Ways to Boost Your Credit Score

22

1 WHY YOUR CREDIT SCORE IS SECRETLY COSTING YOU THOUSANDS OF DOLLARS AND WHAT TO DO ABOUT IT By: R.J. Weiss CFP®, Personal Lines Customer Specialist

-

Upload

raymond-weiss -

Category

Documents

-

view

223 -

download

0

description

It’s safe to say, understanding ways to improve your credit score and how your credit score works can save you over a hundred thousand dollars over your lifetime. Don’t believe me? Let’s say you obtain a $250,000 home loan on a 30 year mortgage. With a 4% fixed mortgage, you will make total payments over 30 years of $429,674 or $1,193.54 a month for 360 months. If your interest rate was instead 6% due to your credit history, your total payments over 30 years will be $539,596 or $1,499 per month for 360 months. A difference of $109,922! Do I have your attention now? The savings doesn’t stop. Your credit score is factored into how much you pay for home and auto insurance also... ...And it’s not a few dollars a year difference. You can save hundreds of dollars a year on home and auto insurance by optimizing your credit score. There are a ton other benefits at well. If you're interested in ways to improve your credit score and raising your credit score, here's the guide you need!

Transcript of Ways to Boost Your Credit Score

1

Why your Credit SCore iS SeCretly CoSting you thouSandS of dollarS and What to do about itBy: R.J. Weiss CFP®, Personal Lines Customer Specialist

2

It’s safe to say, understanding how credit scoring works can save you over a hundred thousand dollars over your lifetime.

Don’t believe me?

Let’s say you obtain a $250,000 home loan on a 30 year mortgage. With a 4% fixed mortgage, you will make total payments over 30 years of $429,674 or $1,193.54 a month for 360 months.

If your interest rate was instead 6% due to your credit history, your total payments over 30 years will be $539,596 or $1,499 per month for 360 months. A difference of $109,922!

Do I have your attention now?

The savings doesn’t stop. Your credit score is factored into how much you pay for home and auto insurance also...

...And it’s not a few dollars a year difference. You can save hundreds of dollars a year on home and auto insurance by optimizing your credit score.

Other benefits include:

• Other loans, such as auto, will have a lower interest rate. You’ll also have more negotiating power as banks love to deal with clients with a high credit score.

• If you rent, even long-term vacation rentals, it’s easier to do so with good credit history.

• You’ll get better credit card offers and interest rates

• And much more...

At Weiss Insurance Agencies, our mission is to properly insure homeowners in Illinois and the Midwest, for the best possible price.

Based on our mission, I feel there’s an obligation to provide current and future clients with information to help them improve their credit score, so they can pay less in insurance...

introduCtionabout r.J. Weiss CfP®, PlCS

3

underStanding your Credit hiStory

What Makes up your Credit Score?

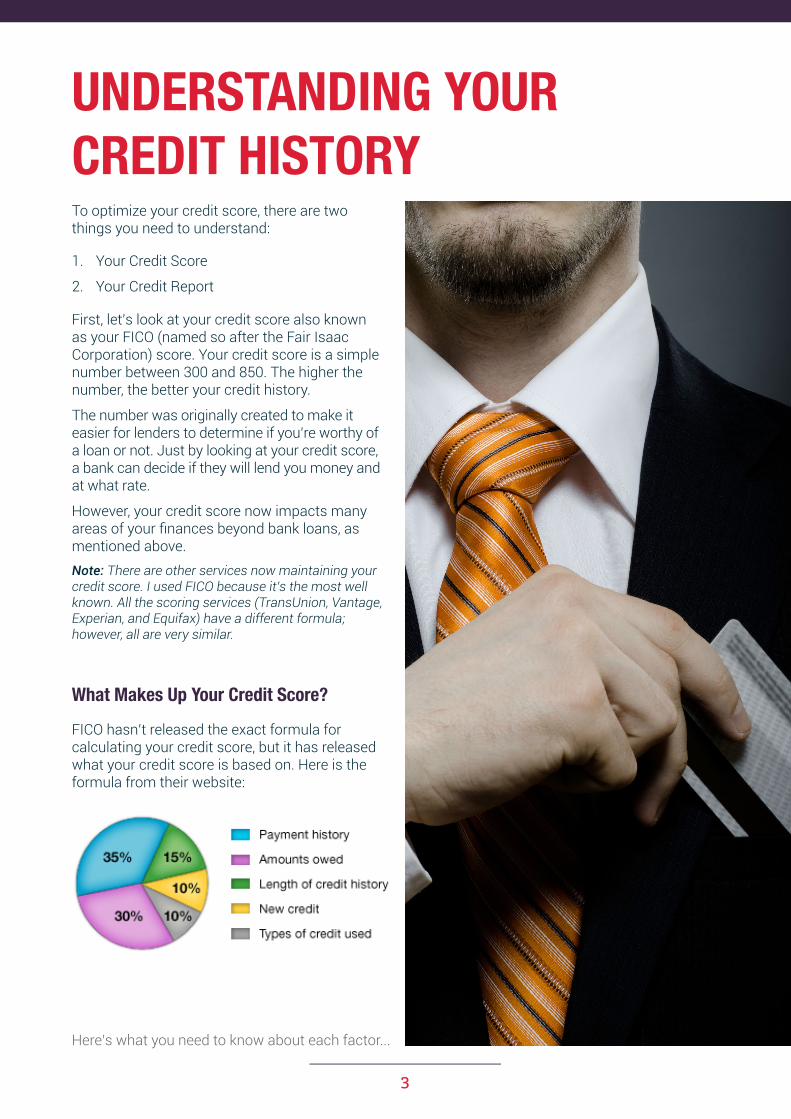

To optimize your credit score, there are two things you need to understand:

1. Your Credit Score

2. Your Credit Report

First, let’s look at your credit score also known as your FICO (named so after the Fair Isaac Corporation) score. Your credit score is a simple number between 300 and 850. The higher the number, the better your credit history.

