· Web viewQUESTION 3 2 August 2009 BSP Limited offered 400,000 shares to the public $1 each,...

35

REVISION QUESTIONS UNIT 4 QUESTION 1 Wonderful Ltd issues a prospectus on 10 June offering 1,000,000 50 cents ordinary shares to the general public. Applications were receive for all the shares by 20 July and the directors allotted the shares on 24 July. Preliminary expenses were paid on the day the shares were allotted and amounted to $10,000. Required: Prepare the general ledger entries to record the above events. QUESTION 2 On 1 July, the directors of Annie Ltd offered for subscription 200,000 $1 ordinary shares payable in full on application. All application moneys were received by 31 July and the directors proceeded to allotment on 3 August. Required: a) Record the relevant events in the journals of Annie Ltd b) Prepare the Balance Sheet at 3 August QUESTION 3 2 August 2009 BSP Limited offered 400,000 shares to the public $1 each, payable in full on application. 31 August 2009 The share issue closed 9 September 2009 All shares were allotted 30 September 2009 The company paid $2,000 in share issue costs Required: Prepare the journal entries to record the share issue. 1

Transcript of · Web viewQUESTION 3 2 August 2009 BSP Limited offered 400,000 shares to the public $1 each,...

REVISION QUESTIONS UNIT 4

QUESTION 1

Wonderful Ltd issues a prospectus on 10 June offering 1,000,000 50 cents ordinary shares to the general public.

Applications were receive for all the shares by 20 July and the directors allotted the shares on 24 July.

Preliminary expenses were paid on the day the shares were allotted and amounted to $10,000.

Required:Prepare the general ledger entries to record the above events.

QUESTION 2

On 1 July, the directors of Annie Ltd offered for subscription 200,000 $1 ordinary shares payable in full on application. All application moneys were received by 31 July and the directors proceeded to allotment on 3 August.

Required:a) Record the relevant events in the journals of Annie Ltdb) Prepare the Balance Sheet at 3 August

QUESTION 3

2 August 2009BSP Limited offered 400,000 shares to the public $1 each, payable in full on application.

31 August 2009The share issue closed

9 September 2009All shares were allotted

30 September 2009The company paid $2,000 in share issue costs

Required:Prepare the journal entries to record the share issue.QUESTION 4

July 2021Achieve Limited was incorporated.

August 2024On 2 August 2024 the company offered 260,000 ordinary shares to the public. The shares of $2.00 each were payable in full on application.

1

On 19 August 2024 the share offer closed with applications received for all shares offered.

On 31 August 2024 the shares were allotted to the new shareholders. Share issue costs were $3,100 cash. The share issue costs were closed to share capital.

November 2026On 1 November 2026 the company made an issue of 1 for 5 bonus shares, of $2.00 each, out of a general reserve.

1 July 2027

The retained earnings of the company were $41,308.

February 2028

The company paid an 8 cents per share interim dividend.

30 June 2028The directors declared a 17 cents per share ordinary dividend (to be voted on at the annual general meeting to be held in November 2028).

An amount of $3,000 was transferred to a general reserve.

The balance of retained earnings on 30 June 2028 was $19,150 credit.

Required

1 Prepare the general journal entries to record the issue of shares in 2024 including the write off of the share issue costs.

2 Prepare the general journal entry to record the bonus share issue in 2026.

3 Prepare the retained earning ledger account for the year ended 30 June 2028.QUESTION 5

Howell Ltd. manufacture and sell pesticides for commercial use. The account balances for this business, sorted in alphabetical order, are provided below:

Howell Ltd Account balances as at 30 June 2010

$Accounts payable 18,000Accounts receivable 217,000Accrued expenses 7,200Accumulated depreciation – equipment

75,000

Accumulated depreciation – vehicles 55,000

2

Allowance for doubtful debts 12,000Bank loan (due 27 September 2010) 65,000Cash at bank 135,000Cost of sales 250,000Current tax liability 90,000Equipment 275,000General reserve 120,000Income tax expense 90,000Inventory 225,000Land (at cost) 600,000Ordinary share capital (400,000 shares)

800,000

Other expenses 50,000Other income 25,000Retained earnings (1 July 2009) 229,800Revaluation reserve 70,000Sales 575,000Vehicles (at cost) 300,000

Other information (not currently included in the account balances above):

1. The final dividend of 8 cents per share declared at the 2009 annual general meeting was paid on 1 December 2009.

2. On 1 January 2010, Howell Ltd issued a prospectus offering 80,000 ordinary shares, payable in full on application at an issue price of $2. The shares were fully subscribed and the directors allotted the shares on 15 April.

