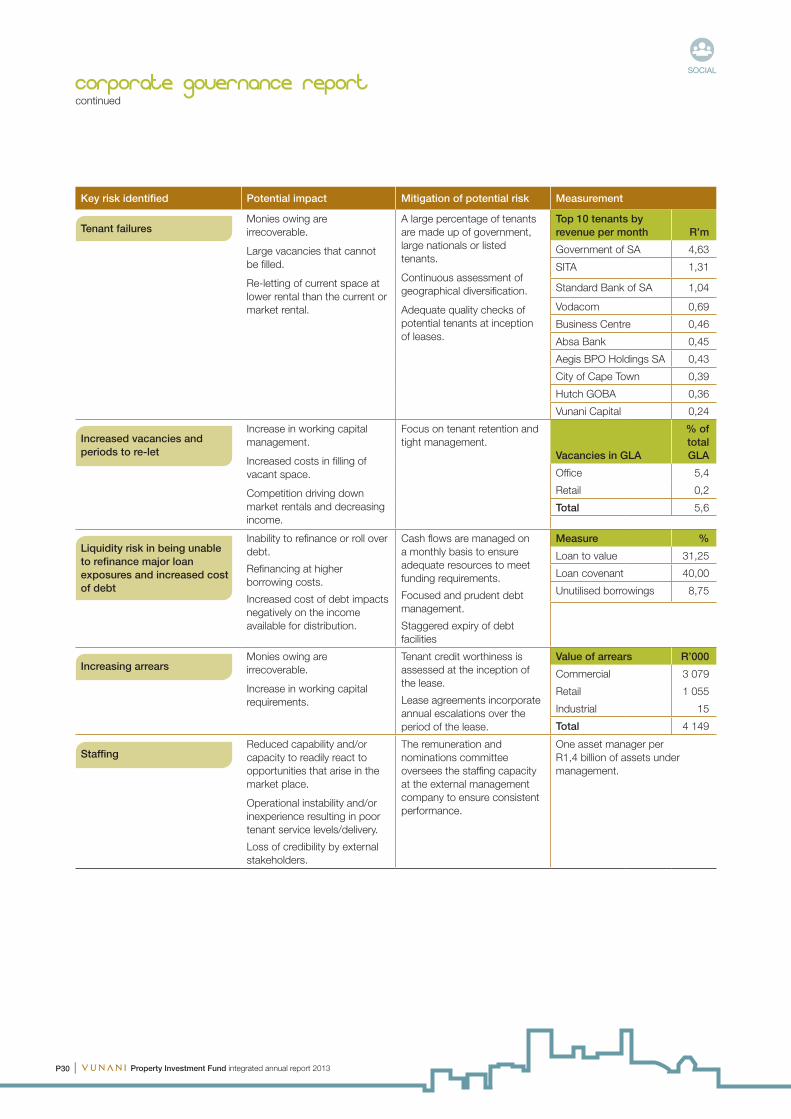

Vunani Property Investment Fund - JSE€¦ · P2 I Property Investment Fund integrated annual...

104

INTEGRATED ANNUAL REPORT 2013 for the year ended 30 June

Transcript of Vunani Property Investment Fund - JSE€¦ · P2 I Property Investment Fund integrated annual...

INTEGRATED ANNUAL REPORT 2013for the year ended 30 June

Highlights 1

Our strategy 1

Who we are 2

Property portfolio 5

Directorate 14

Chairman and CEOs report 16

Corporate governance report 22

Report to stakeholders 32

Annual financial statements 35

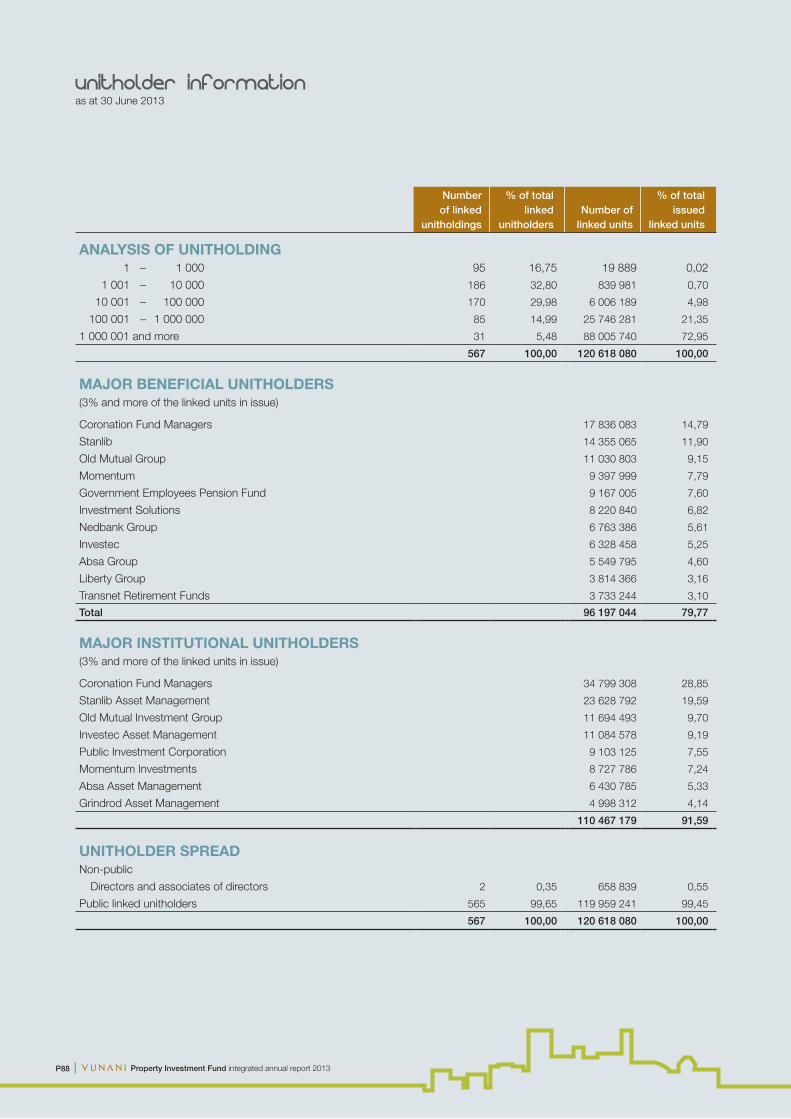

Unitholder information 87

Company information ibc

contents

FOR MORE INFORMATIONYou’ll find links throughout this report, to guide you to further reading or relevant information.

Reporting icons

VPIF takes pleasure in presenting its second integrated annual

report to stakeholders for the year ended 30 June 2013 in line

with the requirements of the King Code and report on corporate

governance for South Africa (King III). The integrated annual report

has been prepared to assist stakeholders in assessing the group’s

ability to create and sustain value.

This integrated annual report was compiled in terms of the discussion

paper as published by the Integrated Reporting Committee of South

Africa on 25 January 2011, which recommends that companies

should not only report on their financial performance, but also on

their sustainability by disclosing social, environmental and economic

influences, both positive and negative.

The scope and boundaries of the information contained in the

report describe our operations and property portfolios. The report is

structured to indicate the following:

aPPROACH TO INTEGRATED REPORTING

FUNDERS OF THE GROUP

(unitholders and debt funders)

OPERATING ENVIRONMENT

SERVICE PROVIDERS

TENANTS

INTEGRATED REPORTINGCorporate responsibility information is integrated throughout our integrated annual report and accounts and is highlighted with the logos below. This reflects how managing our environmental, economic and social impacts is central to how we do business. It also provides readers with insights into the critical linkages in our thinking and activity, and greater clarity on the relationship between our financial and non‑financial key performance indicators.

WHY GO ONLINE?Our corporate website contains detailed information about the company and is frequently updated as additional details become available. You can sign up for email alerts of our latest news and our current share price is displayed on the home page.

ENVIRONMENT SOCIAL

Our corporate websitewww.vpif.co.za

See page/note reference

For more informationsee website

HIGHLIGHTS

our strategy

77,25 cents DISTRIBUTION PER LIKED UNIT

(2012: 64,51 cents) (19,7% growth)

LINKED UNIT PRICE OF 1 005 cents PER LINKED UNIT (2012: 825 cents) (21,8% growth)

31,2% COMPOUND GROWTH

R216,9 million INVESTMENT PROPERTY

INCOME (2012: R165,9 million)

R154,9 million NET PROPERTY INCOME

(2012: R114,0 million)

R1,568 billion PORTFOLIO VALUE

(2012: R1,426 billion) Refer to property portfolio on pages 5 to 13

79,7% BLUE CHIP TENANTS (2012: 80,0%)

Refer to page 3.

5,6% VACANCY (2012: 5,8%)

Refer to page 6.

73% TENANT RETENTION (2012: 89%)

Refer to page 19.

4,75 YEARS WEIGHTED AVERAGE LEASE

EXPIRY (2012: 4,71 years)

145 594m2 OF GROSS LETTABLE

AREA (2012: 135 327m2)

Refer to pages 58 and 59.

GEARING OF 31,25% LOAN TO VALUE

(2012: 31,4%)

Refer to page 82.

R103,05/m2 WEIGHTED AVERAGE

RENTAL PER SQUARE METRE (2012: R102,93/m2)

Refer to pages 57 and 58.

Property Investment Fund integrated annual report 2013 I P1

VPIF’s strategy is aimed at building value for all stakeholders over the short to long term. The following success factors form the basis of our strategy:

n We conduct our business with integrity.

n We deliver on results to unitholders.

n Our tenants and clients are our most valuable assets.

n We are responsible corporate citizens and promote social and environmental sustainability.

n We aim to be a transparent sustainable investment.

Read more on page 22.

OPTIMISED INVESTMENT

RETURN

Increased shareholder

base and liquidity

Transformation

Quality portfolio growth

Decreased funding costs

Partner of choice for

tenants and investors

Sustainable and beneficial partnerships

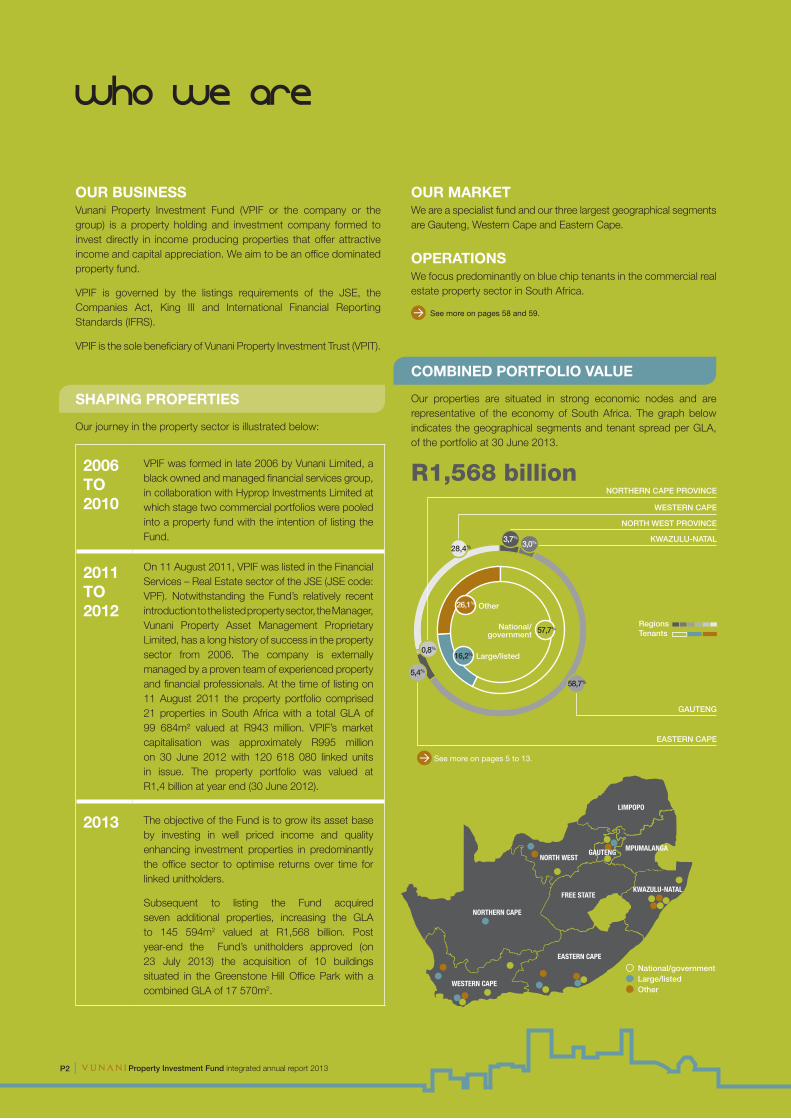

Who we are

OUR BUSINESSVunani Property Investment Fund (VPIF or the company or the group) is a property holding and investment company formed to invest directly in income producing properties that offer attractive income and capital appreciation. We aim to be an office dominated property fund.

