VIETNAM FMCG TODAY AND TOMORROW - Vietnam Business filevietnam fmcg today and tomorrow 10th of june...

21

VIETNAM FMCG TODAY AND TOMORROW 10 th of June 2015 A SHARING SESSION WITH MJN

Transcript of VIETNAM FMCG TODAY AND TOMORROW - Vietnam Business filevietnam fmcg today and tomorrow 10th of june...

VIETNAM FMCGTODAY AND TOMORROW

10th of June 2015

A SHARING SESSION WITH MJN

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

2

MACRO ECONOMY – DO THE NUMBERS ADD UP?

+ 6.03%Q1’15 vs. YA

2015 Target

6.0%GDP

CPI

RETAIL SALES

+ 10%Q1’15 vs. YA

2015 Target

3.7%+ 0.74%Q1’15 vs. YA

EXPORT + 6.9%Q1’15 vs. YA

Cop

yri

gh

t ©

20

15

T

he

Nie

lse

n C

om

pa

ny.

Con

fid

en

tia

l a

nd

pro

pri

eta

ry.

3

37.4

17.214.9

12.4

8.4 5.6 4.2Beverage

Foods

Milk Bases

Cigarette

Personal Care

Home Care

Baby Products

RECOVERY IN THE TREND BUT STILL VERY SLUGGISH

Source: Nielsen Retail Audit – Total 6 cities – Mar’15 data ending

Value % Chg. YA – Q1 ‘15FMCG – Value % Share – Q1 ‘15

8.1%

1.1%

25.9%

18.0% 18.8%

11.6%

2.4% 1.4%-1.9% 0.6% 3.4% 2.3%

4.0%

-10%-5%0%5%

10%15%20%25%30%

Unit Value Change Volume Change Nominal Growth

9.6

5

-1

-5

Beverage

Foods

Milk Bases

Cigarette

7

3

-4

PersonalCare

Home Care

BabyProducts

FMCG GROWTH

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

4

-1.1%

1.2% 1.0% 0.9%0.1% 0.1% 0.3%

3.0%

0.7%

2.6%1.3%

4.8%3.9%

10.4%

-3.4%

-1.6% -1.2%

0.3% 1.4%2.6% 2.8%

0.9%

3.4%

2.2%3.9%

5.2% 6.5%

0.3%

-4.5%

-0.4% -0.2%

1.2% 1.5%

2.7%3.1%

3.8% 4.0%4.8%

5.3%

10.0%10.4% 10.7%

Japan Korea Taiwan Australia Singapore Thailand NZ China Vietnam HK Malaysia India Philippines Indonesia

Unit value change Volume change Nominal growth

Fast Moving Consumer Goods market dynamics REGIONAL SUMMARY – Q1 2015

Cop

yri

gh

t ©

20

15

T

he

Nie

lse

n C

om

pa

ny.

Con

fid

en

tia

l a

nd

pro

pri

eta

ry.

5

CONSUMER CONFIDENCE REBOUNDS AT THE HIGHEST LEVEL OVER LAST 2 YEARS WHILE RETAILERS ARE LESS OPTIMISTIC

Source: Nielsen Consumer Confident Global Survey - Q4’14

Source: Consumer Confidence Survey Q4’14 & Retailer Interview (5thJan – 6thFeb): “What are your major concerns over the next 6 months?”

#1 - HEALTH

#2- ECONOMY

CONSUMERS BIGGEST CONCERNS#: Chg. vs. YA

71

RETAILER CONFIDENCE INDEX (RCI) VIETNAM

CONSUMER CONFIDENCE INDEX (CCI) VIETNAM

98 99 98102 106

Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014

RETAILERS BIGGEST CONCERNS

#1 - CONSUMER SUPPORT

#2 - REVENUE / MARGIN

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

6

FMCG GROWTH IS EXPECTED TO BE SLUGGISH OVER THE NEXT FEW QUARTERS

Source: Nielsen Syndicated Forecasting

• EXPECTED AVERAGE FORECAST as the most likely scenario , 95% chance will be within 2-3% of this scenario• EXPECTED MAX FORECAST most likely happens in optimistic market, with the signal of:

• Big increase in FDI. • Strengthening Forex• Big increase in consumer confidence.