3. On 30 April 2010 the directors decided to make a transfer of $140,000 to the General reserve.

4. On 1 June 2010, a bonus share issue of 1 for 4 was made to ordinary shareholders. The bonus share issue was funded from the general reserve and the issue price was $2 each.

Additional information:On 30 June 2010

Equipment is to be re-valued upwards by $50,000. The directors proposed a final dividend of 10 cents per share to ordinary

shareholders.Required:

(a)Prepare general journal entries to reflect points 1–4 only. Narrations are not required.

(b) Prepare a Statement of Comprehensive Income for year ending 30 June 2010

QUESTION 6

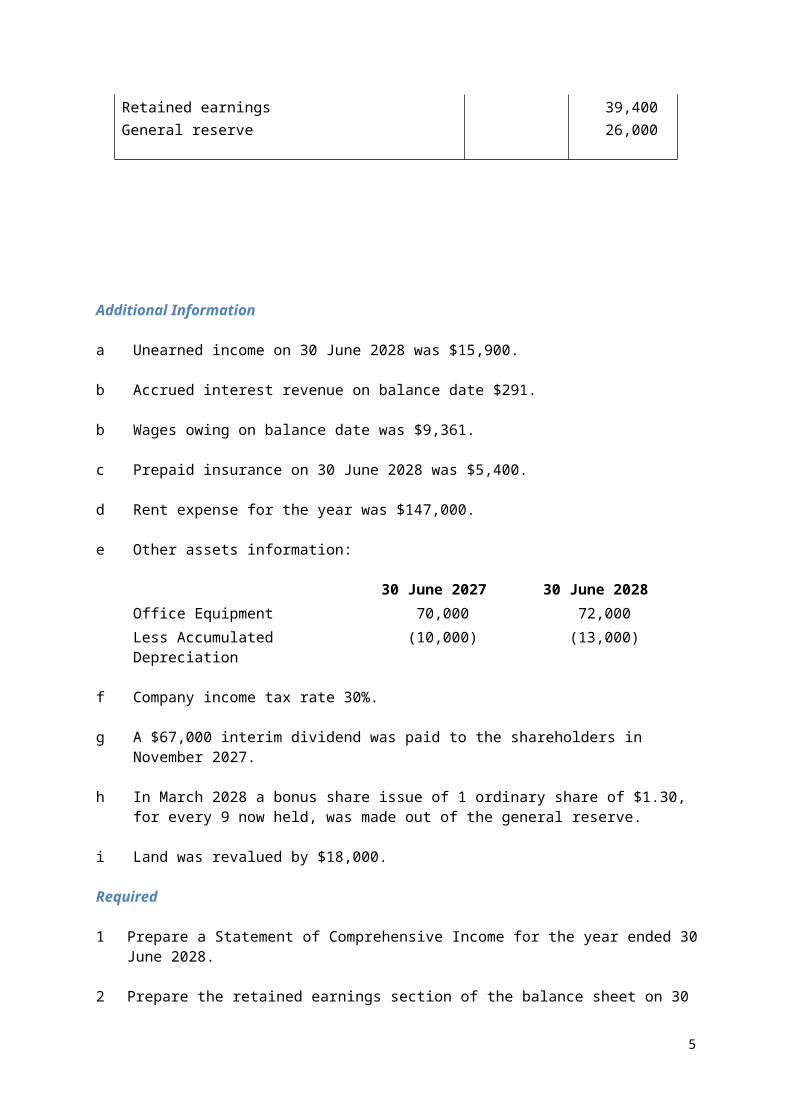

Marketing Consultants Limited

3

Trial Balance (extract)as at 30 June 2028

Ledger Account Title Debit CreditUnearned income 609,010Interest revenue 3,500Interest on loan 7,800Wages 162,000Telephone 33,000Prepaid insurance 25,000Prepaid rent 154,000Share capital (103,950 $1.00 ordinary shares)

101,000

Retained earnings 39,400General reserve 26,000

Additional Information

a Unearned income on 30 June 2028 was $15,900.

b Accrued interest revenue on balance date $291.

b Wages owing on balance date was $9,361.

c Prepaid insurance on 30 June 2028 was $5,400.

d Rent expense for the year was $147,000.

e Other assets information:

30 June 2027 30 June 2028Office Equipment 70,000 72,000Less Accumulated Depreciation

(10,000) (13,000)

f Company income tax rate 30%.

g A $67,000 interim dividend was paid to the shareholders in November 2027.

h In March 2028 a bonus share issue of 1 ordinary share of $1.30, for every 9 now held, was made out of the general reserve.

i Land was revalued by $18,000.

