W. BentzA&MIS 5251 Agenda Today Return quiz and other assignments Go over problem 11-20 Go over...

40

W. Bentz A&MIS 525 1 Agenda Today Agenda Today • Return quiz and other assignments • Go over problem 11-20 • Go over chapter 13 ideas

-

Upload

octavia-evans -

Category

Documents

-

view

214 -

download

0

Transcript of W. BentzA&MIS 5251 Agenda Today Return quiz and other assignments Go over problem 11-20 Go over...

W. Bentz A&MIS 525 1

Agenda TodayAgenda Today

• Return quiz and other assignments

• Go over problem 11-20

• Go over chapter 13 ideas

W. Bentz A&MIS 525 2

The Organization as a System of Interrelated Elements

Remember the Systems View?Remember the Systems View?

W. Bentz A&MIS 525 3

StakeholdersStakeholders

The individuals, groups of individuals, and institutions that define an organization’s success or affect the organization’s ability to achieve its objectives. Stakeholders include customers, employees, suppliers, owners and the “community.”

4 A&MIS 525 W. Bentz

Strategy ConsiderationsStrategy Considerations

1. Identifying the alternative means by which the organization might compete for customers. Where are we going to compete in the golden triangle of cost, quality, and functionality; and in what markets.

2. Evaluating each of these alternative means relative to the capabilities and expectations of the stakeholders.

W. Bentz A&MIS 525 5

Role of StrategyRole of Strategy

The role of strategic planning is to define the relationship that the organization will develop with each of its stakeholder groups so that all the components fit together.

6 A&MIS 525 W. Bentz

Planning, Decision Making,Planning, Decision Making, and Control and Control

Mission identifies organization’s stakeholders and broad objectives

Objectives specify specific performance goals sought over the next 5 to 10 years

Strategies specify the organization’s form, resource allocations, and broad business decisions used to seek

objectives

Observations and measurement of short-term performance determine whether the organization is on

track to achieve its long-term objectives

Planningand

DecisionMaking

Control

11-23 1996 Prentice Hall Business Publishing Management Accounting, 2nd ed., Atkinson, Banker, Kaplan, and Young

W. Bentz A&MIS 525 7

ProcessProcess

Any integrated group of activities designed to achieve a specific purpose.

W. Bentz A&MIS 525 8

Performance measurementPerformance measurement

• Performance measurement focuses on process results and how those results contribute to the organization’s secondary objectives

9 A&MIS 525 W. Bentz

Strategic ObjectivesStrategic Objectives

Primary Objectives - what the owners expect from their participation in the organization

Secondary Objectives - what the organization expects to give to and receive from each stakeholder group other than its owners

Do you agree with this statement from your text?

10 A&MIS 525 W. Bentz

Secondary Objectives Reflect:Secondary Objectives Reflect:

• What the organization expects from each of its stakeholder groups to help it achieve its primary objectives

• What the organization must provide to each stakeholder group to secure from that group what the organization needs to achieve its primary objectives.

W. Bentz A&MIS 525 11

The Nature of Control

GOAL

W. Bentz A&MIS 525 12

In Control???In Control???

• A system is in control if it is on a path that will lead it to achieving its objectives. Otherwise, the system is out of control.

• The key concept here is achieving goals and objectives, not necessarily conformance to plan.

• Another key concept is that controls are not sufficient to achieve control.

13 A&MIS 525 W. Bentz

Organization Level and Organization Level and Measurement FocusMeasurement Focus

Lower production workers, sales staff, customer relations staff

Performance Measurement Type

Organization Level Major Responsibility

Monitor and improve the operations of

existing systems to meet short-term

goals in cost containment, quality, and

response time

Measures of short-term operating

performance that include both output and outcome measures such as yield, productivity, and on-time delivery that

reflect the operations of a single unit in the organization.

11-29 1996 Prentice Hall Business Publishing Management Accounting, 2nd ed., Atkinson, Banker, Kaplan, and Young

14 A&MIS 525 W. Bentz

Organization Level and Organization Level and Measurement FocusMeasurement Focus

Middle supervisors and managers

Performance Measurement Type

Organization Level Major Responsibility

Coordinate existing systems and develop new ones to achieve intermediate-term performance on critical success factors

A mix of operating measures that include both output and outcome measures and reflect how well units are working together to meet stakeholder requirements (system response time, system quality, and rate of new product introduction) and financial measures (cost per unit, productivity, or profit margin) that compare performance to competitors to evaluate the efficacy of the systems the organization has in place

11-30 1996 Prentice Hall Business Publishing Management Accounting, 2nd ed., Atkinson, Banker, Kaplan, and Young