The number was originally created to make it easier for lenders to determine if you’re worthy of a loan or not. Just by looking at your credit score, a bank can decide if they will lend you money and at what rate.

However, your credit score now impacts many areas of your finances beyond bank loans, as mentioned above. Note: There are other services now maintaining your credit score. I used FICO because it’s the most well known. All the scoring services (TransUnion, Vantage, Experian, and Equifax) have a different formula; however, all are very similar.

FICO hasn’t released the exact formula for calculating your credit score, but it has released what your credit score is based on. Here is the formula from their website:

Here’s what you need to know about each factor...

15% of your credit score is based upon how long you have had credit. The longer your credit history, the better.

This is why it’s a good idea to apply for a card when you’re young and keep that card for life. It’s also why it’s a bad idea to cancel your oldest card.

Although it’s not my primary card, I still have my first card for this reason. I use it to pay my cable bill, which is automatically billed each month.

I keep this card active because you want to always have some activity on your credit. Like I mentioned before, applying for a credit card and then never using it, can actually hurt your credit card.

Would you lend $100 to a friend who just borrowed $100 from three other friends? Of course not. Which is why lenders, don’t like to see a lot of new activity, including credit inquiries, on your credit history.

Lenders prefer to see a variety of credit on your credit score. For example, it’s better to have a student loan, one credit card, and a car loan then three credit cards.

This is only 10% of your score, so don’t go out and buy or car or a house just to get variety. The most common mistake made here is carrying too many credit cards.

Many people try to crack the FICO equation, to determine their exact credit score. FICO has never and will never release the exact equation.

It all comes down to common sense though. Pay your bills on time (even if you’re making minimum payments), don’t use all of your credit available, and don’t close your oldest account.

PayMent hiStory - 35%

aMountS oWed - 30%

length of Credit hiStory - 15%

neW Credit - 10%

tyPeS of Credit uSed - 10%

What it all CoMeS doWn to

Your payment history takes in account the timing of your past payments on accounts such as your credit card, retail accounts, and your mortgage. It also takes into account any bills that have gone to collection.

A quick story, back in college I was in a car accident. Wasn’t my fault but the other driver didn’t have insurance. He was going to pay me out of pocket. I had the bill sent to my dorm room. However, I switched dorm rooms over semesters and didn’t receive the bill. Being a dumb 19 year old, I kind of put the situation aside and thought it was taken care of somehow. Turns out the bill ended up going to collections. This one mistake six years ago cost me when I went to apply for a mortgage.

It’s not rocket science, if you want to improve your credit score, pay your bills on time. It’s the #1 thing you can do.

The amount owed is the next biggest weight on your credit score. It’s also commonly referred to as, your credit utilization rate.

This is a ratio of the amount you owe and the amount available. It also takes into account the number of accounts you have with balances.

This perfect credit utilization rate isn’t known. However, we do know some basic facts:

• Don’t max or come close to maxing out your available. A good rule of thumb is to not go beyond 33% of your available credit.

• You want to use at least some credit. Therefore, a utilization rate of 0% could actually hurt your credit score.

Shoot for the lowest percentage you can, with a reasonable credit limit. A good rule of thumb is that your credit limit shouldn’t exceed your emergency fund.

If you’re responsible with paying your bills on time, I repeat if you’re responsible for paying your bills on time, a good tactic to increase your utilization rate is to call up your credit card company and ask for a limit increase.

Please only do this if you have always managed to pay your bills on time (yes I know, I said that 3 times but it’s really important) and have an adequate emergency fund. Otherwise, it could end up hurting you in the long run.

So now that you know 99% of what there is to know about credit scores, you probably want to see what your score is.

There’s two ways to get your credit score, one is more accurate but does require your credit card

hoW to get your Credit SCore

information because after 10 days you’re signed up for a monthly subscription (which you can cancel). The other is more of an estimate but requires no credit card.

