Volkswagen Group in China Dr. Jörg Mull · 2020. 6. 27. · second joint venture in China. Ca. 5.5...

31

Volkswagen Group in China Dr. Jörg Mull Executive Vice President, Finance Volkswagen Group China

Transcript of Volkswagen Group in China Dr. Jörg Mull · 2020. 6. 27. · second joint venture in China. Ca. 5.5...

Volkswagen Group in ChinaDr. Jörg MullExecutive Vice President, Finance

Volkswagen Group China

2

Current China Automotive Market and Sales Performance

Market & Volkswagen Group Outlook

Volkswagen Group in China

Economic Indicators

Financial Results

Products

Capacity and Investment

3

History

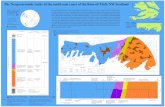

Introduction of Volkswagen Group China

Volkswagen was the automotive pioneer in the modern Chinese market.

1985: Shanghai Volkswagen Automotive Co. (SVW) started production as a joint venture with the Shanghai Automotive Industrial Corporation (or SAIC). Ca. 7.5 million vehicles until February 2012.

1991: FAW-Volkswagen Automotive Co. Ltd. (FAW-VW) started production as the second joint venture in China. Ca. 5.5 million vehicles until February 2012.

2004: Volkswagen Group China was founded to coordinate and manage all activities of Volkswagen in China.

Today: Volkswagen is represented by 17 companies in China (including finance and sales companies).

Total Investments 1984-2011Planned Investments 2012-2016Deliveries to Customers 2011Employees 2011

€ 12.4 Billion€ 14 Billion2.259 Million vehicles48,058

Volkswagen China Investment Company

Beijing

Volkswagen Transmission

Shanghai VolkswagenPowertrain

Shanghai

FAW-Volkswagen(Volkswagen, Audi)

DalianVolkswagen FAW Engine

ChangchunVolkswagen FAW Platform

Chengdu

Nanjing Shanghai Volkswagen

Shanghai Volkswagen(Volkswagen, ŠKODA)

Volkswagen AutomaticTransmission

Foshan

Yizheng

Volkswagen Production Facilities in China

car production plantscomponent plantsplanned plantsHeadquarter Volkswagen Group China

FAW-Volkswagen

Ningbo

4

FoundationShare

Deliveries 2011

1990FAW 60%, VW AG 30%, AUDI AG 10%

993,000

Successful partnership with FAW and SAIC

Octavia RSFabia Scout SuperbOctaviaFabia

Polo HB CrossPoloPolo NB

Passat LingyuTouran TiguanLavida

Santana Santana Vista

Passat

1984SAIC Motor 50%, VW AG 50%

1,141,000

CC

SagitarJetta Bora

Golf Golf GTI Magotan

A6LA4L Q5

5

Volkswagen

Lamborghini, Bentley

Audi

Locally ProducedImport FBU*

220.1

741.1 252.0

920.6

FAW-VW

SVW

61.7

61.0

2.2

Total Deliveries Region China 2.259 million

Deliveries of Volkswagen in China 2011 (‘000 Units)

* incl. Hongkong; Source: Volkswagen Group China

∑ 124.9 ∑ 2.134

6

Current China Automotive Market and Sales Performance

Market & Volkswagen Group Outlook

Volkswagen Group in China

Economic Indicators

Financial Results

Products

Capacity and Investment

7

The economy of China is on a track towards normalization

Economic Indicators Unit 2008 2009 2010 2011 2012 E

GDP [Growth rate] 9.6% 9.2% 10.3% 9.2% 8.3%

Consumption (public +private) [Growth rate] 21.6% 15.5% 18.4% 17.1% 16.9%

Inflation [CPI] 5.9% -0.7% 3.3% 5.4% 3.0%

Investment [Growth rate] 26.1% 30.1% 23.8% 23.8% 17.0%

Key Interest rate -- 1.80% 1.80% 2.25% 2.25% --

Shanghai Composite Index -- 1,820 3,277 2,808 2,823 --

Export [Growth rate] 17.2% -16.0% 31.3% 20.3% 8.0%

Import [Growth rate] 18.5% -11.2% 38.7% 24.9% 9.0%

Foreign Direct Investment [Bn. USD] 92.4 90.0 105.7 100.0 70

Exchange rate as of the end of the report period [RMB/USD] 6.83 6.83 6.78 6.46 6.30

Exchange rate as of the end of the report period [RMB/Euro] 9.66 9.80 8.97 9.01 8.19

Data Source: Deutsche Bank / ING

8

2011 GDP reached a 9.2% growth year on year, and the economy is now in a path of stable growth

CAGR 9.2%

Data Source: The National Bureau of Statistics China

CAGR 10.3%

Q4/09

10.7%

Q3/09

8.9%7.9%6.1%

Q2/09Q1/09 Q4/10Q3/10Q2/10Q1/10

11.9%

9.6%10.3%

9.8%

2009 2010 2011

Q1/11

9.7% 9.5%

Q2/11

9.1%

Q3/11

8.9%

Q4/11

CAGR 9.2%

2012(forecast)