4

Required

1 Prepare a Statement of Comprehensive Income for the year ended 30 June 2028.

2 Prepare the retained earnings section of the balance sheet on 30 June 2028.

QUESTION 7

5

6

(B)

QUESTION 8

QUESTION 9

Ready Set Go LimitedBalance Sheet (extract)As at June 30 2008

Non Current AssetsProperty Plant and Equipment 100,000

Equity

7

Share Capital 382,000Other reserves 60,000Retained earnings (10, 000)Total Equity 432,000

Share Capital on 30 June 2008

16,000 10% preference shares of $4.00 each, fully paid, 62,000 less share issue costs of $2,000

644,000 ordinary shares of .50 cents each, fully paid, less 320,000share issue costs of $2,000

Other reservesGeneral Reserve $60,000

Property Plant and EquipmentLand $40,000Buildings $60,000

Additional information

A For the year ended 30 June 2008, the directors recommended preference shareholders receive their dividend entitlement, and ordinary shareholders receive a divided of 5c per share. These dividends were approved by the shareholders in August 2008 and paid in September 2008

B In April 2009 the ordinary shareholders were paid an interim divided of 4 cents per share and the preference shareholders were paid a 7% interim dividend

C In May 2009 the ordinary shareholders were given 1 fully paid bonus shares for every 10 now held. The bonus share issue was to be made from the general reserve.

D On June 30 2009 the company made a profit after tax of $260,000

E The directors of the company proposed the following final dividends for the year ended 30 June 2009.

The remainder of the annual dividend entitlement to the preference shareholders

An 9 cents per share dividend to the ordinary shareholders

These dividends must be approved by the shareholders at the annual general meeting in September 2009 before they can be paid.

F An amount of $10,000 was transferred to the general reserve from retained earnings.

G On June 30, 2009 it was decided to revalue the land. The current market value of the land is $80,000.

Required:

8

Prepare the retained earning ledger account at 30 June 09 Prepare the general journal entries to distribute profit for the year ended

30 June 09 Show the Non-Current Assets – Property, Plant and Equipment section of

the Balance Sheet and the Equity section of the Balance Sheet as at June 30, 2009.

Show the note attached to the balance sheet for the final dividends at June 30, 2009

QUESTION 10

Lawson Ltd was incorporated in 2003. By 30 June 2006, 220 000 ordinary shares had been issued at a price of $1.80 fully paid on application.

Lawson LtdBalance Sheet (extract)As at June 30 2006

EquityShare Capital 396 000General Reserve 20 000 Retained earnings (1 July 06) 21 500Total Equity 437 500

The following transactions and events occurred during the year ended 30 June 2007

2006 October 1 The company offered 50,000 5% preferences shares for sale to the public at $3.50 each payable in full on application

October 31 Applications for 48,000 shares were received

2 November The 48,000 shares were allotted and issued to shareholders$2,000 in share issue costs were paid

9

2007 June 30 The company recorded a net profit after tax of $72,800

June 30 The directors resolved to:

Provide for the final dividend for preference shares Provide for a final dividend on the ordinary shares of 6 cents per

share Both of these final dividends will be paid on 28 August 2007 A transfer of $10,000 is to be made to the general reserve

Required:a) Prepare the journal and ledger entries to record the share issue made on

October 1 2006b) Prepare general journal entries to record the distribution of profits on June 30, 2007c) Prepare the Retained Earnings ledger account as at June 30 2007d) Prepare the Equity section of the Balance Sheet as at June 30, 2007e) Show the notes attached to the Balance Sheet for final proposed dividends

at 30 June 2007.QUESTION 11

The following information relates to Leighton Ltd for the year ended 30 June 2010.