6

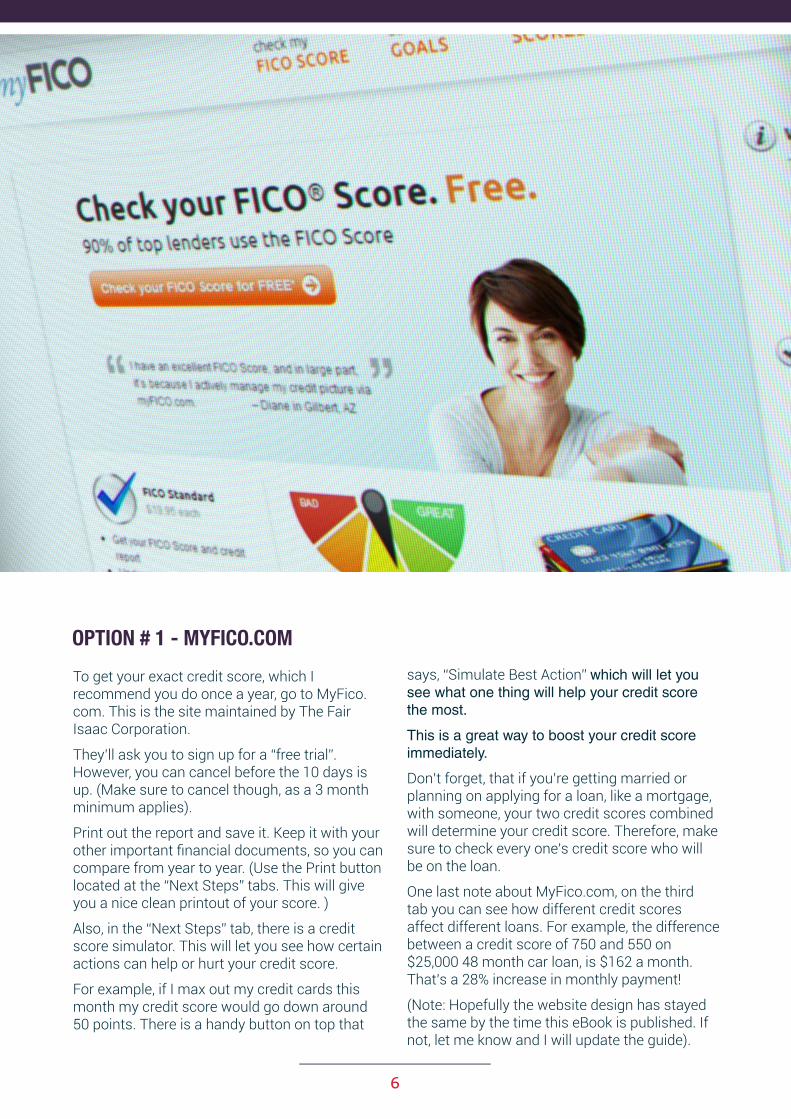

To get your exact credit score, which I recommend you do once a year, go to MyFico.com. This is the site maintained by The Fair Isaac Corporation.

They’ll ask you to sign up for a “free trial”. However, you can cancel before the 10 days is up. (Make sure to cancel though, as a 3 month minimum applies).

Print out the report and save it. Keep it with your other important financial documents, so you can compare from year to year. (Use the Print button located at the “Next Steps” tabs. This will give you a nice clean printout of your score. )

Also, in the “Next Steps” tab, there is a credit score simulator. This will let you see how certain actions can help or hurt your credit score.

For example, if I max out my credit cards this month my credit score would go down around 50 points. There is a handy button on top that

oPtion # 1 - MyfiCo.CoM

says, “Simulate Best Action” which will let you see what one thing will help your credit score the most.

This is a great way to boost your credit score immediately.

Don’t forget, that if you’re getting married or planning on applying for a loan, like a mortgage, with someone, your two credit scores combined will determine your credit score. Therefore, make sure to check every one’s credit score who will be on the loan.

One last note about MyFico.com, on the third tab you can see how different credit scores affect different loans. For example, the difference between a credit score of 750 and 550 on $25,000 48 month car loan, is $162 a month. That’s a 28% increase in monthly payment!

(Note: Hopefully the website design has stayed the same by the time this eBook is published. If not, let me know and I will update the guide).