VPIF is governed by the listings requirements of the JSE, the Companies Act, King III and International Financial Reporting Standards (IFRS).

VPIF is the sole beneficiary of Vunani Property Investment Trust (VPIT).

SHAPING PROPERTIES

Our journey in the property sector is illustrated below:

OUR MARKETWe are a specialist fund and our three largest geographical segments are Gauteng, Western Cape and Eastern Cape.

OPERATIONSWe focus predominantly on blue chip tenants in the commercial real estate property sector in South Africa.

See more on pages 58 and 59.

2006 TO 2010

VPIF was formed in late 2006 by Vunani Limited, a black owned and managed financial services group, in collaboration with Hyprop Investments Limited at which stage two commercial portfolios were pooled into a property fund with the intention of listing the Fund.

2011 TO 2012

On 11 August 2011, VPIF was listed in the Financial Services – Real Estate sector of the JSE (JSE code: VPF). Notwithstanding the Fund’s relatively recent introduction to the listed property sector, the Manager, Vunani Property Asset Management Proprietary Limited, has a long history of success in the property sector from 2006. The company is externally managed by a proven team of experienced property and financial professionals. At the time of listing on 11 August 2011 the property portfolio comprised 21 properties in South Africa with a total GLA of 99 684m² valued at R943 million. VPIF’s market capitalisation was approximately R995 million on 30 June 2012 with 120 618 080 linked units in issue. The property portfolio was valued at R1,4 billion at year end (30 June 2012).

2013 The objective of the Fund is to grow its asset base by investing in well priced income and quality enhancing investment properties in predominantly the office sector to optimise returns over time for linked unitholders.

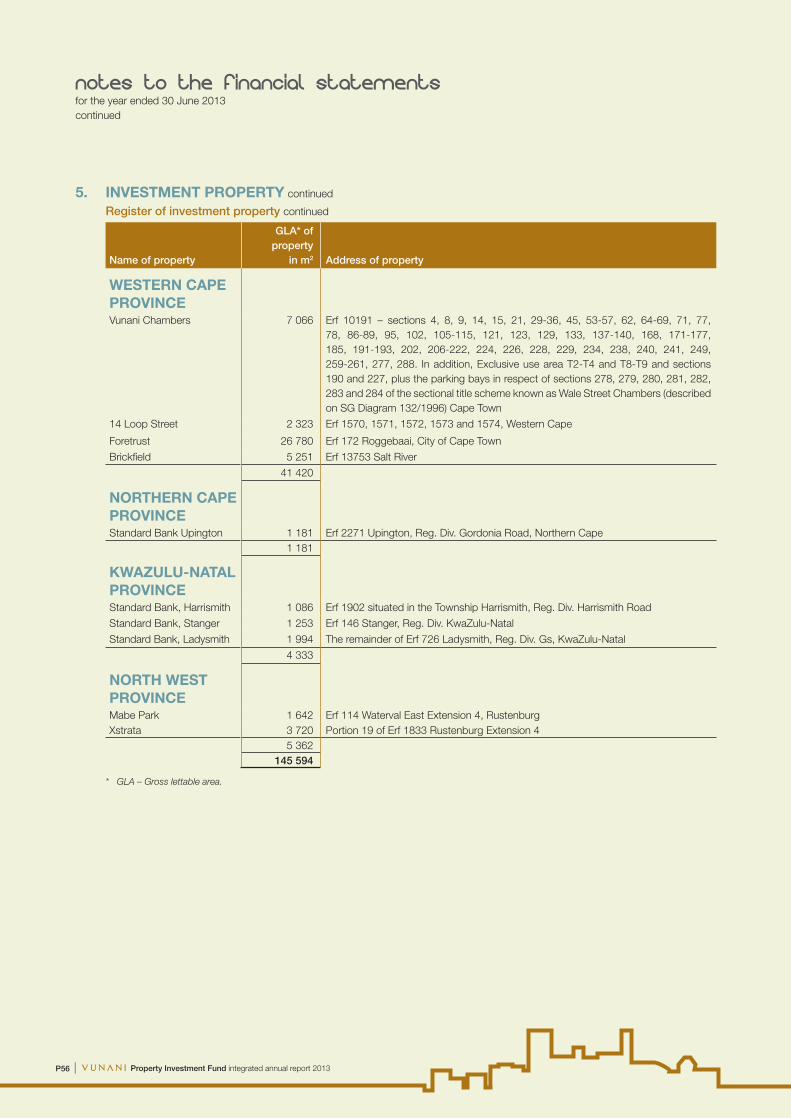

Subsequent to listing the Fund acquired seven additional properties, increasing the GLA to 145 594m2 valued at R1,568 billion. Post year-end the Fund’s unitholders approved (on 23 July 2013) the acquisition of 10 buildings situated in the Greenstone Hill Office Park with a combined GLA of 17 570m2.

I Property Investment Fund integrated annual report 2013P2

COMBINED PORTFOLIO VALUE

Our properties are situated in strong economic nodes and are representative of the economy of South Africa. The graph below indicates the geographical segments and tenant spread per GLA, of the portfolio at 30 June 2013.

National/government Large/listed Other

RegionsTenants

R1,568 billion

GAUTENG

EASTERN CAPE

KWAZULU-NATAL

NORTH WEST PROVINCE

WESTERN CAPE

NORTHERN CAPE PROVINCE

28,4%3,7%

3,0%

58,7%

5,4%

0,8%

See more on pages 5 to 13.

26,1%

16,2%

57,7%National/ government

Large/listed

Other

Property Investment Fund integrated annual report 2013 I P3

Office (91%)

Retail (5%)

Industrial (4%)

SECTORAL SPREAD

Office (94%)

Retail (5%)

Industrial (1%)

BY GLA BY REVENUE

Government/national (91%)

Listed/large entities (5%)

Other (4%)

Blue chip (74%)

TENANT SPREAD

Government/national (91%)

Listed/large entities (5%)

Other (4%)

Blue chip (80%)

Eastern Cape (5%)

Gauteng (59%)

KwaZulu-Natal (3%)

North West province (4%)

Northern province (1%)

Western Cape (28%)

Eastern Cape (6%)

Gauteng (57%)

KwaZulu-Natal (2%)

North West province (4%)

Northern province (1%)

Western Cape (30%)

SECTORAL SPREAD

BY GLA BY REVENUE

BY GLA BY REVENUE

n % of GLA Cumulative

GROUP LEASE EXPIRY PROFILE% of GLA

100

80

60

40

20

0Vacant 2014 2015 2016 >2016

I Property Investment Fund integrated annual report 2013P4

Who we arecontinued

n % of GLA Cumulative

OFFICE LEASE EXPIRY PROFILE% of GLA

100

80

60

40

20

0Vacant 2014 2015 2016 >2016

n % of GLA Cumulative

RETAIL LEASE EXPIRY PROFILE% of GLA

100

80

60

40

20

0Vacant 2014 2015 2016 >2016

n % of GLA Cumulative

INDUSTRIAL LEASE EXPIRY PROFILE% of GLA

100

80

60

40

20

0Vacant 2014 2015 2016 >2016

WEIGHTED AVERAGE RENTAL PER m2 PER SECTOR R/m2

120

100

80

60

40

20

0Industrial Retail Commercial Total

INDIVIDUAL PROPERTIES VACANCY PROFILEm2

Foretrust Building

Investment Place

Vunani Chambers

Standard Bank – Randburg

Vunani Office Park

Rynlal Building

Parthenon Park

Murrayfield Forum

Benstra

0 500 1 000 1 500 2 000 2 500

Property Investment Fund integrated annual report 2013 I P5

property portfolio

A GRADE

BELVEDERE PLACE

LOCATIONSunninghillBlue chip tenants

TYPE

OfficeSIZE

10 874m2

GROSS RENT

R86/m2

OCCUPANCY

100%NUMBER OF TENANTS

SixPROPERTY VALUE

R135,0mKEY HIGHLIGHTTenanted by blue chip tenants, the prominent park remains fully occupied by national tenants, many of whom have been there for some time. Sunninghill as an area seems to be coming into its own after some years of flat growth.

A GRADE

ACS HOUSE

LOCATIONRivoniaBlue chip tenants

TYPE

OfficeSIZE

1 743m2

GROSS RENT

R113/m2

OCCUPANCY

100%NUMBER OF TENANTS

TwoPROPERTY VALUE

R22,0mKEY HIGHLIGHTLocated just off Rivonia Boulevard close to the highway gives the building excellent access. The beautiful gardens and upmarket offices have retained the same tenants for many years.

A+ GRADE

STANDARD BANK PRIVATE BANK

LOCATIONHyde ParkSingle national tenant

TYPE

OfficeSIZE

2 038m2

GROSS RENT

R169/m2

OCCUPANCY

100%NUMBER OF TENANTS

OnePROPERTY VALUE

R42,8mKEY HIGHLIGHTFinished to a premium grade standard, the excellent location and profile of the building ensures a high demand for the space.

I Property Investment Fund integrated annual report 2013P6

property portfoliocontinued

A GRADE

BUSINESS CENTRE BUILDING

LOCATIONRivonia SandtonSingle tenanted

TYPE

OfficeSIZE

4 886m2

GROSS RENT

R94/m2

OCCUPANCY

100%NUMBER OF TENANTS

OnePROPERTY VALUE

R77,5mKEY HIGHLIGHTLocated on Rivonia Boulevard close to the highway gives the building excellent access.

A GRADE

FORETRUST BUILDING

LOCATIONCape TownNational tenants

TYPE

OfficeSIZE

26 780m2

GROSS RENT

R127/m2

OCCUPANCY

91%NUMBER OF TENANTS

ThreePROPERTY VALUE

R288,5mKEY HIGHLIGHTPWD and Nedbank occupy the building. Acquired in 2012, the 9% vacancy was not paid for. The surrounding foreshore of Cape Town is undergoing major upgrades. The property is the next target for our ‘greening’ programme.

