cdn102.files.wordpress.com · Web viewReference is invited to the Investment Guidelines for NPS...

82

ISSN: 2454-5562 Thamasoma Jyothirgamaya HARMONY AN E-MAGAZINE ON CSIR/GoI SERVICE & RELATED ISSUES Ch. Srinivasa Rao Founder-Editor Formerly CoA, CSIR-NGRI, Hyderabad Estd: Jan. 1993 -- 26th year in the service of our esteemed readeRs. Review: B.J. Acharyulu, Head, F&A, CDFD, Hyderabad Dream-weaver: D.S. Sundar, Assistant (F&A), CLRI, Chennai Orders of Central Govt. which are reproduced in "HARMONY" whether duly endorsed by the CSIR or not, are applicable to its employees to a large extent unless and otherwise such Orders involve financial implications. Articles on Service issues, Management, Motivation, Material Management, Behavioural aspects and related issues are welcome through E-mail or other means. May 2019 Vol. XXVI (289)

Transcript of cdn102.files.wordpress.com · Web viewReference is invited to the Investment Guidelines for NPS...

ISSN: 2454-5562

Thamasoma Jyothirgamaya

HARMONY AN E-MAGAZINE ON CSIR/GoI SERVICE & RELATED

ISSUES

Ch. Srinivasa RaoFounder-Editor

Formerly CoA, CSIR-NGRI, Hyderabad

Estd: Jan. 1993 -- 26th year in the service of our esteemed readeRs.

Review: B.J. Acharyulu, Head, F&A, CDFD, Hyderabad Dream-weaver: D.S. Sundar, Assistant (F&A), CLRI, Chennai

Orders of Central Govt. which are reproduced in "HARMONY" whether duly endorsed by the CSIR or not, are applicable to its employees to a large extent unless and otherwise such Orders involve financial implications.

Articles on Service issues, Management, Motivation, Material Management, Behavioural aspects and related issues are welcome through E-mail or other means.

Material published in “HARMONY” can be used with due acknowledgement purely in academic interest. The opinions expressed or inferences drawn in the material published in “HARMONY” do not necessarily reflect the views of Editor or CSIR, New Delhi/ Swamy Publishers (P) Ltd., Chennai. The Editor shall not take any responsibility whatsoever for any inaccuracies or claims. “HARMONY” is transmitted through E-mail. All are welcome to enlist for a copy.

face Book .com/harmonysrinivas E-mail: [email protected] / [email protected]

Mobile: 91-94904 62583 / : 040-2712 2528Res: Ch. Srinivasa Rao, H.No.42-267/1/3, Shramikanagar, Moula Ali, Hyderabad 500 040

May 2019 Vol. XXVI(289)

Please don't print this unless you really need to. Save Trees…

Amendment to the Investment Guidelines for NPS Schemes

Reference is invited to the Investment Guidelines for NPS Schemes (Scheme CG, Scheme SG, Corporate CG and NPS Lite schemes of NPS and Atal Pension Yojana) dated 3-6-2015 issued vide Circular No. PERDA/2015/16/PFM/7, the change in Investment Guidelines for National Pension Scheme with reference to Investment in equity Mutual Funds vide Circular No. PERDA/2018/56/PF/2 dated 20-8-2018 and revised rating criteria for investments under NPS Schemes vide Circular No. PERDA/2018/02/PF/02 dated 8-5-2018. The changes hereunder shall apply only to Scheme CG, Scheme SG, Corporate CG and NPS Lite schemes of NPS and Atal Pension Yojana.

2. In Order to provide flexibility to the Pension Funds to improve the Scheme performance depending upon the market conditions, it has been decided to increase the cap on Govt. Securities and related investments and Short term debt instruments and related investments by 5% each. 3. The asset class wise revised caps on the various asset classes are as under:

Asset Class Caps on Investments for Composite Schemes

Govt. Securities and related investments … Up to 55%Debt Instruments and related investments … Up to 45%Equity & related investments … Up to 15%Asset backed, trust structured, etc. … Up to 5%Short term debt instruments and related investments.. Up to 10%

4. The other terms and conditions as mentioned in the Circular No. PERDA/2015/ 16/PFM/7 dated 3-6-2015, Circular No. PERDA/2018/56/PF/2 dated 20-8-2018 and Circular No. PFRDA/2018/02/PF/02 dated 8-5-2018 shall remain the same.

5. This Circular is issued in exercise of power of the Authority under sub-clause (b) of the sub-Section (2) of Section 14 of PFRDA Act, 2013 read with regulation 14 and 43 of PFRDA (Pension Fund) Regulation, 2015 and is effective from 1-4-2019.

[PFRDA Circular No.PFRDA/2019/8/SUP-PF/2 dated 25-3-2019; www.govtempdiary.com]

Grant of One Notional Increment/Pension Benefits to Retirees who Retired on 30th June under CBIC

The above matter has been examined in the Board and after dismissal of SLP Dy. No.22283/2018 dated 23-7-2018, the matter was referred to the DoP&T for their advice. The DoP&T has advised to refer the matter to Department of Legal Affairs (DoLA) to explore the possibilities of review of the Hon’ble Supreme Court Order dated 23-7-

2

CSIR / Govt. of India Orders

2018 in the said SLP Dy. No.22238/2018. Hence, the matter has not attained finality as yet.

2. It is, therefore, informed that the final decision taken in the matter would be intimated in due course as and when the matter attains finality.

[GoI MoF DoR CBIT&C Lr. F. No.A-26017/16/2019-Ad.IIA dated 18-3-2018; www.govtempdiary.com]

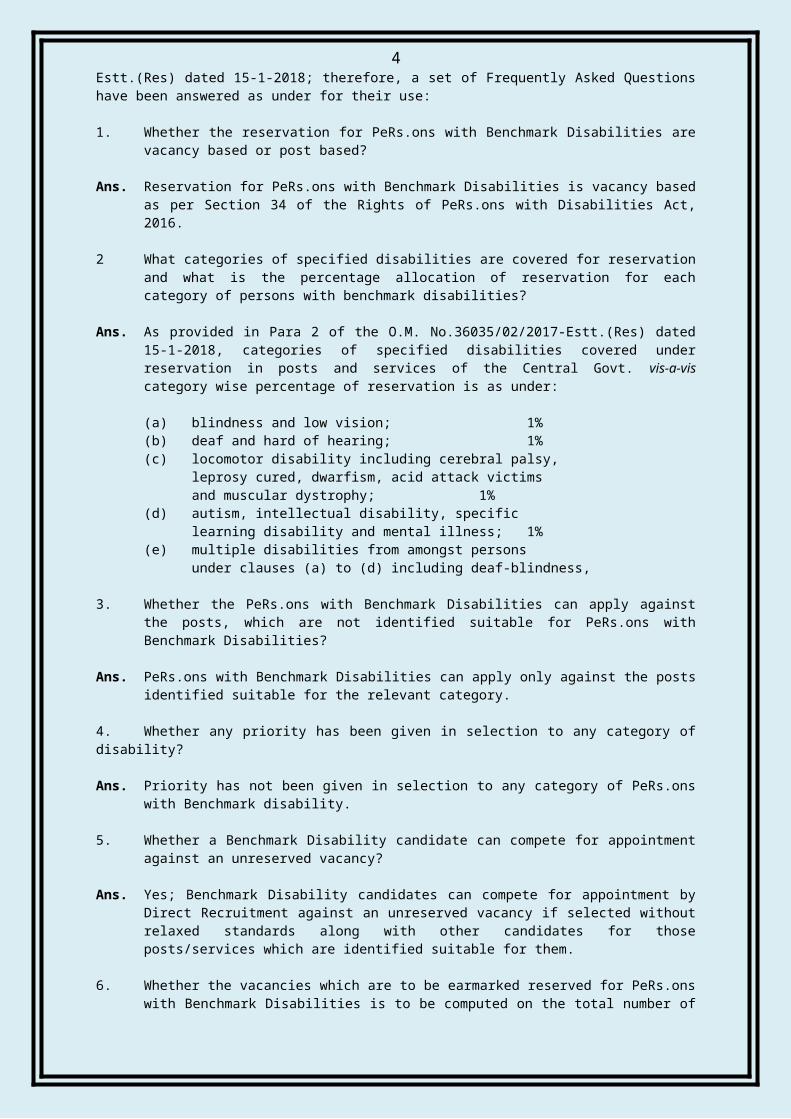

FAQs: Reservation to PeRs.ons with Benchmark Disabilities in Posts/Services under Central Govt.

The DoP&T receives references from various Ministries/Departments seeking clarification on instructions with regard to reservation for PeRs.ons with Benchmark Disabilities issued vide O.M. No.36035/02/2017-Estt.(Res) dated 15-1-2018; therefore, a set of Frequently Asked Questions have been answered as under for their use:

1. Whether the reservation for PeRs.ons with Benchmark Disabilities are vacancy based or post based?

Ans. Reservation for PeRs.ons with Benchmark Disabilities is vacancy based as per Section 34 of the Rights of PeRs.ons with Disabilities Act, 2016.

2 What categories of specified disabilities are covered for reservation and what is the percentage allocation of reservation for each category of persons with benchmark disabilities?

Ans. As provided in Para 2 of the O.M. No.36035/02/2017-Estt.(Res) dated 15-1-2018, categories of specified disabilities covered under reservation in posts and services of the Central Govt. vis-a-vis category wise percentage of reservation is as under:

(a) blindness and low vision; 1%(b) deaf and hard of hearing; 1%(c) locomotor disability including cerebral palsy,

leprosy cured, dwarfism, acid attack victims and muscular dystrophy; 1%

(d) autism, intellectual disability, specific learning disability and mental illness; 1%

(e) multiple disabilities from amongst persons under clauses (a) to (d) including deaf-blindness,

3. Whether the PeRs.ons with Benchmark Disabilities can apply against the posts, which are not identified suitable for PeRs.ons with Benchmark Disabilities?

Ans. PeRs.ons with Benchmark Disabilities can apply only against the posts identified suitable for the relevant category.

