Wave - beamexchange.org · SMK Sekolah Menengah Kejuruan (Vocational High School) UBSP Unit Bersama...

52

Second Wave Report on Maize Sub- Sector in Sumenep 2 nd Wave Longitudinal Livelihood Study (LLS) JANUARY 2017 PRISMA Author: Abdur Rofi Technical Support: Richard Rose

Transcript of Wave - beamexchange.org · SMK Sekolah Menengah Kejuruan (Vocational High School) UBSP Unit Bersama...

Second Wave Report on Maize Sub-

Sector in Sumenep

2nd Wave Longitudinal Livelihood Study

(LLS)

JANUARY 2017

PRISMA

Author: Abdur Rofi

Technical Support: Richard Rose

LLS | January 2017

ii

LLS | January 2017

iii

LONGITUDINAL LIVELIHOOD STUDY

Second Wave Report on Maize Sub-Sector in Sumenep

PRISMA

Author: Abdur Rofi

Technical Support: Richard Rose

January 2017

Table of Contents

List of Abbreviation and Explanation of Expressions .......................................................... 2

1 Introduction ............................................................................................................... 6

2 Sampling .................................................................................................................... 6

2.1 Sampling Quantitative .................................................................................................... 6

2.2 Sampling Qualitative ...................................................................................................... 7

2.3 Poverty Rate of Households using PPI ............................................................................. 7

3 Five Livelihood Assets ................................................................................................. 7

3.1 Human Assets ................................................................................................................ 8

3.2 Physical Assets ............................................................................................................. 10

3.3 Natural Assets .............................................................................................................. 22

3.4 Social Assets................................................................................................................. 23

3.5 Financial Assets ............................................................................................................ 23

4 Income Generation ................................................................................................... 25

4.1 Agricultural Activity with Focus on Maize ...................................................................... 26

4.2 Livestock Activities ....................................................................................................... 31

5 Expenditures and Financial Expenditure ................................................................... 31

5.1 Education Expenditure ................................................................................................. 32

5.2 Social Expenditure ........................................................................................................ 36

5.3 Livestock Expenditure ................................................................................................... 41

5.4 Agricultural Assets and Inputs....................................................................................... 42

5.5 Repaying Debt .............................................................................................................. 42

5.6 Food Expenditures........................................................................................................ 43

6 Income Use of Maize ................................................................................................ 47

7 Seasonality and Vulnerability ................................................................................... 49

LLS | January 2017

Livelihood Study Second wave Report 2

Maize Sub-Sector in Sumenep

PRISMA January 2017

List of Abbreviation and Explanation of Expressions

Abbreviations

DVD Digital Versatile Disc

SD Sekolah Dasar (Primary School)

SMP Sekolah Menengah Pertama (Junior High School)

SMA Sekolah Menengah Atas, (Senior High School),

SMK Sekolah Menengah Kejuruan (Vocational High School)

UBSP Unit Bersama Simpan Pinjam (Small Savings and Borrowings Group)

UPK Unit Pengelola Kagiatan ((Government) Activity Managing Units)

VCR Videocassette Recorder

VCP Videocassette Player

VCD Video Compact Disc

Expressions

Adat Local traditions

Arisan Group-based rotating savings and lending fund

Desa Village

Koperasi, Cooperative

Pasar Local traditional market

Warung Local shop/ restaurant

List of Figures

Figure 1: Highest Education of Persons 25+ years (2015) ......................................................................... 10

Figure 2: Highest Education of Persons 25+ years (2016) ......................................................................... 10

Figure 3: Assets - House and Land (2015) ................................................................................................ 11

Figure 4: Assets - House and Land (2016) ................................................................................................ 11

Figure 5: Assets – Housing 2015) ............................................................................................................. 12

Figure 6: Assets – Housing 2016) ............................................................................................................. 12

Figure 7: Assets – Transport (2015) ......................................................................................................... 13

Figure 8: Assets – Transport (2016) ......................................................................................................... 13

Figure 9: Assets – Communication (2015) ................................................................................................ 14

Figure 10: Assets – Communication (2016) .............................................................................................. 14

Figure 11: Assets – Kitchen and Storage (2015) ....................................................................................... 15

LLS | January 2017

Livelihood Study Second wave Report 3

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 12: Assets – Kitchen and Storage (2016) ....................................................................................... 15

Figure 13: Assets – Other Household Items (2015) .................................................................................. 16

Figure 14: Assets – Other Household Items (2016) .................................................................................. 16

Figure 15: Assets - Agricultural Items (2015) ............................................................................................ 17

Figure 16: Assets - Agricultural Items (2016) ............................................................................................ 17

Figure 17: Large Livestock by Quintile (2015) .......................................................................................... 18

Figure 18: Large Livestock by Quintile (2016) .......................................................................................... 18

Figure 19: Other Livestock by Quintile (2015) .......................................................................................... 19

Figure 20: Other Livestock by Quintile (2016) .......................................................................................... 19

Figure 21: Amount of Large Livestock by Quintile (2015) ......................................................................... 20

Figure 22: Amount of Large Livestock by Quintile (2016) ......................................................................... 20

Figure 23: Amount of Other Livestock by Quintile (2015) ........................................................................ 21

Figure 24: Amount of Other Livestock by Quintile (2016) ........................................................................ 21

Figure 25: Land Holdings by Quintile (2015) ............................................................................................ 22

Figure 26: Land Holdings by Quintile (2016) ............................................................................................ 22

Figure 27: Own Production and Received Food/ Total Food Consumption (2015) .................................... 23

Figure 28: Own Production and Received Food/ Total Food Consumption (2016) .................................... 23

Figure 29: Saving and Borrowing by Quintile (2015) ................................................................................ 24

Figure 30: Saving and Borrowing by Quintile (2016) ................................................................................ 24

Figure 31: Saving and Borrowing by Quintile - total amount in IDR (2015) ............................................... 25

Figure 32: Saving and Borrowing by Quintile - total amount in IDR (2016) ............................................... 25

Figure 33: Agriculture and Livestock Income Generation (2015) .............................................................. 26

Figure 34: Agriculture and Livestock Income Generation (2016) .............................................................. 26

Figure 35: Frequency of Crops mentioned as one of the three most important (except maize) in terms of

income (2015) ................................................................................................................................. 27

Figure 36: Frequency of Crops mentioned as one of the three most important (except maize) in terms of

income (2015) ................................................................................................................................. 27

Figure 37: Crops for Self-consumption (reported no selling) 2015) .......................................................... 28

Figure 38: Crops for Self-consumption (reported no selling) 2016 ........................................................... 28

Figure 39: Crops which are mainly sold (reported as 50%+ selling) (2015) ............................................... 29

Figure 40: Crops which are mainly sold (reported as 50%+ selling) (2016) ............................................... 29

Figure 41: Maize selling by calendar month (2015) .................................................................................. 30

Figure 42: Maize selling by calendar month (2016) .................................................................................. 30

Figure 43: Month when people sell Livestock (2015) ............................................................................... 31

LLS | January 2017

Livelihood Study Second wave Report 4

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 24: Month when people sell Livestock (2016 ................................................................................ 31

Figure 45: Significant household expenditure (2015) ............................................................................... 32

Figure 46: Significant household expenditure (2016) ............................................................................... 32

Figure 47: Expenditure on Education (total) (2015) ................................................................................. 33

Figure 48: Expenditure on Education (total) (2016) ................................................................................. 33

Figure 49: Expenditure on education per child (2015).............................................................................. 34

Figure 50: Expenditure on education per child (2016).............................................................................. 34

Figure 51: financing of Education (2015) ................................................................................................. 35

Figure 52: financing of Education (2016) ................................................................................................. 35

Figure 53: Timing of significant expenditures: Education (2015) .............................................................. 36

Figure 54: Timing of significant expenditures: Education (2016) .............................................................. 36

Figure 55: Social Expenditure (2015) ....................................................................................................... 37

Figure 56: Social Expenditure (2016) ....................................................................................................... 37

Figure 57: Financing Marriage (2015) ...................................................................................................... 38

Figure 58: Financing Marriage (2016) ...................................................................................................... 38

Figure 59: Financing other Adat (2015) .................................................................................................... 39

Figure 60: Financing other Adat (2016) .................................................................................................... 39

Figure 61: Timing of significant expenditure – Marriage (2015) ............................................................... 40

Figure 62: Timing of significant expenditure – Marriage (2015) ............................................................... 40

Figure 63: Timing of significant expenditure (other Adat/ religious/ village celebration) (2015) ............... 41

Figure 64: Timing of significant expenditure (other Adat/ religious/ village celebration) (2016) ............... 41

Figure 65: Timing of Significant Expenditure - buying animal stock (2015) ............................................... 42

Figure 66: Timing of significant expenditure - repaying debt (2015) ......................................................... 42

Figure 67: Timing of significant expenditure - repaying debt (2016) ......................................................... 43

Figure 68: Food Expenditure by Quintile (2015) ....................................................................................... 43

Figure 69: Food Expenditure by Quintile (2016) ....................................................................................... 44

Figure 70: Total Food and non-food Expenditure by Quintile (2015) ........................................................ 44

Figure 71: Total Food and non-food Expenditure by Quintile (2016) ........................................................ 45

Figure 72: Type of Food Expenditure by Quintile (total spend) (2015) ...................................................... 45

Figure 73: Type of Food Expenditure by Quintile (total spend) (2016) ...................................................... 46

Figure 74: Share of Expenditure on Rice and Other staples by Quintile (2015) ......................................... 46

Figure 75: Share of Expenditure on Rice and Other staples by Quintile (2016) ......................................... 47

Figure 76: Most important use of income derived from maize (2015) ...................................................... 47

LLS | January 2017

Livelihood Study Second wave Report 5

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 77: Most important use of income derived from maize (2016) ...................................................... 48

Figure 78: Second most important use of income derived from maize (2015) .......................................... 48

Figure 79: Second most important use of income derived from maize (2016) .......................................... 48

List of Tables

Table 1: Sampling ...................................................................................................................................... 6

Table 2: Sampling of Quantitative Data Collection ..................................................................................... 7

Table 4: Poverty Rate of Households using PPI .......................................................................................... 7

Table 5: Per Capita Expenditure per Quintile in Rp. per Month (2015) ....................................................... 7

Table 5: Per Capita Expenditure per Quintile in Rp. per Month (2016) ....................................................... 7

Table 6: Household Characteristics ............................................................................................................ 8

Table 7: Female-headed households ......................................................................................................... 8

Table 8: Education of People 15 Years or Older ......................................................................................... 8

Table 9: Education of children 7-15 years .................................................................................................. 8

Table 10: School Enrolment by Age Group (2015) ...................................................................................... 9

Table 11: School Enrolment by Age Group (2016) ...................................................................................... 9

Table 12: Income Earned with Maize ....................................................................................................... 30

Table 13: Female Decision Making Power and Engagement in Maize Activities ........................................ 31

Table 14: Control and Decision Power of Earnings from Maize ................................................................ 49

Table 15: Food Security ........................................................................................................................... 49

LLS | January 2017

Livelihood Study Second wave Report 6

Maize Sub-Sector in Sumenep

PRISMA January 2017

1 Introduction

This second wave report is part of a study, which aims to gain a deeper understanding on how targeted

households use additional income generated through the PRISMA intervention. Sumenep is one of many

districts in East Java that has been targeted by PRISMA and where the project tries to alleviate poverty.

PRISMA supports maize farmers by promoting hybrid seed for dry land farming. The goal is to increase the

productivity of maize and therefore increase the income of maize farmers. The goal of this longitudinal

livelihood study (LLS) is to gain a deeper understanding on how the maize farmers use their additional

income anticipated to be generated through the intervention. This will run until the end of the program.

The households interviewed during this year will be tracked during the following years to see how their

livelihood situation has changed and how the changes relate to the intervention. Such a study is

important for PRISMA because it helps assess whether targets selected for raising rural income are

reasonable and how it can affect rural livelihoods.

The goal of this second wave report is to give an overview over the current livelihood situation to see in

later stages how this situation changed. The report provides an overview with special focus on income

generation and use of income. The second wave study uses a mixed method approach including the

collection of both qualitative and quantitative data. 175 households were interviewed for quantitative

data collection with a questionnaire and nine respondents were interviewed for qualitative data collection

through semi-structured interviews. Together this data provides a picture of the current livelihood

situation of the farmers. The same households will be interviewed in coming years as part of the next

waves of the LLS.

The second wave report initially provides the frame sampling for the study (Section 2); the five assets of

the sustainable livelihood framework are described in Section 3; with a discussion of income generation

discussed in Section 4. Section 5 describes expenditure; while Section 6 focuses on use of income

generated by maize earnings. Section 7 discusses seasonality and vulnerability of the households.

2 Sampling

2.1 Sampling Quantitative

Table 1: Sampling

2015 2016

Babbalan 20 17

Batu Dinding 25 22

Bilapora Timur 20 19

Kasengan 34 28

Kebundadap Timur 15 14

Kopedi 20 18

Manding Timur 19 19

Moncek Tengah 20 20

Sarokah 4 2

Totosan 20 16

Total 197 175

LLS | January 2017

Livelihood Study Second wave Report 7

Maize Sub-Sector in Sumenep

PRISMA January 2017

2.2 Sampling Qualitative

Table 2: Sampling of Quantitative Data Collection

Name of Desa Number of

respondents 2015

Number of

respondents 2016

Bilapora Timur 1 1

Babbalan 2 2

Moncek Tengah 2 2

Kopedi 2 2

Kebondadap Timur 2 1

2.3 Poverty Rate of Households using PPI

The Poverty Rate of Households using PPI is given below:

Table 3: Poverty Rate of Households using PPI

2015 2016

Nr. Obs mean Nr.

Obs

mean

100% National Poverty Rate 155.00 9.48 175 8,36

150% National Poverty Rate 155.00 42.30 175 39,35

$2.5 2005 PPP Poverty Rate 155.00 74.27 175 66,35

3 Five Livelihood Assets

The discussion of five livelihood assets of the sustainable livelihood framework gives a good overview over

the resources that are available to a household (DFID, 1999). The assets are classified in five categories

which are human assets, physical assets, natural assets, social assets, and financial assets. As discussed in

the baseline report, the sample and understand information about different quintile levels. Table 5 is

reproduced from the baseline report, table 6 provides the updated figures for 2016.

