Black Gold & Fool’s Gold: Speculation in the Oil Futures Market

Upload

jeremy-loganCategory

view

221download

1

VII: Futures

22: Speculation

Chapter 22: Hedges, Speculation, and Arbitrage © Oltheten & Waspi 2012

Futures

Hedge use futures to reduce risk on an existing

position Speculate

use futures to take on risk in the hope of making a profit

Arbitrage Use the difference between spot and futures

prices to generate risk-free profit

Chapter 22: Hedges, Speculation, and Arbitrage © Oltheten & Waspi 2012

Speculation Susan

50,000 bushels of soybeans costs $210,000.

The price of soybeans is going up

$

$$$50,000 bushels in soybeans

futures costs $8100.

Chapter 22: Hedges, Speculation, and Arbitrage © Oltheten & Waspi 2012

Speculation

420

431

-$40,000

-$30,000

-$20,000

-$10,000

$0

$10,000

$20,000

$30,000

$40,000

360 380 400 420 440 460 480

Price (Soybeans Spot)

Profi

t

Soybean Futures

Soybeans

Chapter 22: Hedges, Speculation, and Arbitrage © Oltheten & Waspi 2012

179.01%

9.52%431

-500%

-400%

-300%

-200%

-100%

0%

100%

200%

300%

400 410 420 430 440 450 460

Price (Soybeans Spot)

Retu

rn

Soybean Futures

Soybeans

9.52%1$210,000$230,000

179.01%$8,100

$14,500

Speculation

Chapter 22: Hedges, Speculation, and Arbitrage © Oltheten & Waspi 2012

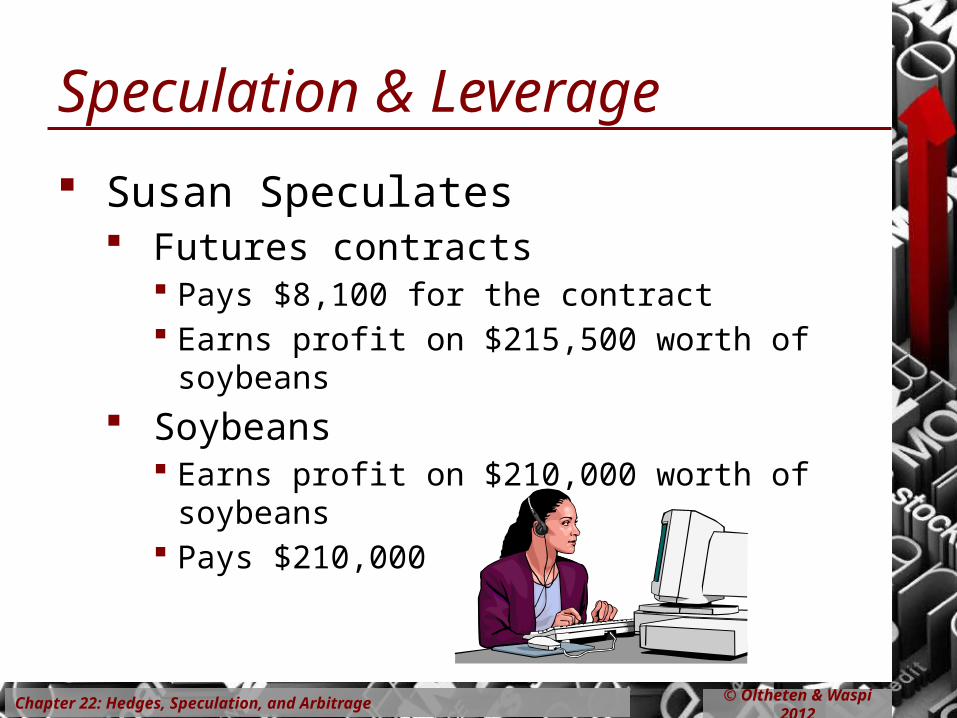

Speculation & Leverage

Susan Speculates Futures contracts

Pays $8,100 for the contract Earns profit on $215,500 worth of soybeans

Soybeans Earns profit on $210,000 worth of soybeans Pays $210,000

Chapter 22: Hedges, Speculation, and Arbitrage © Oltheten & Waspi 2012

Speculation

Let’s really speculate.Let’s use derivatives

Chapter 22: Hedges, Speculation, and Arbitrage © Oltheten & Waspi 2012

Derivative Securities

A derivative is a financial instrument whose underlying security is another financial instrument. Soybean Futures

The underlying security is soybeans. Soybeans are real so soybean futures are NOT Derivatives

Chapter 22: Hedges, Speculation, and Arbitrage © Oltheten & Waspi 2012

Derivatives

Shares of Exxon Mobil The underlying security is Exxon Mobil. Exxon Mobile

is real so Exxon Mobile shares are NOT Derivatives.