4. Whether any priority has been given in selection to any category of disability?

Ans. Priority has not been given in selection to any category of PeRs.ons with Benchmark disability.

5. Whether a Benchmark Disability candidate can compete for appointment against

an unreserved vacancy?

Ans. Yes; Benchmark Disability candidates can compete for appointment by Direct Recruitment against an unreserved vacancy if selected without relaxed standards along with other candidates for those posts/services which are identified suitable for them.

3

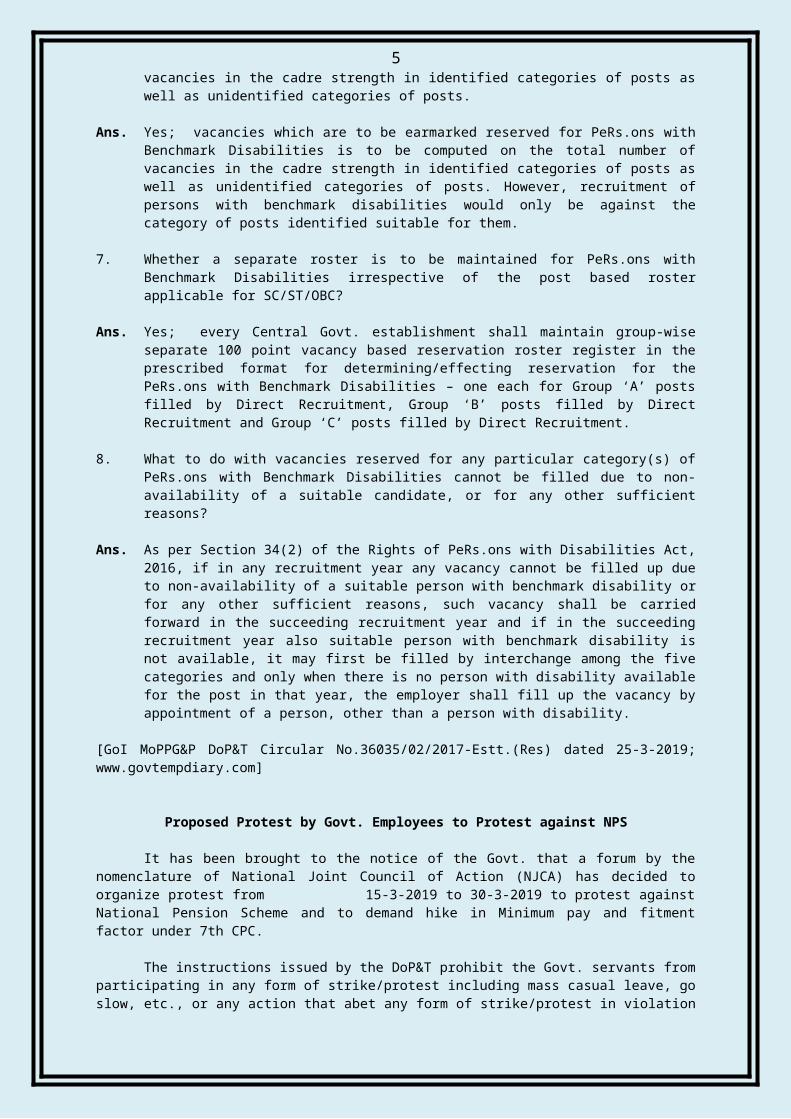

6. Whether the vacancies which are to be earmarked reserved for PeRs.ons with Benchmark Disabilities is to be computed on the total number of vacancies in the cadre strength in identified categories of posts as well as unidentified categories of posts.

Ans. Yes; vacancies which are to be earmarked reserved for PeRs.ons with Benchmark Disabilities is to be computed on the total number of vacancies in the cadre strength in identified categories of posts as well as unidentified categories of posts. However, recruitment of persons with benchmark disabilities would only be against the category of posts identified suitable for them.

7. Whether a separate roster is to be maintained for PeRs.ons with Benchmark Disabilities irrespective of the post based roster applicable for SC/ST/OBC?

Ans. Yes; every Central Govt. establishment shall maintain group-wise separate 100 point vacancy based reservation roster register in the prescribed format for determining/effecting reservation for the PeRs.ons with Benchmark Disabilities – one each for Group ‘A’ posts filled by Direct Recruitment, Group ‘B’ posts filled by Direct Recruitment and Group ‘C’ posts filled by Direct Recruitment.

8. What to do with vacancies reserved for any particular category(s) of PeRs.ons with Benchmark Disabilities cannot be filled due to non-availability of a suitable candidate, or for any other sufficient reasons?

Ans. As per Section 34(2) of the Rights of PeRs.ons with Disabilities Act, 2016, if in any recruitment year any vacancy cannot be filled up due to non-availability of a suitable person with benchmark disability or for any other sufficient reasons, such vacancy shall be carried forward in the succeeding recruitment year and if in the succeeding recruitment year also suitable person with benchmark disability is not available, it may first be filled by interchange among the five categories and only when there is no person with disability available for the post in that year, the employer shall fill up the vacancy by appointment of a person, other than a person with disability.

[GoI MoPPG&P DoP&T Circular No.36035/02/2017-Estt.(Res) dated 25-3-2019; www.govtempdiary.com]

Proposed Protest by Govt. Employees to Protest against NPS

It has been brought to the notice of the Govt. that a forum by the nomenclature of National Joint Council of Action (NJCA) has decided to organize protest from 15-3-2019 to 30-3-2019 to protest against National Pension Scheme and to demand hike in Minimum pay and fitment factor under 7th CPC.

The instructions issued by the DoP&T prohibit the Govt. servants from participating in any form of strike/protest including mass casual leave, go slow, etc., or any action that abet any form of strike/protest in violation of Rule 7 of the CCS (Conduct) Rules, 1964. Besides, in accordance with the proviso to Rule 17(I) of the Fundamental Rules, pay and allowances is not admissible to an employee for his absence from duty without any authority. As to the concomitant rights of an Association after it is formed, they cannot be different from the rights which can be claimed by the individual members of which the Association is composed. It follows that the right to form an Association does not include any guaranteed right to strike/protest.

There is no statutory provision empowering the employees to go on strike. The Supreme Court has also agreed in several judgements that going on a strike/performing any sort of protest is a grave misconduct under the Conduct Rules and that misconduct by the Govt. employees is required to be dealt with in accordance with law. Any employee going on strike/protest in any form would face the consequences which, besides deduction of wages, may also include appropriate disciplinary action. Kind

4

attention of all employees of the DoP&T is also drawn to the DoP&T O.M. No.33012/ 1/(S)/2008 Estt.(B) dated 12-9-2008, on the subject for strict compliance (enclosed as Annexure-A).

All Officers are requested that the above instructions may be brought to the notice of the employees working under their control. All Officers are also requested not to sanction Casual Leave or any other kind of leave to the Officers and employees, if applied for, during the period of proposed Dharna/demonstration, and ensure that the willing employees are allowed hindrance free entry into the Office premises.

In case employees go on protest anytime during the period 15-3-2019 to 30-3-2019, all Divisional Heads are requested to forward a report indicating the number and details of employees, who are absent from duty during the period of said protest, i.e., from 15-3-2019 to 30-3-2019.

[GoI MoPPG&P DoP&T O.M. No.45018/1/2017-Vig. dated 26-3-2019; www.govtempdiary.com]

Judgement(s)/Order(s) of Hon’ble Supreme Court on Aadhaar-PAN for Filing Return of Income

As per clause (ii) of sub-Section (1) of Section 139AA of the Income-tax Act, 1961, with effect from 1-7-2017, every person who is eligible to obtain Aadhaar number has to quote the Aadhaar number in return of income.

2. In a series of judgments, i.e., (i) Binoy Viswam Vs. Union of India reported in (2017) 396 ITR 66 (ii) Final Judgment and Order of the Constitution Bench of Hon’ble Supreme Court dated 26-9-2018 in Justice K. S. Puttaswamy (Retd.) and another [Writ Petition (Civil) No. 494 of 2012]; and (iii) Shreya Sen & Anr. In SLP (Civil) Diary No(s) 34292/2018 dated 4-2-2019, Hon’ble Supreme Court has upheld validity of Section 139AA. 3. In light of the aforesaid judgement(s)/Order(s) of Hon’ble Supreme Court, from 1-4-2019 onwards, to give effect to the above judgements/Orders , it has been decided by the Board that provision of clause (ii) of sub-Section (1) of Section 139AA of the Act would be implemented and it is mandatory to quote Aadhaar while filing the return of income unless specifically exempted as per any notification issued under sub-Section (3) of Section 139AA of the Act. Thus, returns being filed either electronically or manually cannot be filed without quoting the Aadhaar number.

4. Returns which were filed prior to 1-4-2019 without quoting of Aadhaar number as an outcome of any decision of different High Courts in a specific case or returns which were filed during the period when the online functionality for filing the return without quoting of Aadhaar number was so available in the aftermath of decision of Delhi High Court dated 24-7-2018 in W.P. C.M 7444/2018 & C.M. Application No. 28499/2018 in case of Shreya Sen vs. Union of India & ORs., till it was withdrawn post decision of Constitution Bench of the Hon’ble Supreme Court dated 26-9-2018, would also be taken up for processing without causing any adverse consequence for non-quoting of Aadhaar as per provision of Section 139AA of the Act.

[GoI MoF DoR CBDT Circular No.6/2019 dated 31-3-2019; www.govtempdiary.com]

Simplification of Pension Procedure

The Scheme for Payment of Pensions to Central Govt. Civil Pensioners through Authorized Banks, issued by the Central Pension Accounting Office provides for an

5

Undertaking to be submitted by the retiring Govt. servant/pensioner to the pension disbuRs.ing Bank before commencement of pension. The pensioner undertakes to refund or make good any amount to which he is not entitled.

In view of the above DoP&PW issued instructions vide its O.M. No.1/27/2011-P&PW(E) dated 7-5-2014 which were also communicated through this Office O.M. No. CPAO/Tech/Simplification/2014-15/53 dated 28-5-2014. These provisions are reiterated below: (a) It has been established that the first payment of pension after retirement gets

delayed mainly due to two reasons. One, the delay in receipt of intimation by the pensioner that pension papers have reached the Bank and two, delay on part of the pensioner in approaching the Bank for submission of the Undertaking.

