WCM Strategies

44

Some Strategies for Managing Working Capital Duke Ghosh IIFT, 2015

description

Working Capital Management

Transcript of WCM Strategies

Some Strategies for Managing Working Capital

Duke Ghosh

IIFT, 2015

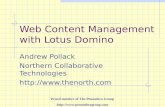

How CA is Funded

TCA

AP + Provisions+ OCL

NWC

Short Term Borrowings

• Note: NWC+STB constitutes the portion of the TCA not funded by the Current Liabilities

• What is a Good Strategy?

• Increase NWC?

• Increase STB?

• Increase CL other than STB?

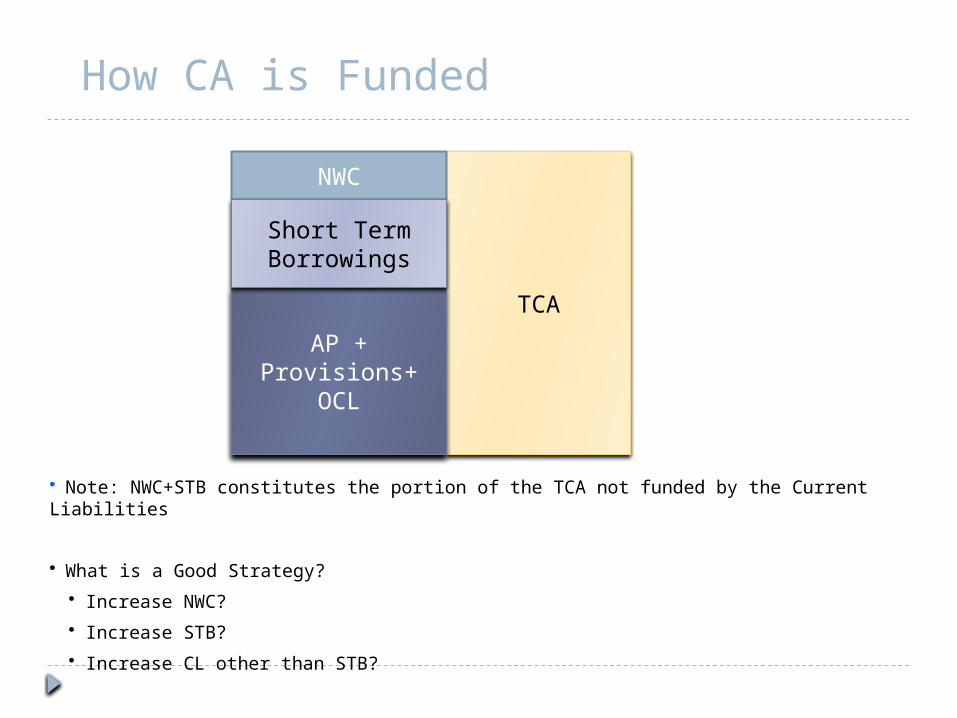

Cycles (of Concern)!Order for RM Placed

Payment to Creditors

Sale of FG on Credit

Collection of Cash from Receivables

TimeO B C D

• Cash flows are not always synchronized – some unwanted cashflows precede the wanted cashflows

• Cash can also be uncertain – timing and amount is not known in advance

• What is the Problem in the cycle ?

• How to handle the mismatch?

Arrival of RM

A

Short Term Financial Policy• Flexible Short Term Financial Policy

• Large balances of Cash and/or MS

• Large Investment in Inventories

• Liberal credit decisions – high level of receivables

• Restrictive Short Term Financial Policy

• Low balances in Cash and/or MS

• Low investments in inventory

• Low account receivables

• Dimensions of the Short Term Financial Policy

• What should be the size of the firm’s investment in CA?

• Flexible (or Accommodative) policy aims at maintaining a high ratio of CA : Sales

• Restrictive Policy implies a low ratio

• What should be the Pattern of Financing of CA

• Flexible policy implies a low ratio of STD/LTD

• Restrictive policy implies a high ratio of STD/LTD

Flexible STFP – What it All Mean?• CA holding level is the highest in the Flexible Policy

• Is the firm risk-averse?

• Is the business model (product – market – technology) require such policy?

• Is this an industry norm?

• Does the firm want to maximize Customer Service Outputs?

• Flexible policies are costly – WHY?

• Cost of liabilities

• Inventory carrying costs

• Rate of return of short term assets < Rate of return on long term assets

• Cost of LTD > Cost of STD

• Tradeoff between short term assets and long term assets

• Transaction costs are low

• Shortage (stock out) costs are low

• Reverse is true true for the Restrictive Policies

Float Management

Float

• Banks with HSBC, Kolkata

• Makes payment to LUMAX by Cheque

• Supplies Liquid Oxygen to NATIONAL

• Banks with SBI, Burdwan

• Makes a supply to NATIONAL; Invoice Value is Rs. 1.00 Lacs

• Collects the cheque from NATIONAL and deposits with SBI

LUMAX AIR LTD. NATIONAL BEARINGS

Float…Contd.

