Wealth Management Topic 2:Setting Financial Goals Mrs. Tobe.

40

Wealth Management Topic 2:Setting Financial Goals Mrs. Tobe

-

Upload

rudolf-horn -

Category

Documents

-

view

218 -

download

0

Transcript of Wealth Management Topic 2:Setting Financial Goals Mrs. Tobe.

Wealth ManagementTopic 2:Setting Financial Goals

Mrs. Tobe

Topic 2.01: Explain forms of financial exchange Cash – ready money; money on hand; money in the

form of bills or coins.

Credit – the ability to buy something or to borrow money with the promise to pay for it later; agreement based largely on trust under which goods, services, or money is exchanged against a promise to pay later. It has the effect of decreasing an asset or expense account, or of increasing a capital, liability, or revenue account. For example, you open a line of credit with the Union Bank and get a credit card to use for purchases. You pay monthly for purchases made throughout the billing period.

Debit – it has the effect of decreasing a capital, liability, or revenue account, or of increasing an asset or expense account.

EFT – electronic funds transfer; as defined in the Electronic Fund Transfer Act (Title XX of the Financial Institutions Regulatory and Interest Rate Control Act of 1978), any transfer of funds, other than a transaction originated by a paper instrument, that is initiated through an electronic terminal, telephone, or computer or magnetic tape and that orders or authorizes a financial institution to debit or credit an account. An example would be an ATM (Automatic Teller Machine) transaction.

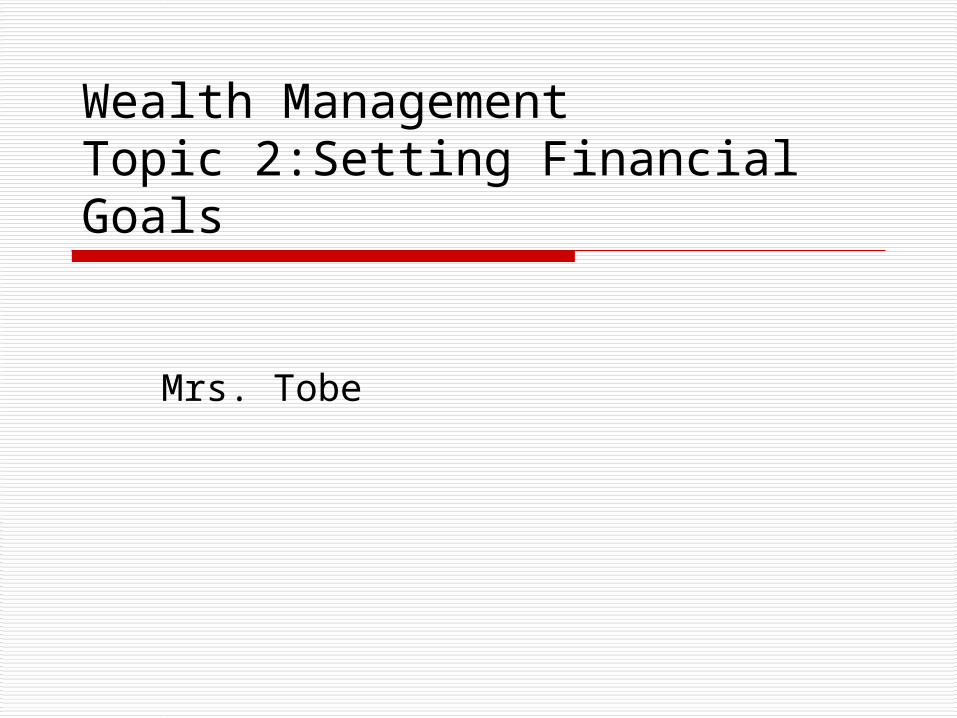

Topic 2.01: Explain forms of financial exchange

Checks A check typically is a paper document signed by you, making it a “negotiable

instrument” that authorizes a withdrawal from your checking account. Americans are using fewer and fewer checks to pay for purchases and bills. In addition, recent check regulations (Check 21) allow merchants and financial institutions to process checks as electronic transfers speeding up the transfer of funds and eliminating the paper check in mid process. If you authorize a direct withdrawal from your checking account over the phone or on an Internet web site, you are allowing the merchant or vendor to create a form of check known as a “demand draft” that doesn't require your signature.

