Water Companies CAIS Reporting Guidance - · PDF fileWater Companies CAIS Reporting Guidance...

54

Water Companies CAIS Reporting Guidance - Final Water Companies CAIS Reporting Guidance Final V2.1 Page 1 of 54 Water Companies CAIS Reporting Guidance Final May 2012

Transcript of Water Companies CAIS Reporting Guidance - · PDF fileWater Companies CAIS Reporting Guidance...

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 1 of 54

Water Companies CAIS Reporting Guidance Final May 2012

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 2 of 54

Table of Contents

Table of Contents 2 Version Control 3 Experian Sign Off version 1.4 3 Industry Sign Off 44 Definitions 55 Overview 66 Water Company Guidance – Principles for Domestic Customers 77 Water Company Guidance on Default Process 9 Payment Scenarios for Full and Default reporting 1111 Unmeasured 1212 Measured 2323 Adding a additional person to an account 2626 Movers 3029 Appendix 1 - Default Only CAIS Fields 3534 Appendix 2 - Full CAIS Data Fields 3635 Appendix 3 - Acceptable CAIS Status Codes 3736 Appendix 4 - Acceptable Flag Settings 3837 Appendix 5 - CAIS Membership Requirements 4443 Appendix 6 – Privacy Notices for Water Companies 4645 Appendix 7 – Full Water Company Guide 4847 Appendix 8 – Notice of Default Wording and Information Sheet 5352

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 3 of 54

Version Control

Version Date Author/Updated by

Section Reason

Water Guidance V1

06/04/2011 CAIS Control All Creation following internal review

Water Guidance V1.1

12/04/2011 CAIS Control New Appendixes

Addition of the wording for Default notice for Water companies and the wording for Privacy Notices for water

Water Guidance V1.2

20/11/2011 Government Affairs

Default process

To allow for earlier registration in the case of CCJs and for the notice of intention to file a default to be sent before 90days.

Water Guidance V1.3

07/11/11 CAIS Consultancy Appendixes Clarify where some fields are not required for water companies

Water Guidance V1.4

13/02/2011 CAIS Consultancy Principles Water Companies reporting principles

Water Guidance V1.5

23/02/12 CAIS Consultancy Various Update following feedback

Water Guidance V1.6

02/03/12 CAIS Consultancy Various Update following feedback

Water GuidanceV1.7

06/03/12 CAIS Consultancy Various Update following feedback

Water Guidance V1.8

04/04/12 CAIS Consultancy Various Update following feedback

Water Guidance V2

13/04/12 CAIS Consultancy All Final Version approved, and issued as V2.

Water Guidance V2.1

30/04/12 CAIS Consultancy New Section

Adding section on person being added to an account

Experian Sign Off version 1.4

Name Role Department Date of Sign off

Gillian Key-Vice Head of Regulatory Developments - EMEA

Regulatory Developments 13/04/12

Jane Keywood CAIS Consultant CAIS Consultancy Team 13/04/12

Caroline Wood CAIS Consultant CAIS Consultancy Team 13/04/12

Claire Vasey Compliance Analyst Compliance Department 13/04/12

Phil Loines Account Director Utilities Credit Services 13/04/12

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 4 of 54

Industry Sign Off

Name Organisation Date of Sign off

Spencer Hough Anglian Water 30/03/12

Carla Tennant Anglian Water 30/03/12

Jonathan Harding Yorkshire Water/Loop 30/03/12

Tim Sheer Yorkshire Water/Loop 30/03/12

Vicky Taylor Yorkshire Water/Loop 30/03/12

Ian Donald Northumbrian Water 30/03/12

Mark Wilkinson Northumbrian Water 30/03/12

Arthur Foster Northumbrian Water 30/03/12

Michelle Simpson Southern Water 30/03/12

Claire Graham Southern Water 30/03/12

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 5 of 54

Definitions

Name Definition

CAIS Credit Account Information Sharing

Full CAIS All active, settled and defaulted account

Default CAIS Default only CAIS accounts reported at status code 8

Sale of debt Where defaulted accounts are sold to another organisation

ICO Information Commissioners Office

OFWAT Office of Water regulators

CC water Consumer Council Water

First Account The customer’s original account reported through to CAIS, for customers who pay their bills on time this will be their only account.

Second Account For customers who do not make payments and move into default, they will have a second account reported to CAIS when the subsequent bill is due.

Mover Where a customer moves out of a property

Measured Customers who pay a fixed standing charge for the service

Unmeasured Customers charged a fixed amount for the charges for the forthcoming year

Arrangement Temporary arrangement where CAIS member agrees to accept reduced payment

CAIS Status Codes See Appendix 3 for a full definition of each CAIS status code

CAIS Flags See Appendix 4 for a full definition of each CAIS flag

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 6 of 54

Overview

CAIS (Credit Account Information Sharing) is a closed user group containing records of customers’ credit commitments whether defaulted, settled or active to provide a month on month indication of their payment performance. CAIS membership is available at either ‘default’ or ‘full’ data levels. The member will then be entitled to retrieve the same level of data in return. A default only member submits and updates only those accounts which are defined as being in default, whereas at a full data level all accounts are submitted and updated whether these are paid and up to date, going into arrears – or in default. The following document covers both default only and full data reporting requirements. Where default only CAIS membership is being entered into, it is possible at a later stage to move into full reporting. When planning for default only reporting the process for full data needs to be followed to ensure adherence to default criteria as outlined in the industry agreement with the Information Commission. Once a member has joined CAIS they will be provided with a source code and members are obliged to send in regular monthly updates, each month’s data will be added to the existing file thereby updating records with the latest balance information and an accumulation of their payment performance history for full providers. CAIS members must also adhere to:

• Principles of Reciprocity

• The ICO Guidance Notes on Defaults

Both of these documents can be found on the Experian website under:- http://www.experian.co.uk/responsibilities/compliance/main-public.html

• The Data Protection Act and its requirements on fair processing and an accurate reflection

of each customer. The link to this is below

http://www.ico.gov.uk/for_organisations/data_protection/the_guide.aspx

• The data sharing code of practice. A link to this is below

http://www.ico.gov.uk/for_organisations/data_protection/topic_guides/data_sharing.aspx

In order to ensure that this initiative has the support of all stakeholders a key milestone in the initial development of data sharing there has been an agreement by OFWAT, CC Water, Water Companies and Water UK of a set of 7 Principles to define high level rules on how water companies should approach data sharing with Experian’s CAIS system (and indeed those systems operated by other credit reference agencies) and reflect this within their published information on their debt recovery procedures (the Code of Practice and Procedure on Debt Recovery) and their debt recovery practices. OFWAT and CC Water support the principle of data sharing but consider the details covered in the later sections of the document outside their area of activity and those aspects have been discussed with the ICO as the primary regulator of CAIS (and other credit referencing systems). As of 04/04/12 – the regulators had no further comments on this document at this point in time.

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 7 of 54

Water Company Guidance – Principles for Domestic Customers

Principle 1 – Code of Practice

• Every water companies Codes of Practice and Procedure on Debt recovery must reflect data

sharing and be agreed with the Regulator prior to the issue of privacy notices.

Principle 2 - Communication

• In accordance with the data protection requirements on fair processing and the guidance note on

defaults [up-date the title when available]. Water Companies must ensure that customers are

advised how information will be reported on their credit file.

• This will be achieved through privacy notices at the outset and communications at each stage

where applicable e.g. If payments are missed or “arrangements” set up.

• The Water companies will consult with CC Water on communication strategies.

• Communication strategies will be designed to ensure that companies provide clear communications

on the impact of data sharing and the availability of the Code of practice and Procedure on debt

Recovery to their customers throughout the collections process.

Principle 3 – Payment

• Unless there is an “arrangement” or court order is in place, any payment made by the customer will

always be posted against the oldest outstanding balance.