7

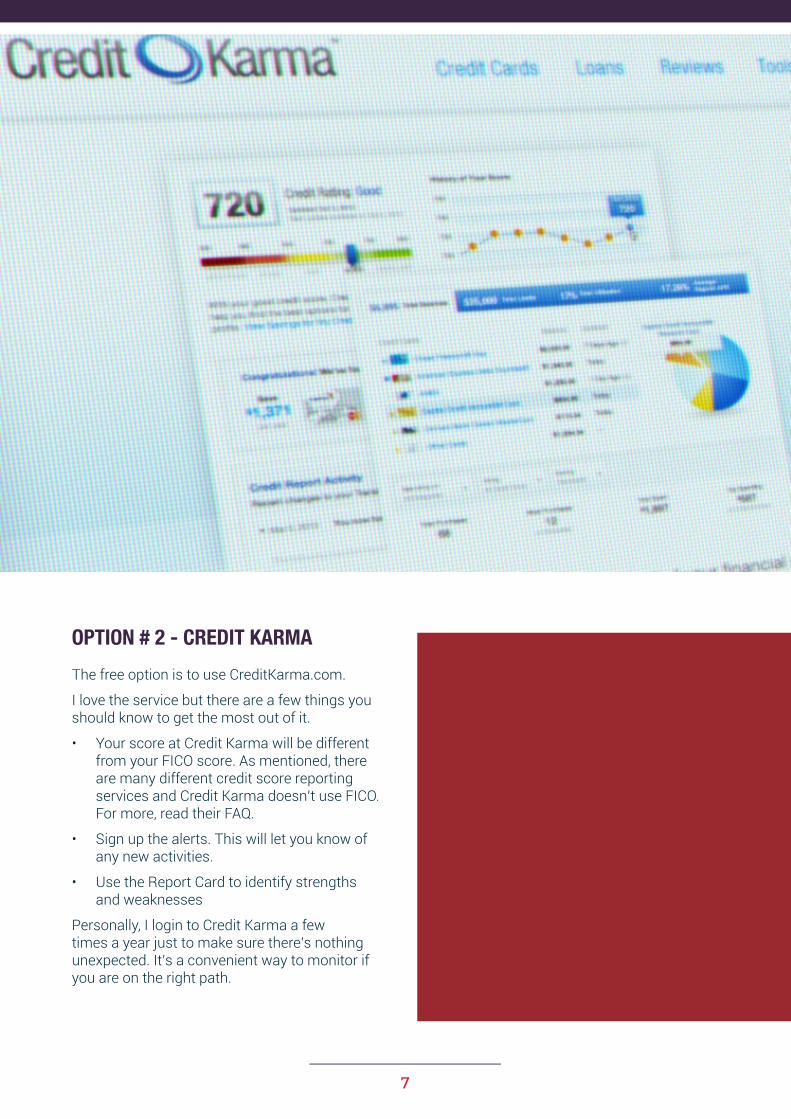

The free option is to use CreditKarma.com.

I love the service but there are a few things you should know to get the most out of it.

• Your score at Credit Karma will be different from your FICO score. As mentioned, there are many different credit score reporting services and Credit Karma doesn’t use FICO. For more, read their FAQ.

• Sign up the alerts. This will let you know of any new activities.

• Use the Report Card to identify strengths and weaknesses

Personally, I login to Credit Karma a few times a year just to make sure there’s nothing unexpected. It’s a convenient way to monitor if you are on the right path.

oPtion # 2 - Credit KarMa

8

Your credit report is a more detailed report of your past credit history. It provides a future lender with just about financial transaction from your past. A little scary, but true.

Getting your credit report is simple and free. Go to annualcreditreport.com.

You’re entitled to a free copy of your credit report from each of the report agencies once a year. You can get these all at once or over a period of a year.

I prefer to spread it out, just in case someone requests a copy of my credit report, I don’t have to pay to get one.

Once you get your credit report, review it!

You want to double check everything. Even basic information such as your name, social security number, address, etc... You won’t believe how many stories I have heard of this information being incorrect, and consequently, negatively affecting someone’s credit without them knowing it.

Besides your basic information, you need to review everything on your credit history. Start from the first page and work your way toward the end.

To show you what you should be looking for, I’m going to take you through a recent copy of my credit report. (The report varies depending on what credit bureau you obtain it from, so don’t worry if yours isn’t the same).

the Credit rePort

9

If you have any unpaid bills that were sent to collections, this is where they’re listed.

orth mentioning is that, Chapter 7, 11, and 12 bankruptcies and unpaid tax liens will remain up to ten years.

The next section gives my accounts that are paid up to date, along with a balance history. Mine include three credit cards and one mortgage. All accounts status currently list “Open/Never late”, a great sign.

On one of my credit card accounts, I’m listed as an authorized user. Meaning it’s not responsibility to pay the bill. Even though this isn’t my credit card, being an authorized user still affects my credit rating.

A bit of history on the authorized user because this has been a back and forth issue. One of the ways you used to be able to increase your credit score was to add yourself as an authorized user to an account

Potentially negative iteMS or iteMS for further revieW

aCCountS in good Standing

in good standing. For example, if your parents had good credit, you can ask for them to add you as an authorized user and their credit history would go on your credit history.

FICO figured out this trick quickly and decided to eliminate authorized user status from the credit score equation for a short time. About two months after, the reversed their decision after the changed reversed their decision stating:

“After consulting with the Federal Reserve Board and the Federal Trade Commission earlier this year, Fair Isaac has decided to include consideration of authorized user trade lines present on the credit report in the FICO 08 model.” - Tom Quinn, Vice President of Global Scoring Solutions for Fair Isaac Corporation

I don’t know this for a fact, but from reading in between the lines I’m guessing that there is no way being an authorized user helps your credit. If the account holder is in good standing and has a good history of paying its bills, it will have no effect at all.

If the account is in bad standing, it will negatively affect your score. Therefore, if you’re an authorized user on an account with a bad credit history, ask to be removed immediately. (You might want to send them this book, while you’re at it)

10

Record of Requests for Your Credit History (Hard Inquiries)

Hard inquiries are done when you’re taking on additional financial obligation. Unfortunately, many businesses don’t come right out and tell you that they are performing a hard inquiry on your credit. However, it does make its way into the fine print.

The most common hard inquiries you will find on your credit report include:

• Banks & Credit Unions

• Credit Card Companies

• Car Dealers

• Insurance Companies – They’re required by law to ask.

• Property Management Companies & Landlords

• Phone & Cable Companies

• Utility Companies

Here’s the statement from Experian on my credit report:

“We make your credit history available to your current and prospective creditors and employers as allowed by law. Experian may list these inquiries for two years so that you will have a record of the companies that accessed your credit information.

The section below lists all of the companies that have reviews your credit history as a result of action you took, such as applying for credit or financing or as a result of a collection. The inquires in this section are shared with companies that view your credit history.”

Each hard inquiry on your credit report will lower your anywhere between 5 and 10 points. If you’re worried about your credit score, anytime before you open a new account just ask if they perform a hard pull on their credit.

aCCountS in good Standing

11

Other Ways to Limit Hard Inquires include:

1. Ask - Anytime you’re opening a new account, ask if they are pulling your credit, when they are pulling your credit, how many times they are going to pull your credit, and how you can get that removed.

