Vikram Nankani (Partner) - bcasonline.org Nankani (Partner) ... Constitutional Amendment Bill...

78

Vikram Nankani (Partner) Service Tax and VAT on Builders / Developers Bombay Chartered Accountants Society 1 22 nd August, 2012

Transcript of Vikram Nankani (Partner) - bcasonline.org Nankani (Partner) ... Constitutional Amendment Bill...

Vikram Nankani (Partner)

Service Tax and VAT on Builders / DevelopersBombay Chartered Accountants Society

1

22nd August, 2012

Finance Act, 2012 – Key Highlights

Tax Rates

Service Tax and Excise Duty – raised from 10% to 12%

GST – no definitive time-line for introduction

Negative list approach to tax services introduced – 17

categories of services covered in the negative list

Provision of Service Rules / Place of Supply Rules introduced

Harmonization of Service Tax and Excise Duty regimes –

Common Tax Code proposed

GST Network to be operational from August, 2012

Settlement Commission provisions extended to Service Tax

cases

Ordinary limitation period under Service Tax law increased to

18 months

No change in the rate of CST

2

Contents

Constitutional framework

Applicability of VAT

VAT on sale of flat, liable?

Judicial Precedents

Bombay High Court Order in case of MCHI

Circular issued basis decision of the High Court in MCHI

Payment of VAT

For the period 20.06.2006 to 31.03. 2010

For the period 1.4.2010 onwards

Applicability of Service tax

Scheme of taxation prior to 1 July, 2012

Taxation under the Negative List Regime

3

Constitutional Framework...

Taxes levied by Central Government and State Government(s)

Authority to levy a tax is derived from the Constitution of India

Which allocates power to levy various taxes between the Centre

and State

Article 265 of the Constitution which states that "No tax shall be

levied or collected except by the authority of law”

Article 246 of the Indian Constitution, distributes legislative

powers including taxation, between the Parliament of India and

the State Legislature

Schedule VII enumerates use of three lists;

List - I Where the parliament is competent to make laws

List - II Where only the state legislature can make laws

List - III Where both the Parliament and the State Legislature can

make laws upon concurrently

4

...Constitutional Framework

Union List State List Concurrent List

• Income Tax

• Custom Duty

• Excise Duty

• Corporation Tax

• Service tax

• Central Sales Tax

• Stamp duty in respect

of bills of exchange,

cheques, promissory

notes, etc

• Taxes on lands and

buildings

• Excise duty on

alcoholic liquor etc

• Entry tax

• Sales Tax

• Tolls

• Luxury Tax

• Stamp duty in respect

of documents other

than those specified in

the provisions of List I

• Stamp duties other

than duties or fees

collected by means of

judicial stamps, but

not including rates of

stamp duty

5

The constant blurring of taxing jurisdiction between the Centre and the

States has necessitated multiple Constitutional challenges

Constitutional Amendment Bill

Introduction of Article 246A in the Constitution:

“Parliament and the Legislature of every State, have power

to make laws with respect to goods

and services tax imposed by the Union or by that State

respectively.

Provided that Parliament has exclusive power to make laws

with respect to goods and services tax where the supply of

goods, or of services, or both takes place in the course of

inter-State trade or commerce.”

6

7

Goods Vs. Services

Lines between the taxation of Goods & Services is constantly blurring

Duality of Charge

Sr.

No.

Activity Customs

duty

Central /

State Excise

duty

Service

tax

VAT / CST

1. Intellectual Property

Services

2. Import of Designs, Technical

Know etc..

3. Works Contract

4. Construction Services

5. Manufacture of Products

liable to State Excise

Duality of charge – pre negative list

Applicability of VAT to

builders / developers

8

Scope of levy under MVAT…

9

Taxable event for the levy of VAT / Sales Tax is „sale‟.

Section 2(24) of the Maharashtra Value Added Tax, 2002 (“MVAT”), defines the

term „sale‟ to mean “a sale of goods made within the State for cash or deferred

payment or other valuable consideration, but does not include a mortgage,

hypothecation, charge or pledge; and the words "sell”, "buy" and "purchase", with all

their grammatical variations and cognate expressions, shall be construedaccordingly.”

Clause (b)(ii) of the Explanation to the above Section, while setting out transactions

that would qualify as „sale‟, provides as under:

Prior to 20.6.2006:

“(ii) the transfer of property in goods (whether as goods or in some other form) involved

in the execution of a works contract”.

W.e.f. 20.6.2006:

“(ii) the transfer of property in goods (whether as goods or in some other form) involved

in the execution of a works contract including, an agreement for carrying out for

cash, deferred payment or other valuable consideration, the building,

construction, manufacture, processing, fabrication, erection, installation, fitting out,

improvement, modification, repair or commissioning of any movable or immovable

property;”

…Scope of levy under MVAT

10

Owing to the amendment to the definition of the term „sale‟, operative w.e.f.

20.6.2006, the building and construction of an immovable property was brought

within the ambit of MVAT.

On 7.02.2007, basis the decision of the Supreme Court on M/s. K. Raheja

Development Corporation [141STC 298 (SC)], a Trade Circular was issued by theCommissioner of Sales Tax to clarify that:

Any transfer of property after 20.6.2006, irrespective of whether an agreement was signed

prior to that date, would be governed by the amended definition of „sale‟.

Tri-partite agreements between land-owners, developers and prospective buyers would

be covered by the amended definition of „sale‟.

If the agreement is entered into after the flat or unit is already constructed, then there

would be no works contract, but so long as an agreement is entered into before the

construction is complete, it would constitute a works contract.

On 9.07.2010, the Government of Maharashtra provided for a composition scheme,

applicable to registered dealers who undertake construction of flats, dwellings,

buildings or premises and transfer them in pursuance of an agreement along with

land or interest underlying the land.

Composition amount prescribed at 1% of the agreement amount or the value specified for

the purpose of Stamp Duty under the Bombay Stamp Act, 1958, whichever is higher.

VAT on sale of flats – Judicial precedents…

K. Raheja Development Corporation Vs. State of Karnataka [2006 (3)

STR 337 (SC)]

Arrangement

Specific arrangement to sell an undivided fractional share, right, title & interest in the

land to the intended buyer

Two separate contracts entered (i) sale of right in land (ii) construction of building

the developer , not being the owners of the land, had lien over the land and building

until the intended buyers pay the full consideration with regard to both land as well as

construction activity

Held that,

the Appellants are undertaking to build as developers for the prospective purchaser on

payment of a price. Therefore, it remains works contract as defined under the Act.

