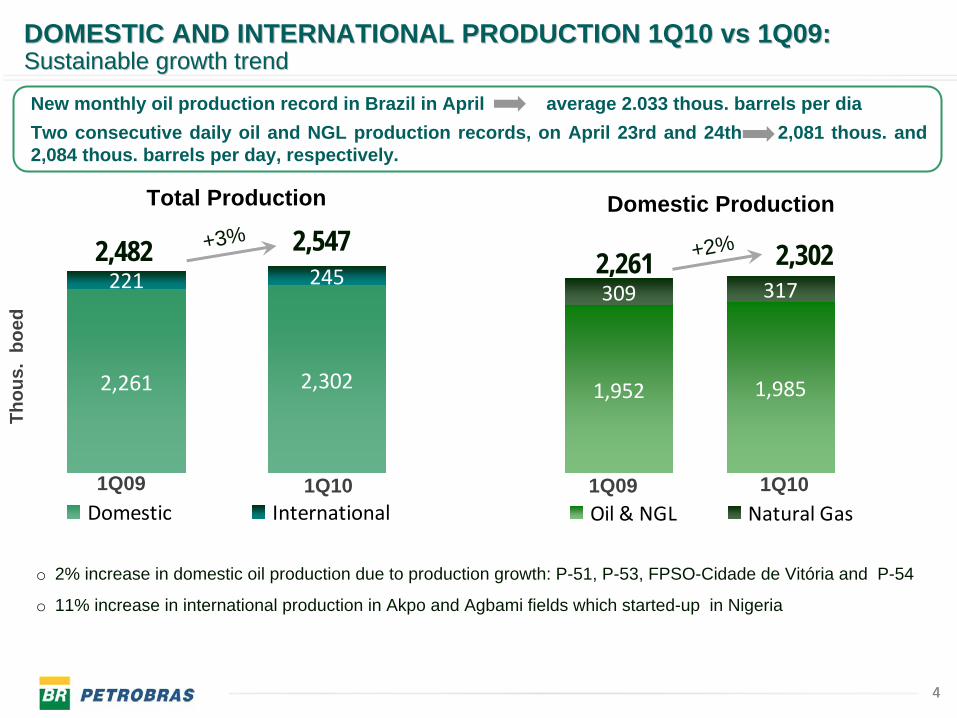

221 245

2,3022,261

Domestic International

309 317

1,9851,952

Oil & NGL Natural Gas

Domestic ProductionTotal Production

1Q09 1Q10

+3%

Thou

s. b

oed

1Q09

+2%2,482 2,547

1Q10

2,261 2,302

o 2% increase in domestic oil production due to production growth: P-51, P-53, FPSO-Cidade de Vitória and P-54

o 11% increase in international production in Akpo and Agbami fields which started-up in Nigeria

4

New monthly oil production record in Brazil in April average 2.033 thous. barrels per diaTwo consecutive daily oil and NGL production records, on April 23rd and 24th 2,081 thous. and 2,084 thous. barrels per day, respectively.

DOMESTIC AND INTERNATIONAL PRODUCTION 1Q10 DOMESTIC AND INTERNATIONAL PRODUCTION 1Q10 vsvs 1Q09:1Q09:SustainableSustainable growthgrowth trendtrend

55

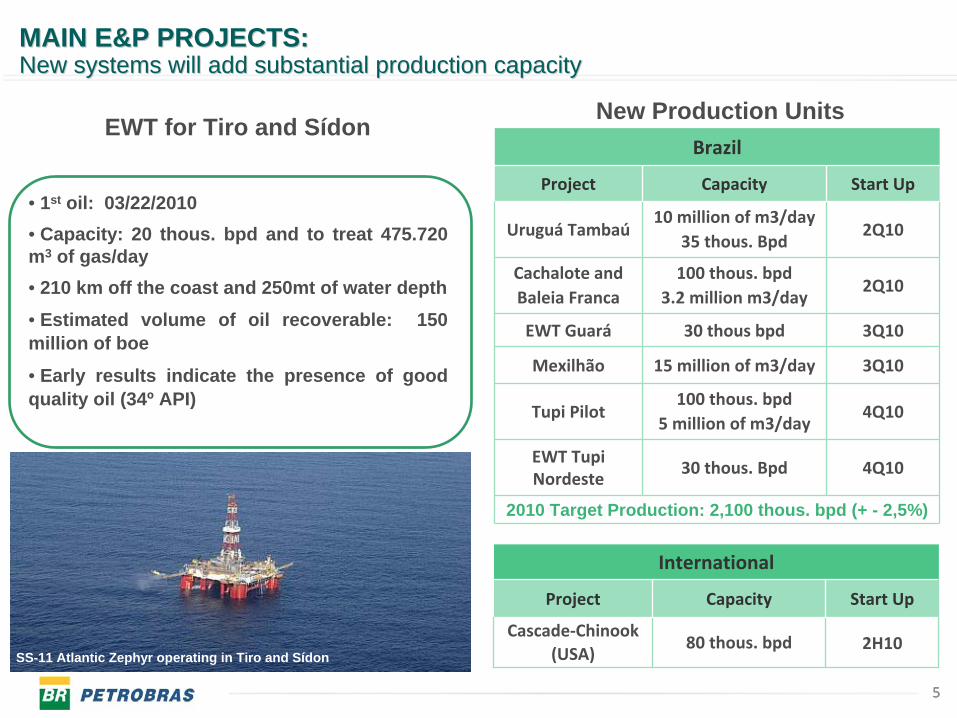

• 1st oil: 03/22/2010 • Capacity: 20 thous. bpd and to treat 475.720 m3 of gas/day• 210 km off the coast and 250mt of water depth• Estimated volume of oil recoverable: 150 million of boe

• Early results indicate the presence of good quality oil (34º API)

EWT for Tiro and Sídon

SS-11 Atlantic Zephyr operating in Tiro and Sídon

Brazil

Project Capacity Start Up

Uruguá

Tambaú10 million

of

m3/day35 thous. Bpd

2Q10

Cachalote andBaleia Franca

100 thous. bpd3.2 million

m3/day2Q10

EWT Guará 30 thous

bpd 3Q10

Mexilhão 15 million

of

m3/day 3Q10

Tupi Pilot100 thous. bpd

5 million

of

m3/day4Q10

EWT Tupi

Nordeste

30 thous. Bpd 4Q10

2010 Target Production: 2,100 thous. bpd (+ - 2,5%)

New Production Units

International

Project Capacity Start Up

Cascade‐Chinook(USA)