15 A&MIS 525 W. Bentz

Organization Level and Organization Level and Measurement FocusMeasurement Focus

Upper vice presidents, presidents

Performance Measurement Type

Organization Level Major Responsibility

Identify opportunities to develop new markets

Aggregated measures of outcome performance, such as return on investment, number of safety incidents, rate of new product introduction that reflects senior level employees’ responsibility for meeting the organization’s commitment to its stakeholders

11-31 1996 Prentice Hall Business Publishing Management Accounting, 2nd ed., Atkinson, Banker, Kaplan, and Young

16 A&MIS 525 W. Bentz

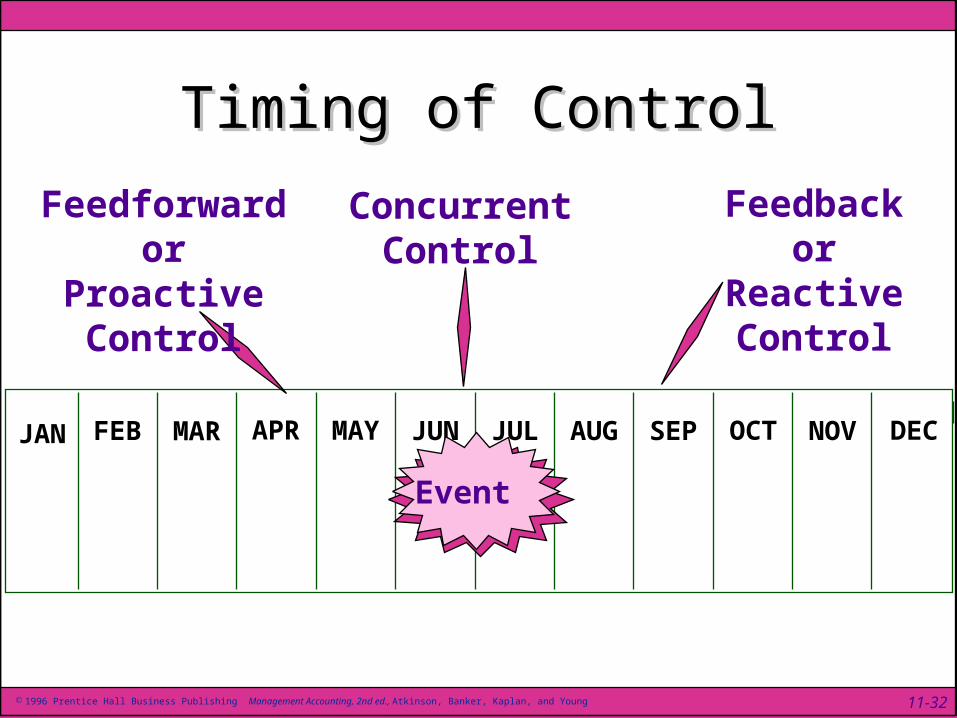

Timing of ControlTiming of Control

APRJAN FEB MAR MAY JUN JUL SEP OCT NOV DECAUG

Event

Feedforward or Proactive Control

Concurrent Control

Feedback or Reactive Control

11-32 1996 Prentice Hall Business Publishing Management Accounting, 2nd ed., Atkinson, Banker, Kaplan, and Young

17 A&MIS 525 W. Bentz

Types of Control SystemsTypes of Control Systems

Task Control - setting rules and ensuring that they are followed

Results Control - specifying what is important in the organization and letting workers decide how best to do the job

18 A&MIS 525 W. Bentz

Element Task Control Results Control

Organization environment Stable ChangingControl question Were rules followed? Were objectives achieved?Locus of responsibility Top down Bottom upEmployee role Follow rules Achieve stated objectivesRisk level High Low

Task and Results Control SummaryTask and Results Control Summary

11-26 1996 Prentice Hall Business Publishing Management Accounting, 2nd ed., Atkinson, Banker, Kaplan, and Young

19 A&MIS 525 W. Bentz

Problems with Results ControlProblems with Results Control

Has the causal link between secondary results and primary results been identified?

Can organizations measure the right thing? (Measure is a strong standard.)

Is it possible to associate a given result with a given person or decision?

Results are influenced by the environment, which is uncontrollable.

20 A&MIS 525 W. Bentz

Managing Causes, Not ResultsManaging Causes, Not Results

Managing the performance of the primary objective requires understanding the causes of that performance and managing those causes effectively.

Managers must manage the secondary performance measures which are drivers of performance on primary objectives.