Principle 4 – Standard Arrangement

• Where a customer makes payments in accordance to the agreed arrangements (no matter the

value) Water companies will never file a default.

Principle 5 – Financially vulnerable

• The Water companies must at least accept the equivalent of DWP deductions, where the customer

is defined as vulnerable by the company.

• The company may accept a lower payment at their discretion.

• In such cases it will be marked as an “Arrangement” in accordance with the agreed processes and

will not progress to default until and unless the arrangement fails. Please refer to Appendix 4 for

acceptable CAIS flag reporting and the examples detailed in the Payment Scenarios on page

17.

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 8 of 54

Principle 6 – No Multiple Defaults

• Only 1 outstanding default can be filed against a customer at any one time, for any one property.

• Any future debt will be posted against the existing default

• In cases where a customer subsequently defaults after satisfying a default, a second default may be

recorded Please refer to the Payment Scenarios section starting on page 11 for details on

Unmeasured default reporting and page 21 for Measured customers.

Principle 7 – Reasonably Disputed Accounts

• Where the liability or accuracy of a bill that is reported to the credit bureau is reasonably disputed by

a customer, no default will be registered until the dispute is resolved.

The dispute will be reported to the credit bureau in accordance with the reporting rules set out in the data protection regulations. Please refer to Appendix 4 for acceptable CAIS flag reporting.

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 9 of 54

Water Company Guidance on Default Process

In addition to the above Principles, discussions have also taken place with the ICO on the circumstances under which a default may be registered. As with many non standard credit products specific rules are agreed and in the case of water providers there is a further complexity as they do not have the choice of ceasing to do business with a defaulting customer. This may lead to them continuing to provide the service and, potentially, find themselves in a similar position of default from that customer again. This requires some differences in the way that such accounts are recorded at CRAs. However, in common with other data providers, as far as is possible, consistency should be observed and the registration of a default, at CRAs, should still occur after 90 days of non payment and before 180 days. In accordance with already documented discussions for other utilities there are a number of triggers which, as long as they are clearly communicated to the customer or business, may be considered to be grounds for the registration of a default being:

• Where the supplier takes or has taken steps to cut off the service provided (or would do so if they were not prevented on social rather than commercial grounds or by other regulations, codes of practice or statute) or take legal action.

• Where there is evidence that the customer has left the property without making payment or arrangements to pay

In common with other credit providers, at least 28 days notice of the intention to file a default is still required. Appendix 6 and 7 provides a copy of the privacy notices that the water companies need to provide to all customers, both the condensed and the full versions of the notices (N.B. these documents are templates and can be modified by companies however they must be supplied to Experian for Compliance sign off). Notice of the intention to file such a default can occur before the 90 days have passed but must take place at least 28 days before the default is registered. In cases such as water where the service cannot be disconnected, the registration of a default should still occur within the normal timescales of between 90 - 180 days past due. In these cases a new account or agreement will be commenced within the water provider’s internal systems in order to register the ongoing supply. For those providers supplying positive as well as negative data this will result in a second account being registered at the CRA(s). The performance on that account will be supplied as normal. In Appendix 8 there is a copy of the standard wording that needs to be used when a customer goes into default along with an Information Sheet which goes with it. As per Principle 6 above, to prevent a large volume of defaults for the same product type and from the same supplier being reported to CRA(s) it is agreed that ideally just 1 default is registered over a 6 year period. Therefore at any time during a 6 year period a customer should normally only have 1 defaulted account and (potentially) one open active full data record. The balance on the defaulted account will vary as more defaults are added and settlements occur. The only time that this may change is if there is a break in the incidence of defaulting such that a default is settled and a new default is registered. In common with other types of accounts shared with CRAs, there are some exceptions to the 90 – 180 days rules such that a default may be registered earlier:

• In cases where legal action has been taken and a county court judgment issued, a default may be registered to co-inside with the date of the CCJ.

• If there is clear evidence of fraud

• If the debtor has absconded without making payment

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 10 of 54

Equally, a default would not be registered if an arrangement has been agreed with the debtor unless the amount offered is not accepted and deemed to be “token” amount, and a default can still be registered. This is covered in Principle 4 and 5 above. For accounts that do go into arrangement the debtor should be advised that in the event that they fail to maintain the arrangement a default will still be registered if the account is 90 days or more past due on the original terms. For more general guidance please see the industry agreement currently known as the ICO Guidance Note on Defaults.

For all accounts that go into arrears or default, the customer must be made aware of the impact on their record at credit reference agencies and which debt any payments made will be allocated to. This is especially important if payments will be allocated to the oldest debt so they are aware of which arrears are reducing – or that the default is being paid off but not any current full data record. This is important, as it may result in the current bill moving into arrears and default in spite of a payment being made, if this payment is allocated to the previous year’s default debt being that which is the oldest. This is covered in Principle 3 above

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 11 of 54

Payment Scenarios for Full and Default reporting

Water is supplied either measured or unmeasured to customers and businesses. Unmeasured customers are charged a set fixed amount which is due in advance and notified to them at the start of the financial year and they may pay their bill annually or half yearly or in instalments – in arrears. Measured customers pay a fixed standing charge for the service and then the charge for the water they have used. They too may pay their bills in instalments, in arrears. Most, if not all, Water Companies will share default data and then move into full data sharing so it is important to agree a methodology that allows the seamless stepping up to full data sharing. Thus these scenarios are designed to set out the recording that will need to be in place, whether or not the water company is actually sharing as a full or default provider. Below are some scenarios of how to report through to CAIS in differing situations – measured paid and unpaid, and unmeasured paid and unpaid bills. Within the tables, the guide provides details how to calculate and then report at full data sharing and default only data sharing.

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 12 of 54

Unmeasured

Unmeasured customers are charged a set fixed amount which is due and notified to them at the start of the financial year and they may pay their bill annually or half yearly or in instalments – in arrears.

Annual Bill unmeasured with full payment being made on time

Due Date Due Amount

Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

Action

25/04/09 £500 £500 22/04/09 0 N/A 0

Every month until the next annual bill is due this account needs to be sent with a 0 status for the full CAIS

data record. No default will be registered at this time. Scenario 1

For all the following scenarios when an account is reported at full data level and it moves into default for the first time, the full data history leading up to default will be reported on the same CAIS record. Thereafter, if a future account goes into default whilst the first default is outstanding the balance needs to be added to the balances on this account. The full data record will need to be supplied with a status U to show that it has been included within the default. Therefore a consumer could have multiple closed full data records at status U and 1 outstanding default. This methodology will be shown in the CAIS guidance so that other CAIS members are aware that this is what a closed status code U account means for a water record. The date of default will remain as the oldest date, the original default amount will be updated to show the increase. The current balance will also change to reflect and increase or decrease as a result of this being updated and payments (if any) are made.

Unmeasured Annual bill – no payment is made account 1 or account 2.

Account 1 Due Date Due

Amount Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

Action

25/04/09 £500 £0 0 N/A £500

25/05/09 £500 £0 1 N/A £500

25/06/09 £500 £0 2 N/A £500

26/07/09 £500 £0 3 N/A £500 Default Notification sent out at least 28 days beforehand

25/08/09 £500 £0 8 £500 Original Default balance £500 and the account moves into default

Scenario 2

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 13 of 54

Account 2 new full data account opened - there will be one default and one full data account

Due Date Due Amount

Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

Action

25/04/10 £500 £0 0 N/A £500 New account opened (the original default account remains on CAIS)

25/05/10 £500 £0 1 N/A £500

25/06/10 £500 £0 2 N/A £500

26/07/10 £500 £0 3 N/A £500 Intention to update the Default record Notification sent at least 28 days beforehand

25/08/10 U N/A £0 New account record reported as a status U with a £0 current balance and closed, at the same time as the existing default is updated

25/08/10 8 £1000 Original Default balance updated on existing default.

