Via E-Filing Michigan Public Service Commission 7109 W ...

114

October 28, 2019 Ms. Lisa Felice Via E-Filing Michigan Public Service Commission 7109 W. Saginaw Hwy. P. O. Box 30221 Lansing, MI 48909 RE: MPSC Case No. U-20373 Dear Ms. Felice: The following is attached for paperless electronic filing: Direct Testimony of Chris Neme on behalf of the Natural Resources Defense Council Exhibits NRD-1 through NRD-11 Proof of Service Sincerely, Lydia Barbash-Riley [email protected] xc: Parties to Case No. U-20373

Transcript of Via E-Filing Michigan Public Service Commission 7109 W ...

October 28, 2019 Ms. Lisa Felice Via E-Filing Michigan Public Service Commission 7109 W. Saginaw Hwy. P. O. Box 30221 Lansing, MI 48909 RE: MPSC Case No. U-20373 Dear Ms. Felice: The following is attached for paperless electronic filing: Direct Testimony of Chris Neme on behalf of the Natural Resources Defense Council Exhibits NRD-1 through NRD-11 Proof of Service Sincerely, Lydia Barbash-Riley [email protected] xc: Parties to Case No. U-20373

STATE OF MICHIGAN

BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION

In the matter, on the Commission’s own motion, regarding the regulatory reviews, revisions, determinations, and/or approvals necessary for DTE ELECTRIC COMPANY to fully comply with Public Act 295 of 2008, as amended by Public Act 342 of 2016

U-20373

ALJ Sharon Feldman

______________________________________________________________________

DIRECT TESTIMONY OF CHRIS NEME

ON BEHALF OF NATURAL RESOURCES DEFENSE COUNCIL

October 28, 2019

TABLE OF CONTENTS

I. INTRODUCTIONS AND QUALIFICATIONS.................................................................. 2

II. TESTIMONY OVERVIEW ................................................................................................. 7

III. DTE SHOULD INCREASE FOCUS ON ELECTRICALLY-HEATED LOW INCOMECUSTOMERS .................................................................................................................... 12

IV. DTE’S PROPOSED PERFORMANCE METRICS SHOULD BE MODIFIED .............. 19

A. DTE's Proposal .............................................................................................................19

B. An Appropriate Average Measure Life for Lifetime Savings Metric...........................23

C. An Alternative to DTE's Proposed Low Income Spending Metric ..............................27

V. DTE SHOULD USE MARGINAL LINE LOSSES WHEN ASSESSING EFFICIENCYCOST-EFFECTIVENESS................................................................................................ 322

VI. DTE SHOULD INCREASE FIRST YEAR SAVINGS TO 2.00% OF SALES ............... 38

A. Overview ......................................................................................................................38

B. DSMore Analyses Suggest Economically Optimal Savings is at Least 2.00% ...........40

C. IRP Suggests 2.00% EWR Savings is Least Cost if End Effects Problem Fixed ........43

i

2

I. INTRODUCTIONS AND QUALIFICATIONS 1

Q: Please state your name, employer and business address. 2

A: My name is Chris Neme. I am a co-founder and Principal of Energy Futures Group, a 3

consulting firm that provides specialized expertise on energy efficiency, demand response, 4

renewable energy and other clean energy markets, programs and policies. My business 5

address is P.O. Box 587, Hinesburg, VT 05461. 6

Q: Please describe your educational background. 7

A: I received a Master of Public Policy degree from the University of Michigan (Ann Arbor) in 8

1986. That is a two-year, multi-disciplinary degree focused on applied economics, statistics 9

and policy development. I also received a Bachelor’s degree in Political Science from the 10

University of Michigan (Ann Arbor) in 1985. My first year of graduate school counted 11

towards both my Masters’ and Bachelor’s degrees. 12

Q: Please summarize your business and professional experience. 13

A: I have worked in the energy industry for more than twenty-five years for clients in more than 14

30 different states, half a dozen Canadian provinces and several European countries. Much 15

of my work has focused on energy efficiency markets, programs and policies. That includes 16

work to develop or review energy efficiency potential studies; develop or review Technical 17

Reference Manuals (“TRM”) of deemed savings assumptions (including the Michigan, Ohio, 18

Illinois and Ontario TRMs); support utility-stakeholder “collaboratives” (including those in 19

Michigan, Illinois and Ohio); negotiate or support development of efficiency program 20

performance incentive mechanisms (including the current Michigan and Ontario 21

3

mechanisms, as well as the mechanism included in Illinois’ Future Energy Jobs Act passed 1

in late 2016); review or develop efficiency programs; and/or review or develop utility load 2

forecasts. I have also worked on demand response issues, distribution system planning 3

issues, non-wires alternatives, the bidding of energy efficiency resources into capacity 4

markets, and forecasts and analyses of the impacts of strategic electrification. In addition, I 5

have led training sessions on efficiency program design, cost-effectiveness analysis of 6

distributed energy resources and other clean energy issues; published widely on a range of 7

topics; and served on numerous national and regional efficiency committees, working groups 8

and forums. 9

I co-founded Energy Futures Group in 2010. Since then I have played lead roles in a variety 10

of energy efficiency consulting projects. Recent examples include: 11

• Representing NRDC in both informal consultations and contested regulatory12

proceedings in Michigan, Illinois and Ohio on energy efficiency and demand response13

program designs, cost-effectiveness analyses, evaluation, and shareholder incentive14

structures; distribution system planning and non-wires alternatives; and integrated15

resource planning;16

• Helping the National Association of Regulatory Utility Commissioners and the17

Michigan Public Service Commission assess the relative merits of alternative18

approaches to defining savings goals for utility efficiency programs (focusing on19

lifetime savings);20

• Serving as an appointed expert representative on the Ontario Energy Board’s21

Evaluation and Audit Committee for gas demand-side management;22

4

• Serving on the Management Committee and leading strategic planning and program1

design for a team of firms, led by Applied Energy Group, that was hired by the New2

Jersey Board of Public Utilities to deliver the electric and gas utility-funded New Jersey3

Clean Energy Programs;4

• Co-authoring the National Standard Practice Manual for Assessing Cost-Effectiveness5

of Energy Efficiency cost-effectiveness screening of energy efficiency measures,6

programs and portfolios, which was published in May 2017, as well as a new Manual,7

scheduled to be published next year (2020), that will address cost-effectiveness8

frameworks for all distributed energy resources;9

• Leading a project for the Northeast Energy Efficiency Partnerships (“NEEP”) to10

document lessons learned from utility and other efforts across the United States over11

the past 25 years to use geographically targeted efficiency programs (sometimes in12

concert with other distributed resources) to cost-effectively defer capital investment in13

transmission and/or distribution system infrastructure; and14

• Drafting policy reports for the Regulatory Assistance Project on a variety of energy15

efficiency and related regulatory policy issues, such as whether 30% electric savings is16

achievable in ten years, the history of efforts across the United States to use17

geographically targeted efficiency programs to cost-effectively defer transmission and18

distribution system investments, and the history of bidding of efficiency resources into19

the PJM and New England capacity markets.20

5

Prior to co-founding Energy Futures Group in 2010, I worked for 17 years for the Vermont 1

Energy Investment Corporation (“VEIC”), the last 10 as Director of its Consulting Division 2

managing a group of 30 professionals with offices in three states. 3

A copy of my curriculum vitae is attached as Exhibit NRD-1. 4

Q: Have you previously filed expert witness testimony in other proceedings before the 5

Commission? 6

A: Yes. I filed testimony in the following Michigan Public Service Commission Dockets: 7

• U-20471, regarding DTE’s assessment of energy efficiency resources in its Integrated 8

Resource Plan; 9

• U-20164, regarding Consumers Energy’s proposed new shareholder incentive 10

mechanism for demand response programs; 11

• U-18419, regarding DTE’s assessment of efficiency potential as part of its IRP put 12

forward by the Company in support of a proposed new gas-fired power plant; 13

• U-18268, regarding DTE’s proposed 2018-2019 gas energy efficiency programs 14

(Energy Waste Reduction) plan; 15

• U-18262, regarding DTE’s proposed 2018-2019 electric energy efficiency programs 16

(Energy Waste Reduction) plan; 17

• U-18261, regarding Consumers Energy Company’s proposed 2018-2021 energy 18

efficiency programs (Energy Waste Reduction) plan; 19

6

• U-17771, regarding Consumers Energy Company’s proposed amendment to its 2017 1

energy efficiency programs (Energy Waste Reduction) plan; 2

• U-17762, regarding DTE’s proposed amendment to its 2017 energy efficiency 3

programs (Energy Waste Reduction) plan; 4

• U-17429, regarding Consumers Energy’s estimates of energy efficiency potential in its 5

assessment of alternatives to its proposal to construct a new 700 MW gas-fired power 6

plant (Thetford); 7

• U-17138, regarding Consumers Energy’s proposed modifications to its 2013-2015 8

Energy Optimization plans; 9

• U-17049, regarding DTE’s proposed modifications to its 2013-2015 Energy 10

Optimization plan; 11

• U-16670, regarding Consumers Energy’s biennial review and Amended Energy 12

Optimization plan; and 13

• U-16671, regarding DTE’s biennial review and Amended Energy Optimization plan. 14