(b) The required Undertaking may be obtained by the Head of Office from the retiring Govt. servant along with Form 5 and other documents before his retirement. This Undertaking shall be forwarded to the pension disbuRs.ing Bank along with the Pension Payment Order by the Accounts Officer/CPAO following the usual procedure.

(c) The pensioner would no longer be required to visit the Bank to activate the first payment of pension. Therefore, after ascertaining that the Bank’s copy has been dispatched by the CPAO, the pensioner’s copy of the Pension Payment Order (PPO) may be handed over to him at the time of retirement along with other retirement dues. This should be feasible in all cases where the Govt. servant had submitted pension papers within the time-limits prescribed in the CCS (Pension) Rules, 1972.

(d) However, if any employee posted at a location away from the Office of the Head of Office or who for any other reasons feels that it would be more convenient to him to obtain his copy of the PPO from the Bank, may inform the Head of Office of his option in writing while submitting his pension papers.

Pension papers and Undertaking

Pay & Account Office/Head of Office should not wait for the copy of PPO (SSA) for confirmation of the dispatch of the same by CPAO to Bank for handing over of the pensioner’s copy to the retiring Govt. servant along with other retirement dues. PAO/Ho0 may confirm the dispatch of Bank’s Copy of PPO by visiting CPAO’s Website, i.e., www.cpao.nic.in -> see your PPO Status.

It has been observed that pensioner’s portion of the PPO is not being handed over to the pensioner, but being sent to the Bank through the CPAO. It seems that the timeline for submission of finalizing the pension cases as mentioned in the CCS (Pension) Rules, 1972 are not being adhered to by the HoO/PAO.

All the Pr. CCAs/CCA/CAs/AGs (with independent charge)/JS (Admin) are requested to issue instructions to all Pay and Accounts Offices/Head of Offices under their jurisdiction to ensure timely submission of pension papers so that the correct procedure is followed strictly. Timeline for finalization of pension cases as prescribed in CCS (Pension) Rules, 1972 is annexed herewith (not reproduced here).

[GoI MoF DoE CPAO O.M. No. CPAO/IT&Tech/11(Vol-VI)/Simplification/2018-19/01 dated 1-4-2019; www.gservants.com]

Replacement of Name of Erstwhile DGS&D by GeM (Govt. e-Marketplace) in GFRs2017

The undersigned is directed to refer Supply Division, Department of Commerce O.M. No. 1(1)/2018-Pol. dated 20-8-2018 proposing changes in GFRs, 2017 and to say

6

that the proposal of DoC has been examined and it has been decided with the approval of Finance Minister to make changes to the GFRs, 2017 as tabulated below:

S.No.

Existing Provisions of GFRs, 2017 Amended Rule

1. Rule 147: Power for procurement of goods:

The Ministries or Departments have been delegated full power to make their own arrangements for procurement of goods. In case, however, a Ministry or Department does not have the required expertise, it may project its indent to the Central Purchase Organisation (e.g. DGS&D) with the approval of competent authority. The indent form to be utilized for this purpose will be as per the standard form evolved by the Central Purchase Organisation.

Rule 147: Power for procurement of goods:

The Ministries or Departments have been delegated full power to make their own arrangements for procurement of goods and services, that are not available on GeM. Common use Goods and Services available on GeM are required to be procured mandatorily through GeM as per Rule 149.

2. Rule 149 Govt. e-Marketplace (GeM):

DGS&D or any other agency authorized by the Govt. will host an online Govt. e-Marketplace (GeM) for common use Goods and Services. DGS&D will ensure adequate publicity including periodic advertisement of the items to be procured through GeM for the prospective suppliers The Procurement of Goods and Services by Ministries or Departments will be mandatory for Goods or Services available on GeM. The credentials of suppliers on GeM shall be certified by DGS&D. The procuring authorities will certify the reasonability of rates. The GeM portal shall be utilized by the Govt. buyers for direct on-line purchases as under:

(i) Up to Rs.50,000/- through any of the available suppliers on the GeM, meeting the requisite quality, specification and delivery period. (ii) Above Rs.50,000/- and up to Rs.30,00,000/ through the GeM Seller having lowest price amongst the available sellers, of at least three different manufacturers, on GeM, meeting the requisite quality, specification and delivery period. The tools for online bidding and online reverse auction available on GeM can be used by the Buyer if decided by the competent authority.

Rule 149 Govt. e-Marketplace (GeM):

Govt. of India has established the Govt. e-Marketplace (GeM) for common use Goods and Services. GeM Special Purpose Vehicle (SPV) will ensure adequate publicity including periodic advertisement of the items to be procured through GeM for the prospective suppliers The Procurement of Goods and Services by Ministries or Departments will be mandatory for Goods or Services available on GeM. The credentials of suppliers on GeM shall be certified by GeM SPV. The procuring authorities will certify the reasonability of rates. The GeM portal shall be utilized by the Govt. buyers for direct on-line purchases as under:

(i) Up to Rs.25,000/- through any of the available suppliers on the GeM, meeting the requisite quality, specification and delivery period.

(ii) Above Rs.25,000/- and up to Rs.5,00,000/- through the GeM Seller having lowest price amongst the available sellers (excluding Automobiles where current limit of 30 lakh will continue), of at least three different manufacturers, on GeM, meeting the requisite quality, specification and delivery period. The tools for online bidding and online reverse auction available on GeM can be used by the Buyers even for procurements less than Rs.5,00,000.

(iii) Above Rs.5,00,000 through the

7

(iii) Above Rs.30,00,000/- through the supplier having lowest price meeting the requisite quality, specification and delivery period after mandatorily obtaining bids, using online bidding or reverse auction tool provided on GeM.

supplier having lowest price meeting the requisite quality, specification and delivery period after mandatorily obtaining bids, using online bidding or reverse auction tool provided on GeM (excluding Automobiles where current limit of 30.00 lakh will continue).

Note: There is no change in clauses (iv) to (viii).

3. Rule 150: Registration of suppliers:

(i) With a view to establishing reliable sources for procurement of goods commonly required for Govt. use, the Central Purchase Organisation (e.g. DGS&D) will prepare and maintain item-wise lists eligible and capable suppliers Such approved suppliers will be known as Registered suppliers All Ministries or Departments may utilise these lists as and when necessary. Such registered suppliers are prima facie eligible for consideration for procurement of goods through Limited Tender Enquiry. They are also ordinarily exempted from furnishing bid security along with their bids. A Head of Department may also register suppliers of goods which are specifically required by that Department or Office, periodically. Registration of the supplier should be done following a fair, transparent and reasonable procedure and after giving due publicity.

(v) The list of registered suppliers for the subject matter of procurement be exhibited on the Central Public Procurement Portal and Websites of the Procuring Entity/e-Procurement/portals.

Rule 150: Registration of suppliers:

(i) For goods and services not available on GeM, Head of Ministry/Department may also register suppliers of goods and services which are specifically required by that Department or Office, periodically. Registration of the supplier should be done following a fair, transparent and reasonable procedure and after giving due publicity. Such registered suppliers should be boarded on GeM as and when the item or service gets listed on GeM.

(v) The list of registered suppliers for the subject matter of procurement be exhibited on Websites of the Procuring Entity/e-Procurement portals.

Note: There is no change in clauses (ii) to (iv).

4. Rule 155: Purchase of Goods by Purchase Committee:

Purchase of goods costing above Rs.25,000/- (Rupees twenty five thousand only) and up to Rs.2,50,000/- (Rupees two lakh and fifty thousand only) each occasion may be made on the recommendations of a duly constituted Local Purchase Committee consisting of three members of an appropriate level as decided by the Head of the Department. The Committee will survey the market to ascertain the reasonableness of rate, quality and specifications and identify

Rule 155: Purchase of Goods by Purchase Committee:

In case a certain item is not available on the GeM portal, Purchase of goods costing above Rs.25,000/- (Rupees twenty five thousand only) and up to Rs.2,50,000/- (Rupees two lakh and fifty thousand only} on each occasion may be made on the recommendations of a duly constituted Local Purchase Committee consisting of three members of an appropriate level as decided by the Head of the Department. The Committee will survey the market to ascertain the

8

the appropriate supplier. Before recommending placement of the purchase Order, the members of the Committee will jointly record a Certificate as under:

"Certified that we, members of the Purchase Committee are jointly and individually satisfied that the goods recommended for purchase are of the requisite specification and quality, priced at the prevailing market rate and the supplier recommended is reliable and competent to supply the goods in question, and it is not debarred by Department of Commerce or Ministry/ Department concerned."

reasonableness of rate, quality and specifications and identify the appropriate supplier. Before recommending placement of the purchase Order, the members of the Committee will jointly record a Certificate as under:

“Certified that we, members of the Purchase Committee are jointly and individually satisfied that the goods recommended for purchase are of the requisite specification and quality, priced at the prevailing market rate and the supplier recommended is reliable and competent to supply the goods in question, and it is not debarred by Department of Commerce or Ministry/Department concerned."

Rule 225 (xiii):

Copies of all contracts and agreements for purchases of the value of Rupees Twenty-five Lakhs and above, and of all rate and running contracts entered into by civil Departments of the Govt. other than the Departments like the Directorate General of Supplies and Disposals for which a special audit procedure exists, should be sent to the Audit Officer and/or the Accounts Officer as the case may be.

Rule 225 (xiii):

Copies of all contracts and agreements for purchases of the value of Rupees Twenty-five Lakhs and above entered into by civil Departments of the Govt., should be sent to the Audit Officer and or the Accounts Officer as the case may be.

2. It has been also decided to delete Rules 148, 156, 159(iv), 160(iii), 173(xv) and 174(iv) of GFRs, 2017 related to rate contracts.