Table 4: Per Capita Expenditure per Quintile in Rp. per Month (2015)

Nr. Obs Mean Sd Min Max

Q1 37.00 328,011.74 49,446.83 193,222.22 396,533.31

Q2 36.00 464,549.17 37,792.70 400,305.53 537,916.63

Q3 37.00 634,447.01 54,087.71 548,416.63 706,966.63

Q4 36.00 789,443.31 52,424.34 711,805.56 913,750.00

Q5 36.00 1,557,029.56 740,344.44 930,955.56 4,432,291.50

Table 5: Per Capita Expenditure per Quintile in Rp. per Month (2016)

Nr. Obs Mean Sd Min Max

Q1 35.00 235.448,2 51.643,0 95.597,2 294.900,0 Q2 35.00 333.799,3 21.409,2 298.750,0 364.783,3 Q3 35.00 405.845,0 25.018,6 364.812,5 444.633,3 Q4 35.00 521.771,3 51.262,4 455.606,7 622.444,4 Q5 35.00 759.369,1 109.137,5 634.086,7 992.861,1

LLS | January 2017

Livelihood Study Second wave Report 8

Maize Sub-Sector in Sumenep

PRISMA January 2017

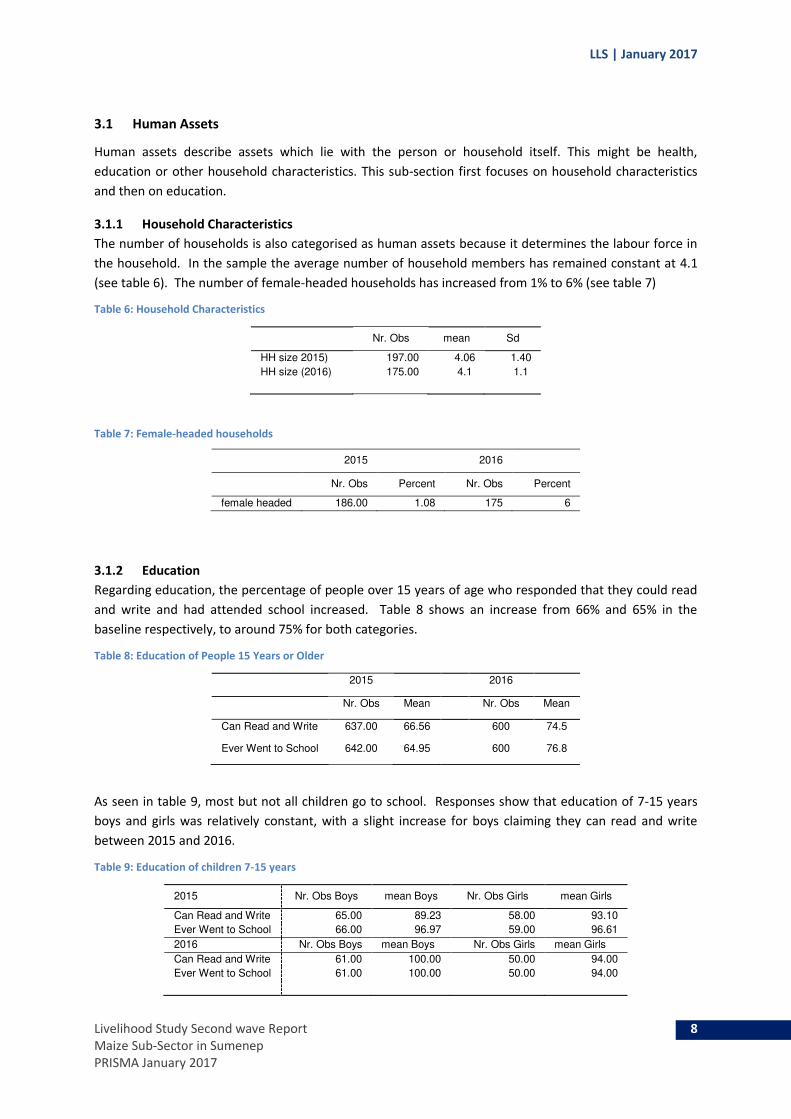

3.1 Human Assets

Human assets describe assets which lie with the person or household itself. This might be health,

education or other household characteristics. This sub-section first focuses on household characteristics

and then on education.

3.1.1 Household Characteristics

The number of households is also categorised as human assets because it determines the labour force in

the household. In the sample the average number of household members has remained constant at 4.1

(see table 6). The number of female-headed households has increased from 1% to 6% (see table 7)

Table 6: Household Characteristics

Nr. Obs mean Sd

HH size 2015) 197.00 4.06 1.40

HH size (2016) 175.00 4.1 1.1

Table 7: Female-headed households

2015 2016

Nr. Obs Percent Nr. Obs Percent

female headed 186.00 1.08 175 6

3.1.2 Education

Regarding education, the percentage of people over 15 years of age who responded that they could read

and write and had attended school increased. Table 8 shows an increase from 66% and 65% in the

baseline respectively, to around 75% for both categories.

Table 8: Education of People 15 Years or Older

2015 2016

Nr. Obs Mean Nr. Obs Mean

Can Read and Write 637.00 66.56 600 74.5

Ever Went to School 642.00 64.95 600 76.8

As seen in table 9, most but not all children go to school. Responses show that education of 7-15 years

boys and girls was relatively constant, with a slight increase for boys claiming they can read and write

between 2015 and 2016.

Table 9: Education of children 7-15 years

2015 Nr. Obs Boys mean Boys Nr. Obs Girls mean Girls

Can Read and Write 65.00 89.23 58.00 93.10

Ever Went to School 66.00 96.97 59.00 96.61

2016 Nr. Obs Boys mean Boys Nr. Obs Girls mean Girls

Can Read and Write 61.00 100.00 50.00 94.00

Ever Went to School 61.00 100.00 50.00 94.00

LLS | January 2017

Livelihood Study Second wave Report 9

Maize Sub-Sector in Sumenep

PRISMA January 2017

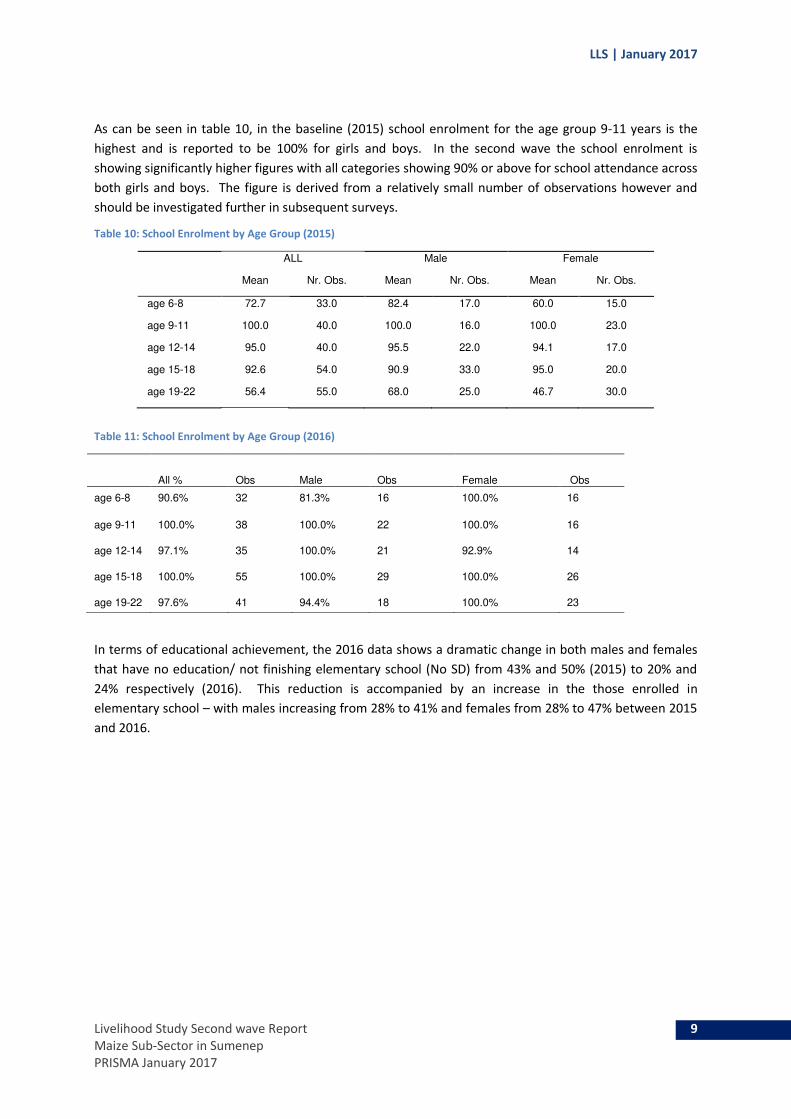

As can be seen in table 10, in the baseline (2015) school enrolment for the age group 9-11 years is the

highest and is reported to be 100% for girls and boys. In the second wave the school enrolment is

showing significantly higher figures with all categories showing 90% or above for school attendance across

both girls and boys. The figure is derived from a relatively small number of observations however and

should be investigated further in subsequent surveys.

Table 10: School Enrolment by Age Group (2015)

ALL Male Female

Mean Nr. Obs. Mean Nr. Obs. Mean Nr. Obs.

age 6-8 72.7 33.0 82.4 17.0 60.0 15.0

age 9-11 100.0 40.0 100.0 16.0 100.0 23.0

age 12-14 95.0 40.0 95.5 22.0 94.1 17.0

age 15-18 92.6 54.0 90.9 33.0 95.0 20.0

age 19-22 56.4 55.0 68.0 25.0 46.7 30.0

Table 11: School Enrolment by Age Group (2016)

In terms of educational achievement, the 2016 data shows a dramatic change in both males and females

that have no education/ not finishing elementary school (No SD) from 43% and 50% (2015) to 20% and

24% respectively (2016). This reduction is accompanied by an increase in the those enrolled in

elementary school – with males increasing from 28% to 41% and females from 28% to 47% between 2015

and 2016.

All % Obs Male Obs Female Obs

age 6-8 90.6% 32 81.3% 16 100.0% 16

age 9-11 100.0% 38 100.0% 22 100.0% 16

age 12-14 97.1% 35 100.0% 21 92.9% 14

age 15-18 100.0% 55 100.0% 29 100.0% 26

age 19-22 97.6% 41 94.4% 18 100.0% 23

LLS | January 2017

Livelihood Study Second wave Report 10

Maize Sub-Sector in Sumenep

PRISMA January 2017

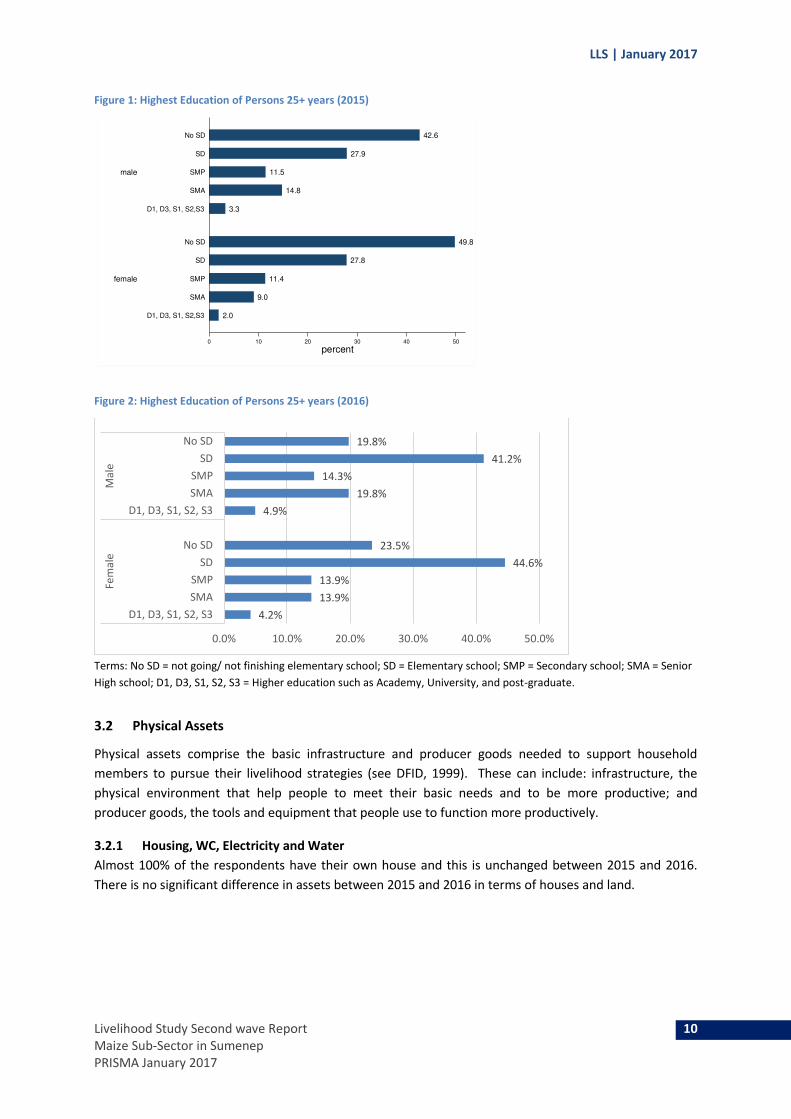

Figure 1: Highest Education of Persons 25+ years (2015)

Figure 2: Highest Education of Persons 25+ years (2016)

Terms: No SD = not going/ not finishing elementary school; SD = Elementary school; SMP = Secondary school; SMA = Senior

High school; D1, D3, S1, S2, S3 = Higher education such as Academy, University, and post-graduate.

3.2 Physical Assets

Physical assets comprise the basic infrastructure and producer goods needed to support household

members to pursue their livelihood strategies (see DFID, 1999). These can include: infrastructure, the

physical environment that help people to meet their basic needs and to be more productive; and

producer goods, the tools and equipment that people use to function more productively.

3.2.1 Housing, WC, Electricity and Water

Almost 100% of the respondents have their own house and this is unchanged between 2015 and 2016.

There is no significant difference in assets between 2015 and 2016 in terms of houses and land.