Q: Have you been an expert witness on energy efficiency matters before other regulatory 15

commissions? 16

A: Yes, I have filed expert witness testimony on more than 40 occasions before similar 17

regulatory bodies in eleven other states and provinces, including the neighboring 18

jurisdictions of Ohio, Illinois and Ontario. 19

7

Q: Are you sponsoring any exhibits? 1

A: Yes, I am sponsoring the following exhibits: 2

NRD-1: 3

NRD-2: 4

NRD-3: 5 6 7

NRD-4: 8

NRD-5: 9

NRD-6: 10 11 12

NRD-7: 13 14

NRD-8: 15 16

NRD-9: 17

NRD-10: 18 19

NRD-11: 20

Christopher Neme CV

DTE Electric’s Response to NRDCDE-1.25a

DTE Electric’s Response to NRDCDE-1.5 with Attachment NRDCDE-1.5-01 2016 DTE Appliance Saturation Survey – Question 12 and Question 14

Table CE3.3 of the 2015 Residential Energy Consumption Survey

DTE Electric’s Response to NRDCDE-1.25di through 1.25diii

DTE Electric’s Response to NRDCDE-1.1ai with Attachment NRDCDE-1.1ai-01 DSMore 2018 Batch Tool -2020-2021 EWR Plan – Res Utility Input and C&I Utility Input tabs

NRDCDE-1.1aix1, aix3b, and aix4 with Attachment NRDCDE-1.1aix4-01 Line Loss Study 1999

Valuing the Contribution of Energy Efficiency to Avoided Marginal Line Losses

U-20471 DTE Electric’s Response to MECNRDCSCDE-4.24eii4

U-20471 WP LKM-650 2018 Rev Req Working Model – Rev Requirement Summary Tab

U-20471 WP KLB-26 EWR DSMore Aggregation 1.50%_Tiered Costs –Test Results Tab21

II. TESTIMONY OVERVIEW22

Q: What is the purpose of your testimony? 23

A: My testimony addresses the reasonableness of DTE’s proposed electric Energy Waste 24

Reduction (“EWR”) plan for 2020 and 2021. 25

8

Q: What are your summary findings? 1

A: DTE’s EWR plan has a number of good attributes. For example, it has a broad and fairly 2

comprehensive set of efficiency program offerings. That said, I have several concerns with 3

the plan. They are as follows: 4

• DTE is not adequately addressing opportunities to retrofit electrically-heated low 5

income housing, both single family and multi-family. 19% of DTE customers with 6

annual incomes below $20,000, and 12% of DTE customers with annual incomes 7

between $20,000 and $60,000, reside in homes whose primary heating fuel is 8

electricity. However, very few of those electrically heated customers have participated 9

in DTE’s low income efficiency programs – only about 0.5% of the 17,000 participants 10

in its 2018 programs and only about 0.2% of the more than 11,000 participants in the 11

first eight months of 2019. Electrically heated homes typically offer substantial 12

opportunities for low income electricity savings. Indeed, to the extent that low income 13

homes use electric resistance heat – and it appears that many do – retrofitting cold 14

climate heat pumps, coupled with sealing air leaks and upgrading insulation where 15

feasible and appropriate, is likely to reduce customers’ heating bills by 40-50% or 16

more.1 That would have both much greater immediate impact and much greater longer-17

term impact on low income energy affordability than just installing efficient lighting 18

and other low-cost measures. 19

1 Note that most electrically heated homes also have electric water heaters. Thus, there is often also an opportunity for acquiring significant additional electric savings in such buildings by replacing existing in efficient electric water heaters with very efficient heat pump water heaters.

9

• DTE’s proposed low income performance metric – dollars of low income program 1

spending – is not appropriate. DTE has proposed that 25% of its maximum 2

shareholder incentive be tied to the amount of money it spends on its low income 3

efficiency programs.2 However, money can be spent well or poorly; it can produce 4

large benefits for program participants or more modest benefits. Thus, the utility 5

should not be rewarded for simply spending money – without regard to how effectively 6

it was spent. Instead, performance should ideally be measured in outcomes that truly 7

make a difference for low income customers, such as lifetime energy savings produced 8

and/or other indicators of the depth of savings achieved in participating low income 9

buildings (deep savings is typically necessary to have a meaningful impact on reducing 10

energy burdens and improving the comfort and well-being of low-income customers). 11

Given limited data available on how much lifetime savings DTE could acquire by more 12

comprehensively addressing low income efficiency opportunities, including 13

opportunities from electrically-heated homes, it may be reasonable for this two-year 14

plan cycle to base part of DTE’s low income performance metric on spending. 15

However, the maximum incentive for spending should be tied to spending levels 16

necessary to begin to treat significant numbers of electrically heated single family and 17

multi-family homes. And the weight assigned to the spending metric should be only 18

10% rather than the 25% proposed by the Company. In addition, to ensure that the 19

Company begins to effectively address those electric space heat opportunities, I 20

recommend that there also be a low income performance metric tied to the number of 21

heat pumps retrofitted into low income homes to displace inefficient electric resistance 22

2 DTE Exhibit A-8.

10

heat, with the maximum incentive tied to installing 500 heat pumps in 2020 and 1000 1

heat pumps in 2021. I recommend that this metric be assigned the other 15% of weight 2

for low income metrics. 3

• DTE’s lifetime savings metric is based on too low of an average measure life. The 4

Company has estimated that it will achieve 1.625% first year savings with an average 5

measure life of 12.11 years in 2020 and 1.75% first year savings with an average 6

measure life of 12.29 years in 2021.3 However, it proposes that it be able to earn its 7

maximum shareholder incentive if it achieves 1.50% savings with an average measure 8

life of 11 years. In other words, it is proposing that it earn its maximum shareholder 9

incentive at lifetime savings that are 16% below its forecast savings in 2020 and 23% 10

below its forecast savings in 2021. That is not reasonable. While the Company is 11

permitted by statute to maximize its shareholder incentive at first year savings equal to 12

1.50% of sales, there is no reason that the lifetime savings target should not be equal to 13

1.50% first year savings multiplied by the average measure life the company is 14

proposing (i.e., 12.11 years in 2020 and 12.29 years in 2021). That would still be 7% 15

and 14% below the lifetime savings it is planning to achieve in 2020 and 2021, 16

respectively. 17

• DTE continues to use average loss rates rather than marginal loss rates when 18

assessing the generation-level impacts and cost-effectiveness of efficiency 19

programs. Marginal loss rates are typically about 150% of average loss rates. And 20

marginal loss rates during peak hours are typically 300% of average annual loss rates. 21

3 DTE Application, page 4; DTE Exhibit A-4.

11

Thus, by continuing to use average loss rates, DTE continues to understate the impacts 1

and cost-effectiveness of its efficiency programs. The Company should be required to 2

begin using marginal loss rates, using the multipliers I just referenced until it has 3

completed a new line loss study which provides better values for DTE’s service 4

territory. 5

• DTE’s proposed savings target – ramping up to 1.75% of sales – is lower than the 6

economically optimal level of savings. As I discuss in my testimony in DTE’s IRP 7

case (U-20471), the Company’s own analyses using DSMore – the analytical tool it 8

uses to assess the cost-effectiveness of its EWR portfolios – show that 2.00% savings 9

per year produces greater net benefits for its customers than 1.75% savings per year. 10

While the Company’s IRP modeling suggested that 1.75% per year was economically 11

preferable to a 2.00% savings level, that was largely because the Company’s IRP 12

analysis included virtually all of the increase in costs associated with increasing savings 13

from 1.75% to 2.00%, but only about 85% of the increase in benefits (a problem which 14

does not exist in its DSMore analyses). When that bias is corrected, the Company’s 15

IRP model also suggests that 2.00% savings per year is the economically optimal level 16

of efficiency savings. 17

Also, though I do not comprehensively address potential concerns with DTE’s approach to 18

design and delivery of its low income multi-family program, I am familiar with and support 19

the testimony of National Housing Trust witness Annika Brink on that issue. 20

12

III. DTE SHOULD INCREASE FOCUS ON ELECTRICALLY-HEATED LOW 1 INCOME CUSTOMERS2

Q: Do DTE’s low income programs serve electrically heated customers? 3

A: Electrically-heated customers are eligible to participate in DTE’s low income programs. 4

However, the participation of electrically heated customers in those programs is extremely 5

low. Indeed, as Table 1 shows, only two of the more than 10,000 multi-family housing units 6

treated through its low income program between January 2018 and August 2019 (i.e., less 7

than 0.02%) were electrically heated. Similarly, only three of the more than 7,000 Home 8

Energy Consultation participants between January 2018 and August 2019 (less than 0.04%) 9

were electrically heated. And only 108 of the nearly 10,000 customers treated through the 10

Energy Efficiency Assistance program between January 2018 and August 2019 (about 1.1%) 11

were electrically heated. 12

Table 1: Electrically-Heated Customers in DTE 2018/2019 Low Income Programs4 13

14

Q: Are those numbers concerning? 15

A: Yes, because they mean that DTE is not addressing the opportunity to generate very large 16

electric bill savings for a significant portion of its low income customers. 17

4 Exhibit NRD-2, Response to NRDCDE-1.25a.

20182019 thru

August 20182019 thru

August 20182019 thru

August 20182019 thru

AugustLow Income 6146 4353 4644 3081 5956 3655 16,746 11,089 Low Income Elec Heat 2 0 1 2 88 20 91 22 % Elec Heat Customers 0.03% 0.00% 0.02% 0.06% 1.48% 0.55% 0.54% 0.20%