Benefits Paper trail. Some security issues. Comfort.

Cautions Security issues. Postage costs. Possibility of overdrawing your account.

Topic 2.01: Explain forms of financial exchange

Credit Cards Unlike debit cards which provide access to your own money,

credit cards access loans from the card issuers. When you use a credit card to make a purchase, the merchant or service provider is paid for your purchase by the card issuer, then you pay back the card issuer when you pay your monthly statement. If you don't pay off your entire balance each month, you'll pay interest on the unpaid balance. If you pay late, you will incur late fees.

Benefits Convenience. Flexibility. Emergency access to cash. Good consumer protection. Record keeping.

Cautions Self-discipline is required. Interest and fees. Risk of card theft or compromise of account information.

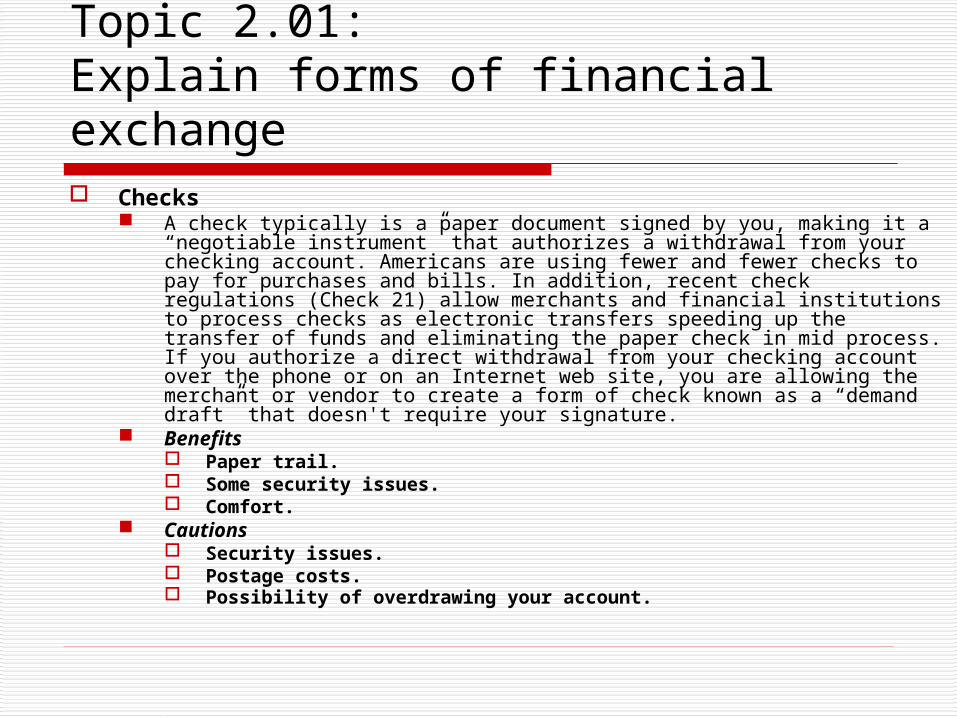

Topic 2.01: Explain forms of financial exchange

Debit Cards Recently, debit cards became the most popular payment

method in the US for purchases made in person at the point of sale or service. A debit card, also called a check card, links directly to a checking account and typically has a Visa® or MasterCard® logo on it. It usually serves as your ATM card for all your accounts at the issuing institution. When you use a debit card to make a purchase the money is electronically deducted directly from your checking account.

Benefits Convenience. Debt management. Record keeping.

Cautions Risk of card theft or compromise of account information. Timeliness of access to your funds during investigation. Less consumer protections than credit cards. Possibility of overdrawing your account.

Topic 2.01: Explain forms of financial exchange

Cash What's the role for good, old-fashioned

cash? Depending on your individual circumstances, you may find that cash still offers the best option for many everyday purchases.