Exxon Mobil100

Shares

Exxon Mobil

Chapter 22: Hedges, Speculation, and Arbitrage © Oltheten & Waspi 2012

Derivatives

Exxon Mobile Stock Options The security underlying the option is a share of Exxon

Mobile. Shares are financial instruments; the options on the shares are derivatives.

Exxon Mobil100

Shares

Exxon Mobil

OPTION

100Shares

Exxon Mobil

Chapter 22: Hedges, Speculation, and Arbitrage © Oltheten & Waspi 2012

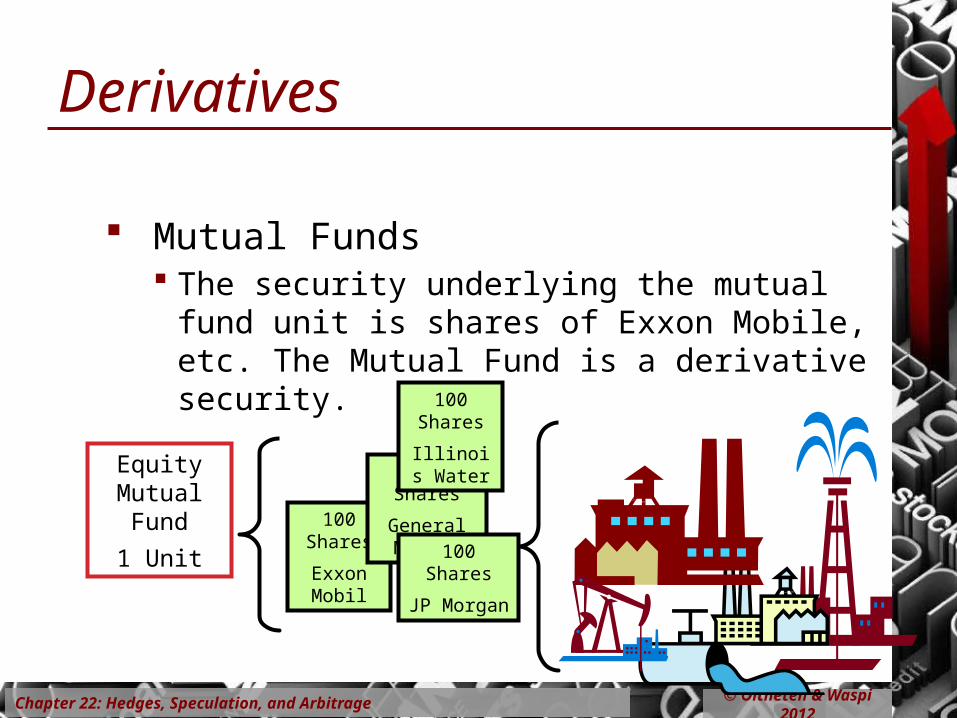

Derivatives

Mutual Funds The security underlying the mutual fund unit is shares

of Exxon Mobile, etc. The Mutual Fund is a derivative security.