A GRADE

LOCATIONSandtonNational tenants

TYPE

OfficeSIZE

8 625m2

GROSS RENT

R126/m2

OCCUPANCY

100%NUMBER OF TENANTS

SevenPROPERTY VALUE

R125,0mKEY HIGHLIGHTA grade offices, recently refurbished and predominantly occupied by national tenants on long leases.

VUNANI OFFICE PARK

ENVIRONMENT

Property Investment Fund integrated annual report 2013 I P7

A GRADE

LOCATIONCape Town CBD National tenants

TYPE

OfficeSIZE

7 066m2

GROSS RENT

R93/m2

OCCUPANCY

91%NUMBER OF TENANTS

TwentyPROPERTY VALUE

R55,0mKEY HIGHLIGHTRecently refurbished, the building has quality tenants, most of whom have been in the building for many years.

VUNANI CHAMBERS

A GRADE

INVESTMENT PLACE

LOCATIONSandtonBlue chip tenants

TYPE

OfficeSIZE

6 253m2

GROSS RENT

R131/m2

OCCUPANCY

50%NUMBER OF TENANTS

ThreePROPERTY VALUE

R92,8mKEY HIGHLIGHTInvestment Place is well located on William Nicol Highway in Hyde Park. All foyers are currently being refurbished to a high standard and negotiations are in place to retenant the vacancy.

A GRADE

LION ROARS

LOCATIONPort ElizabethNational tenants

TYPE

OfficeSIZE

4 117m2

GROSS RENT

R140/m2

OCCUPANCY

100%NUMBER OF TENANTS

FivePROPERTY VALUE

R55,0mKEY HIGHLIGHTThe prominent, attractive office park is located in the main decentralised node in PE and all tenants are national or listed.

I Property Investment Fund integrated annual report 2013P8

property portfoliocontinued

A GRADE

STANDARD BANK HARRISMITH

LOCATIONHarrismith (KZN) National tenant

TYPE

OfficeSIZE

1 086m2

GROSS RENT

R59/m2

OCCUPANCY

100%NUMBER OF TENANTS

OnePROPERTY VALUE

R7,0mKEY HIGHLIGHTThis attractive, prominent property is located on the busy main town square and the bank has repeatedly renewed its lease.

A GRADE

BUILDING 9, GREENSTONE OFFICE PARK

LOCATIONGreenstone HillNational tenants

TYPE

OfficeSIZE

1 827m2

GROSS RENT

R98/m2

OCCUPANCY

100%NUMBER OF TENANTS

ThreePROPERTY VALUE

R23,0mKEY HIGHLIGHTGreenstone Office Park was completed in 2012 and comprises 15 buildings in a landscaped setting. It has excellent access and has attracted listed and national tenants with little or no vacancies. Building 9 has two national tenants on long leases.

A GRADE

MABE PARK

LOCATIONRustenburgGovernment tenants

TYPE

OfficeSIZE

1 642m2

GROSS RENT

R162/m2

OCCUPANCY

100%NUMBER OF TENANTS

TwoPROPERTY VALUE

R26,0mKEY HIGHLIGHTLocated in the only A grade office park in Rustenburg, the two buildings each house a government department.

Property Investment Fund integrated annual report 2013 I P9

A GRADE

LINGER LONGER

LOCATIONSandtonSingle tenanted

TYPE

RetailSIZE

597m2

GROSS RENT

R152/m2

OCCUPANCY

100%NUMBER OF TENANTS

OnePROPERTY VALUE

R5,0mKEY HIGHLIGHTThis site has been consolidated with the adjacent Vodacom site to give the Fund a development opportunity of 35 000m2 in a strongly growing node, two blocks from Gautrain.

A GRADE

STANDARD BANK LADYSMITH

LOCATIONLadysmith (KZN) National tenants

TYPE

OfficeSIZE

1 994m2

GROSS RENT

R68/m2

OCCUPANCY

100%NUMBER OF TENANTS

ThreePROPERTY VALUE

R12,6mKEY HIGHLIGHTLocated on the main road in the busy town, the building is prominent and well suited to the tenant who has renewed the lease repeatedly.

A GRADE

STANDARD BANK UPINGTON

LOCATIONUpington National tenant

TYPE

OfficeSIZE

1 181m2

GROSS RENT

R77/m2

OCCUPANCY

100%NUMBER OF TENANTS

OnePROPERTY VALUE

R9,75mKEY HIGHLIGHTThe property forms a cornerstone in the thriving town of Upington with the bank repeatedly renewing its lease.

I Property Investment Fund integrated annual report 2013P10

property portfoliocontinued

A GRADE

XSTRATA BUILDING

LOCATIONRustenburgNational tenant

TYPE

OfficeSIZE

3 720m2

GROSS RENT

R84/m2

OCCUPANCY

100%NUMBER OF TENANTS

ThreePROPERTY VALUE

R33,8mKEY HIGHLIGHTThe property houses the regional offices of Xstrata who recently renewed their lease. Purpose built for them, the property is fit for purpose with competitive rentals.

A GRADE

VODACOM PARK

LOCATIONSandtonNational tenant

TYPE

OfficeSIZE

5 101m2

GROSS RENT

R134/m2

OCCUPANCY

100%NUMBER OF TENANTS

OnePROPERTY VALUE

R100,0mKEY HIGHLIGHTVodacom has occupied the park for many years and Wierda Valley is fast becoming a very desirable location, being two blocks from Gautrain and just off the congestion of Sandton Central. The property has been consolidated with the adjacent Linger Longer site which is being rezoned to give 35 000m2 bulk. The development will achieve a Green Star rating and will be tenant led.

B GRADE

BENSTRA BUILDING

LOCATIONPretoria CBDGovernment tenant

TYPE

OfficeSIZE

7 818m2

GROSS RENT

R107/m2

OCCUPANCY

100%NUMBER OF TENANTS

ThreePROPERTY VALUE

R47,1mKEY HIGHLIGHTLocated in the Pretoria CBD ‘government district’, the tenant has again renewed the lease.

ENVIRONMENT

Property Investment Fund integrated annual report 2013 I P11

B GRADE

MOTHERWELL RETAIL CENTRE

LOCATIONMotherwellNational tenants

TYPE

RetailSIZE

3 764m2

GROSS RENT

R87/m2

OCCUPANCY

100%NUMBER OF TENANTS

ThirteenPROPERTY VALUE

R37,5mKEY HIGHLIGHTThe retail centre is the nucleus of the area and repeated extensions are satisfying the huge demand. The last remaining extension will start at the end of 2014.

B GRADE

BRICKFIELD BUILDING

LOCATIONWoodstock Cape TownSingle tenanted

TYPE

IndustrialSIZE

5 251m2

GROSS RENT

R34/m2

OCCUPANCY

100%NUMBER OF TENANTS

OnePROPERTY VALUE

R23,4mKEY HIGHLIGHTWoodstock is an industrial area which are changing and becoming a vibey upmarket commercial node.

A GRADE

14 LOOP STREET

LOCATIONCape Town CBD Government tenants

TYPE

OfficeSIZE

2 323m2

GROSS RENT

R138/m2

OCCUPANCY

100%NUMBER OF TENANTS

TwoPROPERTY VALUE

R37,1mKEY HIGHLIGHTWinner of the 2012 Energy Efficiency Award, this 1904 building was extensively redeveloped in 2009 on ‘green principles’. The building enjoys an energy cost of 33% of the portfolio average and 4% water consumption. The A grade building is located in the new financial district of Cape Town and is fully let to a government tenant on long lease.

ENVIRONMENT

To be refurbished as above

I Property Investment Fund integrated annual report 2013P12

B GRADE

PARTHENON PARK

LOCATIONPretoria EastNational tenants

TYPE

Office/retailSIZE

4 454m2

GROSS RENT

R84/m2

OCCUPANCY

83%NUMBER OF TENANTS

SeventeenPROPERTY VALUE

R38,75mKEY HIGHLIGHTUpgraded and consolidated with Murrayfield, the offices are dominated by Impala Platinum and the retail by a suitable neighbourhood retailer mix, most of whom have been there many years.

property portfoliocontinued

B+ GRADE

PERSEUS PARK

LOCATIONLynnwood Ridge Pretoria Government tenants

TYPE

OfficeSIZE

13 838m2

GROSS RENT

R96/m2

OCCUPANCY

100%NUMBER OF TENANTS

OnePROPERTY VALUE

R157,0mKEY HIGHLIGHTSITA is a long-term tenant in the building and has indicated possible interest in expanding by using the available bulk on site.

B GRADE

MURRAYFIELD FORUM

LOCATIONPretoria EastNational tenants

TYPE

Office/retailSIZE

1 417m2

GROSS RENT

R85/m2

OCCUPANCY

77%NUMBER OF TENANTS

EightPROPERTY VALUE

R8,0mKEY HIGHLIGHTRecently upgraded, the neighbourhood centre is now stable and enjoys good visibility and access. Predominant tenant is Total on a 15 year lease.

Property Investment Fund integrated annual report 2013 I P13

B GRADE

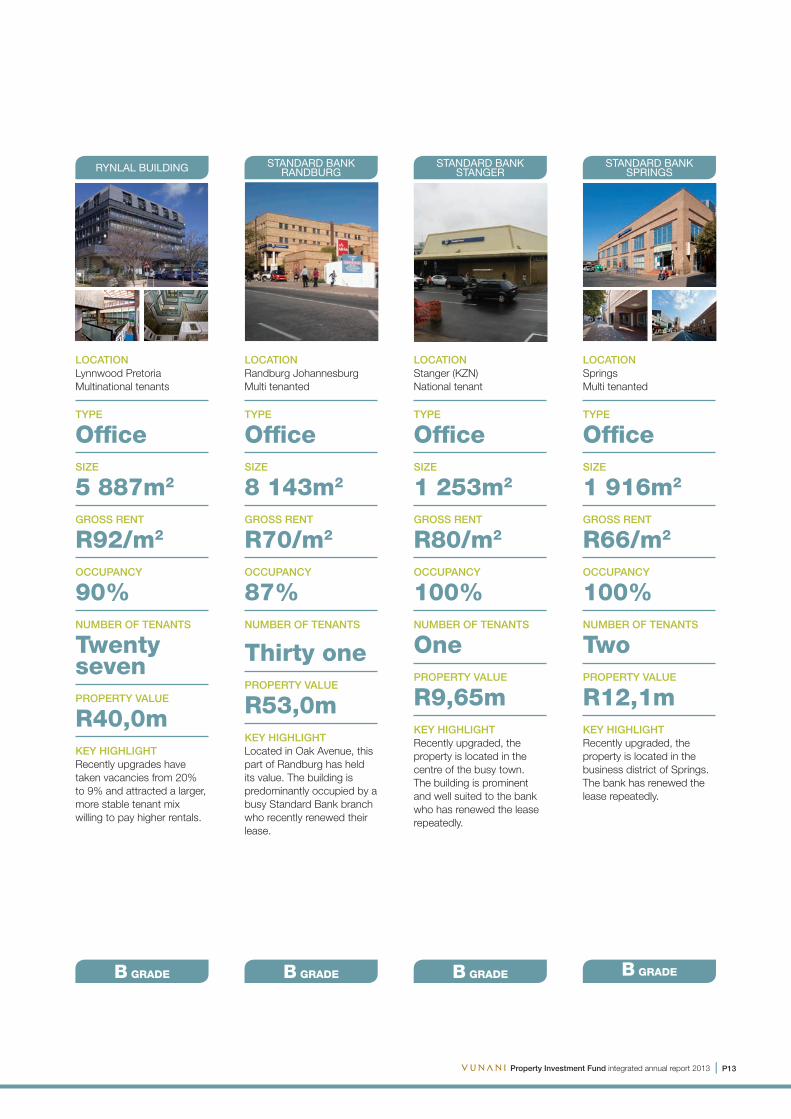

RYNLAL BUILDING

LOCATIONLynnwood PretoriaMultinational tenants

TYPE

OfficeSIZE

5 887m2

GROSS RENT

R92/m2

OCCUPANCY

90%NUMBER OF TENANTS

Twenty sevenPROPERTY VALUE

R40,0mKEY HIGHLIGHTRecently upgrades have taken vacancies from 20% to 9% and attracted a larger, more stable tenant mix willing to pay higher rentals.