Scenario 3

In this scenario, if the customer does not pay in account 3 also then this will follow the same process for account 2 until such time as the customer makes a payment or it reaches 6 years since the original default. Normally, once 6 years has passed since the original Default Date a record will automatically be removed. To ensure that customers who fall into the above scenario, who are continually not making payments, do not have the default disappear, a running default will effectively be created. This will involve the oldest default details dropping off at year 6 and the newest default adding in. In order to manage this process there needs to be some changes made to the Original Default Balance and the Default Date field.

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 14 of 54

Year 6 – This assumes the customer defaulted by £500 each year, did not make any payments and no charges have been added.

Due Date Due

Amount Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

Action

25/04/15 £500 £0 0 N/A £500

25/05/15 £500 £0 1 N/A £500

25/06/15 £500 £0 2 N/A £500

26/07/15 £500 £0 3 N/A £500 Intention to update the Default Notification sent at least 28 days beforehand

25/08/15 U N/A £0 New account data record marked as a status U with a £0 current balance at the same time as the existing default is updated

25/08/15 8 £2500 Original Default balance updated with the year 6 amount. The default date is then updated to be 25/08/2010 which was the second default and ensures the record is not removed.

Scenario 4

For each new defaulted account providers must keep a record (separate to the CAIS reporting) of the default amount and the date at which this was defaulted. Using this information to remove the oldest default amount from the original default balance as this is due to drop off CAIS, and add in the latest amount. Additionally, the default date will need to be amended to reflect the next oldest default date. Every year following year 6 will follow the same pattern if no payment is ever made, the default date will be changed and the amount adjusted to remove the oldest default amount. In these cases, multiple full data accounts will be reported and will show as closed status U accounts but it would only be in the case where a customer continues to default year on year. This option is more complex, but more accurate and fairer to the customer. It has been agreed with the Information Commission that a review will take place after 5 years to see if this scenario does actually occur as it is suspected that once customers realise they will get defaulted by water companies they will not default account after account.

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 15 of 54

Unmeasured Annual Bill of £500 – Full payment made over 2 instalments as agreed at time of first bill

Due Date Due

Amount Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

Action

25/04/09 £250 £250 22/04/09 0 N/A £250

25/05/09 £0 0 N/A £250

25/06/09 £0 0 N/A £250

26/07/09 £0 0 N/A £250

25/08/09 £0 0 N/A £250

25/09/09 £0 0 N/A £250

25/10/09 £250 £250 22/10/09 0 N/A £0

25/11/09 £0 0 N/A

25/12/09 £0 0 N/A

25/01/10 £0 0 N/A

25/02/10 £0 0 N/A

25/03/10 £0 0 N/A Scenario 5

This full data record will continue to be reported every year until such time as it is closed (such as when the customer leaves the property) or moves into default. Unmeasured Annual bill of £500 – Agreed to pay in 2 half yearly instalments, however does not pay the first agreed instalment.

Due Date Due Amount

Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

Action

25/04/09 £250 £0 0 N/A £500

25/05/09 £250 1 N/A £500

25/06/09 £250 2 N/A £500

26/0709 £500 3 N/A £500 Default Notification sent out for full £500 at least 28 days beforehand

25/08/09 £500 8 £500 Default registered for full year charge of £500

Scenario 6

In this scenario, as the customer has not made the first payment once they reach 3 months in arrears and the terms are such that the full amount is then due on demand, the water company can issue the default notice for the full annual sum due and the default amount will be registered as the full £500.

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 16 of 54

Unmeasured Annual bill of £500 – Customer moves to pay by monthly instalments and does pay

Due Date Due

Amount Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

Action

25/04/09 £500 0 N/A 0 N/A £500 Customer has called and moved to pay bill via instalments

25/05/09 £45 £45 24/05/09 0 N/A £455

25/06/09 £45 £45 24/06/09 0 N/A £410

26/07/09 £45 £45 24/07/09 0 N/A £365

25/08/09 £45 £45 24/08/09 0 N/A £320

25/09/09 £45 £45 24/09/09 0 N/A £275

25/1009 £45 £45 24/10/09 0 N/A £230

25/11/09 £45 £45 24/11/09 0 N/A £185

25/12/09 £45 £45 24/12/09 0 N/A £140

25/01/10 £45 £45 24/01/10 0 N/A £95

25/02/10 £45 £45 24/02/10 0 N/A £50

25/03/10 £50 £50 24/03/10 0 N/A £0

If payments are made over 8 or 10 instalments, then the CAIS current balance will reduce to 0 earlier. This will then be reported each month until the following annual bill as a status code 0.

Scenario 7

Unmeasured Annual bill of £500 – Customer moves to pay by monthly instalments, makes initial payments and then ceases to pay

Due Date Due

Amount Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

Action

25/04/09 £500 0 N/A 0 N/A £500 Customer has called and moved to pay bill via instalments

25/05/09 £45 £45 24/05/09 0 N/A £455

25/06/09 £45 £45 24/06/09 0 N/A £410

26/07/09 £45 £45 24/07/09 0 N/A £365

25/08/09 £45 £0 1 N/A £365

25/09/09 £90 £0 2 N/A £365

25/10/09 £135 £0 3 N/A £365 Default Notification sent out for £365 at least 28 days beforehand

25/11/09 £365 £0 8 £365 Default Registered

Scenario 8

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 17 of 54

Unmeasured Annual bill of £500 – customer defaults on bill and then moves out of the property half way through the year.

Due Date Due

Amount Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

Action

25/04/09 £500 £0 0 N/A £500

25/05/09 £500 £0 1 N/A £500

25/06/09 £500 £0 2 N/A £500

26/07/09 £500 £0 3 N/A £500 Default Notification sent out for full £500 at least 28 days beforehand

25/08/09 £500 £0 8 £500 Default for full years £500

25/11/09 8 £350 Customer advised moved out, therefore the Original Default balance and the current balance reduced to reflect the reduced amount owed.

If the customer subsequently moves, the Original default balance will be amended to reflect what they owe at the time they left the property, but the default will remain, unless the default amount is equal to or less than the refund. The new customer moving into the property will have a separate full CAIS records reflecting the amount they owe from that point until the next annual bill.

Scenario 9

Unmeasured Annual bill of £500 – customer pays bill within 28 days of default notice Due Date Due

Amount Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

Action

25/04/09 £500 £0 0 N/A £500

25/05/09 £500 1 N/A £500

25/06/09 £500 2 N/A £500

26/07/09 £500 3 N/A £500 Default Notification sent out for full £500 at least 28 days beforehand

25/08/09 £500 £500 24/08/09 0 N/A £0 Payment made within 28 days so default is not registered and full data account is reported as up to date and is not closed

Scenario 10

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 18 of 54

Unmeasured Annual bill of £500 – customer negotiates a “reschedule” to pay the arrears at a higher value but to original terms (i.e. Debt cleared by year end) following the receipt of the Notice of Default but prior to the default being registered at the CRA. Please see appendix 4 for full details on re aging or re scheduling agreements.

Due Date

Due Amount

Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

CAIS Flag

Action

25/04/09 £500 £0 0 N/A £500

25/05/09 £500 £0 1 N/A £500

25/06/09 £500 £0 2 N/A £500

26/07/09 £500 £0 3 N/A £500 Default notification sent out at least 28 days beforehand

25/08/09 £500 £100 24/08/09 0 N/A £400 Customer contacts to request an Arrangement to pay more than original terms to bring the account back in line

25/09/09 £100 £100 24/09/09 0 N/A £300

25/10/09 £100 £100 24/10/09 0 N/A £200

25/11/09 £100 £100 24/11/09 0 N/A £100

25/12/09 £100 £100 24/12/09 0 N/A £0 Account now back up to date

25/01/10 £0 0 £0

25/02/10 £0 £0

25/03/10 £0 £0 Scenario 11

Unmeasured annual bill of £500 – Customer misses payment by due date and calls to set up payment arrangement after grace period expires. Customer cannot meet commitment for payment scheme to cover debt by next bill so an instalment arrangement is set up. Arrangement flag reported to CAIS and CAIS status deteriorates during the arrangement but not defaulted.