Day 1: NATIONAL Issues the Cheque

Day 2: LUMAX collects the Cheque

Day 3: LUMAX deposits the Cheque with SBI

Day 4: SBI lodges the cheque for clearing

Day 5: Clearing

Day 6: Clearing

Day 7: LUMAX : Rs. 1.00 Lacs (Cr) NATIONAL: Rs. 1.00 Lacs (Dr.)

0

Float…Contd.Further Assumption:

(a) Day 0: Credit Balance in National’s A/c was Rs. 100.00 Lacs. Book Balance & Bank Balance were Reconciled

(b) Day 1: Credit Balance in Lumax A/c was Rs. 75.00 Lacs. Book Balance & Bank Balance Reconciled

(c) No other cheques were received or issued

Float…Contd.

• Day 1, 2, 3, 4, 5, 6

Book Balance: Rs. 99.00 LacsBank Balance: Rs. 100.00 Lacs

Bank Bal > Book Bal

• Day 7

Book Bal = Bank Bal = 99.00 Lacs

• Day 2, 3, 4, 5, 6

Book Bal = Rs. 76.00 Lacs Bank Bal = Rs. 75.00 Lacs

Bank Bal < Book Bal

• Day 7

Book Bal = Bank Bal = 76.00

LUMAX AIR LTD. NATIONAL BEARINGS

Disbursement Float

For the period Day 0 – Day 6, NATIONAL can utilize EXTRA Balance of Rs. 1.00 Lacs

The company can withdraw Rs. 1.00 Lacs, invest in shares, sell them on Day 6, earn capital gains and replenish the Bank account.

Or

The company can withdraw cash, purchase some trading goods, sell them on day 6, earn profit and replenish the Bank account

This extra cash (Bank Balance – Book Balance) available to the company is called Disbursement Float

Disbursement Float (DF) is beneficial to the company, provided the company can profitably use this DF

Positive DF implies that Bank Balance > Book Balance

Collection Float

During the period Day 1 - Day 6, LUMAX can never utilize the amount of Rs. 1.00 Lacs BECAUSE Cash is not available to it, inspite of the fact that it has received payment.

For LUMAX this Rs. 1.00 Lacs is called the Collection Float

Collection Float is Disadvantageous to the Firm

Positive CF implies that Book Balance < Bank Balance

Cost of Collection Float: Opportunity cost associated with not being able to use the cash i.e. the loss of interest, which, otherwise the firm could have earned by parking the cash meaningfully.

Net Float

A Firm is both a Supplier and a Customer

It issues Cheques and Receives Cheques

At any point in time, it has both Disbursement Float and Collection Float

Net Float = Disbursement Float - Collection Float

NF>0 implies that Bank Balance > Book BalanceNF<0 implies that Book Balance > Bank Balance

NF>0 is favourableNF<0 is unfavourable

Float Management

Philosophy of Float Management:Efforts to make NF>0 and as large as possible

CorollaryIncrease Disbursement FloatReduce Collection Float

Cost of Float (Cost of Collection Float): The opportunity cost (the interest loss) of not availing the cash

Float Management also tries to minimize this Cost

• Try to Accelerate conversion of Collected Cheques to Cash (Reduce Collection Float)• Try to Slow Down conversion of issued cheques to cash (Increase Disbursement Float)