2.0

9.0

11.4

27.8

49.8

3.3

14.8

11.5

27.9

42.6

0 10 20 30 40 50

percent

female

male

D1, D3, S1, S2,S3

SMA

SMP

SD

No SD

D1, D3, S1, S2,S3

SMA

SMP

SD

No SD

4.2%

13.9%

13.9%

44.6%

23.5%

4.9%

19.8%

14.3%

41.2%

19.8%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0%

D1, D3, S1, S2, S3

SMA

SMP

SD

No SD

D1, D3, S1, S2, S3

SMA

SMP

SD

No SD

Fe

ma

leM

ale

LLS | January 2017

Livelihood Study Second wave Report 11

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 3: Assets - House and Land (2015)

Figure 4: Assets - House and Land (2016)

Not all households have electricity. In 2015 (figure 5) over 80% of the households have electricity across

all expenditure quintiles, this is unchanged in 2016. Significantly the data shows that while in 2015 more

than 50% of homes had a W/C (with the percentage rising to over 90% in the highest quintile) the 2016

data shows that ownership is steady across all quintiles at around 40-45%. Well/ Tube-well ownership

appears to have increased significantly across all quintiles and dramatically amongst lower quintiles (from

17% to 51% in Q1). These figures should be investigated further before any conclusions can be drawn in

terms of attribution to the intervention.

100.0

91.9

52.8

100.0

94.4

61.8

97.394.6

54.1

97.2100.0

55.6

97.2100.0

57.1

0

20

40

60

80

100

Q1 Q2 Q3 Q4 Q5

Assets: House and Land

House Agricultural Land

Other House/Building

100.0% 100.0%94.3%

91.4%

100.0%

91.4% 97.1% 94.3%

94.3%

91.4%

57.1%60.0%

51.4%

68.6%

57.1%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

Q1 Q2 Q3 Q4 Q5

House Agricultural Land Other House/Building

LLS | January 2017

Livelihood Study Second wave Report 12

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 5: Assets – Housing 2015)

Figure 6: Assets – Housing 2016)

3.2.2 Transport

The most common means of transportation in Sumenep remains the motor cycle (figures 7 and 8). More

households possess motor cycles in higher expenditure quintiles. Bicycle ownership appears to have

reduced though ownership remains proportionately less than motor-cycles and more than cars/ trucks.

86.5

43.2

62.9

16.7

86.1

57.1

68.6

17.6

89.2

54.3

88.9

8.1

94.4

77.8

88.9

41.7

82.9

69.4

90.9

52.8

0

20

40

60

80

100

Q1 Q2 Q3 Q4 Q5

Electricity Floor not Eearth or Bamboo

WC Well/Tubewell

91.4% 91.4%94.3%

97.1% 97.1%

85.7%94.3%

97.1%94.3%

100.0%

45.7%40.0%

42.9% 42.9%40.0%

51.4%48.6%

54.3%51.4%

71.4%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

Q1 Q2 Q3 Q4 Q5

Electricity Floor not eart/bamboo WC Well/Tubewell

LLS | January 2017

Livelihood Study Second wave Report 13

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 7: Assets – Transport (2015)

Figure 8: Assets – Transport (2016)

3.2.3 Communication Assets

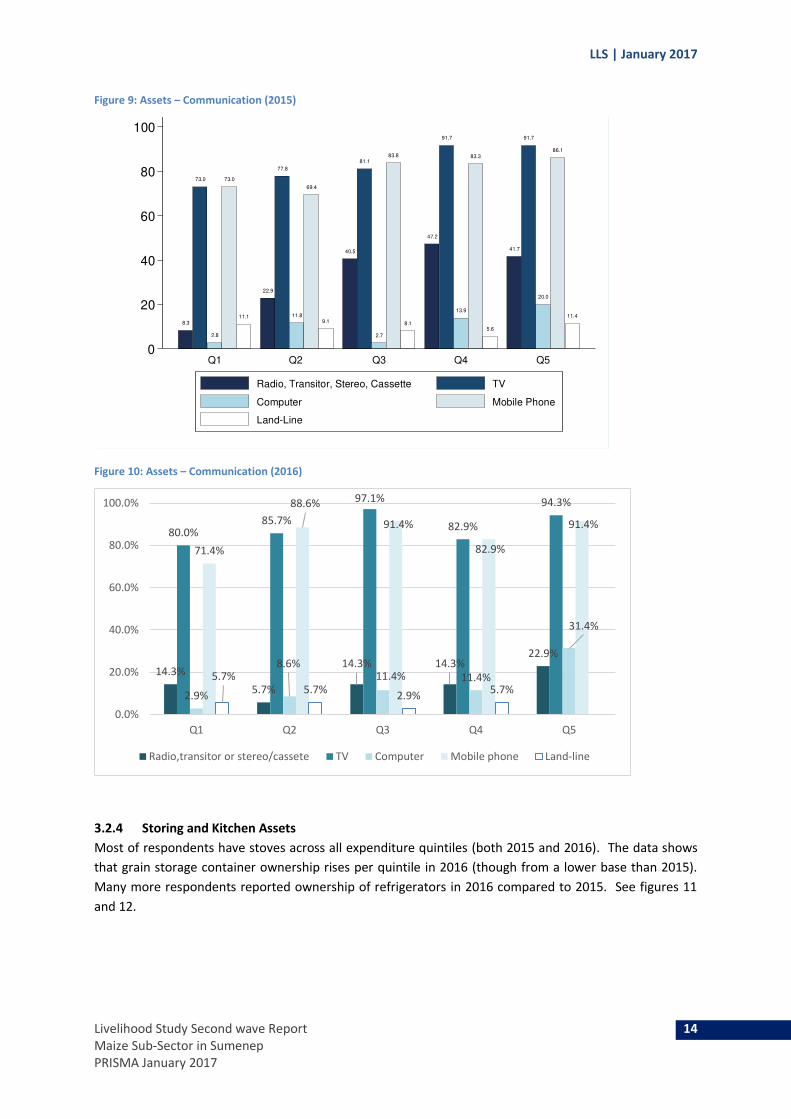

As seen figures 9 and 10, television and mobile phone are the most common communication assets.

There is no significant change across 2015 and 2016, except that the number of respondents claiming

ownership of stereos/ radios has reduced.

0.0

67.6

86.5

0.0

63.9

75.0

2.7

67.6

81.1

0.0

63.9

94.4

0.0

69.4

100.0

0

20

40

60

80

100

Q1 Q2 Q3 Q4 Q5

Assets: Transport

Car/Truck Bicycle

Motorbike

0.0%

5.7%8.6%

0.0%

8.6%

40.0%

48.6%

37.1%40.0%

54.3%

74.3%

88.6% 88.6% 88.6%

97.1%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

Q1 Q2 Q3 Q4 Q5

Car/Truck Bicycle Motorbike

LLS | January 2017

Livelihood Study Second wave Report 14

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 9: Assets – Communication (2015)

Figure 10: Assets – Communication (2016)

3.2.4 Storing and Kitchen Assets

Most of respondents have stoves across all expenditure quintiles (both 2015 and 2016). The data shows

that grain storage container ownership rises per quintile in 2016 (though from a lower base than 2015).

Many more respondents reported ownership of refrigerators in 2016 compared to 2015. See figures 11

and 12.

8.3

73.0

2.8

73.0

11.1

22.9

77.8

11.8

69.4

9.1

40.5

81.1

2.7

83.8

8.1

47.2

91.7

13.9

83.3

5.6

41.7

91.7

20.0

86.1

11.4

0

20

40

60

80

100

Q1 Q2 Q3 Q4 Q5

Radio, Transitor, Stereo, Cassette TV

Computer Mobile Phone

Land-Line

14.3%

5.7%

14.3% 14.3%22.9%

80.0%85.7%

97.1%

82.9%

94.3%

2.9%

8.6%11.4% 11.4%

31.4%

71.4%

88.6%

91.4%

82.9%

91.4%

5.7%5.7%

2.9%5.7%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

Q1 Q2 Q3 Q4 Q5

Radio,transitor or stereo/cassete TV Computer Mobile phone Land-line

LLS | January 2017

Livelihood Study Second wave Report 15

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 11: Assets – Kitchen and Storage (2015)

Figure 12: Assets – Kitchen and Storage (2016)

3.2.5 Other Household Assets

Washing and sewing machines remain uncommon amongst households in the 2016 sample (figure 14).

Most respondents have jewellery in their household. VCR/CP/VCD/DVD ownership increases by wealth

quintile.

83.3

30.6

2.7

75.0

44.1

2.9

64.9

40.5

5.6

72.2

44.4

16.7

80.077.8

19.4

0

20

40

60

80

Q1 Q2 Q3 Q4 Q5

Assets: Kitchen and Storing

Stove Grain Storage Container

Fridge/Freezer

80.0%

94.3%

88.6% 88.6%91.4%

14.3%

28.6%

31.4%

40.0%

51.4%

22.9%

40.0%

45.7%

37.1%

51.4%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

Q1 Q2 Q3 Q4 Q5

Stove Grain storage container Fridge/Freezer

LLS | January 2017

Livelihood Study Second wave Report 16

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 14: Assets – Other Household Items (2016)

3.2.6 Agricultural Assets

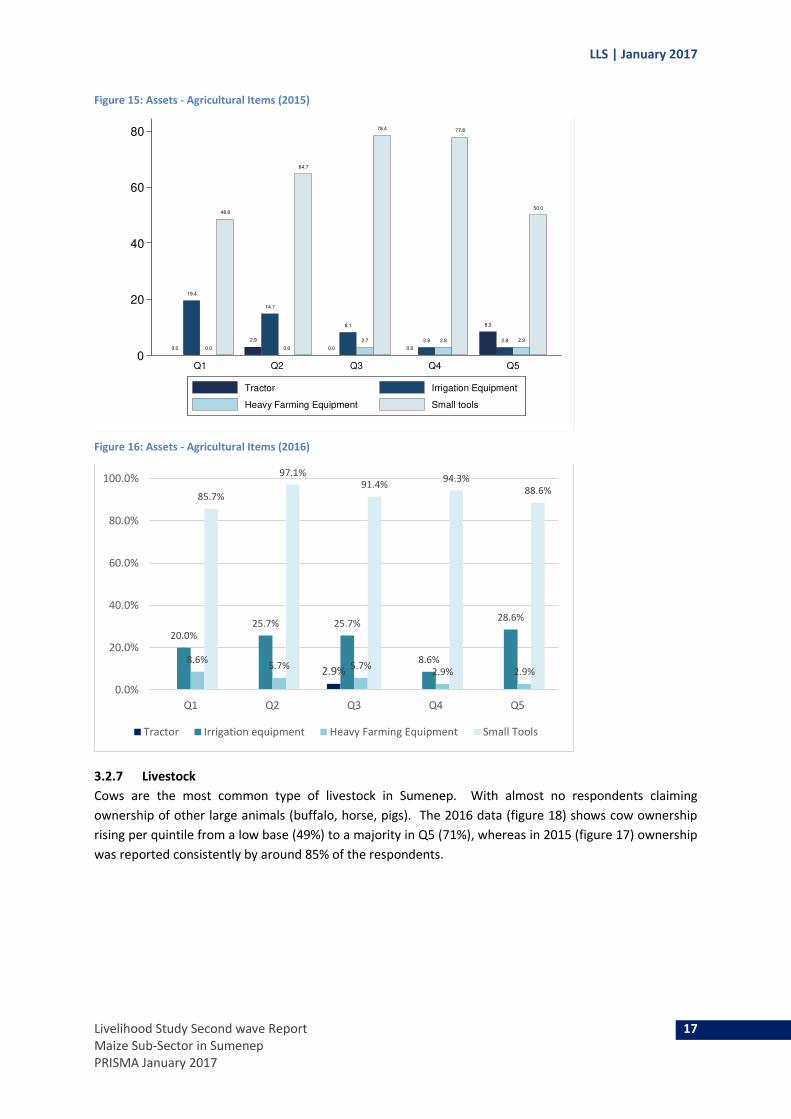

2016 (figure 15) is consistent with the 2015 data (figure 14) in that very few households reported

owning tractors or other heavy farming equipment. Irrigation systems are not common locally with

around 20% of respondents across all quintiles (2016). Ownership of small tools is common across all

expenditure quintiles.

5.7%

2.9%

5.7%

2.9%5.7%

2.9%

2.9%

60.0%

77.1% 77.1% 77.1%

82.9%

22.9%

31.4%

37.1%40.0%

48.6%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

Q1 Q2 Q3 Q4 Q5

Sewing Machine Washing Machine Jewerly VCR/VCP/VCD/DVD

Figure 13: Assets – Other Household Items (2015)

2.8

0.0

73.0

13.5

2.9 2.9

63.9

20.0

2.7

0.0

56.855.6

11.1

2.8

66.7

63.9

14.3

2.9

50.0 50.0

0

20

40

60

80

Q1 Q2 Q3 Q4 Q5

Sewing Machine Washing Machine

Jewelry VCR/VCP/VCD/DVD

LLS | January 2017

Livelihood Study Second wave Report 17

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 15: Assets - Agricultural Items (2015)

Figure 16: Assets - Agricultural Items (2016)

3.2.7 Livestock

Cows are the most common type of livestock in Sumenep. With almost no respondents claiming

ownership of other large animals (buffalo, horse, pigs). The 2016 data (figure 18) shows cow ownership

rising per quintile from a low base (49%) to a majority in Q5 (71%), whereas in 2015 (figure 17) ownership

was reported consistently by around 85% of the respondents.

0.0

19.4

0.0

48.6

2.9

14.7

0.0

64.7

0.0

8.1

2.7

78.4

0.0

2.8 2.8

77.8

8.3

2.8 2.9

50.0

0

20

40

60

80

Q1 Q2 Q3 Q4 Q5

Assets: Agricultural Items

Tractor Irrigation Equipment

Heavy Farming Equipment Small tools

2.9%

20.0%

25.7% 25.7%

8.6%

28.6%

8.6%5.7% 5.7%

2.9% 2.9%

85.7%

97.1%91.4%

94.3%

88.6%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

Q1 Q2 Q3 Q4 Q5

Tractor Irrigation equipment Heavy Farming Equipment Small Tools

LLS | January 2017

Livelihood Study Second wave Report 18

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 17: Large Livestock by Quintile (2015)

Figure 18: Large Livestock by Quintile (2016)

The 2016 data for smaller animals (figure 20) shows that chickens are the most common livestock after

cows in Sumenep. The 2015 data (figure 19) and the 2016 data show a broadly similar picture – with

chicken ownership with around 40-65% of households, and goat and sheep ownership at around 10 – 35%

depending upon expenditure quintile.

