Water UK City Conference January 21, 2004 Research into Water Industry Financial Structures: Main...

22

Water UK City Conference January 21, 2004 Research into Water Industry Financial Structures: Main Findings John Smith

Transcript of Water UK City Conference January 21, 2004 Research into Water Industry Financial Structures: Main...

Water UK City ConferenceJanuary 21, 2004

Research into Water Industry

Financial Structures: Main Findings

John Smith

2

Background and Government Objectives

Background

• Government concern over shift away from equity and emergence of highly-geared structures.

• Does this affect the capacity of the industry to fund substantial investment programmes?

• What are the risks to delivery of Government objectives for the sector?

3

Background and Government Objectives

Government objectives for the sector

• To protect public health

• To protect and improve the environment – ensuring the industry can continue to finance and deliver quality and environmental improvements with minimum impact on bills

• To meet social goals – including ‘affordability’

• To safeguard services to customers

4

Project Scope and Methods

Project scope• Review reasons for recent changes• Understand properties of new structures• Consider whether the industry retains the capacity to fund

substantial investment programmes over next 15-20 years • Assess risks to delivery of Government objectives• Consider policy implications – for Government and Regulator

5

Project Scope and Methods

Methods• Review of evidence and literature• Interviews (>40) with relevant parties – water companies,

investors, rating agencies etc• Analysis of properties of different ‘models’• Three main types of analysis: - risk accommodation for the sector - investment requirements across companies - high level modelling to better understand

properties of different types of structure

6

Trends in Debt and GearingNet debt, Total WASCs over time

0

4,000

8,000

12,000

16,000

20,000

1993-94 1994-95 1995-96 1996-97 1997-98 1998-99 1999-00 2000-01 2001-02 2002-03

Net debt (£m 2002-03 prices)

Net debt / RCV gearing, Total WASCs

0%

10%

20%

30%

40%

50%

60%

70%

1993-94 1994-95 1995-96 1996-97 1997-98 1998-99 1999-00 2000-01 2001-02 2002-03

Net debt/ RCV (real prices)

7

Range of Structural Models

At least 4 models can be identified:

• CLG (Glas)• Thin equity (Anglian;Southern)• Pure Conventional (Wessex; Kelda)• Diversified groups with conventional structures (Severn

Trent;UU)

Key dimensions include structured finance; financial gearing; % of non appointed turnover

8

Drivers of Change: Views of Companies and Investors

Negative factors:

• low equity returns from 1999 review

• regulatory risk

• negative cash outflow - a factor contributing to French withdrawal

• financial failures – Hyder and Enron

Positive factors:• low risk profile attractive to

debt investors• favourable debt market

conditions• regulatory transparency• changes in equity market

9

Views on Prospects going forward

• Concerns – by companies and investors - about further extension of structured finance across the sector

• Strong commitment to retention of basic equity model within the sector

• Mixed capital structure seen as desirable – but concern that PR04 could force more companies could down the structured finance route. PR04 seen as a watershed – with some companies ‘sitting on the fence’

• Industry and investors looking for higher equity returns; improved incentives with scope for outperformance

• Where companies are foreign-owned, returns from UK water will be compared with those internationally

• Relaxation of merger regime seen as desirable – but limited impact on investor sentiment

10

1. Will the loss of equity from the sector weaken incentives?2. How much equity does the sector need?3. Will highly leveraged structures have the same appetite for

investment ?4. What are the implications for access to capital markets?5. Are highly leveraged companies more constrained by

financial ratios in financing future investment programmes?

Also (covered in the report):6. Are highly-leveraged structures more at risk of financial

distress?7. Are there risks of ‘systemic failure?’

Key Public Policy Issues

Some key findings

Full report: Structure of the Water Industry in England:

Does it Remain Fit for Purpose?

Report for: Defra and Ofwat

Authors: John Smith and Duncan Hannan

November 2003

12

1. Incentives and the properties of equity

• Conventional debt/equity dichotomy over-simplistic: in practice, there exists a spectrum of types of capital from most to least risk-taking

• Characteristics of equity replicable to some extent by forms of debt

• Weaker equity incentives compensated for, in part, by stronger accountability and governance arrangements within new structures - plus continued comparative competition; but

• Further losses of the equity model from sector remain a cause for concern – until such time as performance of new structures proven

13

2. How much equity does the sector need?

• Low risk, mature sector with stable cash flows and rising RCV. More limited value-upside potential

• Level of financial risk primarily related to annual spend (opex, capital maintenance & enhancement) rather than gearing per se

• High financial gearing of sector countered by low operational gearing (spend/RCV)

• Concept of ‘Equity/spend multiple’• On the basis of this measure, water sector enjoys greater level

of risk accommodation than other regulated sectors• Within water sector, lower levels of risk accommodation in

highly-leveraged structures. Less of a problem if low risk properties of sector confirmed