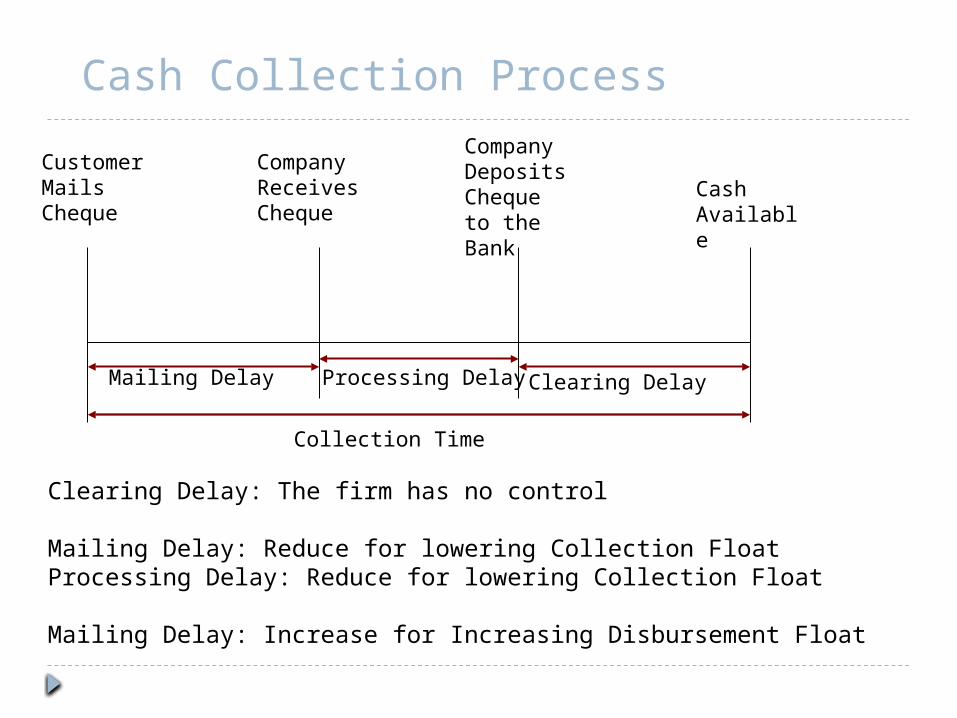

Cash Collection Process

Collection Time

Customer Mails Cheque

Company Receives Cheque

Company Deposits Cheque to the Bank

Cash Available

Mailing Delay Processing Delay Clearing Delay

Clearing Delay: The firm has no control

Mailing Delay: Reduce for lowering Collection FloatProcessing Delay: Reduce for lowering Collection Float

Mailing Delay: Increase for Increasing Disbursement Float

Cash Concentration• Normally a company has customers spread across the country• It receives cheques at all locations• The cheques are sent to the Central Office• The cheques are encashed at a Central Location

The above procedure is generally preferred on account of:(a) Better Control over Cash(b) Better Cash Management(c) Ease of Budgeting

The system is called Cash Concentration

However, note that, Cash Concentration has the following demerits:(d) Mailing Delay Increases(e) Clearing Delay Increases (for clearing of outstation cheques)(f) Additional Cost incurred for settlement of outstation cheques

Concentration Banking• Open Account with a Bank having branch at each location where

cheques are collected• Cheques are Collected by the Company• Cheques are deposited at the respective Branches• Cheques are cleared through Local Clearing• Funds are Transferred to a Central Account (under control of HO)

This system of Banking is called Concentration Banking

The Bank with which the Central Account is maintained is called the Concentration Bank

In case, the Concentration Bank does not have accounts at all locations it enter

into an arrangement with some other Bank (Corresponding Bank)

Concentration Banking helps to minimize:(a) Mailing Delay(b) Clearing Delay(c) Costs associated with Outstation Clearing

Cash Management System

Most Banks are offering the CMS Service as a Corporate Banking Solution

CMS is a Concentration Banking System with the following add-on facilities:

(a) Cheque Pick-up Facility(b) Same Day Credit (even for Non-High Value Cheques), pending

clearing [High Value Clearing > Rs. 1.00 Lacs] for local cheques(c) Instant Fund Transfer to the Central Account or any Account as

specified by the Client(d) In case of outstation cheques, the Cash is available within 2 days

from the date of collection of the Cheque

The Banks offer the service at a Fee

CMS was first started in India by Corporation Bank and then followed by the Citi Bank.