80 thous. bpd 2H10

MAIN E&P PROJECTS:MAIN E&P PROJECTS:New systems will add substantial production capacityNew systems will add substantial production capacity

6

PRODUÇÃO 2010

Tupi

Guará

Tupi NETupi Alto

Macunaíma

Guará Norte

FrancoLibra

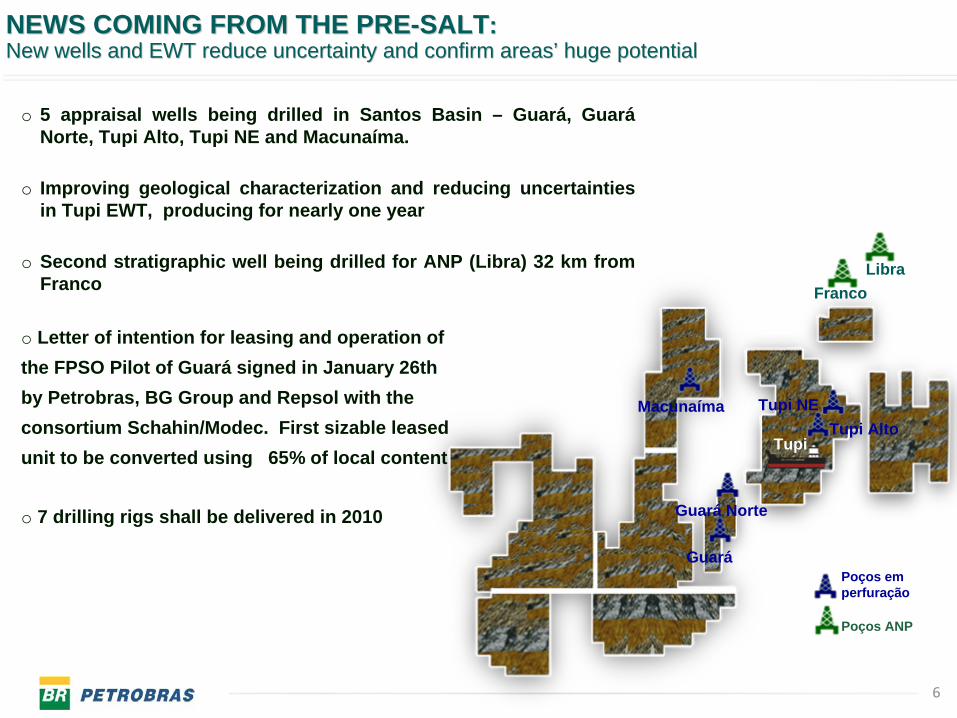

o 5 appraisal wells being drilled in Santos Basin – Guará, Guará Norte, Tupi Alto, Tupi NE and Macunaíma.

o Improving geological characterization and reducing uncertainties in Tupi EWT, producing for nearly one year

o Second stratigraphic well being drilled for ANP (Libra) 32 km from Franco

Poços em perfuração

Poços ANP

o Letter of intention for leasing and operation of the FPSO Pilot of Guará signed in January 26th by Petrobras, BG Group and Repsol with the consortium Schahin/Modec. First sizable leased unit to be converted using 65% of local content

o 7 drilling rigs shall be delivered in 2010

NEWS COMING FROM THE PRENEWS COMING FROM THE PRE--SALTSALT::New wells and EWT reduce uncertainty and confirm areasNew wells and EWT reduce uncertainty and confirm areas’’ huge potentialhuge potential

7

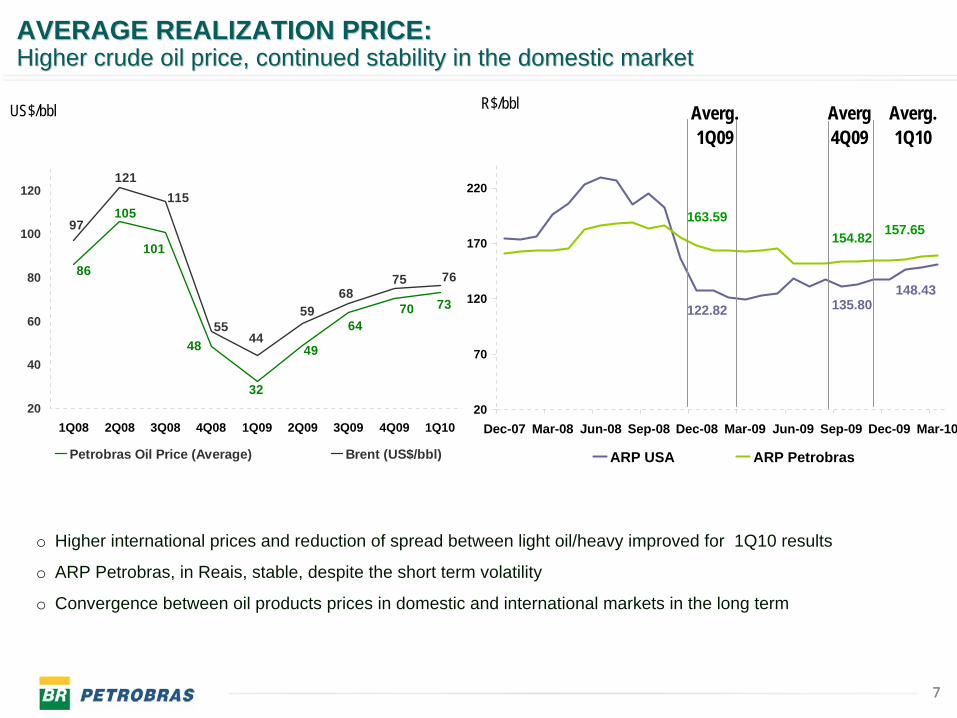

20

70

120

170

220

Dec-07 Mar-08 Jun-08 Sep-08 Dec-08 Mar-09 Jun-09 Sep-09 Dec-09 Mar-10

ARP USA ARP Petrobras

7

R$/bbl

o Higher international prices and reduction of spread between light oil/heavy improved for 1Q10 results

o ARP Petrobras, in Reais, stable, despite the short term volatility

o Convergence between oil products prices in domestic and international markets in the long term

7064

101

105

86

48

32

49

73

4455

115121

97

5968

75 76

20

40

60

80

100

120

1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10

Petrobras Oil Price (Average) Brent (US$/bbl)