Also, if the agreement is entered into after the flat or unit is already constructed, then

there would be no works contract, but so long as agreement is entered into before the

construction is complete, it would be a Works Contract

Liable under VAT

11

VAT on sale of flats – Judicial precedents…

Assotech Realty Pvt. Ltd. vs. State of UP [2007 (7) STR 129 All.]

Arrangement

Developer issued allotment letter, specifying that terms and conditions of allotment are

subject to sale deed to be signed by parties in future

Under the said terms, the allottee agreed that no right will accrue in his favour until the

sale deed is executed

Further agreed, the petitioner shall remain the owner and the construction thereon and

no rights shall devolve upon the allottee by way of allotment even though any all

payment has been received by petitioner

Held:

Developer continues to remain the owner of apartments including all construction till

execution of the sale deed of such apartment, hence no works contract for construction

The petitioner not carrying out construction activity for and on behalf of the allottee as

the right ,title and interest in construction remained with petitioner at all times till

execution of sale deed of apartment as a whole

No liability to VAT

Distinguished K Raheja decision as the agreement in K Raheja provided that the developer will

construct for and on behalf of the person who agreed to purchase the flat. 12

…VAT on sale of flats – Judicial precedents…

Larsen and Toubro Ltd & Anr. vs. State of Karnataka [2008-(SC2)-

GJX-2195-(SC)]

Held:

If the ratio of K. Rahejs‟s case is accepted then there would be no difference

between the works contract and a contract for sale of chattel as a chattel

The case of K. Raheja Development needs re-consideration.

Matter referred to Larger Bench

13

…VAT on sale of flats – Judicial precedents…

14

Maharashtra Chamber of Housing Industry and Ors v. State of Maharashtra

and Ors [2012-VIL-35-BOM]

The constitutional validity of the amended definition of „sale‟, the Trade Circular

dated 7.02.2007 and the 1% Composition Scheme introduced w.e.f. 9.07.2010, was

challenged in a spate of writ petitions.

On behalf of the petitioners, it was contended as under:

The amendment was beyond the scope of the States power to tax under Sl. No. 54 of List

II of the Seventh Schedule to the Constitution.

In order to attract the application of Article 366(29A)(b), a contract would have to inter alia

involve a transfer of property in „goods‟ and immovable property does not constitute

„goods‟.

Consequent to the 46th Amendment to the Constitution, only a transfer of property in

goods involved in the execution of a works contract is taxable and a contract for the sale

of immovable property is not a works contract.

A works contract involves only two elements viz. (i) the transfer of property in goods; and

(ii) supply of labour and services. If a third element, the sale of immovable property, is

involved in the contract it does not constitute a works contract and hence to such a

contract, the legal fiction which is created by Article 366(29A) would not apply.

…VAT on sale of flats – Judicial precedents…

15

Agreements contemplated to be brought within the purview of the amended definition of

sale, per the Circular dated 07.02.2007, are simplicitor agreements for the sale of

immovable property.

Contracts governed by the Maharashtra Ownership Flats (Regulations of the Promotion of

Construction, Sale, Management and Transfer) Act, 1963 („MOFA‟) cannot be regarded

as a works contract, being agreements for the purchase of immovable property.

The MVAT ignores the concept of plurality of deemed sales. Where the developer is the

owner of the land, the promoter is both the owner and developer. Alternately, a developer

may enter into a development agreement with the owner of the land. When a promoter

appoints a sub contractor and gets a building constructed, that contract is a works

contract under Article 366(29A) and a transfer of the property in the goods involved in the

execution of the works contract takes place to the developer. That would be the first

deemed sale. When the developer enters into an agreement with a purchaser under the

MOFA, a sale of goods is not involved since that would amount to a second deemed sale

of the same goods which cannot be brought to tax. Once a promoter has appointed a sub

contractor the property passes to him as a promoter owner or to the owner, as the case

may be, where there is only a developer. Property has already passed on accretion and

the same transaction of deemed sale cannot be taxed twice.

An executory contract does not fit into the conception of a sale of goods within the

meaning of Entry 54 of the State List to the Seventh Schedule. The amended definition of

sale was beyond the scope of the States power to tax under Sl. No. 54 of List II of the

Seventh Schedule to the Constitution.

…VAT on sale of flats – Judicial precedents…

16

On behalf of the Revenue, it was contended as under:

An unduly restrictive or contrived meaning should not be given to the provisions of Article

366(29A) otherwise the object underlying the Constitutional amendment would be

defeated.

The purpose underlying the enactment of the deeming fiction in Article 366(29A) was to

override the limited definition of the expression „sale‟ in the Sale of Goods Act, 1930 and

to isolate the sale of goods element involved, inter alia, in a contract which is a works

contract. The amended definition of „sale‟ falls within the compass of Article 366(29A).

A works contract is a contract to execute works and encompasses a wide range of

contracts; it is not restricted to building contracts having only two elements viz. the sale of

material and goods and the supply of labour and services.

The well settled connotation of the expression „works contract‟ is that a building contract

may also involve in certain situations a sale of land. A works contract does not cease to

be such merely because any other obligation exists.

In an agreement which is governed by the MOFA, a conveyance of the interest in the flat

or at any rate an interest therein is created at the stage of the execution of an agreement.

The doctrine of accretion is always subject to a contract to the contrary. The provisions of

the MOFA contain a statutory stipulation to the contrary where the accretion to the

property enures to the benefit of the flat purchaser; and

The Trade Circular and the deduction schemes are only clarificatory in nature.

…VAT on sale of flats – Judicial precedents

17

Held:

Works contracts have numerous variations and it is not possible to accept the contention

either as a matter of first principle or as a matter of interpretation that a contract for work

in the course of which title is transferred to the flat purchaser would cease to be a works

contract.

The effect of the amendment to Section 2(24) is to clarify the legislative intent that a

transfer of property in goods involved in the execution of works contract including an

agreement for building and construction of immovable property would fall within the

description of a sale of goods within the meaning of the provision.

The constitutional validity of the provisions of the MVAT Act, 2002, as amended, is not

contingent upon any other statutory regulation of apartments under cognate legislation in

the State of Maharashtra.

Having regard to this statutory scheme, it is not possible to accept the submission

that a contract involving an agreement to sell a flat within the purview of the MOFA is

an agreement for sale of immovable property simplicitor.

The Constitutional validity of the amended definition of „sale‟, the Trade Circular dated

7.02.2007 etc. upheld.