86.5

0.0 0.0 0.0

83.3

2.80.0 0.0

86.5

0.0 0.0 0.0

83.3

0.0 0.0 0.0

86.1

13.9

0.0 0.00

20

40

60

80

Q1 Q2 Q3 Q4 Q5

Livestock 1

Cow Buffalo

Horse Pig

48.6%51.4%

65.7%68.6%

71.4%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

Q1 Q2 Q3 Q4 Q5

Cow Bufallo Horse

LLS | January 2017

Livelihood Study Second wave Report 19

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 19: Other Livestock by Quintile (2015)

Figure 20: Other Livestock by Quintile (2016)

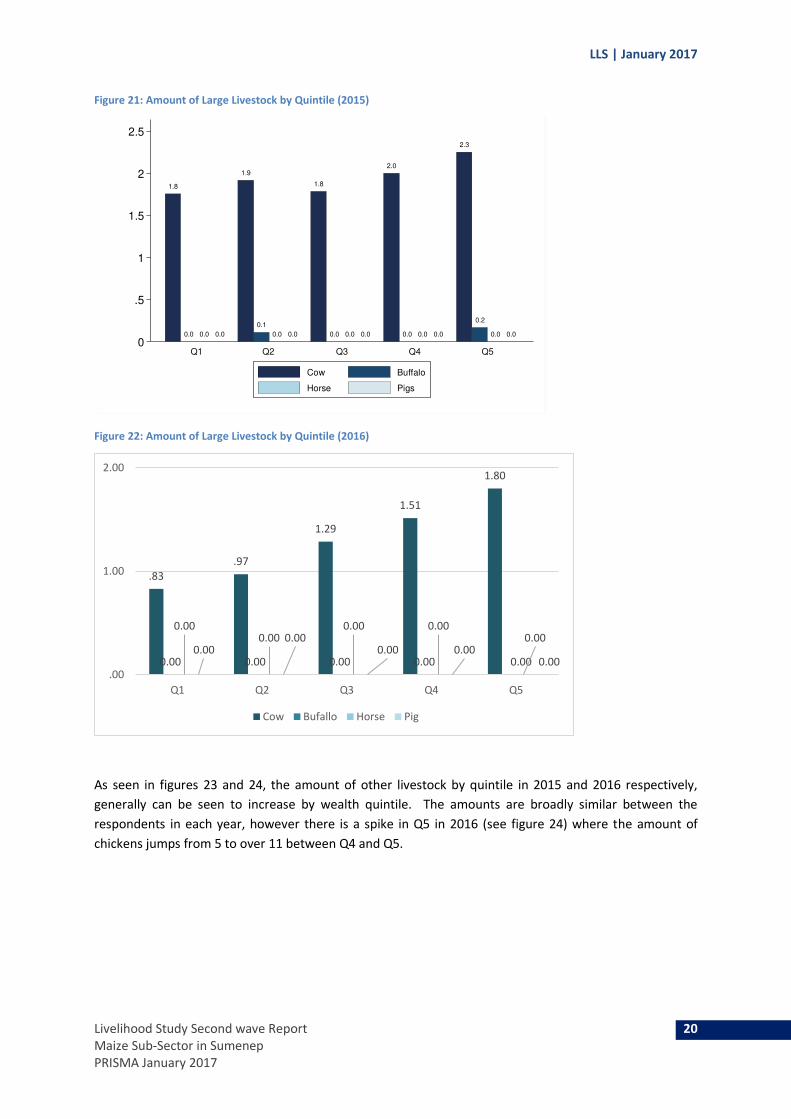

In terms of the amount of large livestock owned by respondents in Sumenep, the 2016 data (figure 22)

shows a sharp increase per wealth quintile, consistent with the findings in 2015 (figure 21). However, the

2016 data also shows a greater disparity between the lowest quintile (at 0.83 animals per household – in

the 2015 the figure was 1.8) and the highest (1.8 in 2016 – compared with 2.3 in 2015). It is notable that

the 2016 amount of livestock for the highest quintile is the same as the 2015 amount for the lowest.

24.3

43.2

0.0 0.0

33.3

47.2

2.80.0

21.6

62.2

0.0 0.0

33.3

66.7

5.6

0.0

30.6

66.7

5.6 5.6

0

20

40

60

80

Q1 Q2 Q3 Q4 Q5

Livestock 2

Goat and Sheeps Chicken

Duck Fish

11.4%

34.3%

20.0%22.9%

17.1%

42.9%

65.7%68.6%

62.9%60.0%

5.7%2.9% 2.9% 2.9% 2.9%2.9%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

Q1 Q2 Q3 Q4 Q5

Goat and sheep Chicken Duck Fish

LLS | January 2017

Livelihood Study Second wave Report 20

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 21: Amount of Large Livestock by Quintile (2015)

Figure 22: Amount of Large Livestock by Quintile (2016)

As seen in figures 23 and 24, the amount of other livestock by quintile in 2015 and 2016 respectively,

generally can be seen to increase by wealth quintile. The amounts are broadly similar between the

respondents in each year, however there is a spike in Q5 in 2016 (see figure 24) where the amount of

chickens jumps from 5 to over 11 between Q4 and Q5.

1.8

0.0 0.0 0.0

1.9

0.1

0.0 0.0

1.8

0.0 0.0 0.0

2.0

0.0 0.0 0.0

2.3

0.2

0.0 0.0

0

.5

1

1.5

2

2.5

Q1 Q2 Q3 Q4 Q5

Amount of Livestock 1

Cow Buffalo

Horse Pigs

.83

.97

1.29

1.51

1.80

0.00 0.00 0.00 0.00 0.00

0.000.00

0.00 0.000.00

0.000.00

0.00 0.000.00

.00

1.00

2.00

Q1 Q2 Q3 Q4 Q5

Cow Bufallo Horse Pig

LLS | January 2017

Livelihood Study Second wave Report 21

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 23: Amount of Other Livestock by Quintile (2015)

Figure 24: Amount of Other Livestock by Quintile (2016)

0.6

2.5

0.0

1.1

3.1

0.1

0.6

3.2

0.0

1.1

5.1

0.4

1.1

5.5

0.1

0

2

4

6

Q1 Q2 Q3 Q4 Q5

Goat and Sheeps Chicken

Duck

.74 .89 .74 .83 .71

2.29

4.513.89

5.29

11.49

1.20.31

.06 .34 .29

0.00

.31

0.00 0.000.00

.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

Q1 Q2 Q3 Q4 Q5

Goat and sheep Chicken Duck Fish

LLS | January 2017

Livelihood Study Second wave Report 22

Maize Sub-Sector in Sumenep

PRISMA January 2017

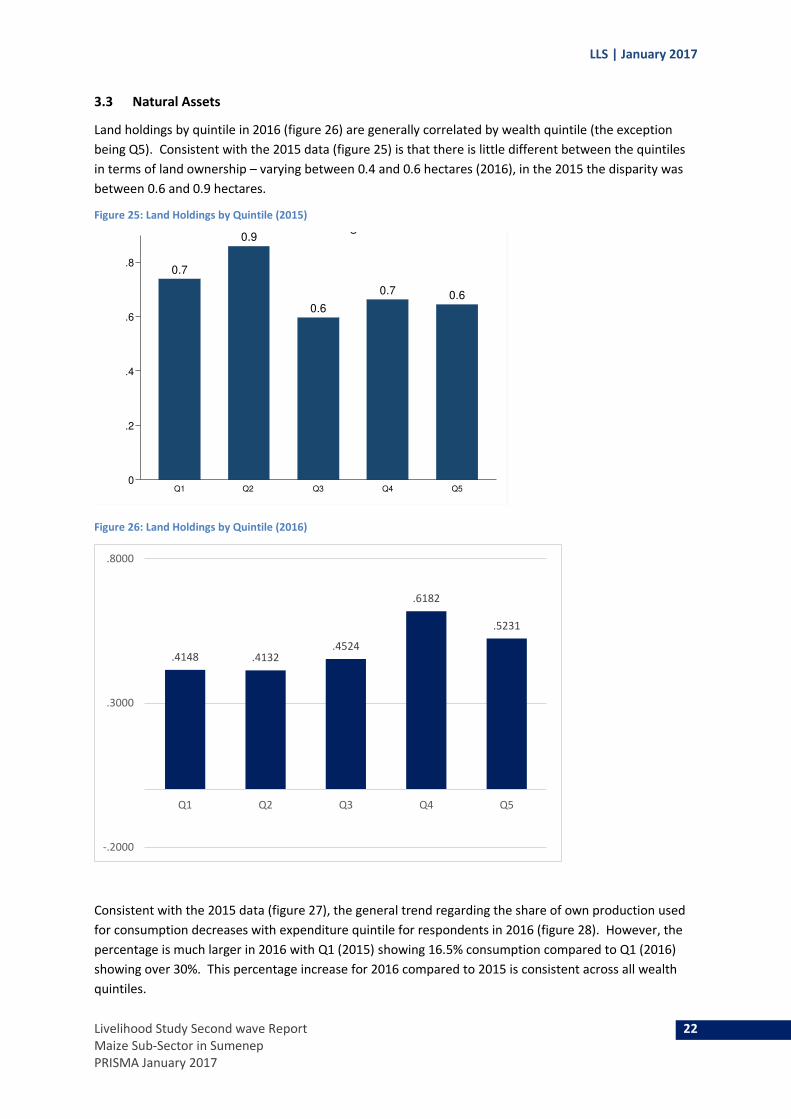

3.3 Natural Assets

Land holdings by quintile in 2016 (figure 26) are generally correlated by wealth quintile (the exception

being Q5). Consistent with the 2015 data (figure 25) is that there is little different between the quintiles

in terms of land ownership – varying between 0.4 and 0.6 hectares (2016), in the 2015 the disparity was

between 0.6 and 0.9 hectares.

Figure 25: Land Holdings by Quintile (2015)

Figure 26: Land Holdings by Quintile (2016)

Consistent with the 2015 data (figure 27), the general trend regarding the share of own production used

for consumption decreases with expenditure quintile for respondents in 2016 (figure 28). However, the

percentage is much larger in 2016 with Q1 (2015) showing 16.5% consumption compared to Q1 (2016)

showing over 30%. This percentage increase for 2016 compared to 2015 is consistent across all wealth

quintiles.

0.7

0.9

0.6

0.7 0.6

0

.2

.4

.6

.8

Q1 Q2 Q3 Q4 Q5

Land Holdings

.4148 .4132.4524

.6182

.5231

-.2000

.3000

.8000

Q1 Q2 Q3 Q4 Q5

LLS | January 2017

Livelihood Study Second wave Report 23

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 27: Own Production and Received Food/ Total Food Consumption (2015)

Figure 28: Own Production and Received Food/ Total Food Consumption (2016)

3.4 Social Assets

No new qualitative data collected for social assets.

3.5 Financial Assets

Financial assets show a stark difference between 2015 data (figure 29) and 2016 data (figure 30). In 2015

a far higher percentage of respondents claimed to have savings in lower quintiles while borrowing was

relatively stable across all wealth quintiles (with the exception of Q3). In 2016 the picture is reversed,

with over 50% of respondents in lower quintiles claiming to have borrowed, and savings being relative

stable across all quintiles. It is unclear at this stage why the data would show such a profound change and

it is recommended that this is investigated for the final analysis.

16.5

11.2

13.4

7.2

13.9

0

5

10

15

20

Q1 Q2 Q3 Q4 Q5

Total Food Conusmption

30.59

19.3021.17 20.94

17.90

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

Q1 Q2 Q3 Q4 Q5

LLS | January 2017

Livelihood Study Second wave Report 24

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 29: Saving and Borrowing by Quintile (2015)

Figure 30: Saving and Borrowing by Quintile (2016)

59.5

10.8

52.8

14.3

37.840.5 41.7

14.3

27.8

19.4

0

20

40

60

Q1 Q2 Q3 Q4 Q5

Saving and Borrowing

Saving Borrowing

17.1%14.3%

17.1%

8.6%

17.1%

51.4%

71.4%

60.0% 60.0%

42.9%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

Q1 Q2 Q3 Q4 Q5

Saving Borrowing

LLS | January 2017

Livelihood Study Second wave Report 25

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 31: Saving and Borrowing by Quintile - total amount in IDR (2015)

Figure 32: Saving and Borrowing by Quintile - total amount in IDR (2016)

Regarding the amounts saved or borrowed per quintile, the 2015 and 2016 data show significant

deviation. As with the percentage of savings vs borrowings (figures 29 and 30), the data shows a reverse

picture of the amounts on borrowing and savings in 2016 compared to 2015. Also the absolute values

have changed substantially, with the highest reported borrowing amounts in Q5 at 2.6M IDR (2015)

where in 2016 it is over 5.3M IDR. The 2016 data shows no correlation between borrowing amount and

quintile, where savings appears to reduce by wealth quintile.