Averg4Q09

Averg.1Q10

Averg.1Q09

US$/bbl

148.43135.80122.82

163.59154.82 157.65

AVERAGE REALIZATION PRICE:AVERAGE REALIZATION PRICE:Higher crude oil price, continued stability in the domestic markHigher crude oil price, continued stability in the domestic marketet

8

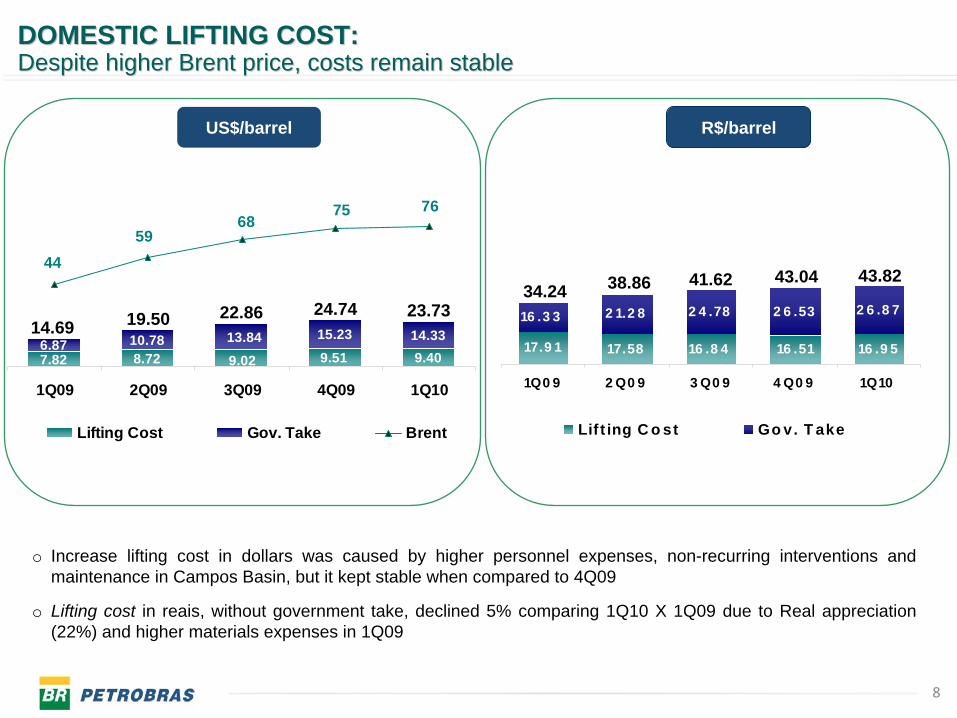

R$/barrel

9.408.727.82 9.02 9.5114.3310.786.87 13.84 15.23

75 7668

5944

1Q09 2Q09 3Q09 4Q09 1Q10

Lifting Cost Gov. Take Brent

17.9 1 17.58 16 .8 4 16 .51 16 .9 5

16 .3 3 2 1.2 8 2 4 .78 2 6 .53 2 6 .8 7

1Q0 9 2 Q0 9 3 Q0 9 4 Q0 9 1Q10

Lif t ing C o st Go v. T ake

34.24 38.86 41.62 43.04 43.82

14.69 19.50 22.86 24.74 23.73

US$/barrel

o Increase lifting cost in dollars was caused by higher personnel expenses, non-recurring interventions and maintenance in Campos Basin, but it kept stable when compared to 4Q09

o Lifting cost in reais, without government take, declined 5% comparing 1Q10 X 1Q09 due to Real appreciation (22%) and higher materials expenses in 1Q09

DOMESTIC LIFTING COST:DOMESTIC LIFTING COST:Despite higher Brent price, costs remain stableDespite higher Brent price, costs remain stable

9

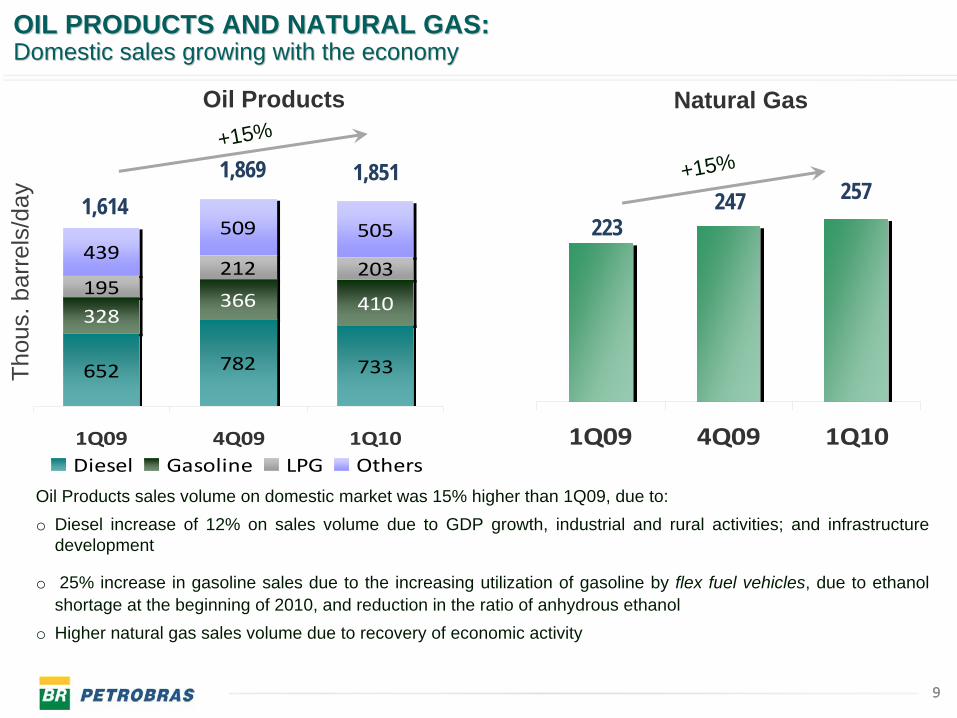

1Q09 4Q09 1Q10

+15%

247 257223

9

Oil Products sales volume on domestic market was 15% higher than 1Q09, due to:o Diesel increase of 12% on sales volume due to GDP growth, industrial and rural activities; and infrastructure

development

o 25% increase in gasoline sales due to the increasing utilization of gasoline by flex fuel vehicles, due to ethanol shortage at the beginning of 2010, and reduction in the ratio of anhydrous ethanol

o Higher natural gas sales volume due to recovery of economic activity

Natural Gas

Thou

s. b

arre

ls/d

ay

652 782 733

366195

212 203439

509 505

410328

1Q09 4Q09 1Q10Diesel Gasoline LPG Others

Oil Products

1,6141,869 1,851+15%

OIL PRODUCTS AND NATURAL GAS:OIL PRODUCTS AND NATURAL GAS: Domestic sales growing with the economyDomestic sales growing with the economy

