Vietnam Office Occupier Update H1/2019 · ROT RTE % 0.1 PPT 2.6 P N/A % 66,958 EY ETE EE 4% 9.1 11...

9

savills.com.vn Vietnam – Oct.2019 Media Brief Office Occupier Update REPORT Savills Research

Transcript of Vietnam Office Occupier Update H1/2019 · ROT RTE % 0.1 PPT 2.6 P N/A % 66,958 EY ETE EE 4% 9.1 11...

savills.com.vn

Vietnam – Oct.2019

Media BriefOffice Occupier Update

R E P O R T

Savills Research

REGIONAL REVIEW

GDP increased 6.8% in H1/2019. Manufacturing and processing continue to be the key economic drivers. CPI was 2.6 %, the lowest H1 increase in three years.

Total exports increased 7% year on year (YoY) to reach US$122.7 billion. The USA and the EU continue to be the main export markets. The $34 million trade deficit was mainly due to higher import costs.

Registered FDI was over US$18 billion with China and Korea the largest contributors. Disbursed FDI reached US$9.1billion, up 8% YoY.

International visitors continue to grow with 8.4 million arrivals, up 8% YoY.

Over the next 3 years Vietnam has the highest GDP growth in Southeast Asia. Fixed investment has increased, credit is under control, and the stock market has recovered after a slump. Investor confidence is also high, driven by improvement in the business environment.

Figure 2: GDP Forecast, 2019-2021

Figure 1: Regional Prime Benchmark

Figure 3: Stock Index Movement, H1/2019

Source CEIC

Source Trading Economics

Figure 4: Credit to Private Sector (%/GDP), 2018 Figure 5: Business Confidence Index, 2019/20

Source TheGlobalEconomy.comSource World Bank

VIETNAM MACRO INDICATORS H1/2019

2.4%

4.8%

3.5%

5.2%

6.6%

6.5%

Singapore

Malaysia

Thailand

Indonesia

Philippines

Vietnam

-4.5%

3.8%

0.6%

5.1%

11.1%

Malaysia

Thailand

Indonesia

Philippines

Vietnam

121.9

119.3

112.5

32.7

49.9

133.3

Singapore

Malaysia

Thailand

Indonesia

Philippines

Vietnam

-11.0

-5.8

-1.4

19.2

46.7

34.7

Singapore

Malaysia

Thailand

Indonesia

Philippines

Vietnam

Value YoY Growth Rate(%)

80RETAIL SALES

13%BILLION $ 6.2

CREDITGROWTH

%6.8

GDPGROWTH RATE

0.1 PPT%

2.6CPI

N/A

% 66,958

NEWLY ESTABLISHEDBUSINESSES

4%

9.1

11

MORTGAGERATE

% Stable

INTERNATIONALVISITORS

8.4 8%

0.3 ppt

MILLION

TRADEDEFICIT

34MILLION $

FDI

18.48%10%

0.7 ppt

BILLION $

UNIT

(Registered FDI) (FDI Disbursement)

0

20

40

60

80

100

0

20

40

60

80

100

120

Singapore HCMC Hanoi Jakarta Manila Kuala Lumpur

%US$/m2/mth

Gross Rent

Occupancy

Source International Monetary Fund

Office Occupier Update - H1/2019

H1/2019

REGIONAL REVIEW

GDP increased 6.8% in H1/2019. Manufacturing and processing continue to be the key economic drivers. CPI was 2.6 %, the lowest H1 increase in three years.

Total exports increased 7% year on year (YoY) to reach US$122.7 billion. The USA and the EU continue to be the main export markets. The $34 million trade deficit was mainly due to higher import costs.

Registered FDI was over US$18 billion with China and Korea the largest contributors. Disbursed FDI reached US$9.1billion, up 8% YoY.

International visitors continue to grow with 8.4 million arrivals, up 8% YoY.

Over the next 3 years Vietnam has the highest GDP growth in Southeast Asia. Fixed investment has increased, credit is under control, and the stock market has recovered after a slump. Investor confidence is also high, driven by improvement in the business environment.