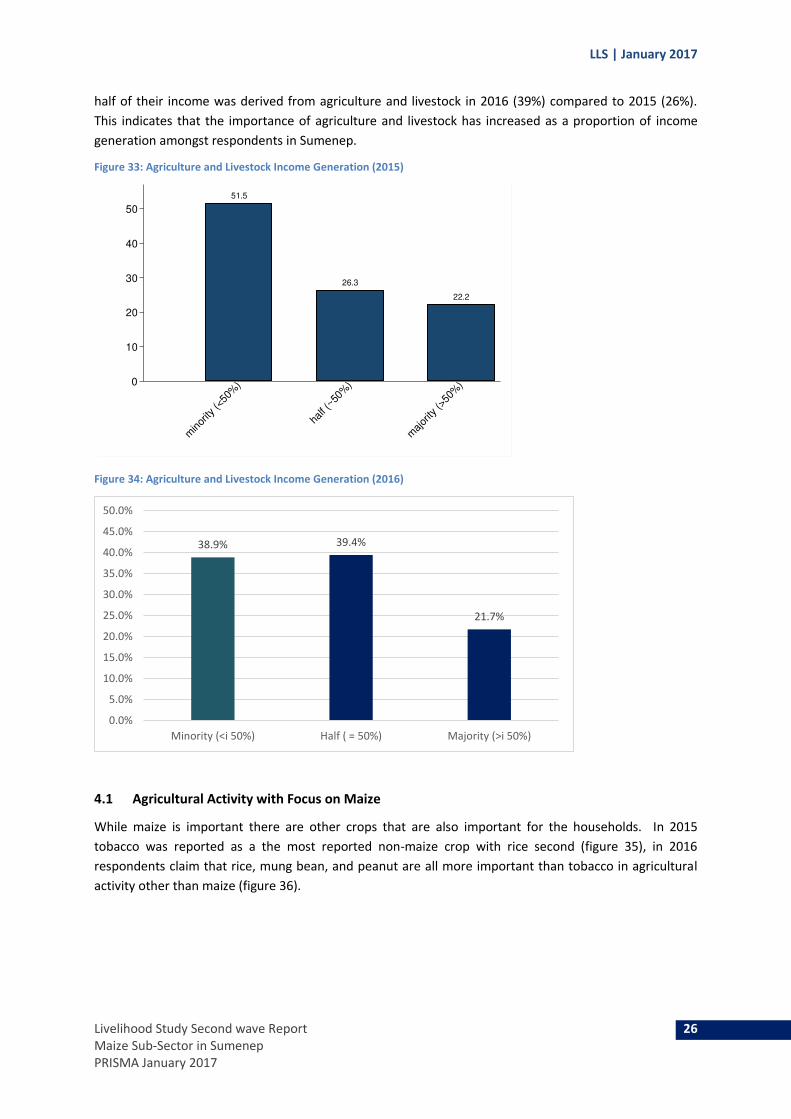

4 Income Generation

Regarding the income generation strategies of the households, as can be seen in figures 33 and 34, a

similar percentage of respondents confirmed that a majority of their income is derived from agriculture

and livestock (just over 20%) in both 2015 and 2016. A higher proportion of respondents claimed that

1.5

0.6

2.4

0.7

3.0

1.5

3.1

0.8

2.8

2.6

0

1

2

3

Q1 Q2 Q3 Q4 Q5

Saving and Borrowing

Saving Borrowing

2,950,000

2,295,157

1,275,000

775,000

1,941,683

2,888,889

4,136,000

3,783,333

2,082,286

5,366,667

-

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

Q1 Q2 Q3 Q4 Q5

IDR

Savings Borrowing

LLS | January 2017

Livelihood Study Second wave Report 26

Maize Sub-Sector in Sumenep

PRISMA January 2017

half of their income was derived from agriculture and livestock in 2016 (39%) compared to 2015 (26%).

This indicates that the importance of agriculture and livestock has increased as a proportion of income

generation amongst respondents in Sumenep.

Figure 33: Agriculture and Livestock Income Generation (2015)

Figure 34: Agriculture and Livestock Income Generation (2016)

4.1 Agricultural Activity with Focus on Maize

While maize is important there are other crops that are also important for the households. In 2015

tobacco was reported as a the most reported non-maize crop with rice second (figure 35), in 2016

respondents claim that rice, mung bean, and peanut are all more important than tobacco in agricultural

activity other than maize (figure 36).

51.5

26.3

22.2

0

10

20

30

40

50

minor

ity (<

50%

)

half (~

50%

)

major

ity (>

50%

)

Agricultural and Livestock Income Geneartion

38.9% 39.4%

21.7%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

Minority (<i 50%) Half ( = 50%) Majority (>i 50%)

LLS | January 2017

Livelihood Study Second wave Report 27

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 35: Frequency of Crops mentioned as one of the three most important (except maize) in terms of income (2015)

Figure 36: Frequency of Crops mentioned as one of the three most important (except maize) in terms of income (2015)

Regarding self-consumption crops (where no-selling was reported), maize remains the most important

crop for self-consumption relative to the others, with rice second (figures 37 and 38). Mung bean and

peanut are also used as a source of consumption by a significant number of respondents.

118

9

1

8

55

1

5

12

28

36

1

12

2

0 50 100 150frequency

Tobacco

Cassava

Watermelon

Banana

Rice

Pineapple

Cucumber

Soybeans

Peanut

Mung Bean

Guava

Chili Pepper

Chili

cro

p

in Terms of Income

81

69

61

28

10

8

5

4

3

2

1

1

0 10 20 30 40 50 60 70 80 90

Rice

Peanut

Mung Bean

Tobacco

Cassava

Banana

Long Nourishing (String bean)

Coconut: Fruit

Chili Pepper

Cucumber Trees

Avocado

Shallots

Frequency

Cro

ps

LLS | January 2017

Livelihood Study Second wave Report 28

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 37: Crops for Self-consumption (reported no selling) 2015)

Figure 38: Crops for Self-consumption (reported no selling) 2016

The picture for crops that are primarily sold (more than 50%+ going to market), has changed dramatically

between 2015 and 2016 (see figures 39 and 40). Where in 2015 the most sold crops were maize and

tobacco, in 2016 is mung bean (21 respondents), tobacco (14), and peanut (12), with a very low number

of respondents (3) claiming to sell maize. This is derived from a fairly small sample size however.

2

1

15

1

64

1

0 20 40 60frequency

Cassava

Banana

Rice

Mung Bean

Maize

Chili Pepper

cro

p

Crops for Self-Consumption(Reported No Selling)

68

54

29

21

8

8

5

3

2

2

1

0 10 20 30 40 50 60 70 80

Maize

Rice

Peanut

Mung Bean

Cassava

Tobacco

Long Nourishing (String bean)

Chili Pepper

Banana

Cucumber Trees

Avocado

Frequency

Cro

ps

LLS | January 2017

Livelihood Study Second wave Report 29

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 39: Crops which are mainly sold (reported as 50%+ selling) (2015)

Figure 40: Crops which are mainly sold (reported as 50%+ selling) (2016)

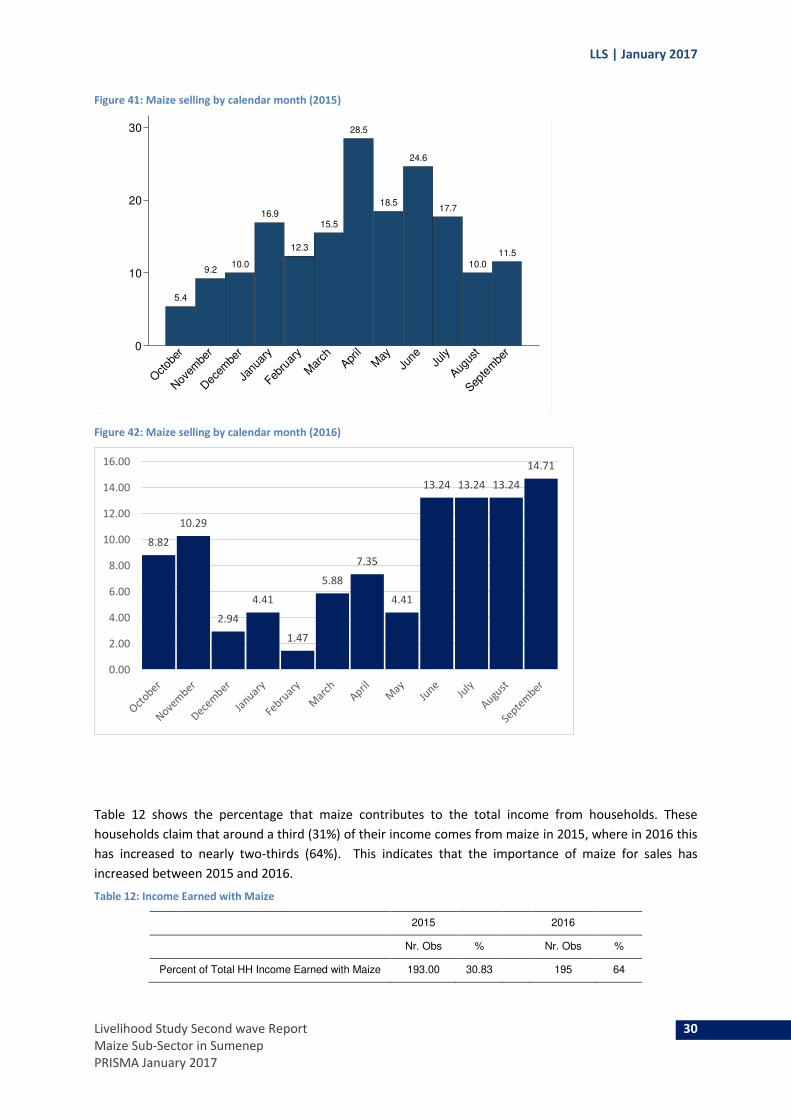

In 2015 households generated most income from maize between April and June (figure 41) whereas in

2016 (figure 42) there is a more even distribution with most sold between June and September.

115

7

1

7

30

1

5

12

27

35

1

120

8

2

0 50 100 150frequency

Tobacco

Cassava

Watermelon

Banana

Rice

Pineapple

Cucumber

Soybeans

Peanut

Mung Bean

Guava

Maize

Chili Pepper

Chili

cro

p

1

3

21

12

6

14

6

0 5 10 15 20 25

Coconut: Fruit

Maize

Mung Bean

Peanut

Rize

Tobacco

Others

LLS | January 2017

Livelihood Study Second wave Report 30

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 41: Maize selling by calendar month (2015)

Figure 42: Maize selling by calendar month (2016)

Table 12 shows the percentage that maize contributes to the total income from households. These

households claim that around a third (31%) of their income comes from maize in 2015, where in 2016 this

has increased to nearly two-thirds (64%). This indicates that the importance of maize for sales has

increased between 2015 and 2016.

Table 12: Income Earned with Maize

2015 2016

Nr. Obs % Nr. Obs %

Percent of Total HH Income Earned with Maize 193.00 30.83 195 64

5.4

9.210.0

16.9

12.3

15.5

28.5

18.5

24.6

17.7

10.0

11.5

0

10

20

30

Octob

er

Nov

embe

r

Dec

embe

r

Janu

ary

Febru

ary

Mar

chApr

ilM

ayJu

ne July

Augus

t

Septe

mbe

r

Month When People Sell Maize

8.82

10.29

2.94

4.41

1.47

5.88

7.35

4.41

13.24 13.24 13.24

14.71

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

LLS | January 2017

Livelihood Study Second wave Report 31

Maize Sub-Sector in Sumenep

PRISMA January 2017

Table 13: Female Decision Making Power and Engagement in Maize Activities

2015 2016

Nr. Obs mean Nr. Obs mean

Most important decision maker in HH is female: Selling

Maize

129.00 27.13 112 34,8

Second important decision maker in HH is female: Selling

Maize

128.00 75.78 112 56,2

Table 13 shows the responses regarding female decision-making power in selling maize. This shows a

small increase in the respondents’ reporting that the most important decision-maker is female from 27%

(2015) to 35% (2016). Correspondingly there is a reduction in the second most important from 76%

female (2015) to 56% (2016). This may be related to the number of female-headed households in the

locality.

4.2 Livestock Activities

Livestock rearing is also part of household income. As discussed the livestock can be seen as a form of

investment. They are sold throughout the year as can be seen in figure 24.

Figure 43: Month when people sell Livestock (2015)

Figure 44: Month when people sell Livestock (2016

5 Expenditures and Financial Expenditure

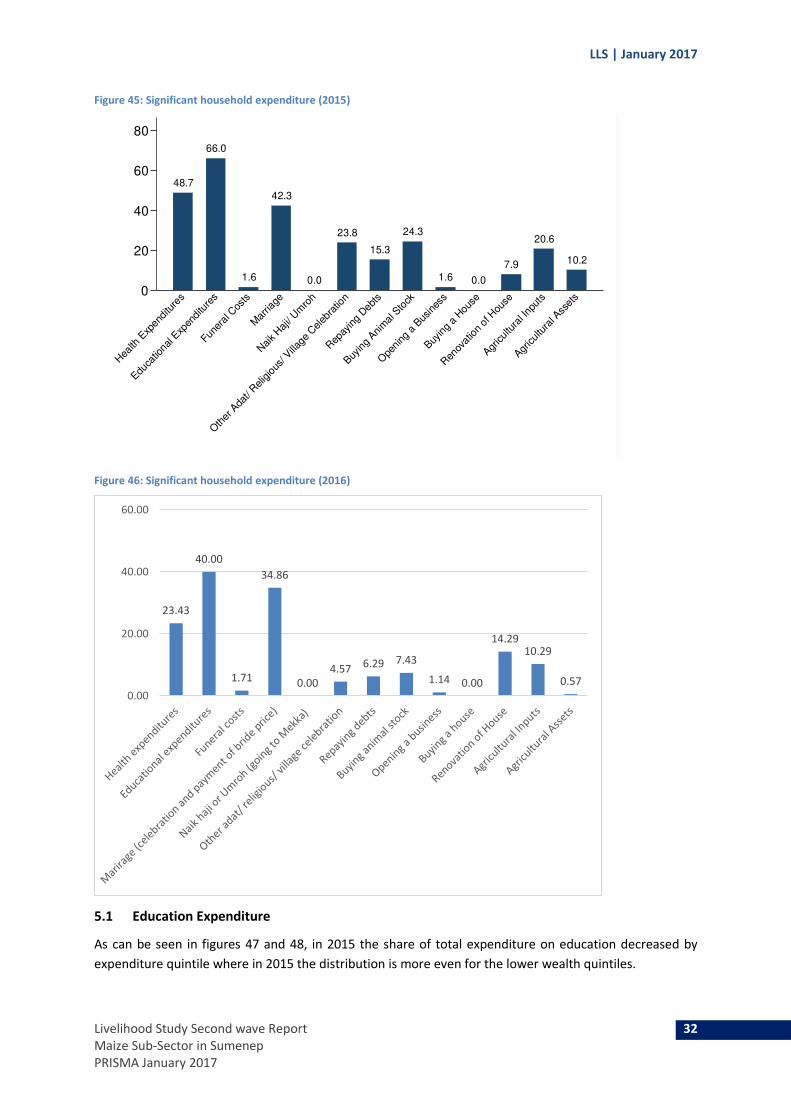

As can be seen in figure 45, in 2015 education expenditure was mentioned by 66% of the households to

be a significant expenditure in the last 12 months. Also health, marriage and other adat celebrations

were mentioned as most significant expenditure. For 24% of the households buying animal stock is a

significant expenditure and 21% consider agricultural inputs are a significant expenditure. In 2016 (figure

46) there is a similar picture with education, health, and marriage seen as the most significant

expenditure.

10.710.1

18.519.6

19.017.9

27.4

14.9 15.5

17.9

23.2

9.5

0

10

20

30

Octob

er

Nov

embe

r

Dec

embe

r

Janu

ary

Febru

ary

Mar

chApr

ilM

ayJu

neJu

ly

Augus

t

Septe

mbe

r

Month When People Sell Livestock

LLS | January 2017

Livelihood Study Second wave Report 32

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 45: Significant household expenditure (2015)

Figure 46: Significant household expenditure (2016)

5.1 Education Expenditure

As can be seen in figures 47 and 48, in 2015 the share of total expenditure on education decreased by

expenditure quintile where in 2015 the distribution is more even for the lower wealth quintiles.