10

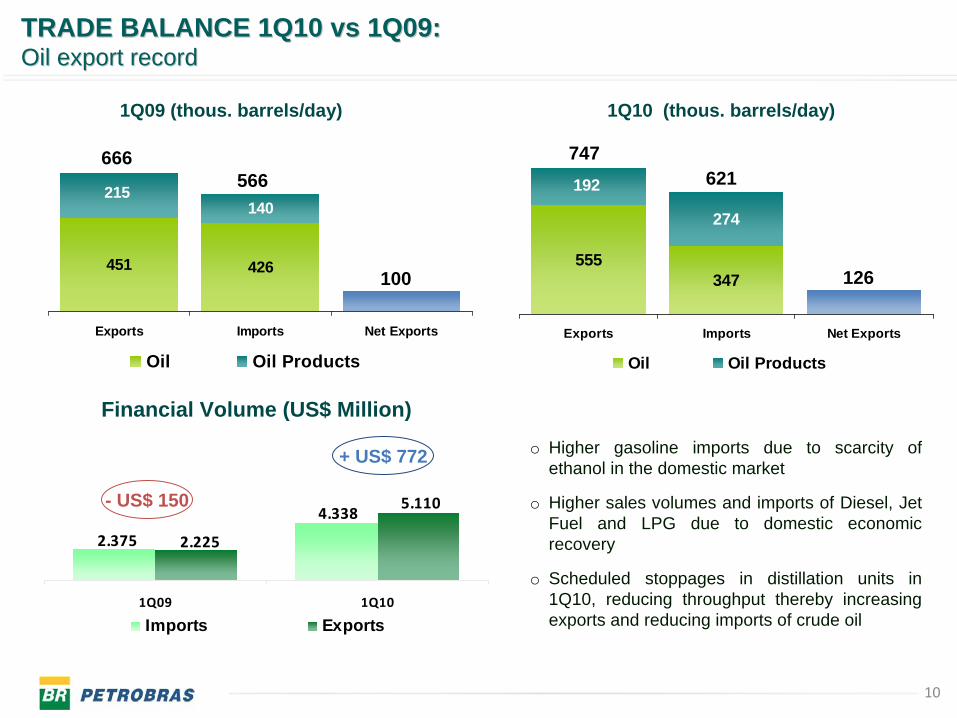

1Q09 (thous. barrels/day)

o Higher gasoline imports due to scarcity of ethanol in the domestic market

o Higher sales volumes and imports of Diesel, Jet Fuel and LPG due to domestic economic recovery

o Scheduled stoppages in distillation units in 1Q10, reducing throughput thereby increasing exports and reducing imports of crude oil

451 426

140215

Exports Imports Net Exports

Oil Oil Products

1Q10 (thous. barrels/day)

555

274

347

192

Exports Imports Net Exports

Oil Oil Products

747621

126100

566666

2.375

4.338

2.225

5.110

1Q09 1Q10

Imports Exports

Financial Volume (US$ Million)

- US$ 150

+ US$ 772

TRADE BALANCE 1Q10 TRADE BALANCE 1Q10 vsvs 1Q09:1Q09:OilOil exportexport recordrecord

11

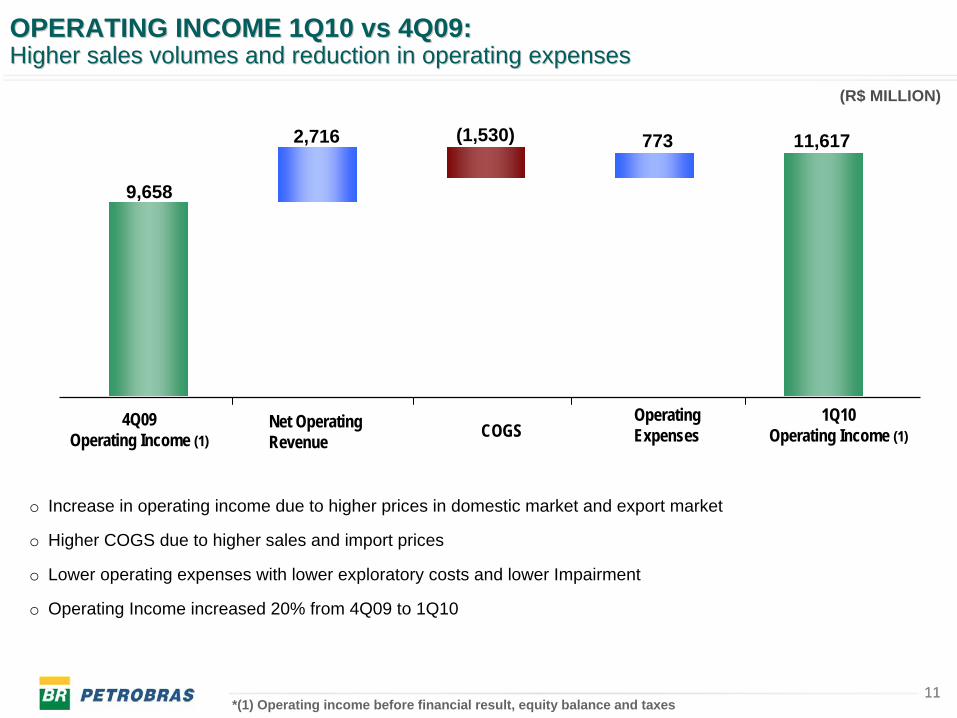

OPERATING INCOME 1Q10 vs 4Q09:OPERATING INCOME 1Q10 vs 4Q09:HigherHigher salessales volumes volumes andand reductionreduction in in operatingoperating expensesexpenses

(R$ MILLION)

4Q09Operating Income (1)

Net Operating Revenue COGS

Operating Expenses

1Q10Operating Income (1)