3. This O.M. is also available on our Website www.doe.gov.in -> Notification -> Circular --> Procurement Policy OM.

[GoI MoF DoE O.M. No.F.1/26/2018-PPD dated 2-4-2019; www.staffnews.in]

Maternity Benefit (Mines and Circus) Rules, 1963

G.S.R. 57(E).– Whereas a draft of certain Rules further to amend the Maternity Benefit (Mines and Circus) Rules 1963, among other Rules, were published as required by sub-Section (1) of Section 28 of the Maternity Benefit Act, 1961 (53 of 1961), in the Gazette of India, Extraordinary, Part II, Section 3, sub-Section (i) vide notification of the GoI in the MoL&E No. G.S.R.413(E) dated 23-4-2018, inviting objections and suggestions from all persons likely to be affected thereby, within a period of three months, from the date on which copies of Official Gazette containing the said notification were made available to the public;

And whereas copies of the said Official Gazette were made available to the general public on the 23-4-2018;

And whereas the objections and suggestions received on the said draft Rules from the public have been considered by the Central Govt.;

9

Now, therefore, in exercise of the power conferred by Section 28 of the said Act, the Central Govt. hereby makes the following Rules further to amend the Maternity Benefit (Mines and Circus) Rules, 1963, namely:

1. These Rules may be called the Maternity Benefit (Mines and Circus) Amendment Rules, 2019.

They shall come into force on the date of their publication in the Official Gazette.

2. In the Maternity Benefit (Mines and Circus) Rules, 1963, for Rule 16, the following Rule shall be substituted, namely:

‘16. Annual return.- (1) The employer of every mine or Circus shall, on or before the 1st day of February in each year, upload a unified annual return in Form X online on the Web portal of the Central Govt. in the Ministry of Labour and Employment, giving information as to the particulars specified, in respect of the preceding year:

Provided that during inspection, the inspector may require the production of accounts, books, register and other documents maintained in electronic form or otherwise

Explanation.- For the purposes of this sub-Rule, the expression “electronic form” shall have the same meaning as assigned to it in clause (r) of Section 2 of the Information Technology Act, 2000 (21 of 2000).

(2) If the employer of a mine or Circus to which the Act applies sells, abandons or discontinues the working of the mine or Circus, then, he shall, within one month of the date of such sale or abandonment or four months of the date of such discontinuance, as the case may be, upload online, on the Web portal of the Central Govt. in the Ministry of Labour and Employment, a further unified return in Form X referred to in sub-Rule (1) in respect of the period between the end of the preceding year and the date of the sale, abandonment or discontinuance.’

Note: The Maternity Benefit (Mines and Circus) Rules, 1963 was published in the Gazette of India vide Notification number G.S.R.1642, dated 5-10-1963 and lastly amended vide Notification No. G.S.R.435(E) dated 29-5-2015.

[GoI MoL&E Gazette Notification No.Z-20025/23/2018-LRC dated 29-1-2019; www.gconnect.in]

Extension of Validity Period of HCOs under CGHS

With reference to above mentioned subject attention is drawn to Office Order dated 20-12-2018 whereby empanelment of all existing empanelled Health Care Organizations (HCOs) under CGHS was extended till 31-3-2019.

In this regards it has been now decided to extend empanelment of all HCOs already empanelled under CGHS for a further period of three months w.e.f. 1-4-2019 till 30-6-2019 or till next empanelment whichever is earlier on same terms conditions and rates on which they are presently empanelled.

[GoI MoH&FW DG, CGHSF. No: S-11045/36/2016-CGHS (HEC) Office Order dated 27-3-2019; www.gconnect.in]

Voluntary Exit under Atal Pension Yojana

The functionality of online Voluntary Exit was released in the month of August 2017 by Central Record Keeping Agency (CRA) – NSDL e-Governance Infrastructure

10

Limited to smoothen the process of Voluntary Exit under Atal Pension Yojana (APY). However, it has been observed that some POPs and branches of POPs are sending physical exit forms to PFRDA instead of processing through their APY module. This causes delay in execution of voluntary exit, which in turn increases grievances from the subscribers.

2. In view of the same, POPs are advised –

i) to process voluntary exit request only through their APY module; and

ii) to sensitize all their branches which are performing Atal Pension Yojana related activities to process voluntary exit as per the guidelines.

3. The physical forms are NOT to be submitted to PFRDA.

[PFRDA Circular No. PFRDA/2019/10/APY/1 dated 8-4-2019; www.staffnews.in]

Income Tax (3rd Amendment) Rules, 2019

G.S.R. 304(E).-In exercise of power conferred by Sections 200 and 203 read with Section 295 of the Income tax Act, 1961 (43 of 1961), the Central Board of Direct Taxes hereby makes the following Rules further to amend the Income-tax Rules, 1962, namely:

1. Short title and commencement

(1) These Rules may be called the Income-tax (3rd Amendment) Rules, 2019.

(2) They shall come into force on 12th day of May, 2019.

2. In the Income-tax Rules, 1962, in Appendix II–(A) in Form No. 16,–

(i) the “Notes” occurring after “Part A” shall be omitted;(ii) for “Part B (Annexure)”, the following shall be substituted Part B, namely:

(Annexure has not been reproduced here)

Notes:

1. Government deductors to fill information in item I of Part A if tax is paid without production of an income-tax challan and in item II of Part A if tax is paid accompanied by an income-tax challan.

2. Non-Government deductors to fill information in item II of Part A.

3. The deductor shall furnish the address of the Commissioner of Income-tax (TDS) having jurisdiction as regards TDS statements of the assessee.

4. If an assessee is employed under one employer only during the year, certificate in Form No. 16 issued for the quarter ending on 31st March of the financial year shall contain the details of tax deducted and deposited for all the quarters of the financial year.

5.(i) If an assessee is employed under more than one employer during the year, each of the employers shall issue Part A of the certificate in Form No. 16 pertaining to the period for which such assessee was employed with each of the employers.

(ii) Part B (Annexure) of the certificate in Form No.16 may be issued by each of the employers or the last employer at the option of the assessee.

6. In Part A, in items I and II, in the column for tax deposited in respect of deductee, furnish total amount of tax, surcharge and health and education Cess.

11

7. Deductor shall duly fill details, where available, in item numbers 2(f) and 10(k) before furnishing of Part B (Annexure) to the employee.”;

(B) in Form No. 24Q, for “Annexure II”, the following “Annexure” shall be substituted, namely (Annexure has not been reproduced here):

Notes:

1. Salary includes wages, annuity, pension, gratuity (other than exempted under section 10(10)), fees, commission, bonus, repayment of amount deposited under the Additional Emoluments (Compulsory Deposit) Act, 1974 (8 of 1974), perquisites, profits in lieu of or in addition to any salary or wages including payments made at or in connection with termination of employment, advance of salary, any payment received in respect of any period of leave not availed (other than exempted under section 10 (10AA)), any annual accretion to the balance of the account in a recognised provident fund chargeable to tax in accordance with rule 6 of Part A of the Fourth Schedule of the Income-tax Act, 1961, any sums deemed to be income received by the employee in accordance with sub‐rule (4) of rule 11 of Part A of the Fourth Schedule of the Income-tax Act, 1961, any contribution made by the Central Government to the account of the employee under a pension scheme referred to in section 80CCD or any other sums chargeable to income-tax under the head 'Salaries'.

2. Where an employer deducts from the emoluments paid to an employee or pays on his behalf any contributions of that employee to any approved superannuation fund, all such deductions or payments should be included in the statement.

3. Permanent Account Number of landlord shall be mandatorily furnished where the aggregate rent paid during the previous year exceeds one lakh rupees.

4. Permanent Account Number of lender shall be mandatorily furnished where the housing loan, on which interest is paid, is taken from a person other than a Financial Institution or the Employer.”.

[Notification No. 36/2019/F.No. 370142/4/2019-TPL]

Note: The Principal Rules were published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (ii) vide notification number S.O. 969(E) dated the 26th of March, 1962 and were last amended vide notification number G.S.R No. 279(E) dated 1-4-2019.

[GoI MoF DoR CBDT Notification dated 12-4-2019; www.govtempdiary.com]

Judgement(s)/Order(s) of Hon'ble Supreme Court on Aadhaar-PAN for Filing Return of Income

As per clause (ii) of sub-Section (1) of Section 139AA of the Income-tax Act, 1961, with effect from 1-7-2017, every person who is eligible to obtain Aadhaar number has to quote the Aadhaar number in return of income.

2. In a series of judgements, i.e., (i) Binoy Viswam Vs. Union of India reported in (2017) 396 ITR 66 (ii) Final Judgment and Order of the Constitution Bench of Hon'ble Supreme Court dated 26-9-18 in Justice K. S. Puttaswamy (Retd.) and another (Writ Petition (Civil) No. 494 of 2012); and (iii) Shreya Sen & Anr. In SLP (Civil) Diary No(s) 34292/2018 dated 4-2-2019, Hon'ble Supreme Court has upheld validity of Section 139AA.

3. In light of the aforesaid judgement(s)/Order(s) of Hon'ble Supreme Court, from 1-4-2019 onwards, to give effect to the above judgements/Orders , it has been decided

12

by the Board that provision of clause (ii) of sub-Section (1) of Section 139AA of the Act would be implemented and it is mandatory to quote Aadhaar while filing the return of income unless specifically exempted as per any notification issued under sub-Section (3) of Section 139AA of the Act. Thus, returns being filed either electronically or manually cannot be filed without quoting the Aadhaar number.

4. Returns which were filed prior to 1-4-2019 without quoting of Aadhaar number as an outcome of any decision of different High Courts in a specific case or returns which were filed during the period when the online functionality for filing the return without quoting of Aadhaar number was so available in the aftermath of decision of Delhi High Court dated 24-7-2018 in W.P. C.M 7444/2018 and C.M. Application No.28499/2018 in case of Shreya Sen vs. Union of India & ORs., till it was withdrawn post decision of Constitution Bench of the Hon'ble Supreme Court dated 26-9-2018, would also be taken up for processing without causing any adverse consequence for non-quoting of Aadhaar as per provision of Section 139AA of the Act.