Leighton LtdAfter closing Trial BalanceAs at 30 June 2010Land 593,900Buildings 186,000Less accumulated depreciation on buildings 48,000Plant and Equipment 134,000Less accumulated depreciation of Plant and Equipment 39,000Cash at Bank 70,400Accounts receivable 23,900Prepaid advertising 5,600Inventory 34,600Accrued Income 1,600Investments (in other companies) 41,000Interim Ordinary dividend 14,000Retained earnings 65,600Ordinary share capital 576,000Profit and Loss (before tax) 83,600General reserve 48,000

10

Asset revaluation reserve 64,000

Accounts payable 64,000

Accrued expenses 2,800Unearned income 2,000Current tax liability 22,00

010% debentures (repayable in 2014) 90,00

01,105,000

1,105,000

Additional information:

Issued capital consists of $1 fully paid shares During the year a bonus share issue was made consisting of 1 bonus share

for every five shares already being held – this was paid out of the asset revaluation reserve.

The directors decided to transfer $10,000 to the general reserve from retained earnings.

For year ended 30 June 2010 the directors recommended a 10c per share dividend paid. This dividend is subject to shareholders approval.

Required:(1) Prepare a statement of changes in equity for Leighton Ltd for year ended 30

June 2010(2) Prepare a Balance Sheet for Leighton Ltd as at 30 June 2010.(3) Prepare the notes to the Balance Sheet for Property, Plant and Equipment Calculate the amount of the final dividends recommended on 30 June 2010

QUESTION 12

The following information relates ASK Ltd for the year ended 30 June 2009ASK LtdTrial Balance As at 30 June 2009Ordinary Capital 300,000Asset Revaluation Reserve 40,000Retained earnings 1,500Cash at Bank 46,200Accounts Receivable 62,800Inventory 17,000Accounts Payable 20,50014% Debentures (due November 2011) 50,000Profit and Loss 131,500Plant and Equipment 65,000Accumulated depreciation of Plant and Equipment

18,500

Land 260,000

11

Buildings 230,000Accumulated depreciation of Buildings 62,000Interim dividend 20,000General Reserve 80,000

702,500 702,500

Additional information: The ordinary share capital consists of fully paid 50 cents shares Current tax liability is $42,000 A final dividend of 5 cents per share is to be declared $25,000 is to be transferred from the general reserve

Required:a) Prepare journal entries to distribute profitb) Prepare a Statement of Changes in Equity for year ended 30 June 2009.c) Prepare a Balance Sheet at 30 June 2009d) Prepare notes to the Balance Sheet – for Shareholders’ Equity, Dividends

and Property Plant and Equipment

QUESTION 13

12

13

t

QUESTION 1414

QUESTION 15

15

QUESTION 16Mineral Water Wholesalers Limited

16

Trial Balanceas at 30 June 2019

Ledger Account Title Debit CreditCash at Bank 19,614Inventory 2,500Prepaid Insurance (3 months paid in advance) 900Land 105,000Plant and Equipment 40,700Accumulated Depreciation of Plant and Equipment 5,000Debentures (repayable in March 2020) 9,600Debentures (repayable in 2025) 22,400Share Capital($0.50 ordinary shares less share issue costs of $1,600)

101,400

General Reserve 3,000Retained Earnings 27,314

$168,714 $168,714

Transactions for the year ended 30 June 2020:

a 69,100 bottle of mineral water were sold for cash at $3.00 per bottle.

b The 69,100 bottles of mineral water sold included 2,100 bottles of mineral water sold in advance. These 2,100 bottles will be delivered to customers in August 2020.

c The cost price of each bottle of mineral water sold was $1.80.

d Closing inventory of mineral water on 30 June 2020 was $4,800.

e All bottles of mineral water were purchased for cash.

f Wages paid for the year were $51,000, with $1,900 of accrued wages on 30 June 2020.

g The annual insurance premium was renewed on 1 October 2019 for $3,720 cash.

h Interest paid during the year was $2,500. There was no accrued interest expense on30 June 2020.

i The plant and equipment accumulated depreciation on 30 June 2020 was $11,000.

j The income tax rate is 30% of the profit. The income tax for 2020 will be paid in 2021.

k A 5 cents per share interim dividend was paid in March 2020.

l $2,000 was transferred from the general reserve to retained earnings.