Held Liable to VAT

Position as on date…

Trade circular No. 14T of 2012 dated 06.08.2012, issued by the

Commissioner of Sales Tax, Maharashtra

Issue pursuant to the Decision of Hon‟ble Bom. High Court in

MCHI case

States that developers are liable to pay tax under the MVAT Act,

w.e.f. 20.06. 2006

Provides for certain facilitation for obtaining registration, grant

administrative relief for unregistered period, and filing of returns

for the period from 20.06.2006

Issued FAQs on taxation of developers

18

Position as on date…

For the period 20.06.2006 to 31.3.2010

For payment of VAT, three options available

Composition Scheme under Section 42(3)

VAT payable @ 5% tax on the agreement value

Land deduction is not available

Input tax credit is available subject to the reduction of 4 per cent.

Actual Expense Method under Rule 58

the deduction of Labour and service charges is available on actual basis.

Land deduction is also available

Set-off available subject to the condition u/r 53 and 54

Standard Deduction Method U/r 58-

Deduction of land cost will be allowed

Thereafter 30% standard deduction from remaining amount as per proviso to

sub-rule1

Set-off available subject to the condition u/r 53 and 54

19

…Position as on date

For the period after 01.04.2010

In addition to the three option discussed in the earlier slide the

developer has one more option under Section 42(2A) read with

Notification No. VAT 1510/CR-65/Taxation-1 dated 09.07.2010

All agreements registered on or after 01.04.2010 covered

VAT payable @ 1% tax on agreement value.

No land deduction available

No input tax credit is available.

20

FAQs…

21

Questions Answers

Whether Credit available of input tax paid

on purchases of materials like cement, iron,

steel etc.

Yes, input tax credit available, if the taxes u/r 58

or u/s 42 (3) i.e. except 1% scheme

what point of time the VAT would be

payable

Taxability arises on agreement. Tax is levied as

and when the instalments become due and

payable or are received, whichever is earlier.

The agreement to sell the flat was

executed before 20.06.2006 and the

building was under construction and

possession is given after 20.06.2006.

Whether the VAT will apply in such case? If

yes how the sale value will be determined

for calculation of VAT? Whether the amount

received prior to 20.06.2006 will be exempt

from VAT

Yes. VAT will apply. It will be levied on value

received or receivable after 20th June, 2006

The point of liability when advances are

received and agreement is executed much

later.

Tax will be levied from the date of the

agreement. The amount of advance, as and

when it is adjusted towards the agreement

amount, will be taxed.

…FAQs

22

Questions Answers

Non-refundable deposits and other

charges under the agreement such as

electricity deposit, water charges, legal

charges, development charges etc. will

also form part of sale price for VAT?

No. The amounts which are received as

deposits will be deducted to the extent

such amounts are actually paid to other

authorities.

Whether VAT applicable be collected by

raising a debit note or the same should

be mentioned in the agreement itself?

Whether VAT should be collected on

each instalment or at one go uponexecution of the agreement

Yes. It can be collected by raising a

debit note. Specific mention in the

agreement is a choice of the contracting

parties. It should be collected as and

when the instalment becomes due.

What will be VAT the implications where

mere advances are received from buyers

and agreement for sale is not executed

with the buyer?

There is no tax liability.

Service tax- Erstwhile provisions

23

Commercial or Industrial Construction…

Commercial or Industrial Construction Services introduced

w.e.f. 10.09.2004

Taxable Service defined under Section 65(105)(zzq)

means any service provided or to be provided to any person by any

person in relation to commercial or industrial construction

Explanation Inserted w.e.f. 01.07.2010

The construction of a new building which is intended for sale,

wholly or partly, by a builder or any person authorised by the

builder before, during or after construction (except in cases for

which no sum is received from or on behalf of the prospective

buyer by the builder or the person authorised by the builder before

grant of completion certificate by the authority competent to issue

such certificate under any law for the time being in force)

shall be deemed to be service provided by the builder to the buyer

24

Commercial or industrial construction - defined under Section

65(25b) w.e.f. 16.06.2005

Construction of a new building or a civil structure or a part; or

Construction of pipeline or conduit; or

Completion and finishing services

such as glazing, plastering, painting, floor and wall tiling….,

construction of swimming pools, acoustic applications or fittings and

other similar services, in relation to building or civil structure; or

Repair, alteration, renovation or restoration of, in relation to,

building or civil structure, pipeline or conduit,

Which is-

Used / occupied / engaged, primarily in;

Commerce or industry, or work intended for commerce or industry

but does not include such services provided in respect of roads,

airports, railways, transport terminals, bridges, tunnels and dams

25

…Commercial or Industrial Construction

Construction of Complex Service introduced w.e.f.16.05.2005

Taxable Service defined under Section 65(105)(zzzh)

Means any service provided or to be provided to any person, by any

other person, in relation to construction of complex

Explanation inserted w.e.f. 01.07.2010

The construction of a complex which is intended for sale, wholly or

partly, by a builder or any person authorised by the builder before,

during or after construction (except in cases for which no sum is

received from or on behalf of the prospective buyer by the builder or

the person authorised by the builder before grant of completion

certificate by the authority competent to issue such certificate under

any law for the time being in force)

shall be deemed to be service provided by the builder to the buyer

26

Construction of Complex Service…

Construction of complex - defined under Section 65(30a) w.e.f.

16.6.2005

Construction of a new residential complex or a part thereof; or

Completion and finishing services in relation to a residential

complex

such as glazing, plastering, painting, ….,construction of swimming

pools, acoustic applications or fittings and other similar services; or

Repair, alteration, renovation or restoration of…., in relation to,

„residential complex‟

Section 65(91a) of the Act defines “residential complex”, to

mean any complex comprising of-

A building or buildings, having more than twelve residential units;

A common area; and

27

…Construction of Complex Service…

Any one or more of facilities or services

such as park, lift, parking space, community hall, common water

supply or effluent treatment system,

Located within a premises and the layout of such premises is

approved by an authority under any law for the time being in force,

but does not include a complex which is constructed by a person

directly engaging any other person for designing or planning of the

layout, and the construction of such complex is intended for

personal use as residence by such person

Explanation

“personal use” includes permitting the complex for use as residence

by another person on rent or without consideration

“residential unit” means a single house or a single apartment

intended for use as a place of residence

28

…Construction of Complex Service

Works Contract Services

Works Contract Services was introduced w.e.f. 01.06.2007

Taxable service defined under Section 65(105)(zzzza)