48.7

66.0

1.6

42.3

0.0

23.8

15.3

24.3

1.6 0.0

7.9

20.6

10.2

0

20

40

60

80

Hea

lth E

xpen

ditu

res

Educa

tiona

l Exp

endi

ture

s

Funer

al C

osts

Mar

riage

Nai

k Haj

i/ Um

roh

Oth

er A

dat/

Relig

ious

/ Villa

ge C

eleb

ratio

n

Rep

ayin

g Deb

ts

Buyin

g Ani

mal

Sto

ck

Ope

ning

a B

usin

ess

Buyin

g a

Hou

se

Ren

ovat

ion

of H

ouse

Agricul

tura

l Inp

uts

Agricul

tura

l Ass

ets

Significant Expendiutres

23.43

40.00

1.71

34.86

0.00

4.57 6.29 7.43

1.14 0.00

14.2910.29

0.57

0.00

20.00

40.00

60.00

LLS | January 2017

Livelihood Study Second wave Report 33

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 47: Expenditure on Education (total) (2015)

Figure 48: Expenditure on Education (total) (2016)

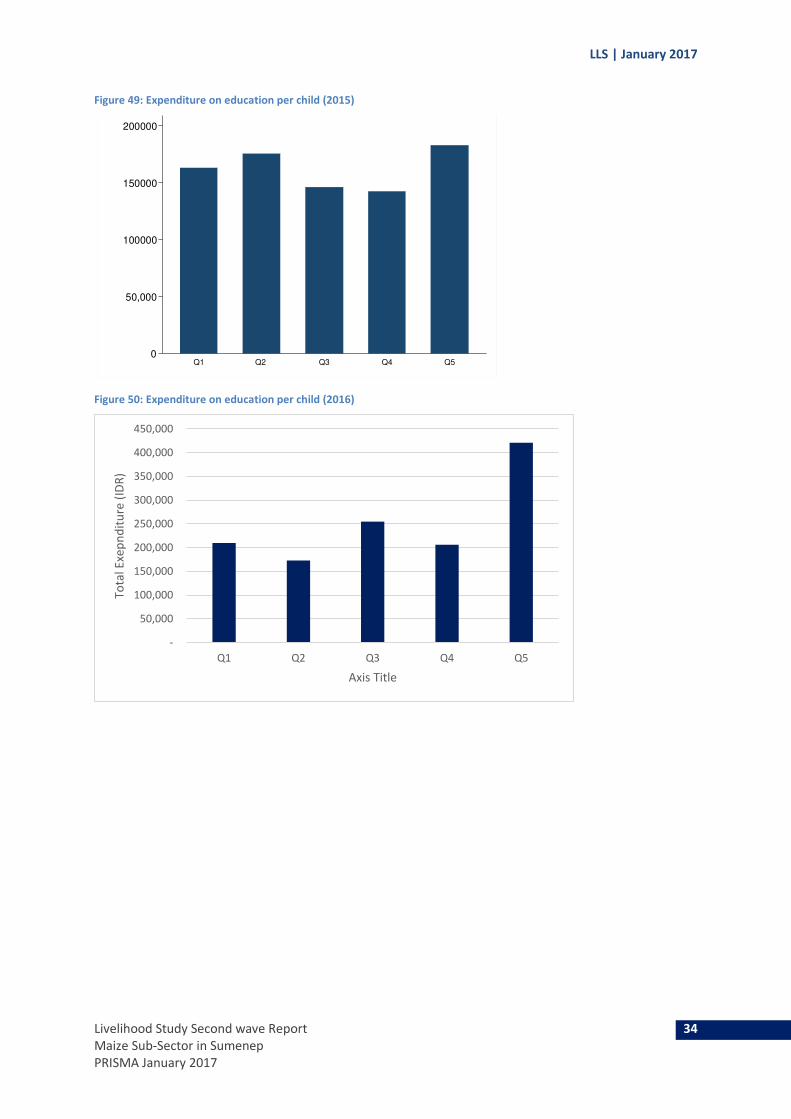

In terms of actual expenditure on education, the distribution across quintiles and the total amounts are

broadly similar between 2015 (figure 49) and 2016 (figure 50). The outlier is Q5 (2016) where there is a

large increase in reported expenditure (from under 200,000 IDR to over 400,000 IDR).

10.710.3

7.0

4.8

3.3

0

2

4

6

8

10

Q1 Q2 Q3 Q4 Q5

Education Expenditure

21.43 21.43

25.71

12.86

18.57

0.00

5.00

10.00

15.00

20.00

25.00

30.00

Q1 Q2 Q3 Q4 Q5

LLS | January 2017

Livelihood Study Second wave Report 34

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 49: Expenditure on education per child (2015)

Figure 50: Expenditure on education per child (2016)

0

50,000

100000

150000

200000

Q1 Q2 Q3 Q4 Q5

Education Expenditure per Child

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

Q1 Q2 Q3 Q4 Q5

To

tal

Exe

pn

dit

ure

(ID

R)

Axis Title

LLS | January 2017

Livelihood Study Second wave Report 35

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 51: financing of Education (2015)

Figure 52: financing of Education (2016)

As can be seen in figure 51, in 2015 most households financed education through selling crops and

livestock or by drawing upon their savings. In 2016 (figure 52) the majority of respondents claimed that

education was financed through savings with no respondents claiming they sell livestock for this reason.

This is a significant change given that this was the main mains of financing education in 2015.

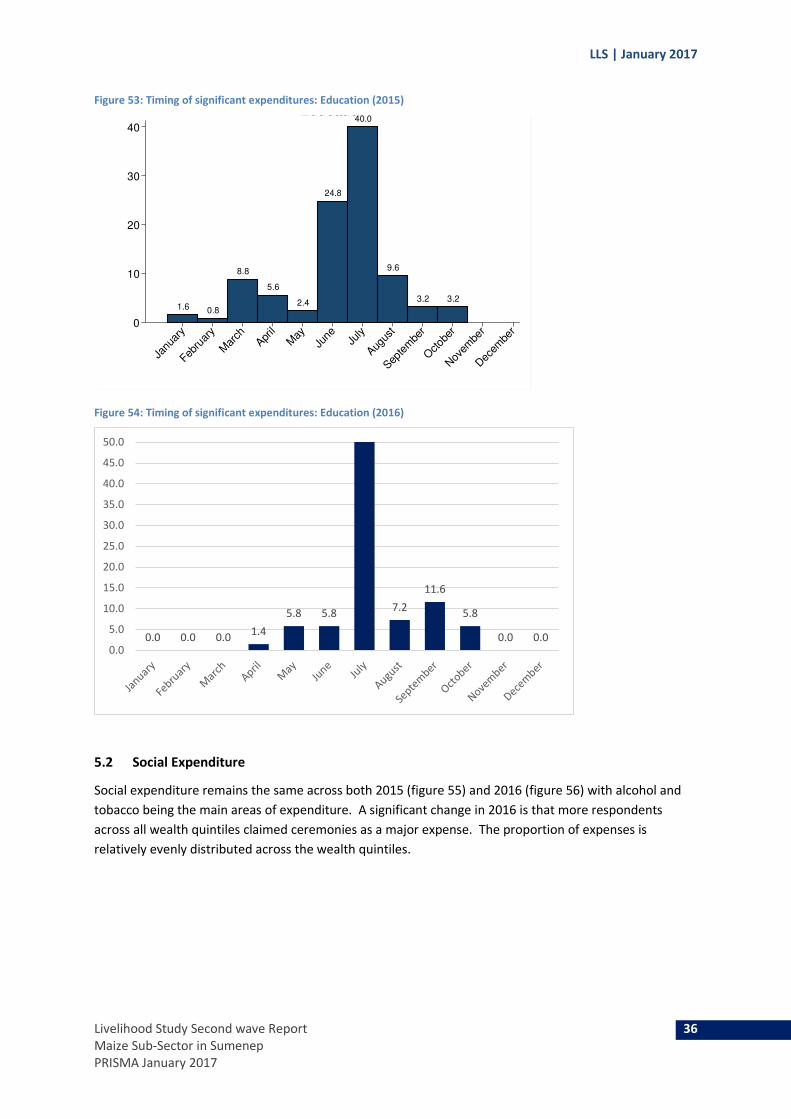

The timing of significant expenditure remains similar across both 2015 and 2016 (figures 53 and 54

respectively) with these expenditures being made in July.

33.1

0.8 0.8 0.8 0.8

40.3

19.4

4.0

0

10

20

30

40

Sav

ings

Hel

p fro

m R

elat

ives

/Frie

nds

Hel

p fro

m G

over

nmen

t

Hel

p fro

m N

GO/R

eligio

us In

stitu

tion

Cha

nge

Eatin

g Pat

tern

s

Em

ploy

ed H

ouse

hold

Mem

bers

Inte

nsified

Wor

k

Adu

lt Hou

seho

ld M

embe

rs S

tarte

d to

Wor

k

Hou

seho

ld M

embe

rs M

igra

te

Red

uce

Exp

endi

ture

s on

Hea

lth a

nd/ o

r Edu

catio

n

Cre

dit

Sell A

gricultu

ral A

sset

s

Sell D

urab

le A

sset

s

Sell L

and/

Build

ing

Sell C

rop

Sto

ck

Sell L

ives

tock

Inte

nsify

Fishi

ng

Sen

d Chi

ldre

n to

Live

Elsew

here

Spirit

ual E

fforts

Cur

rent

Inco

me

Did

Not

Do

Any

thin

g

Oth

er

Financing Education

78.6

0.0 0.0

14.3

0.0 0.0 0.05.7

0.0 1.4

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

LLS | January 2017

Livelihood Study Second wave Report 36

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 53: Timing of significant expenditures: Education (2015)

Figure 54: Timing of significant expenditures: Education (2016)

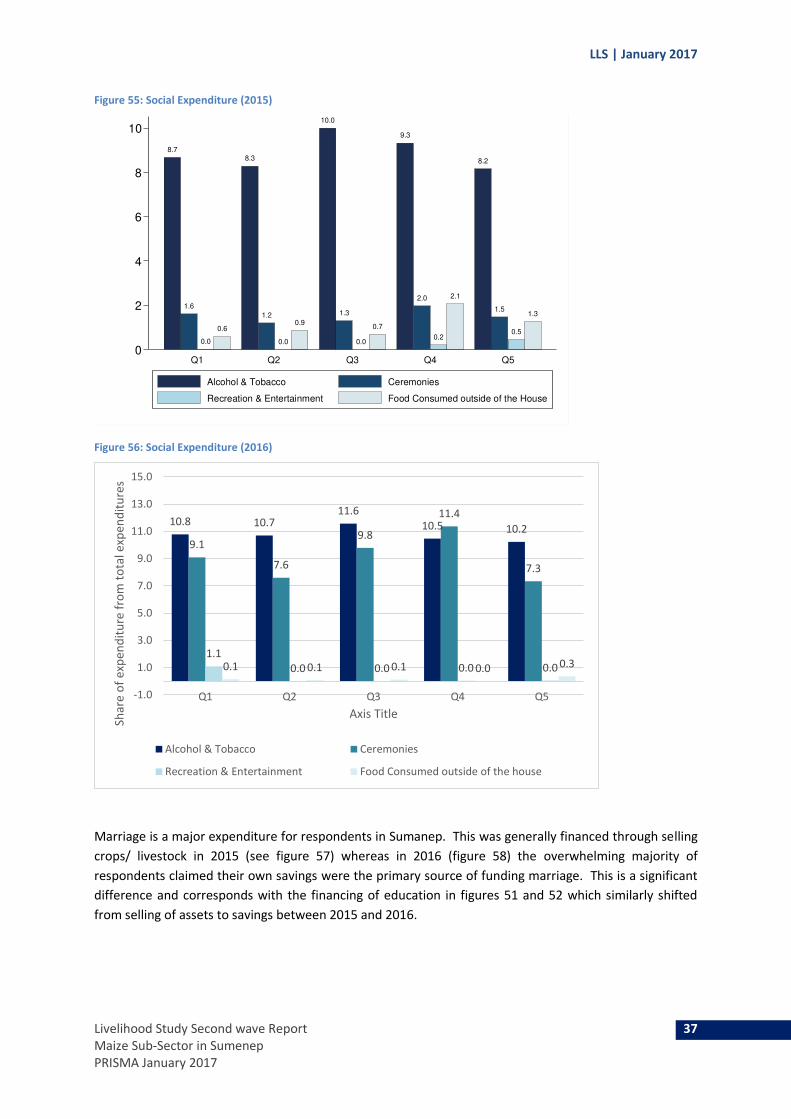

5.2 Social Expenditure

Social expenditure remains the same across both 2015 (figure 55) and 2016 (figure 56) with alcohol and

tobacco being the main areas of expenditure. A significant change in 2016 is that more respondents

across all wealth quintiles claimed ceremonies as a major expense. The proportion of expenses is

relatively evenly distributed across the wealth quintiles.

1.6 0.8

8.8

5.6

2.4

24.8

40.0

9.6

3.2 3.2

0

10

20

30

40

Janu

ary

Febru

ary

Mar

chApr

ilM

ayJu

ne July

Augus

t

Septe

mbe

r

Octob

er

Nov

embe

r

Dec

embe

r

Education

0.0 0.0 0.01.4

5.8 5.87.2

11.6

5.8

0.0 0.00.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

LLS | January 2017

Livelihood Study Second wave Report 37

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 55: Social Expenditure (2015)

Figure 56: Social Expenditure (2016)

Marriage is a major expenditure for respondents in Sumanep. This was generally financed through selling

crops/ livestock in 2015 (see figure 57) whereas in 2016 (figure 58) the overwhelming majority of

respondents claimed their own savings were the primary source of funding marriage. This is a significant

difference and corresponds with the financing of education in figures 51 and 52 which similarly shifted

from selling of assets to savings between 2015 and 2016.