B GRADE

STANDARD BANK STANGER

LOCATIONStanger (KZN) National tenant

TYPE

OfficeSIZE

1 253m2

GROSS RENT

R80/m2

OCCUPANCY

100%NUMBER OF TENANTS

OnePROPERTY VALUE

R9,65mKEY HIGHLIGHTRecently upgraded, the property is located in the centre of the busy town. The building is prominent and well suited to the bank who has renewed the lease repeatedly.

B GRADE

STANDARD BANK SPRINGS

LOCATIONSpringsMulti tenanted

TYPE

OfficeSIZE

1 916m2

GROSS RENT

R66/m2

OCCUPANCY

100%NUMBER OF TENANTS

TwoPROPERTY VALUE

R12,1mKEY HIGHLIGHTRecently upgraded, the property is located in the business district of Springs. The bank has renewed the lease repeatedly.

B GRADE

STANDARD BANK RANDBURG

LOCATIONRandburg Johannesburg Multi tenanted

TYPE

OfficeSIZE

8 143m2

GROSS RENT

R70/m2

OCCUPANCY

87%NUMBER OF TENANTS

Thirty onePROPERTY VALUE

R53,0mKEY HIGHLIGHTLocated in Oak Avenue, this part of Randburg has held its value. The building is predominantly occupied by a busy Standard Bank branch who recently renewed their lease.

I Property Investment Fund integrated annual report 2013P14

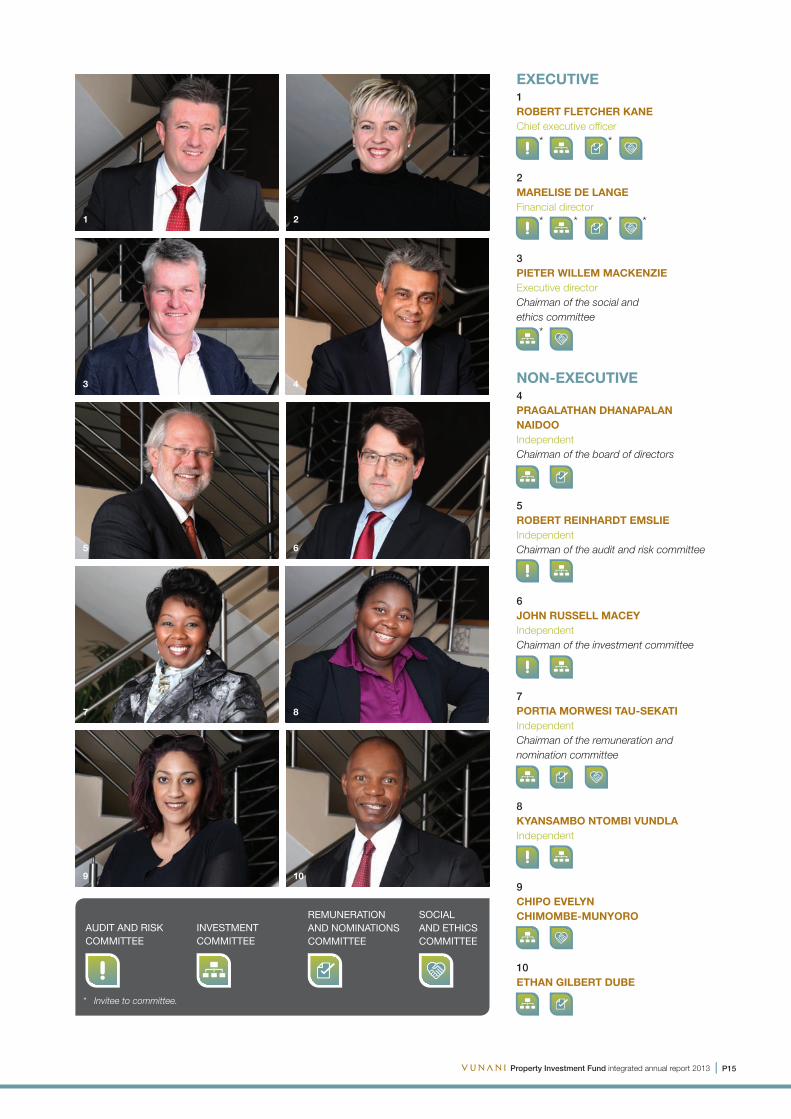

directorate

EXECUTIVE

1ROBERT FLETCHER KANE (53)Chief executive officerBSc (CIV) Eng, MBA

Rob has over 28 years’ experience in all aspects of the property industry. After completing his BSc degree at the University of Cape Town, he was employed by Wilson Bayly Holmes-Ovcon Limited as a building contractor. He gained his Pr Eng qualification in 1989 and then worked as a consultant in the United Kingdom for 18 months prior to completing an MBA at Bath University. He joined Kennedy & Donkin (UK) as the business development manager responsible for Western Europe, Scandinavia, Turkey and Africa. Rob returned to South Africa in 1996 and joined Herbert Penny as a property investment broker. He managed his own property development and investment broking business between 1998 and 2003. Rob joined Vunani Properties in 2004, where his focus has been on VPIF and Western Cape developments. He has been CEO of VPIF since mid-2008. He is Chairman of the Cape Town City Improvement District and a board member of the Cape Town Partnership. He is a member of the Investment Analysts Society and a committee member of the Western Cape South African Property Owners Association.

2MARELISE DE LANGE (41)Financial directorBCom (Law), BCom (Hons) (Acc)

Marelise obtained BCom (Law) and BCom (Hons) (Acc) degrees and commenced her career at Absa Corporate and Merchant Bank in the Structured Finance division. She later worked at Absa Capital where she held the position of Business Manager – Structured Capital Market. In June 2008, Marelise joined International Housing Solutions, a property equity fund for affordable housing, as financial director where her duties included the implementation of IFRS accounting and reporting systems for the South Africa Workforce Housing Fund. Her finance and accounting experience extends over 18 years. Marelise joined the Vunani Group in June 2009 as group financial manager and as financial

director is responsible for the full finance and accounting function of Vunani Property Investment Fund Limited.

3PIETER WILLEM MACKENZIE (49)Executive directorBSc Building Management, MBA

Pete has over 20 years’ experience in all aspects of the property industry. He is the managing director of Vunani Properties and has held this position since April 2003. His responsibilities include the day-to-day management and financial control of Vunani Properties, which focuses on both property development and investment. Pete was with Pegasus III Properties from January 1994 until March 2003 where he was managing director in his final two years, and was responsible for all construction and development activities in the Corovest Property Group. During the period January 1992 to December 1993, he was the Development Director of Dallaway Developments where he was responsible for all construction and development activities. Pete obtained a BSc degree in Building Management from the University of Cape Town in 1987 and an MBA from Wits Business School in 1998. Pete is a member of the South African Property Owners Association.

NON-EXECUTIVE

4PRAGALATHAN DHANAPALAN NAIDOO (55)IndependentBSc (Hons) Civil Engineering, Pr Eng

Dempsey is the founder and executive chairman of PD Naidoo & Associates, a diversified consulting engineering group based in Johannesburg, which focuses mainly on infrastructure, mining and regeneration projects. Dempsey combines his engineering qualifications and experience with business and leadership acumen to develop and drive consistently successful major commercial undertakings, in both large corporate and professional environments.

5ROBERT REINHARDT EMSLIE (55)IndependentBCom (Hons), CA(SA)

Robert Emslie is a member of a number of boards of listed and unlisted companies (mainly as an independent director). He has more than 30 years’ experience in the financial services sector and retired as a career banker in 2008. He is a qualified chartered accountant.

6JOHN RUSSELL MACEY (51)Independent BBusSci (Hons), BCom (Hons), CA(SA)

John studied at UCT and completed his articles with Deloitte in 1991. Since leaving Deloitte he has gained eight years of experience as CFO to manufacturing companies. He was also a staff member of the now College of Accounting at UCT for nine years, leaving as a tenured member of staff in 2009 to start his own advisory business. He is a qualified chartered accountant and serves on the boards and audit committees of three JSE listed companies.

7PORTIA MORWESI TAU-SEKATI (42)IndependentBA (Hons), PDM (Bus ad), Board Leadership (Gibs), African Leadership (UNISA)

Portia is currently the CEO of The Property Sector Charter Council. She has worked in various public and private entities and has extensive knowledge and is an expert in “transformation” as driven in the RSA by the BBBEE framework. She also has extensive experience in dealing with and lobbying government. Previously she served as the CEO of the National Association of Real Estate Agencies. Portia’s background is in marketing and she has held senior marketing positions both locally and abroad in companies such as Thebe Investment Corporation, Roche Pharmaceuticals and Gillette Company. She has also been appointed as a member of the company’s investment committee, social and ethics committee and remuneration and nominations committee.

8KYANSAMBO NTOMBI VUNDLA (34)IndependentBCom (Accounting), HDip Acc, CA(SA)

Kyansambo is a Chartered Accountant (SA) and is currently the CFO of Regiments Capital having previously held the position of CFO of Momentum Group Employee Benefits Division. She holds a number of directorships and memberships including Chairperson of the audit and risk committee for the Estate Agency Affairs board and she is also an independent non-executive director of Workforce Limited. Her previous memberships included audit and risk committee of the Bonitas Medial Aid Fund. She has also been appointed as a member of the company’s audit and risk committee.

9CHIPO EVELYN CHIMOMBE-MUNYORO (40)BA, LLB, LLM (Commercial Law/Maritime Law)

Evelyn is an admitted attorney of the High Court of South Africa. She was previously a director and partner at Fairbridges Attorneys. Evelyn initially served on the board of Vunani as a non-executive director and during 2006 she joined Vunani as an executive director. She has served in the capacity of a non-executive director on the boards of various JSE listed companies and is the current chairperson of PSV Holdings Limited.

10ETHAN GILBERT DUBE (53)MSc (Statistics), Executive MBA (Sweden)

Ethan has an extensive corporate finance and asset management background which he gained at Standard Chartered Merchant Bank, Southern Asset Managers and Infinity Asset Management. Ethan was a founder and has been managing director of Vunani Capital Proprietary Limited (previously African Harvest Capital) since its inception in the late 1990s. He is a director of a number of JSE listed companies, inter alia Hyprop.