2. Don’t Rate Chase - A common, but damaging trend is to chase low introductory rates on credit cards. The more accounts you open, the more hard inquiries you will see on your credit.

3. Avoid Applying to Receive 10% Discount - When you’re checking out at a popular retail store they will ask you if you want to save 10% today by applying for a store card. The same trick is done by issuing free T-Shirts at sporting events or pizzas on college campus. Every time you fill out an application, they pull a hard inquiry.

4. Don’t Do Business With Companies That Routinely Check Your Credit - A lot of businesses will make it a habit to pull your credit on a regular basis. Unfortunately, this is legal because they put it on the 22nd page of their terms and conditions that you had agreed to.

5. Avoid A Sharp Increase in Inquiries - This isn’t exactly a tip to eliminate a hard inquiry, but it’s still important. Many people, who want to get a credit card, will go out and apply for 4 or even ten credit cards at once. Please avoid doing this. It shows you’re in desperate need for credit, which isn’t what a future lender wants to see.

6. Avoid Don’t Pay Till 2014 Deals - Say you went into Best Buy and want to buy a brand new big screen. They have a promotion going on that says, “0% Financing to 2014”.

12

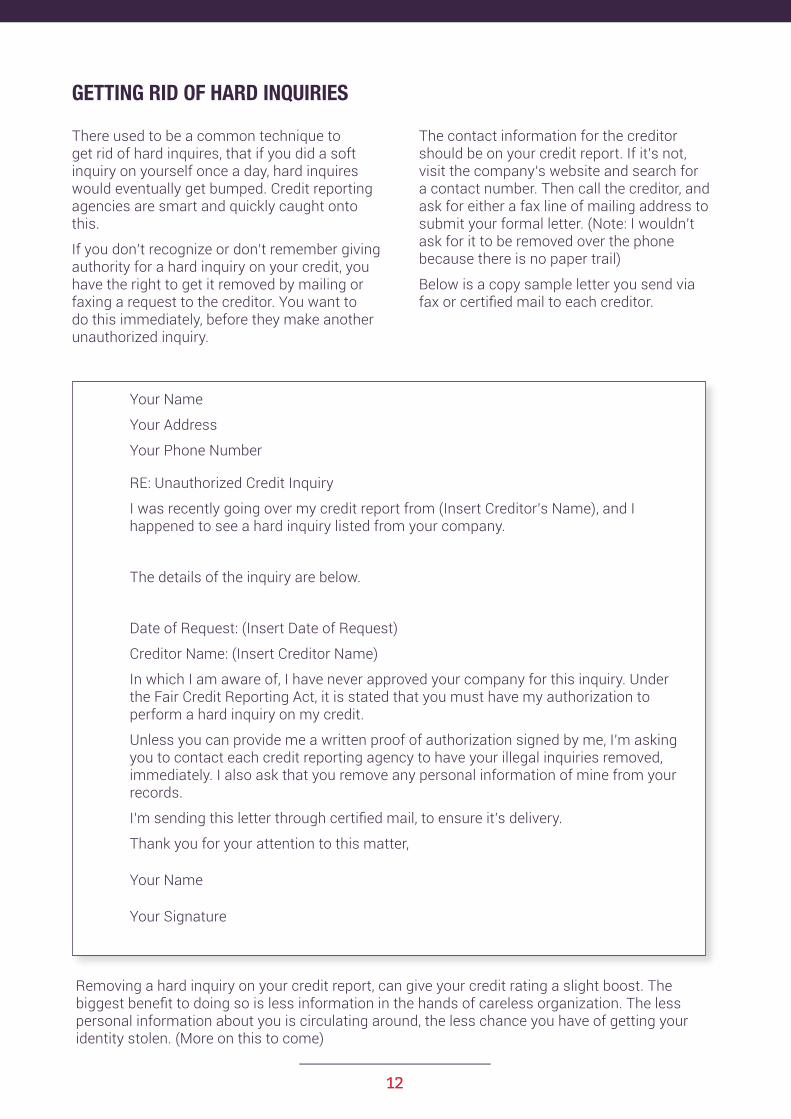

There used to be a common technique to get rid of hard inquires, that if you did a soft inquiry on yourself once a day, hard inquires would eventually get bumped. Credit reporting agencies are smart and quickly caught onto this.

If you don’t recognize or don’t remember giving authority for a hard inquiry on your credit, you have the right to get it removed by mailing or faxing a request to the creditor. You want to do this immediately, before they make another unauthorized inquiry.

getting rid of hard inquirieS

Your Name

Your Address

Your Phone Number

RE: Unauthorized Credit Inquiry

I was recently going over my credit report from (Insert Creditor’s Name), and I happened to see a hard inquiry listed from your company.

The details of the inquiry are below.

Date of Request: (Insert Date of Request)

Creditor Name: (Insert Creditor Name)

In which I am aware of, I have never approved your company for this inquiry. Under the Fair Credit Reporting Act, it is stated that you must have my authorization to perform a hard inquiry on my credit.

Unless you can provide me a written proof of authorization signed by me, I’m asking you to contact each credit reporting agency to have your illegal inquiries removed, immediately. I also ask that you remove any personal information of mine from your records.