Figure 2: GDP Forecast, 2019-2021

Figure 1: Regional Prime Benchmark

Figure 3: Stock Index Movement, H1/2019

Source CEIC

Source Trading Economics

Figure 4: Credit to Private Sector (%/GDP), 2018 Figure 5: Business Confidence Index, 2019/20

Source TheGlobalEconomy.comSource World Bank

VIETNAM MACRO INDICATORS H1/2019

2.4%

4.8%

3.5%

5.2%

6.6%

6.5%

Singapore

Malaysia

Thailand

Indonesia

Philippines

Vietnam

-4.5%

3.8%

0.6%

5.1%

11.1%

Malaysia

Thailand

Indonesia

Philippines

Vietnam

121.9

119.3

112.5

32.7

49.9

133.3

Singapore

Malaysia

Thailand

Indonesia

Philippines

Vietnam

-11.0

-5.8

-1.4

19.2

46.7

34.7

Singapore

Malaysia

Thailand

Indonesia

Philippines

Vietnam

Value YoY Growth Rate(%)

80RETAIL SALES

13%BILLION $ 6.2

CREDITGROWTH

%6.8

GDPGROWTH RATE

0.1 PPT%

2.6CPI

N/A

% 66,958

NEWLY ESTABLISHEDBUSINESSES

4%

9.1

11

MORTGAGERATE

% Stable

INTERNATIONALVISITORS

8.4 8%

0.3 ppt

MILLION

TRADEDEFICIT

34MILLION $

FDI

18.48%10%

0.7 ppt

BILLION $

UNIT

(Registered FDI) (FDI Disbursement)

0

20

40

60

80

100

0

20

40

60

80

100

120

Singapore HCMC Hanoi Jakarta Manila Kuala Lumpur

%US$/m2/mth

Gross Rent

Occupancy

Source International Monetary Fund

savills.com.vn

H1/2019

Office Occupier Update - H1/2019

Figure 6: Grade A&B Performance Figure 7: Tenant Proportion

HCMC - OFFICE

Co-working has become more popular for enterprise solutions. Offering flexible space, Co-working used to be popular amongst most

start-ups, now more established corporations are considering this option as it provides flexible solutions.

Tu Thi Hong An, Associate Director,Head of Commercial Leasing

Figure 8: Proportion by Industry, 2017-2019

1.9 million m2

SUPPLY

2% QoQ3% YoY

31US$/m2/mth

RENT

Stable QoQ6% YoY

97%OCCUPANCY

-1 ppt QoQ1 ppt YoY

KEYFINDINGS

20%

42%

80%

58%

Grade A Grade BLocal Foreign

OverviewWith overall occupancy of 98% and Grade A rental of US$60/m²/mth, HCMC’s office market is one of the best performing within Asia. The strong performance is expected to continue, with just 20,000m² expected to enter in the next two years. Tenants seeking new space or merely wishing to expand need to carefully weigh up their options as the near future will be marked by limited opportunities. Already companies who cannot afford the higher prices are relocating to fringe and decentralized locations. WhyVietnam’s strongly emerging economy is transitioning rapidly, particularly the commercial sector. The Finance, Insurance and Real Estate sector (F.I.R.E) lags behind regional peers and so has a long way to grow, with massive office demand expected. With 100,000m² leased over the last two years, this sector had the highest take-up. The deregulation of the insurance industry has resulted in 20% pa growth in demand; which will in turn flow through to office occupation. The great excitement around Fintech in Vietnam pivots on the under penetration of Vietnam’s banking sector at 59% compared to Thailand at 86 percent. Alongside the maturity of the banking sector, greater office demand is also expected. The Information and Communication Technology sector (ICT) has had rapid take-up of around 50,000m² in the last two years and is expected to translate to higher office space requirements in the future. WhatFrom 2017 until now, domestic (37%) and foreign (63%) firms have occupied similar amounts of Grade A and B space. However,80% of take-up by international corporations was Grade A. Deals in HCMC have been dominated by Real Estate with 57% and ICT with 14%. Within the real estate sector, the majority breakdown is Co-Working spaces, such as WeWork. It will be interesting to see how WeWork’s apparent fairytale performance now unfolds that the CEO has replaced by a non-executive, the valuation slashed, and the IPO delayed. Disruption in the property industry continues as Proptech garners massive funding support of up to US$1B/month globally. ImpactExpect higher rents or be prepared to negotiate strongly or decentralize. With most companies only committing to 3-year leases, most will fall within the bookends of the present strong cycle. Renewal options will come under the microscope and those without capped upward movement should expect increases. It will be a testing time for poorly written leases that haven’t fully considered the future.