11*(1) Operating income before financial result, equity balance and taxes

9,658

2,716 (1,530) 773 11,617

o Increase in operating income due to higher prices in domestic market and export market

o Higher COGS due to higher sales and import prices

o Lower operating expenses with lower exploratory costs and lower Impairment

o Operating Income increased 20% from 4Q09 to 1Q10

12

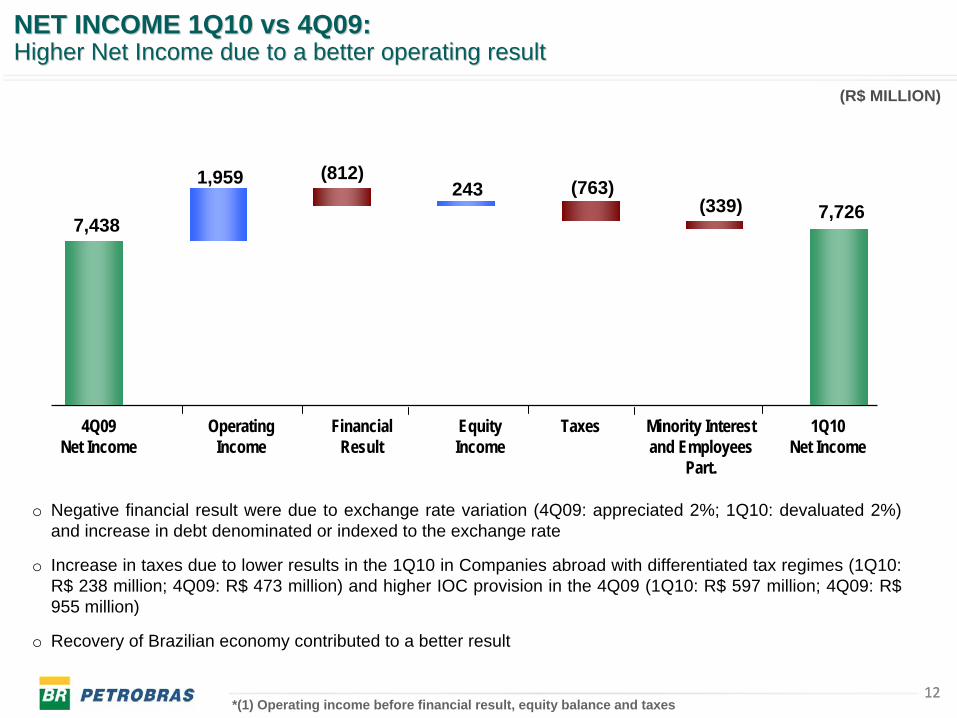

(R$ MILLION)

12

7,438

1,959 (812)243 (763)

(339) 7,726

1Q10Net Income

4Q09Net Income

Taxes Minority Interest and Employees

Part.

Financial Result

Equity Income

Operating Income

*(1) Operating income before financial result, equity balance and taxes

o Negative financial result were due to exchange rate variation (4Q09: appreciated 2%; 1Q10: devaluated 2%) and increase in debt denominated or indexed to the exchange rate

o Increase in taxes due to lower results in the 1Q10 in Companies abroad with differentiated tax regimes (1Q10: R$ 238 million; 4Q09: R$ 473 million) and higher IOC provision in the 4Q09 (1Q10: R$ 597 million; 4Q09: R$ 955 million)

o Recovery of Brazilian economy contributed to a better result

NET INCOME 1Q10 vs 4Q09:NET INCOME 1Q10 vs 4Q09:HigherHigher Net Net IncomeIncome duedue to a to a betterbetter operatingoperating resultresult

13

(R$ MILLION)

13

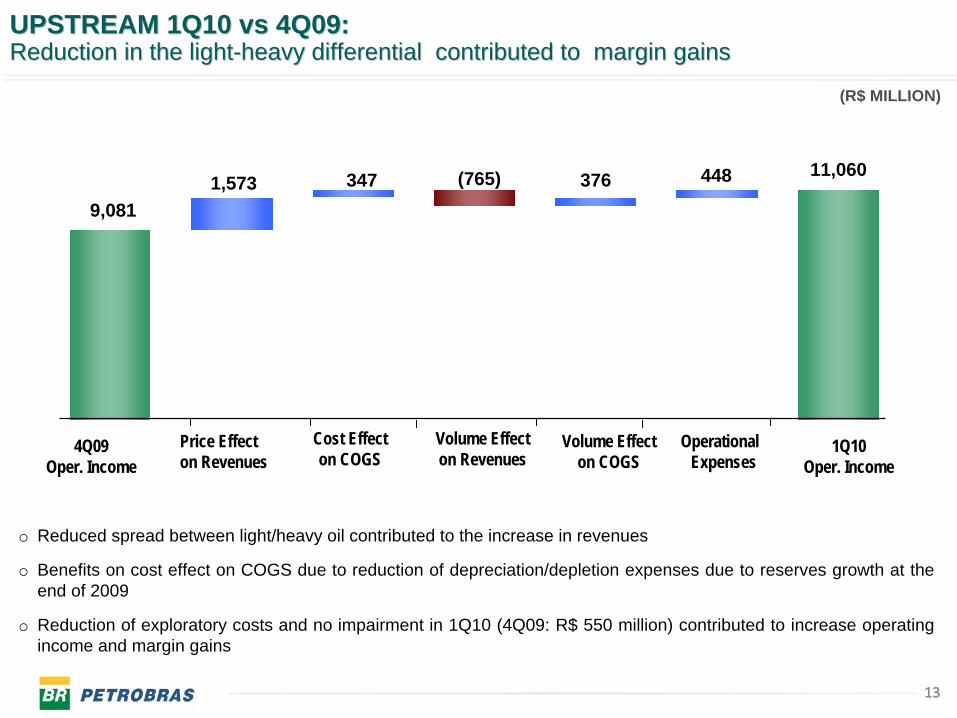

9,0811,573 (765)347 376 448 11,060

4Q09Oper. Income

1Q10Oper. Income

Price Effect on Revenues

Volume Effecton Revenues

Cost Effecton COGS

OperationalExpenses

Volume Effecton COGS

o Reduced spread between light/heavy oil contributed to the increase in revenues

o Benefits on cost effect on COGS due to reduction of depreciation/depletion expenses due to reserves growth at the end of 2009

o Reduction of exploratory costs and no impairment in 1Q10 (4Q09: R$ 550 million) contributed to increase operating income and margin gains

UPSTREAM UPSTREAM 1Q10 vs 4Q09: 1Q10 vs 4Q09: ReductionReduction in in thethe lightlight--heavyheavy differentialdifferential contributedcontributed to to marginmargin gainsgains

14

(R$ MILLION)