Property Investment Fund integrated annual report 2013 I P15

EXECUTIVE1ROBERT FLETCHER KANE)Chief executive officer

2MARELISE DE LANGE1)Financial director

3PIETER WILLEM MACKENZIE9)Executive directorChairman of the social and ethics committee

NON-EXECUTIVE 4PRAGALATHAN DHANAPALAN NAIDOO)IndependentChairman of the board of directors

5ROBERT REINHARDT EMSLIEIndependentChairman of the audit and risk committee

6JOHN RUSSELL MACEYIndependent Chairman of the investment committee

7PORTIA MORWESI TAU-SEKATIIndependentChairman of the remuneration and nomination committee

8KYANSAMBO NTOMBI VUNDLAIndependent

9CHIPO EVELYN CHIMOMBE-MUNYORO)

10ETHAN GILBERT DUBE

1 2

3 4

5 6

7 8

9 10

AUDIT AND RISK COMMITTEE

INVESTMENT COMMITTEE

REMUNERATION AND NOMINATIONS COMMITTEE

SOCIAL AND ETHICS COMMITTEE

* Invitee to committee.

* *

* * * *

*

I Property Investment Fund integrated annual report 2013P16

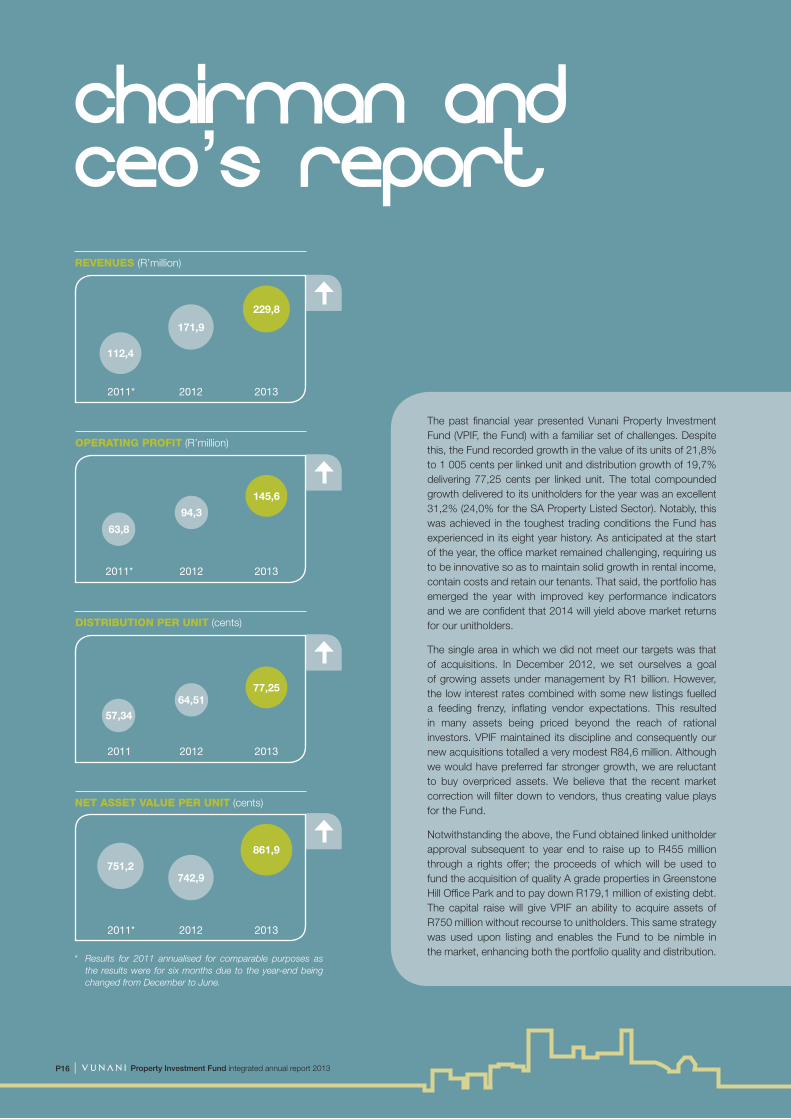

The past financial year presented Vunani Property Investment Fund (VPIF, the Fund) with a familiar set of challenges. Despite this, the Fund recorded growth in the value of its units of 21,8% to 1 005 cents per linked unit and distribution growth of 19,7% delivering 77,25 cents per linked unit. The total compounded growth delivered to its unitholders for the year was an excellent 31,2% (24,0% for the SA Property Listed Sector). Notably, this was achieved in the toughest trading conditions the Fund has experienced in its eight year history. As anticipated at the start of the year, the office market remained challenging, requiring us to be innovative so as to maintain solid growth in rental income, contain costs and retain our tenants. That said, the portfolio has emerged the year with improved key performance indicators and we are confident that 2014 will yield above market returns for our unitholders.

The single area in which we did not meet our targets was that of acquisitions. In December 2012, we set ourselves a goal of growing assets under management by R1 billion. However, the low interest rates combined with some new listings fuelled a feeding frenzy, inflating vendor expectations. This resulted in many assets being priced beyond the reach of rational investors. VPIF maintained its discipline and consequently our new acquisitions totalled a very modest R84,6 million. Although we would have preferred far stronger growth, we are reluctant to buy overpriced assets. We believe that the recent market correction will filter down to vendors, thus creating value plays for the Fund.

Notwithstanding the above, the Fund obtained linked unitholder approval subsequent to year end to raise up to R455 million through a rights offer; the proceeds of which will be used to fund the acquisition of quality A grade properties in Greenstone Hill Office Park and to pay down R179,1 million of existing debt. The capital raise will give VPIF an ability to acquire assets of R750 million without recourse to unitholders. This same strategy was used upon listing and enables the Fund to be nimble in the market, enhancing both the portfolio quality and distribution.

chairman and ceo’s report

REVENUES (R’million)

2011*

229,8

2012

171,9

2013

112,4

NET ASSET VALUE PER UNIT (cents)

2011*

861,9

2012

742,9

2013

751,2

* Results for 2011 annualised for comparable purposes as the results were for six months due to the year-end being changed from December to June.

OPERATING PROFIT (R’million)

2011* 2012 2013

94,3

63,8

145,6

DISTRIBUTION PER UNIT (cents)

2011 2012 2013

64,5157,34

77,25

Property Investment Fund integrated annual report 2013 I P17

Management have a solid pipeline of acquisitions under negotiation and we have put in place adequate resources internally to effect the deals. Consequently, we anticipate accelerated (but controlled) acquisition activity in 2014.

During the year, VPIF converted to a Real Estate Investment Trust (REIT), effective from 1 July 2013. The conversion to REIT status provides capital gains tax benefits and will be likely to attract foreign interest to the sector as it provides a familiar benchmark for international investors. Furthermore, Vunani Limited disposed of its 15,5% stake in VPIF to facilitate its other commitments. Key management however retained their shareholding and intend to follow their rights in the August capital raise.

Overall, 2013 was an excellent year for the Fund. We have developed a strong platform from which to grow and the results to date are pleasing.

OPERATING ENVIRONMENTA moribund global economy and continued uncertainty over the Eurozone formed the backdrop to the operating environment over the last year. Albeit slow, signs of recovery in both Europe and the United States indicate that the next year should see some uplift in South Africa’s main trading partners. The United States’ Federal Reserve Bank’s indication that it will reduce quantitative easing gave our bond markets (and consequently the property sector) an overdue correction. The disparity between our long bond yields and those of the property listed sector remains a concern with another correction possible in the coming months. Thus, the sector now offers investors a more stable platform going forward, with predictable income.

On a portfolio level, the market remains tough despite the continuing low interest rate environment as the South African economy continues to stumble along with little direction. The South African Reserve Bank’s June quarterly bulletin indicates a narrowing in the current account deficit to 5,8% of gross domestic product (GDP) from 6,5% in the first quarter. Investor confidence has been shaken

by domestic disruption, labour unrest and rand volatility. With the GDP growth forecast falling and a weaker economic outlook, consumer spending has slowed, making tenants cautious when assessing their requirements.

The office sector has not been immune to the dull economic forecasts, however we are comfortable that the office sector is at the bottom of the cycle and are pleased to report that VPIF has outperformed all property sectors by some margin despite these tough conditions.

We have experienced the usual upward pressures on administration and operating costs, such as municipal rates and utilities (electricity, water and waste). These costs have successfully been managed and controlled through a combination of greening initiatives and prudent management. We are pleased to report that solid advances are being made with regard to our greening initiatives, following VPIF’s receiving the 2012 Energy Efficiency Forum Award for its refurbishment of 14 Loop Street, a 1904 heritage building.

Our vacancy rate is a stable 5,6% which compares well with the industry average of 10,7%. The sector vacancies in 2014 may even be exacerbated in those nodes where speculative development will result in landlords competing for the same pool of tenants. VPIF unitholders will be pleased to know that it has little exposure to this cannibalisation.

ACQUISITIONSOur main considerations when acquiring assets will always be a keen focus on the property fundamentals and our downstream ability to manage the assets competently. Management is cognisant of the real cost of poor acquisitions, much of which is only evidenced some time later. Similarly, it is the responsibility of management to improve the quality of the portfolio and this needs to be balanced with the appetite of investors for above market distributions.

cPortfolioR1,568bn

GREENSTONE OFFICE PARK

ENVIRONMENT

I Property Investment Fund integrated annual report 2013P18

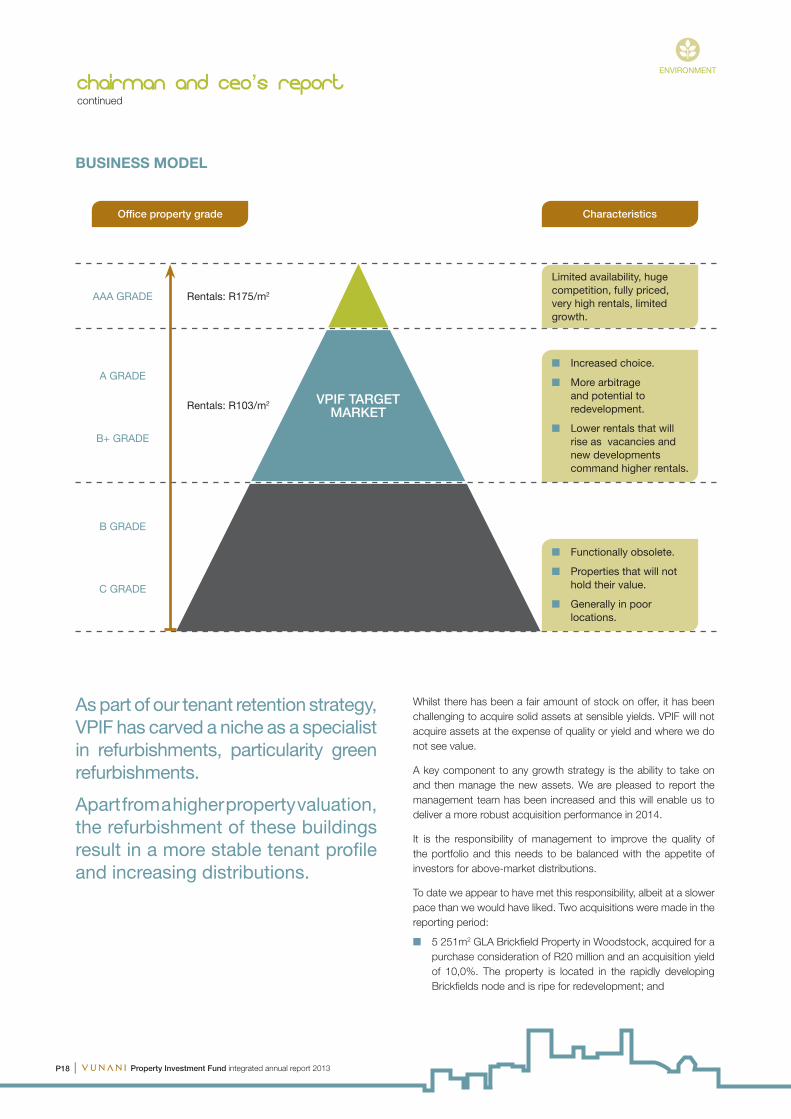

Whilst there has been a fair amount of stock on offer, it has been challenging to acquire solid assets at sensible yields. VPIF will not acquire assets at the expense of quality or yield and where we do not see value.