• EXPECTED MIN FORECAST most likely happens in pessimistic market, with the signal of:• Recession – 2 periods of declining GDP growth• Tax hikes – introduction of GST, gas prices tax increase • Political turmoil

BUT THERE ARE OPPORTUNITIES

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

8

4 BIG CONSUMER TRENDS

IT’S ALL ABOUT ME

CONNECT ME TO THE

WORLD

I’M ON THE MOVE

I HAVE THEPOWERTO BUY

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

9

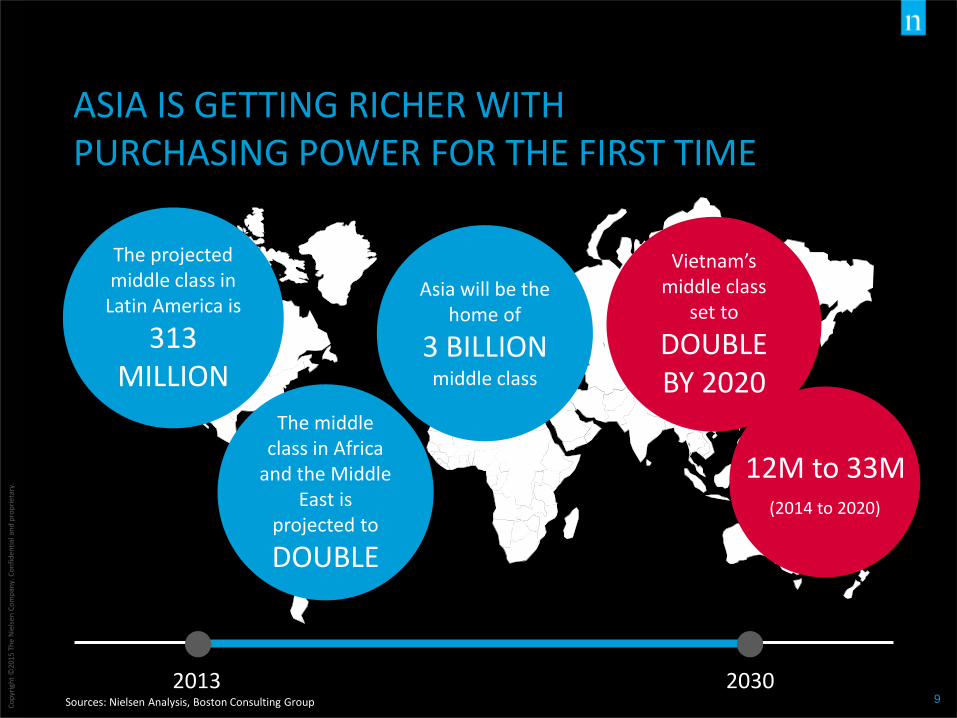

20302013

Asia will be the home of

3 BILLION middle class

The projected middle class in

Latin America is

313 MILLION

The middle class in Africa

and the Middle East is

projected to

DOUBLE

ASIA IS GETTING RICHER WITH PURCHASING POWER FOR THE FIRST TIME

Sources: Nielsen Analysis, Boston Consulting Group

Vietnam’smiddle class

set to

DOUBLE BY 2020

(2014 to 2020)

12M to 33M

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

10

57% population below 35 years old

YOUNG POPULATION

Sources: Data results of the Viet Nam Household Living Standards Survey 2012 – VN GSOStatistical Yearbook of Vietnam 2013 – VN GSOVietnam Urbanization Review 2011 – World BankNielsen Vietnam Pocket Book

ALL SET TO SOAR

HIGH LABOR FORCE13% increase in labor force participation

HIGHER INCOME

44% increase in monthly income per capita(2010 vs. 2012)

MORE EXPENDITURE

32% growth in monthly total consumption expenditure per capita (2010 vs. 2012)