Arrangements to Pay – this is where an agreement has been made with the consumer to pay a temporary reduced payment. The original payment terms along with the agreed payment will be shown on the CAIS extract and the arrears will accrue and this will be reflected on the monthly status record. An Arrangement is where the consumer has fallen into financial difficulties and requires a reduced payment to help clear the arrears. This is not the same as a Payment Plan which is agreed at the start of agreement for the consumer to pay their water bill over a period of time. Please see appendix 4 for full details on Arrangements and re aging or re scheduling agreements.

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 19 of 54

Due Date

Due Amount

Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

CAIS Flag

Action

25/04/09 £500 £0 0 N/A £500

25/05/09 £500 £0 1 N/A £500

25/06/09 £500 £0 2 N/A £500

26/07/09 £500 £0 3 N/A £500 Default notification sent out at least 28 days beforehand

25/08/09 £500 £30 24/08/09 4 N/A £470 A Customer contacts to request an Arrangement to pay an amount less than the original terms.

25/09/09 £100 £30 24/09/09 5 N/A £440 A

25/10/09 £100 £30 24/10/09 6 N/A £410 A

25/11/09 £100 £30 24/11/09 6 N/A £380 A

25/12/09 £100 £30 24/12/09 6 N/A £350 A

25/01/10 £0 £30 24/01/10 6 N/A £320 A

25/02/10 £0 £30 24/02/10 6 N/A £290 A

25/03/10 £0 £30 24/03/10 6 N/A £260 A When the new bill is issued, the outstanding amount from this year will be added on and a new monthly payment agreed where possible.

Scenario 12

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 20 of 54

Unmeasured Annual bill of £500 – customer negotiates arrangement to pay following the receipt of the Notice of Default but prior to the default being registered at the CRA, makes payments under the new terms and then stops.

Due Date

Due Amount

Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

CAIS Flag

Action

25/04/09 £500 £0 0 N/A £500

25/05/09 £500 £0 1 N/A £500

25/06/09 £500 £0 2 N/A £500

26/07/09 £500 £0 3 N/A £500 Default notification sent out at least 28 days beforehand

25/08/09 £500 £100 24/08/09 4 N/A £400 A Customer contacts to request an arrangement to pay. Default is not registered and an A flag is supplied on the account to reflect the arrangement

25/09/09 £100 £100 24/09/09 5 N/A £300 A Arrears status will continue to accrue even though on arrangement

25/10/09 £100 6 N/A £300 A No payment is made. Send out revised default notification for £300 at least 28 days beforehand

25/11/09 8 £300 Register default for £300 outstanding

Scenario 13

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 21 of 54

Unmeasured Annual bill of £500 – customer on monthly instalments, but makes payments sporadically then stops paying

Scenario 14

Unmeasured Annual bill of £500 – customer doesn’t pay, and asks to be put onto an arrangement, but the amount offered is low and the arrangement is not “approved” so customer account is defaulted even though the token payments are being made – no arrangement flag is used in this case. Where the amount is accepted no matter what value this will not be defaulted as per Principle 4.

Due Date

Due Amount

Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

Action

25/04/09 £500 0 N/A £500

25/05/09 £500 1 N/A £500

25/06/09 £500 2 N/A £500

26/07/09 £500 3 N/A £500 Default notification sent out at least 28 days beforehand

25/08/09 £490 £10 24/08/09 8 £490 Customer calls and makes a payment for £10 and offers to pay £10 per month. This is a token payment, so account continues to default with the original default balance being that at the date of default (in this case £490) and the balance reducing as further payments are made.

Scenario 15

Due Date Due Amount

Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

Action

25/04/09 £45 £45 24/04/09 0 N/A £455

25/05/09 £45 £45 24/05/09 0 N/A £410

25/06/09 £45 1 N/A £410

26/07/09 £45 2 N/A £410

25/08/09 £45 £45 24/08/09 2 N/A £365

25/09/09 £45 £90 24/09/09 0 N/A £275

25/10/09 £45 £45 24/10/09 0 N/A £230

25/11/09 £45 1 N/A £230

25/12/09 £45 2 N/A £230

25/01/10 £45 3 N/A £230 Send out Default Notification for £230 at least 28 days beforehand

25/02/10 £230 8 £230 Default registered

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 22 of 54

Unmeasured Annual bill of £500 – customer defaults year 1, pays year 2 and satisfies the default, then in year 3 defaults again

Account 1 – Customer Defaults Due Date

Due Amount

Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

Action

25/04/09 £500 £0 0 N/A £500

25/05/09 £500 £0 1 N/A £500

25/06/09 £500 £0 2 N/A £500

26/07/09 £500 £0 3 N/A £500 Default Notification sent out at least 28 days beforehand

25/08/09 £500 £0 8 £500 Original Default balance £500 and the account moves into default

Scenario 16A

Account 2 – Customer pays and satisfies the outstanding default from year 1 Due Date

Due Amount

Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

Action

25/04/10 £500 £1000 24/04/10 0 N/A £0 A new full data record is recorded

25/04/10 8 £0 Default already registered in year 1 marked with a £0 balance and the default satisfaction date recorded as 24/04/2010

25/05/10 £0 0 £0 Full data record continues to be updated throughout the remainder of the year

25/06/10 £0 0 £0

26/07/10

25/08/10 Scenario 16B

Account 3 – Customer Defaults again – a new (second) default is registered

Due Date

Due Amount

Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

Action

25/04/11 £500 £0 0 N/A £500

25/05/11 £500 £0 1 N/A £500

25/06/11 £500 £0 2 N/A £500

26/07/11 £500 £0 3 N/A £500 Default Notification sent out at least 28 days beforehand

25/08/11 £500 £0 8 £500 Original Default balance £500 and the account moves into default

Scenario 16C

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 23 of 54

Measured

Measured customers pay a fixed standing charge for the service and then the charge for the water they have used. They too may pay their bills in instalments, in arrears.

Measured accrues a charge of £400 over the year and arranged to pay quarterly with an estimated annual bill of £400 in 4 instalments of £100 – all fully paid on time.

Due Date

Due Amount

Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

Action

25/04/09 £100 £100 24/04/09 0 N/A £0

25/05/09 £0 0 N/A £0

25/06/09 £0 0 N/A £0

26/07/09 £100 £100 24/07/09 0 N/A £0

25/08/09 £0 0 N/A £0

25/09/09 £0 0 N/A £0

25/10/09 £100 £100 24/10/09 0 N/A £0

25/11/09 £0 0 N/A £0

25/12/09 £0 0 N/A £0

25/01/10 £100 £100 24/01/10 0 N/A £0

25/02/10 £0 0 N/A £0

25/03/10 £0 0 N/A £0 Scenario 1

Measured Quarterly bill payment. Customer does not make the first payment as agreed but pays it as the second payment falls due in July. Then misses the second payment but pays that together with the third payment and then pays on time.