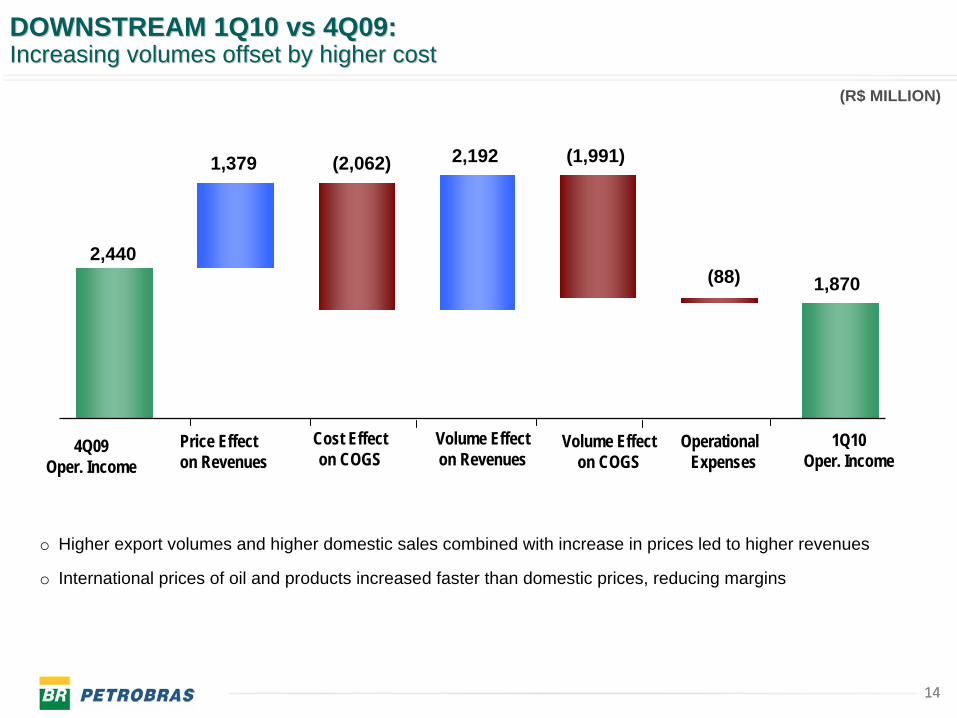

14

2,440

1,379 2,192(2,062) (1,991)

(88) 1,870

4Q09Oper. Income

1Q10Oper. Income

Price Effect on Revenues

Volume Effecton Revenues

Cost Effecton COGS

OperationalExpenses

Volume Effecton COGS

o Higher export volumes and higher domestic sales combined with increase in prices led to higher revenues

o International prices of oil and products increased faster than domestic prices, reducing margins

DOWNSTREAM 1Q10 DOWNSTREAM 1Q10 vsvs 4Q09:4Q09:Increasing volumes offset by higher costIncreasing volumes offset by higher cost

15

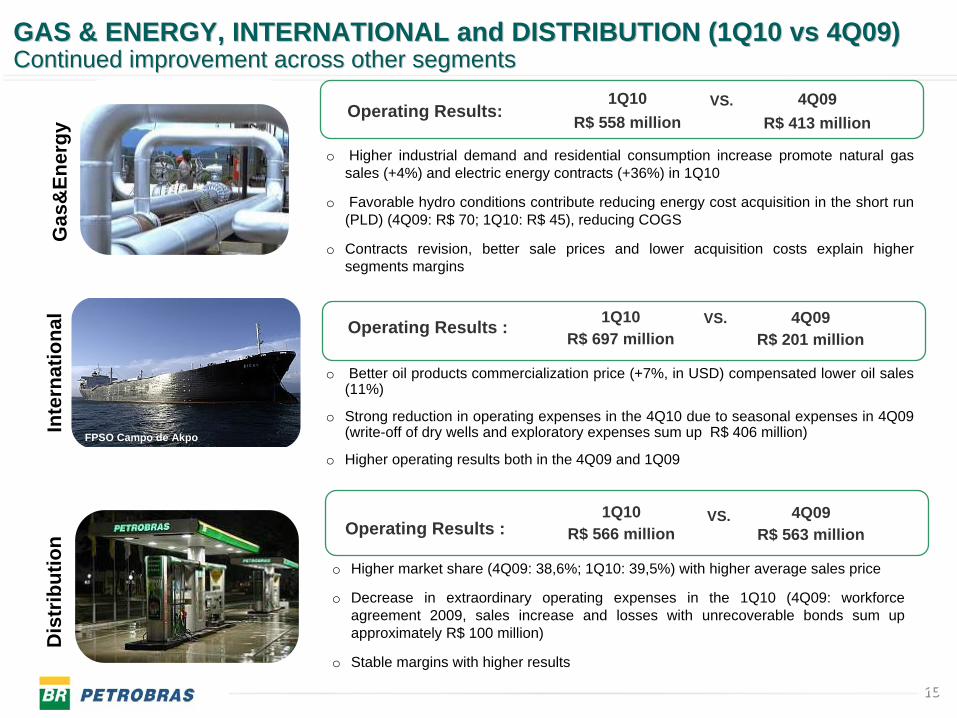

GAS & ENERGY, INTERNATIONAL and DISTRIBUTION (1Q10 GAS & ENERGY, INTERNATIONAL and DISTRIBUTION (1Q10 vsvs 4Q09)4Q09)Continued improvement across other segmentsContinued improvement across other segments

15

Gas

&En

ergy

Inte

rnat

iona

lD

istr

ibut

ion

Operating Results:1Q10

R$ 558 million4Q09

R$ 413 millionVS.

Operating Results : 1Q10R$ 697 million

4Q09R$ 201 million

VS.

Operating Results :1Q10

R$ 566 million4Q09

R$ 563 millionVS.