I’m sending this letter through certified mail, to ensure it’s delivery.

Thank you for your attention to this matter,

Your Name

Your Signature

The contact information for the creditor should be on your credit report. If it’s not, visit the company’s website and search for a contact number. Then call the creditor, and ask for either a fax line of mailing address to submit your formal letter. (Note: I wouldn’t ask for it to be removed over the phone because there is no paper trail)

Below is a copy sample letter you send via fax or certified mail to each creditor.

Removing a hard inquiry on your credit report, can give your credit rating a slight boost. The biggest benefit to doing so is less information in the hands of careless organization. The less personal information about you is circulating around, the less chance you have of getting your identity stolen. (More on this to come)

13

Soft inquiries are inquires that you’re not even aware of. For example, the companies that send you pre-approved credit card applications through the mail perform a soft inquiry before sending you that application. Soft inquiries have no bearing on your credit score.

On my credit report from Experian it states in bold letters:

“We offer credit information about you to those with a permissible purpose, for example to:

• Other creditors who want to offer you preaproved credit

• An employer who wished to extend an offer of employment

• A potential investor is assessing the risk of a current obligation

• Experian Consumer assistance to process a report for you

• Your current creditors to monitor your accounts

• A static copy of your credit report provided to a subsequent user necessary to complete your mortgage loan application

These inquiries do not affect your credit score.”

Although they don’t have any bearing on your credit score, it’s still interesting to take a look at what companies are looking up your credit history each year.

inquirieS Share only With you (Soft inquirieS)

CoMMon queStionS about Credit rePortS

What do i do if there is an error on my Credit report?

What is revolving Credit?

does applying for a Credit Card hurt your Credit Score?

If something is wrong on your credit report, you want to immediately contact the reporting agency that issued the report.

The FTC has great instructions on what to do if there are any errors. Follow their steps, including using their template. Make sure to copy anything you send, for your own records and record dates of everything you send.

Revolving credit is a term used for credit that has no expiration. For example, a car payment, student loans, or a mortgage isn’t considered revolving because you eventually pay these types of loans off. Otherwise known as installment credit.

A credit card is a revolving payment because the credit is always available. As long as you pay it off each month, it’s always there for you.

Your FICO score looks at the amount of revolving credit you have compared to installment credit. The less revolving credit the better, in the eyes of FICO. If you’re looking for a quick increase in your credit score, a great way to achieve this is by paying off your revolving credit.

Yes, applying for a credit card is a hard inquiry, which can negatively affect your credit score in the short-term. You can expect your credit score to go down around 5 points for six months any times a hard pull is done.

Keep this in mind, if you’re applying for a loan in the near future. For example, don’t apply for a new credit card right before applying for a car loan, to increase your credit utilization rate. Last, this another great reason not to get that department store credit card or apply for a credit card for a free pizza.

opting out of Credit Card offers

Once I moved into a home, the amount of credit card offers I received was startling. Every day, I would receive at least one and sometimes more of the following applications in the mail; credit card, home equity line of credit, and mortgage insurance.

Luckily, I discovered OptOutPrescreen.com, where I can stop this junk mail from filling up my mailbox. The site was created as a result of Fair Credit Reporting Act and a link to the site can be found on the Federal Trade Commission’s website.

There are many advantages to stopping junk mail:

• No chance of someone stealing your credit card applications through the mail.

• Out of sight, out of mind. You willn’t be tempted to sign up for any credit card offers that you don’t need.

• Save paper.

• The fewer the amount of companies with your social security number the better.

You can choose to either opt out electronically or permanently by mail. If you choose electronically, you will be opted out for only 5 years. If you choose to opt out by mail, you will never receive a credit card offer again.

I wasn’t tracking the days to the exact date, but I would estimate that around four weeks after opting out, I was no longer receiving any prescreened offers through the mail. In other words, I’m receiving as much junk mail as I am fan mail. (:

Another tip, if you’re also tired of receiving catalogs, there is a free service Catalog Choice that can help you reduce your junk mail even more. It’s pretty simple; you just enter in your address and the catalog number of the catalog you want to eliminate.

16

A credit freeze, also known as a credit lockdown or a security freeze, is a way to prevent new lines of credit being open underneath your name. When you apply a credit freeze, you’re issued a PIN (Personal Identification Number) by the credit reporting agency, which only temporally allows access to your credit by a third-party. Without this PIN, no one can have access to your credit report.

So why would someone want to freeze their credit?

Anyone who is at a high risk of getting their identity stolen, would benefit from applying a credit freeze in their account. For example, if you recently lost your wallet, which contained your social security number on your driver’s

license, now would be a good time to apply for a credit freeze.

With just the

• No one can open any new lines of credit, without the PIN.

• Extra steps for you to open a new line of credit, to prevent bad financial behavior.

• Less personal information of yours circulating around because companies can’t inquire about your credit history.

What’s a Credit freeze?

What’s a Credit freeze?

information on your driver’s license, someone could easily apply for a new line of credit in your name.

Another person who would be at high risk of identity theft is someone who has recently lost an important document through the mail. In general, any time your social security number is floating around, is a great time for you to apply for a credit freeze.

17

• Can’t immediately open any new lines of credit. This could cause problems when applying for a mortgage, car, etc...