What's more, cash in your hand is not working for you. Keeping money in your savings account until you absolutely need it allows your money to grow.

Topic 2.01: Explain forms of financial exchange

Explain why money is used as a medium of exchange. It must be generally accepted as a means of payment by all

parties. Did you ever wonder why a restaurant owner is willing to give you a pizza for a piece of paper with Alexander Hamilton's picture on it?

Discuss how money is used as a unit of measure. It must provide a common unit for measuring the value of

every good and service. This allows those who are selling to set prices.

Describe how money is used as a store of value. It must retain its purchasing power over time. People do not

want to make purchases every time they sell something. You can see that items like corn, or other goods that spoil, are not very good substitutes for money because they cannot function as a store of value.

Topic 2.02: What will your money do for you

Economic Incentives are offered to influence our behavior. Positive economic incentives reward people financially

for making certain choices and behaving in a certain way. They reward you with money or some sort of financial gain

such as a better price, a free item, or an upgraded item. Coupons, sales, freebies, discounts, and rewards can be positive economic incentives. They are called positive because they are associated with things many people would like to get.

Negative economic incentives punish people financially for making certain choices and behaving in a certain way. These incentives cost you money. Fines, fees, and tickets

can be negative economic incentives. They are called negative because they are things you don't want to get.

Topic 2.02: What will your money do for you

Incentives – employee motivation technique that offers cash, gifts, special recognition, or other awards for exceeding performance goals. An incentive program may be a contest with a single employee or group of employees winning a prize, or it may be structured to reward as many employees as are able to achieve the defined performance goal. Many incentive programs are designed to support sales or piecework goals. To be effective, the rules of the incentive program must be clearly understood and fairly administered.

Values – worth of all benefits and rights of arising from ownership; price X quantity. For example, the value of all desks in the room is $250 X 14= $4,250.

Risk – the potential for loss of value; probability that an actual return on an investment will be lower than the expected return.

Topic 2.03: Why is money an incentive

Return – profit on a securities or capital investment, usually expressed as an annual percentage rate.

Profit – best known measure of the success of a company, it is the surplus remaining after total costs are deducted from total revenue, and the basis on which tax is computed and dividend is paid. Profit is reflected in reduction in liabilities, increase in assets, and/or increase in owners' equity.

Interest – cost of using money, expressed as a rate per period of time, usually one year, in which case it is called an annual rate of interest.

Self-interest – personal advantage or interest.

Topic 2.03: Why is money an incentive

Identify types of economic incentives Prices, wages, profits, subsidies, and taxes

Positive - Coupons, sales, freebies, discounts, and rewards

Negative - Fines, fees, and tickets

Topic 2.03: Why is money an incentive

Topic 2.03: Why is money an incentive Discuss the relationship between risk and return.

All investments provide a certain level of return and are subject to a certain level of risk. Basically this means that as well as making money on your investment there's also a chance you could either lose money or not make as much as you expected.

As a general rule, the larger the potential investment return, the higher the investment risk, and the longer you need to remain invested to reduce that risk.

Explain ways to use incentives to increase an activity. The surest way to get people to behave in

desirable ways is to reward them for doing so—in other words provide them with incentives. This is so obvious that you might think it hardly deserves mention. But it does.

You might say that people shouldn't have to be rewarded (bribed) to do desirable things. Even when you acknowledge that incentives are necessary, it is not obvious how to establish the ones that motivate desirable action.

Topic 2.03: Why is money an incentive

Describe ways to use incentives to decrease an activity. Just like rewarding a person to increase

an activity, you can punish people to try to decrease an activity. Fees, fines, tickets, detentions, Saturday schools and being grounded are all ways to decrease and activity.

Topic 2.03: Why is money an incentive

Saving – a reduction in the amount of time or money used; avoidance of excess expenditures.

Investing – to commit money or capital in order to gain a financial return.

Financial needs – technique used to determine how much life insurance is required, by considering the future needs of the policy's beneficiaries.