[GoI MoF DoR CBDT Circular No.6/2019 dated 31-3-2019]

Amendment to Maternity Benefit (Mines and Circus) Rules 1963,

G.S.R. 57(E).—Whereas a draft of certain Rules further to amend the Maternity Benefit (Mines and Circus) Rules 1963, among other Rules, were published as required by sub-Section (1) of Section 28 of the Maternity Benefit Act, 1961 (53 of 1961), in the Gazette of India, Extraordinary, Part II, Section 3, sub-Section (i) vide notification of the Govt. of India in the Ministry of Labour and Employment number G.S.R. 413(E), dated the 23rd April, 2018, inviting objections and suggestions from all persons likely to be affected thereby, within a period of three months, from the date on which copies of Official Gazette containing the said notification were made available to the public;

And whereas copies of the said Official Gazette were made available to the general public on the 23-4-2018;

And whereas the objections and suggestions received on the said draft Rules from the public have been considered by the Central Govt.;

Now, therefore, in exercise of the power conferred by Section 28 of the said Act, the Central Govt. hereby makes the following Rules further to amend the Maternity Benefit (Mines and Circus) Rules, 1963, namely:

1.(1) These Rules may be called the Maternity Benefit (Mines and Circus) Amendment Rules, 2019.

(2) They shall come into force on the date of their publication in the Official Gazette.

2. In the Maternity Benefit (Mines and Circus) Rules, 1963, for Rule 16, the following Rule shall be substituted, namely:

‘16. Annual return.- (1) The employer of every mine or Circus shall, on or before the 1st day of February in each year, upload a unified annual return in Form X online on the Web portal of the Central Govt. in the MoL&E, giving information as to the particulars specified, in respect of the preceding year:

Provided that during inspection, the inspector may require the production of accounts, books, register and other documents maintained in electronic form or otherwise.

Explanation.- For the purposes of this sub-Rule, the expression “electronic form” shall have the same meaning as assigned to it in clause (r) of Section 2 of the Information Technology Act, 2000 (21 of 2000).

13

(2) If the employer of a mine or Circus to which the Act applies sells, abandons or discontinues the working of the mine or Circus, then, he shall, within one month of the date of such sale or abandonment or four months of the date of such discontinuance, as the case may be, upload online, on the Web portal of the Central Govt. in the MoL&E, a further unified return in Form X referred to in sub-Rule (1) in respect of the period between the end of the preceding year and the date of the sale, abandonment or discontinuance.

Note: The Maternity Benefit (Mines and Circus) Rules, 1963 was published in the Gazette of India vide notification No.G.S.R.1642, dated 5-10-1963 and lastly amended vide notification number G.S.R.435(E) dated 29-5-2015.

[GoI MoL&E Notification No. Z-20025/23/2018-LRC dated 29-1-2019]

Transfer of NPS to GPF

I am to say that various cases for transferring NPS subscriptions into GPF account have been received to this Office after Order of Hon’ble High Court of Delhi in respect of WP(C) No.3834/2013 and WP(C) No.2810/2016 vide which benefits of Old pension Scheme are extended to personnel joined in the year 2004. As there is a large number of subscribers under this kind of transfer and many requests are received along with information of Office Orders issued by various authorities (i.e., the Commandants, the DIGs, the IGs, etc.,). In this regard, it is requested to issue appropriate Orders to concerned formation to send these cases with the following documents: (i) Necessary administrative approval from the administrative Head of the

Department;(ii) Application (in the format enclosed) duly filled by the subscriber;(iii) Month-wise details of NPS subscriptions duly certified by the DDO;(iv) Copy of Office documents such as Court Order, etc., related to counting of

previous Govt. service rendered before 1-1-2004;(v) Copy of Order vide which previous service of the subscriber is counted (if

applicable);(vi) Copy of technical resignation of the subscriber (if applicable); and cases should be

sent only after NPS subscription is stopped and GPF subscription is started from salary.

2. Further, the cases should be sent through the Administrative HoD to this Office. There are some instances where Offices are asking subscribers to apply for re-issue of PRAN card for submission with the case for NPS to GPF transfer. In this regard it is to inform that only if PRAN card is available it may be sent and there is no need for re-issue the PRAN card for this purpose. The details of PRANs are available in pay and service related records. The cases can be forwarded to Principal Accounts Office, MoHA for further processing only after the aforementioned documents are received.

Compensation for Non-Deposit or Delayed Deposit of Contribution under NPS during 2004-12

The undersigned is directed to invite attention to the guidelines issued by Controller General of Accounts, MoF, DoE vide O.M. No.1(7)/2003/TA/Part file/279 dated 2-9-2008 for streamlining of procedure for remittances of contributions under the National Pension System (NPS) by PA0s/CDDOs and NCDDOs which provides, inter-alia, the detailed procedure for the purpose of crediting of the NPS contribution to the NPS Trustee Banks so as to ensure that the contribution is credited to the NPS regulatory system as per the timelines prescribed therein without delay.

Based on the recommendations of the 7th CPC and the recommendations of a Committee of Secretaries, as set up in pursuance of the decision of the Govt. contained in para 15 of the Resolution of the DoE bearing No. 1-2/2016-IC dated 25-7-2016 to

14

suggest measures for streamlining the implementation of the NP5, the DoFA, MoF, has issued a Notification F. No. 1/3/2016-PR dated 31-1-2019, clause 1(2)(x), 1(2)(xi) and 1(2)(xii) thereof provides as under: Compensation for non-deposit or delayed deposit of contribution

(a) In all cases, where the NPS contributions were deducted from the salary of the Govt. employee but the amount was not remitted to CRA system or was remitted late, the amount may be credited to the NPS account of the employee along with interest for the period from the date on which the deductions were made till the date the amount was credited to the NPS account of the employee, as per the rates applicable to GPF from time to time, compounded annually.

GPF Interest for delayed deposit of Govt. contribution

(b) In all cases where the NPS contributions were not deducted from the salary of the Govt. employee for any period during 2004-2012, the employee may be given an option to deposit the amount of employee contribution now. In case he opts to deposit the contributions now, the amount may be deposited in one lump sum or in monthly installments. The amount of installment may be deducted from the salary of the Govt. employee and deposited in his NPS account. The same may qualify for tax concessions under the Income Tax Act as applicable to the mandatory contributions of the employee.

(c) In all cases where the Govt. contributions were not remitted to CRA system or were remitted late (irrespective whether the employee contributions were deducted or not), the amount of Govt. contributions may be credited to the NPS account of the employee along with interest for the period from the date on which the Govt. contributions were due till the date the amount is actually credited to the NPS account of the employee, as per the rates applicable to GPF from time to time. Instructions to this effect may be issued by the DoE/CGA. All such cases of delay may be resolved within a period three months.

In pursuance of the aforesaid provisions of the said Notification dated 31-1-2019,

all the Ministries/Departments are required to ensure that the decisions, as contained therein insofar as these relate to the issue of delayed credit of NPS contribution to CRA system, are carried out in respect of Central Govt. employees under their administrative purview in consultation with the concerned Financial Advisors and the respective pension accounting organizations, i.e., Controller General of Accounts in respect of Central Civil Ministries/Departments, Railway Accounts in respect of Ministry of Railways, P&T Accounts in respect of employees of DoPosts and DoT and the CGDA in respect of Defence Civilians.

While carrying out the above decision contained in the afore said notification dated 31-1-2019, it has to be ensured that the modalities for implementing the same are uniform across the pension accounting organizations and, therefore, for this purpose, the Office of CGA of the DoE shall be the nodal organization for laying down the modalities. Accordingly, the Office of CGA shall issue guidelines for the purpose. The concerned Financial Advisor shall be the central point for the purpose in the respective Ministries/ Departments.

It is likely that the concerned Ministries/Departments need data and information from the Central Record-Keeping Agency, namely, NSDL, to carry out the above decision in respect of employees under their administrative domain. In Order, therefore, to facilitate such action by the Ministries/Departments, the CRA shall look into its record and in all cases which are covered under the decision contained in the aforesaid Notification dated 31-1-2019, it shall pass on such employee-wise details, on its own, to the concerned Head of the Office and DDO/PAO, where the employee is currently posted within 15 days of the date of issue of these Orders so that the desired and timely action gets initiated by the Ministries/Departments.

15

[GoI MoF DoE O.M. No.1(21)/EV/2018 dated 12-4-2019; www.gservants.com]

Extension of Old Pension Scheme to the Employees who were Selected during the

Year 2003 and who had Joined Service on or after 1-1-2004

Ref: (1) Judgment of the Hon’ble High Court of Delhi Judgment in WP(C)3834/ 2013 & in WP(C) 2810/2016 dated 27-3-2017.

(2) MoHA (PAO) CRPF Lr. No.PAO/CRPF/MHA/NPS/DA-9(1)/2018-19/797 dated 15-3-2019.

You are aware that the Staff Side of National Council (JCM) is representing in various forums to withdraw the National Pension System and to restore the old Pension Scheme under CCS (Pension) Rules, 1972, to the Defence Civilian Employees recruited on or after 1-1-2004, since the NPS is detrimental to the employees as there is no defined guarantee for Pension during the old age. This was one of the important demands, for which the NJCA has served Strike notice on the Govt. for observing Indefinite Strike. However due to the assurance given by the Group of Ministers, the proposed Indefinite Strike was deferred.

At present based on the Judgment of the Hon’ble High Court of Delhi in the above referred cases, the MoHA have decided to extend the benefits of the old pension Scheme under CCS (Pension) Rules, 1972, to the Para-Military forces who were selected during the year 2003, but joined service on or after 1-1-2004. In this regard your kind attention is drawn to the letter of MoHA dated 15-3-2019 referred at (2) above. The MoHA have decided to transfer the NPS contribution of the concerned employees to the GPF Scheme and also to bring the employees who were selected during 2003 on the basis of notification issued during 2002/2003 and joined service on or after 2004, under the coverage of CCS (Pension) Rules, 1972.