Due Date

Due Amount

Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

Action

25/04/09 £100 £0 0 N/A £100

25/05/09 £100 1 N/A £100

25/06/09 £100 2 N/A £100

26/07/09 £100 £100 22/07/09 0 N/A £100

25/08/09 £100 1 N/A £100

25/09/09 £100 2 N/A £100

25/10/09 £100 £200 24/10/09 0 N/A £0

25/11/09 £0 0 N/A £0

25/12/09 £0 0 N/A £0

25/01/10 £100 £100 24/01/10 0 N/A £0

25/02/10 £0 0 N/A £0

25/03/10 £0 0 N/A £0 Scenario 2

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 24 of 54

Measured charge due to be paid through Quarterly Bill when issued – no payments received

Due Date

Due Amount

Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

Action

25/04/09 £100 £0 0 N/A £100

25/05/09 £0 1 N/A £100

25/06/09 £0 2 N/A £100

26/07/09 £100 £0 3 N/A £100 Default notification sent for £200 at least 28 days beforehand

25/08/09 £0 8 £100 Original Default balance £200

25/09/09 No CAIS Update

25/10/09 £100 £0 £200 Intention to update the Default Notification sent

25/11/09 £0 £200 Original default balance updated to £300

25/12/09 No CAIS Update

25/01/10 £100 £0 £300 Intention to update the Default Notification sent

25/02/10 £0 £00 Original default balance updated to £400

25/03/10 No CAIS Update Scenario 3

By the end of the year they will have 1 default account showing £400 original default balance.

For all the above scenarios where a default is registered, it must show the annual position when the financial year ends. Then for the following year – or billing cycle the record will restart as a new account to record the full data record as up to date and will move through the cycle once more as per the scenario in the unmeasured. This will follow the same process for year on year defaults up to year 6. Measured charge of £350 due to be via a budget plan over 10 months - all payments made

Due Date

Due Amount

Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

Action

25/04/09 £35 £35 24/04/09 0 N/A £315

25/05/09 £35 £35 24/05/09 0 N/A £280

25/06/09 £35 £35 24/06/09 0 N/A £245

26/07/09 £35 £35 24/07/09 0 N/A £210

25/08/09 £35 £35 24/08/09 0 N/A £175

25/09/09 £35 £35 24/09/09 0 N/A £140

25/10/09 £35 £35 24/10/09 0 N/A £105

25/11/09 £35 £35 24/11/09 0 N/A £70

25/12/09 £35 £35 25/12/09 0 N/A £35

25/01/10 £35 £35 25/01/10 0 N/A £0

25/02/10 £0 0 N/A £0

25/03/10 £0 0 N/A £0 Scenario 4

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 25 of 54

Measured charge of £350 due to be via a budget plan over 10 months – non payment after the first 2 instalments

Due Date

Due Amount

Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

Action

25/04/09 £35 £35 24/04/09 0 N/A £315

25/05/09 £35 £35 24/05/09 0 N/A £280

25/06/09 £35 1 N/A £280

26/07/09 £35 2 N/A £280

25/08/09 3 N/A £280 Default notification issued

25/09/09 8 £280 Default registered for the outstanding £280

Scenario 5

If a customer satisfies a default account, the default satisfaction date needs to be supplied, and if a customer then goes into default again, a new default will be registered in these instances the existing default will not be updated.

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 26 of 54

Adding a additional person to an account

If an account has been registered in a single name, and it is then identified that there are 2 or more people who are jointly and severally liable the additional parties need to be added onto CAIS so that accounts are identified as joint agreements. The parties added to the account will need to be advised that the account is being changed to a joint account on CAIS. Where a party is being added to a solo account already reported to CAIS the existing account number requires an account number change by adding the joint account indicator of 1 in the 20th byte of the account number (please refer to the CAIS layout manual for the full process). The party or parties being added to the account should be supplied each as an additional record with the same account number details but a 2 etc (depending on the number of parties being added) in the 20

th

byte.

Unmeasured or measured where a party is being added to an existing account that has no arrears.

Due Date Due Amount

Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

Action

25/04/09 £500 £500 25/04/09 0 N/A £0

25/05/09 £0 0 N/A £0

25/06/09 £0 0 N/A £0 Become aware that others are in property and are also liable for debt. Notify the parties that the record on CAIS is to be amended. New party to be added to the account, and using the new account number field add 1 in the 20

th byte

to the existing account number, the new party is added as a separate record with 2 in the 20

th byte of the

account number, and so on for more parties

26/07/09 £0 0 N/A

26/08/09 £0 0 N/A £0

Scenario 1 Account number 1 and 2

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 27 of 54

In the event that the account is already in arrears, but not in default, the new party should be notified that they are jointly and severally liable for the debt and that it is in arrears. They should be given time to make payment or seek an arrangement so there should be a time period of 28 days between notifying them that they are to be added to the account and are jointly liable for the debt and adding them to CAIS. If they do not make payment or some other satisfactory arrangement in the intervening period then they should be added to the account as outlined above.

Unmeasured or measured where a party is being added to an existing account that is in arrears. Due Date Due

Amount Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

Action

25/04/09 £500 £500 25/04/09 0 N/A £500

25/05/09 £0 1 N/A £500

25/06/09 £0 2 N/A £500 Advised that there are others in property, notify of liability and intention to add to account if no acceptable arrangements or payments made in next 28 days.

25/07/09 £0 3 N/A £500 If no payment made or acceptable arrangements made add new party, and using the new account number field add 1 in the 20

th byte

to the existing account number, the new party is added as a separate record with 2 in the 20

th byte of the

account number. The status code on the new account will be the arrears level as the original account

Scenario 2 Account number 1 and 2

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 28 of 54

If an account is already registered as having a default in a single name and then it is identified that there are 2 or more people who are jointly and severally liable the additional parties need to be added onto the providers’ own records and onto CAIS. A notice of intention to file a default should be sent to the additional parties to give them time to make payment or other arrangements ahead of being added to the file. After 28 days, if they have not made satisfactory arrangements the fields relating to default should be supplied to CAIS to match the original default. If satisfactory arrangements are made then the original defaulted account should have the default fields removed and the status code on both accounts reported as the arrears level prior to default.

Unmeasured or measured where a party is being added to an existing account that is in default and they do not offer payment or arrangement to bring the account in line Due Date Due

Amount Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

Action

25/04/09 £500 £500 25/04/09 0 N/A £500

25/05/09 £0 1 N/A £500

25/06/09 £0 2 N/A £500

25/07/09 £0 3 N/A £500 25/08/09 £500 8 £500 Advised that there

are others in property, notify of liability and intention to add to account and send notice of intention to file a default If no payment made or acceptable arrangements made add new party and add 1 in the 20

th byte to the

existing account number supplied The new party is added as a separate record with 2 in the 20

th

byte of the account number.

If however alternative arrangements are offered, such as DWP payments, the status codes must be reset to the status prior to the adding to the default.

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 29 of 54

Unmeasured or measured where a party is being added to an existing account that is in default and they offer payment or other remedy such DWP payments

Due Date Due Amount

Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

Action

25/04/09 £500 £500 25/04/09 0 N/A £500

25/05/09 £0 1 N/A £500

25/06/09 £0 2 N/A £500

25/07/09 £0 3 N/A £500 25/08/09 £500 3 £500 At this stage the

account number has been changed to add the 1 in the 20

th byte

Scenario 3 Account number 1

Due Date Due Amount

Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

Action

25/08/09 £500 £500 27/04/09 3 N/A £500 Account reported as new record with a joint account indictor of 2 etc depending in the number of parties being added

Scenario 3 Account number 2

Measured or Unmeasured Customer advises they have moved into a property, where the existing customer has already got a default registered.

If a customer moves into a property and is becoming jointly and severally liable with the existing occupant, the additional parties should be added onto CAIS. However in this scenario the new party is not liable for the existing default, the default must remain separate in the name of the original customer. A new account will have to be started and reported as a joint agreement with a 1 in the 20

th byte reported for the first party and a 2 etc (depending on the number of parties being added) for

the parties joining the agreements.