W. Bentz A&MIS 525 21

Performance MeasuresPerformance Measures

• Entity measures– Stock returns (dividends + appreciation)– Return on total investment (ROI)– Return on equity (ROE)– Residual income (including EVA)– Income from operations– Income from continuing activities– Net income

W. Bentz A&MIS 525 22

Performance MeasuresPerformance Measures

• Segment measures

–Contribution margin

–Short-run performance margin

–Segment margin

–Variances from plan

W. Bentz A&MIS 525 23

Performance measuresPerformance measures

• Short-run performance margin Definition: contribution margin less separable, discretionary fixed costs (a.k.a. performance margin).

• Segment marginDefinition: Performance margin less separable, committed fixed costs

W. Bentz A&MIS 525 24

Control versus ResponsibilityControl versus Responsibility

• Spheres of responsibility are primary, control less achievable.

• The opportunity to influence is a consideration in constructing performance reports.

W. Bentz A&MIS 525 25

Accounting MethodsAccounting Methods

Accounting performance measures are frequently modified to reflect the level of control, or lack of control, that individuals may have in specific situations.

•Modify a budget to reflect the actual activity volumes experienced (flexible budgeting)

•Adapt a plan to reflect the operating environment actually experienced.

W. Bentz A&MIS 525 26

Accounting MethodsAccounting Methods

• Adopt a relative performance standard against which to evaluate individuals. For example, a purchasing agent’s ability to get good prices can be measured against a price index or some simple trading rule that constitutes an external, relative standard.

• Limit reporting to key success factors

W. Bentz A&MIS 525 27

Accounting MethodsAccounting Methods

• Emphasize more controllable factors, and de-emphasize less controllable factors as in segment reports

• Isolate one factor at a time in variance systems to focus on areas of responsibility related to single performance factors

• Use of reporting entities consistent with responsibility levels

W. Bentz A&MIS 525 28

An overriding issueAn overriding issue

• Strategic alignment of incentives– Individual vis-a-vis organization– Function vis-a-vis function– Entity vis-a-vis entity

• Incentives do work!

W. Bentz A&MIS 525 29

Accounting entitiesAccounting entities

• cost center

• revenue center

• profit center

• investment center

• administered center

• support center

• division (business unit)

W. Bentz A&MIS 525 30

Balanced ScorecardBalanced Scorecard

A set of performance targets and an approach to performance measurement that stresses meeting all the organization’s objectives relating to both its primary and secondary objectives - hence the balance. Obviously, this leaves open the question of trade-offs.

31 A&MIS 525 W. Bentz

Balanced Business Scorecard

Business Processes

What business processes are the

value drivers?

Organization Learning

Are we able to sustain innovation, change and improvement

Customer Perspective

How do we look to our customers?

Financial Perspective

How do we look to our shareholders?

Vision & Strategy

11-41 1996 Prentice Hall Business Publishing Management Accounting, 2nd ed., Atkinson, Banker, Kaplan, and Young

W. Bentz A&MIS 525 32

Implementing a Balanced ScorecardImplementing a Balanced Scorecard

Management must define the organization’s primary objectives

1. 1.

W. Bentz A&MIS 525 33

Implementing a Balanced ScorecardImplementing a Balanced Scorecard

The organization must understand how stakeholders and processes contribute to its primary objectives

2. 2.

W. Bentz A&MIS 525 34

Implementing a Balanced ScorecardImplementing a Balanced Scorecard

The organization must develop a set of secondary objectives that are the drivers of performance on primary objectives

3. 3.

W. Bentz A&MIS 525 35

Implementing a Balanced ScorecardImplementing a Balanced Scorecard

The organization must develop a set of measures to monitor performance on both primary and secondary objectives

4. 4.

W. Bentz A&MIS 525 36

Implementing a Balanced ScorecardImplementing a Balanced Scorecard

The organization must develop a set of processes, along with their attendant implicit and explicit contracts with stakeholders, to achieve those primary objectives

5. 5.

W. Bentz A&MIS 525 37

Implementing a Balanced ScorecardImplementing a Balanced Scorecard

The organization must make specific and, therefore, public statements about its beliefs concerning how processes create results

6. 6.

38 A&MIS 525 W. Bentz

A Balanced Scorecard Provides:A Balanced Scorecard Provides:

A method for the organization to systematically consider what it should do to develop an internally consistent and comprehensive system of planning and control

and . . .

39 A&MIS 525 W. Bentz

A Balanced Scorecard Provides:A Balanced Scorecard Provides:

a basis for understanding the difference between successful and unsuccessful organizations

W. Bentz A&MIS 525 40