Multi-FamilyHome Energy Consultation

Energy Efficiency Assistance Total

13

Q: What portion of DTE low income customers heat primarily with electricity? 1

A: DTE’s 2016 appliance saturation survey suggests that about 11% of all its residential 2

customers use electricity as their primary heating fuel,5 with the numbers skewed towards 3

lower income customers. Indeed, nearly 19% of all residential households with incomes less 4

than $20,000 per year and 12% of all households with incomes between $20,000 and $59,000 5

per year used electricity as their primary heating fuel.6 In other words, the fraction of DTE 6

low income customers with electric heat is on the order of 10 to 20 times greater than the 7

fraction of electrically heated customers treated through DTE’s Energy Efficiency Assistance 8

program and nearly a thousand times greater than the fraction of electrically heated 9

customers treated through DTE’s Low Income Multi-Family program. 10

Q: Why is it important that DTE’s low income programs serve electrically-heated low 11

income customers in numbers more representative of the electrically-heated low 12

income population? 13

A: In a climate like Michigan’s, nearly 60% of all residential energy consumption is associated 14

with space heating.7 Thus, if the Company is not reaching low income customers with 15

electric heat, those low income customers do not have the opportunity to improve efficiency 16

of by far the largest portion of their energy consumption. That is particularly important when 17

5 This is a little more than the statewide average of 9% according to U.S. Census data (see: https://factfinder.census.gov/faces/tableservices/jsf/pages/productview.xhtml?pid=ACS_17_5YR_B25040&prodType=table) 6 Exhibit NRD-3, Attachment to Response to NRDCDE-1.5, U-20373 NRDCDE-1.5-01 2016 DTE Appliance Saturation Survey, Questions 12-13, page 2 (Response to Question 12). 7 Exhibit NRD-4, U.S. Energy Information Administration’s 2015 Residential Energy Consumption Survey Table CE3.3 (Annual Household Site End-Use Consumption in the Midwest – Totals and Averages, 2015), data for the East North Central region, which is comprised of the states of Michigan, Wisconsin, Ohio, Indiana and Illinois is available at https://www.eia.gov/consumption/residential/data/2015/index.php?view=consumption#by%20end%20uses.

14

one considers that electricity prices are currently considerably higher than natural gas prices 1

in Michigan.8 As a result, all other things being equal, the energy burden of electrically 2

heated low income customers will be much greater than the energy burden of gas heated low 3

income customers. Again, this should put a premium on efforts to enroll electrically heated 4

customers into the Company’s efficiency programs. 5

Q: How could DTE’s low income efficiency programs produce very large bill savings for 6

those electrically-heated low income customers? 7

A: Broadly speaking, there are two ways to reduce electric space heating consumption in 8

electrically heated homes. First, one can improve the efficiency of the building through air 9

leakage reduction and insulation upgrades so that less heat is needed. Second, one can 10

displace inefficient electric heating technology with more efficient technology such as cold 11

climate heat pumps. lt is worth noting that of those DTE low income customers heating 12

primarily with electricity, about half appear to heat with very inefficient electric resistance 13

heat.9 Cold climate heat pumps typically consume 50-70% less electricity per unit of heat 14

8 For example, the residential winter gas price used in the Company’s DSMore analyses is about $0.70/CCF (“Res Utility Input” tab to NRDCDE-1.1ai-01 DSMore 2018 Batch Tool – 2020-2021 EWR Plan.xlsx). That translates to about $7 per MMBtu of site energy used. In contrast, the residential winter electric rate used in the Company’s DSMore analyses is 14.4 cents/kWh, which translates to about $42 per MMBtu of site energy provided – or roughly six times the gas price. A little of that difference would be offset by the difference in efficiency between electric resistance heat (100%) and gas heating equipment (80% to 95%). Also, the Company has a variety of electric rate options, some of which may lead to somewhat lower electricity costs for electric space heat (see: https://www.newlook.dteenergy.com/wps/wcm/connect/23195474-a4d1-4d38-aa30-a4426fd3336b/WholeHouseRateOptions.pdf?MOD=AJPERES&CACHEID=23195474-a4d1-4d38-aa30-a4426fd3336b). However, none of the electric rate options would be low enough to come close to fully offsetting the difference in cost between electric resistance space heat and cost of gas space heat. 9 Exhibit NRD-3, Attachment to Response to NRDCDE-1.5, U-20373 NRDCDE-1.5-01 2016 DTE Appliance Saturation Survey, Questions 12-13, page 3 (Response to Question 13).

15

delivered to a home than inefficient electric resistance heat.10 Thus, a heat pump retrofit that 1

fully displaced electric resistance heat could lower the variable component of a customers’ 2

annual electric bill by 30-40%; a heat pump that displaced only half of the electric resistance 3

heat would lower the variable component of a customer’s annual electric bill by 15-20%.11 4

Q: What explanation has DTE offered for why its low income programs have addressed 5

such a small number of electrically-heated customers? 6

A: DTE states that its multi-family low income program “has and will continue to market to 7

electrically heated customers”, but that that the historically very low participation of 8

electrically heated customers suggests “this is a limited market.”12 9

The Company states that its Home Energy Consultation and Energy Efficiency Assistance 10

programs “plan to market to electrically heated customers in 2020 and 2021.” This response 11

would seem to imply that those two programs did not market to electrically heated customers 12

in 2018 and 2019. 13

Q: Is DTE’s conclusion that electrically-heated, low income multi-family buildings are a 14

“limited market” reasonable? 15

A: No. As I have already explained, the fraction of DTE low income customers heating 16

primarily with electricity is orders of magnitude greater than the participation rates of 17

10 For example, see Faesy, Richard et al., Ductless Heat Pump Meta Study, published by Northeast Energy Efficiency Partnerships, November 13, 2014 (https://neep.org/sites/default/files/products/NEEP-Ductless-Heat-Pump-Meta-Study-Report_11-13-14.pdf) which estimated average season COPs of between 2.4 and 3.0. 11 These estimates are rough approximations designed to illustrate the significance of the energy savings that can be provided by heat pumps. They were derived by simply multiplying 50-70% space heating savings by the average of 60% of energy consumed for space heating. 12 Exhibit NRD-5, Responses to NRDCDE-1.25di-iii, page 1 (Response to NRDCDE-1.25di).

16

electrically heated customers in DTE’s low income programs. While DTE data on the 1

breakdown of electric heat between single family and multi-family buildings is not available, 2

in my experience in northern climates electric heat tends to be more prevalent in multi-family 3

buildings than in single family buildings.13 This suggests that the extremely low levels of 4

electrically heated homes historically participating in the Company’s low income multi-5

family program is a function of program marketing and/or program design rather than a 6

function of size of the market. 7

Q: Is there any evidence to suggest that DTE is planning to ramp up participation by 8

electrically-heated low income customers? 9

A: DTE has indicated that it plans to offer new (i.e., for the first time) incentives for heat pumps 10

in its low income Audit and Weatherization and Energy Assistance programs. That is a 11

positive development.14 And the Company has indicated that it will continue to offer 12

prescriptive rebates for packaged terminal heat pumps and custom incentives for ductless 13

mini-split heat pumps through its low income multi-family program, which is also a positive. 14

13 For example, Commonwealth Edison, the utility serving the Chicago area, estimates that about 10% of all its customers use electricity as their primary heating fuel, but that masks significant differences between its multi-family customers – 24% of which are electrically-heated – and its single family customers – only 4% of which are electrically-heated (Opinion Dynamics, ComEd Residential Saturation/End-Use, Market Penetration & Behavioral Study, April 2013, filed by ComEd as Exhibit 1.0, Appendix E in Illinois Commerce Commission Docket 13-0495, available at https://www.icc.illinois.gov/docket/files.aspx?no=13-0495&docId=202448). Though I am unaware of comparable data for DTE regarding the difference between multi-family and single family saturations of primary electric heat, Census data suggest that the percent of renter-occupied Michigan homes using electricity as their primary heating fuel (19%) is almost four times greater than the percent of owner-occupied homes using electricity as their primary heating fuel (5%). (see:https://factfinder.census.gov/faces/tableservices/jsf/pages/productview.xhtml?pid=ACS_17_5YR_B25117&prodType=table). While not all renters live in multi-family buildings, I would expect them to be disproportionately living in multi-family buildings. Indeed, Census data also show that there are more than ten times as many renters in multi-family buildings as in single family buildings in Michigan (https://factfinder.census.gov/faces/tableservices/jsf/pages/productview.xhtml?pid=ACS_17_1YR_B25033&prodType=table). 14 Exhibit NRD-5, page 2 (Response to NRDCDE-1.25dii).