MNCs seldom operate in isolation and have the choice of regional locations to base business. Vietnam is evolving rapidly, however operations capability may not be in step, available office space is an example. If domestic and export demand are both growing then a local base is logical, provided it can be afforded; otherwise, an alternate location within the region will become more appealing.

From a capital markets perspective, many of the MNCs conducting insurance will be turning out profits that will be repatriated to home countries. If there were investment options available in Vietnam, then these profits could be committed locally. However, ongoing paralysis in administration currently precludes a wide choice of investment opportunities.

0

15

30

45

0

300

600

900

1,200

2014 2015 2016 2017 2018 H1/2019

thou

sand

m2

US

$/m2/m

th

Leased Vacant Avg. gross rent

(1) Data collection as of H1/2019(2) Occupancy calculated by leased areadivided by leasable area

QoQ: Quarter on Quarter comparisonYoY: Year on Year comparison

Source Savills Research and Consultancy Source Savills Research and Consultancy

Source Savills Research and ConsultancyNote: ICT: Information & Communication Technology

24%

13%12% 11%

9% 8%

5%

Manufacturing Distribution ICT Real estate Consultancy Utility

2017

2019

Finance,Bank &

Insurance

Office

savills.com.vn

Figure 6: Grade A&B Performance Figure 7: Tenant Proportion

HCMC - OFFICE

Co-working has become more popular for enterprise solutions. Offering flexible space, Co-working used to be popular amongst most

start-ups, now more established corporations are considering this option as it provides flexible solutions.

Tu Thi Hong An, Associate Director,Head of Commercial Leasing

Figure 8: Proportion by Industry, 2017-2019

1.9 million m2

SUPPLY

2% QoQ3% YoY

31US$/m2/mth

RENT

Stable QoQ6% YoY

97%OCCUPANCY

-1 ppt QoQ1 ppt YoY

KEYFINDINGS

20%

42%

80%

58%

Grade A Grade BLocal Foreign

OverviewWith overall occupancy of 98% and Grade A rental of US$60/m²/mth, HCMC’s office market is one of the best performing within Asia. The strong performance is expected to continue, with just 20,000m² expected to enter in the next two years. Tenants seeking new space or merely wishing to expand need to carefully weigh up their options as the near future will be marked by limited opportunities. Already companies who cannot afford the higher prices are relocating to fringe and decentralized locations. WhyVietnam’s strongly emerging economy is transitioning rapidly, particularly the commercial sector. The Finance, Insurance and Real Estate sector (F.I.R.E) lags behind regional peers and so has a long way to grow, with massive office demand expected. With 100,000m² leased over the last two years, this sector had the highest take-up. The deregulation of the insurance industry has resulted in 20% pa growth in demand; which will in turn flow through to office occupation. The great excitement around Fintech in Vietnam pivots on the under penetration of Vietnam’s banking sector at 59% compared to Thailand at 86 percent. Alongside the maturity of the banking sector, greater office demand is also expected. The Information and Communication Technology sector (ICT) has had rapid take-up of around 50,000m² in the last two years and is expected to translate to higher office space requirements in the future. WhatFrom 2017 until now, domestic (37%) and foreign (63%) firms have occupied similar amounts of Grade A and B space. However,80% of take-up by international corporations was Grade A. Deals in HCMC have been dominated by Real Estate with 57% and ICT with 14%. Within the real estate sector, the majority breakdown is Co-Working spaces, such as WeWork. It will be interesting to see how WeWork’s apparent fairytale performance now unfolds that the CEO has replaced by a non-executive, the valuation slashed, and the IPO delayed. Disruption in the property industry continues as Proptech garners massive funding support of up to US$1B/month globally. ImpactExpect higher rents or be prepared to negotiate strongly or decentralize. With most companies only committing to 3-year leases, most will fall within the bookends of the present strong cycle. Renewal options will come under the microscope and those without capped upward movement should expect increases. It will be a testing time for poorly written leases that haven’t fully considered the future.