Q2/12E Q3/12E Q4/12E

CAGR 8.3%

Q1/12E

7.8%8.4% 8.5% 8.6%

9

GDP Growth development is expected to differentiate more strongly between the various Chinese regions

Zhejiang

Heilongjiang

Jilin

Liaoning

Hebei Tianjin

Shandong

Henan

Anhui

Jiangsu

Jiangxi

Fujian

Guangdong

Hunan

Hubei

Hainan

Beijing

Shanghai

Inner Mongolia

Shanxi

Guangxi Yunnan

Guizhou

Sichuan

Shaanxi

Ningxia

Gansu Qinghai

Tibet

Xinjiang

Chongqing

Expected GDP Growth 201212-15%

10-12%

8-10%

Estimate of Chinese GDP 2012 per Province

Province ExpectedGrowth 2012

Total GDP 2011 (trillion RMB)

Inner Mongolia 15.0% 1.40Guizhou 14.0% 0.56

Chongqing 13.5% 1.00Shaanxi 13.0% 1.20Hainan 13.0% 0.25Anhui 12.6% 1.50

Sichuan 12.0% 2.00Heilongjiang 12.0% 1.10

Tianjin 12.0% 1.10Shanxi 12.0% 1.10

Jilin 12.0% 1.04Gansu 12.0% 0.52Ningxia 12.0% 0.21Qinghai 12.0% 0.16Yunnan 12.0% 0.88Liaoning 11.0% 2.20Hunan 11.0% 1.96Fujian 11.0% 1.75Guanxi 11.0% 1.20Xinjiang 11.0% 0.66

Tibet 11.0% 0.06Henan 10.0% 2.70Hubei 10.0% 1.80Jiangxi 10.0% 1.20

Shangdong 9.5% 4.54Hebei 9.0% 2.40

Guangdong 8.5% 5.30Zhejiang 8.5% 3.18Jiangsu 8%-10% 4.80

Shanghai 8.0% 1.92Beijing 8.0% 1.60

Data Source: Provincial Government Report

10

Current China Automotive Market and Sales Performance

Market & Volkswagen Group Outlook

Volkswagen Group in China

Economic Indicators

Financial Results

Products

Capacity and Investment

11

After a strong boom in the past two years, passenger car market growth in China is stabilizing

2003

* Estimate; Data Source: CKD – CPCA; FBU - Registration

2011201020092008

2,266

5,503

8,482

11,457

+35%

Total Passenger Car Market – China (incl. HK)‘000 Units

+54%

CAGR +19%

12,386

+9%

2012E

8-10%*

12

Volkswagen Group is aiming for a new record in the Chinese market as a strategic target for the near future

20112007 2008 2009 2010

1,024910

1,400

1,923

‘000 Units

Source: Volkswagen Group China

2,259

2012E

Ranking Group YTD MS%Jan-Feb 12

YTD MS%Jan-Feb 11

1 VW Group 19.2% 17.7%

2 GM Group 10.9% 11.0%

3 Hyundai Group 8.6% 8.3%

4 Nissan Group 6.2% 5.0%

5 Toyota Group 5.3% 5.4%

6 Honda Group 4.2% 5.0%

7 Geely Group 3.7% 3.8%

8 BYD 3.5% 3.7%

9 Chery Group 3.4% 3.3%

10 PSA Group 3.1% 3.1%

Others 31.9% 33.7%

13

In Jan-Feb 2012, Volkswagen Group maintained its Number 1 position by market share in China Mainland

Average Market Share in %China Mainland (2012 Jan-Feb)

VolkswagenGroup

14

VW brand maintained the 1st place in the Chinese Passenger Car market

Data Source: Manufacturers exchange data; Volkswagen Group China

Constant Growth of VW BrandMarket Leader in China Passenger Car Market

2007 2008 201020092006

Deliveries to customers

2011 Jan-Feb2012 Jan-Feb

+10%

+3%

+13%

+2%

2011 2012E

In Units In ‘000 Units

15

Audi brand further improved its 1st position in the Chinese Premium Passenger Car market

Data Source: Manufacturers exchange data; Volkswagen Group China

2007 2008 2010200920062011 Jan-Feb2012 Jan-Feb

+43%

+28%

+35%

+22%

Market Leader in China Premium Passenger Car Market Rapid Growth of Audi Brand

2012E2011

Deliveries to customersIn Units In ‘000 Units

16

ŠKODA Brand growing further in 2012

Data Source: Manufacturers exchange data; Volkswagen Group China

2007 2008 201020092011 Jan-Feb

+8%

+16%

+51%

Skoda Brand Competitiveness Skoda Brand is Growing Fast

2012E2012 Jan-Feb

-20%

2011

Deliveries to customersIn Units In ‘000 Units

17

Significant growth of dealer networks planned

~3,000

1,590

1,120

230240

>1,900

>500

>500

2011 Mid-term

18

Current China Automotive Market and Sales Performance

Market & Volkswagen Group Outlook

Volkswagen Group in China

Economic Indicators

Financial Results

Products

Capacity and Investment

19

Volkswagen will continue to launch new products in China, in order to satisfy customer demands (local production)