17

However, DTE has provided no evidence to suggest it is making special or concerted efforts 1

to target market its low income programs to electrically-heated customers.15 Moreover, 2

when I reviewed the list of measures comprising the Company’s build-up of its savings 3

estimates for its 2020 and 2021 low income efficiency programs,16 I found no evidence to 4

suggest the Company is expecting to produce any savings through those programs from heat 5

pump measures. Indeed, the Company appears to be forecasting savings from only one space 6

heating heat pump measure in its entire program portfolio – SEER 21 mini-split heat pumps 7

in its (non-low income) Residential HVAC program. And that measure has only 25 forecast 8

participants in 2020. Though the Company did assume some savings from air leakage 9

reduction and insulation measures in its Energy Efficiency Assistance program, the assumed 10

savings per measure are quite modest, suggesting that the measures are only forecast to be 11

installed in gas heated homes in which they would provide some cooling and/or furnace fan 12

savings (rather than the much more substantial savings that would be realized if they were 13

installed in electrically-heated homes). And there are no HVAC or building envelop 14

measures assumed to provide savings in the Company’s Multi-Family Low Income program. 15

In fact, only five efficiency measures are assumed to provide any electric savings in that 16

program – four different kinds of light bulbs and an efficient refrigerator/freezer measure. 17

That limited measure list is not going to provide the depth of electric savings necessary to 18

significantly affect the energy burdens of low income multi-family customers. It is also 19

15 For example, there is no suggestion of target marketing electrically heated customers in the descriptions of the Energy Efficiency Assistance or Low Income Multifamily program descriptions in DTE Exhibit A-9 (pages 43-50). 16 Attachment to Response to NRDCDE-1.1ai, NRDCDE-1.1ai-01 DSMore 2018 Batch Tool - 2020-2021 EWR Plan.xlsb.

18

inconsistent with the concept of comprehensive treatment of efficiency opportunities that is 1

discussed in greater detail in the testimony of National Housing Trust witness Annika Brink. 2

Q: Given DTE’s new heat pump incentive offerings, is it possible that the Company will 3

acquire substantial savings from electrically heated low income homes, but has 4

conservatively not accounted for those savings in its program forecasts? 5

A: It is possible that the Company’s filed plan understates the savings it will acquire from 6

electrically heated low income customers. However, to the extent that is the case, the 7

Company has also likely understated spending on those low income programs because heat 8

pump retrofits are expensive. And that could create a perverse incentive for the Company to 9

not aggressively pursue opportunities for such retrofits in order to manage its budget. 10

Further, the Company is changing nothing about its heat pump incentives for electrically-11

heated multi-family buildings. Since the Company has had virtually no electrically heated 12

multi-family participants in its programs in recent years, it is clear that either its rebate 13

offerings are inadequate and/or its efforts to recruit participation from electrically heated 14

buildings would need to be changed in order to gain significant traction in that market. 15

Nothing about what the Company has put forward in its filing suggest any such changes are 16

planned. 17

Q: How do you recommend that DTE’s plan be changed to ensure that the Company more 18

effectively addresses substantial savings opportunities from electrically heated low 19

income customers? 20

A: First, I recommend that the Company add $2.5 million to its 2020 low income program 21

budgets and $5.0 million to its 2021 low income program budgets. That should enable the 22

19

Company to pay for the full cost of approximately 500 heat pumps in 2020 and 1000 heat 1

pumps in 2021.17 The heat pumps should be installed in both single family homes and multi-2

family apartments with electric resistance heat (either electric furnaces or electric baseboard 3

heating systems). The heat pumps should be cold climate models whenever feasible and 4

economic, as they are able to efficiently address heating needs during much more of the 5

Michigan winter than standard air source heat pump products. 6

Second, I recommend that the Company initiate an aggressive effort to identify and recruit 7

low electrically heated low income customers to its programs. Analysis of its own billing 8

data, and historical usage patterns by season, should enable target marketing. 9

Finally, as I discuss in the next section of my testimony, DTE’s shareholder incentive 10

mechanism should have a performance metric related to the number of low income heat 11

pump installations achieved through its programs. 12

IV. DTE’S PROPOSED PERFORMANCE METRICS SHOULD BE MODIFIED13

A. DTE’s Proposal14

Q: Please summarize DTE proposed shareholder incentive mechanism? 15

A: As shown in Exhibit A-8 to Jason Kupser’s direct testimony, DTE has proposed a 16

performance incentive mechanism that would enable its shareholders to earn between 15% 17

17 DTE estimates that a SEER 18 Ductless Mini-Split costs about $3000 and a centrally ducted SEER 16 costs about $5700. See Exhibit NRD-5, page 3 (Response to NRDCDE-1.25diii). The budget increase I have proposed should be enough to cover a reasonable mix of those two systems, including some additional marketing costs to recruit electrically-heated participants.

20

and 20% of efficiency program spending based on the performance of its efficiency programs 1

relative to three metrics: 2

• First year MWh savings (as a percent of annual sales) from its entire program3

portfolio;4

• Lifetime MWh savings from its entire efficiency program portfolio; and5

• Low income program spending.6

The Company would not earn any performance incentives just for meeting first year savings 7

targets. Rather, the Company’s performance on first year MWh savings establishes the 8

“ceiling” on what it can earn. That ceiling starts at 15% of program spending for achieving 9

1.00% first year savings and increases linearly to 20% of spending for achieving 1.50% first 10

year savings. 11

The actual shareholder incentive earned would then be a function of how well DTE 12

performed relative to the other two metrics. The Company would earn 12% of efficiency 13

program portfolio spending for reaching its “100% target” for lifetime savings and 16% of 14

spending for reaching 150% of its lifetime savings target. It would earn 3% of efficiency 15

program portfolio spending as an incentive for its “100% target” for low income spending 16

and 5% of spending as an incentive for spending 150% of that amount. Put another way, the 17

Company has assigned an 80% weight to the portfolio lifetime MWh savings metric and a 18

25% weight to the low income spending metric. The fact that those weights add up to more 19

than 100% means that the Company does not have to maximize performance on both metrics 20

in order to earn the maximum 20% of spending permitted. 21

21

Q: How did DTE establish its proposed “100% targets” for the lifetime MWh savings and 1

low income spending metrics? 2

A: The 100% target for the lifetime MWh savings target is equal to the first year savings target 3

expressed in MWh multiplied by an average annual savings life of 11 years.18 However, 4

DTE is also proposing that the lifetime savings target be reduced in the event that there are 5

changes to the assumed measure life for LED light bulbs, with the reduction being equal to 6

the reduction in lifetime savings per light bulb multiplied by the number of LED light bulbs 7

the Company is currently planning to installed through its residential programs. 8

The 100% target for low income spending is equal to two-thirds of the Company’s planned 9

low income spending, such that the Company would earn its maximum low income incentive 10

for simply spending the amount it is budgeting for its low income programs. 11

Q: How does DTE’s proposed shareholder incentive mechanism compare to the 12

mechanism approved for its previous EWR plan? 13

A: DTE’s proposed shareholder incentive mechanism differs from the mechanism approved for 14

its previous EWR plan in a couple of important ways, one structural and another contextual. 15

The structural difference is that the mechanism approved for its previous EWR plan had two 16

different low income metrics – one (with 15% weight) based on low income spending and 17

another (with 10% weight) based on the percentage of multi-family buildings that received 18

comprehensive energy assessments (an indicator of comprehensiveness in addressing 19

18 Direct Testimony of Jason Kupser, page 39.

22

efficiency opportunities) – rather than just the one spending metric DTE is currently 1

proposing for 2020 and 2021.19 2

The contextual difference is that the EWR plan DTE has proposed in this proceeding is 3

designed – and budgeted – to achieve greater lifetime savings than the Company’s last EWR 4

plan. 5

Q: Do you consider DTE’s proposed shareholder incentive mechanism for 2020 and 2021 6

to be reasonable? 7

A: There are a number of elements of DTE’s proposal that are reasonable given the objectives 8

of its EWR plan. For example, I strongly support DTE’s proposal to use first year savings 9

solely to establish the ceiling for shareholder incentives, as first year savings are not the best 10

indicator of the value of energy savings. I also strongly support DTE’s proposal to place 11

80% weight on the portfolio lifetime savings metric because lifetime savings are a much 12

better indicator of the value of efficiency investments. I also strongly support the Company’s 13

proposal to include a low income performance metric. Because low income programs 14

generally produce savings at a much higher cost than non-low income programs, a 15

shareholder incentive mechanism that only rewarded total savings would create a 16

disincentive to invest in low income programs. Having counter-balancing performance 17

metrics for low income programs ensures that the Company will devote attention and 18

resources to such programs, which is important to ensuring that the customers who are likely 19

most in need and who would benefit most from efficiency investments have the opportunity 20

to do so. Finally, I support the Company’s proposal to have the sum of the weights for the 21

19 Case No. U-18262, April 12, 2018, Order Approving Settlement Agreement, Attachment D.

23

different performance metrics to add up to a little more than 100%, as I think it is reasonable 1

to allow a utility to earn its maximum incentive without having to have achieved the highest 2

possible performance on every metric (as long as it has to perform at least very well on every 3

metric).20 4

That said, there are a couple of elements of DTE’s proposal that I consider to be problematic. 5

Specifically, I think it is unreasonable to base the Company’s portfolio lifetime savings goals 6

on an average measure life of 11 years when its forecast average is over 12 years. Second, I 7

think it is unreasonable to measure and reward low income performance based solely upon 8

how much money is spent rather than on the results of that spending (i.e., the benefits that 9

low income customers realize from that spending). I discuss each of these concerns below. 10

B. An Appropriate Average Measure Life for Lifetime Savings Metrics11

Q: Please summarize the nature of your concern about DTE’s proposal to base its portfolio 12

lifetime savings metric on an average measure life of 11 years? 13

A: The Company has estimated that the average life of the savings it will achieve in 2020 is 14

greater than 11 years. For 2020, the Company estimates an average life of 12.11 years; for 15

2021, it estimates an average life of 12.29 years.21 Thus, the Company is proposing that its 16

portfolio lifetime savings metrics be based on an average measure life that is about 10% less 17

than it plans to achieve. 18

20 For example, under DTE’s proposal, if the Company achieved 150% of its portfolio lifetime savings metric, it would still have to achieve 125% of its low income metric to earn its maximum incentive; alternatively, if it achieved 150% of its low income metric, it would still have to achieve 137.5% of its portfolio lifetime savings metric to earn its maximum incentive. 21 Direct Testimony of Jason Kupser, page 37; DTE Exhibit A-4.