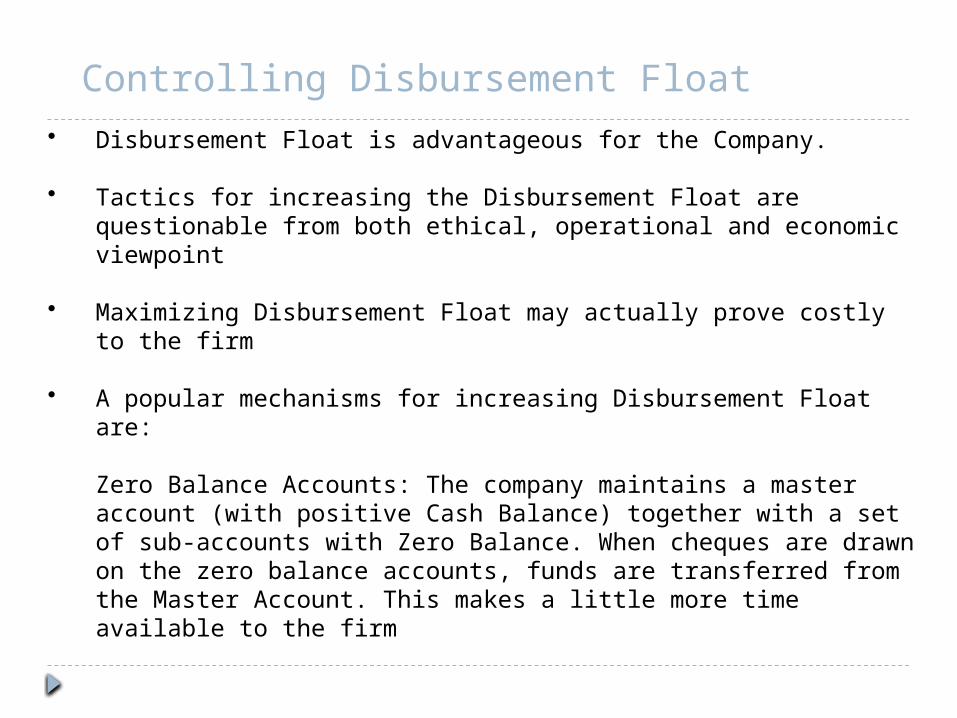

Controlling Disbursement Float• Disbursement Float is advantageous for the Company.

• Tactics for increasing the Disbursement Float are questionable from both ethical, operational and economic viewpoint

• Maximizing Disbursement Float may actually prove costly to the firm

• A popular mechanisms for increasing Disbursement Float are:

Zero Balance Accounts: The company maintains a master account (with positive Cash Balance) together with a set of sub-accounts with Zero Balance. When cheques are drawn on the zero balance accounts, funds are transferred from the Master Account. This makes a little more time available to the firm

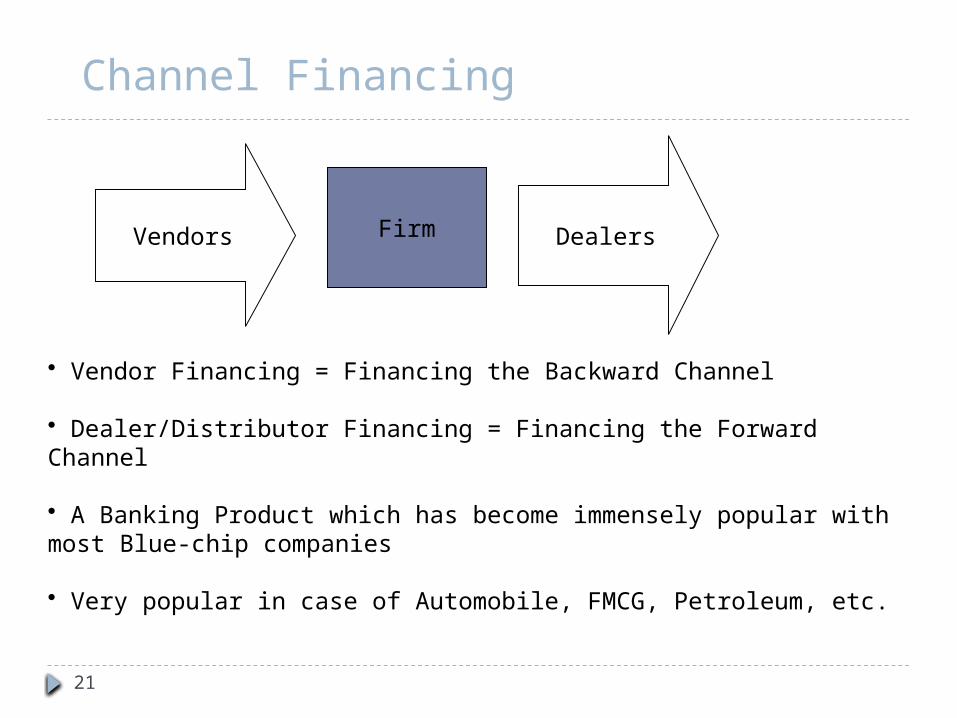

Channel Financing

Channel Financing

21

FirmVendors Dealers

• Vendor Financing = Financing the Backward Channel

• Dealer/Distributor Financing = Financing the Forward Channel

• A Banking Product which has become immensely popular with most Blue-chip companies

• Very popular in case of Automobile, FMCG, Petroleum, etc.

Channel Financing…Contd.

22

Mechanism of Channel Financing (Forward Channel)

• Principal Company negotiates with a Bank and arranges for individual Credit Limit (from Bank) for the Dealers

• After sales, the receipted copy of the invoice is sent to the Bank

• Bank pays the principal company the Invoice Amount

• The corresponding amount is treated as Credit given to a particular dealer

• The Dealer has to pay the Bank the amount along with the Interest

• The arrangement improves the Cashflow position of the Principal

• Because the Principal negotiates with the Bank on behalf of a large number of dealers, the arrangement enables the Dealers to get better Deal (Limit & Interest Rate) that what each could have managed in case it negotiated individually

Channel Financing…Contd.