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 30 of 54

Movers

If a customer moves house within the same region (and therefore the same water company) the account will continue and the address needs to be updated, therefore the history of their account will move with them to the new property. Unmeasured or measured customer who notifies the water company they are moving address within the same region

Due Date Due Amount

Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

Action

25/04/09 £500 £500 25/04/09 0 N/A £0

25/05/09 £0 0 N/A £0

25/06/09 £0 0 N/A £0

26/07/09 £0 0 N/A Customer contacts to advise moving house. Account continues to be reported but the address information is updated to be the new property.

26/08/09 £0 0 N/A £0

Scenario 1

Unmeasured or measured customer who notifies the water company they are moving address into a different region Due Date

Due Amount

Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

CAIS Close Date

Action

25/04/09 £500 £500 25/04/09 0 N/A £0

25/05/09 £0 0 N/A £0

25/06/09 £0 0 N/A £0

25/07/09 £0 0 N/A £0 24/07/09 Customer advises moving house out of the region. CAIS account is closed with no further updates required.

Scenario 2

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 31 of 54

Measured or Unmeasured customer who has defaulted at address and subsequently moved house without notification. The new occupant advises the water company they have moved into the property

Due Date Due

Amount Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

CAIS Flag

Action

25/04/09 £500 £0 0 N/A £500

25/05/09 £500 £0 1 N/A £500

25/06/09 £500 £0 2 N/A £500

26/07/09 £500 £0 3 N/A £500 Default Notification sent out at least 28 days beforehand

25/08/09 £500 £0 8 £500 Original Default balance £500 and the account moves into default

25/09/10 8 £500 G- Gone Away

New Customer advises they have moved in. Default marked with a Gone away flag, all other details remain the same

The new occupant of the house will have a new full CAIS record started – following either the measured for unmeasured scenarios above

Scenario 3

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 32 of 54

Measured or Unmeasured Customer advises they are moving house, they do not pay final bill nor provide a forwarding address

Due Date Due

Amount Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

CAIS Flag

Action

25/04/09 £500 £0 0 N/A £500

25/05/09 £500 £0 1 N/A £500 G – Gone Away

25/06/09 £500 £0 2 N/A £500 G – Gone Away

26/07/09 £500 £0 3 N/A £500 G – Gone Away

Default Notification sent out at least 28 days beforehand

25/08/09 £500 £0 8 £500 G – Gone Away

Original Default balance £500 and the account moves into default

Where the final bill is not paid, the customer will still escalate through the cycle into arrears. The last known address will be reported through to CAIS, and the Gone Away flag will also be added to the account.

Scenario 4

If a customer moves house out of the region then a final bill will be sent for settlement. If the customer pays this in full the settlement date will be added the record will remain on their CAIS file for 6 years from that date. It is recognised that there will be cases where the debtor is no longer, or believed to be no longer at the address at which the debt was incurred. If a (reliable) forwarding address is known, the default should be registered at that address. Under the terms of CAIS membership, the address must be validated to ensure that the debtor is at a new address before doing so, in other words, unless the debtor themselves has provided a new address; using a tracing service and locating a person of the same or similar name is not sufficient, you must have made other checks to satisfy yourselves that the new address is correct, and then the notice should be sent to that address. If you cannot, validate the new address, even where it is believed that the debtor is no longer resident you must have sent at least one default notice and therefore it must be sent to the last known address.

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 33 of 54

Sale of Debt

There are two different processes regarding the updating of CAIS records for sale of debt depending on whether the debt purchaser is already a member of CAIS or not. Both procedures are referred to in the ICO guidance note on default records as noted below, and they do suggests that lenders have an interest to make sure the debt purchaser they sell to is a member of CAIS. Sale of debt to a non member of CAIS If the records are sold to non-CAIS members then the records should remain in the name of the original lender but the debt show satisfied. This is done by providing the records on the normal monthly file but as a default (if it is defaulted) with a zero current default balance. Records should also be updated with the CAIS flag of “C” debt assigned. Measured or Unmeasured default sold to a Debt Purchaser who is not a CAIS member

Due Date

Due Amount

Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

CAIS Flag

Action

25/04/09 £500 £0 0 N/A £500

25/05/09 £500 £0 1 N/A £500

25/06/09 £500 £0 2 N/A £500

26/07/09 £500 £0 3 N/A £500 Default Notification sent out at least 28 days beforehand

25/08/09 £500 £0 8 £500 Original Default balance £500 and the account moves into default

25/09/10 8 £0 C – Debt sold to None CAIS Member

When debt sold the C flag will be set and the account updated to show £0 current balance. Original default balance remains as £500

Scenario 1

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 34 of 54

Sale of debt to a CAIS member If the records are sold to a CAIS member then the records should remain on the water company portfolio, but the debt show satisfied with the CAIS flag of “S”. To achieve this, the default account will be updated to show a zero current balance and the S flag will be supplied. The original default amount and the default date will remain. (See description of flags later in this document). Measured or Unmeasured default sold to a Debt Purchaser who is a CAIS member

Due Date

Due Amount

Payment Amount

Payment Date

Full Data CAIS Status

Default Data CAIS Status

CAIS Current Balance

CAIS Flag

Action

25/04/09 £500 £0 0 N/A £500

25/05/09 £500 £0 1 N/A £500

25/06/09 £500 £0 2 N/A £500

26/07/09 £500 £0 3 N/A £500 Default Notification sent out at least 28 days beforehand

25/08/09 £500 £0 8 £500 Original Default balance £500 and the account moves into default

25/09/10 8 £0 S – Sold to CAIS Member

When debt sold the S flag will be set and the account updated to show £0 current balance. Original default balance remains as £500

Scenario 2

Where debt is sold to a CAIS member, they register the default account with the balance outstanding a per the sale. Typically when a sale is taking place a three-way discussion is arranged between the client, the Debt Purchaser and Experian on when this will take place and we will see the new records being added onto CAIS by the new owner.

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 35 of 54

Appendix 1 - Default Only CAIS Fields

The following 2 sections provide information on which fields must be populated when submitting the CAIS file at default only level and full data sharing, and some useful comments on these fields.

Description of field Default Data Record Comments

Account Number Mandatory This must be unique for each customer

Account Type Mandatory Account type 39 to be used for all accounts

Start Date Mandatory This will generally be the date the customer moves in

Default Date Mandatory The date the default becomes effective

Monthly Payment Not Applicable N/A on defaulted accounts

Repayment Period Not Applicable

Current Balance Mandatory Set to current amount outstanding

Credit Balance Indicator Not Applicable

Account Status Mandatory For default only reporting this is always 8

Special Instruction Indicator

Where Applicable D - may be used if ever need to delete an account. A - Must be used if need to change the address on a defaulted account

Experian block

Payment Amount Not Applicable

Credit Payment Indicator Not Applicable

Last Statement Balance Not Applicable

Last stat balance indicator

Not Applicable

Number of cash advances

Not Applicable

Value of cash advances Not Applicable

Payment Code Not Applicable

Promotional Activity flag Not Applicable

Transient Association Flag

Where Applicable To be used on all accounts to prevent financial associations being created.

Air-time flag Not Applicable

Flag Settings Where Applicable Use all applicable on default accounts

Name & Address Mandatory Must be provided and for the name this includes title, forename, middle initial if known and surname

Credit Limit Not Applicable

Date of Birth Mandatory Must be provided on all accounts

Transferred to collection Account flag

Not Applicable

Balance Type Not Applicable

Credit turnover Not Applicable

Primary Account indicator Not Applicable

Default Satisfaction Date Where Applicable To be provided when the default is paid off in full

Transaction Flag Not Applicable

Payment Frequency Where Applicable

Original Default Balance Mandatory Balance set to amount customer goes into default for. This field can be updated with future defaults until satisfied

New Account Number Where Applicable To be used if the original account number supplied is being changed.