24

Furthermore, as I noted above, DTE is planning – and budgeting – to achieve first year 1

savings of 1.625% in 2020 and 1.75% in 2021. That is 8% to 17% more than the first year 2

savings levels upon which its maximum shareholder incentive proposal is based. 3

As Table 2 shows, the combined effects of these two factors is that DTE is proposing that it 4

earn its maximum shareholder incentive – or at least the portion of the maximum incentive 5

tied to portfolio lifetime savings – if it achieved only 84% of its planned savings in 2020 and 6

only 77% of its planned savings in 2021. That level of savings achievement, relative to 7

planned savings, would be far from exemplary and should not merit a maximum shareholder 8

incentive. 9

Table 2: 2020-2021 Planned Savings vs. Proposed Max Shareholder Incentive 10

11

Q: Wasn’t the DTE portfolio lifetime savings metric adopted for 2018 and 2019 in DTE’s 12

last EWR plan case developed using the same assumptions DTE has proposed in this 13

case – i.e., 1.50% first year savings multiplied by an average measure life of 11 years? 14

2020 2021

Statutory First Year Savings Target (% of sales) 1.00% 1.00%Statutory First Year Savings Target (GWh) 468 465 Max Incentive Assumed Average Measure Life 11.00 11.00Tier 1 Incentive (GWh) 5,144 5,117 Max Incentive First Year Savings % of Sales 1.50% 1.50%Max Incentive Lifetime Savings (GWh) 7,717 7,676

DTE First year Savings (% of sales) 1.63% 1.75%DTE First Year Savings (MWh) 760 814 DTE Avg Measure Life (years) 12.11 12.29DTE Lifetime Savings (MWh) 9,201 10,004 DTE Max Incentive Lifetime Savings as % of Planned Lifetime Savings

84% 77%

DTE Proposed Max Incentive for Lifetime Savings

DTE Planned Lifetime Savings

25

A: It was. However, as I noted above there is an important contextual difference between that 1

proceeding and this one. Specifically, DTE is planning on achieving greater lifetime savings 2

in in 2020 and 2021 than it planned for 2018 and 2019. 3

Most notably, for 2020 and 2021 DTE is planning to achieve 1.625% and 1.75% first year 4

savings (as percent of sales) rather than the 1.50% first year savings it was planning to 5

achieve in 2018 and 2019. And DTE is seeking approval of a higher budget in order to 6

achieve that higher level of savings. In other words, it has significant additional resources 7

with which to work to achieve a higher savings target. In addition, the average measure life 8

implicit in DTE’s 2018 and 2019 plan – 11.92 years in both cases22 – is a little lower than 9

the 12.11 and 12.29 it is planning to achieve in 2020 and 2021. 10

As a result, as Table 3 shows, for 2018 and 2019 the portion of DTE’s maximum shareholder 11

incentive tied to portfolio lifetime savings could only be earned if the Company achieved 12

92% of its planned lifetime savings. That is a much higher percentage than the 84% and 13

77% implicit in its proposed lifetime savings metric for 2020 and 2021. 14

22 Computed from Attachment to Case No. U-18262Response to NRDCE 3.4, NRDC -3.4 Portfolio Measure Life.xlsx. Note that this value is lower than DTE reported in Case No. U-18262 Exhibit A-4. However, DTE improperly calculated average measure life in that proceeding – using a different (and inaccurate) formula than the correct one it has used in this proceeding.

26

Table 3: 2018-2019 Planned Lifetime Savings vs. Approved Max Shareholder Incentive 1

2

Q: How do you propose that the Company’s portfolio lifetime savings metric be modified? 3

A: I propose that the metric remained tied to the 1.50% first year savings level, solely to 4

maintain symmetry with the statute regarding the savings level at which maximum 5

shareholder incentives are earned. However, I propose that value be multiplied by DTE’s 6

forecast average savings life of 12.11 years for 2020 and 12.29 years for 2021. As Table 4 7

shows, DTE would still be rewarded with a maximum shareholder incentive at lifetime 8

savings levels below what it is planning to achieve. In other words, it would still have a non-9

trivial amount of “headroom” as a cushion against uncertainty in its planned performance. 10

The 2020 max incentive as a percent of planned savings – 93% – would be very similar to 11

the 92% values approved for 2018 and 2019 rather than the 84% proposed by DTE; the 2021 12

max incentive as a percent of planned savings – 86% – would be lower than the ratios 13

approved for 2018 and 2019, but at least much closer than the 77% ratio implicit in DTE’s 14

proposal. 15

2018 2019

Statutory First Year Savings Target (% of sales) 1.00% 1.00%Statutory First Year Savings Target (MWh) 471 468 Max Incentive Assumed Average Measure Life 11.00 11.00Tier 1 Incentive (MWh) 5,181 5,153 Max Incentive First Year Savings % of Sales 1.50% 1.50%Max Incentive Lifetime Savings (MWh) 7,772 7,729

DTE First year Savings (% of sales) 1.50% 1.50%DTE First Year Savings (MWh) 707 703 DTE Avg Measure Life (years) 11.92 11.92DTE Lifetime Savings (MWh) 8,422 8,376 DTE Max Incentive Lifetime Savings as % of Planned Lifetime Savings

92% 92%

DTE Proposed Max Incentive for Lifetime Savings

DTE Planned Lifetime Savings

27

Table 4: 2020-2021 DTE Planned Savings vs. NRDC Proposed Max Shareholder Incentive 1

2

C. An Alternative to DTE’s Proposed Low Income Spending Metric3

Q: Please summarize the nature of your concern about DTE’s proposal to base its low 4

income performance metric on the amount of money it spends on low income 5

programs? 6

A: Performance metrics based on spending are not ideal because they do not measure outcomes 7

that matter, such as total lifetime savings, comprehensiveness of treatment of savings 8

opportunities, bill savings, etc. At best, they are uncertain proxies for those outcomes. At 9

worst, they can create perverse incentives to spend money in sub-optimal ways. Thus, in the 10

context of shareholder incentive mechanisms, spending benchmarks are better suited as 11

“minimum requirements” for earning incentives rather than as the measure of performance 12

upon which the amount of incentive earned is based. 13

2020 2021

Statutory First Year Savings Target (% of sales) 1.00% 1.00%Statutory First Year Savings Target (MWh) 471 468 Max Incentive Assumed Average Measure Life 12.11 12.29Tier 1 Incentive (MWh) 5,704 5,757 Max Incentive First Year Savings % of Sales 1.50% 1.50%Max Incentive Lifetime Savings (MWh) 8,556 8,636

DTE First year Savings (% of sales) 1.63% 1.75%DTE First Year Savings (MWh) 760 814 DTE Avg Measure Life (years) 12.11 12.29DTE Lifetime Savings (MWh) 9,201 10,004 NRDC Max Incentive Lifetime Savings as % of DTE Planned Lifetime Savings

93% 86%

NRDC Proposed Max Incentive for Lifetime Savings

DTE Planned Lifetime Savings

28

Q: Wasn’t DTE’s 2018 and 2019 shareholder incentive mechanism based, in part, on low 1

income spending? 2

A: For 2018 and 2019 DTE had two low income performance metrics: one based on low income 3

spending, to which 15% weight was assigned, and one which was an indicator of progress in 4

more comprehensively treating multi-family building efficiency to which 10% weight was 5

assigned. While not ideal, because 60% of the low income performance weight (15% out of 6

a total of 25%) was assigned to low income spending, it was at least not all based on spending 7

as the Company’s current proposal is. It is also worth noting that though Consumers 8

Energy’s approved 2018-2021 plan also had 25% weight assigned to low income 9

performance metrics, none of that weight was associated with low income spending; it was 10

all assigned to either lifetime low income savings or a measure of comprehensiveness of 11

treatment of multi-family buildings.23 12

Q: What would you propose as preferable alternatives to DTE’s 2020 and 2021 low income 13

performance metrics? 14

A: Ideally, low income performance metrics should be tied entirely to ultimate outcomes of the 15

Company’s programs, like the lifetime savings achieved and/or indicators of comprehensive 16

treatment of buildings and deep savings. However, DTE has little historical experience or 17

data regarding what it could achieve with a much more concerted effort to comprehensively 18

address low income electric savings opportunities, particularly in electrically-heated low 19

income homes in general and in low income multi-family buildings in particular. In that 20

context, it may be reasonable – for just the next two years covered by its filed plan – to 21

23 Case No. U-18261, January 23, 2018, Order Approving Settlement Agreement, Attachment C.

29

include both a spending metric and a metric that is an indicator of progress in more 1

comprehensively and deeply addressing electric savings opportunities. Thus, I propose the 2

following two metrics: 3

• Number of heat pumps retrofitted into electric-resistance heated low income4

homes. This metric should have 15% of the performance incentive mechanism weight.5