17

Required

Prepare a Statement of Financial Position as at 30 June 2020.

QUESTION 17

QUESTION 18

18

QUESTION 19

19

QUESTION 20

20

QUESTION 21The management of Lizard Ltd. require you to prepare a statement of cash flows for their business for the year ended 30 June 2010. Unfortunately they do not

21

have balance sheets for the past two financial years available but they have been able to provide you with the following account balances (sorted in alphabetical order).

2010 2009$ $

Accounts payable 104,000 82,000Borrowings 300,000 180,000Cash holdings 21,000 45,000Income tax payable 192,000 136,000Inventories 173,000 188,000Investments 650,000 750,000Property, plant and equipment 2,003,000 1 550,000Receivables 120,000 119,000General reserve 300,000 250,000Retained earnings 111,000 169,000Share capital 2,000,000 1 900,000Short-term deposits 40,000 65,000

Notes:Property, plant and equipment 2010 2009Land, at cost 900,000 900,000Plant and equipment, at cost 1,290,000 795,000Accumulated depreciation of plant and equipment 187,000 145,000

1,103,000 650,000Property, plant and equipment, book value 2,003,000 1,550,000

An item of plant originally purchased for $65,000 and with a book value of $12,000 was sold during the year for cash.

22

Lizard LtdIncome statement

for the year ended 30 June 2010

$Sales 2,850,00

0Less cost of sales 1,340,00

0Gross profit 1,510,00

0Add interest revenue 2,400 Gain on sale of plant and equipment 8,000 Dividends received 24,000

1,544,400

Less interest expense 18,750 Other expenses 670,300Profit before taxLess income tax expenseProfit for the year

855,350192,000663,350

Other information:

Income tax provided on 30 June 2009 was paid during the year. The change in borrowings during the year was due to an issue of

debentures. It is company policy that the purchase and sale of all non-current assets

be for cash.

Prepare a Statement of cash flows for Lizard Ltd. for the year ended 30 June 2010. (35 marks)

QUESTION 22(30 marks)

Financial reports are an essential component of all business activity as they provide a wide variety of information for both internal and external users. Over recent years corporate failures have called into question the reliability of financial information.

(a) Explain the roles of the FRC, AASB, ASX, ASIC, IASB (full titles should be included in your answer) and external auditors. (18 marks)

(b) Describe the effectiveness of these organisations in ensuring the reliability of financial statements. (12 marks)

QUESTION 23

23

There is acceptance within the broader community that government, business and individuals must all do their part to reduce their impact on the natural environment. In relation to business, it is generally the large mining, petroleum, oil and gas and chemical manufacturing organisations which attract most regulatory and public attention. However, businesses of all sizes must implement policies and procedures to reduce their environmental impact.

(a) Outline four incentives for businesses to act in an environmentally responsible manner.

(8 marks)

(b) Describe the potential benefits to a business of engaging in environmentally responsible practices. (12 marks)

(c) Describe the potential costs to a business of engaging in environmentally responsible practices. (4 marks)

(d) Explain briefly corporate social responsibility. Using two examples (other than environmental), explain how these demonstrate corporate social responsibility.

(6 marks)

QUESTION 24Mia has $10,000 to invest and is considering the acquisition of ordinary shares in Goldpost, a mining firm with several gold mining sites in regional Western Australia. A summary of the firm’s performance over the last three financial years is outlined in the table below:

Ratio 30/6/2007 30/6/2008 30/6/2009 Industry average

Debt to equity 40% 55% 70% 45%Quick asset 1.15 1.38 1.70 1.05Price/earnings 15 12 8 14Profit 7% 9% 10% 14%

(a) For each of the ratios contained in the table above, briefly:

define what each is measuring discuss the trend suggest one reason for the trend.