Means any service provided or to be provided to any person, by any

other person in relation to the execution of works contract, excluding

works contract in respect of roads, airports, railways, transport terminals,

bridges, tunnels and dams and the term “service provider” shall be

construed accordingly

Explanation – “Works Contract” means a contract wherein,-

Transfer of property in goods involved in the execution of such contract is

leviable to tax as sale of goods, and

Such contract is for the purpose of carrying out,-

Erection, commissioning or installation of plant, machinery…

Construction of a new building or a civil structure or a part therefof, or of a pipeline

or conduit, primarily for the purposes of commerce or industry; or

Construction of a new residential complex or a part thereof; or

Completion and finishing services, repair, alteration, renovation or restoration of, or

similar services

Turnkey projects including engineering, procurement and construction or

commissioning (EPC) projects29

Service tax on sale of flats – Judicial precedents

Magus Construction Pvt. Ltd. vs. Union of India [2008 (11) S.T.R. 225 (Gau.)]

when a builder, promoter or developer undertakes construction for its own self,in such cases, there would not be a question of providing „taxable service‟ byone person to another. The only transaction between the Petitioner and theprospective buyer is that on sale and purchase of flat. Any advance paid by theprospective buyer represents consideration received towards sale of flat tosuch prospective buyer and is not for obtaining service from the Petitioner

Held – Not liable to Service tax

M/s. G S Promoters vs. Union of India and another [2011 (21) S.T.R.

100 (P & H)]

There is element of service involved in a transaction of builder selling a flat,

whether or not service is involved has to be seen not only from the point ofview of builder but also from the point of view of service recipient

Constitutional validity of levy upheld

Held – Liable to Service tax

30

Service tax on sale of flats – Judicial precedents

Maharashtra Chamber of Housing Industry Vs Union of India

[2012-VIL-15-BOM-ST]

Upheld the constitutional validity of the Explanations added to the

taxing entries for „construction of complex service‟ and „commercial or

industrial construction service‟ by the Finance Act, 2010.

These Explanations brought to tax consideration received by a builder

from a buyer under an agreement of sale if any part of the

consideration was received prior to the issuance of the completion

certificate.

Held – Liable to Service tax

31

Payment of Service tax…

Various options available for payment of Service tax Commercial or Industrial Construction Service / Construction of

Complex Service

32

Particulars Option 1 Option 2 Option 3 Option 4

Rate of tax 3.399%of

the Gross

Amount

charged

(tax on 33% of

amount

charged)

2.575% of the Gross

Amount charged

(Not available if cost

of land separately

recovered)(tax on 25% of

amount charged)

10.3% of Gross

Amount less

value of goods

10.3% of Gross

Amount

charged

Availability

of Credit to

Service

provider

No credit

available

No credit available Capital Goods

& input service

available

Full credit of

Inputs, Capital

Goods & Input

Services

…Payment of Service tax

Works Contract Service

Options available to the contractors engaged by the Builders &

Developers

33

Particulars Option 1 Option 2

Rate of tax 4.12% of (Gross

Amount charged Less

VAT/Sales tax)

10.3% of [(Gross amount Less

VAT / Sales tax) Less value of

goods]

Availability of

Credit to Service

provider

Available for Capital

Goods & Input Services

Available for Capital Goods &

Input services

New Scheme of

Taxation

34

Paradigm shift – Negative List approach of taxing adopted

If an activity meets characteristics of “service”, it is taxable, unless:

- Specified in negative list

- Exempted vide a Notification

New charging section 66B which levies taxes on all services

other than those in the negative list, provided or agreed to be provided inthe taxable territory by one person to another

Taxable territory has been defined in Section 65B (52)

It means the territory to which the provisions of Chapter V of theFinance Act, 1994 apply i.e. whole of India excluding the state ofJammu and Kashmir

“Non-taxable territory” is defined in sub-section 35 ibid accordingly asthe territory other than the taxable territory.

Overview of the New Scheme

35

The erstwhile Service tax regime, focused on a selective taxation ofservices, by incremental additions to the list of taxable services

Negative list - Approach Defining what a service is, and

Tax all services, except for some specifically defined services which

would be kept outside the purview of the tax Taxation of services would be comprehensive, with some limited exceptions

Approach under the New scheme

Exempt/ Non-taxable

services

Taxable services

Selective taxation Comprehensive taxation

Taxable services

Exempt services

36

Change in provisions – Finance Act

Section 65 - Definitions

Section 65A - Classification

Section 66 – Charging Section

Section 66A – Charging Section in

case of import of services

Section 65B - Definition

Section 66B – Charging Section

Section 66F - Classification

Section 66C – Place of Provision

Section 66D – Negative List

Section 66E – Declared Services

Section 67A – Rate and Value

Following provisions will cease to

exist from a date to be notified

Following provisions will come into

force from a date to be notified

Section 68 – Payment of Service tax

Section 66C – Place of Provision

Old Provisions under Finance

Act

New Provisions under Finance

Act

37

Charging Section

Old charging provision (Section

66)

“There shall be levied a tax

(hereinafter referred to as the

service tax) at the rate of twelve

per cent. of the value of taxable

services referred to in sub-

clauses [ ] of clause (105) of

section 65 and collected in such

manner as may be prescribed.”

New charging provision (Section

66B)

“There shall be levied a tax

(hereinafter referred to as the

service tax) at the rate of twelve

per cent. on the value of all

services, other than those

services specified in the

negative list, provided or agreed

to be provided in the taxable

territory by one person to

another and collected in such

manner as may be prescribed.”

38

‘Service’

Means Includes But shall not include

- Any activity

- Carried out by

a person for

another

- For

consideration

-Includes a declared service

1. Renting of immovable property

2. Construction of a complex,

building, civil structure or a part

thereof; including a complex or

building intended for sale to a

buyer, wholly or partly except

where consideration is received

prior completion

3. Temporary transfer or permitting the

use or enjoyment of any intellectual

property right

4. Information technology software

services

5. Obligation to refrain from an act, or

to tolerate an act or a situation, or to

do an act

6. Service in relation to lease or hire of

goods and hire purchase

transactions

7. Execution of Works Contracts

8. Service portion in the serving of

foods or other article of human

consumption

-any activity that constitutes merely a

transfer in title of goods or immovable

property by way of sale, gift or in any

other manner;

-such transfer, delivery or supply of any

goods which is deemed to be a sale

within the meaning of clause (29A) of

Article 366 of the Constitution;

- a transaction in money or actionable

claim;

- any service provided by an employee

to an employer in the course of or in

relation to his employment;

- fees taken in any Court or a tribunal

established under any law for the time

being in force

- by a Constitutional authority under the

Indian Constitution or a member of an

Indian Legislature or a local self-

government in that capacity

39

Negative List of Services (indicative list)

Sr.

No.

Description of services which are not liable to Service Tax

1 Selling of space or time slots for advertisements other than

advertisements broadcast by radio or television. „Advertisement‟ has

been specifically defined.