I would propose that the maximum incentive for 2020 be set at 500 units installed, with6

the lower end of the Tier 1 incentive set at 333 installations. For 2021, the maximum7

incentive should be earned at 1000 installations, with the lower end of Tier 1 set at 6678

units. These values are consistent with the program recommendations (and budget9

increases) I provided in the previous section of my testimony. Furthermore, to both10

ensure that the Company gains experience with this technology in both single family11

and multi-family buildings, at least one-third of the heat pumps installed should be in12

multi-family buildings. That should be a minimum requirement for any shareholder13

incentive.14

• Total low income spending. This metric should be assigned only 10% of the weight15

for the shareholder incentive mechanism. The maximum shareholder incentive16

achievable for this metric should be earned for spending at levels equal to the17

Company’s proposed total low income program budget (i.e., $14.7 million in 2020 and18

$15.5 million in 2021), plus the increase in spending I have proposed to cover the cost19

of heat pump installations (i.e., $2.5 million more for 2020 and $5.0 million more for20

2021), plus any additional increases necessary to achieve the low income multi-family21

spending levels put forward by NHT witness Annika Brink. The lower end of the Tier22

1 incentive level for this metric should be earned at spending levels equal to two-thirds23

30

of maximum incentive level. Given the Company’s historically limited focus on 1

comprehensive treatment of multi-family buildings, the ratio of actual spending on 2

DTE’s low income multi-family program to actual spending on all low income 3

programs should be at least equal to the ratio of the approved budget for the low income 4

multi-family program to the approved budget for all low income programs.24 That 5

should be a minimum requirement for earning any incentive for this metric.25 6

Q: Why is your proposed structure for low income performance metrics better than DTE’s 7

proposed structure? 8

A: I place less emphasis on spending and most of the emphasis on a measure – numbers of heat 9

pump installations – that is both a more direct indicator of benefits for low income customers 10

in 2020 and 2021, as well as an indicator of critically important “foundation-building” for 11

the future. By “foundation building” I mean that a performance metric tied to significant 12

numbers of heat pump installations will strongly encourage the Company to develop 13

relationships with cold climate heat pump contractors that should enable more effective 14

program delivery in the future, as well as to test and fine-tune approaches to retrofitting heat 15

pumps in significant volumes in different types of buildings. It may also help create 16

economies of scale necessary to bring down the cost of a technology that is probably not sold 17

in very large quantities today in DTE’s service territory. 18

24 For the purpose of calculating the budget ratio, I would propose that half of my proposed low income budget increase to pay for heat pump retrofits be allocated to the low income multi-family program. 25 An exception to this rule would be if actual low income multi-family spending is greater than budgeted low income multi-family program spending (i.e., the ratio of multi-family to total low income spending can be lower than the ratio of approved budgets, if the total multi-family approved budget has been spent).

31

After the 2021 (i.e., in the Company’s next plan), when we have much more data available 1

regarding the opportunities to more comprehensively treat low income customers with 2

electric heat as well as multi-family buildings, it will likely be best to eliminate spending 3

metrics and focus entirely on outcome metrics. Additional outcome metrics that may merit 4

consideration at that time include total lifetime MWh savings, average savings as a percent 5

of annual consumption of homes treated, and possibly other metrics of depth of savings (e.g., 6

number of major measures installed – including, but not limited to heat pumps). 7

To that end, I would also strongly suggest that DTE be required to direct its evaluators to 8

conduct process and impact evaluations of both their single family and multi-family low 9

income programs. Such evaluations should include efforts to 10

• better characterize the low income housing markets the programs are targeting;11

• understand ways the programs could be more effective in recruiting electrically-heated12

low income customers (leveraging experience from other jurisdictions);13

• quantify the fraction of multi-family building owners who follow through on major14

measure recommendations;15

• document the reasons why building owners do not follow through;16

• document and understand the time lags between when assessments are completed and17

when major measures get installed;18

• document the reduction in energy burden associated with participating in the programs,19

both for electrically-heated and non-electrically heated participants;20

32

• assess non-energy benefits both low income customers and multi-family building1

owners, and the extent to which they could be better leveraged when promoting the2

programs to low income customers and building owners; and3

• better understand how the programs’ future design and/or delivery could be improved.

V. DTE SHOULD USE MARGINAL LINE LOSSES WHEN ASSESSING EFFICIENCY4 COST-EFFECTIVENESS 5

Q: What are T&D loss rates? 6

A: When electricity is generated, it must be sent through the utility’s transmission and/or 7

distribution (T&D) system infrastructure to residential and business customers. Some of the 8

electricity is “lost” in the process. Thus, the amount of electricity that needs to be generated 9

is greater than the amount of electricity that is ultimately consumed by residential and 10

business customers. The amount by which it is greater is the T&D loss rate. 11

Q: Why are loss rate assumptions important in the context of analyses of efficiency 12

program savings? 13

A: DTE and other utilities typically measure efficiency program savings at their customers’ 14

homes or businesses. Indeed, that is the way their savings goals are articulated. Thus, when 15

assessing the cost-effectiveness of efficiency programs, the utility must make assumptions 16

about loss rates because they need to understand the impacts that saving electricity at their 17

customers’ meters will have on generation requirements. 18

33

Q: What is DTE’s loss rate assumption? 1

A: DTE converts both estimated customer energy savings and estimated customer peak demand 2

savings to generation savings using a 6.8% T&D loss rate assumption.26 3

Q: Is that 6.8% assumption an average loss rate or a marginal loss rate? 4

A: The 6.8% is an average annual loss rate.”27 5

Q: Is that a reasonable assumption for an average loss rate for DTE? 6

A: I have no opinion whether it is a reasonable assumption for an average annual loss rate for 7

DTE, but it is not an appropriate rate for estimating the effects of efficiency programs on 8

generation requirements. To the contrary, if it is a reasonably precise estimate of average 9

annual T&D losses for DTE, then it will significantly understate the reduction in losses 10

caused by efficiency programs. 11

Q: Please explain. 12

A: Line losses grow (largely) exponentially with load.28 That means that the T&D loss 13

associated with adding one more kWh of demand to the system in any given hour of the year 14

26 Exhibit NRD-6, Attachment U-20373 NRDCDE-1.1ai-01 DSMore 2018 Batch Tool - 2020-2021 EWR Plan, “Res Utility Input” and “C&I Utility Input” tabs. Cell A3 in both the “Res Utility Input” and “C&I Utility Input” tabs of NRDCDE-1.1ai-01 DSMore 2018 Batch Tool – 2020-2021 EWR Plan.xlsx shows that the 6.8% is used for annual electric losses. Cell A2 in the same tabs enables users of DSMore to insert a multiplier to generate a higher peak or T&D loss rate. However, the DTE input is 100% (i.e., peak loss rate is assumed to be the same as annual energy loss rate). 27 Exhibit NRD-7, Responses to NRDCDE-1.1aix1, aix3b, and aix4 and Attachment, page 1 (Response to NRDCDE-1.1aix1). 28 Exhibit NRD-8, Lazar, Jim and Xavier Baldwin, Valuing the Contribution of Energy Efficiency to Avoided Marginal Line Losses and Reserve Requirements, Regulatory Assistance Project, August 26, 2011, available at https://www.raponline.org/knowledge-center/valuing-the-contribution-of-energy-efficiency-to-avoided-marginal-line-losses-and-reserve-requirements/?sf_data=results&_sf_s=lazar+line+loss.

34

will be higher than the average T&D loss for all kWh of demand at that hour. Simply put, 1

marginal loss rates are higher than average loss rates. 2

Q: How is that relevant to analyzing the effects of efficiency programs? 3

A: By definition, efficiency programs savings occur “on the margin”. Thus, their impacts on 4

T&D losses should be valued using marginal loss rates. This is clearly explained in the 5

National Standard Practice Manual for Assessing Cost-Effectiveness of Energy Efficiency 6

Resources (commonly referred to as the NSPM): 7

“When estimating the magnitude of avoided line losses, it is important to 8 recognize that line losses grow exponentially with load. As a result, the 9 marginal loss rate associated with the last increment of load added to – or 10 removed from – the T&D system (i.e. incremental losses divided by 11 incremental load) is greater than the average loss rate for all load (i.e. total 12 losses divided by total load). Thus, the magnitude of line loss reductions 13 associated with efficiency savings should be based on estimates of marginal 14 – not average – line loss rates.”29 15

Q: How should loss rates be used to convert annual customer peak demand savings to 16

generation capacity savings? 17

A: Because loss rates grow largely exponentially with load, loss rates used to convert customer 18

peak demand savings to peak demand savings at generation should be higher than loss rates 19

used to convert annual customer energy savings to annual energy savings at generation. This 20

is clearly explained in the NSPM: 21

“…there should be separate average marginal line loss rates for energy 22 savings and peak demand savings. By definition, marginal line loss rates at 23

29 Woolf, Tim, et al., National Standard Practice Manual for Assessing Cost-Effectiveness of Efficiency Resources, Edition 1, Spring 2017, page 51, available at https://nationalefficiencyscreening.org/wp-content/uploads/2017/05/NSPM_May-2017_final.pdf.