A key component to any growth strategy is the ability to take on and then manage the new assets. We are pleased to report the management team has been increased and this will enable us to deliver a more robust acquisition performance in 2014.

It is the responsibility of management to improve the quality of the portfolio and this needs to be balanced with the appetite of investors for above-market distributions.

To date we appear to have met this responsibility, albeit at a slower pace than we would have liked. Two acquisitions were made in the reporting period:

n 5 251m2 GLA Brickfield Property in Woodstock, acquired for a purchase consideration of R20 million and an acquisition yield of 10,0%. The property is located in the rapidly developing Brickfields node and is ripe for redevelopment; and

As part of our tenant retention strategy, VPIF has carved a niche as a specialist in refurbishments, particularity green refurbishments.

Apart from a higher property valuation, the refurbishment of these buildings result in a more stable tenant profile and increasing distributions.

BUSINESS MODEL

STRATEGY

chairman and ceo’s reportcontinued

ENVIRONMENT

Office property grade Characteristics

n Increased choice.

n More arbitrage and potential to redevelopment.

n Lower rentals that will rise as vacancies and new developments command higher rentals.

Limited availability, huge competition, fully priced, very high rentals, limited growth.

n Functionally obsolete.

n Properties that will not hold their value.

n Generally in poor locations.

Rentals: R175/m2AAA GRADE

A GRADE

B+ GRADE

B GRADE

C GRADE

Rentals: R103/m2 VPIF TARGET MARKET

Property Investment Fund integrated annual report 2013 I P19

n Business Centre property located prominently in Rivonia Boulevard, Sandton for a purchase consideration of R64,5 million with an acquisition yield of 9,6%. The 4 886m2 GLA property is single tenanted under a 10 year triple net lease.

REFURBISHMENTS AND EXTENSIONSAs part of our tenant retention strategy, VPIF has carved a niche as a specialist in refurbishments, particularity green refurbishments. Apart from a higher property valuation, the refurbishment of these buildings result in a more stable tenant profile and increasing distributions.

Since listing, we have undertaken six refurbishments of varying sizes. In the last reporting period we calculated that for every rand spent we achieve at least three rand in value uplift. Far more important than an enhanced valuation, is the rental growth and improved quality of the offering.

The Fund completed a number of modest, but important upgrades in the reporting period and is pleased with the results.

Investment Place is currently undergoing a refurbishment project where all the foyers and washrooms are being overhauled. Tenanting commences in August 2013.

On the back of the successful 14 Loop Street refurbishment, we have made further encouraging and significant strides in developing other properties into environmentally friendly buildings. This will further enhance VPIF’s portfolio and reputation as a greening refurbishment specialist. We are now looking to leverage this expertise by implementing the same strategy on a much larger scale at the Foretrust Building, located in the fast developing node of the Cape Town Foreshore. On the basis of significant savings (as much as R15 per m2 at 14 Loop Street) we strongly believe that refurbishments according to green principles will sustain the growth of the Fund over the long term. As such, each building in our portfolio is currently being assessed by way of a rating model and we have recently appointed a consulting team of green experts to further develop our offering.

VACANCIESVPIF started the year with 23,3% of leases due to expire. It achieved a very successful 73% retention rate, with the 3 158m2 vacancy in May at Investment Place being the dominant non-renewal. Fortunately, we only have two material leases expiring in 2014 amounting to 7% of our lettable area, 5,5% of which is under a lease renewal offer. Thus, the Fund has very little exposure to expiring leases in 2014. We do not see any notable risks and are confident that there will be few if any reversions as rentals are very much in line with, if not below the market average. The overall weighted average lease expiry is 4,75 years with the average lease escalations at approximately 7,7%.

LEASE EXPIRIESVPIF started the year with 23,3% of leases due to expire. It achieved a very successful 73% retention rate, with the 3 158m2 vacancy

at Investment Place being the dominant non-renewal. Fortunately, we only have two material leases expiring in 2014 amounting to 7% of our lettable area, 5,5% of which is under a lease renewal offer. Thus, the Fund has very little exposure to expiring leases in 2014. We do not see any notable risks and are confident that there will be few if any reversions as rentals are very much in line with, if not below the market average. The overall weighted average lease expiry is 4,75 years with the average lease escalations at approximately 7,7%.

FINANCIALSOverall, VPIF produced a very pleasing set of results in the financial year ended 30 June 2013, delivering distribution growth of 19,7% and capital growth of 21,8%. The total compound growth for the period was 31,2%.

The Fund reported a strong performance and exceeded its distribution targets, with the linked unit price commensurately improving. On 3 December 2012, the Fund released a trading update announcing that the anticipated interim distribution would be 18% to 24,4% greater than the comparable interim period. VPIF declared an interim distribution of 38,0 cents per linked unit. Subsequently, on 31 May 2013, the Fund again released an additional trading statement to indicate a further 16% to 18% distribution growth on the comparable period. The board of directors declared a final distribution of 39,25 cents per linked unit, giving total distributions of 77,25 cents per linked unit. Management believes the platform is solid and that factors will continue to have an enduring and sustainable impact on future distributions.

Investment property income increased by 30,8% from R165,860 million to R216,883 million for the year to 30 June 2013.

Total property related expenses increased by 29,5% from R57,874 million to R74,948 million mainly due to a full 12 month reporting period and acquisitions made during the year. Management believes that life cycle costing and the retention of quality in both its buildings and tenants are more important considerations and therefore does not focus exclusively on expense ratios.

BORROWINGS Net borrowings at 30 June 2013 of R489,905 million equates to a gearing ratio of 31,25%, which is well within the covenants and the directors do not expect that gearing levels will exceed 40%. The blended average cost of debt is 8,7%, broken down into an average of 9,3% (inclusive of margin) for fixed debt for a remaining period of four years and floating at an average of 7,6% (inclusive of margin).

R179,1 million of the R455 million rights offer will be used to pay down the Fund’s floating debt. Coupled with this, we renegotiated our rates with Standard Bank which also significantly reduced our cost of funding in addition to bedding down a facility of R670 million.

In the near future, VPIF plans to enter debt capital markets through a domestic medium-term notes programme to raise further cash to fund acquisitions. DMTN programmes are currently more cost effective than conventional bank funding.

ENVIRONMENT

I Property Investment Fund integrated annual report 2013P20

The subscription price of 987,33 cents per rights offer unit comprises a clean price of 938,07 cents and total pre-paid distributions of 49,26 cents. As a result, the rights offer units will be entitled to the full final 2013 distribution.

Proceeds of the rights offer will be used to fund the acquisition of quality A grade properties in Greenstone Hill Office Park and settle approximately R179,1 million of floating debt, giving us capacity to acquire buildings using available debt capacity. Post the acquisition, VPIF will own 11 of the 15 properties in the office park.

OUTLOOKVPIF continued to outperform the sector and delivered on its promises to all stakeholders. Positive distribution growth of the upcoming financial year is expected with distribution growth anticipated to be between 84,00 and 86,00 cents per linked unit.

As mentioned before, the outlook is tough but we trade well in a tough market.

NOTE OF GRATITUDEOur sincere thanks goes to every VPIF staff member and the property management team who gave of their very best every day and continue to shine in a dull market. Our performance is a reflection of this hard work, which is greatly appreciated by ourselves and the rest of the board of directors.

Our appreciation is also extended to our fellow executives on the board. Their commitment, depth of knowledge and skills are invaluable. Finally, we would not have a fund if it was not for the support received from all our institutional linked unitholders who have believed in our vision to build a very stable, sustainable business, and of our tenants who continue to support us.

PD Naidoo RF Kane Chairman Chief executive officer

STRATEGYVPIF will continue to focus on its chosen niche as specialists in the A+, A and B+ grade offices where arbitrage opportunities are greatest. With that said, management is open to buying assets in other classes, be they industrial or retail, provided that there is value and we are confident we can manage the assets. The Fund will remain office dominated.

We will continue to focus on growing the assets under management through strategic acquisitions that fit within the Fund investment criteria of yield and quality enhancing assets, whilst avoiding trophy assets which remain in high demand and are highly priced. The recent rerating should provide some acquisition opportunities.

The management team has an eight year proven track record of extracting value from its portfolio. Together with the green initiatives gaining traction, the Fund is well positioned for continued growth in distribution to unitholders and to ensure the long-term capital appreciation of our assets.

CORPORATE GOVERNANCEVPIF is committed to continuously improving corporate governance, in line with the recommendations by the King Code on Corporate Governance for South Africa 2009 (King III). We were delighted to announce the recent appointment of Portia Tau-Sekati and Kyansambo Vundla as independent non-executive directors. Portia was subsequently appointed to the investment, social and ethics, remuneration and nomination committees and Kyansambo to the audit and risk committee.

The board now consists of three executive directors, five independent non-executive directors and two non-executive directors.

SUBSEQUENT EVENTSPost the financial year end, VPIF received approval from the JSE to raise up to R455 million. The Fund offered a total of 48 503 939 new linked units to unitholders at a subscription price of 987,33 cents per rights offer unit (which includes the accrued distribution and antecedent). This is in the ratio of 40,21283 rights offer units for every 100 linked units held on the record date for the rights offer.

chairman and ceo’s reportcontinued

ENVIRONMENT SOCIAL

Property Investment Fund integrated annual report 2013 I P21 Property Investment Fund integrated annual report 2013 I P21

We adopt values and philosophies which are the benchmark against which we measure behaviour and the practices in our business. Our values require that directors and management operate with utmost integrity, displaying consistent and uncompromising moral strength and conduct in order to promote and maintain trust.

BENSTRA BUILDING

I Property Investment Fund integrated annual report 2013P22

corporate governance reportINTRODUCTIONThe board ultimately provides leadership based on an ethical foundation, and oversees the overall process and structure of corporate governance. In formulating our governance framework, we aim to apply the highest standards of corporate governance practice, in a pragmatic manner. This enables us to:

n Build and sustain an ethical corporate culture in the company;

n Provide effective supervision and leadership based on ethical imperatives;

n Identify and mitigate significant risks, including reputational risk;

n Direct strategy and operations for sustainable business

n Exercise effective review and monitoring of our activities;

n Promote informed and sound decision making;

n Enable effectiveness, efficiency, responsibility and accountability;

n Enhance stakeholder perceptions of the business;

n Ensure the company is a responsible corporate citizen;

n Facilitate legal and regulatory compliance;

n Secure the trust and confidence of all stakeholders;

n Protect our reputation;

n Ensure sustainable business practices, including social and environmental activities;

n Disclose the necessary information to enable all stakeholders to make a meaningful analysis of our financial position and actions;

n Respond appropriately to changes in market conditions and the business environment;

n Remain at the forefront of international corporate governance practices;

n Ensure company ethics are managed effectively through the social and ethics committee; and

n Track measurements and key performance indicators for ongoing corporate social investment.

The Fund is managed externally by Vunani Property Asset Management Proprietary Limited (VPAM), in terms of the asset management agreement concluded between the parties. The day-to-day management and operational functions are performed by employees of VPAM. The Fund has no employees or personnel of its own.

