Visa Inc. 2017 Investor Day Visa: The Investment Proposition · Visa Inc. 2017 Investor Day Visa:...

40

Visa Inc. 2017 Investor Day Visa: The Investment Proposition Vasant Prabhu Chief Financial Officer

Transcript of Visa Inc. 2017 Investor Day Visa: The Investment Proposition · Visa Inc. 2017 Investor Day Visa:...

Visa Inc. 2017 Investor Day

Visa: The Investment Proposition

Vasant Prabhu

Chief Financial Officer

Visa: The Investment Proposition

• The Global Growth Opportunity

• Visa’s Core Assets

• Capturing the Growth Opportunity

• Managing the Challenges

• Visa’s Track Record

• The Growth Model

• Capital Allocation Priorities

The Global Growth Opportunity

• $17 Trillion cash and check conversion opportunity

• Growth is approaching an inflectionpoint, one of four over Visa’s 60 year history

• Connected devices could drive a massive expansion in use cases and acceptance points

• Significant opportunity to accelerate payments volume and transaction growth

North America

$3.2TAsia Pacific

$6.1T

Europe

$3.5T

LAC

$1.8T

Cash and Check OpportunityUSD, 2016

CEMEA

$2.4T

$17 Trillion Cash and Check Conversion Opportunity

Source: Visa analysis of data from Oxford Economics, The Nilson Report, Euromonitor, Haver Analytics, UK Card Association, the Central Bank of the Russian Federation, The Norges Bank, The Swiss National Bank, The Bank of Thailand, Reserve Bank of Australia, Federal Reserve, Statistics New Zealand, Saudi Arabian Monetary Agency and the Central Bank of Ireland

Growth is Approaching an Inflection Point, One of Four over Visa’s 60 Year History

Cards

Payments Volume

| Opportunity Through New Inflection Points | June 7, 20173

1970’s

~40 Million

~$10 Billion

(1975)

The Platform as a Service

| Opportunity Through New Inflection Points | June 7, 20174

1990’s

~450 Million

~$600 Billion

(1995)

eCommerce goes mainstream

2010’s

3 Billion+

$7 Trillion+

(2016)

Visa is Everywhere You Want to Be

Inflection Points

1960’s

<1 Million

<$1 Billion

(1960)

Opening the Network

Connected Devices Could Drive a Massive Expansion in Use Cases and Acceptance Points

Source: Visa Operating Certificates CY2016. Merchant locations are provided by Visa’s issuing and acquiring financial institutions; card counts include cards carrying the Visa, Visa Electron, V PAY and Interlink brands as well as PLUS proprietary cards.