8.7

1.6

0.0

0.6

8.3

1.2

0.0

0.9

10.0

1.3

0.0

0.7

9.3

2.0

0.2

2.1

8.2

1.5

0.5

1.3

0

2

4

6

8

10

Q1 Q2 Q3 Q4 Q5

Social Expenditures

Alcohol & Tobacco Ceremonies

Recreation & Entertainment Food Consumed outside of the House

10.8 10.711.6

10.5 10.2

9.1

7.6

9.8

11.4

7.3

1.1

0.0 0.0 0.0 0.00.1 0.1 0.1 0.0 0.3

-1.0

1.0

3.0

5.0

7.0

9.0

11.0

13.0

15.0

Q1 Q2 Q3 Q4 Q5

Sh

are

of

exp

en

dit

ure

fro

m t

ota

l e

xpe

nd

itu

res

Axis Title

Alcohol & Tobacco Ceremonies

Recreation & Entertainment Food Consumed outside of the house

LLS | January 2017

Livelihood Study Second wave Report 38

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 57: Financing Marriage (2015)

Figure 58: Financing Marriage (2016)

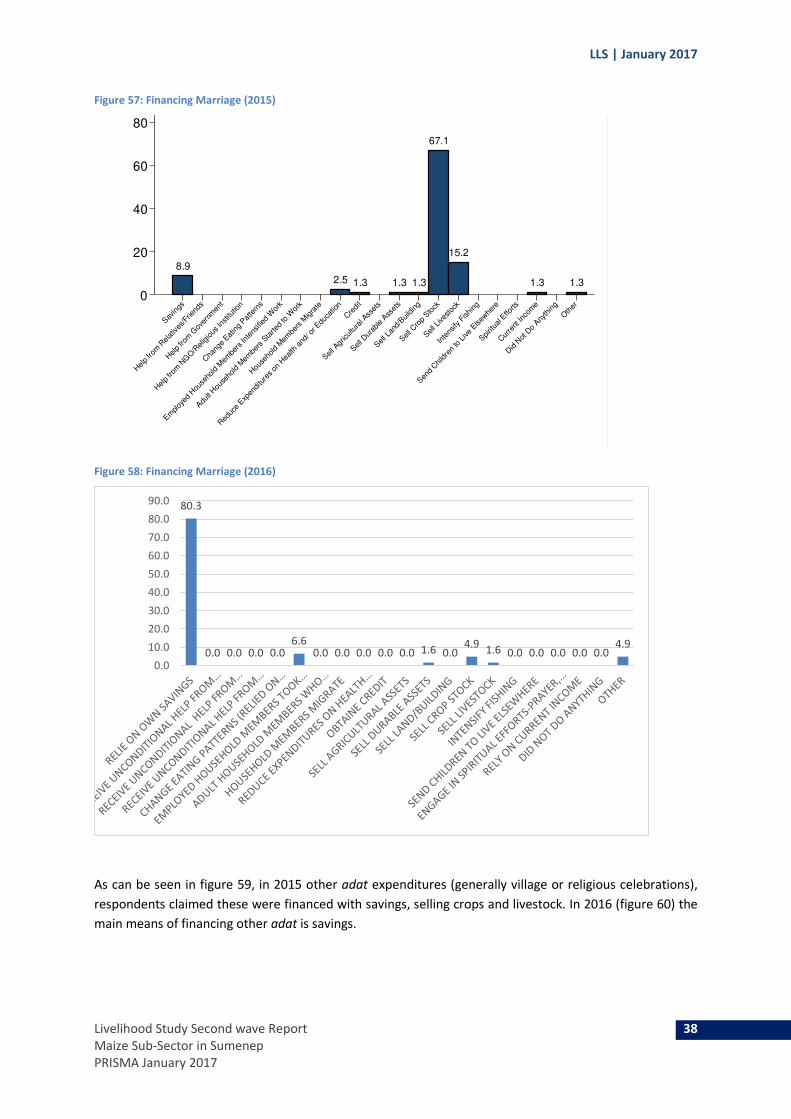

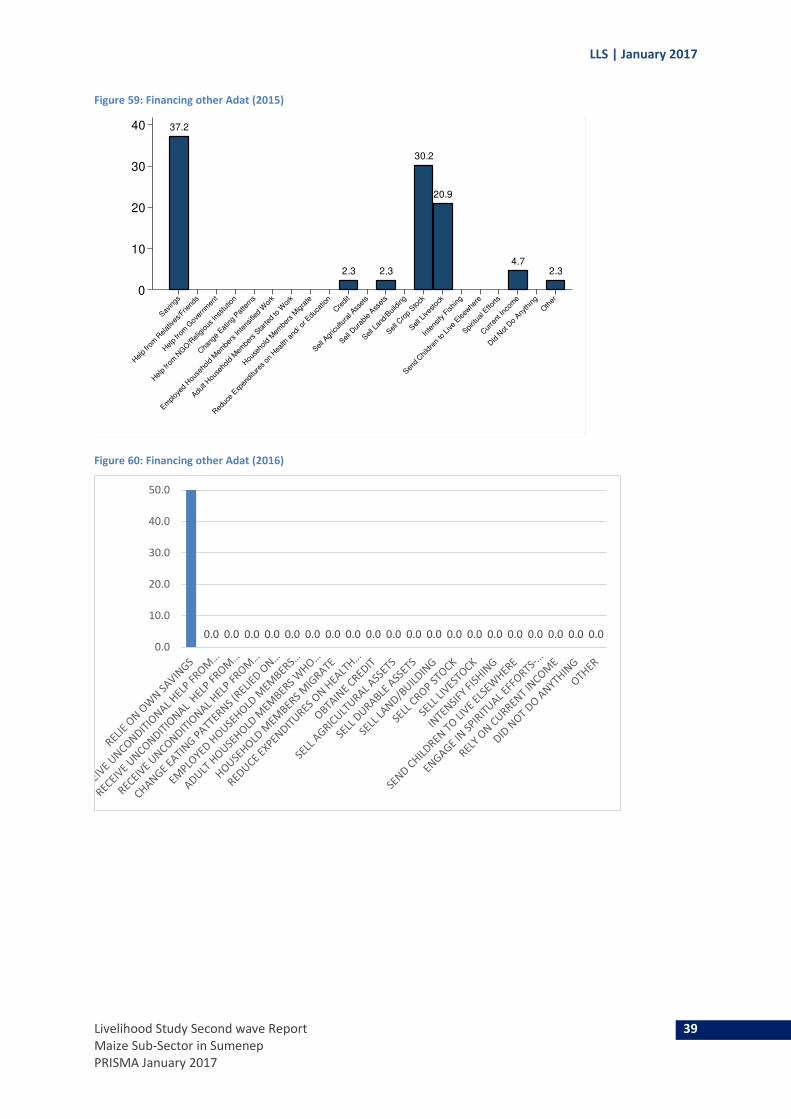

As can be seen in figure 59, in 2015 other adat expenditures (generally village or religious celebrations),

respondents claimed these were financed with savings, selling crops and livestock. In 2016 (figure 60) the

main means of financing other adat is savings.

8.9

2.5 1.3 1.3 1.3

67.1

15.2

1.3 1.3

0

20

40

60

80

Sav

ings

Hel

p fro

m R

elat

ives

/Frie

nds

Hel

p fro

m G

over

nmen

t

Hel

p fro

m N

GO/R

eligio

us In

stitu

tion

Cha

nge

Eatin

g Pat

tern

s

Em

ploy

ed H

ouse

hold

Mem

bers

Inte

nsified

Wor

k

Adu

lt Hou

seho

ld M

embe

rs S

tarte

d to

Wor

k

Hou

seho

ld M

embe

rs M

igra

te

Red

uce

Exp

endi

ture

s on

Hea

lth a

nd/ o

r Edu

catio

n

Cre

dit

Sell A

gricultu

ral A

sset

s

Sell D

urab

le A

sset

s

Sell L

and/

Build

ing

Sell C

rop

Sto

ck

Sell L

ives

tock

Inte

nsify

Fishi

ng

Sen

d Chi

ldre

n to

Live

Elsew

here

Spirit

ual E

fforts

Cur

rent

Inco

me

Did

Not

Do

Any

thin

g

Oth

er

80.3

0.0 0.0 0.0 0.06.6

0.0 0.0 0.0 0.0 0.0 1.6 0.04.9

1.6 0.0 0.0 0.0 0.0 0.04.9

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

LLS | January 2017

Livelihood Study Second wave Report 39

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 59: Financing other Adat (2015)

Figure 60: Financing other Adat (2016)

37.2

2.3 2.3

30.2

20.9

4.72.3

0

10

20

30

40

Sav

ings

Hel

p fro

m R

elat

ives

/Frie

nds

Hel

p fro

m G

over

nmen

t

Hel

p fro

m N

GO/R

eligio

us In

stitu

tion

Cha

nge

Eatin

g Pat

tern

s

Em

ploy

ed H

ouse

hold

Mem

bers

Inte

nsified

Wor

k

Adu

lt Hou

seho

ld M

embe

rs S

tarte

d to

Wor

k

Hou

seho

ld M

embe

rs M

igra

te

Red

uce

Exp

endi

ture

s on

Hea

lth a

nd/ o

r Edu

catio

n

Cre

dit

Sell A

gricultu

ral A

sset

s

Sell D

urab

le A

sset

s

Sell L

and/

Build

ing

Sell C

rop

Sto

ck

Sell L

ives

tock

Inte

nsify

Fishi

ng

Sen

d Chi

ldre

n to

Live

Elsew

here

Spirit

ual E

fforts

Cur

rent

Inco

me

Did

Not

Do

Any

thin

g

Oth

er

Financing other Adat

0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.00.0

10.0

20.0

30.0

40.0

50.0

LLS | January 2017

Livelihood Study Second wave Report 40

Maize Sub-Sector in Sumenep

PRISMA January 2017

The timing of marriage in Sumanep is generally in May-June and August-September – this is consistent

across 2015 (figure 61) and 2016 (figure 62). In the 2016 more respondents also claimed that marriage

expenditure is timed in February than respondents in 2015.

Figure 61: Timing of significant expenditure – Marriage (2015)

Figure 62: Timing of significant expenditure – Marriage (2015)

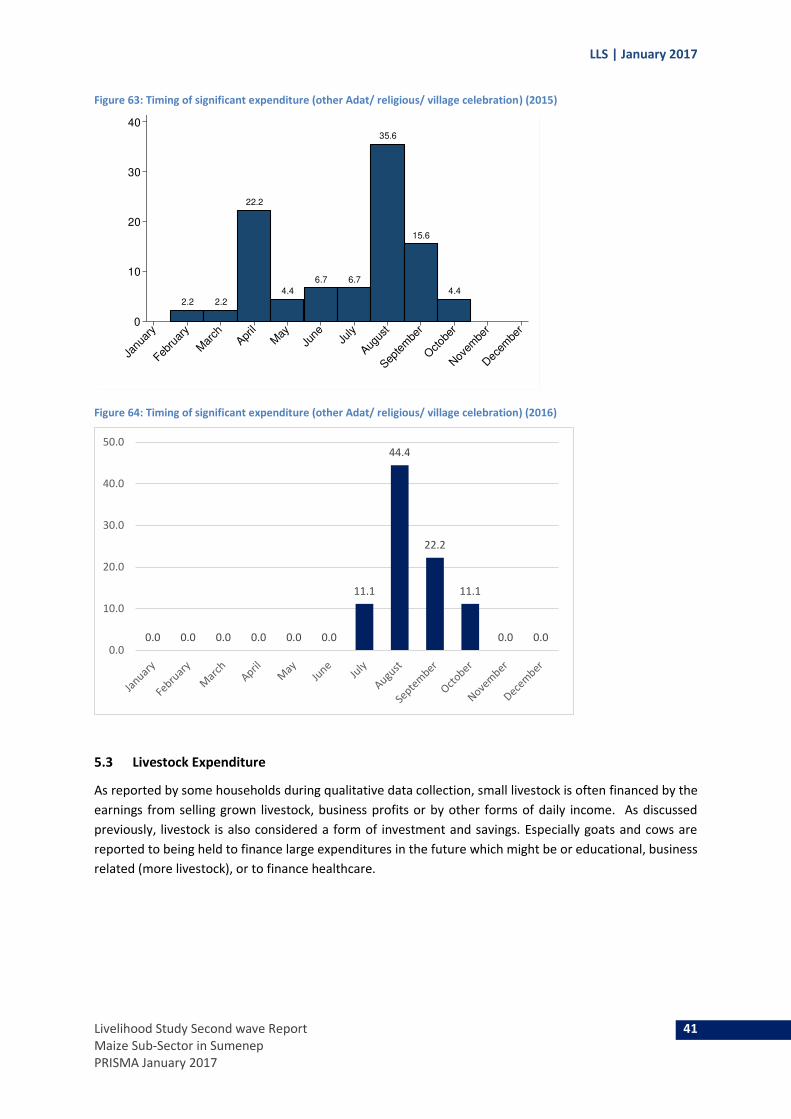

Regarding the timing of significant other expenditure (such as other adat, religious or village

celebrations), the months of August and September are the peak months for both 2015 (figure 63) and

2016 (figure 64).

2.5 2.53.8

2.5

15.0

20.0

7.5 7.5

15.0

23.8

0

5

10

15

20

25

Janu

ary

Febru

ary

Mar

chApr

ilM

ayJu

neJu

ly

Augus

t

Septe

mbe

r

Octob

er

Nov

embe

r

Dec

embe

r

Marriage

0.0

5.0

10.0

15.0

20.0

25.0

LLS | January 2017

Livelihood Study Second wave Report 41

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 63: Timing of significant expenditure (other Adat/ religious/ village celebration) (2015)

Figure 64: Timing of significant expenditure (other Adat/ religious/ village celebration) (2016)

5.3 Livestock Expenditure

As reported by some households during qualitative data collection, small livestock is often financed by the

earnings from selling grown livestock, business profits or by other forms of daily income. As discussed

previously, livestock is also considered a form of investment and savings. Especially goats and cows are

reported to being held to finance large expenditures in the future which might be or educational, business

related (more livestock), or to finance healthcare.

2.2 2.2

22.2

4.4

6.7 6.7

35.6

15.6

4.4

0

10

20

30

40

Janu

ary

Febru

ary

Mar

chApr

ilM

ayJu

neJu

ly

Augus

t

Septe

mbe

r

Octob

er

Nov

embe

r

Dec

embe

r

0.0 0.0 0.0 0.0 0.0 0.0

11.1

44.4

22.2

11.1

0.0 0.00.0

10.0

20.0

30.0

40.0

50.0

LLS | January 2017

Livelihood Study Second wave Report 42

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 65: Timing of Significant Expenditure - buying animal stock (2015)

5.4 Agricultural Assets and Inputs

No data available for 2016.