VALUES AND ETHICS We adopt values and philosophies which are the benchmark against which we measure behaviour and the practices in our business. Our values require that directors and management operate with utmost integrity, displaying consistent and uncompromising moral strength and conduct in order to promote and maintain trust. Sound corporate governance is entrenched in our values, culture, processes, functions and organisational structure. Our governance

structures are designed to ensure that our values are embedded in our business and processes. We have a strong organisational culture of entrenched values, which form the cornerstone of our interactions with all stakeholders. These values are embodied in a written statement of values, which serves as our code of ethics.

SUSTAINABILITY PRACTICES Our sustainability goals reflect our culture of continuous advancement and reaffirm our belief that sustainability in its broadest sense is about managing and positioning the business for the long term. The Fund’s sustainability philosophy is based on the recognition that we are driven by our commitment to our culture and values.

Our approach to sustainability reflects our acute awareness of the need for longevity and an ingrained understanding of the practices that underpin sustainability. This approach is documented throughout the integrated report. The Fund has decided to report on a basis that integrates both financial and non-financial information in line with King III’s recommendations.

BOARD STATEMENT The Fund through its board and management is committed to complying with the disclosure and transparency rules of the JSE Limited (JSE) Listings Requirements, the Companies Act, 2008 and the King Code of Governance Principles for South Africa 2009 (King III). Consequently, all stakeholders can be assured that we are being managed ethically and in compliance with all relevant legislation, regulation and recognised best practice and that the specific requirements set out in the JSE Listings Requirements have been complied with throughout the financial year.

KING IIIThe Institute of Directors of South Africa (IoDSA) is the convener of the King Committee and the custodian of the King Reports. It is one of the main objectives of the IoDSA to promote corporate governance, and one of the best ways to do this is to enable application of the King Report on Governance in South Africa, 2009 (King III).

Challenges with King IIIThere are two primary challenges for organisations when attempting to implement King III:

n King III has to be interpreted and understood within the nature, size and complexity of an organisation; and

n There has been no credible and generally accepted national benchmark to measure and compare application of King III.

Challenges avertedTo assist with the above challenges, the IoDSA has developed the Governance Assessment Instrument (GAI), an online tool that will assist in the following ways:

n Evaluating implementation of governance structures and processes as recommended in King III;

SOCIAL

Property Investment Fund integrated annual report 2013 I P23

n Enabling ongoing tracking of progress on implementation of King III, understanding that it’s a process;

n Providing a simplified framework to the board for a risk-based review of the application of King III, without voluminous reading;

n Facilitating a meaningful scoring mechanism reflective of an organisation’s adoption of King III;

n Providing a framework by which governance can be assured by independent service providers;

n Giving holding companies a concise view of their subsidiaries’ governance status;

n Providing an audit programme for internal and external service providers; and

n Offering a reporting benchmark to stakeholders, that is fit for peer-to-peer comparison of organisations, enhancing confidence in governance reporting.

The GAI calculates an overall score indicating the status of application of King III as follows:

Ratings key AAA Highest application AA High application

BB Notable application B Moderate application

C Application to be improved L Low application

The Fund made use of the GAI for the purposes of assessing the level of compliance with King III, which results in the scores per category as detailed below. Details of the full checklist have been included on our website www.vpif.co.za. The Fund’s overall rating in terms of the GAI is AAA. Additional information is provided on all scores below AA.

Category Score

Board composition AAA

Remuneration AA

Governance office bearers AAA

Chairman AAA

CEO AAA

Company secretary AAA

Board roles and duties

Focal point of corporate governance AAA

Fiduciary duties AAA

Strategy AAA

Ethical leadership AAA

Corporate citizenship and leadership AAA

Risk AAA

IT governance AA

Compliance AAA

Internal audit AAA

Business rescue AAA

Accountability AA

Stakeholder relations AAA

Integrated reporting and disclosure BB

Category Score

Performance assessment AA

Board committees

Audit committee AAA

Risk committee AAA

Remuneration committee AAA

Nomination committee AAA

Social and ethics committee AAA

Group boards N/A

King III distinguishes between statutory provisions, voluntary principles and recommended practices. The King III Report provides best practice recommendations, whereas the King III Code details the principles that all entities should apply. The majority of the principles of King III are being applied and this is evidenced in the various sections of this report. The checklist of our level of compliance with King III can be found on our website. The following principles of King III are currently not being applied:

n Sustainability reporting and disclosure should be independently assured:

– Sustainability reporting and related disclosure was not independently assured by an external expert. The audit and risk committee has overseen the integrated report, including sustainability disclosures; and

– We recognise the importance of sustainability reporting and verification of our efforts in this area. This is a developmental area and we will aim to commission external verification in future.

n The evaluation of the board, its committees and individual directors should be performed annually:

– Performance evaluations have been embarked on and will be completed in the new financial year.

FINANCIAL REPORTING AND GOING CONCERN The directors are satisfied that the Fund has adequate resources to continue in business for the foreseeable future. The assumptions underlying the going concern statement are discussed at every board meeting and again at the time of the approval of the annual financial statements by the board and these include:

n Budgeting and forecasts;

n Profitability;

n Capital; and

n Solvency and liquidity.

In addition, the directors are responsible for monitoring and reviewing the preparation, integrity and reliability of the financial statements, accounting policies and the information contained in the annual report. In undertaking this responsibility, the directors are supported by an ongoing process for identifying, evaluating and managing the risks faced in preparing the financial and other information contained in this annual report. This process was in

I Property Investment Fund integrated annual report 2013P24

corporate governance reportcontinued

place for the year under review and up to the date of approval of the annual report and financial statements. The process is implemented by management and independently monitored for effectiveness by the audit and risk committee and other sub-committees of the board, which are detailed on pages 27 to 31.

Our financial statements are prepared on a going concern basis, taking into consideration:

n The Fund’s strategy, prevailing market conditions and business environment;

n Nature and complexity of our business;

n Risks we assume, and their management and mitigation;

n Key business and control processes in operation;

n Access to capital;

n Needs of all our stakeholders;

n Operational soundness;

n Accounting policies adopted;

n Corporate governance practices;

n Desire to provide relevant and clear disclosures; and

n Operation of board committee support structures.

The board is of the opinion, based on its knowledge of the Fund, key processes in operation and specific enquiries, that there are adequate resources to support the Fund as a going concern for the foreseeable future. Furthermore, the board is of the opinion that the risk management processes and the systems of internal control are effective.

BOARD OF DIRECTORS The board seeks to exercise leadership, integrity and sound judgement in pursuit of strategic goals and objectives, to achieve long-term sustainability, growth and prosperity. The board is accountable for the performance and governance of the Fund.

The board subscribes to the following code of ethics:

The board of directors commits itself to ensure, that the company and its agents conduct the business according to the highest ethical standards and, in particular:

n Comply with all laws of the country that affect the company;

n Comply with the rules of the JSE Limited;

n Act in the best interests at all times of all the stakeholders;

n Be transparent in disclosing all material information that may influence investors and potential investors;

n Not act in any way that may be regarded as harmful business practice;

n Conduct the business as a responsible corporate citizen;

n Trade in securities of the company only in open periods and with the prior written permission of the chairman and/or financial director;

n Not trade in competition with the company; and

n Not hold positions that give rise to a conflict of interests and, should any potentially conflicting situations arise, make full, prior written disclosure to the board and abstain from participating in any discussions or voting on the matter, unless the board consents thereto.

The board provides leadership within a framework of prudent and effective controls which ensures risks are assessed and properly managed. The board has adopted a board charter, which provides a framework of how the board operates as well as the type of decisions to be taken by the board and those which should be delegated to management. The board meets its objectives by reviewing and guiding corporate strategy, setting the values and ethical standards, promoting high standards of corporate governance, approving key policies and objectives, ensuring that obligations to its unitholders and other stakeholders are understood and met, understanding the key risks we face, determining our risk tolerance and approving and reviewing the processes in operation to mitigate risk from materialising, including the approval of the terms of reference of key supporting board committees. To achieve its objectives, the board may delegate certain of its duties and functions to various board committees or the CEO, without abdicating its own responsibilities:

n The board has formally defined and documented, by way of terms of reference, the authority it has delegated to various actions and functions; and

n In fulfilling its responsibilities, the board is supported by management in implementing the plans and strategies approved by the board.

Furthermore, directly or through its sub-committees, the board:

n Assesses the quantitative and qualitative aspects of the Fund’s performance through a comprehensive system of financial and non-financial monitoring involving an annual budget process, detailed monthly reporting, regular review of forecasts and regular management strategic and operational updates;

n Approves annual budgets, capital plans, projections and business plans;

n Monitors compliance with relevant laws, regulations and codes of business practice;

n Ensures there are processes in place enabling complete, timely, relevant, accurate and accessible risk disclosure to stakeholders and monitors our communication with all stakeholders and disclosures made to ensure transparent and effective communication;

n Identifies and monitors key risk areas and key performance indicators;

n Reviews processes and procedures to ensure the effectiveness of internal systems of control;

n Ensures we adopt sustainable business practices, including our social and environmental activities;

n Assisted by the audit and risk committee, ensures appropriate information technology (IT) governance processes are in place,

Property Investment Fund integrated annual report 2013 I P25

and ensures that the process is aligned to the performance and sustainability objectives of the board;

n Ensures the appropriate risk governance, including IT, is in place including continual risk monitoring by management and determines the levels of risk tolerance and that risk assessments are performed on a continual basis;

n Ensures the integrity of the company’s integrated report, which includes sustainability reporting;

n Ensures the induction and ongoing training and development of directors; and

n Considers succession planning.

Independence As at 30 June 2013, the board is compliant with Chapter 2, Principle 2.18 of King III in that the majority of non-executive directors are independent.

Chairman The chairman of the board, Dempsey Naidoo, is considered to be independent as contemplated by King III.

Chairman and chief executive officer The roles of the chairman and chief executive officer are distinct and separate with a clear division of responsibilities that has been approved by the board. The chairman leads the board and is responsible for ensuring that the board receives accurate, timely and clear information to ensure that directors can perform their duties effectively.

Board composition The board is of the view that the non-executive directors are independent of management and promote the interests of stakeholders. The balance of executive and non-executive directors is such that there is a clear division of responsibility to ensure a balance of power, such that no one individual or group can dominate board processes or have unfettered powers of decision making. The board believes that it functions effectively and evaluates its performance annually.

Skills, knowledge, experience and attributes of directors The board considers that the skills, knowledge, experience and attributes of the directors as a whole are appropriate for their responsibilities and our activities. The directors bring a diverse range of skills and expertise to the board including:

n International business and operational experience;

n Understanding of the economics of the property sector in which we operate;

n Knowledge of the regulatory environments in which we operate; and

n Financial, accounting, legal and property experience and knowledge.

The skills and experience profile of the board and its committees are regularly reviewed to ensure an appropriate and relevant composition from a governance, succession and effectiveness perspective.

Board’s and directors’ performance evaluationThe performance of the board, its committees and individual directors will be evaluated annually according to recognised corporate governance practices. The formal process has been approved by the remuneration and nominations committee and will be implemented early in the new financial year. The performance evaluation process will take place both informally, through personal observations and discussions, as well as more formally, through completion of questionnaires. The results will be considered and discussed by the board. The chairman will conduct face-to-face meetings with each director to discuss the results of the formal and informal evaluations and, in particular, seek comments on strengths and developmental areas of the members, the chairman and the board as a whole. Individual training and development needs will discussed with each board member.