Today

3B+cards

44Mmerchant locations

Tomorrow: 10x Increase

~30Bways to pay

~400Mways to be paid

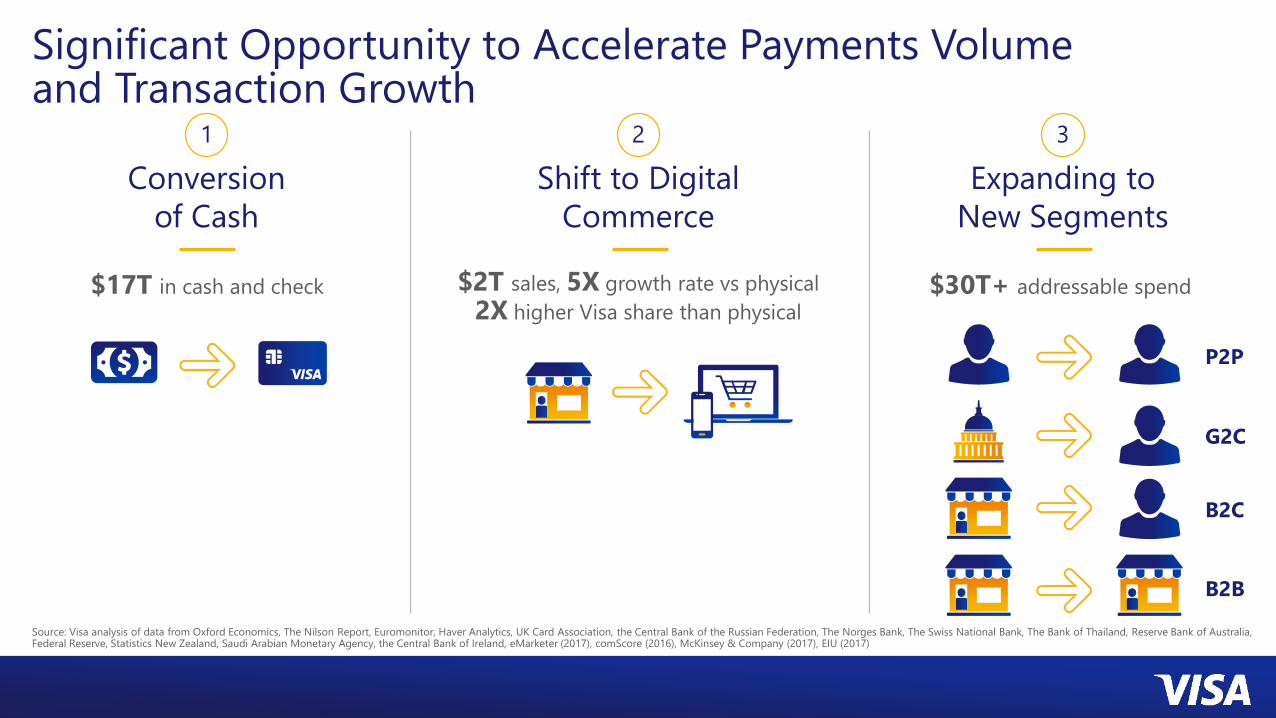

1

Conversion

of Cash

$17T in cash and check

2

Shift to Digital

Commerce

$2T sales, 5X growth rate vs physical

2X higher Visa share than physical

3

Expanding to

New Segments

$30T+ addressable spend

B2B

P2P

G2C

B2C

Significant Opportunity to Accelerate Payments Volume and Transaction Growth

Source: Visa analysis of data from Oxford Economics, The Nilson Report, Euromonitor, Haver Analytics, UK Card Association, the Central Bank of the Russian Federation, The Norges Bank, The Swiss National Bank, The Bank of Thailand, Reserve Bank of Australia, Federal Reserve, Statistics New Zealand, Saudi Arabian Monetary Agency, the Central Bank of Ireland, eMarketer (2017), comScore (2016), McKinsey & Company (2017), EIU (2017)

Visa’s Core Assets

The resources of the four-party network reinforced by new strategic partners

The scale, reliability and security of VisaNet

The power of the Visa Brand

Financial resources of Global Visa

The Resources of the Four-Party Network Reinforced by New Strategic Partners

Source: Operating certificates and Visa Networks CY201

Issuance Acceptance

Strategic Partners

Governments

3B+cards

13,000+ issuers

3,000+acquirers

44Mmerchant locations

Scale

Reliability

Security

• 100+ billion processed transactions

• 160 currencies processed

• 200+ countries

• Multiple data centers connected via multiple high bandwidth circuits

• Redundant connectivity, power, and cooling systems

• Data replication across centers for seamless failover

• Multiple layers of security

• Intelligence driven security

• Moving from reactive to proactive

The Scale, Reliability and Security of VisaNet

The Power of the Visa Brand

ConfidenceSecurityAcceptance Frictionless

The best way to pay and be paid, for everyone, everywhere.

Financial Resources of Global Visa(2011- 2016)

Note: For a reconciliation of our GAAP to Non-GAAP financial metrics, please refer to our annual reports on form 10K.