23

• Channel Financing is of two types:

(a) Without Recourse: In case of default by the Dealer, the Bank takes up the case with the dealer

(b) With Recourse: Should there be a defaulting dealer, the Principal stands as the guarantor with a commitment to pay back to the bank

• Typically, Interest Rates for Channel Financing Without Recourse is higher than that for Channel Financing with Recourse

Factoring

Risks: International Transactions

25

Apart from Credit Risk and Sovereign Risks, the International Transactions have the following additional Risks:

Translation Risk • With fluctuations in Exchange Rates [since the previous reporting period], Assets, Liabilities, Revenues, Expenses, Profits and Losses can change

• Applicable to Multinational and Transnational Companies

Transaction Risk• Changes in the value of Foreign Currency Denominated contracts due to the change in Exchange Rates

• Change in the value of these Contracts can change the Future Cash Flows of the Exporter/Importer

• The resulting differentials are known as Currency Gains and Losses

• Receivables, can suffer considerable change because of of the Transaction Risk

Risks: International Transactions…contd.

26

Operating Risk • Currency Fluctuations can have an impact on the future Cash Flows of the Exporter/Importer

• With the exchange rate fluctuations, the Competitive Position of the Exporter/Importer can change and, hence, the associated Cash Flows can change

• Exchange Rate fluctuations can alter the scenarios associated with Export/Import

Economic Risk

• Operating Exposure + Transaction Exposure, which sums up the change in Future Cash Flows of the Exporter/Importer

• The Economic Risk can directly affect the VALUE of the Exporter/Importer

What it Means?

27

• Exporters perceive more than normal risk in their customers

• Importers perceive more than normal risk in their suppliers

• Banks/ Financial Institutions perceive more than normal risks in funding Exporters/Importers

• Stringent norms guide Export Finance

• More than normal security is enforced by banks

• LCs guided by the Doctrine of Strict Compliance

• Due to the stringent norms associated with LCs, the instrument is losing popularity and most customers are unwilling to open LCs because of higher cost and time

International Factoring

28

An agreement between the Exporter and the Factor by means of which:

• Export Receivables are sold to the Factor

• Assignment of Title of the goods and services to the Factor

• Factor becomes responsible for credit control and debt collection

Most international Banks offer Factoring Services in various countries

There are specialized Factors (other than Banks) who operate in various countries

Factoring is becoming increasingly popular mode of Export Financing

How it Operates?

29

Exporter Importer

Export Factor

Import FactorIn

tern

ati

onal B

oun

dary

Goods

Payment

Payment

Payment

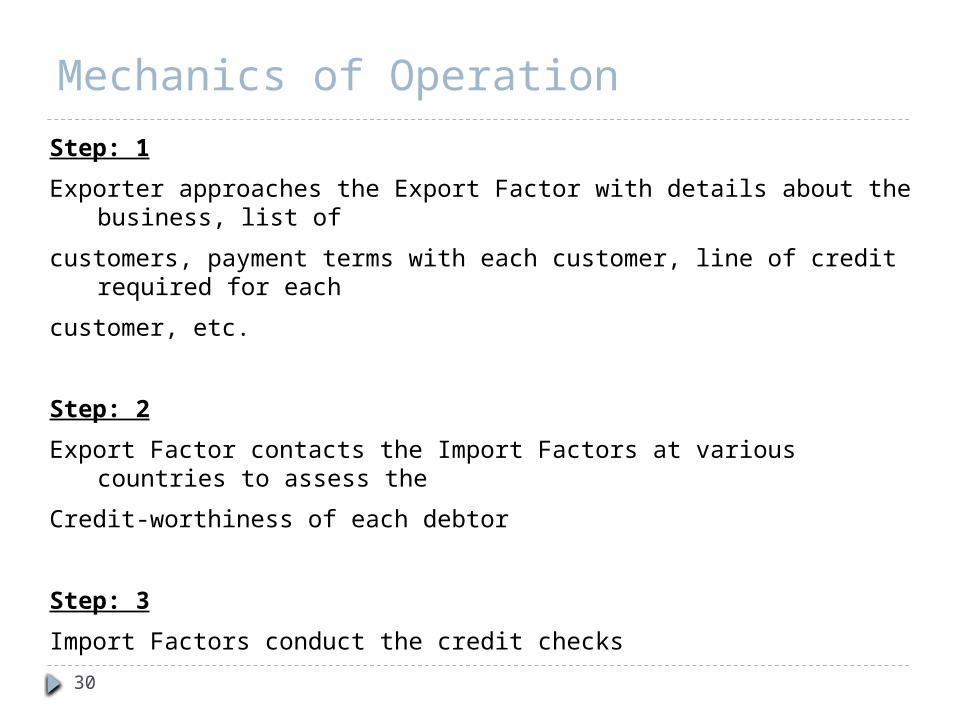

Mechanics of Operation

30

Step: 1

Exporter approaches the Export Factor with details about the business, list of

customers, payment terms with each customer, line of credit required for each

customer, etc.