2 Service by way of access to a road or a bridge on payment of toll

charges

3 Services by way of renting of residential dwelling for use as

residence. The term „renting‟ has been specifically defined.

4 Services by way of extending deposits, loans or advances in so far

as the consideration is represented by way of interest or discount or

inter se sale or purchase of foreign currency amongst banks or

authorised dealers of foreign exchange or amongst banks and such

dealers

40

Exempted Services... (indicative list)

Sr.

No.Description of service in respect of which exemption from payment of

Service Tax is granted

1 Services of- (a) renting of precincts of a religious place meant for general

public; or (b) conduct of any religious ceremony.

2 Services by way of erection or construction of original works pertaining to,-

(a) airport, port or railways;

(b) single residential unit otherwise as a part of a residential complex;

(c) low- cost houses up to a carpet area of 60 square metres per house in a

housing project approved by competent authority empowered under the

‘Scheme of Affordable Housing in Partnership’ framed by the Ministry of

Housing and Urban Poverty Alleviation, Government of India;

(d) post- harvest storage infrastructure for agricultural produce including a

cold storages for such purposes; or

(e) mechanised food grain handling system, machinery or equipment for

units processing agricultural produce as food stuff excluding alcoholic

beverages;41

Sr.

No.

Description of service in respect of which exemption from payment of Service Tax

is granted

3 Services provided to the Government or local authority by way of erection, construction,

maintenance, repair, alteration, renovation or restoration of -

(a) a civil structure .. meant predominantly for a non-industrial or non-commercial use;

(b) a historical monument, archaeological site or remains of national importance...

(c) a structure meant predominantly for use as (i) an educational, (ii) a clinical, or (iii) an

art or cultural establishment;

(d) canal, dam or other irrigation works;

(e) pipeline, conduit or plant for (i) drinking water supply (ii) water treatment (iii)sewerage

treatment or disposal; or

(f) a residential complex predominantly meant for self-use or the use of their employees

or other persons specified in the Explanation 1 to clause 44 of section 65 B of the said

Finance Act;

4 Services provided by way of erection, construction, maintenance, repair, alteration,

renovation or restoration of,-

(a) road, bridge, tunnel, or terminal for road transportation for use by general public;

(b) building owned by an entity registered under section 12AA of the Income tax Act,

1961(43 of 1961) and meant predominantly for religious use by general public;

(c) pollution control or effluent treatment plant, except located as a part of a factory; or

(d) electric crematorium;

...Exempted Services (indicative list)

42

Construction of Complex

Construction of a complex, building, civil structure or a part

thereof, including a complex or building intended for sale to a

buyer, wholly or partly, except where the entire consideration

is received after issuance of certificate of completion by a

competent authority

Circular 51/2/2012-STdated 10.02.2012 bearing F.No.332/13/2011-

TRU as also the Education Guide issued by the Board clarified the

taxability of the following arrangements in the context of existing

taxable service:

1. Tripartite model,

2. Redevelopment model,

3. Investment model,

4. Reconversion model,

5. BOT projects and

6. Joint development agreement model.

43

Tripartite Business Model…

Parties involved

Landowner

Builder/developer

Contractor

Transactions involved

Sale of land by the landowner

Not a taxable service

Construction service provided by the builder/developer

Consideration received by the builder/developer

From landowners – land/development rights

Other buyers – cash

44

…Tripartite Business Model…

Period Liable to Service

tax

Comments

Prior to 01.7.2010 No Vide Board Circular No. 108/02/2009-ST

dated 29.1.2009

Post 01.7.2010 Yes If any part of the consideration is received

before issuance of completion certificate

Valuation

Consideration for providing services to landowners is value of land /

developments rights

Value of land / development rights may not be ascertained

Therefore, value of flats given to land owners shall be equal to those

charged for similar flats by the builder/developer from other buyers

Service tax payable by the builder / developer when possession or right in the

property of the said flats is transferred to the landowner

i.e. by entering into a conveyance deed or an allotment letter

In other cases viz sale to other buyers, value will be determined in terms of

Section 67

Applicability of Service tax to builder / developer

45

Redevelopment including SRA…

Land owned by a society comprising of members

Each member entitled to his share by way of an apartment

Society / its members will give NOC for re-construction

The builder / developer makes new flats with same or different

carpet area for original flat owners

Additionally, builder / developer may also be involved in

Construction of additional flats for sale to other buyers

Arranging rental accommodation or rent payments for society

members for stay during the period of reconstruction

Payment of additional amount to the original owners of flats

In such case builder / developer receives

consideration from members of the society for land development

rights including the permission for additional number of flats

Consideration from other buyers in cash46

…Redevelopment including SRA

Valuation determined in accordance with Section 67(1)(i)

Flats given to other buyers

47

Activity Taxability Comments

Reconstruction undertaken by

society by directly engaging a

builder/developer

No Meant for personal use of

the members

Construction of additional flats

undertaken as part of the

reconstruction for non-members of

society prior

No Not taxable during the

period prior to 01.07.2010

Yes For the period post

01.07.2010

Taxability

Investment Model…

Project is offered to investor before commencement by

earmarking a specified area of construction / flat of a specified

area is allotted to the investors;

Investor may be promised a fixed rate of interest

Options to investor

Exit on receipt of the amount invested along with interest; or

Re-sell the said allotment to another buyer; or

Retain the flat for his own use

Taxability

Investment amount shall be treated as consideration paid in

advance for construction services by builder / developer

Liable to service tax48

…Investment Model

If investor exits, before / after issuance of completion certificate

Builder / Developer entitled to take credit under Rule 6(3) of the

Service Tax Rules, 1994, to the extent it has refunded the original

amount

If the builder/developer resells the flat before the issuance of

completion certificate

Liable to service tax

49

Conversion Model

Conversion of any hitherto untaxed construction / complex / part

thereof into a building or civil structure to be used for commerce

or industry, after lapse of a period of time

Mere change in use of the building does not involve any taxable

service, unless conversion falls within the meaning of

commercial or industrial construction service

50

Build-Operate-Transfer (BOT) Projects…

Parties involved

Government or its agency

Concessionaire (Builder / Developer himself or independent)

Users

Transactions involved

At first level, Government or its agency transfers the „right to use‟

and / or „right to develop‟ to the Concessionaire

For a specified period – usually 30 years

For construction of a building or furtherance of business or commerce

Consideration paid to Government

Upfront lease amount

Annual charges

Government or its agency provides renting of immovable property

service

Liable to service tax 51

…Build Operate Transfer (BOT) Projects

Under such arrangement, Concessionaire is not a service provider

since such construction has been undertaken by him on his own

account and he remains the owner of the building during the

concession period.