High Growth

Net RevenueGrowth

10%

High Margin

Operating ProfitMargin

Mid-60’s

High Cash

Cumulative Operating Cash Flow

$30B+

Capturing the Growth Opportunity

Develop Best Talent

Transform

Technology

Champion

Security

Foundational Pillars

Leverage

World-Class Brand

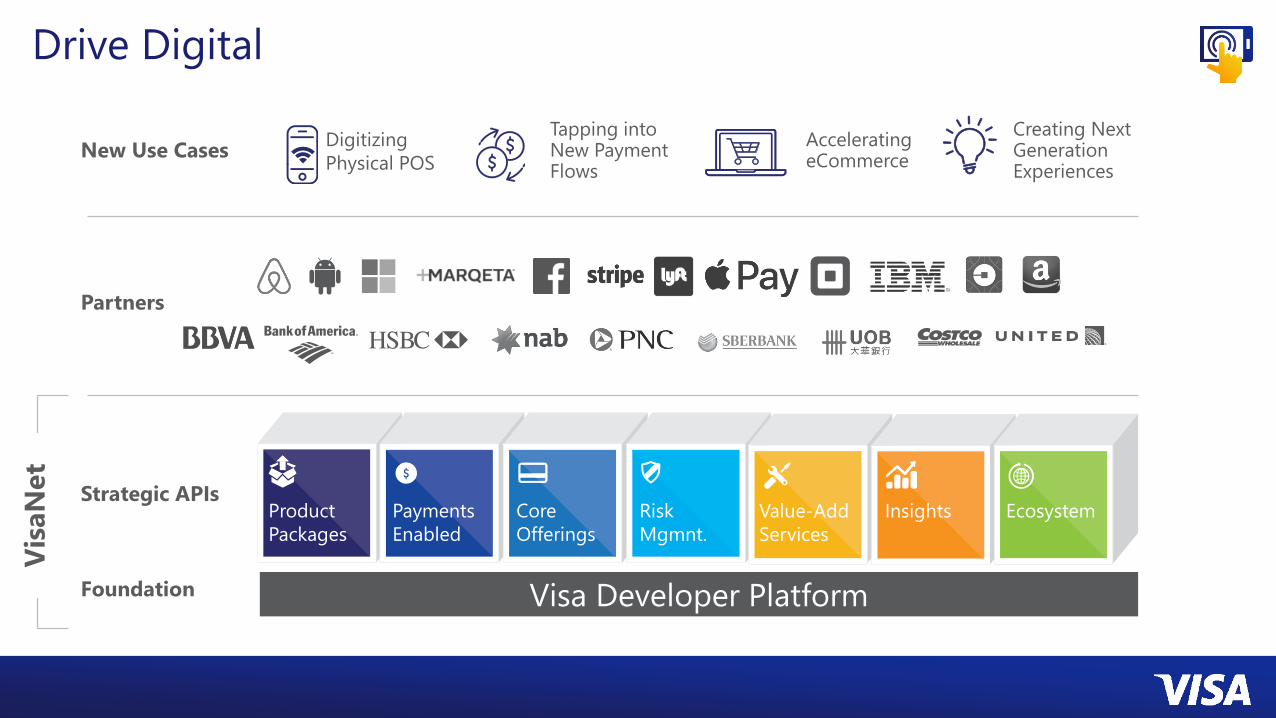

Drive Digital Deepen Partnerships Expand Access

Growth Pillars

Deepen Client Partnerships: Banks

Loyalty & Offers

Acquiring

Consulting

Fraud & Risk

Marketing Digital & Innovation

Core Products

STIP

Deepen Client Partnerships: Merchants

Loyalty & Offers

Co-Brand

Consulting

Fraud & Risk

Marketing Digital & Innovation

Acceptance& Operations

New Use Cases

Visa Developer PlatformFoundation

Vis

aN

et

Strategic APIs

Partners

Product

Packages

Payments

Enabled

Core

Offerings

Risk

Mgmnt.