MNCs seldom operate in isolation and have the choice of regional locations to base business. Vietnam is evolving rapidly, however operations capability may not be in step, available office space is an example. If domestic and export demand are both growing then a local base is logical, provided it can be afforded; otherwise, an alternate location within the region will become more appealing.

From a capital markets perspective, many of the MNCs conducting insurance will be turning out profits that will be repatriated to home countries. If there were investment options available in Vietnam, then these profits could be committed locally. However, ongoing paralysis in administration currently precludes a wide choice of investment opportunities.

0

15

30

45

0

300

600

900

1,200

2014 2015 2016 2017 2018 H1/2019

thou

sand

m2

US

$/m2/m

th

Leased Vacant Avg. gross rent

(1) Data collection as of H1/2019(2) Occupancy calculated by leased areadivided by leasable area

QoQ: Quarter on Quarter comparisonYoY: Year on Year comparison

Source Savills Research and Consultancy Source Savills Research and Consultancy

Source Savills Research and ConsultancyNote: ICT: Information & Communication Technology

24%

13%12% 11%

9% 8%

5%

Manufacturing Distribution ICT Real estate Consultancy Utility

2017

2019

Finance,Bank &

Insurance

Office

Office Occupier Update - H1/2019

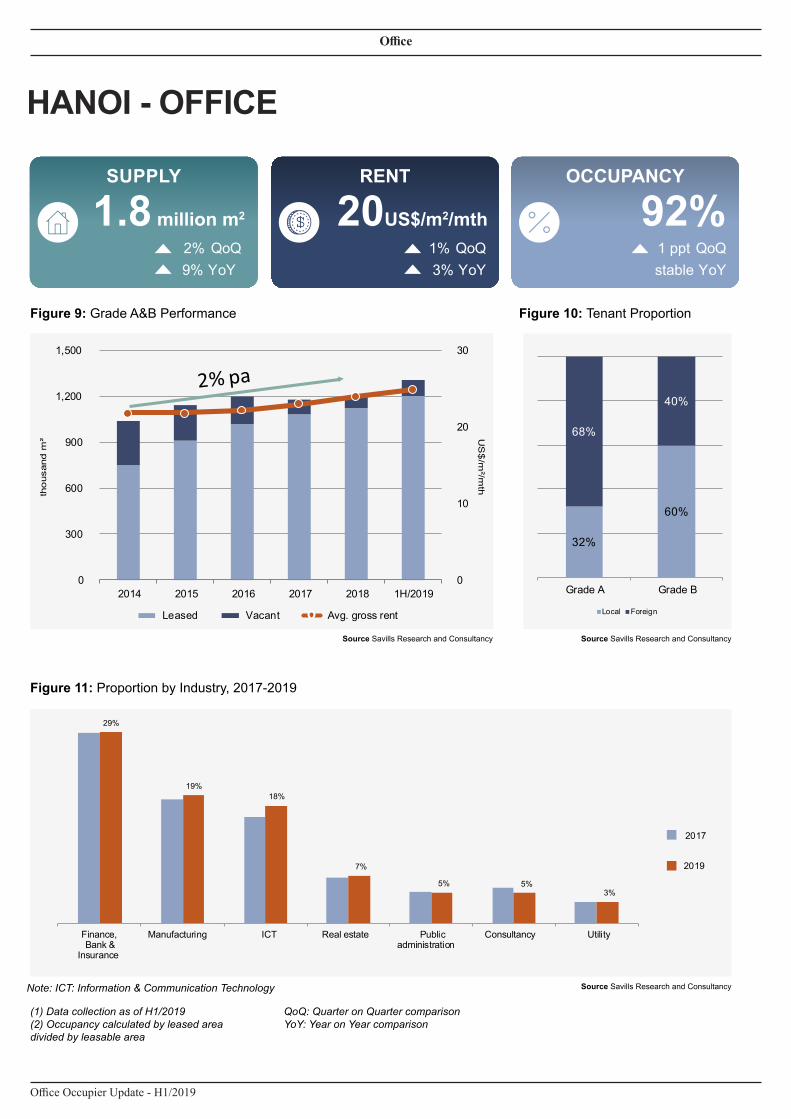

Figure 9: Grade A&B Performance Figure 10: Tenant Proportion

HANOI - OFFICE

Technology and Start-ups accounted for most office absorption over the last year, mainly in Ba Dinh and Cau Giay. Even with

limited supply, Hoan Kiem and Ba Dinh still attract high demand. Key selection criteria include location, rent, building

quality and technology.Hoang Nguyet Minh, Associate Director, Commercial Leasing

Figure 11: Proportion by Industry, 2017-2019

1.8 million m2

SUPPLY

2% QoQ9% YoY

20US$/m2/mth

RENT

1% QoQ3% YoY

92%OCCUPANCY

1 ppt QoQstable YoY

KEYFINDINGS

OverviewAverage occupancy has remained at 93% for the past two years. With the exception of one recently launched building, Grade A projects were limited - existing buildings in the CBD are rapidly ageing and lack modern facilities. As high-quality office space is more attractive to foreign tenants, interest for Grade A is anticipated to increase in line with good FDI and vigorous M&A activities. Demand for Grade B will remain high due to affordability. Savills expects a dynamic Grade A and B market in upcoming years, particularly in the Secondary and Western areas. The low vacancy and limited future CBD supply; means tenants are relocating to the Midtown and West. Many lease expiries will need to accept rent increases.