A large number of Central Govt. Employees in various Departments like Railways, Defence, Postal and other Departments are similarly placed. These employees were selected for appointment during the year 2003, based on the employment notification issued during 2002/2003, however, due to delay in receiving the Attestation Forms (Police Verification Report), Medical Fitness, etc., they were forced to join service on or after 1-1-2004. Due to no mistake of theirs. they were brought under the coverage of the NPS, thereby denying them the benefit of GPF and Defined Guaranteed Pension under the CCS (Pension) Rules, 1972. These employees also have now started representing for extending the benefit given to the Home Ministry Staff for them, and their demand is fully justified and is covered under the Judgement of Hon’ble High Court of Delhi.

In view of the above, it is requested that you may kindly look into the matter and arrange to issue instructions for extending the benefit given to the Para-Military forces in the Home Ministry to the similarly placed Central Govt. Employees by extending them the benefit of Old Pension Scheme under CCS (Pension) Rules, 1972. A copy of your instruction may please be endorsed to this Office.

[National Council (Staff Side) for CG Employees Lr. No. No.NC-JCM-2019/Pension/NPS dated 23-4-2019; www.gservants.com]

GPF for Those Who Have Been Recruited on or After 1-1-2004

This has reference to Item No. 5 of the agenda point discussed in the 47th meeting of National Council (JCM) held under the Chairmanship of Cabinet Secretary on 13-4-2019.

16

You are aware that the Staff side of the National Council JCM is repeatedly demanding for withdrawing the NPS and re introduce the defined Guaranteed pension Scheme under the CCS (Pension) Rules, 1972 to the employees who have been recruited on or after 1-1-2004. However pending the same the staff side has represented for extending the benefit of GPF for those employees who have been appointed on or before 1-1-2004 and governed under NPS on an optional basis. In the 47th National Council JCM meeting held on 13-4-2019, the Staff side reiterated their demand and requested that the GPF Scheme may be extended to the NPS employees who opt for the same as an additional saving benefit. The Cabinet Secretary desired that the demand of the Staff Side may be considered favorably. Your good self has also assured that the demand of the Staff side would be considered and decision taken at the earliest.

In view of the above we submit the following justification for extending the GPF benefit on optional basis to the employees who are governed under the NPS Scheme.

The advantage of GPF to the employees is as follows:

(1) The interest rate for GPF accumulation is 8% as on date.

(2) Advances from GPF is permissible for the following purposes.

(i) Illness of self, family members or dependants.(ii) Education of family members or dependant of the subscriber. Education

will include primary, secondary and higher education, covering all streams and educational institutions.

(iii) Obligatory expenses, viz., betrothal, marriage, funerals or other ceremonies.

(iv) Cost of legal proceedings(v) Cost of defence(vi) Purchase of consumer durables(vii) Pilgrimage and visiting places of eminence. This will include any travel and

tourism related activities.

(3) Apart from the advances as mentioned above GPF subscribers are entitled for withdrawals from GPF for the following purposes.

(i) Education -- This will include primary, secondary and higher education covering all streams and institutions.

(ii) Obligatory expenses, viz., betrothal, marriage, funerals, or other ceremonies of self or family members and dependants.

(iii) Illness of self, family members or dependants.(iv) Purchase of consumer durables.(v) Housing including building or acquiring a suitable house or a ready-built

flat for his residence.(vi) Repayment of outstanding housing loan.(vii) Purchase of house site for building a house.(viii) Constructing a house on a site acquired.(ix) Reconstructing or making additions on a house already acquired.(x) Renovating, additions or alterations of ancestral house.(xi) Purchase of motor car/motor cycle/scooter, etc., or repayment of loan

already taken for the purpose.(xii) Extensive repairs/overhauling of motor car.(xiii) Making deposit to book a motor car/motor cycle/scooter, moped, etc.

Apart from the above tax deduction under Section 80C is also available. Annual statements will be issued on the 1st of April every year.

From the above it is amply clear that the GPF is more advantages to the employees than the Tier-II Scheme of NPS. Therefore as stated by the staff side in the National Council JCM meeting held on 13-4-2019 it is once again reiterated that the GPF Scheme may be extended to the willing NPS employees who opt for the same. Necessary

17

Orders in this regard may please be issued at the earliest. A copy of your instructions may please be endorsed to this Office.

[National Council (Staff Side), JCM Lr. No. No.NC-JCM-2019/Pension/NPS dated 23-4-2019; www.gservants.com]

Regulation of LTC Claims when Portion of Journey is Performed by Private Transport

This Directorate has sought clarification from the Nodal Ministry regarding reimbursement of LTC claims where a part of the journey (be it in the beginning, middle or end) has been performed by the Govt. servant by unauthorized mode of transport (private bus/private taxi etc.) and rest of the journey to the declared place of visit by authorized mode of transport.

2. The Nodal Ministry has issued following clarification:

(I) DOP&T’s O.M. No. 31011/3/2015-Estt.(A.IV) dated 9-2-2017 provides that cases where a Govt. servant travels on LTC up to the nearest airport/railway station/bus terminal by authorized mode of transport and undertakes rest of the journey to the declared place of visit by private transport/own arrangement (such as personal vehicle or private taxi, etc.), may be dealt with as follows:

(a) In all such cases the Govt. servant may be required to submit a declaration that he and the members of the family in respect of whom the claim is submitted have indeed travelled up to the declared place of visit.

(b) If a public transport is available in a particular area, the Govt. servant will be reimbursed the fare admissible for journey by otherwise entitled mode of public transport from the nearest airport/railway station/bus terminal to the declared place of visit by shortest direct route.

(c) In case, there is no public transport available in a particular stretch of journey, the Govt. servant may be reimbursed as per his entitlement for journey on transfer for a maximum limit of 100 Kms covered by the private/personal transport based on a self-certification from the Govt. servant. Beyond this, the expenditure shall be borne by the Govt. servant.

(II) In view of the above provisions, a Govt. employee shall get fare reimbursement in cases where the initial or end part of the LTC journey from the source/destination to the nearest railhead/airport or vice-versa, as the case may be, has been performed by a private/personal mode of transport while the major part of the journey from the nearest railhead/airport has been performed by the authorized mode of transport.

3. Taking into account the advice of the Nodal Ministry in this regard, action may kindly be taken in similar cases only on the basis of the above advice and in any case of deviation from the above, the advice of the Directorate may be sought for.

[GoI MoC DoPosts Lr. F.No.20-04/2015-PAP dated 15-2-2019; www.gconnect.in]

.o.

18

Income Tax Returns for Salaried Employees for the year 2019-20

Income Tax Returns for Salaried Employees for the year 2019-20 have been notified. Either ITR-1 or ITR-2 will have to be filed by Salaried Employees not having income from profits and gains of business or profession, depending upon total income, number of house property possessed and amount of agricultural income.

Income Tax Department has notified Income Tax Returns for the year 2018-19 (Financial Year) 2019-20 (Assessment Year) recently vide Notification No. 32/2019 dated 1-4-2019. As per this Notification, Income Tax Returns from ITR-1 to ITR-7 for various types of Income have been notified by the Govt.

As far as Salaried Employees are concerned, ITR-1 and ITR-2 will be applicable.

ITR-1: Income Tax Return is applicable to a Salaried Employee in the following cases:

Total income of the salaried employee during the financial year 2018-19 did not exceed Rs.50.00 lakh.

The employee concerned should not own more than one House Property

Agricultural income received the salaried employee, if any, should not exceed more than Rs.5,000/-

Employees having ‘Other income’ sources such as interest subject total income limit of Rs.50.00 lakh can file ITR-1

ITR-2: IT Return will be applicable Salaried Employees in the following cases:

Total income a salaried employee from salary, other resources such as interest and more than one house property exceeded Rs.50.00 lakh.

When a Salaried Employee owns more than one House property

When a salaried employee having income from other than salary such as interest income, rental income, agricultural income exceeding Rs.5000/-, etc.

Salaried Employees receiving income from profits and gains of business or Profession is not entitled to file ITR-1 or ITR-2. In such cases ITR-3 will have to be filed.

ITR Form Number Applicable to

ITR-1 SAHAJ For individuals being a resident (other than not ordinarily resident) having total income up to Rs.50.00 lakh, having Income from Salaries, one house property, other sources (Interest, etc.), and agricultural income up to Rs.5,000/-]

[Not for an individual who is either Director in a Company or has invested in unlisted equity shares]

19

News & Views

ITR-2 For Individuals and HUFs not having income from profits and gains of business or profession

ITR-3 For individuals and HUFs having income from profits and gains of business or Profession

ITR-4 SUGAM For Individuals, HUFs and Firms, other than Limited Liability PartneRs.hip (LLP), being a resident having total income up to Rs.50.00 lakh and having income from business and profession which is computed under Sections 44AD, 44ADA or 44AE]

[Not for an individual who is either Director in a Company or has invested in unlisted equity shares]

ITR-5 For persons other than, (i) individual, (ii) HUF, (iii) Company and (iv) person filing Form ITR-7]

ITR-6 For Companies other than companies claiming exemption under Section 11

ITR-7 For persons including companies required to furnish return under Sections 139(4A) or 139(4B) or 139(4C) or 139(4D)

[Source: www.gconnect.in]

Important Factors for CG Employees on Pension

All Central Govt. employees are entitled to receive pension on their retirement. But, there is an eligibility criterion too. A Central Govt. employee should complete 10 or more years of service to receive the pension. A retiring pension is granted to a Govt. servant who is permitted to retire after completing qualifying service of 25 years Currently, in India, pension is calculated at 50% of emoluments (last pay) or average emoluments (for last 10 months), whichever is more beneficial to the Central Govt. employees. However, there are certain rules and regulations in regards to how one should manage their pension account. It can be in case of withdrawals, transfer or any other services related to their Bank account. Hence, if you are a Central Govt. employee, then note these important factors given by RBI on your pension.

1. Govt. employees can draw their pension from Bank branches. Also, even those employees who earlier used to draw their pension from treasury or from a Post Office, have the option to draw their pension from the authorized Bank’s branches

2. The pensioner is not required to open a separate pension account. The pension can be credited to his/her existing savings/current account maintained with the branch selected by the pensioner.

3. All pensioners of the Central Govt. Pensioners can open Joint Account with their spouses.

4. One can continue their family pension, even after the death of a pensioner. The Banks should not insist on opening of a new account in case of Central Govt. pensioner if the spouse in whose favour an authorization for family pension exists in the Pension Payment Order (PPO) is the survivor and the family pension should be credited to the existing account without opening a new account by the family pensioner for this purpose.