14

2. How much equity does the sector need?

Equity spend multiples in regulated sectors

0

4,000

8,000

12,000

16,000

20,000

£m

0.0x

0.5x

1.0x

1.5x

2.0x

2.5xRCV - Net debt

Annual spend

Equity spend multiple

15

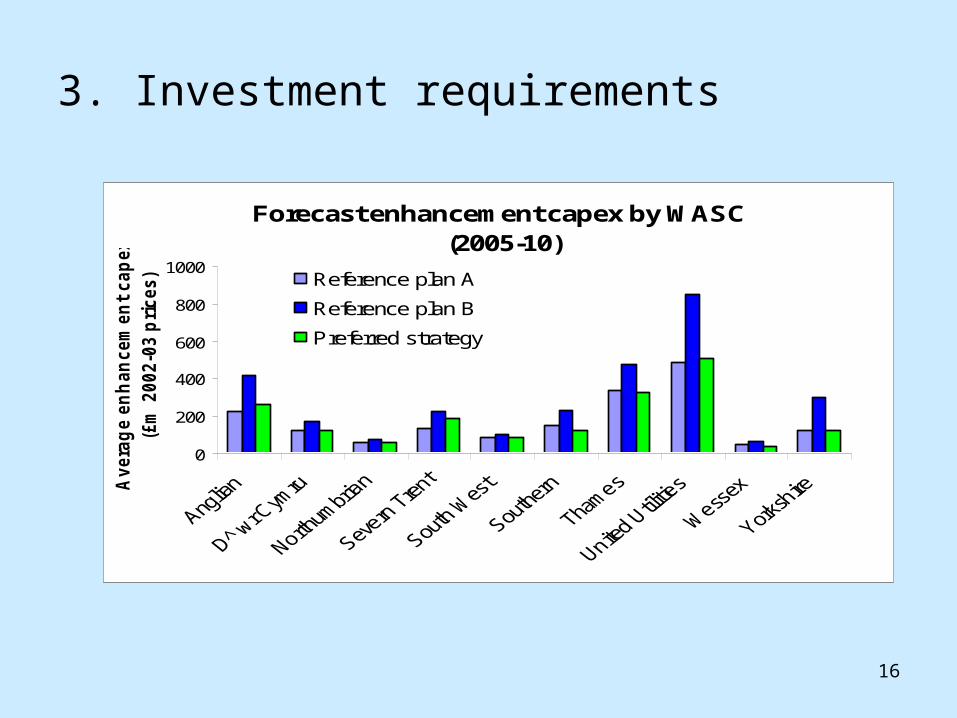

3. Investment requirements

• Scale of enhancement programme for PR04 substantial but significant variation across companies

• 3 WASCs account for 59% of projected enhancement spend (reference plan A)

• No obvious correlation between investment levels of preferred strategy and financial structure

• Company with biggest programme the first to raise new equity to fund investment in regulated business.

16

3. Investment requirements

Forecast enhancement capex by WASC (2005-10)

0

200

400

600

800

1000

Avera

ge e

nh

an

cem

en

t cap

ex p

.a.

(£m

2002-0

3 p

rices) Reference plan A

Reference plan B

Preferred strategy

17

4. Access to Capital Markets

• Financeability the key issue with the scale of capital the industry needs to raise

• Leveraged structures designed to tap a wider range of debt market segments (eg Eurobond market)

• Conventionally financed companies will also continue to be heavily dependent on debt markets

• Diversity of structures should broaden access to capital markets

18

5. Financeability

• Conventional companies have more flexibility for debt-financing investment at the margin – but face greater upward pressure on gearing

• Highly geared companies may find it easier to maintain gearing levels – because lower marginal contribution required from equity – even though they have less financial headroom below gearing covenants

• Reliance upon retained earnings has implications for dividend policy and regulatory determination (scope for outperformance)

• Financial ratio tests/covenants may change over time to reflect changing perceptions of risk

19

Conclusions

• No evidence that recent developments are jeopardising Government objectives

• Nevertheless, reasons to be cautious about new structures – particularly given success of traditional equity model since privatisation, and their limited track record

• Criticisms of highly leveraged structures take insufficient account of risk mitigation/governance features (new disciplines)

• Scale of financing requirement such that industry needs continued access to both debt and equity capital

• Strong case for seeking to maintain current diversity in corporate and financial structures

‘If Government objectives are best served by companies remaining focused on core business, recent developments can be viewed as helpful’

20

Some Policy Implications

Government• Benefits from consistency of Government policy towards the

sector – within long term framework• ‘Stability and certainty in institutional and management

arrangements’ important for investor confidence• Scale of investment requirements must be proportionate –

affordability and financeability are both important• Recognise that it is customers who ultimately pay• What sort of water industry would best meet Government

objectives in the longer term?

21

Some Policy Implications

Regulatory• Challenge is to provide a continued basis for viable equity

model – and avoid more companies coming under pressure to adopt structured finance

• Scope for outperformance will determine extent to which companies can generate retained earnings to fund investment at the margin.

• Need to evaluate performance of different structures over CP04

• Continued regulatory transparency• For future, application of incentive-based regulation to capital

structures?

22

Outstanding Questions

• Confirmation of the fundamental low risk properties of the sector – on which investor confidence is based

• Extent to which new structures are reversible• Financeability properties of different financial structures over

time?• Should junior debt be included in future regulatory

assessments of gearing and financeability?• Will there be further pressure from rating agencies for

structural protections?