100Shares

Exxon Mobil

EquityMutualFund

1 Unit

100Shares

General Motors100

Shares

JP Morgan

100Shares

Illinois Water

Chapter 22: Hedges, Speculation, and Arbitrage © Oltheten & Waspi 2012

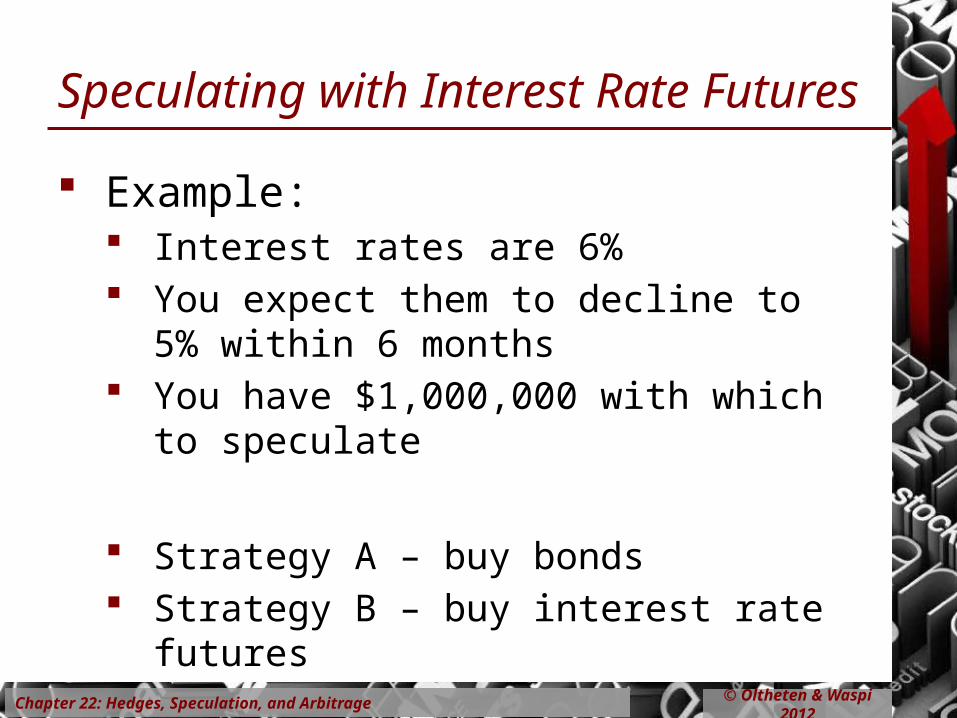

Speculating with Interest Rate Futures

Speculation on interest rates is easier in the futures market than in the spot market. It is as easy to sell as to buy Investments are leveraged

Chapter 22: Hedges, Speculation, and Arbitrage © Oltheten & Waspi 2012

Speculating with Interest Rate Futures

Example: Interest rates are 6% You expect them to decline to 5% within 6

months You have $1,000,000 with which to speculate

Strategy A – buy bonds Strategy B – buy interest rate futures

Chapter 22: Hedges, Speculation, and Arbitrage © Oltheten & Waspi 2012

Buy $1m 20 year 6% T-bonds @100-00 -$1,000,000

Strategy A: Buy T-Bonds

Chapter 22: Hedges, Speculation, and Arbitrage © Oltheten & Waspi 2012

Buy $1m 20 year 8% T-bonds @100-00 -$1,000,000

Six months later I am right7%

I am wrong9%

Coupon [$1,000,000 * .06 * ½] +$30,000. +$30,000.

Sell 19½ year 6% T-Bonds at 5% [112:12] +$1,123,750.

Sell 19½ year 6% T-Bonds at 7% [89:14] +$894,375.

Final Market Value $1,153,750. $924,375.

Rate of Return (over six months) +15.375% -7.5625%

LJ

Strategy A: Buy T-Bonds

Chapter 22: Hedges, Speculation, and Arbitrage © Oltheten & Waspi 2012

T-Bond Futures

The T-Bond future is defined as a contract to deliver the equivalent of a $100,000 20 year 6% T-Bond

Initial margin is $2,500 per contract

Chapter 22: Hedges, Speculation, and Arbitrage © Oltheten & Waspi 2012

Buy 400 6 month T-Bond Futures @ 100-00[-$40,000,000] margin:

-$1,000,000

Strategy B: T-Bond Futures

Chapter 22: Hedges, Speculation, and Arbitrage © Oltheten & Waspi 2012

Buy 400 6 month T-Bond Futures @ 100-00[-$40,000,000]

margin: -$1,000,000

Six months later I am right5%

I am wrong7%

Sell 400 T-Bond futures @ 5% [112:12]Profit:

Margin:

Sell 400 T-Bond futures @ 9% [89:31]Profit:

Margin:

Rate of Return (over six months)

LJ

Strategy B: T-Bond Futures

Futures IV