Step: 2

Export Factor contacts the Import Factors at various countries to assess the

Credit-worthiness of each debtor

Step: 3

Import Factors conduct the credit checks

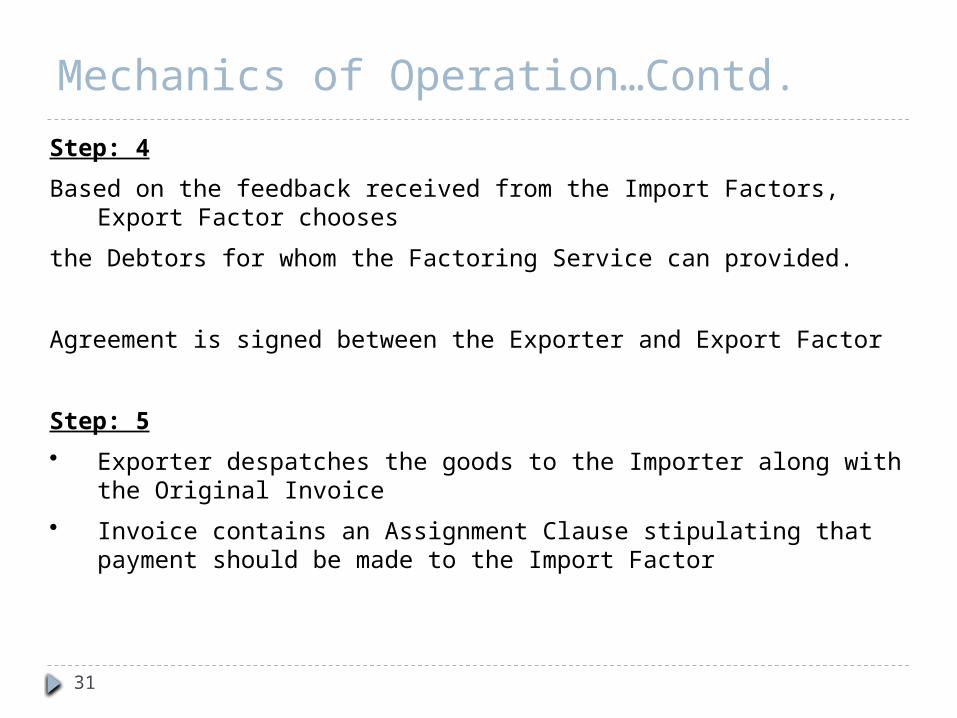

Mechanics of Operation…Contd.

31

Step: 4

Based on the feedback received from the Import Factors, Export Factor chooses

the Debtors for whom the Factoring Service can provided.

Agreement is signed between the Exporter and Export Factor

Step: 5

• Exporter despatches the goods to the Importer along with the Original Invoice

• Invoice contains an Assignment Clause stipulating that payment should be made to the Import Factor

Mechanics of Operation…Contd.

32

Step: 6

• 2 Copies of the Invoice are sent to the Export Factor

• Exporter releases a pre-agreed part of the Invoice Value

Step: 7

Export Factor despatches a copy of the Invoice to the Import Factor

Step: 8

Import Factors collects payments from the Importers and remits to the Export

Factor

Mechanics of Operation…Contd.