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 36 of 54

Appendix 2 - Full CAIS Data Fields

Description of field Default Data Record Comments

Account Number Mandatory This must be unique for each customer

Account Type Mandatory Account type 39 to be used for all accounts

Start Date Mandatory This will generally be the date the customer moves in

Close Date Mandatory The date they no longer take your water supply

Monthly Payment Not Applicable Could be supplied for those paying a fixed monthly amount. Not all accounts will have this detail

Repayment Period Not Applicable

Current Balance Mandatory Set to current amount outstanding

Credit Balance Indicator Not Applicable

Account Status Mandatory 0,1,2,3,4,5,6,8,U,D can be supplied. See full layout for details

Special Instruction Indicator

Where Applicable D - may be used if ever need to delete an account.

Experian block Mandatory

Payment Amount Not Applicable

Credit Payment Indicator Not Applicable

Last Statement Balance Not Applicable

Last stat balance indicator

Not Applicable

Number of cash advances

Not Applicable

Value of cash advances Not Applicable

Payment Code Not Applicable

Promotional Activity flag Not Applicable

Transient Association Flag

Where Applicable To be used on all accounts to prevent financial associations being created.

Air-time flag Not Applicable

Flag Settings Where Applicable Use all applicable on default accounts

Name & Address Mandatory Must be provided and for the name this includes title, forename, middle initial if known and surname

Credit Limit Not Applicable

Date of Birth Mandatory Must be provided on all accounts

Transferred to collection Account flag

Not Applicable

Balance Type Not Applicable

Credit turnover Not Applicable

Primary Account indicator Not Applicable

Default Satisfaction Date Where Applicable To be provided when the default is paid off in full

Transaction Flag Applicable to certain Account Types

Payment Frequency Where Applicable

Original Default Balance Mandatory Balance set to amount customer goes into default for.

New Account Number Where Applicable To be used if the original account number supplied is being changed.

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 37 of 54

Appendix 3 - Acceptable CAIS Status Codes

These are the status codes that can be reported through to CAIS. For full data sharing all of these may be required. For default only reporting only status 8 will be used.

Status code

Description

U Unclassified - The member is unable to make any statement, whether positive or adverse on the performance of this account for the period in question. A 'U' may be used for the first period of the life of an account when the first payment is yet to be made. (Maximum 2 months unless BNPL account)

0 In advance, up-to-date or less than one payment due but unpaid (or were due and unpaid when settled).

1 More than one but less than two payments due but unpaid (or were due and unpaid when settled).

2 More than two but less than three payments due but unpaid (or were due and unpaid when settled).

3 More than three but less than four payments due but unpaid (or were due and unpaid when settled).

4 More than four but less than five payments due but unpaid (or were due and unpaid when settled).

5 More than five but less than six payments due but unpaid (or were due and unpaid when settled).

6 Six or more payments due but unpaid or (or due and unpaid when settled).

8 Defaulted Balance - At the date of default the customer had failed to meet the contractual obligations and had failed to satisfactorily respond to requests that the account be put into order. The circumstances where an account should be defaulted are more fully explained in the ICO guidance note on the filing of defaults and members are advised to follow this as a guide to best practice. In outline

• As best practice defaults should not normally be filed where the debt is less than three consecutive months in arrears.

• Accounts where payments have not been received for six months should normally be filed as being in default.

• Exceptions may occasionally apply where the credit is over a very short or very long term or where there is some element of fraud.

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 38 of 54

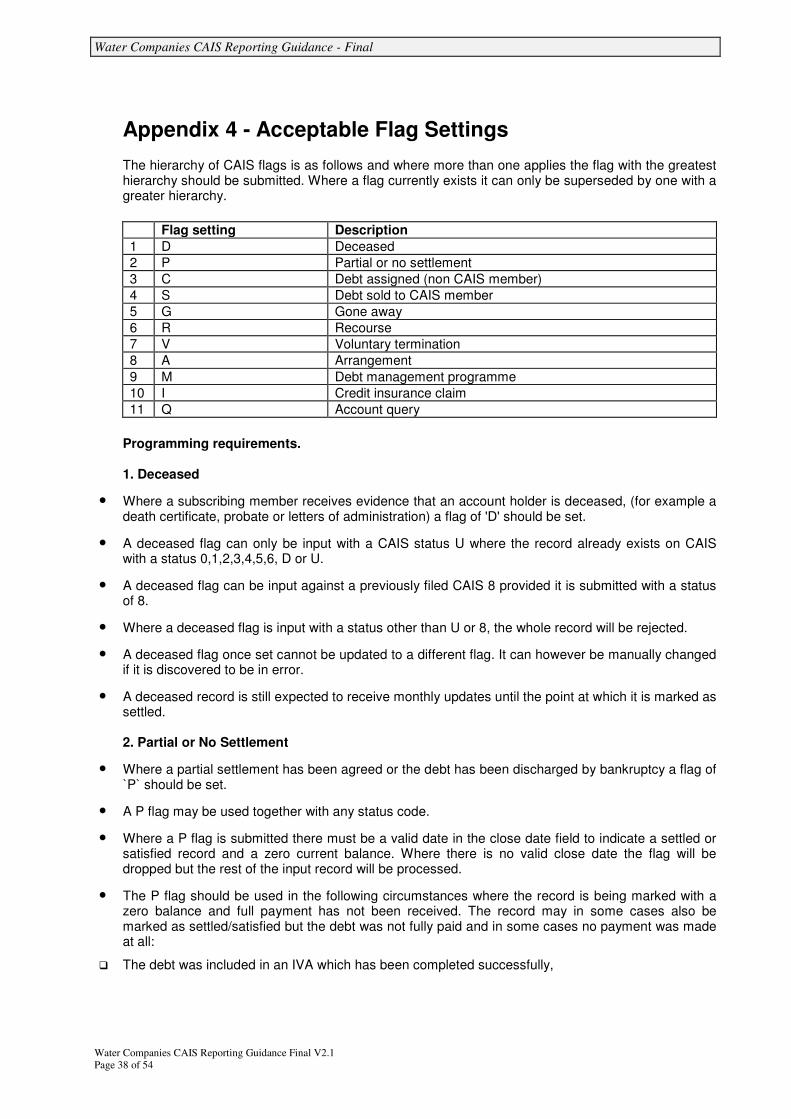

Appendix 4 - Acceptable Flag Settings The hierarchy of CAIS flags is as follows and where more than one applies the flag with the greatest hierarchy should be submitted. Where a flag currently exists it can only be superseded by one with a greater hierarchy.

Flag setting Description

1 D Deceased

2 P Partial or no settlement

3 C Debt assigned (non CAIS member)

4 S Debt sold to CAIS member

5 G Gone away

6 R Recourse

7 V Voluntary termination

8 A Arrangement

9 M Debt management programme

10 I Credit insurance claim

11 Q Account query

Programming requirements. 1. Deceased

• Where a subscribing member receives evidence that an account holder is deceased, (for example a death certificate, probate or letters of administration) a flag of 'D' should be set.

• A deceased flag can only be input with a CAIS status U where the record already exists on CAIS with a status 0,1,2,3,4,5,6, D or U.

• A deceased flag can be input against a previously filed CAIS 8 provided it is submitted with a status of 8.

• Where a deceased flag is input with a status other than U or 8, the whole record will be rejected.

• A deceased flag once set cannot be updated to a different flag. It can however be manually changed if it is discovered to be in error.

• A deceased record is still expected to receive monthly updates until the point at which it is marked as settled. 2. Partial or No Settlement

• Where a partial settlement has been agreed or the debt has been discharged by bankruptcy a flag of `P` should be set.

• A P flag may be used together with any status code.

• Where a P flag is submitted there must be a valid date in the close date field to indicate a settled or satisfied record and a zero current balance. Where there is no valid close date the flag will be dropped but the rest of the input record will be processed.