No Service tax on the Concessioner

At second level, Concessionaire may engage a contractorService tax payable by the contractor on the construction service

provided by the Contractor to the Concessionaire

No Service tax is payable if the activity is specifically excluded

At third level, Concessionaire enters into agreement with several

users for commercial exploitation of the buildingConcessionaire is the service provider providing taxable services

„Renting of immovable property service‟, „business support

service‟, „management, maintenance or repair service‟ etc

Liable to service tax

52

Joint Development Agreement Model…

Landowner and builder / developer join hands

Create a new entity / SPV; or

Operate as an unincorporated association on partnership / joint /

collaboration basis

Mutuality of interest

Common risk / profit

New entity undertakes construction on behalf of landowner and

builder / developer

Circular 148/17/2011-ST dated 13/12/2011 shall apply mutatis

mutandis, particularly paragraphs 7,8 and 9(Clarification on levy of

service tax on distributors/sub-distributors of films & exhibitors of

movie)

Where a distributor enters into an arrangement with an exhibitor to share

revenue / profits and not provide the service on P2P basis, a new entity

emerges, distinct from its constituents and therefore such activities would

be taxable

Service tax payable under the Joint Development arrangement53

Non-requirement of Completion Certificate

Requirement of completion certificates waived /required in

certain States for certain specified types of buildings

Taxability

Equivalent of completion certificate used as the dividing line

between service and sale

Authority competent to issue completion certificate includes an

architect or chartered engineer or licensed surveyor – Service Tax

(Removal of Difficulty) Order, 2010, dated 22/06/2010

54

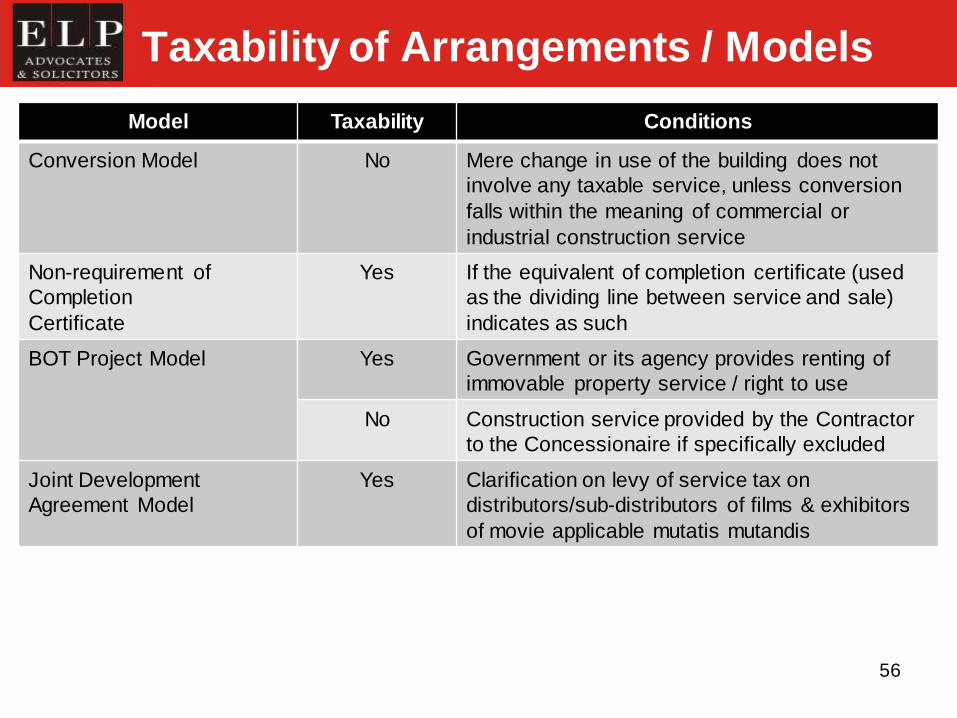

Taxability of Arrangements / Models

Model Taxability Conditions

Tripartite Business Model No Prior to 01.07.2010 - Vide Board Circular No.

108/02/2009-ST dated 29.1.2009

Yes If any part of the consideration is received before

issuance of completion certificate

Redevelopment including

SRA

No Reconstruction undertaken by society by directly

engaging a builder / developer-Meant for

personal use of the members

No Construction of additional flats undertaken as

part of the reconstruction for non-members of

society during the period prior to 01.07.2010

Yes Construction service provided by the builder /

developer for non-members of society for the

period post 01.07.2010

Investment Model Yes If investment amount treated as consideration

paid in advance

Yes If builder / developer resells the flat before the

issuance of completion certificate

55

Taxability of Arrangements / Models

Model Taxability Conditions

Conversion Model No Mere change in use of the building does not

involve any taxable service, unless conversion

falls within the meaning of commercial or

industrial construction service

Non-requirement of

Completion

Certificate

Yes If the equivalent of completion certificate (used

as the dividing line between service and sale)

indicates as such

BOT Project Model Yes Government or its agency provides renting of

immovable property service / right to use

No Construction service provided by the Contractor

to the Concessionaire if specifically excluded

Joint Development

Agreement Model

Yes Clarification on levy of service tax on

distributors/sub-distributors of films & exhibitors

of movie applicable mutatis mutandis

56

Payment of Service tax

Notification 26/2012-ST dated 20.06.2012

Taxable Service ST payable on

Percentage

value

Conditions

Construction of a complex,

building, civil structure or a part

thereof, intended for a sale to a

buyer, wholly or partly except

where entire consideration is received after issuance of

completion certificate by the

competent authority

25% (i) CENVAT credit on inputs used

for providing the taxable service

has not been taken under the

provisions of the CENVAT Credit

Rules, 2004. (ii)The value of land is included

in the amount charged from the

service receiver.

57

Prior to 01.07.2010 Post 01.07.2010 Taxability Comments

- Agreement to sell

- Complete Construction

- Completion certificate

(certificate) received

- Payment x Taxable event is the

construction

- Agreement to sell

- Complete Construction

- Certificate received

- Payment before

certificate received

x Taxable event is the

construction

- - - Complete Construction

- Certificate received

- Payment after certificate

x Payment post receipt of

certificate

- - - Complete Construction

- Payment prior to receipt

of certificate

√ -

- 60% construction

complete

- Payment for 60%

construction made

- Balance 40%

construction

- Payment for 40%

construction prior to

receipt of certificate

√ Service tax would be

payable on the payment

for the balance 40%

construction completed

after 01.07.2010

Taxability during transition of law…

58

Prior to 01.07.2010 Post 01.07.2010 Taxability Comments

- 60% construction

complete

- Balance 40%

construction

- Payment for 100%

construction after

receipt of certificate

x -

- 60% construction

complete

- Balance 40%

construction

- Payment for 100%

construction prior to

receipt of certificate

√

- Agreement to sell

- 60% construction

complete

- Payment for 60%

construction

made

- Balance 40%

construction

- Payment for 40%

construction after

receipt of certificate

√ No clarity has been provided in

circumstances where balance

payment for construction post

01.07.2010 is made after

certificate received.