Audi A6 L

2011+8

+5

+8

Sagitar

Passat Polo NB Fabia

201420132012+8

+7

Magotan

20

>100 vehicles

Field test

Various models

>10,000 vehicles

Series

2 models

E-optimized series

Range100-200 km

Range options

2010-2013 2014-2018 After 2018

>100,000 vehicles

Phase 1: Test

3-phase introduction of e-mobility in China

Phase 2: Start of series production Phase 3: Mass market

21

Current China Automotive Market and Sales Performance

Market & Volkswagen Group Outlook

Volkswagen Group in China

Economic Indicators

Financial Results

Products

Capacity and Investment

22

Chengdu

Nanjing

Beijing

The investment strategy of Volkswagen Group China is self-funded through the Joint Ventures

Source: Volkswagen Group China

North

East

“Go South Strategy”

“Go West Strategy”

Total Investments

2010 - 2012 € 6.0bn

2012 - 2016 € 14.0bn

FAW-VW

SVW

FAW-VW

FAW-VW

Changchun

Shanghai

Foshan

Yizheng

Ningbo

Existing vehicle plant

New vehicle plant / expanding capacity

Nanjing

23

Volkswagen Group China capacity increase(‘000 Units)

Source: Volkswagen Group China

More working days (wd)

Further capacity optimization

2011 2014

Upwardflexibility

~47%

250 wd

250 wd

3 additional plants+

significant increasein one existing plant

1,500

700

3,000

24

Current China Automotive Market and Sales Performance

Market & Volkswagen Group Outlook

Volkswagen Group in China

Economic Indicators

Financial Results

Products

Capacity and Investment

25

Volkswagen Group China – Achievements

Deliveries to Customers 1,024 1,400

Production (100%) 975 1,387

Operating profit (quotal) 831

(’000 Units)

(’000 Units)

(€ m) 395

2008 2009

Source: Volkswagen Group China

1: SVW Group / FAW-VW Group

1

1

2010

1,923

1,914

1,907

2011

2,259

2,202

2,616

26

Current China Automotive Market and Sales Performance

Market & Volkswagen Group Outlook

Volkswagen Group in China

Economic Indicators

Financial Results

Products

Capacity and Investment

27

Total Passenger Car Market in China will develop further in the future

Source: Volkswagen Group China / IHS Global Insight

2020E2011

12,386

>15,000

>20,000

>7%

‘000 Units

2013E2012E

Average AnnualGrowth Rate

Total Passenger Car Market Forecast – China (incl. HK)

8-10%

>8%

28

Mega and midsized cities will be the engine of GDP growth

3

Big town(<0.5M) 572

Small(0.5-1.5M) 171

Mid-sized(1.5-5.0M) 64

Big(5-10M) 11

Mega(10M+)

2005821 cities

8

488

252

114

10

2020872 cities

% of GDP

2005 2020

13 25

21

29

20

17

12

34

19

9

New cities

35

64

6054

117130

44246

Distribution by city size

5

Source: McKinsey Insights China

Remarks: 8 mega cities in 2010 (Shanghai, Beijing, Chongqing, Shenzhen, Tianjin, Wuhan, Chengdu, Guangzhou)

City Level (Population)

Appendix

30

Industry stock levels increased to 2.0 month by the end of February 2012

Data Source: CPCA, Volkswagen Group China

(>1.5) (<1.2)

Current stock level (in month) of major OEMs

Volkswagen Group

Comp.10

Comp.11

Comp.15

Comp.5

Comp.9

SVWVW

Comp.6

Comp.8

AudiComp.3

Comp. 2

Comp. 1

Comp.4

FAW-VWVW

Comp.14

Comp.13

ŠKODAComp.7

(>1.5) (1.2~1.5)3.4

2.42.3

1.82.0

1.7 1.71.5 1.4

1.31.41.21.3 1.2

0.9

1.4 1.3

Industry Average

2.0

Volkswagen Group

1.21.3

Comp.12

Disclaimer

This presentation contains forward-looking statements and information on the business development of the Volkswagen Group. These statements may be spoken or written and can be recognized by terms such as “expects”, “anticipates”, “intends”, “plans”, “believes”, “seeks”, “estimates”, “will” or words with similar meaning. These statements are based on assumptions relating to the development of the economies of individual countries, and in particular of the automotive industry, which we have made on the basis of the information available to us and which we consider to be realistic at the time of going to press. The estimates given involve a degree of risk, and the actual developments may differ from those forecast.

Consequently, any unexpected fall in demand or economic stagnation in our key sales markets, such as in Western Europe (and especially Germany) or in the USA, Brazil or China, will have a corresponding impact on the development of our business. The same applies in the event of a significant shift in current exchange rates relative to the US dollar, sterling, yen, Brazilian real, Chinese Renminbi and Czech koruna.

If any of these or other risks occur, or if the assumptions underlying any of these statements prove incorrect, the actual results may significantly differ from those expressed or implied by such statements.

We do not update forward-looking statements retrospectively. Such statements are valid on the date of publication and can be superceded.

This information does not constitute an offer to exchange or sell or an offer to exchange or buy any securities.