35

the time of system peak will be considerably higher than the weighted average 1 of marginal line loss rates across all hours of the year when energy is saved.”30 2

Q: Does DTE agree marginal loss rates are more accurate reflections of the impacts of 3

efficiency on energy and capacity savings? 4

A: No. However, the Company has provided no explanation for that position in this 5

proceeding.31 6

Q: Is there evidence from DTE’s service territory to support the conclusion that marginal 7

losses are greater than average losses? 8

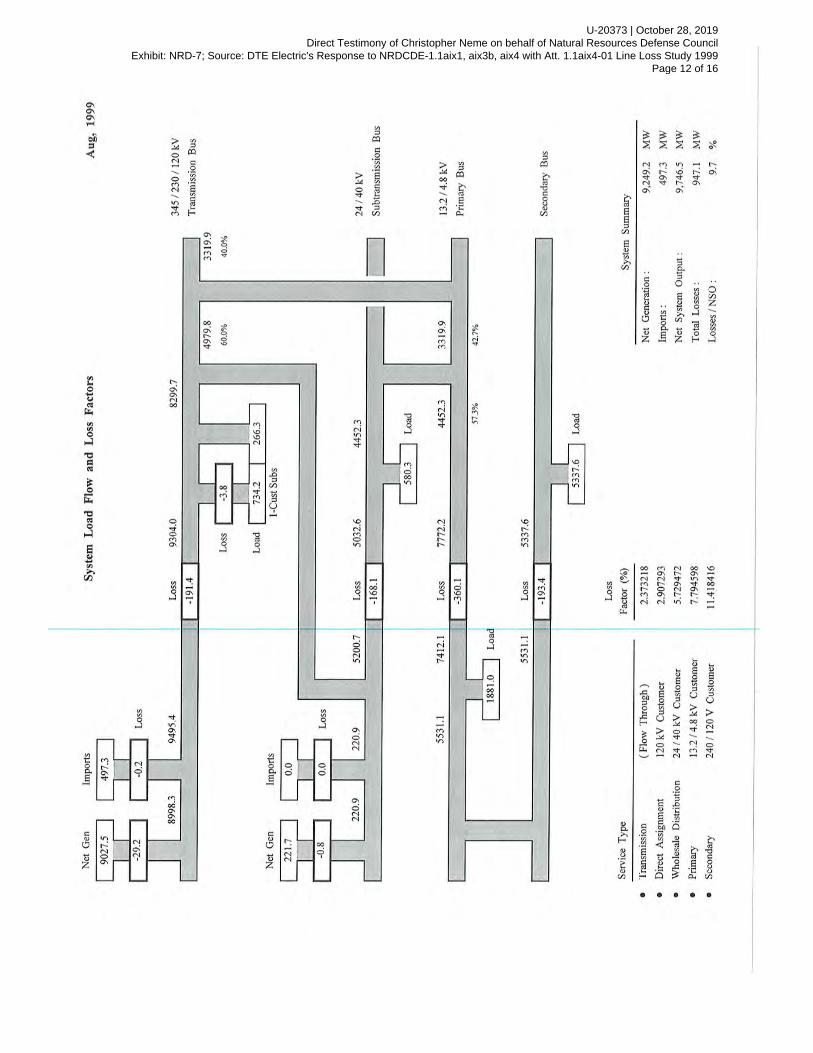

A: Yes. Data from DTE’s 1999 line loss study32 – apparently the most recent such study 9

conducted by the Company – supports the notion that line losses grow as load grows. That 10

is the fundamental principle underlying the concept that marginal loss rates are larger than 11

average loss rates. 12

To be clear, the 1999 DTE study did not estimate marginal line loss rates; nor did it provide 13

loss rates at the time of system peak. What it did provide are average monthly loss rates. As 14

Figure 1shows, the months with lowest average demands had the lowest average line loss 15

rates; the months with highest average demands (all summer months) had the highest average 16

line loss rates. To be clear, I am not suggesting that loss rates from a 1999 study are 17

necessarily reflective of loss rates on DTE’s system today, twenty years later. However, the 18

30 Id. 31 Exhibit NRD-7, page 2 (Response to NRDCDE-1.1aix3b). 32 Exhibit NRD-7, pages 3-16 (Response to NRDCDE-1.1aix4 and attachment U-20373 NRDCDE-1.1aix4-01 Line Loss Study 1999).

36

pattern reflected in the study results – of increasing loss rates as demand grows – is consistent 1

with both engineering expectations and the results of other studies. 2

Figure 1: Average DTE Monthly Demand and Loss Rates in 1999 3

4

Q: What are the implications of DTE’s decision to use an average loss rate rather than a 5

marginal loss rate – both for energy and capacity? 6

A: Using average loss rates will understate the value of avoided energy costs. Similarly, using 7

the same average annual loss rate to estimate peak demand impacts will understate the value 8

of avoided capacity and avoided T&D benefits. 9

Q: By how much will the use of average loss rates understate the benefits of efficiency? 10

A: For energy savings, it is reasonable to assume that average marginal loss rates are 11

approximately 1.5 times average annual loss rates. In other words, if DTE’s average annual 12

37

loss rate is 6.8%, its average marginal loss rate could be reasonably estimated to be on the 1

order of 10.2%. Put another way, DTE has likely understated the avoided energy benefits of 2

its efficiency programs by about 3%. 3

For peak demand savings, it is reasonable to assume that the marginal loss rate at the time of 4

system peak is on the order of 2.0 times the average annual marginal loss rate – or about 5

20.4% for DTE. Put another way, DTE has likely understated the avoided capacity and 6

avoided T&D benefits of its efficiency programs by about 13%. 7

These multipliers are consistent with research published several years ago by the Regulatory 8

Assistance Project33 and an internal study conducted by Commonwealth Edison, the utility 9

serving the Chicago area.34 10

Q: What are the implications of such understatements of the benefits of DTE’s efficiency 11

programs? 12

A: The result is an understatement of the cost-effectiveness of DTE’s programs. That could 13

lead DTE to inappropriately screen out or lower emphasis on some efficiency measures or 14

programs. In addition, to the extent that the Company continues to inappropriately use 15

average line loss rates in studies to assess cost-effective efficiency potential, in IRPs and in 16

other planning processes, it will bias such analyses and plans in favor of lower levels of 17

energy efficiency. 18

33 Exhibit NRD-8, Lazar, Jim and Xavier Baldwin, Valuing the Contribution of Energy Efficiency to Avoided Marginal Line Losses and Reserve Requirements, Regulatory Assistance Project. 34 See Commonwealth Edison, 2018-2021 Energy Efficiency and Demand Response Plan, Exhibit A, filed June 30, 2017, Illinois Commerce Commission Docket 17-0312, available at https://www.icc.illinois.gov/docket/files.aspx?no=17-0312&docId=254601.

38

Q: What could be done to address the resulting underestimate of the benefits and cost-1

effectiveness of DTE’s efficiency programs? 2

A: First, the Commission could instruct DTE to begin using average annual marginal loss rates 3

to assess the value of avoided energy benefits and marginal loss rates during peak hours to 4

assess the value of avoided capacity and avoided T&D benefits. 5

Second, DTE should conduct a new study of line loss rates to inform the marginal line loss 6

assumptions it uses in the future. That study should (1) quantify the difference between 7

average annual marginal loss rates and average annual loss rates; (2) quantify the difference 8

between average peak hour loss rates and average annual loss rates; and (3) quantify the 9

difference between marginal loss rates during peak hours and average loss rates during peak 10

hours. 11

Finally, until such a new line loss study is completed, the Company should use the proxy 12

multipliers I discuss above: (1) assuming average annual marginal loss rates are 150% of 13

average annual loss rates; and (2) assuming marginal peak loss rates are 200% of average 14

annual marginal loss rates (i.e., 300% of average annual loss rates). 15

VI. DTE SHOULD INCREASE FIRST YEAR SAVINGS TO 2.00% OF SALES16

A. Overview17

Q: What is DTE’s rationale for its proposal to ramp up to just 1.75% savings? 18

A: DTE’s proposed ramp up to 1.75% is based on the EWR savings levels that it proposed in its 19

Integrated Resource Plan (IRP) filing in Case No. U-20471.35 20

35 Direct Testimony of Jason Kupser, pages 20-21.

39

Q: Has the Company presented any other evidence in this proceeding to suggest that 1

1.75% is the economically optimal level of EWR savings to pursue? 2

A: No. 3

Q: Has the Commission approved DTE’s IRP or otherwise approved that level of savings? 4

A: No. As of the date on which I am filing this testimony, DTE’s IRP case is being contested 5

and has not reached a conclusion. 6

Q: Is 1.75% EWR savings the economically optimal level of efficiency savings for DTE? 7

A: No. It is clear that 1.75% savings is less than the economically optimal level of energy 8

savings for DTE, particularly in the near term. 9

Q: What is the basis for that conclusion? 10

A: I discuss this issue at length in testimony I filed in the DTE IRP case. Essentially, there are 11

two sets of analyses which demonstrate that savings of at least 2.00% provide greater net 12

economic benefits to DTE customers than savings at 1.75%: 13

1. DTE’s own energy efficiency cost-effectiveness analyses, using the same EWR cost-14

effectiveness tool that it uses to estimate the cost-effectiveness of its program portfolio15

in this proceeding (DSMore), suggest that 2.00% EWR produces greater net economic16

benefits than 1.75% savings; and17

2. When correcting for just one fundamental flaw in DTE’s IRP modeling of energy18

efficiency – its inclusion of all EWR costs through 2040 but exclusion of all post-204019

benefits that flow from those costs (commonly known as an “end effects” problem) –20