Financial goals – objective or target, usually driven by specific future financial needs. For example, common financial goals for an individual are: saving for a comfortable retirement, saving to send children to college, managing finances to enable a home purchase, minimizing taxes, maximizing return on investments given a certain risk tolerance, and estate or trust planning.

Topic 2.04: What is saving and investing

Identify types of financial needs. College loan, car loan, house mortgage,

business, retirement fund, kids college and monthly bills

Discuss ways individuals meet financial needs. Saving and investing

Various types for each

Topic 2.04: What is saving and investing

Topic 2.04: What is saving and investing Investing is a way to

make money with your money. First, you have to earn money. As a kid, you get money from allowance, gifts, services, or from selling goods such as lemonade. Try to save some, if not all of this money. The next step is to make your money grow through investing.

Why Should I Invest? There are two main reasons why you should

invest: To stay ahead of inflation To achieve financial goals

Topic 2.04: What is saving and investing

Compare the outcome of saving/investing early versus late in life. Matt and Chuck Example

Rule of 72 – formula to find out how quick your money will double Divide 72 by the interest rate

72 divided by 6 = 12 years

Topic 2.04: What is saving and investing

Good faith – the observance of honorable intent in business relations and the avoidance of any attempts to deceive in assuming and performing contractual obligations. For example, the autoworkers bargained with management in good faith so that all parties would benefit.

Disclosure – the release of relevant information. For example, a college or university will disclose the people who gave money to it for tax purposes.

Float – period between the beginning and the close of a transaction.

Topic 2.05: What are legal aspects of exchange

Describe how borrowers and lenders benefit from financial exchanges. Many individuals are not aware that they are

lenders, but almost everybody does lend money in many ways. A person lends money when he or she: puts money in a savings account at a bank contributes to a pension plan pays premiums to an insurance company invests in government bonds/company share

Topic 2.05: What are legal aspects of exchange

Borrowers Individuals borrow money via bankers‘

loans for short term needs or longer term mortgages to help finance a house purchase.

Companies borrow money to aid short term or long term cash flows. They also borrow to fund modernization or future business expansion.

Topic 2.05: What are legal aspects of exchange

Explain how the concept of good faith applies to financial exchanges. A Good Faith Estimate is an estimate

that lists all fees paid before closing, all closing costs, and any escrow costs you will encounter when purchasing a home.

The lender must supply it within three days of your application so that you can make accurate judgments when shopping for a loan.

Topic 2.05: What are legal aspects of exchange

Discuss the lender’s responsibility to disclose terms and conditions of financial exchanges. It protects borrowers from abuses by lending institutions

by mandating that lenders fully inform borrowers about all closing costs, lender servicing and escrow account practices, and business relationships between closing service providers and other parties to the transaction.

Lenders are not allowed to discriminate in any way against potential borrowers on the basis of race, color, nationality, religion, sex, familial status, or disability

Topic 2.05: What are legal aspects of exchange

Explain the borrower’s responsibility to disclose information that would prohibit repayment to the lender. Be sure to read and understand everything before

you sign.

Refuse to sign any blank documents. Do not buy property for someone else. Do not overstate your income. Do not overstate how long you have been employed. Do not overstate your assets.

Topic 2.05: What are legal aspects of exchange

Accurately report your debts. Do not change your income tax returns for any

reason. Tell the whole truth about gifts. Do not list fake co-borrowers on your loan

application. Be truthful about your credit problems, past and

present. Be honest about your intention to occupy the

house. Do not provide false supporting documents.

Topic 2.05: What are legal aspects of exchange

Explain the impact of electronic financial services on financial exchanges. Establishes the rights and liabilities of the consumer,

as well as the responsibilities of all participants in EFT activities (including financial institutions).

ATM and POS (point of sale) transactions, like using your debit or check card at the grocery store.

Telephone transfers and preauthorized transfers — in other words, whenever you tell your bank to make some type of automatic transfers for you. Monthly direct deposits and monthly mortgage payments all count.