WhyFinance, Bank & Insurance tenants occupied the largest proportion of leased areas (29%), followed by Manufacturing (19%) and ICT (18%). These three sectors increased their shares from 2017 to 2019, particularly ICT at 2-ppt growth. Finance, Bank & Insurance had the highest CBD and Secondary area share whilst ICT and Manufacturing were the greatest in the West. Many large F.I.R.E enterprises and government offices have relocated from the CBD to the Secondary and the Western areas.Tenants of ICT and Finance, Bank & Insurance industries leased the largest average size. Occupiers of over 1,000 m² accounted for 9% of tenants but a considerable 53% of leased area.

WhatCompared to 2017, the proportion of Vietnamese and foreign tenants in Grade A & B segments has remained relatively stable at 43% and 57%. However, most foreign tenants prefer superior space with higher rent. At 1H/2019, 68% of the leased area in Grade A buildings was occupied by international tenants. Major international tenants included Korean and Japanese companies.The CBD will have no new infrastructure for the next ten years; metro developments and the upgrade and expansion of Ring Roads 2 and 3 are prioritised for the West and the Secondary areas.Previously only appealing to start-up companies, Co-Working spaces are now considered by established corporations. Brands such as Regus, Up, Toong, Cogo, Tiktak, CEO Suite, Dreamplex and WeWork all have locations in Hanoi. Within the past 12 months, Up opened four new sites with a total scale of 15,500 m² while Toong launched three new spaces providing 7,000 m². In the past 24 months, Cogo opened five new outlets supplying 11,500 m².As co-working spaces are still new to the market, growth is set to accelerate in the coming years. The entry of international operators will usher in a period of M&A, a trend that is already occurring in other markets in the Asia Pacific. Foreign investors have contributed to 17 business sectors in Viet Nam with a focus on manufacturing, which typically creates demand for office space. The M&A market is expected to grow strongly due to favorable economic environment as well as rising demand for human and investment capital. A wide range of modern technologies and techniques could be applied to the workplace to boost productivity and staff satisfaction. Additional amenities are expected to suit the needs of new generations of occupiers.