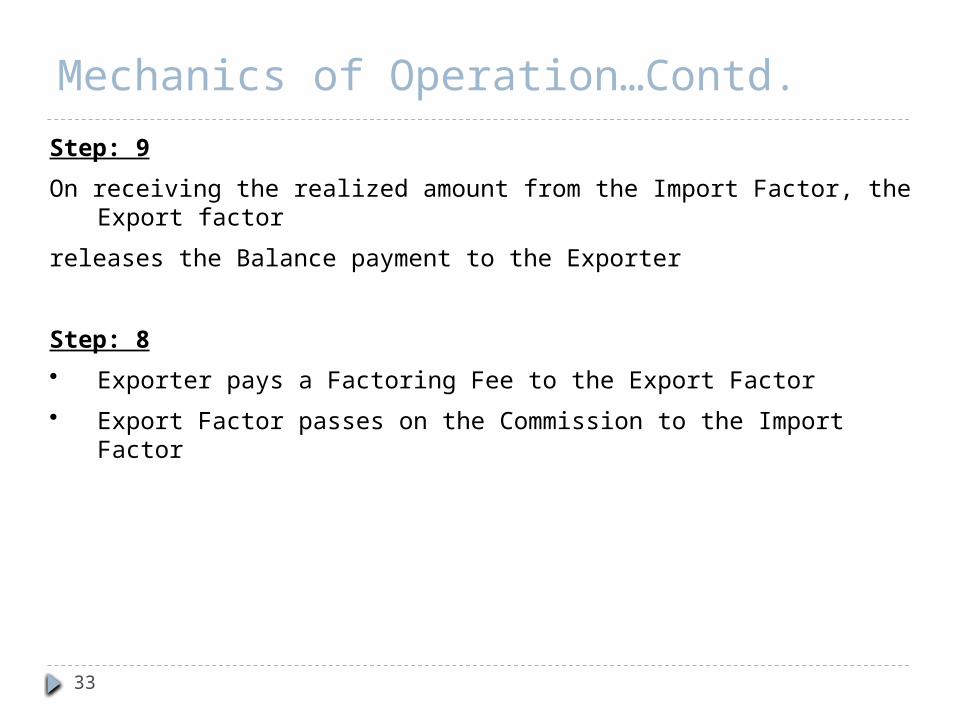

33

Step: 9

On receiving the realized amount from the Import Factor, the Export factor

releases the Balance payment to the Exporter

Step: 8

• Exporter pays a Factoring Fee to the Export Factor

• Export Factor passes on the Commission to the Import Factor

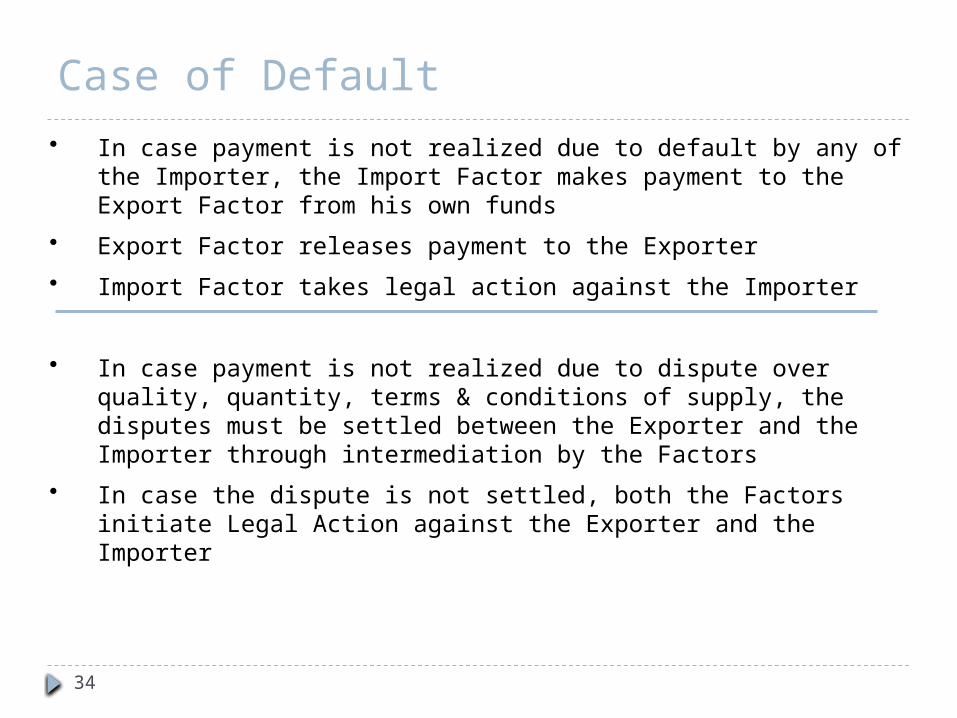

Case of Default

34

• In case payment is not realized due to default by any of the Importer, the Import Factor makes payment to the Export Factor from his own funds

• Export Factor releases payment to the Exporter

• Import Factor takes legal action against the Importer

• In case payment is not realized due to dispute over quality, quantity, terms & conditions of supply, the disputes must be settled between the Exporter and the Importer through intermediation by the Factors

• In case the dispute is not settled, both the Factors initiate Legal Action against the Exporter and the Importer

Factoring - Advantages

35

• Immediate Finance upto a certain percentage (75-80%) of Export Receivables

• The payment is released by the factor even if the sales is not backed by an LC

• Credit checking of the overseas debtors is done by the Factor – with the help of its own database and/or database of factors operating in the country of the debtors and/or international credit rating agencies

• Collections from the debtors are done in a “diplomatically correct” yet efficient way

• Factors provide protection against bad debts upto 100% for pre-agreed debtors

• Factors provide consultancy services in relation to the special laws regulations, etc. of the countries to which products are exported