Ongoing training and development All new and inexperienced directors are required to attend the JSE AltX induction programme which is mandatory for all new inexperienced directors to attend this course. The cost of attending appropriate external training courses is paid by the company. As the JSE AltX induction training is wide-ranging, a programme specific to the company will be formulated and implemented during the course of the 2014 financial year to cater for further continuing education and training. Following the board’s and directors’ performance evaluation process, any training needs will be communicated and the needs addressed.

Terms of appointment On appointment, non-executive directors are provided with a letter of appointment. The letter sets out, among other things, duties, responsibilities and expected time commitments, details of our policy on obtaining independent advice and, where appropriate, details of the board committees of which the non-executive director is a member. An insurance policy is in place that insures directors against liability they may incur in carrying out their duties.

Independent advice Through the company secretaries, individual directors are entitled to seek professional independent advice on matters related to the exercise of their duties and responsibilities at the expense of the Fund. No such advice was required during the 2013 financial year.

Remuneration The executive directors who are employed by VPAM will not be remunerated directly by the Fund for their services, as the Fund pays the asset management fee to VPAM. The remuneration paid to directors for the year ending 30 June 2013 is set out on pages 73 and 74 of the financial statements. The proposed

I Property Investment Fund integrated annual report 2013P26

corporate governance reportcontinued

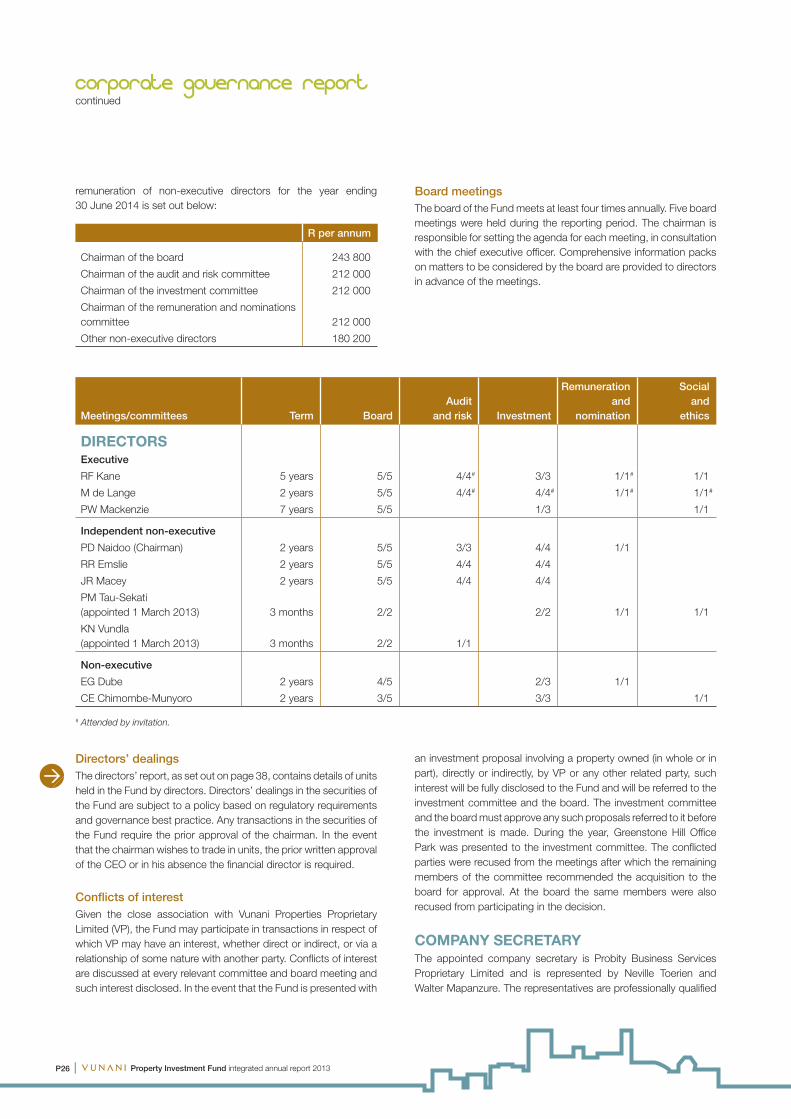

remuneration of non-executive directors for the year ending 30 June 2014 is set out below:

R per annum

Chairman of the board 243 800

Chairman of the audit and risk committee 212 000

Chairman of the investment committee 212 000

Chairman of the remuneration and nominations committee 212 000

Other non-executive directors 180 200

Directors’ dealings The directors’ report, as set out on page 38, contains details of units held in the Fund by directors. Directors’ dealings in the securities of the Fund are subject to a policy based on regulatory requirements and governance best practice. Any transactions in the securities of the Fund require the prior approval of the chairman. In the event that the chairman wishes to trade in units, the prior written approval of the CEO or in his absence the financial director is required.

Conflicts of interest Given the close association with Vunani Properties Proprietary Limited (VP), the Fund may participate in transactions in respect of which VP may have an interest, whether direct or indirect, or via a relationship of some nature with another party. Conflicts of interest are discussed at every relevant committee and board meeting and such interest disclosed. In the event that the Fund is presented with

Board meetings The board of the Fund meets at least four times annually. Five board meetings were held during the reporting period. The chairman is responsible for setting the agenda for each meeting, in consultation with the chief executive officer. Comprehensive information packs on matters to be considered by the board are provided to directors in advance of the meetings.

an investment proposal involving a property owned (in whole or in part), directly or indirectly, by VP or any other related party, such interest will be fully disclosed to the Fund and will be referred to the investment committee and the board. The investment committee and the board must approve any such proposals referred to it before the investment is made. During the year, Greenstone Hill Office Park was presented to the investment committee. The conflicted parties were recused from the meetings after which the remaining members of the committee recommended the acquisition to the board for approval. At the board the same members were also recused from participating in the decision.

COMPANY SECRETARY The appointed company secretary is Probity Business Services Proprietary Limited and is represented by Neville Toerien and Walter Mapanzure. The representatives are professionally qualified

Meetings/committees Term BoardAudit

and risk Investment

Remunerationand

nomination

Social and

ethics

DIRECTORSExecutive

RF Kane 5 years 5/5 4/4# 3/3 1/1# 1/1

M de Lange 2 years 5/5 4/4# 4/4# 1/1# 1/1#

PW Mackenzie 7 years 5/5 1/3 1/1

Independent non-executive

PD Naidoo (Chairman) 2 years 5/5 3/3 4/4 1/1

RR Emslie 2 years 5/5 4/4 4/4

JR Macey 2 years 5/5 4/4 4/4

PM Tau-Sekati (appointed 1 March 2013) 3 months 2/2 2/2 1/1 1/1

KN Vundla (appointed 1 March 2013) 3 months 2/2 1/1

Non-executive

EG Dube 2 years 4/5 2/3 1/1

CE Chimombe-Munyoro 2 years 3/5 3/3 1/1

# Attended by invitation.

Property Investment Fund integrated annual report 2013 I P27

and have the required experience gained over a number of years of professional practice. Their services will also be evaluated by the board members during the annual board evaluation process. In compliance with the JSE Listings Requirements, the board has considered and is satisfied that Neville and Walter are competent, have the relevant qualifications and experience and maintain an arm’s-length relationship with the board. In addition, the board confirms that neither Neville nor Walter have ever served as directors on the board, nor do they take part in board deliberations but only advise on matters of governance, form or procedure.

BOARD COMMITTEES AND RESPONSIBILITIES Committees are established by the board to assist the board in the discharge of its duties.

Board committees have unrestricted access to company information and any resources required to help them fulfil their responsibilities, including professional advice which is paid for by the company.

Every board committee has a board-approved term of reference. The board determines and amends the scope and responsibilities of the committees, as well as the appointment of new committee members.

The CEO and financial director are present at all board committee meetings in order to promote sound corporate governance and optimise the sharing of information. The company secretary attends all board committee meetings.

Board of directorsn Approves the Fund’s strategy;

n Ensures that the Fund complies with all applicable laws;

n Is responsible for the governance of risk, including that of information technology (IT);

n Acts as focal point for, and custodian of, corporate governance;

n Provides effective leadership based upon an ethical foundation;

n Approves the terms of reference of board committees;

n Assesses the going-concern fundamentals;

n Ensures that adequate controls are in place; and

n Ensures the Fund operates as a responsible corporate citizen.

Audit and risk committeeThe audit and risk committee comprises three independent non-executive directors. The CEO, financial director and internal and external auditors are present at meetings, by standing invitation.

The committee members are:RR Emslie (Chairman)JR MaceyKN Vundla

The committee invitees are:RF Kane (CEO)M de Lange (FD)LA Rowan (JHI)M Lever (Excellerate – internal audit)D Thompson (KPMG – external audit)A de Bruyn (KPMG – external audit)N Toerien (Probity Business Services – company secretary)W Mapanzure (Probity Business Services – company secretary)

The committee maintains an active working relationship with the board. The committee is governed by its terms of reference, the Act and the King III Report and Code of Governance. The terms of reference are aligned to both the King III Report and Code and the new Companies Act.

The committee meets quarterly with ad hoc meetings arranged as and when necessary. To assist the board in its supervisory and governance responsibilities, the responsibilities of the committee include the following:

n Ensuring adequate processes are in place to safeguard the company’s assets;

n Ensuring adequate accounting records are maintained;

n Reviewing reports and financial statements and integrated report prior to recommendation to the board for approval;

n Reviewing the appropriateness of accounting policies and their application;

n Overseeing the external audit process;

n Considering the external audit scope;

n Ensuring the effectiveness of internal controls is regularly reviewed and effective systems of internal control are maintained;

n Ensuring an open channel of communication is maintained between directors and accounting staff, as well as external auditors;

n Ensuring an external auditor is appointed at all times to determine the scope for each external audit. The committee reviews and sets auditors’ fees for the annual audit;

n Reviewing internal audit plans, reports, capacity and capability;

n Ensuring compliance with legal requirements, accounting standards and the JSE Listings Requirements;

n The adoption and implementation of an appropriate risk management policy specifically for REITs which will be in accordance with industry practice and prohibit the entering into of any derivative transactions which are not in the normal cause of business;

n Ensuring the finance functions of the Manager, as they pertain to the Fund, are adequately skilled, resourced and experienced; and

n Ensuring that the external auditors are independent.

I Property Investment Fund integrated annual report 2013P28

corporate governance reportcontinued

Remuneration and nominations committeeAs the operations of the Fund are undertaken by the Manager, the Fund does not have any employees. The remuneration and nominations committee therefore does not make decision relating to the remuneration of executive directors. The executive directors are employed by the Manager and are not remunerated for their services as directors of the Fund. The board does however, assess and comment on the suitability of executive remuneration. The remuneration of the non-executive directors is determined by the committee and recommended to the board and unitholders for approval. The level of fees paid to non-executive directors is reviewed by the remuneration and nominations committee on an annual basis. For details regarding fees paid during the current and prior year, refer to note 30 to the financial statements. There are no service contracts for non-executive directors. For details pertaining to direct or indirect beneficial holdings in units of the Fund in the current or prior year, refer to page 38. The fees paid to non-executive directors are approved annually in advance of the annual general meeting.

The committee members are:PM Tau-Sekati (Chairman)PD NaidooEG Dube

The committee invitees are:RF Kane (CEO)M de Lange (FD)N Toerien (Probity Business Services – company secretary)W Mapanzure (Probity Business Services – company secretary)