40

the Company’s IRP modeling also shows 2.00% EWR to be the most cost-effective 1

savings level. 2

As I explain in my testimony in the IRP case, there are a variety of other conservatisms or 3

biases in DTE’s IRP analyses of energy efficiency.36 They include a failure to use marginal 4

line loss rates instead of average line loss rates (a problem that persists in DTE’s analysis of 5

the cost-effectiveness of efficiency in this EWR plan proceeding), an assumption that 6

evaluation and other portfolio overhead costs would need to increase linearly with other 7

program spending and the Company’s failure to optimize incentive levels and the efficiency 8

measures selected for analysis in its different EWR savings scenarios. Correcting for any of 9

these problems would only enhance the economic advantage of a 2.00% EWR savings level 10

relative to a 1.75% level. 11

B. DSMore Analyses Suggest Economically Optimal Savings is at Least 2.00%12

Q: Please describe the DSMore cost-effectiveness analyses that DTE performed for its IRP. 13

A: DTE analyzed the cost-effectiveness of multiple different levels of energy efficiency savings 14

every year through 2040.37 That included analyses of 1.50%, 1.75%, 2.00%, 2.25% and 15

2.50% savings per year. The Company analyzed the cost-effectiveness of those different 16

levels of energy savings under three different set of EWR cost assumptions: 17

• “tiered costs”, in which the costs of per unit of savings as savings levels increased based18

on an assumption that efficiency measure incentives would be equal to 35% of the cost19

36 Case No. U-20471, Direct Testimony of Christopher Neme, 7 TR 2664-2673. 37 Though there was an assumed ramp up period to achieve savings levels higher than 1.50%.

41

efficiency measures at a 1.50% savings level and 50% of the cost of efficiency 1

measures at a 2.00% savings level (and therefore increase faster than linearly as savings 2

levels increased); 3

• “flat low costs”, in which the costs per unit of savings were the same per kWh, based4

on an assumption that efficiency measure incentives would be equal to 35% of the cost5

of efficiency measures at all savings levels (but therefore increase linearly in absolute6

terms as the level of savings increased); and7

• “flat high costs”, in which the costs per unit of savings were the same per kWh, based8

on an assumption that efficiency measure incentives would be equal to 50% of the cost9

of efficiency measures at all savings levels (but therefore still increase linearly in10

absolute terms as the levels of savings increased).11

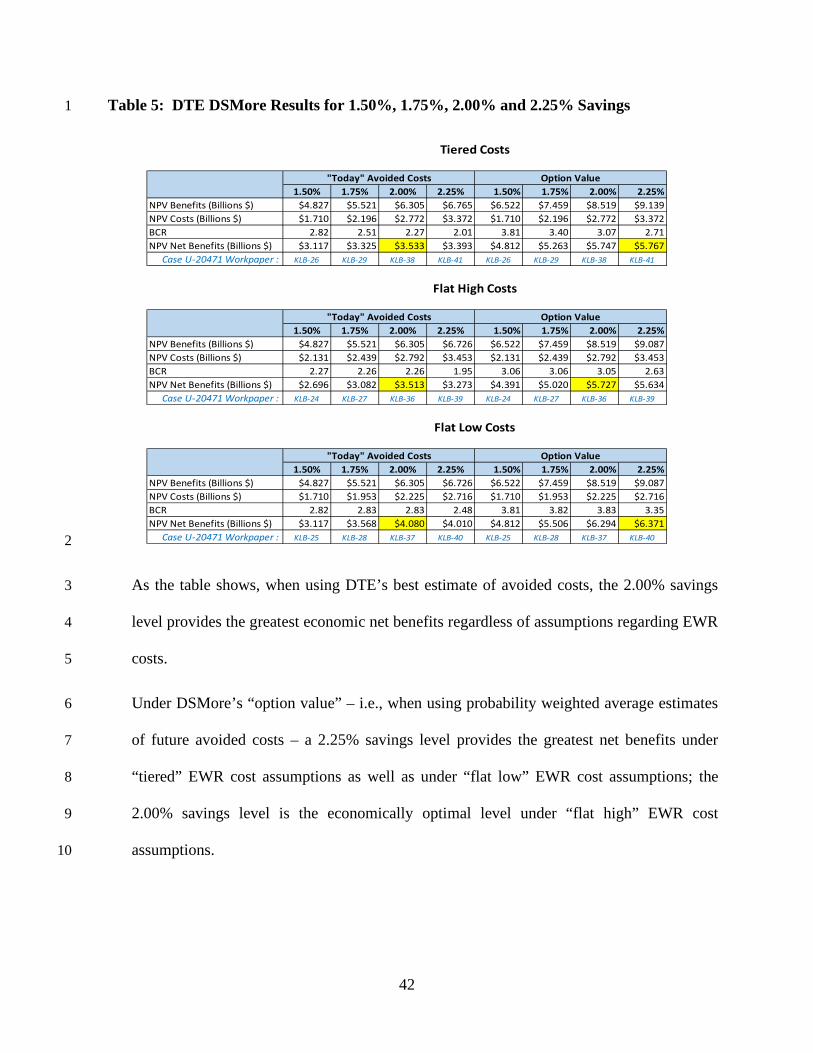

Q: What were the results of these DSMore analyses? 12

A: Table 5 below (and also in Table 9 of my testimony in the DTE IRP case) presents the results 13

of DTE’s DSMore analyses for each level of energy efficiency from 1.50% to 2.25%. The 14

results are presented for each of the three different set of efficiency cost assumptions 15

analyzed by the Company, as well as for two different estimates of avoided costs (what 16

DSMore calls “today” avoided costs, which are avoided costs DTE believes most closely 17

reflect prices in its current forecast, as well as what DSMore calls an “option value” analysis). 18

The “sources” shown in the bottom row of each part of the table are different workpapers 19

developed by DTE Witness Kevin Bilyeu in the IRP case. 20

42

Table 5: DTE DSMore Results for 1.50%, 1.75%, 2.00% and 2.25% Savings 1

2

As the table shows, when using DTE’s best estimate of avoided costs, the 2.00% savings 3

level provides the greatest economic net benefits regardless of assumptions regarding EWR 4

costs. 5

Under DSMore’s “option value” – i.e., when using probability weighted average estimates 6

of future avoided costs – a 2.25% savings level provides the greatest net benefits under 7

“tiered” EWR cost assumptions as well as under “flat low” EWR cost assumptions; the 8

2.00% savings level is the economically optimal level under “flat high” EWR cost 9

assumptions. 10

1.50% 1.75% 2.00% 2.25% 1.50% 1.75% 2.00% 2.25%NPV Benefits (Billions $) $4.827 $5.521 $6.305 $6.765 $6.522 $7.459 $8.519 $9.139NPV Costs (Billions $) $1.710 $2.196 $2.772 $3.372 $1.710 $2.196 $2.772 $3.372BCR 2.82 2.51 2.27 2.01 3.81 3.40 3.07 2.71NPV Net Benefits (Billions $) $3.117 $3.325 $3.533 $3.393 $4.812 $5.263 $5.747 $5.767

Case U-20471 Workpaper : KLB-26 KLB-29 KLB-38 KLB-41 KLB-26 KLB-29 KLB-38 KLB-41

1.50% 1.75% 2.00% 2.25% 1.50% 1.75% 2.00% 2.25%NPV Benefits (Billions $) $4.827 $5.521 $6.305 $6.726 $6.522 $7.459 $8.519 $9.087NPV Costs (Billions $) $2.131 $2.439 $2.792 $3.453 $2.131 $2.439 $2.792 $3.453BCR 2.27 2.26 2.26 1.95 3.06 3.06 3.05 2.63NPV Net Benefits (Billions $) $2.696 $3.082 $3.513 $3.273 $4.391 $5.020 $5.727 $5.634

Case U-20471 Workpaper : KLB-24 KLB-27 KLB-36 KLB-39 KLB-24 KLB-27 KLB-36 KLB-39

1.50% 1.75% 2.00% 2.25% 1.50% 1.75% 2.00% 2.25%NPV Benefits (Billions $) $4.827 $5.521 $6.305 $6.726 $6.522 $7.459 $8.519 $9.087NPV Costs (Billions $) $1.710 $1.953 $2.225 $2.716 $1.710 $1.953 $2.225 $2.716BCR 2.82 2.83 2.83 2.48 3.81 3.82 3.83 3.35NPV Net Benefits (Billions $) $3.117 $3.568 $4.080 $4.010 $4.812 $5.506 $6.294 $6.371

Case U-20471 Workpaper : KLB-25 KLB-28 KLB-37 KLB-40 KLB-25 KLB-28 KLB-37 KLB-40

"Today" Avoided Costs Option Value

Flat High Costs

"Today" Avoided Costs Option Value

Tiered Costs

Flat Low Costs

"Today" Avoided Costs Option Value

43

Q: Why are DSMore’s “option value” scenario results of interest? 1

A: As noted above, the “today” avoided costs are akin to a current “best estimate” of what future 2