5. Individual Banks have framed their own Rules in this regards to maintaining a minimum balance in your Bank account. This Rule is different from Bank to Bank.

20

Hence, you should always check with your Bank about balance in your pension account.

6. The disbursement of pension by the paying branch is spread over the last four working days of the month depending on the convenience of the pension paying branch except for the month of March when the pension is credited on or after the first working day of April.

7. Pensioner can transfer his/her pension account from one branch to another branch of the same Bank and from one authorized Bank to another authorized Bank within the same Centre or at a different Centre;

8. The pensioner is required to furnish a Life Certificate/Non–Employment Certificate

or Employment Certificate to the Bank in the prescribed format in the month of November every year to ensure continued receipt of pension without interruption.

9. A pensioner having Aadhaar number can alternatively submit Jeevan Pramaan, a Digital Life Certificate introduced by the Govt. of India. For obtaining this, he/she will have to enroll and biometrically authenticate himself/herself by downloading the application generating digital life Certificate from the Website jeevanpramaan.gov.in or other means described on the Website.

10. The pension paying Bank is responsible for deduction of Income Tax from pension amount in accordance with the rates prescribed by the Income Tax authorities from time to time. While deducting such tax from the pension amount, the paying Bank will also allow deductions on account of relief to the pensioner available under the Income Tax Act.

11. The paying branch, in April each year, will also issue to the pensioner a Certificate of tax deduction as per the prescribed form. If the pensioner is not liable to pay Income Tax, he should furnish to the pension paying branch, a declaration to that effect in the prescribed form.

Hence, manage your pension account at your Bank accordingly in Order to avoid charges or fees. The Govt. gives minimum pension of Rs.9,000/-, and it shall not be higher than 50% of the highest pay in Govt. Rs.1,25,000/-.

[Source: zeebiz; www.gconnect.in; Vinotha Tilak, April 8, 2019]

Right of Children to Free and Compulsory Education Rules

The Constitution (Eighty-sixth Amendment) Act, 2002 inserted Article 21-A in the Constitution of India to provide free and compulsory education of all children in the age group of six to fourteen years as a Fundamental Right in such a manner as the State may, by law, determine. The Right of Children to Free and Compulsory Education (RTE) Act, 2009, which represents the consequential legislation envisaged under Article 21-A, means that every child has a right to full time elementary education of satisfactory and equitable quality in a formal school which satisfies certain essential norms and standards.

Article 21-A and the RTE Act came into effect on 1-4-2010. The title of the RTE Act incorporates the words ‘free and compulsory’. ‘Free education’ means that no child, other than a child who has been admitted by his or her parents to a school which is not supported by the appropriate Govt., shall be liable to pay any kind of fee or charges or expenses which may prevent him or her from pursuing and completing elementary education. ‘Compulsory education’ casts an obligation on the appropriate Govt. and local authorities to provide and ensure admission, attendance and completion of elementary education by all children in the 6-14 age group. With this, India has moved forward to a rights based framework that casts a legal obligation on the Central and State Govts. to

21

implement this fundamental child right as enshrined in the Article 21A of the Constitution, in accordance with the provisions of the RTE Act.

The RTE Act provides for the right of children to free and compulsory education till completion of elementary education in a neighbourhood school.

It clarifies that ‘compulsory education’ means obligation of the appropriate Govt. to provide free elementary education and ensure compulsory admission, attendance and completion of elementary education to every child in the six to fourteen age group. ‘Free’ means that no child shall be liable to pay any kind of fee or charges or expenses which may prevent him or her from pursuing and completing elementary education.

It makes provisions for a non-admitted child to be admitted to an age appropriate class.

It specifies the duties and responsibilities of appropriate Govts., local authority and parents in providing free and compulsory education, and sharing of financial and other responsibilities between the Central and State Governments.

It lays down the norms and standards relating inter alia to Pupil Teacher Ratios (PTRs.), buildings and infrastructure, school-working days, Teacher-working hours.

It provides for rational deployment of Teachers by ensuring that the specified pupil Teacher ratio is maintained for each school, rather than just as an average for the State or District or Block, thus ensuring that there is no urban-rural imbalance in Teacher postings. It also provides for prohibition of deployment of Teachers for non-educational work, other than decennial census, elections to local authority, state legislatures and parliament, and disaster relief.

It provides for appointment of appropriately trained Teachers, i.e., Teachers with the requisite entry and academic qualifications.

It prohibits (a) physical punishment and mental harassment; (b) screening procedures for admission of children; (c) capitation fee; (d) private tuition by Teachers and (e) running of schools without recognition,

It provides for development of curriculum in consonance with the values enshrined in the Constitution, and which would ensure the all-round development of the child, building on the child’s knowledge, potentiality and talent and making the child free of fear, trauma and anxiety through a system of child friendly and child-centered learning.

[Source: www.gconnect.in]

Pension and Gratuity Linked Rules for CG Employees and Pensioners

Central and State Govt. employees become eligible for a pension if she/he has put into service a minimum of 10 years However, a retirement pension is granted to a Govt. employee who is allowed to retire after completing qualifying service of 25 years Central Govt. employees and pensioners form a base of over 1.10 crore staffers. The Govt. employees who have joined services before 2004 get pension according to the old pension Rules while those recruited after 2004 will get pension as per the New Pension Scheme or National Pension System. Below are some of the Rules that a serving employee or a pensioner must know:

Pension: (Applicable to the Govt. servant who joined service before 1-1-2004)

The Govt. had raised the maximum limit for commutation to 40% to w.e.f. 1-1-1996. Thus, a Govt. employee can commute a lump sum payment of up to 40% from his/her pension.

22

If a Govt. employee or pensioner is missing, a family pension can be paid only after a period of six months from the date of an FIR with the police authorities.

A judicially separated spouse of the deceased Govt. servant with children can get a family pension after the children cease to be eligible till his/her death/ remarriage, whichever is earlier.

Dependent parents and widowed/divorced daughter/unmarried daughter are now included in the definition of Family for the purpose of consideration for grant of family pension.

Family pension is also admissible to a posthumous child and also to children from the void or the voidable marriage as per the relevant provisions in the Rules.

Normal family pension is now at a uniform rate of 30% of pay last drawn, subject to a minimum of Rs.9000/- w.e.f. 1-1-2016.

Gratuity:

The maximum limit of all types of gratuity has been raised to Rs.20.00 lakhs w.e.f. 1-1-2016

Dearness Allowance admissible on the date of retirement/death is included in the emoluments for the purpose of computing all types of gratuity.

Interest (at the rate applicable to GPF deposits determined from time to time by the Govt. of India) is payable on delayed payment of DCRG, if it is delayed beyond three months from the date of retirement.

[Source: www.gconnect.in; Vinotha Tilak, April 12, 2019]

Higher Pension under EPS Scheme: Important Factors

Until recently, the pension you could get under the Employees’ Pension Scheme (EPS) was capped at Rs.7,500/- per month. But thanks to a recent Supreme Court (SC) ruling, this cap has now been lifted. Your pension will now depend on your last drawn pensionable (basic salary plus dearness allowance) salary.

Expectedly, the labour activists are happy: “The Supreme Court has cleared all doubts and now everyone can get a pension based on their last-drawn salaries. I suggest they opt for their full pension,” says Virjesh Upadhyay, All India General Secretary, Bhartiya Mazdoor Sangh. But before you jump with joy, you must understand that this higher pension will come from your own pocket.

Currently, 12% of your pensionable salary goes into the EPF. Your employer matches this 12%. Prior to the SC ruling, 8.33% of the employer’s contribution or Rs.1,250/-, whichever was higher, went into the EPS and the rest went into EPF. Now, if you opt for full pension, the entire 8.33% of your pensionable salary will go into the EPS. So, while your EPS contribution will go up, your contribution to EPF will fall proportionately.

You can get a much higher pension now

Pension under EPS has now been linked to your last-drawn salary.

Years in service Current pension

Increased Pension-Based on Salary*

Rs.30,000 Rs.60,000 Rs.90,000

23

5 NA NA NA NA10 Rs.2,143 Rs. 4,286 Rs. 8,571 Rs.12,85715 Rs.3,214 Rs. 6,429 Rs.12,857 Rs.19,28620 Rs.4,286 Rs. 8,571 Rs.17,143 Rs.25,71425 Rs.5,357 Rs.10,714 Rs.32,429 Rs.32,14330 Rs.6,429 Rs.12,857 Rs.25,714 Rs.38,57135 Rs.7,500 Rs.15,000 Rs.30,000 Rs.45,000

Pensionable salary means basic salary plus dearness allowance.

To illustrate, if you are 58 and about to retire after 35 years of service, and want a full pension, you will have to shift the entire 8.33% of the employers.’ contribution from EPF to EPS from the date you started working. So, if your salary grew at 7% per annum and is currently Rs.90,000/-, the additional contribution for the last 35 years will be to the tune of Rs.10.35 lakh, plus interest.

Interest is what makes the real difference. When you add the interest, the additional contribution comes close to Rs.45.15 lakh. You will have to shift this amount from the EPF to the EPS to be eligible for your full pension - Rs.45,000/- per month.

Monthly EPS contribution will shoot up

Now 8.33% of your actual pensionable salary will go towards EPS. Earlier, pensionable salary was capped at Rs.15,000/-.

Old Regime New regime

Your last drawn salary (p.m.) Rs.90,000 Rs.90,000Employer’s contribution (12% of salary Rs.10,800 Rs.10,800Of this, what goes into EPS* Rs. 1,250 Rs. 7,500Balance that goes into EPF Rs. 9,550 Rs. 3,300

*Contribution to EPS is less because of the Rs.15,000/- pensionable salarycap under the old regime.

The Supreme Court ruling in a nutshell

Arbitrary restriction of Rs.15,000/- on pensionable salary has been removed. Now, you can opt for a higher pension, if your pensionable salary more than Rs.15,000/-.