…Taxability during transition of law

59

Works Contract…

In terms of Article 366 (29A) of the Constitution of India transfer of property

in goods involved in execution of works contract is deemed to be a sale of

such goods.

A works contract can be segregated into a contract of sale of goods and

contract of provision of service.

Supreme Court decision in BSNL„s case [2006(2) STR 161 (SC)]

Service portion in execution of a works contract included in declared list of

services

Works contract has been defined in section 65B of the Act as a contract

wherein transfer of property in goods involved in the execution of such contract

is leviable to tax as sale of goods and such contract is for the purpose of

carrying out construction, erection, commissioning, installation, completion,fitting out, improvement, repair, renovation, alteration of any building or

structure on land or for carrying out any other similar activity or a part thereof in

relation to any building or structure on land.

Value of service portion in works contracts will be determined in terms of the

Service Tax (Determination of Value) Rules, 2006 (“Valuation Rules”).

60

…Works Contract…

Gross amount includes Gross amount does not include

Labour charges for execution of the works Value of transfer of property in goods involved

in the execution of the said works contract.

Note:

Where Value Added Tax has been paid on the

actual value of transfer of property in goods

involved in the execution of the works contract,

then such value adopted for the purposes of

payment of Value Added Tax, shall be taken as

the value of transfer of property in goods

involved in the execution of the said works

contract.

Amount paid to a sub-contractor for labour and

services

Charges for planning, designing and architect‟s

fees

Charges for obtaining on hire or otherwise,

machinery and tools used for the execution of

the works contract

Cost of consumables such as water, electricity,

fuel, used in the execution of the works

contract

Cost of establishment of the contractor

relatable to supply of labour and services and

other similar expenses relatable to supply of

labour and services

Value Added Tax (VAT) or sales tax, as the

case may be, paid, if any, on transfer of

property in goods involved in the execution of

the said works contract

Profit earned by the service provider relatable

to supply of labour and services

61

…Works Contract…

Is there any simplified scheme for determining the value of

service portion in a works contract?

Yes. The scheme is contained in the revised Rule 2A of the

Valuation Rules.

As per this scheme the value of the service portion, where value has

not been determined in the manner as explained in earlier slide, shall

be determined in the manner explained in the table below -

Where works contract is for… Value of the service portion shall be…

(i) execution of original works forty percent of the total amount charged for

the works contract

(iii) works contracts, other than contracts for

execution of original works, including contracts

for completion and finishing services such as

glazing, plastering, floor and wall tiling,

installation of electrical fittings

sixty percent of the total amount charged for

the works contract

(iii) Works contract for maintenance or repair

or reconditioning or restoration or servicing of

any goods

seventy percent of the total amount charged

for the works contract

62

…Works Contract…

“total amount” means the sum total of the gross amount charged

for the works contract and the fair market value of all goods and

services supplied in or in relation to the execution of the works

contract, whether or not supplied under the same contract or

any other contract, after deducting-

(i) the amount charged for such goods or services, if any; and

(ii) the value added tax or sales tax, if any, levied thereon:

Original works‟ means :

all new constructions;

all types of additions and alterations to abandoned or damaged

structures on land that are required to make them workable;

63

…Works Contract…

Person liable to pay Service tax

Vide Notification 30/2012-S.T. dated 20.06.2012 (applicable w.e.f.

01.07.2012), in respect of Works Contract service:

Both the service provider and service recipient are required to discharge 50%

of the Service tax liability

Applicable only where the service provider is individual or HUF or

partnership firm or LLP or AOP and the service recipient is a body

corporate

In other cases, service provider is required to apply and recover tax

64

…Works Contract…

Issues

Whether contracts for painting of a building, repair of a

building, renovation of a building, wall tiling, flooring be

covered under „works contract‟?

Yes, if such contracts involve provision of materials as well

How is the value of goods or services supplied free of cost be

determined to arrive at the total amount charged for a works

contract?

If the value of goods and services supplied free of cost for use in

or in relation to execution of a works contract is not

ascertainable, the same shall be determined on the basis of the

fair market value of the goods or services that have close

resemblance to goods made available

65

…Works Contract…

Is duty paid on any goods, property in which is transferred (whether

as goods or in some other form) in the execution of works contract,

available as Cenvat Credit?

No. Such Cenvat Credit is not available, irrespective of the fact

that the value of service portion is determined in the manner

explained above, since such goods are not inputs for the service

provided. However, the goods not forming part of such transfer

will be eligible for input tax credit subject to the provisions of the

Cenvat Credit Rules, 2004 including the provisions relating to

reversal of credits contained in rule 6 of the said rules.

66

…Works Contract

Duality of taxes (Works Contract / Construction services)

Differing schemes of abatements under VAT Laws and Service Tax law

Original Works, Contract value = Rs. 100/-

Service Tax @12.36% on Rs. 40/- (abatement of 60%)

VAT @ 14.5% on Rs. 75/- (abatement of 25% under VAT Laws)

Effective value of contract subjected to Indirect Taxes is Rs.115/- as against an

actual realization of Rs. 100/-

Taxing impact further aggravated for other than Original Works on account of

the Service tax abatement being only 40%, therefore effective value of contract

subject to Indirect Taxes is Rs.135/-

Credits of Excise Duty paid on goods not available on account of conditions of the

abatement scheme

Results in increasing the tax cost

Manner of applying VAT - Levy of VAT on the Service tax portion in the

transaction

Service tax paid or payable forms part of sale value and hence liable to Service

tax - DDQ-11-2007/Adm-3/16/B-1 dated 20.10.2012

This position seems incorrect. The intention of legislature would not be to levy tax

on tax 67

Service tax- Renting of immovable property

68

Renting of Immovable Property…

Renting of Immovable Property introduced w.e.f.16.05.2005

Taxable service defined under Section 65(105)(zzzz)

Means any service provided or to be provided to any person, by any

other person, by renting of immovable property or any other service in

relation to such renting, for use in the course of or, for furtherance of,

business or commerce

Explanation 1 – Immovable Property includes

Building and a part of a building, and the land appurtenant thereto;

Land incidental to the use of such building or part of a building;

The common or shared areas and facilities relating thereto;

In case of a building located in a complex or an industrial estate, all

common areas and facilities relating thereto, within such complex or

estate, and

Vacant land, given on lease or license for construction of building or

temporary structure at a later stage to be used for furtherance of

business or commerce

69

…Renting of Immovable Property…

But does not include

Vacant land solely used for agriculture, ….;

Vacant land, whether or not having facilities clearly incidental to the

use of such vacant land;

Land used for educational, sports… parking purposes; and

Building used solely for residential purposes and buildings used for

the purposes of accommodation, including hotels ….