5.5 Repaying Debt

Usually households borrow money from their neighbours, family, and friends but have also access to

formal institutions as discussed previously. Data from 2015 (figure 66) and 2016 (figure 67) are consistent

in showing that the majority of expenditure on repaying debt is in the August-September window.

Figure 66: Timing of significant expenditure - repaying debt (2015)

6.5 6.5

8.7

10.9

6.5

8.7

17.4 17.4

10.9

4.3

2.2

0

5

10

15

20

Janu

ary

Febru

ary

Mar

chApr

ilM

ayJu

neJu

ly

Augus

t

Septe

mbe

r

Octob

er

Nov

embe

r

Dec

embe

r

7.1

3.6

10.7 10.7

3.6 3.6

17.9

21.4 21.4

0

5

10

15

20

Janu

ary

Febru

ary

Mar

chApr

ilM

ayJu

neJu

ly

Augus

t

Septe

mbe

r

Octob

er

Nov

embe

r

Dec

embe

r

Repaying Debt

LLS | January 2017

Livelihood Study Second wave Report 43

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 67: Timing of significant expenditure - repaying debt (2016)

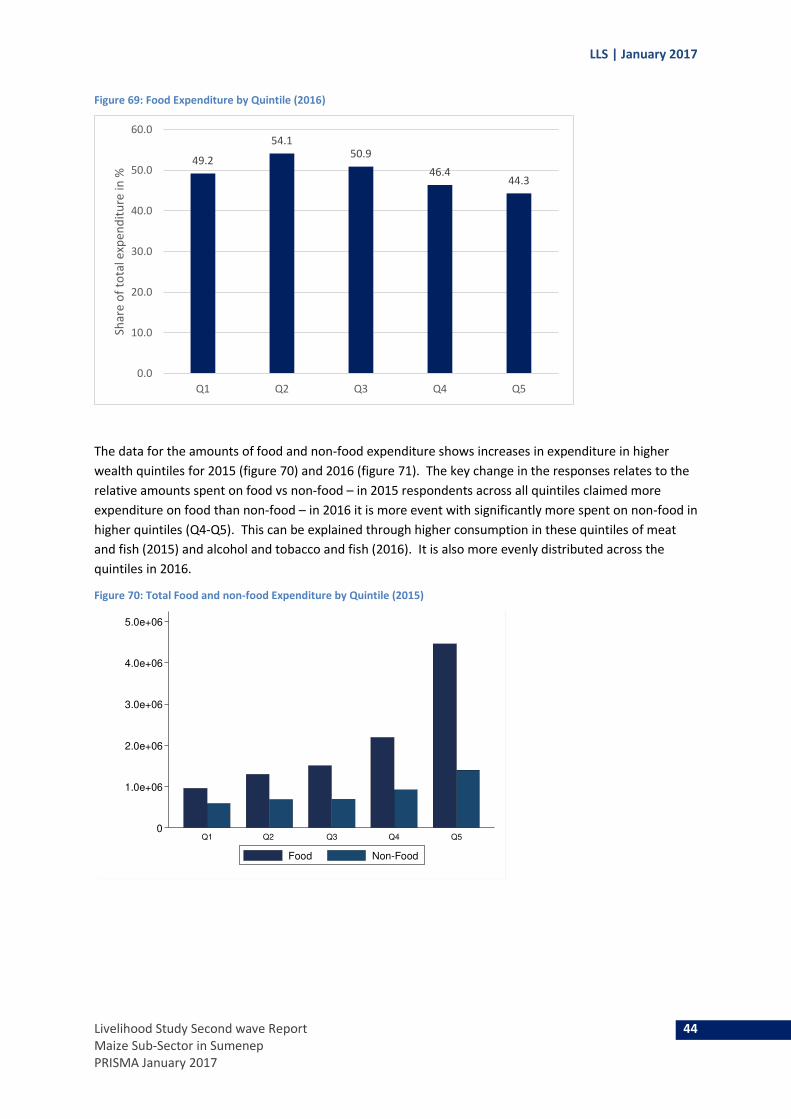

5.6 Food Expenditures

The share of food consumption is increased with expenditure quintile in 2015 (figure 68), which was

surprising, since wealthier households usually tend to have lower shares of food expenditure. In 2016

(figure 69) the data shows a slight decline in the percentage of expenditure on food by wealth quintile.

Figure 68: Food Expenditure by Quintile (2015)

9.1%

0.0% 0.0% 0.0% 0.0%

9.1%

0.0%

18.2%

9.1%

36.4%

9.1%

0.0%0.0%

10.0%

20.0%

30.0%

40.0%

63.465.7

69.470.9

74.0

0

20

40

60

80

Q1 Q2 Q3 Q4 Q5

Food Expenditure

LLS | January 2017

Livelihood Study Second wave Report 44

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 69: Food Expenditure by Quintile (2016)

The data for the amounts of food and non-food expenditure shows increases in expenditure in higher

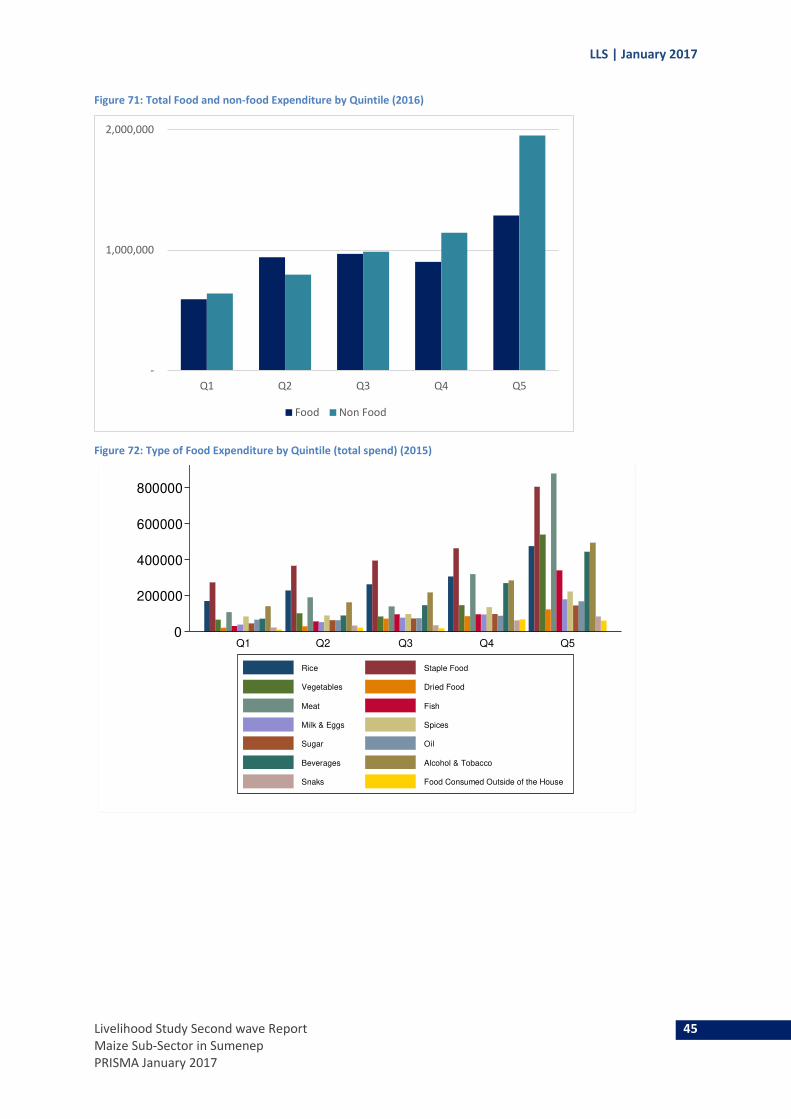

wealth quintiles for 2015 (figure 70) and 2016 (figure 71). The key change in the responses relates to the

relative amounts spent on food vs non-food – in 2015 respondents across all quintiles claimed more

expenditure on food than non-food – in 2016 it is more event with significantly more spent on non-food in

higher quintiles (Q4-Q5). This can be explained through higher consumption in these quintiles of meat

and fish (2015) and alcohol and tobacco and fish (2016). It is also more evenly distributed across the

quintiles in 2016.

Figure 70: Total Food and non-food Expenditure by Quintile (2015)

49.2

54.150.9

46.444.3

0.0

10.0

20.0

30.0

40.0

50.0

60.0

Q1 Q2 Q3 Q4 Q5

Sh

are

of

tota

l exp

en

dit

ure

in

%

0

1.0e+06

2.0e+06

3.0e+06

4.0e+06

5.0e+06

Q1 Q2 Q3 Q4 Q5

Total Food and Non-Food Expendiures by Quintile

Food Non-Food

LLS | January 2017

Livelihood Study Second wave Report 45

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 71: Total Food and non-food Expenditure by Quintile (2016)

Figure 72: Type of Food Expenditure by Quintile (total spend) (2015)

-

1,000,000

2,000,000

Q1 Q2 Q3 Q4 Q5

Food Non Food

0

200000

400000

600000

800000

Q1 Q2 Q3 Q4 Q5

Rice Staple Food

Vegetables Dried Food

Meat Fish

Milk & Eggs Spices

Sugar Oil

Beverages Alcohol & Tobacco

Snaks Food Consumed Outside of the House

LLS | January 2017

Livelihood Study Second wave Report 46

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 73: Type of Food Expenditure by Quintile (total spend) (2016)

The share of expenditure on rice and other staples is largely similar between 2015 (figure 74) and 2016

(figure 75). The percentage of expenditure on staples is around 15-20% in 2015 and 2016, where rice is

around 10-15% for both years (with exception being Q2 in 2016). The reported expenditure on alcohol

and tobacco is substantially increased in 2016 against 2015.

Figure 74: Share of Expenditure on Rice and Other staples by Quintile (2015)

-

50,000.0

100,000.0

150,000.0

200,000.0

250,000.0

300,000.0

Q1 Q2 Q3 Q4 Q5To

tal

exp

en

du

ture

pe

r m

on

th

Rice Staple food (included rice) Vegatable

Dried Food Meat Fish

Milk&Eggs Spices Oil

Sugar Beverages Alcohol&Tobacoo

Snaks

0

5

10

15

20

Q1 Q2 Q3 Q4 Q5

Rice Staple Food

Vegetables Dried Food

Meat Fish

Milk & Eggs Spices

Sugar Oil

Beverages Alcohol & Tobacco

Snaks Food Consumed Outside of the House

LLS | January 2017

Livelihood Study Second wave Report 47

Maize Sub-Sector in Sumenep

PRISMA January 2017

Figure 75: Share of Expenditure on Rice and Other staples by Quintile (2016)

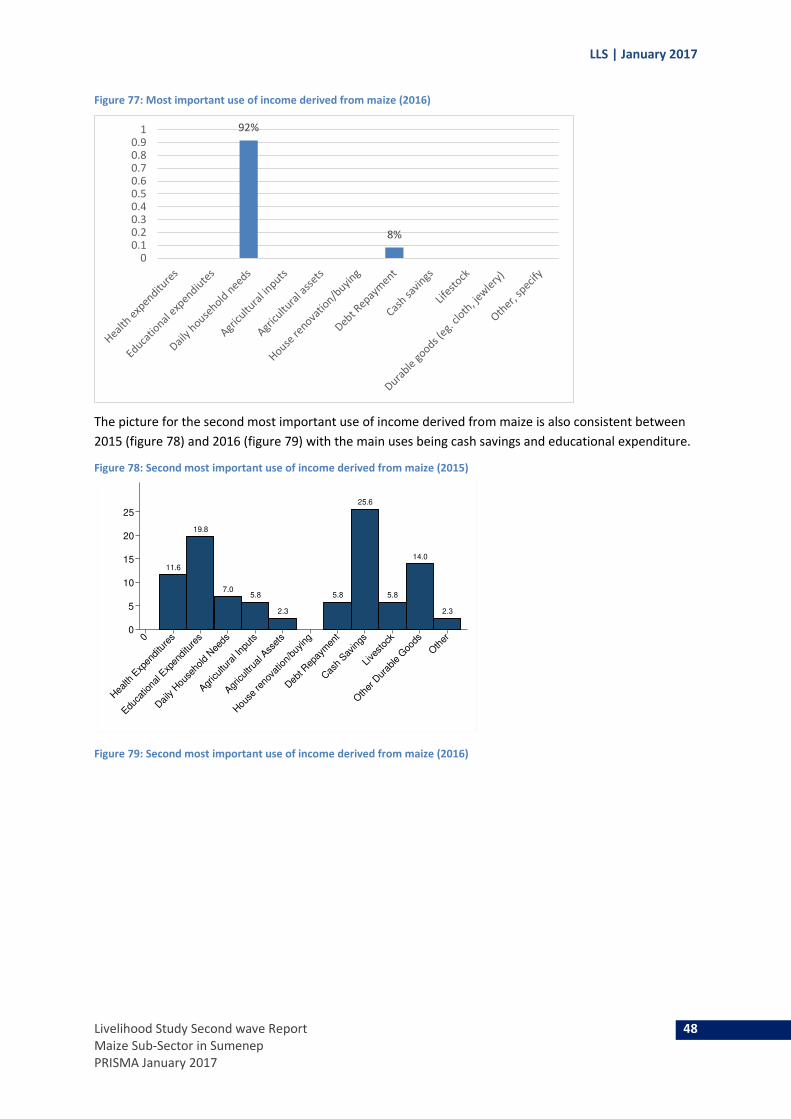

6 Income Use of Maize

The way income of maize is reported to be used. As can be seen in 2015 (figure 76) ad 2016 (figure 77),

maize earnings are mainly used to finance daily household needs.

Figure 76: Most important use of income derived from maize (2015)

0.0

5.0

10.0

15.0

20.0

25.0

Q1 Q2 Q3 Q4 Q5

Sh

are

of

tota

l exp

en

dit

ure

Rice Staple food (icluded rice) Vegatable Dried Food

Meat Fish Milk&Eggs Spices

Oil Sugar Beverages Alcohol&Tobacoo

Snaks

10.2

14.1

46.1

10.2

0.8 1.6

9.4

3.9 3.9

0

10

20

30

40

50

0

Hea

lth E

xpen

ditu

res

Educa

tiona

l Exp

enditu

res

Daily H

ouse

hold N

eeds

Agricultu

ral Inp

uts

Agricultru

al A

sset

s

Hou

se re

nova

tion/

buying