Warm up for 10.8.13 Please answer the following questions in the same section of your notebook as...

14

Warm up for 10.8.13 • Please answer the following questions in the same section of your notebook as your CNN student logs please. I will check your logs for CNN and warm ups on Friday, 10.11 • 1. What is a contract? • 2. What is a warranty? • 3. How is it legal for a minor, someone under the age of 18, to sign a contract? • 4. What are the three parts of a contract? • 5. Make up an example of a contract and identify the three parts of a contract.

-

Upload

gladys-flynn -

Category

Documents

-

view

213 -

download

1

Transcript of Warm up for 10.8.13 Please answer the following questions in the same section of your notebook as...

Warm up for 10.8.13

• Please answer the following questions in the same section of your notebook as your CNN student logs please. I will check your logs for CNN and warm ups on Friday, 10.11

• 1. What is a contract?• 2. What is a warranty?• 3. How is it legal for a minor, someone under the age of 18, to

sign a contract?• 4. What are the three parts of a contract? • 5. Make up an example of a contract and identify the three

parts of a contract.

Credit & Banking

Hook: Who has a credit score? A person? A gov’t? What is it?

Excellent, Good, Poor

• http://www.freescore.com/good-bad-credit-score-range.aspx

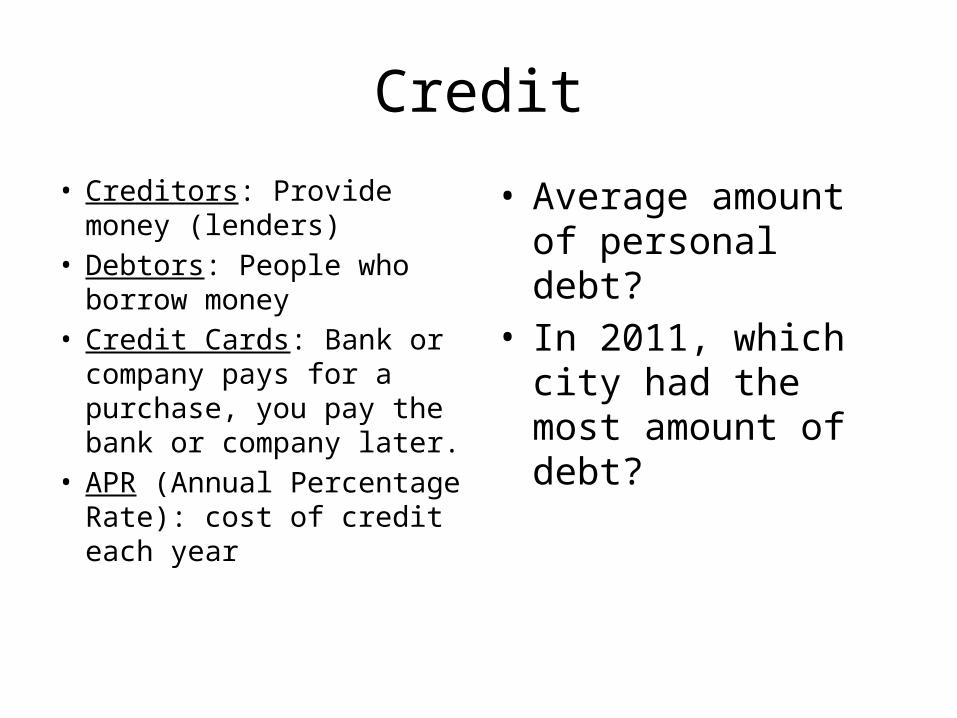

Credit

• Creditors: Provide money (lenders)

• Debtors: People who borrow money

• Credit Cards: Bank or company pays for a purchase, you pay the bank or company later.

• APR (Annual Percentage Rate): cost of credit each year

• Average amount of personal debt?

• In 2011, which city had the most amount of debt?

Banking

• By law, banks must provide customers with a statement about their accounts.

• Electronic Fund Transfer Act: Banks must investigate an error within 10 business days of a complaint.– Electronic Funds Transfer

Act

ATM (Debit) Cards

• Using these cards is the same process of writing a check.– You must have the $ for

a purchase in your account.

Stop Payment

• If a debit card or check book is stolen the bank can cancel the account.– Fees may apply.