Explanation 2 – Immovable property partly for use in the course or

furtherance of business or commerce and partly for residential or

any other purposes shall be

deemed to be immovable property for use in the course or

furtherance of business or commerce

70

…Renting of Immovable Property

Renting of immovable property is defined under Section 65(90a)

Includes renting, letting, leasing, licensing or other similar

arrangements of immovable property for use in the course or

furtherance of business or commerce

Does not include

Renting of immovable property by a religious body; or

Renting of immovable property to an educational body …;

Explanation 1 – “for use in the course or furtherance of business or

commerce” includes use of immovable property as factories, office

buildings, warehouses, theatres, exhibition halls and multiple-use

buildings

Explanation 2 – “renting of immovable property” includes allowing or

permitting the use of space in an immovable property, irrespective of the

transfer of possession or control of the said immovable property

71

Home Solutions Retail India Ltd vs. UOI [2009 20 STT 129 (Delhi)]

Levy held unconstitutional - Renting of immovable property itself does not entail

any value addition

Special leave petition filed in the Supreme Court – pending

Finance Act 2010, with retrospective effect, amended the definition of

taxable service to explicitly provide that renting per se is a taxable service

The said amendment was challenged by a writ in Home Solutions Retail India Ltd. vs. UOI [2010 26 STT 418 (Delhi)]

Stay granted from recovery of Service tax

To be decided after instructions from Supreme Court

Similar challenge in other High Courts including Bombay

Shubh Timb Steels Ltd. vs. UOI [2010 (20) S.T.R. 737 (P & H)]

Upheld the constitutional validity and retrospective levy

Very recently Delhi HC in Home Solution(2) continued the stay granted

earlier

Taxing entry contained the word „services to be provided…‟, whereas in Home

solution(1) it has been concluded that renting does not constitute a service

Considered the P&H HC order

Service tax on renting of immovable property -

position in proceedings

72

Service tax on renting of immovable property - position in

proceedings

Delhi High Court in the case of Home Solutions Retail Vs UOI while

examining the issue of constitutionality observed

On the question of penalty due to non-payment of tax, it is open to the

Government to examine whether any waiver or exemption can be

granted

Subsequently, in the matter of Retailers Assn. of India Vs Union of

India, the Hon‟ble Apex court, had ruled on October 14, 2011, that

litigants should pay 50% of the arrears within six months in three equated

instalments

For the balance, solvent surety should be furnished

Proposed that penalty may be waived who pay the service tax due on

renting of immovable property service (as on the sixth day of March,

2012), in full along with interest within six months

Section 80A is being introduced for this purpose

Those who fail to avail the benefit will be treated as if this section did not

exist

73

Renting of immovable

property - Taxability

under the New

Scheme

74

Renting of immovable property…

Renting has been defined in section 65B as

allowing, permitting or granting access, entry, occupation, usage

or any such facility, wholly or partly, in an immovable property with

or without the transfer of possession or control of the said

immovable property and includes letting, leasing, licensing or

other similar arrangements in respect of immovable property‟

Immovable property has not been defined in the Act

definition of immovable property in the General Clauses Act, 1897

will be applicable which defines immovable property to include

land, benefits to arise out of land, and things attached to the earth,

or permanently fastened to anything attached to the earth.

75

…Renting of immovable property…

Renting of certain kinds of property not liable to Service tax

Covered under the negative list

renting of vacant land, with or without a structure incidental to its use,

relating to agriculture

renting of residential dwelling for use as residence

renting out of any property by Reserve Bank of India

renting out of any property by a Government or a local authority to all

non-business entity.

Exemptions in respect of renting of immovable property

Threshold level exemption up to Rs. 10 lakh.

Renting of precincts of a religious place meant for general public

Renting of a hotel, inn, guest house, club, campsite or other

commercial places meant for residential or lodging purposes,

having declared tariff of a room below rupees one thousand per

day or equivalent is exempt

76

…Renting of immovable property

Sl.

No.

Nature of Activity Taxability

1. Renting of property to educational body Chargeable to service tax; no exemption

2. Renting of vacant land for animal

husbandry or floriculture

Not chargeable to service tax as it is

covered in the negative list entry relating

to agriculture

3. Permitting use of immoveable property

for placing vending/dispensing machines

Chargeable to service tax as permitting

usage of space is covered in the definition

of renting

4. Allowing erection of communication tower

on a building for consideration

Chargeable to service tax as permitting

usage of space is covered in the definition

of renting

5. Renting of land or building for

entertainment or sports

Chargeable to service tax as there is no

specific exemption

6. Renting of theatres by owners to film

distributors

Chargeable to service tax as the

arrangement amounts to renting of

immovable property.

Applicability of Service tax on certain activities of renting

77

Mumbai1502, A Wing, Dalamal Towers, Nariman Point, Mumbai 400 021

Phone: + 91 22 6636 7000, Fax: + 91 22 6636 7172, Email: [email protected]

Delhi405-406, 4th Floor, World Trade Centre, Barakhamba Lane, New Delhi 110 001

Phone: + 91 11 4152 8400, Fax: + 91 11 4152 8404, Email: [email protected]

Ahmedabad801, Abhijeet III, Mithakali Six Roads, Ellisbridge, Ahmedabad-380 006

Phone: +91 79 6605 4480 / 8, Fax: +91 79 6605 4482, Email: [email protected]

Pune Suyog Fusion, 7th Floor, No.1, 97 Dhole Patil Road, Nr. Ruby Hall Clinic, Pune 411 001

Tel:+91 20 4146 7400 / 02 Fax:+91 20 4146 7499Email: [email protected]

![Priest Rapids P08 GCB Incident WSU Relay School...iaw1 ibw1 icw1 iaw2 ibw2 icw2 iaw3 ibw3 icw3 iaw4 in icw4 246a 246 out 4 = alarm [6] IN 1 = GEN 7 52b](https://static.fdocuments.us/doc/165x107/6123a4d483bd92352f24065a/priest-rapids-p08-gcb-incident-wsu-relay-school-iaw1-ibw1-icw1-iaw2-ibw2-icw2.jpg)