Value-Add

Services

Insights Ecosystem

Drive Digital

Digitizing

Physical POS

Accelerating eCommerce

Tapping into New Payment Flows

Creating Next Generation Experiences

Drive Digital

Digitizing the POSAccelerating eCommerce

Next Gen CommerceNew Payment Flows

• Visa Checkout

• Token Push & Controls

• Internet of Things

• Innovation Centers

• Visa Direct• “Pays” and HCE

• Scan & Pay

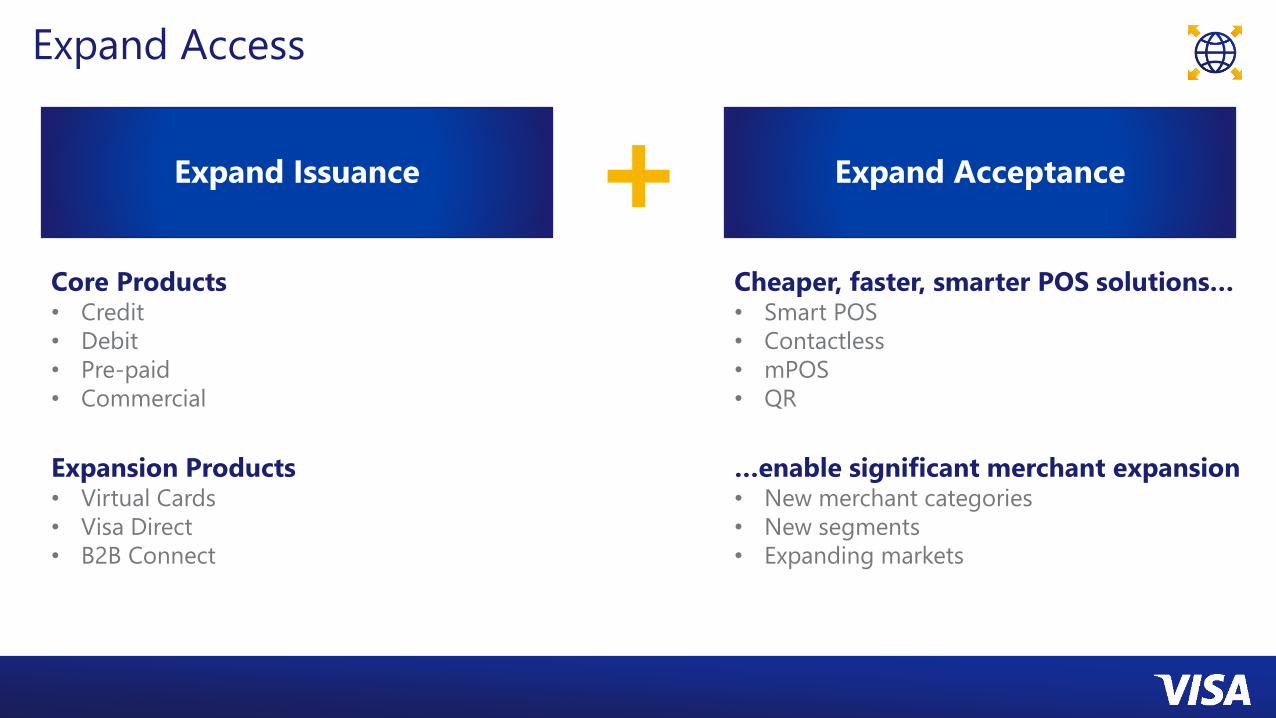

Expand Access

Expand Acceptance+Expand Issuance

Core Products• Credit

• Debit

• Pre-paid

• Commercial

Expansion Products• Virtual Cards

• Visa Direct

• B2B Connect

Cheaper, faster, smarter POS solutions…• Smart POS

• Contactless

• mPOS

• QR

…enable significant merchant expansion• New merchant categories

• New segments

• Expanding markets

Transform Technology

Transform Technology

Champion Security

Empower ConsumersEngage cardholders in

payment security

Devalue DataRender data useless

Protect DataSafeguard payment data

Harness DataStop fraud before it occurs

• Encryption

• PCI

• Detection

• Disruption

• Exchange

• Authentication

• EMV chip

• Tokenization • Alerts

• Digital controls

Data

Leverage World Class Brand

Attract Best Talent

Global / Local

69countries with Visa staff

Investing in Areas of Growth

65%growth in Technology

& Innovation

Experienced Leadership (VP+)

42% 16%>10 years <2 years

Tailoring Our Approach by Market

Note: PCE penetration includes both credit and debit cards

Source: Visa Business and Economic Insights analysis of data from Oxford Economics, The Nilson Report, Euromonitor, Haver Analytics, UK Card Association, the Central Bank of the Russian Federation, The Norges Bank, The Swiss National Bank, The Bank of Thailand, Reserve Bank of Australia, Federal Reserve, Statistics New Zealand, and Saudi Arabian Monetary Agency; Primary: Euromonitor Passport Database, Secondary: Timetric, Lafferty and RBR-EFTPOS; World Bank – World Development Indicators (CY2015)

Market Characteristics ApproachTerminals

per 1,000 pop

PCE

Penetration

GDP per Capita

($K)

Developed >15 >20% >$25

• Provide innovative, convenient ways to pay and be paid

(contactless, IoT, PAYs)

• Partner with technology disruptors to create new payment

experiences

• Expand into new segments and categories

• Provide innovative merchant solutions

Developing 5-20 10-25% $5-$25

• Offer full range of products: affluent credit, commercial,

pre-paid, etc.

• Massively expand acceptance, targeting everyday spend merchant

categories

• Grow preference for Visa cards versus alternatives

• Government partnerships to drive electronification

Emerging <5 <10% <$5

• Introduce and grow core products: debit, credit and prepaid

• Build acceptance in core categories – emphasis on mobile/digital

• Government partnerships to drive electronification

Managing the Challenges

National Payment Schemes

Faster Payments Technology Disruptors

Visa Advantages

• World-Class Brand

• Global Acceptance

• Superior Products

• Digital and Innovation

• Scale

• Proven Real Time Network (VisaNet)

• Push Payment Capabilities

(Visa Direct)

• Established Operating Regulations

• Trusted Brand

• Established Connection

(Banks/Merchants)

• Open Access to VisaNet and Visa

Services via API (Visa Developer

Platform)

• Compete aggressively with new products & innovation

• Continue driving preference among issuers, merchants, and consumers

• Use scale advantages to fund local investments in brand, acceptance, and new features

• Expand real-time Visa Direct product capabilities around the world globally

• Partner with key global platforms to embed Visa Direct as preferred payment method

• Develop deep commercial partnerships that support and expand the four-party model

• Make Visa the commerce platform of choice for any and all developers

• Compete vigorously where needed

Net Revenue ($B)

CAGR 10%

Operating Leverage (% Margin)

+7 ppts

Operating Income ($B)

CAGR 13%

Visa’s Track RecordOperating Performance

1) Includes issuance of preferred stock convertible into approximately 79M of class A common stock in June 2016. Figures shown for fiscal year ending September 30 on adjusted Non-GAAP basis and excludes one-time, non-recurring items. For a reconciliation of our GAAP to Non-GAAP financial metrics, please refer to our annual reports on form 10K

9.2

15.1

2011 2016

=x

Tax Rate (%)

-7 ppts

36.3

29.1

2011 2016

59.0 66.0

2011 2016

Weighted Average Shares Outstanding (B) 1

-15% Total

2.82.4

2011 2016

5.5

10.0

2011 2016

EPS ($)