Topic 2.05: What are legal aspects of exchange

Describe federal legislation that protects borrowers. Truth in Lending and Consumer Leasing

Acts Equal Credit opportunity Act (ECOA) Fair Credit Opportunity Act Fair Credit Reporting Act Consumer Credit Reporting Reform Act

Topic 2.05: What are legal aspects of exchange

Time value of money – (TMV) price put on the time an investor or lender has to wait until the investment or loan is fully recouped. TVM is based on the concept that money received earlier is worth more than the same amount of money received later, because it can be 'employed' to earn interest over time. Computed as compound interest.

Inflation – persistent increase in the average price level in the economy. Inflation occurs when the AVERAGE price level (that is, prices IN GENERAL) increases over time. This does NOT mean that ALL prices increase the same, nor that ALL prices necessarily increase. Some prices might increase a lot, others a little, and still other prices decrease or remain unchanged. Inflation results when the AVERAGE of these assorted prices follows an upward trend. Inflation is the most common phenomenon associated with the price level.

Topic 2.06: What’s your money worth

Interest rate – price of funds expressed as a percentage of the total amount loaned or borrowed. This is the cost of borrowing funds and the payment received for lending. Interest rates are invariably expressed as an annual percentage of the amount borrowed/loaned. A 10 percent interest rate, to run through an easy example, tells us that the cost of borrowing $1,000 for one year is $100.

Present value – amount of money today that, after interest is added, would have the same value as an amount some time in the future. For example, $100 today, given a 10 percent interest rate, would have a value of $110 in one year ($100 plus $10 in interest). Conversely, $110 in one year, given a 10 percent interest rate, would be equivalent to $100 today. The process of translating a future payment into its present value, such an amount to be received when a bond reaches its date of maturity, is often termed discounting.

Topic 2.06: What’s your money worth

Compound interest – interest that's added to a principal at regular intervals such that each subsequent interest calculation is based on the original principal and the added interest. For example, suppose you have a $100 savings account that pays 5 percent interest. Without compound interest, such that your 5 percent interest is paid only at the end of a year, you will have exactly $105 in one year. However, if your interest is compounded each month you end up with $105.12 after a year. The extra 12 cents comes from interest on the interest paid the first month, interest on the interest paid the second month, interest on the interest paid the third month...

Topic 2.06: What’s your money worth

Describe how time impacts the value of money. The increase of an amount of money due to

earned interest or dividends Save or invest money instead of spending it, the

money could be worth more later because you would earn interest or dividends

Think of the time value of money as an opportunity costs

Topic 2.06: What’s your money worth

Explain information that is needed when considering the time value of money Date at which the dollar amount is

measured and the interest rate applied Principal Future value Annuity Present value

Topic 2.06: What’s your money worth

Explain the impact of inflation on the value of money. During rapid inflation-it takes more money

to buy the same amount of goods or services Inflation 5% - computer a year ago $1000,

would now cost $1050 Main cause of inflation is increase in

demand without an increase in supply

Topic 2.06: What’s your money worth

Discuss situations in which the present value is needed. To see the amount of money need to

deposit now to have a desired amount in the future

If you want to have $1000 in 5 yrs for a down payment on a car, you would need to deposit $784 now.

Topic 2.06: What’s your money worth

Discuss the value of planning in meeting financial goals.

Life situations Personal values Economics factors

Identify obstacles to meeting financial goals.

Consumer pricing Consumer spending Interest rates

Topic 2.07: What are your financial goals

Describe characteristics of useful financial goals.

Assessing your present financial situations

Making a list of your current needs Deciding how to plan for future needs

Topic 2.07: What are your financial goals

Explain a financial goal-setting process.1. Obtain- working, making investments and

owning property2. Plan- how to spend and save money3. Spend Wisely- spend less than you earn4. Save- save on a regular basis, you will have

more money to pay your bills, make major purchases, and cope with emergencies

5. Borrow Wisely- borrow only when needed

Topic 2.07: What are your financial goals

6. Invest- to increase current growth and achieve long term growth

7. Manage Risk- insurance to protect resources in case or injury, sickness, or death

8. Plan for Retirement- consider the age you want to retire, where you wan to live, how you want to spend your time; part time job, doing volunteering work, enjoying hobbies/sports

Topic 2.07: What are your financial goals