SMALLERHOUSEHOLD SIZEFrom 4.44 to 3.85 people/ household (2002 vs. 2012)

URBANISATION

30% urbanisation rate with 3.4% growth rate per year

QUALITY

73% willing to pay more for higher quality

39% considering health as top concern in life

HEALTH

MORE EDUCATED1.6 times more college/university graduates(2006 vs. 2012)

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

11

VIETNAMESE CONSUMERS ARE DISCERNING

“I will wait until an innovation

has proven itself before

purchasing”(% Agree)

.. and sustained over at least 2 years

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

VIETNAMESE ARE AMONG THE YOUNGEST CONSUMERS IN THE WORLD

Source: US Central Intelligence Agency – The World Fact Book

Nig

eria

Ken

ya

Gh

ana

Paki

stan

Ph

ilip

pin

es

Egyp

t

Sau

di A

rab

ia

S. A

fric

a

Alg

eria

Mal

aysi

a

Mo

rocc

o

VIE

TNA

M

Ind

on

esia

Ku

wai

t

UA

E

Sin

gap

ore

Thai

lan

d

New

zea

lan

d

Au

stra

lia

Ko

rea

Jap

an

18 1921 23 24 25 26 26

27 28 28 29 29 2930

3437 38 38

40

45Median Age of Population

US 38

CHINA 37

VIETNAM 29

DEVELOPING DEVELOPED

12

THE EMERGENCE OF NEW CHANNELS

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

14

RETAILERS RULE IN VIETNAM

Source: Retail Index Universe for # of stores, CIA factbook for Population numbers

# of Traditional Storesin Universe

# of TT stores per Million inhabitants

2,533,025

1,044,014

1,011,115

408,135

33,172

2,253

INDONESIA

PHILIPPINES

VIETNAM

THAILAND

MALAYSIA

SINGAPORE

10,085

9,875

10,934

6,051

1,120

413

URBAN

93% OF SHOPPER SHOP ON

AUTO PILOT

RURAL

9/10 RETAILERS GIVE

RECOMMENDATIONS AND 3/10 BUY BECAUSE

OF THESE

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

15

NEXT UP: E-CONVENIENCE?

Hours per week

Consumers in Asia Pacific are among the most connected in the world

Source: Survey of Internet users Nielsen Cross Platform report

VIETNAM

15.5

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

CONVENIENCE FOOTPRINT IN ASIA IS EXPLODING

X = Growth since 2004Source: Nielsen Retail Census

2.7 X

2 X

2 X

1.4 X

3 X

3 X

1.5 X

CHINA

KOREA

THAILAND

TAIWAN

MALAYSIA

PHILIPPINES

SINGAPORE

Number of Stores In 2014

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

17

147

863

304

130

428

11612

321

98

259

1082

300236

523

11217

421

89

348

1452

313 326

547

10015

602

94

CVS Minimart Super/Hypermarket

CVS Minimart Super/Hypermarket

CVS Minimart Super/Hypermarket

URBAN HCMC HANOI

2012 2013 2014

Number of Modern Trade stores in Vietnam

Source: Nielsen Retail Establishment Survey (RES)

THIS IS STARTING TO HAPPEN IN VIETNAM, BUT IT IS EARLY DAYS

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

18

ENORMOUS OPPORTUNITY IN VIETNAMWhat is the right offer in each area?

Number of People per Convenience Store

Convenience stores are now truly convenient in many countries

1,835

2,300

5,261

5,556

7,040

7,300

21,000

37,000

69,000

KOREA

TAIWAN

HK

THAILAND

MALAYSIA

SINGAPORE

CHINA

PHILIPPINES

VIETNAM

Source: Nielsen Retail Census

(% OF POPULATION)

WHERE TO FROM HERE

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

20

MORE PURCHASING POWERYOU NEED KNOW WHAT MAKES THEM TICK

REACH

WHO WHAT HOW

REACT RESONATE

Driving differentiated outcomes for your business in Vietnam

CONVENIENCE IS NOT A STORE FRONT, IT’S A WAY OF LIFE