CAGR 18%

1.25

2.84

2011 2016

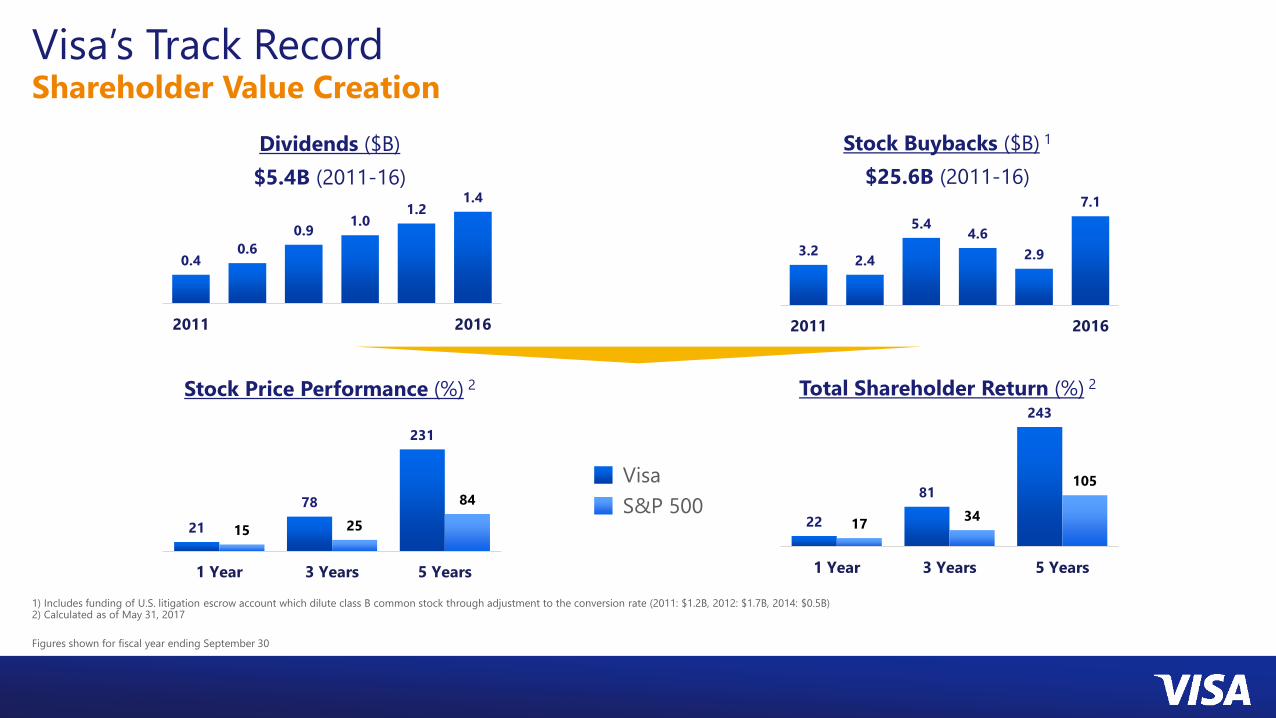

Dividends ($B)

$5.4B (2011-16)

Stock Buybacks ($B) 1

$25.6B (2011-16)

Visa’s Track RecordShareholder Value Creation

1) Includes funding of U.S. litigation escrow account which dilute class B common stock through adjustment to the conversion rate (2011: $1.2B, 2012: $1.7B, 2014: $0.5B)2) Calculated as of May 31, 2017