• Small fee to freeze and unfreeze credit. For victims of identity theft, the fee is usually waived.

• Thieves can still use your existing accounts. Which brings me to a really good point: Never carry all of your credit or debit cards in one place. Say you lost your wallet, while you have placed a credit freeze on yourself. A lot of the time, it takes a few days to temporally unfreeze your credit because you have to send the request in through certified mail. So now you have no access to cash and are stuck waiting a few days, until your credit report unfreezes. Not a situation, you want to find yourself in.

Each state has different fees, laws, and regulations, on how to freeze your credit.

General rules are as follows:

• You have to apply with each different credit reporting agency. You can do this online. (Equifax, Transunion, and Experian)

• You must pay a small fee to freeze your credit

For additional protection against identity theft, review your homeowners or renters insurance policy (or just call us). Many policies contain coverage.

disadvantages of freezing how to freeze your Credit

18

1. Buy a Shredder - Shred anything you’re about to throw out with your personal information on it. Especially, anything with your social security number and applications (insurance, credit cards, phone, cable etc...)

2. Choose Hard Passwords and PIN’s and Store Them Offline - If your pin number is your birthday or your password is something as simple as your middle name and birthday, change it immediately. Also, there are a couple of Open Source options for password management, such as KeePass for Windows and KeyChain for Mac. Last, don’t choose similar passwords for your banking accounts. If a hacker has one, he has them all.

3. Have Emergency Cards and Copies - Never keep all of your information in one place, especially your wallet. Just because you have a credit card, doesn’t mean you have to carry it with you at all times.

4. Don’t Store SS # on Your License or Keep SS Card in Your Wallet

5. Never insert your credit card information, on a website you don’t trust.

6. Hold mail at the post office, when you’re out of town. Never let boxes and packages sit on a doorstep overnight.

7. Use Anti-Spyware software for your computer

8. Learn how to erase your hard drive, if selling or donating your old computer.

9. If you need to mail an important document, such as your taxes, either hand it to the mail man or drop it off in a collection box or at the post office.

10. Never give your personal information away over the phone from a solicitation.

11. Review your credit card bill every month. Make sure there is nothing on there that you don’t recognize. A lot of the time, thieves will a small charge initially on your account, wait a month to see if you notice it, then put a bigger charge later.

12. Don’t list your social security number on a resume, and then send it out to 20 companies online.

13. If you can manage to pay your bill in full each month, use a credit card instead of a debit card. Credit cards typically have better protection against identity theft.

14. Use ATM’s sparingly and never use an ATM late at night. There are plenty of people who like to look over your shoulder to see your ATM #.

15. Keep all of your checkbooks in a very secure place at home. Never store your checkbook in your purse, wallet, or car.

16. Use your shredder to get rid of old checkbooks.

17. Store copies of important documents and cards in a secure place in your house. Make sure to get copies of the front and back. If your credit card gets stolen, the number you want to call is on the back of your credit card.

18. Keep a list of everything in your wallet or purse. If you ever lose either, make sure that each account in your wallet was cancelled.

19. If you have an old credit card that you rarely use, make sure to check the balance monthly. You can ever use a service like Mint, to do all the tracking for you.

20. If you lose your license, ask for a new driver’s license number.

21. Freeze your credit, if you’re at high risk of identity theft.

22. Don’t keep deposit slips in your wallet. Store in a safe place, until you see that money deposited is correct, then shred.

disadvantages of freezing

19

23. When traveling in a place known for pick pocketing, don’t leave your wallet in your back pocket.

24. Don’t write your PIN on a little piece of paper and keep it inside your wallet.

25. If someone steals your purse with your keys inside, immediately contact your landlord or if you own, have your locks rekeyed.

26. If someone has stolen your wallet or purse, mark on your calendar to check your credit report one month after the incident.

27. Keep credit card receipts in a safe place. Never just toss, without looking to see if your full credit card number is listed.

28. Don’t give away your old ID

29. Limit the amount of credit cards you carry.

30. Use electronically delivery for every bill.

31. Pay bills online.

32. Never check a bank account or other personal accounts on a public computer. If you have to, delete the cookies.

33. Have new checks ordered to the bank. Never get them sent directly to your house. They come in a very obvious small box.

34. Don’t store your information on multiple sites. When you’re checking out of a retail store online, they will ask you to register as a user. Even if they don’t ask for your personal information, always check out as a guest.

35. If your Social Security # is on your health insurance card or any other type of statement, ask for it to be removed. Ask the company to create you a new ID # that isn’t your social security number.

36. Shred old documents. You only need to keep tax records for the previous seven years.

37. If you’re good with a scanner, keep your financial records on an external hard drive and hide it in a safe place.

38. Check your credit report at least once every six months. As I said previously, I alternate what credit report I can check every six months. Mark the date you check your credit report on your calendar.

39. Buy a secure safe for the house. Don’t just have a filing cabinet with a lock. Store your important documents such as passports, social security cards, tax returns, etc... in a safe and hide it away.

40. Use a gel pen with blank ink when you’re writing a check. Gel ink can’t be chemically altered.

41. If you start seeing credit card offers in the mail before your child turns 18, immediately ask for a credit report for them. Unfortunately, your child isn’t protected against identify theft. Credit card offers in the mail, are a sign that someone is attempting to steal your child’s identity.