24

QUESTION 25

QUESTION 26

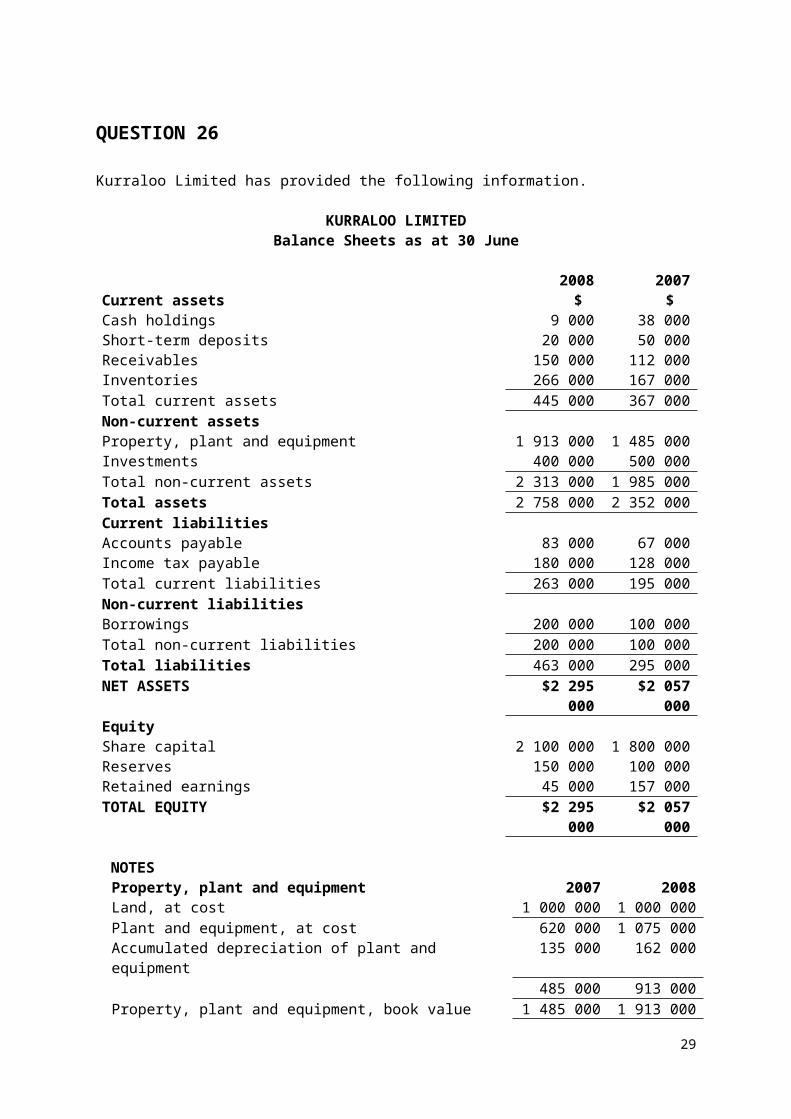

Kurraloo Limited has provided the following information.

KURRALOO LIMITEDBalance Sheets as at 30 June

2008 2007Current assets $ $Cash holdings 9 000 38 000

25

Short-term deposits 20 000 50 000Receivables 150 000 112 000Inventories 266 000 167 000Total current assets 445 000 367 000Non-current assetsProperty, plant and equipment 1 913 000 1 485 000Investments 400 000 500 000Total non-current assets 2 313 000 1 985 000Total assets 2 758 000 2 352 000Current liabilitiesAccounts payable 83 000 67 000Income tax payable 180 000 128 000Total current liabilities 263 000 195 000Non-current liabilitiesBorrowings 200 000 100 000Total non-current liabilities 200 000 100 000Total liabilities 463 000 295 000NET ASSETS $2 295

000$2 057

000EquityShare capital 2 100 000 1 800 000Reserves 150 000 100 000Retained earnings 45 000 157 000TOTAL EQUITY $2 295

000$2 057

000

NOTESProperty, plant and equipment 2007 2008Land, at cost 1 000 000 1 000 000Plant and equipment, at cost 620 000 1 075 000Accumulated depreciation of plant and equipment 135 000 162 000

485 000 913 000Property, plant and equipment, book value 1 485 000 1 913 000

An item of plant originally purchased for $50 000 and with a book value of $8 000 was sold during the year for cash.

KURRALOO LIMITEDIncome Statement (summarised) for year ended 30 June 2008

$Sales 2 450 000Less Cost of sales 1 280 000Gross Profit 1 170 000Add Interest revenue 1 200

Sale of plant and equipment 5 000 Dividends received 18 000

1 194 200Less Interest expense (13 500)

Other expenses (580 700)Profit before tax $600 000

Other information

26

The short-term deposits are used as part of the company’s cash management function.