Figures shown for fiscal year ending September 30

0.40.6

0.91.0

1.21.4

2011 2016

Stock Price Performance (%) 2

3.22.4

5.44.6

2.9

7.1

2011 2016

Total Shareholder Return (%) 2

21

78

231

15 25

84

1 Year 3 Years 5 Years

Visa

S&P 50022

81

243

1734

105

1 Year 3 Years 5 Years

The Growth Model

Net Revenue Growth

Operating Leverage

Operating Income Growth

Financial Levers

EPS Growth

Payments Volume &

Transaction Growth

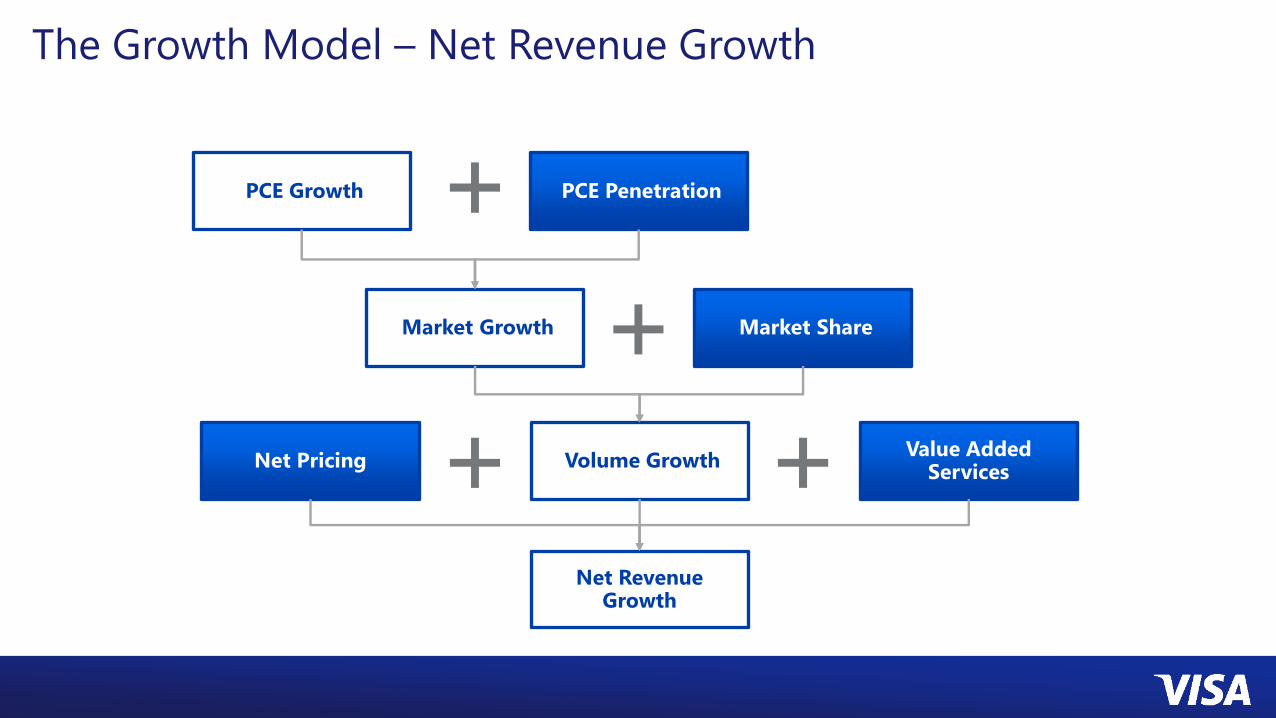

The Growth Model – Net Revenue Growth

PCE Growth PCE Penetration

Market Growth

Volume Growth

Market Share

Net Revenue Growth

Value AddedServices

Net Pricing

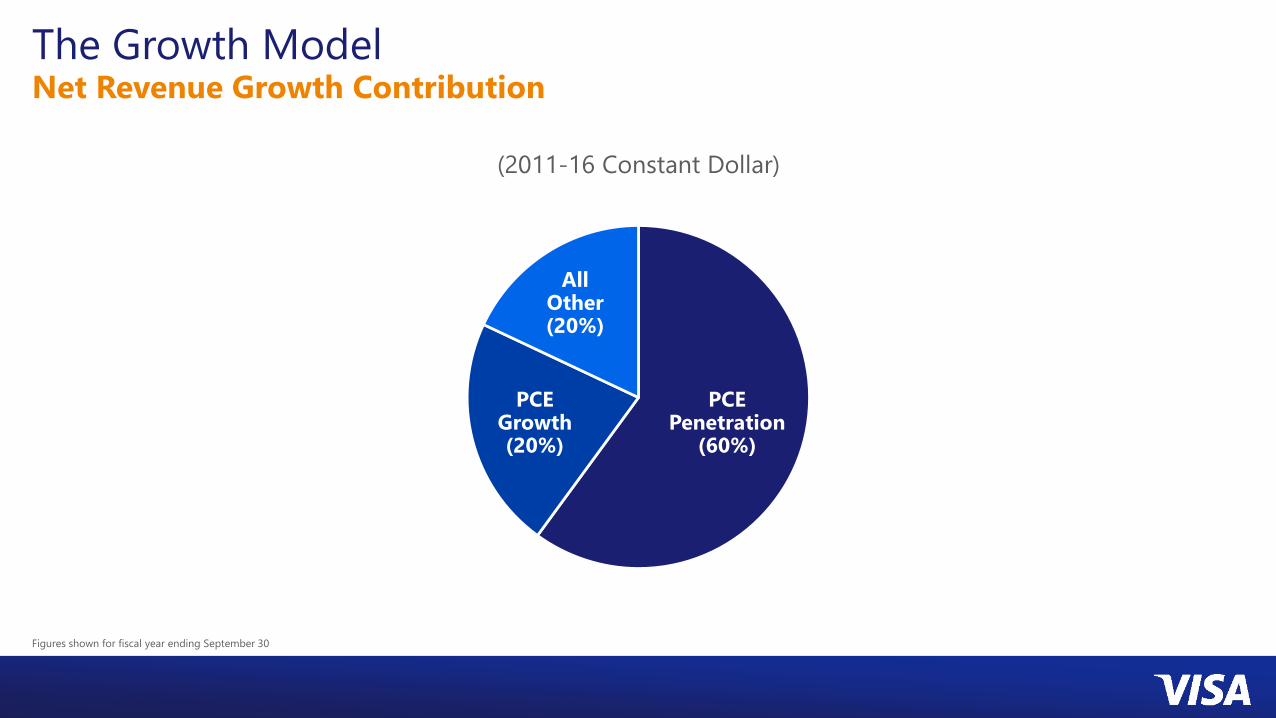

The Growth ModelNet Revenue Growth Contribution

Figures shown for fiscal year ending September 30

(2011-16 Constant Dollar)

PCE Growth(20%)

PCE Penetration

(60%)

All Other(20%)

The Growth Model – Client Incentives

Nominal dollar basis fiscal year ending September 30

• Drive Payments Volume and Transaction growth

• Incent “win-win” outcomes

• Secure multi-year contracts

• Ensure price competitiveness

Why Client Incentives?

Why High Growth?

Why Difficult to Forecast?

• Growth of Payments Volume and Transactions

• Exclusivity

• Longer contract terms

• Issuer consolidation

• Expansion to U.S. Merchants and Acquirers

• Timing of renewal

• Terms of renewal

• Actual volumes/mixvs.

Forecast volumes/mix

Client incentives are a means to an end…

driving volume & Net Revenue

The Bottom Line

Payments

Volume9%

Processed

Transactions10%

Net Revenue 10%

(2011-16 CAGR)

The Growth Model – Operating Leverage

Volume Growth

Fixed Cost Inflation

Core Expense Growth

Productivity

Operating Expense Growth

Investments

Variable CostGrowth

The Growth Model – Operating Leverage

1. Fiscal year 2016. Excludes certain items that are either non-recurring or have no cash impact

2. Support Functions include Finance, Legal, Risk, HR, Strategy and Government Relations

Components of Expense Growth

(Illustrative)

Technology Related

35%

Product, Sales and Service Related

30%

Brand Related

20%

Drivers of Operating Leverage

• Economies of scale (fixed vs. variable cost mix)

• Productivity and purchasing savings

Offset by ...