29%

19%18%

7%

5% 5%3%

Finance,Bank &

Insurance

Manufacturing ICT Real estate Publicadministration

Consultancy Utility

32%

60%

68%

40%

Grade A Grade B

Local Foreign

0

10

20

30

0

300

600

900

1,200

1,500

2014 2015 2016 2017 2018 1H/2019

US

$/m

²/mth

tho

usan

d m

²

Leased Vacant Avg. gross rent

2017

2019

(1) Data collection as of H1/2019(2) Occupancy calculated by leased areadivided by leasable area

QoQ: Quarter on Quarter comparisonYoY: Year on Year comparison

Source Savills Research and Consultancy Source Savills Research and Consultancy

Source Savills Research and ConsultancyNote: ICT: Information & Communication Technology

Office

savills.com.vn

Figure 9: Grade A&B Performance Figure 10: Tenant Proportion

HANOI - OFFICE

Technology and Start-ups accounted for most office absorption over the last year, mainly in Ba Dinh and Cau Giay. Even with

limited supply, Hoan Kiem and Ba Dinh still attract high demand. Key selection criteria include location, rent, building

quality and technology.Hoang Nguyet Minh, Associate Director, Commercial Leasing

Figure 11: Proportion by Industry, 2017-2019

1.8 million m2

SUPPLY

2% QoQ9% YoY

20US$/m2/mth

RENT

1% QoQ3% YoY

92%OCCUPANCY

1 ppt QoQstable YoY

KEYFINDINGS

OverviewAverage occupancy has remained at 93% for the past two years. With the exception of one recently launched building, Grade A projects were limited - existing buildings in the CBD are rapidly ageing and lack modern facilities. As high-quality office space is more attractive to foreign tenants, interest for Grade A is anticipated to increase in line with good FDI and vigorous M&A activities. Demand for Grade B will remain high due to affordability. Savills expects a dynamic Grade A and B market in upcoming years, particularly in the Secondary and Western areas. The low vacancy and limited future CBD supply; means tenants are relocating to the Midtown and West. Many lease expiries will need to accept rent increases.

WhyFinance, Bank & Insurance tenants occupied the largest proportion of leased areas (29%), followed by Manufacturing (19%) and ICT (18%). These three sectors increased their shares from 2017 to 2019, particularly ICT at 2-ppt growth. Finance, Bank & Insurance had the highest CBD and Secondary area share whilst ICT and Manufacturing were the greatest in the West. Many large F.I.R.E enterprises and government offices have relocated from the CBD to the Secondary and the Western areas.Tenants of ICT and Finance, Bank & Insurance industries leased the largest average size. Occupiers of over 1,000 m² accounted for 9% of tenants but a considerable 53% of leased area.

WhatCompared to 2017, the proportion of Vietnamese and foreign tenants in Grade A & B segments has remained relatively stable at 43% and 57%. However, most foreign tenants prefer superior space with higher rent. At 1H/2019, 68% of the leased area in Grade A buildings was occupied by international tenants. Major international tenants included Korean and Japanese companies.The CBD will have no new infrastructure for the next ten years; metro developments and the upgrade and expansion of Ring Roads 2 and 3 are prioritised for the West and the Secondary areas.Previously only appealing to start-up companies, Co-Working spaces are now considered by established corporations. Brands such as Regus, Up, Toong, Cogo, Tiktak, CEO Suite, Dreamplex and WeWork all have locations in Hanoi. Within the past 12 months, Up opened four new sites with a total scale of 15,500 m² while Toong launched three new spaces providing 7,000 m². In the past 24 months, Cogo opened five new outlets supplying 11,500 m².As co-working spaces are still new to the market, growth is set to accelerate in the coming years. The entry of international operators will usher in a period of M&A, a trend that is already occurring in other markets in the Asia Pacific. Foreign investors have contributed to 17 business sectors in Viet Nam with a focus on manufacturing, which typically creates demand for office space. The M&A market is expected to grow strongly due to favorable economic environment as well as rising demand for human and investment capital. A wide range of modern technologies and techniques could be applied to the workplace to boost productivity and staff satisfaction. Additional amenities are expected to suit the needs of new generations of occupiers.