• The P flag should be used in the following circumstances where the record is being marked with a zero balance and full payment has not been received. The record may in some cases also be marked as settled/satisfied but the debt was not fully paid and in some cases no payment was made at all:

� The debt was included in an IVA which has been completed successfully,

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 39 of 54

� The debt was included in a bankruptcy which has since been discharged,

� A smaller amount has been agreed and accepted in full and final settlement, and the term has been conveyed to the customer

� An asset has been repossessed and the outstanding balance is not to be pursued.

• A record with the P flag is not expected to receive any further monthly updates. Further financial updates will therefore be rejected unless the flag is removed by manual amendment. 3. Debt Assigned

• The debt assigned flag should be used where the rights to a debt have been assigned to a new owner who is not a member of CAIS and therefore will not be registering the debt on CAIS in their own name. The record remains in the original lender's name, shown as settled or satisfied together with the debt assigned flag to indicate that the record is closed due to its sale.

• A debt assigned flag may be used together with any status code.

• Where the debt assigned flag is being used, the current balance must be zero.

• The close date field must contain a valid date of settlement or the original default date. Where there is no valid close date the flag will be dropped but the rest of the input record will be processed.

• A record assigned to a new owner is not expected to receive any further monthly updates. Further financial updates will therefore be rejected unless the flag is removed by manual amendment. 4. Debt Sold to CAIS Member

• The debt sold to CAIS member flag should be used where the rights to a debt have been assigned to a new owner that is already a CAIS member. In this circumstance the new owners should have already agreed to supply the record onto their own CAIS portfolio. In this situation, the original record will remain on CAIS indicated as sold to CAIS member, shown as settled or satisfied together with this flag to indicate the record is closed due to its sale. The new owners will continue to supply the performance of the record via their own portfolio.

• A Debt sold to CAIS member flag can be used together with any status code. However, the flag is not intended as an alternative to transfer of credit history across portfolios for sales of full data books. Please contact the CAIS team before using this flag for sales of full data.

• Where this flag is being used the current balance must be zero.

• The closed date field must contain a valid date of settlement or the original default date provided for default records. Where there is no valid closed date the flag will be dropped but the rest of the input record will be processed.

• A record assigned to a new owner is not expected to receive any further monthly updates. Further financial updates will therefore be rejected unless the flag is removed by manual amendment

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 40 of 54

5. Gone Away

• Where the address of the customer is no longer known and the account is falling into arrears, a `G` flag should be used together with the last known address.

• A gone-away flag does not necessarily indicate a defaulted account.

• A gone away flag can only be registered if the account is in arrears. The CAIS status code accompanying the flag must be 1,2,3,4,5,6, or 8.

• If the status is 0, D or U the gone-away flag will be dropped but the rest of the input record will be processed.

• A record input with a blank in the flag field which matches to a previously filed gone away flag, will remove all reference to the gone away flag from that record.

• A gone away record is still expected to receive monthly updates until the point at which it is marked as settled or is defaulted.

• If a gone away record is received with any other type of flag the record will be updated with the new flag. (It is assumed that the person is now located).

6. Recourse

• Where an account is invoked with a recourse agreement (for instance between a dealer and a lender or where guarantor takes over a mortgage), the record should be set at the status code applicable when the recourse action took place together with a flag of `R`.

• The date of recourse should be entered in the Close Date field and no further update is then necessary.

• A recourse flag can only be registered if the account is in arrears. The CAIS status must be 1,2,3,4,5,6, or 8.

• If the status is 0, D or U then the flag will be dropped but the rest of the input record will be processed.

• A recourse flag once set should not be updated to a different flag. It can however be manually changed.

• A recoursed record is not expected to receive any further monthly updates.

• A new CAIS account should be opened in the name of the guarantor which is linked to the original account by the joint account indicator in byte 20 of the account number field (see field 1 for customer records above for further details)

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 41 of 54

7. Voluntary Termination

There are three situations to be considered.

I. Where a Customer Credit Act Section 100 balance is outstanding and there is no arrangement a 'V' flag should be set along with a CAIS status of 8.

II. Where a Section 100 balance is outstanding and there is an arrangement, then a 'V' flag should be set and the CAIS status code appropriate to the repayment performance.

III. Where a Section 100 balance has been met, the 'V' flag should be set but the account should be closed with the appropriate status code and a balance of zero.

• A voluntary termination can only be set if the record is a Hire Purchase agreement (CAIS Account Type 01,20 and 29). If the voluntary termination flag is set on a record where the account type is not 01,20 and 29, the flag will be dropped but the rest of the input record will be processed.

• A voluntary termination flag can be set alongside any status code.

• Where a voluntary termination is registered at other than a status 8 or settled status 0, the account is deemed to be an arrangement within a voluntary termination. At this stage, two monthly payments will be registered, the current monthly payment (arrangement amount) and the previous monthly payment (how much was being paid before the voluntary termination was enforced). If the two monthly payment values are equal, the flag will be dropped but the rest of the input record will be processed.

8. Arrangement

An arrangement can only be set if the status is 0,1,2,3,4,5,6,D or U.

• Where a customer is granted an arrangement to pay a reduced amount, the arrears that accrue against the original contract should continue to be shown by the appropriate status code. An ‘A’ flag and the arranged monthly payment pertinent at that particular time should accompany this status code. Please also refer to the guidance note on the filing of default data.

• As a customer maintains the arrangement and in due course becomes a good payer once again, the status code can be reduced back to 0 and the flag removed.

• If the terms of the arrangement is placed on a more formal basis it is normal practice for a new agreement to be put in place and the performance should then be recorded against the revised terms. This may also apply is arrears are capitalised.

• If the arrangement is placed on a more formal basis it is normal practice to “re-age” the account when the arrangement has been maintained satisfactorily. In such cases the status code will reflect the performance of the arrangement. Such cases will continue to have an arrangement flag set even if the status code is 0 but will not display an end date for the arrangement thus indicating that it is still operating.

• Conversely, if the customer strays outside of the arrangement terms, this should be regarded as a serious breach of the agreement and the debt should continue to age against the original contract, upon removal of the flag.

• For eligible accounts, the revised monthly payment is submitted in the usual monthly payment field (see field 5 above). Two monthly payments will be shown on the CAIS record during a credit search, the current monthly payment (arrangement amount) and the previous monthly payment (how much was being paid before the arrangement was enforced).

� Only when they are equal i.e. the customer returns to repaying the original contracted amount, will the arrangement be marked with an end date. This is achieved as follows:

Water Companies CAIS Reporting Guidance - Final

Water Companies CAIS Reporting Guidance Final V2.1

Page 42 of 54

� Where the two monthly payment values are equal, the flag will be dropped but the rest of the record carried forward.

� For account types that do not display the revised monthly payment the arrangement is closed off by removal of the flag at which time an end date will be appended.

• Where the same record with a blank flag is subsequently submitted an end date of the arrangement will automatically be added to the record.

9. Debt Management Programme

• The flag of 'M' should be used where the customer has entered into a debt management programme such as those run by the Citizens' Advice Bureau.

• The status should reflect the arrears of the account at the time the programme was entered into (similar to arrangement above).

• A debt management programme can only be set on a record where the status is 0,1,2,3,4,5,6, D or U.

• Two monthly payments are registered on CAIS, the current monthly payment (managed amount) and the previous monthly payment (how much was being paid before the programme was enforced).

• Where the two monthly payment values are equal, the flag will be dropped but the rest of the record carried forward.

• Where the same record with a blank flag is subsequently submitted, an end date of the programme will automatically be added to the record.

10. Credit Insurance Claim

• This flag is to be set at the point in time when the customer notifies the lender of the claim. A flag setting of 'I' should be used along with a status setting of U for the life of the claim.

• When used, the words 'CPI CLAIM' will appear below the status summary lines.