Income tax provided on 30 June 2007 was paid during the year. $100 000 cash was raised during the year by an issue of debentures and

$300 000 by an issue of ordinary shares. Dividends totalling $472 000 were paid during the year. All purchases and sales of inventory are made on credit. During the year

ended 30 June 2008 the total inventory purchased was $1 384 000. It is company policy that the purchase and sale of all non-current assets be

for cash. ‘Other expenses’ included depreciation and loss on sale of plant and

equipment.

Required

(a) Prepare a cash flow statement for Kurraloo Limited for the year ended 30 June 2008 showing the cash from operating activities and investing activities ONLY.

(28 marks)(b) Explain the meaning of ‘cash and cash equivalents’. Refer to the Cash Flow

Statement of Kurraloo Limited in Part A of this question to provide examples for your answer.

(4 marks)

(c) Use the Cash Flow Statement you have prepared to explain the changes in the cash holdings of Kurraloo Limited over the past financial year.

(4 marks)QUESTION 27

City Traders LimitedBalance Sheets

as atItem 30 June 2016 30 June 2017

AssetsCash at Bank 11 40Cash on Hand 8 6Accounts Receivable 33 47Less Allowance for Doubtful Debts

(7) (9)

Prepaid Rent 13 21Inventory 10 11Motor Vehicles 60 72Accumulated Depreciation (14) (17)Total Assets $114 $171

27

Liabilities and EquityAccrued Wages 19 20Income Tax Payable 2 1Debentures 20 25Share Capital 61 110General Reserve 8 9Retained Earnings 4 6Total Liabilities and Equity $114 $171

City Traders LimitedIncome Statement

for the year ended 30 June 2017Sales 165Less Sales Returns 3 162

Less Cost of Sales 37Gross Profit 125Add Other IncomeGain on Sale of Motor Vehicle 8Interest 2 10

135Less Other ExpensesRent 65Discount Allowed 2Interest 1Doubtful Debts 6Wages 30Other Expenses 25 129Profit before Tax 6Less Income Tax Expense 1Profit $5

28

Additional Information

a A motor vehicle had been purchased during the last year for $34 cash.

b The accumulated depreciated of the motor vehicle sold was $13 to the date of sale.

c The “other expenses” include the depreciation of motor vehicles.

Required

Prepare a cash flow statement for the year ended 30 June 2017.

QUESTION 28Perth Traders Limited Balance Sheet as

at 30 June 2025AssetsCash at Bank 40Office Supplies 5Accounts Receivable 34Motor Vehicles 190Prepaid Rent 11Inventory 110Total Assets 390LiabilitiesAccounts Payable 92Accrued Expenses 8Income Tax Liability 30Debentures (repayable in 2029) 40Total Liabilities 170Net Assets $220EquityShare Capital 125Reserves 40Retained Earnings 55Total Equity $220

Perth Traders Limited - Income Statement

for the year ended 30 June 2025Sales (all credit) 352Less Sales Returns 10

29

342Less Cost of Sales 204Gross Profit 138Less Interest 15Less Other Expenses 33Profit before Tax 90Less Income Tax Expense 27Profit $63

Additional information

a The total assets of Perth Traders Limited on 1 July 2024 was $270.

b Perth Traders Limited issued:290 $0.25 ordinary shares for 335 days in the year480 $0.25 ordinary shares for 30 days in the year.

c A $16 preference dividend was paid in March 2025.

d On 30 June 2025 the market price of an ordinary share of Perth Traders Limited was $3.00.

e A $0.31 per ordinary share dividend was paid in March 2025.

f The accounts receivable of Perth Traders Limited on 1 July 2024 was $14.

g The inventory on 1 July 2024 of Perth Traders Limited was $46.

Required

1 Calculate the following ratios for Perth Traders Limited:• current or working capital ratio• quick asset or liquidity ratio• debt to equity ratio• times interest earned• rate of return on assets• earnings per ordinary share• price earnings ratio• dividend yield• debtors’ collection period• inventory turnover ratio.

2 Comment on the performance and health of Perth Traders Limited.

30

31

![AonRiskServicesAustraliaLimitedvAustralianNationalUniversity[2009]HCA27(5 August 2009)](https://static.fdocuments.us/doc/165x107/577d39941a28ab3a6b9a1c38/aonriskservicesaustralialimitedvaustraliannationaluniversity2009hca275-august.jpg)