42. Don’t leave your ATM receipt in the machine. Keep it in your pocket and shred it when you get home.

43. Anytime someone solicits you over the phone, ask to be deleted from their database effective immediately.

44. Did you know that if you’re being held up at an ATM, there is usually a secret code that your bank uses to alert authorities? For example, with some banks if you enter your password backwards, it will automatically have the ATM machine eat your card and say you have a zero balance. It varies per bank, so ask your bank if they have this feature if you find yourself using your ATM card by yourself a lot.

20

45. Know when and how your credit card statements usually arrive. If your statement comes by mail and is a few days late, go online and check your statement to make sure there are no fraudulent charges. If your statement arrives by email, and is more than one day late, immediately check your statement online. Missing statements could mean that someone changed either your email or physical address.

46. Avoid logging on from financial accounts from an unsecured wireless network.

47. Learn how to properly secure your home wireless network.

48. When on vacation, use the safe in the hotel room. Store your computer, phone, copies of passports and ID’s, in the safe at all times.

49. If you have a Smartphone, buy an app which deletes all the data on the phone the moment it’s stolen.

50. Always use cash at a bar. I’m sure we all know someone who has left the bar and still has a tab open. Therefore, the card stays in the bars possession overnight and is visible to every employee coming in that morning starting with the cleaning crew.

51. If you have a Landline register for the Do Not Call List by calling 1-888-382-1222.

52. If you see a mass forwarded email from one of your friends, marketing a product. It’s usually a scam. What normally happens is someone hacks into your friends account and sends a blast to everyone on their contact list. Be very suspicious if you receive an email from a friend that seems uncharacteristic.

The reason, I dedicated hours and hours to this project is I feel it’s an obligation I have, as an insurance agent who represents companies that base their pricing on credit scoring.

There’s so much to be gained by understanding credit scoring and knowing how to improve your score.

All the best,

R.J. Weiss

Conclusion

21

about WeiSS inSuranCe agenCieS

What doeS an indePendent agent do?

At Weiss Insurance Agencies, we believe consumers should be educated on their purchasing decisions. You’re not buying insurance just because you need to. You’re buying it because you want to be protected in case anything bad happens.

When you fill out the form on our site for a free home, auto, life, or any other type of quote, here’s what you can expect:

1. We start with a thorough review of your current policy. While discussing your goals for the future. If you have any other lines of insurance such as jewelry, RV, boat, motorcycle, rental property, etc…please let us know. You’ll save a lot of money by insuring all your lines of coverage through one carrier.

2. We then fill in the information gap, by asking you a few questions. Going through a detailed

There are two types of insurance agents--independent and captive.

Captive agents work exclusively for one insurance company. A captive agent’s profile is to bring in business for their parent company as generally they cannot use any other insurance company.

Independent agents, like us at Weiss Insurance Agencies, represent multiple insurance companies and work in the best interests of our clients to find a policy that matches our clients’ needs.

What other benefits are there to having an independent agent?

When you do suffer a loss, you have an experienced team of insurance professionals, representing your best interests--not the insurance company’s.

quoting process gives us access to the information we need to properly insure you. Just as important, asking these questions allows us to discover the discounts you’re eligible for. This takes care of the second half of our goal—to insure you for the best possible price.

3. For 90% of our quotes, we use advanced software that lets us quote your insurance out to multiple carriers at one time. We then manually review your information and get final pricing from each carrier. Other times, due to premium size or loss history, we’re only able to get prices from a select few our carriers. It’s important you know all of the carriers we represent are A rated insurance carriers. More importantly, we have hand selected these carriers because they offer the best combination of price and coverage.

An independent agent is not just your outlet to insurance carriers but your personal insurance adviser. We work with you to determine the optimal combination of price, coverage, and service for your unique situation.

• You have a small team of experienced professionals who service your account. When you call in with a question, you’re working with a team who’s familiar with your needs.

• One-stop shopping--beyond personal home and auto insurance, Weiss Insurance offers business, life, and health insurance, as well as wealth management services.

To get started working with Weiss Insurance Agencies, click the following link, personal insurance, and select the type of insurance you’re interested in reviewing.

22

here’S What our ClientS Say: “After suffering a major casualty loss insured by a major insurance company with little compensation. A close friend recommended I check out Weiss Insurance Agencies. It was the best suggestion ever given me. The agent spent countless hours finding the best fit for my circumstances and in the end saved me more than a thousand dollars bundling all my personal insurance needs. Weiss has found a lifetime customer in me.” - Walter J.

“My experience with Weiss insurance has been nothing but great. Anything I have a question on, you guys are able to answer right away. I always give Weiss Insurance the first opportunity I have when it comes to my insurance needs and you guys always are competitive if not better than everyone else. Everyone is very helpful and accommodating there.” - Brent P.

“I cannot thank Weiss Insurance enough for the understanding, assistance and compassion everyone at the agency has shown me. Patricia W.

Disclaimer: This report was written by R.J. Weiss of Weiss Insurance Agencies. All information provided in this guide is for informational purposes only. Weiss Insurance Agencies makes no representations as to the accuracy, completeness, suitability or validity of any information in this guide and will not be liable for any errors or omissions in this information or any damages arising from its display or use.

If you have any questions about your situation, seek a qualified credit counselor or CERTIFIED FINANCIAL PLANNER®.