FPSO Campo de Akpo

o Higher industrial demand and residential consumption increase promote natural gas sales (+4%) and electric energy contracts (+36%) in 1Q10

o Favorable hydro conditions contribute reducing energy cost acquisition in the short run (PLD) (4Q09: R$ 70; 1Q10: R$ 45), reducing COGS

o Contracts revision, better sale prices and lower acquisition costs explain higher segments margins

o Better oil products commercialization price (+7%, in USD) compensated lower oil sales (11%)

o Strong reduction in operating expenses in the 4Q10 due to seasonal expenses in 4Q09 (write-off of dry wells and exploratory expenses sum up R$ 406 million)

o Higher operating results both in the 4Q09 and 1Q09

o Higher market share (4Q09: 38,6%; 1Q10: 39,5%) with higher average sales price

o Decrease in extraordinary operating expenses in the 1Q10 (4Q09: workforce agreement 2009, sales increase and losses with unrecoverable bonds sum up approximately R$ 100 million)

o Stable margins with higher results

16

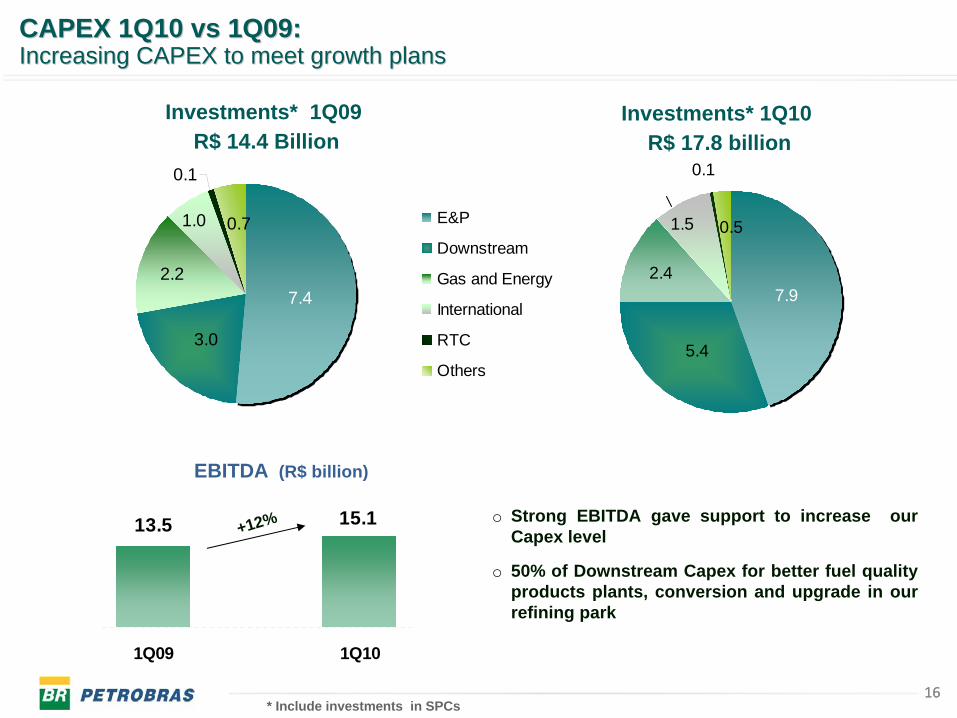

Investments* 1Q09 R$ 14.4 Billion

5,6

6,1

24,710,1

0,05

1,3

1,1

3,8

CAPEX 1Q10 CAPEX 1Q10 vsvs 1Q09:1Q09:Increasing CAPEX to meet growth plansIncreasing CAPEX to meet growth plans

Investments* 1Q10R$ 17.8 billion

5.4

1.5

7.92.4

0.1

0.5

3.0

1.0

7.42.2

0.1

0.7 E&P

Downstream

Gas and Energy

International

RTC

Others

16* Include investments in SPCs

EBITDA (R$ billion)

+12% o Strong EBITDA gave support to increase our Capex level

o 50% of Downstream Capex for better fuel quality products plants, conversion and upgrade in our refining park

13.5 15.1

1Q09 1Q10

1717

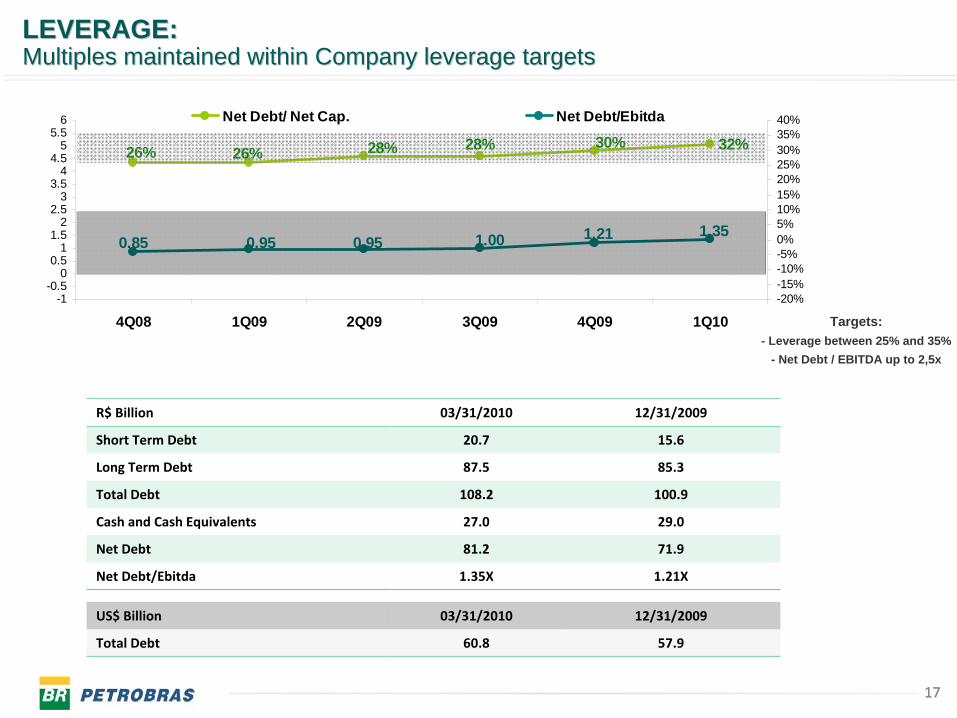

R$ Billion 03/31/2010 12/31/2009

Short Term Debt 20.7 15.6

Long Term Debt 87.5 85.3

Total Debt 108.2 100.9

Cash and Cash Equivalents 27.0 29.0

Net Debt 81.2 71.9

Net Debt/Ebitda 1.35X 1.21X

US$ Billion 03/31/2010 12/31/2009

Total Debt 60.8 57.9

26%26% 28% 28% 30% 32%

0.95 0.95 1.00 1.21 1.350.85

-1-0.5

00.5

11.5

22.5

33.5

44.5

55.5

6

4Q08 1Q09 2Q09 3Q09 4Q09 1Q10-20%-15%-10%-5%0%5%10%15%20%25%30%35%40%Net Debt/ Net Cap. Net Debt/Ebitda

LEVERAGE:LEVERAGE: Multiples maintained within Company leverage targets Multiples maintained within Company leverage targets