• Notify the bank in 2 days:

• Notify the bank in 60 days:

• Afterwards:

Lost Credit Cards

• Only responsible for $50 after reporting a lost or stolen card

• Fair Credit Billing Act: If a billing error is reported within 60 days, the creditor must respond within 90 days.

• Fair Credit Billing Act

Beware!

• Balloon Payments: Early payments are much smaller than later payments

• Acceleration Clause: Creditors can require future payments are made immediately

• Bill Consolidation: Combining debt into one payment

• Truth in Lending Act: Must receive basic information about the credit

Equal Credit Opportunity Act

• Consumers cannot be refused credit based on race, gender, marital status, religion or source of income.

• Equal Credit Opportunity Act

• Equal Credit Opportunity Act

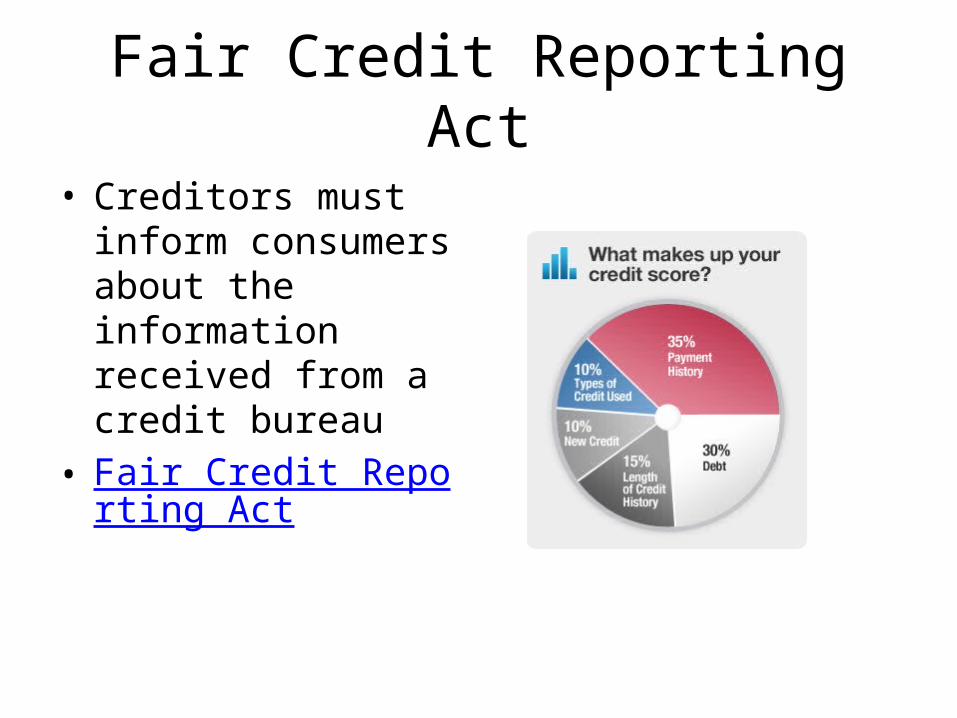

Fair Credit Reporting Act

• Creditors must inform consumers about the information received from a credit bureau

• Fair Credit Reporting Act

Oh No! I can’t pay!• Default: A consumer

who is unable to pay a debt

• Fair Debt Collection Practices Act: Protects consumers from abusive and unfair debt collection– Fair Debt Collection Act– Fair Debt Collection Act

Oh No! I still can’t pay!

• Bankruptcy: Federal courts take control of a debtors assets– May sell items– Remain in credit report

for 10 years

• Default Judgment: A creditor may sue a debtor

Still not paying!!

• Garnishment: employees are forced to give their salary directly to creditors– Wage Garnishment Act– Wage Garnishment Act

• Repossession: Creditors will take the collateral or possession to regain loan.– Rep Video

![Hidden Gems in CF10 - CArehart.org › presentations › Hidden_Gems_in_CF10.pdf• New “access logs” enabled by default (in addition to your web server logs) • in [cf10]\cfusion\runtime\logs,](https://static.fdocuments.us/doc/165x107/5f0d0fd57e708231d4387d46/hidden-gems-in-cf10-a-presentations-a-hiddengemsincf10pdf-a-new-aoeaccess.jpg)