• Wage and expense inflation

• P&L investments in new capabilities and growth programs

Operating Expense1

Support Functions2

15%

Vo

lum

e G

row

th

Scale

Pro

du

cti

vit

y

Infl

ati

on

Invest

men

t

Exp

en

se G

row

th

9-10%

6%

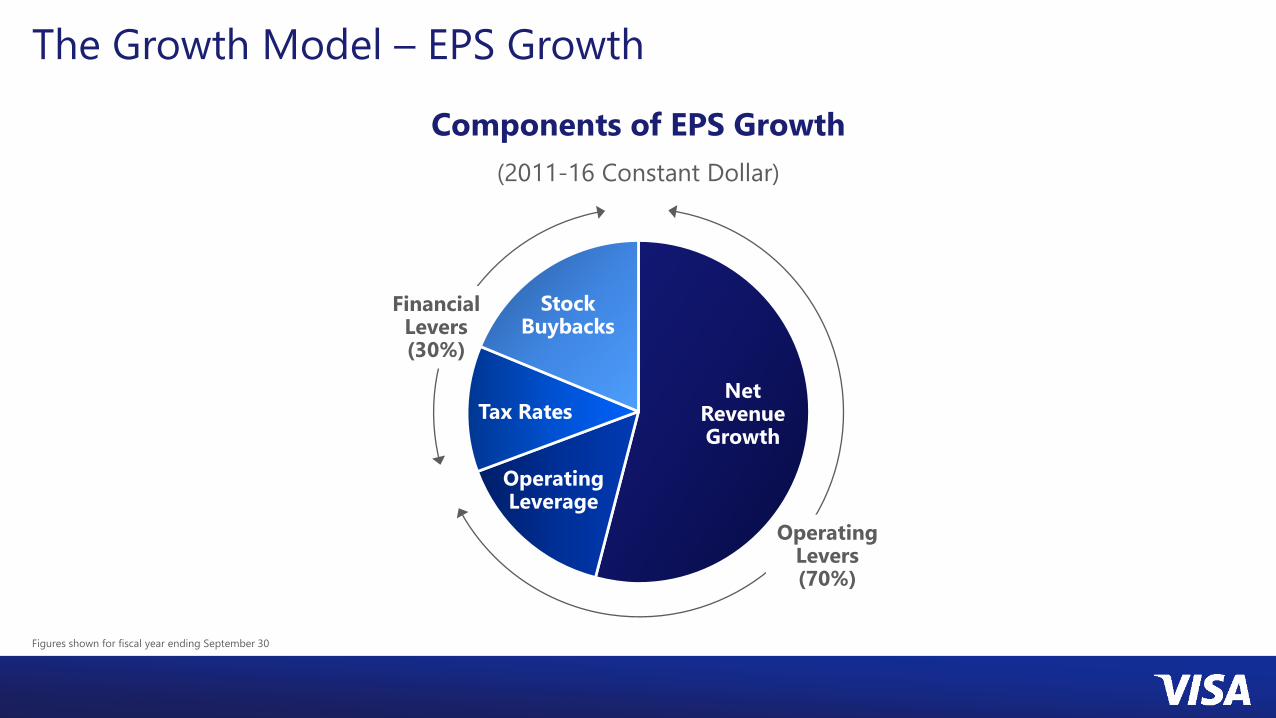

Operating Levers(70%)

Financial Levers(30%)

The Growth Model – EPS Growth

Figures shown for fiscal year ending September 30

Components of EPS Growth

(2011-16 Constant Dollar)

Stock Buybacks

Net Revenue Growth

Tax Rates

Operating Leverage

Capital Allocation Priorities

Invest to Fund Growth Initiatives

Pay 20% to 25% of EPS in Dividends

Return Excess Cash Through Stock Buybacks

Manage Capital Structure to Sustain Debt Ratings

1

2

3

4

P&L Cash InvestmentsCapital Investments

Capital Allocation Priorities

Figures shown for fiscal year ending September 30

Selective Acquisitions and Investments

Acquisitions

Minority

Investments

2010 2011 2012 2013 2014 2015 2016 2017

Europe

(2011-16)

~$3-3.5B

(2011-16)

$2.7B(2011-16)

~$24B

• Invest to fund growth programs

• Acquire or invest in new technologies / capabilities

Invest to Fund Growth Initiatives1

Payout Ratio (%)

Buybacks 1

Capital Allocation Priorities

1) Includes funding of U.S. litigation escrow account which dilute class B common stock through adjustment to the conversion rate (2011: $1.2B, 2012: $1.7B, 2014: $0.5B)2) Includes issuance of preferred stock convertible into approximately 79M of class A common stock in June 2016

Figures shown for fiscal year ending September 30

Dividends

Weighted Average Shares Outstanding (B) 2

12

20

2011 2016

2.82.4

2011 2016

20% - 25%

Payout Ratio

Deploy “excess”

cash to buyback

stock

(2011-16)

$5.4B

(2011-16)

$25.6B

Dividends2

Stock Buybacks3

1.51.4

1.3

12/31/15 9/30/16 3/31/17

4.0

6.8

Gross Debt / EBITDA (x LTM) 1 Debt Maturity Schedule ($16B)

Capital Allocation Priorities

1) EBITDA is a Non-GAAP metric defined as Operating Income plus Depreciation and Amortization, pro forma for the acquisition of Visa Europe and excluding one-time, non-recurring items

1.75

3.0

2.25

4.0

1.5

3.5

2017 2020 2022 2025 2035 2045

Current Rating: S&P (A+/A-1) / Moody’s (A1/P-1)

Target Leverage: 1.2x – 1.5x Gross Debt / EBITDA

Cash and Investments ($10.8B)

Required Backstop for Settlement

(At 3/31/17)

Manage Capital Structure to Sustain Debt Ratings4

Summary

• Sizeable global growth opportunity

• Visa has powerful assets to capture this opportunity

• Well defined strategy and tactics tailored by market

• Track record of revenue and EPS growth

• Disciplined capital allocation

• Well positioned to sustain superiorshareholder value creation

This presentation contains forward-looking statements within the meaning of the U.S. Private Securities Litigation Reform Act of 1995

that relate to, among other things, our future operations, prospects, developments, strategies, business growth and financial outlook.

Forward-looking statements generally are identified by words such as "believes," "estimates," "expects," "intends," "may," "projects,"

“could," "should," "will," "continue" and other similar expressions. All statements other than statements of historical fact could be

forward-looking statements, which speak only as of the date they are made, are not guarantees of future performance and are subject to

certain risks, uncertainties and other factors, many of which are beyond our control and are difficult to predict. We describe risks and

uncertainties that could cause actual results to differ materially from those expressed in, or implied by, any of these forward-looking

statements in our filings with the U.S. Securities and Exchange Commission, including our Annual Report on Form 10-K for the year

ended September 30, 2016 and our subsequent reports on Forms 10-Q and 8-K. Except as required by law, we do not intend to update

or revise any forward-looking statements as a result of new information, future events or otherwise.

***

Note: All brand names and logos are the property of their respective owners, are used for identification purposes only, and do not imply

product endorsement or affiliation with Visa. With the exception of slide titled “Acceptance Penetration Drives PCE Penetration,” PCE is

defined as Purchase PCE (does not include non-financial transactions).

Forward-Looking Statements