Factoring - Disadvantages

36

• Delay in Credit Decisions

• Delay in Remittance of Funds

• Elaborate Documentation

Export Financing from Commercial Banks

Export Finance in India

38

• Commenced in 1967 by RBI

• Goal: Make available short term finance to exporters at internationally comparable interest rate

• RBI fixes the ceiling on interest rates to be charged by the Banks

• Banks are free to charge lower interest rates based on their assessment of the borrower

Exporters are given Preference

39

• Focus on increasing Exports – Exports EARN FOREX

• Minimum 12% of the Net Bank Credit to be allocated for Financing Exports

• Performance of each Bank is quarterly reviewed by the Directives Division of RBI

• Concession in Interest Rates: PLR-2.50% upto 180 Days

• Timelines for Credit Decision

(a) Fresh Sanction/ Enhancement: Within 45 Days

(b) Renewal: Within 30 Days

(c) Adhoc Facility: Within 15 Days

• Quarterly Reporting to RBI (Annexure 2 of the Master Circular, July, 2007)

• CONCERN: Export Credit should not be Misused

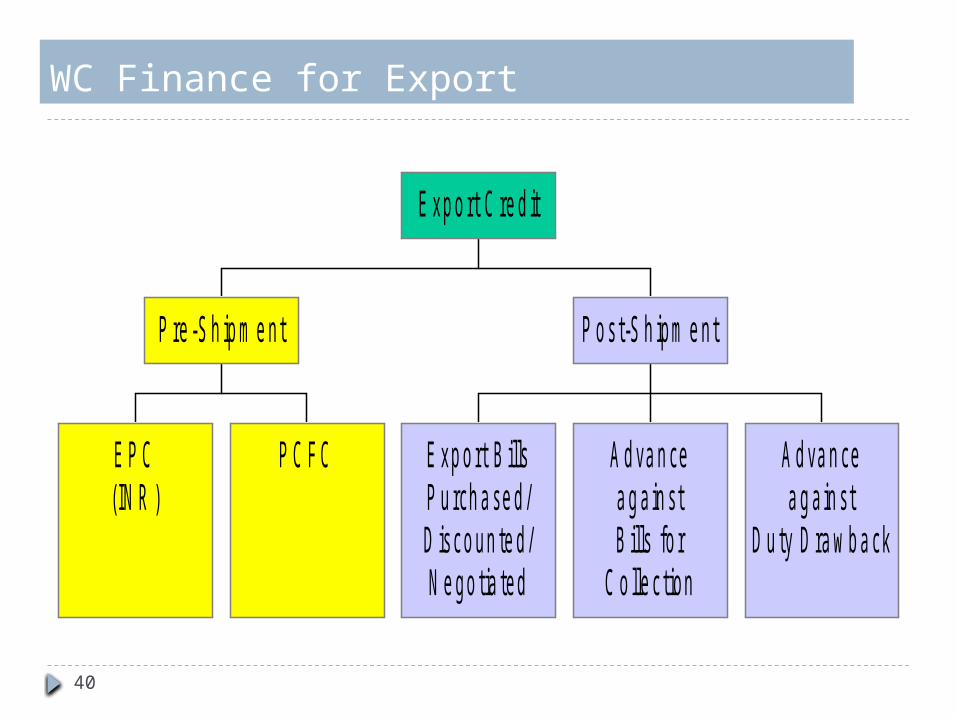

WC Finance for Export

40

E P C(IN R )

P C F C

P re -S h ip m e nt

E xp o rt B illsP u rch a se d/D isco un te d /N e go tia ted

A d va n cea g a in stB ills fo r

C o lle c tion

A d va n cea g a in st

D u ty D ra w b a ck

P o s t-S h ipm e nt

E xp o rt C re d it

Pre-Shipment Credit: Definition

41

Loan provided by a bank to an exporter for financing

• purchase, processing, manufacturing and packing of goods prior to shipment

• working capital expenses towards rendering services

On the basis of

• the LC opened in his favour or in favour of some other person by an overseas buyer

• a confirmed and irrevocable order for the export of goods/services from India

• any other evidence of an order for export from India having been placed on the exporter

Unless, lodgement of Export Order or LC with the Bank has been waived

Post-Shipment Credit - Definition

42

Post-shipment Credit is any loan or advance granted or any other credit provided

by a bank to an exporter of goods/services from India, from the date date of

shipment of goods to the date of realization of export proceeds

AND/OR

Includes any loan or advance granted to an exporter, in consideration of, or on

the security of any duty drawback allowed by the Government from time to time.

Mechanism of Export Credit

43

Exporter

Bank

Overseas Buyer

Order/LC

Intim

atio

n

Dr

Goods

Exp

ort D

ocs

Cr Dr

Remittance

Cr