Average pensionable salary will be based on 12 months’ pay and not 60 months’ pay as was the case earlier.

Employees from organisations with PF trusts can also opt for higher EPS contribution for higher pensions.

Recently retired people can also opt for higher pension. But they will have to return proportionate amount of EPF money.

Are you financially prudent?

If you prefer spending money over saving for the future, you must go for the full pension option. Though some experts suggest that shifting money from the EPF to the EPS may not be really needed to secure your retirement. “Allowing the money to accumulate in the EPF and then investing it at the time of your retirement will be a better option (there will be several products available at that time),” says Mrin Agarwal, Founder Director, Finsafe India and Co-founder, Womantra.

24

However, even financially-savvy people may also not be able to manage their finances at an advanced age, when they need the security of a regular monthly income. “Due to the increase in life expectancy, we all need some regular monthly income. So, it will be better if people opt for higher EPS contributions,” says Amol Joshi, Founder, Plan Rupee Investment Services.

If you choose to let the money accumulate in the EPF, you may use it to purchase an annuity. But annuity from an insurance Company will fetch you a slightly lower income. For instance, if you put Rs.45.15 lakh in LIC Jeevan Akshay, you would get a monthly annuity of Rs.32,054/-. But the monthly additional pension under EPS would be Rs.37,500/-.

EPS is a better option than annuity

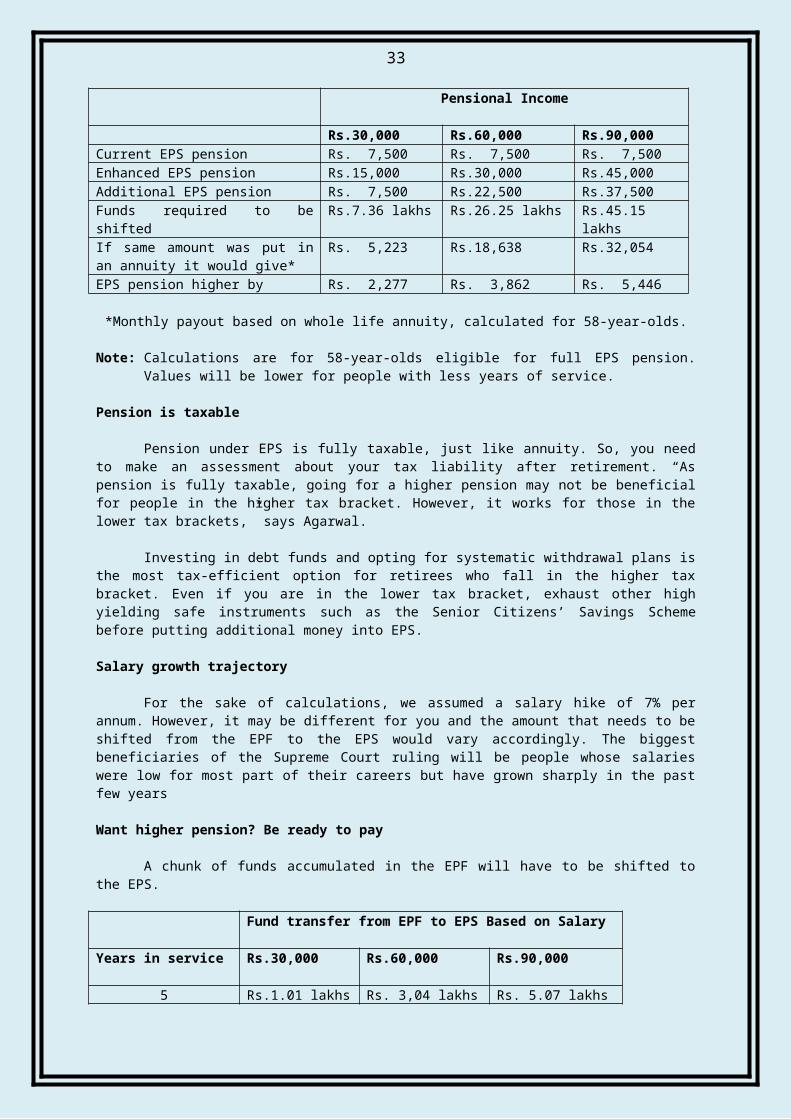

The payout under EPS can be higher by 16-40% depending on income level

Pensional Income

Rs.30,000 Rs.60,000 Rs.90,000Current EPS pension Rs. 7,500 Rs. 7,500 Rs. 7,500Enhanced EPS pension Rs.15,000 Rs.30,000 Rs.45,000Additional EPS pension Rs. 7,500 Rs.22,500 Rs.37,500Funds required to be shifted Rs.7.36 lakhs Rs.26.25 lakhs Rs.45.15 lakhsIf same amount was put in an annuity it would give*

Rs. 5,223 Rs.18,638 Rs.32,054

EPS pension higher by Rs. 2,277 Rs. 3,862 Rs. 5,446

*Monthly payout based on whole life annuity, calculated for 58-year-olds.

Note: Calculations are for 58-year-olds eligible for full EPS pension. Values will be lower for people with less years of service.

Pension is taxable

Pension under EPS is fully taxable, just like annuity. So, you need to make an assessment about your tax liability after retirement. “As pension is fully taxable, going for a higher pension may not be beneficial for people in the higher tax bracket. However, it works for those in the lower tax brackets,” says Agarwal.

Investing in debt funds and opting for systematic withdrawal plans is the most tax-efficient option for retirees who fall in the higher tax bracket. Even if you are in the lower tax bracket, exhaust other high yielding safe instruments such as the Senior Citizens’ Savings Scheme before putting additional money into EPS.

Salary growth trajectory

For the sake of calculations, we assumed a salary hike of 7% per annum. However, it may be different for you and the amount that needs to be shifted from the EPF to the EPS would vary accordingly. The biggest beneficiaries of the Supreme Court ruling will be people whose salaries were low for most part of their careers but have grown sharply in the past few years

Want higher pension? Be ready to pay

A chunk of funds accumulated in the EPF will have to be shifted to the EPS.

Fund transfer from EPF to EPS Based on Salary

Years in service Rs.30,000 Rs.60,000 Rs.90,000

5 Rs.1.01 lakhs Rs. 3,04 lakhs Rs. 5.07 lakhs

25

10 Rs.2.16 “ Rs. 6.04 “ Rs. 9.92 “15 Rs.3.11 “ Rs. 8.99 “ Rs.14.86 “20 Rs.3.97 “ Rs.12.13 “ Rs.20.28 “25 Rs.4.71 “ Rs.15.71 “ Rs.26.71 “30 Rs.5.86 “ Rs.20.43 “ Rs.35.00 “35 Rs.7.35 “ Rs.26.25 “ Rs.45.14 “

* Historical salaries have been computed assuming an increase of 7% per annum.

* Due to the jump in salaries, this will be a great boon for such people and they should opt for the higher pension,” says Joshi. If you are not sure how your salary has grown over the years, you can approach the EPFO Office. It will help you determine the exact amount that needs to be shifted from your EPF to the EPS, based on the growth in your salary.

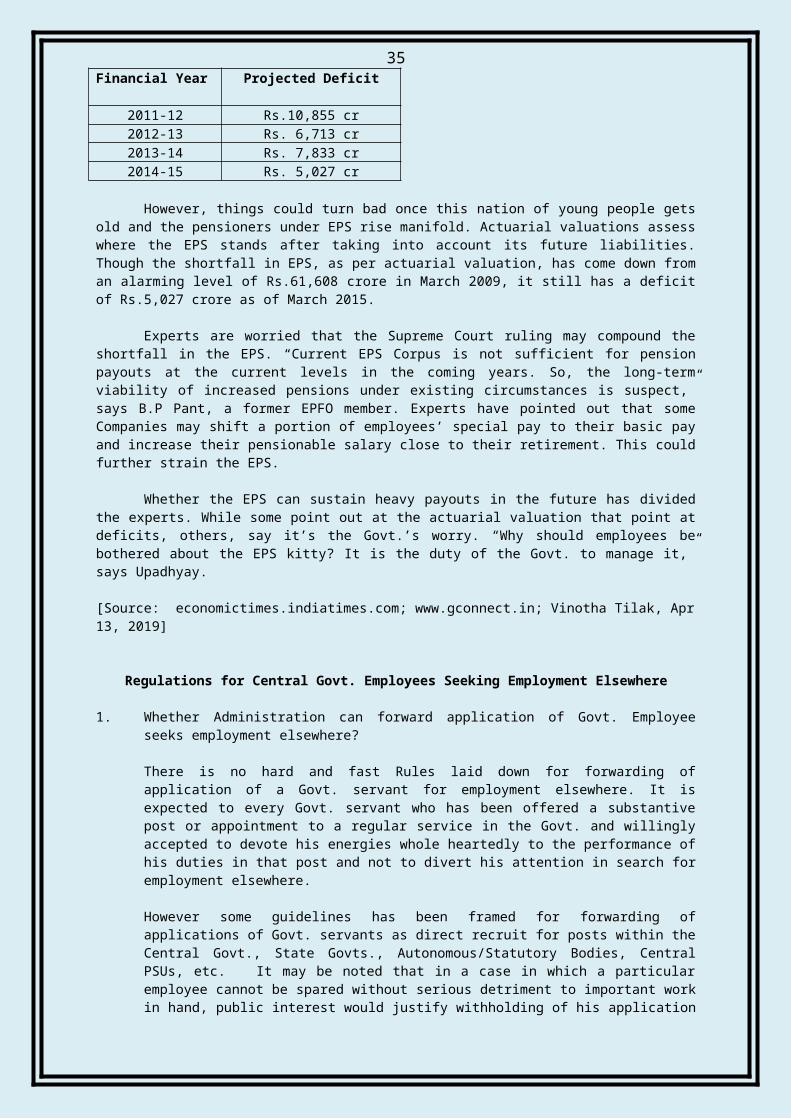

Higher pensions sustainable?

As EPS has a huge corpus and is controlled by the Ministry of Labour, most people assume that it is totally risk free. Also, as inflows in the EPS are far higher than outflows, currently it appears as a safe product.