Targets:- Leverage between 25% and 35%

- Net Debt / EBITDA up to 2,5x

18

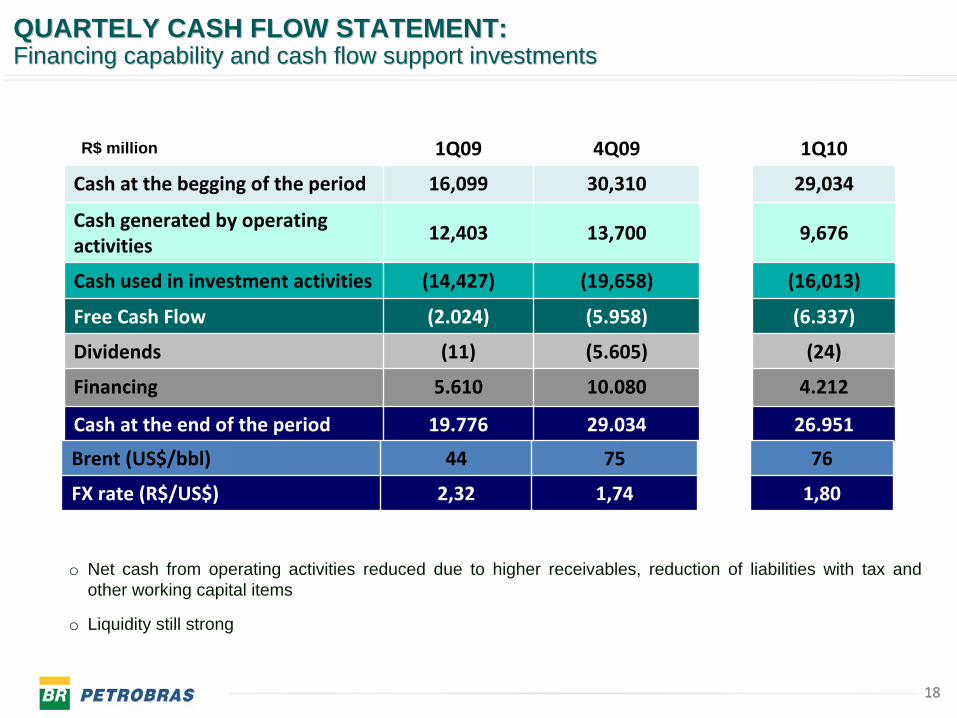

1Q09 4Q09 1Q10

Cash at the begging of the period 16,099 30,310 29,034

Cash generated by operating

activities12,403 13,700 9,676

Cash used in investment activities (14,427) (19,658) (16,013)

Free

Cash

Flow (2.024) (5.958) (6.337)

Dividends (11) (5.605) (24)

Financing 5.610 10.080 4.212

Cash at the end of the period 19.776 29.034 26.951

R$ million

o Net cash from operating activities reduced due to higher receivables, reduction of liabilities with tax and other working capital items

o Liquidity still strong

18

Brent (US$/bbl) 44 75 76

FX rate (R$/US$) 2,32 1,74 1,80

QUARTELY CASH FLOW STATEMENT:QUARTELY CASH FLOW STATEMENT:Financing capability and cash flow support investmentsFinancing capability and cash flow support investments

19

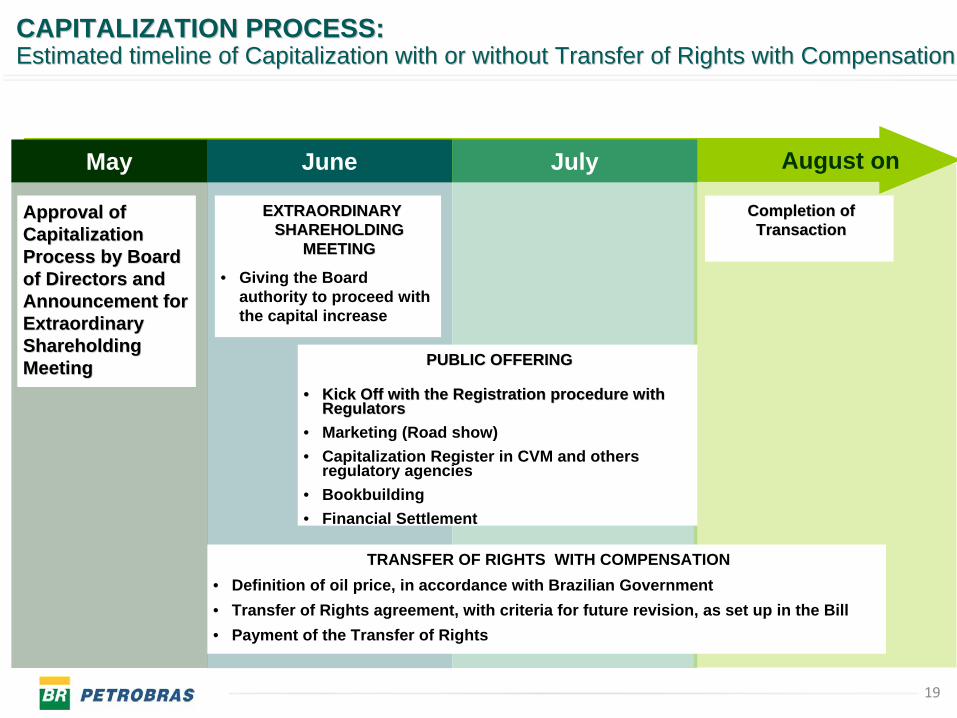

CAPITALIZATION PROCESS:CAPITALIZATION PROCESS:Estimated timeline of Capitalization with or without Transfer ofEstimated timeline of Capitalization with or without Transfer of Rights withRights with CompensationCompensation

Approval of Approval of Capitalization Capitalization Process by Board Process by Board of Directors and of Directors and Announcement for Announcement for Extraordinary Extraordinary Shareholding Shareholding MeetingMeeting

EXTRAORDINARY EXTRAORDINARY SHAREHOLDING SHAREHOLDING

MEETINGMEETING

• Giving the Board authority to proceed with the capital increase

August onMay July

Completion of Completion of TransactionTransaction

June

TRANSFER OF RIGHTS WITH COMPENSATION• Definition of oil price, in accordance with Brazilian Government• Transfer of Rights agreement, with criteria for future revision, as set up in the Bill• Payment of the Transfer of Rights

PUBLIC OFFERINGPUBLIC OFFERING

•• Kick Off with the Registration procedure with Kick Off with the Registration procedure with RegulatorsRegulators

• Marketing (Road show)• Capitalization Register in CVM and others

regulatory agencies• Bookbuilding• Financial Settlement