29%

19%18%

7%

5% 5%3%

Finance,Bank &

Insurance

Manufacturing ICT Real estate Publicadministration

Consultancy Utility

32%

60%

68%

40%

Grade A Grade B

Local Foreign

0

10

20

30

0

300

600

900

1,200

1,500

2014 2015 2016 2017 2018 1H/2019

US

$/m

²/mth

tho

usan

d m

²

Leased Vacant Avg. gross rent

2017

2019

(1) Data collection as of H1/2019(2) Occupancy calculated by leased areadivided by leasable area

QoQ: Quarter on Quarter comparisonYoY: Year on Year comparison

Source Savills Research and Consultancy Source Savills Research and Consultancy

Source Savills Research and ConsultancyNote: ICT: Information & Communication Technology

Office

Office Occupier Update - H1/2019

Publications

1

Tech Cities in Motion

World Research – 2019

REPORT

Savills Research

SAVILLS VIETNAM - PUBLICATIONS

Savills ResearchWe’re a dedicated team with an unrivalled reputation for producing well-informed and accurate analysis, research and commentary across all sectors of the Vietnam property market.

Research O�ce

Troy Gri�thsDeputy Managing Director +84 (0) 933 276 663

tgri�[email protected]

Tu Thi Hong AnAssociate Director, Head of Commercial Leasing, HCMC+84 (0) 904 272 612 [email protected]

Savills plc: Savills is a leading global real estate service provider listed on the London Stock Exchange. The company established in 1855, has a rich heritage with unrivalled growth. It is a company that leads rather than follows, and now has over 700 o�ces and associates throughout the Americas, Europe, Asia Pacific, Africa and the Middle East.

This report is for general informative purposes only. It may not be published, reproduced or quoted in part or in whole, nor may it be used as a basis for any contract, prospectus, agreement or other document without prior consent. Whilst every e�ort has been made to ensure its accuracy, Savills accepts no liability whatsoever for any direct or consequential loss arising from its use. The content is strictly copyright and reproduction of the whole or part of it in any form is prohibited without written permission from Savills Research.

Industry award fees are being redirected to help local people. Charities for underprivileged around the country will receive donations.

Savills is committed to caring forthe community

Do Thi Thu HangDirector,Advisory Services, Hanoi +84 (0) 912 000 [email protected]

Hoang Nguyet MinhAssociate Director,Commercial Leasing, Hanoi+84 (0) 983 218 389 [email protected]

savills.com.vn

1

Tech Cities in Motion

World Research – 2019

REPORT

Savills Research

SAVILLS VIETNAM - PUBLICATIONS

Savills ResearchWe’re a dedicated team with an unrivalled reputation for producing well-informed and accurate analysis, research and commentary across all sectors of the Vietnam property market.

Research O�ce

Troy Gri�thsDeputy Managing Director +84 (0) 933 276 663

tgri�[email protected]

Tu Thi Hong AnAssociate Director, Head of Commercial Leasing, HCMC+84 (0) 904 272 612 [email protected]

Savills plc: Savills is a leading global real estate service provider listed on the London Stock Exchange. The company established in 1855, has a rich heritage with unrivalled growth. It is a company that leads rather than follows, and now has over 700 o�ces and associates throughout the Americas, Europe, Asia Pacific, Africa and the Middle East.

This report is for general informative purposes only. It may not be published, reproduced or quoted in part or in whole, nor may it be used as a basis for any contract, prospectus, agreement or other document without prior consent. Whilst every e�ort has been made to ensure its accuracy, Savills accepts no liability whatsoever for any direct or consequential loss arising from its use. The content is strictly copyright and reproduction of the whole or part of it in any form is prohibited without written permission from Savills Research.

Industry award fees are being redirected to help local people. Charities for underprivileged around the country will receive donations.

Savills is committed to caring forthe community

Do Thi Thu HangDirector,Advisory Services, Hanoi +84 (0) 912 000 [email protected]

Hoang Nguyet MinhAssociate Director,Commercial Leasing, Hanoi+84 (0) 983 218 389 [email protected]